tuesday, december 05, 2017 - hmblaw.com · powerpoint presentation this presentation will be posted...

TRANSCRIPT

Tuesday, December 05, 2017

Doug Lindholm & William McArthur, Jr.

Council on State Taxation TE Connectivity

Fred Marcus Principal

Horwood Marcus & Berk Chartered

Willie Geist

Ginny Buckner Kissling Chief Operating Officer and Principal

Ryan, LLC

Savannah Guthrie

Hosted by

&

Chris Matthews & Chuck Todd

with

Special Thank You

Michael Garcia

Producer

Ryan, LLC

Dallas, Texas

Program Overview

Mark Eidman- Texas

Harley Duncan- Federal Tax Reform

Jayne Calhoun– Louisiana

Jason Wyman– Illinois

Edwin Antolin- California

David Shipley- Pennsylvania

Mark Sommer- Kentucky

FEATURING SPECIAL GUESTS:

Mr. John Coalson

Partner

Alston & Bird LLP

Atlanta, GA

Ms. Diann L. Smith

Counsel

McDermott Will & Emery LLP

Washington, DC

FEATURING SPECIAL GUESTS:

Mr. Richard Genetelli

Managing Director

Genetelli Consulting Group

New York, New York

Mr. Jason Zorfas

Executive Director

EY LLP

Boston, Massachusetts

Mr. Mitchell Newmark

Partner

Morrison & Foerster LLP

New York, New York

PowerPoint Presentation

This presentation will be posted to :

bit.ly/HMBNYU2017

Texas Developments

Mr. Mark Eidman

Managing Partner

Ryan Law Firm, LLP

Austin , TX

512.459.6606

Texas Franchise Tax Updates

American Multi-Cinema v. Hegar, No. 03-14-00397-CV (Tex. App.—Austin January 6, 2017)

• The Texas COGS deduction includes all direct costs of acquiring or producing the goods

• On audit, the Comptroller allowed AMC to deduct COGS related to concessions, but not for its costs of acquiring and exhibiting films

• The trial court ruled that AMC could include film exhibition costs in the COGS deduction, but took a limited view of the qualifying expenses

Texas Franchise Tax Updates –

Cont.

American Multi-Cinema v. Hegar, No. 03-14-00397-CV (Tex. App.—Austin January 6, 2017) –Cont.

• The Court of Appeals upheld the trial court’s ruling, and allowed additional film exhibition costs requested by AMC

• Original Court of Appeals decision focused on the first part of the definition of tangible personal property

• “personal property that can be seen, weighed, measured, felt, or touched or that is perceptible to the senses in any other manner” Tax Code § 171.1012(a)(3)(A)(i)

• Comptroller requested rehearing, claiming the decision would be too broadly applied and would result in fiscal disaster for Texas

Texas Franchise Tax Updates –

Cont.

American Multi-Cinema v. Hegar, No. 03-14-00397-CV (Tex. App.—Austin January 6, 2017) –Cont.

• Revised Court of Appeals decision still granted refunds to AMC, but was based on the narrower definition of tangible personal property

• “films, sound recordings, videotapes, live and prerecorded television and radio programs, books, and other similar property embodying words, ideas, concepts, images, or sound, without regard to the means or methods of distribution or the medium in which the property is embodied…” Tax Code § 171.1012(a)(3)(A)(ii)

Texas Franchise Tax Updates –

Cont.

American Multi-Cinema v. Hegar, No. 03-14-00397-CV (Tex. App.—Austin January 6, 2017) –Cont.

• Petition for Review pending at the Texas Supreme Court

• Legislature has amended the Tax Code to allow movie theaters to include in COGS qualifying costs “in relation to the acquisition, production, exhibition, or use of a film or motion picture, including expenses for the right to use the film or motion picture.”

Texas Franchise Tax Updates –

Cont. Hegar v. Gulf Copper & Manufacturing Corporation, No. 03-16-00250-CV (Tex. App.—Austin August 11, 2017)

• Taxpayer was a corporation engaged in surveying, manufacturing, upgrading, and repairing offshore oil rigs.

• Taxpayer presented two issues:

• Issue 1: A revenue exclusion from the tax base of the franchise tax for flow through payments to subcontractors.

• Issue 2: COGS deduction for labor costs.

Texas Franchise Tax Updates –

Cont. Hegar v. Gulf Copper & Manufacturing Corporation, No. 03-16-00250-CV (Tex. App.—Austin August 11, 2017) –Cont.

• Issue 1: Gulf Copper excluded “flow-through” payments to subcontractors for work they preformed on behalf of Gulf Copper for approximately $70 million of work. This reduced its taxable margin to only $23 million.

Texas Franchise Tax Updates –

Cont. Hegar v. Gulf Copper & Manufacturing Corporation, No. 03-16-00250-CV (Tex. App.—Austin August 11, 2017) –Cont.

• In claiming the exclusion, Gulf Copper relied on former section 171.1011(g)(3):

• A taxable entity shall exclude for its total revenue, to the extent [reported to the federal IRS as income], only the following flow-through funds that are mandated by contract to be distributed to other entities:

• Subcontracting payments handled by the taxable entity to provide services, labor, or materials in connection with the actual or proposed design, construction, remodeling, or repair of improvements on real property….

Texas Franchise Tax Updates –

Cont. Hegar v. Gulf Copper & Manufacturing Corporation, No. 03-16-00250-CV (Tex. App.—Austin August 11, 2017) –Cont.

• Flow-through funds for qualifying subcontractor payments were allowed as a deduction from revenue because oil rigs were extensions of real property.

• The work performed by the subcontractors plainly meet the requirements of section 171.1011(g)(3).

• Form of subcontract does not dictate qualification for deduction from revenue

• Court rejected Comptroller’s attempt to limit the applicability of Titan Transportation v. Combs

Texas Franchise Tax Updates –

Cont. Hegar v. Gulf Copper & Manufacturing Corporation, No. 03-16-00250-CV (Tex. App.—Austin August 11, 2017) –Cont.

• Issue 2: Gulf Copper also claimed COGS deduction for furnishing labor costs for the improvement of real property under section 171.1012(h).

• But, COGS deduction granted by trial court was rejected by appellate court because Gulf Copper used an improper method for calculating COGS.

• Qualifying deductions must be based on a cost-by-cost analysis.

• The case was remanded to the trial court for proper determination of COGS.

Texas Franchise Tax Updates –

Cont. Hegar v. Sunstate Equipment Co., LLC, No. 03-15-00427-CV (Tex. App. — Austin January 20, 2017)

• Sunstate was a construction company that included in its COGS the delivery and pick-up costs of construction equipment to construction sites under subsection 171.1012(k-1).

• But, the appellate court disagreed holding that subsection 171.1012(k-1) was passed by the Legislature to allow the deduction of costs to acquire and use equipment, not for its delivery.

• Delivery and pick-up costs were not costs of “acquiring” or “producing” the property that was subsequently rented out, as required by the statute.

Texas Franchise Tax Updates –

Cont. Hegar v. Autohaus LP, LLP, No. 03-15-00427-CV (Tex. App.— Austin February 24, 2017)

• Autohaus was a body shop that took a COGS deduction for the installation of body parts on cars.

• Appellate court held that the installation of the parts was not a cost in “acquiring” or “producing” the goods Autohaus sold.

• While the statute allows installation costs to be a COGS deduction, the installation costs had to be related to producing a good. Autohaus simply purchased auto parts and installed them. Court held that no production had occurred, as required by the statute.

Texas Franchise Tax Updates –

Cont. Owens Corning v. Hegar, 04-16-00211-CV, 2017 WL 1244444 (Tex. App.—San Antonio Apr. 5, 2017, pet. filed)

• Owens Corning made a $2.1 billion payment into an asbestos trust fund as part of a products liability settlement, and took the payment as a COGS.

• Owens Corning argued that the $2.1 billion payment constituted a cost of quality control and was thus a deductible COGS under subsection 171.1012(d)(9).

Texas Franchise Tax Updates –

Cont. Owens Corning v. Hegar, 04-16-00211-CV, 2017 WL 1244444 (Tex. App.—San Antonio Apr. 5, 2017, pet. filed) –Cont.

• Appellate court found that because Owens Corning was asking for a COGS deduction the statute was construed narrowly against the taxpayer.

• Appellate court held that the payment was not for improving the quality of the goods sold and thus did not fall with the scope of 171.1012(d)(9).

Texas Franchise Tax Updates –

Cont. Rule changes for COGS deduction (Rule 3.588)

• Adds presumption of ownership of goods based on legal title (subject to rebuttal).

• Provides COGS guidance for entities furnishing labor and materials to projects for real property construction, improvement, remodeling, repair, or industrial maintenance.

• Qualifying labor and materials must be used in the “direct prosecution” of the project

• Definitions based on Texas Property Code

Texas Franchise Tax Updates –

Cont. Rule changes for COGS deduction (Rule 3.588) –Cont.

• Specific industry provisions

• Movie theaters

• Pipeline companies

Texas Franchise Tax Updates –

Cont. Policy change for temporary credits

• Temporary credits of an entity that leaves the combined group may be used by the combined group if the departing entity left the group during the accounting period on which the report is based.

• Any temporary credit of the departing entity that cannot be used may not be carried forward and used in subsequent report years.

• Amended reports may be filed for reports that are within the statute of limitations.

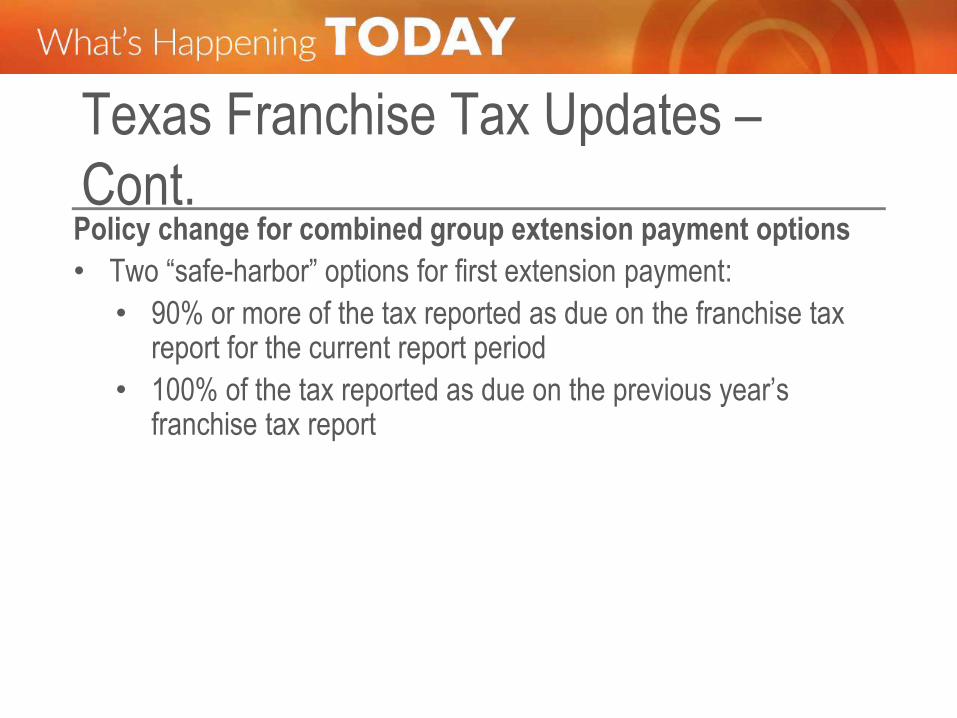

Texas Franchise Tax Updates –

Cont. Policy change for combined group extension payment options

• Two “safe-harbor” options for first extension payment:

• 90% or more of the tax reported as due on the franchise tax report for the current report period

• 100% of the tax reported as due on the previous year’s franchise tax report

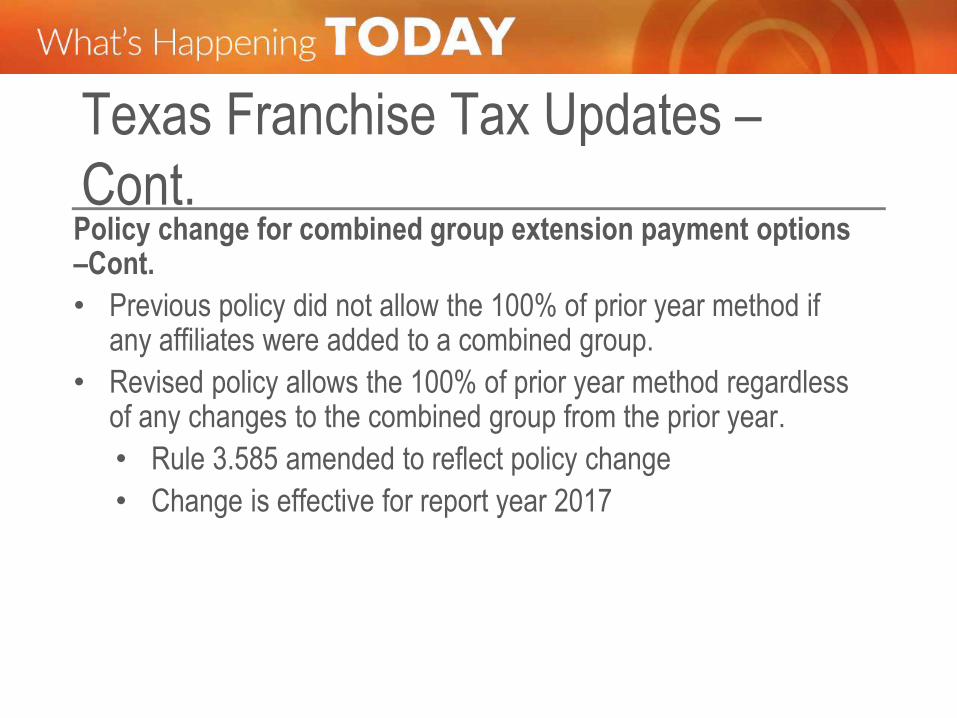

Texas Franchise Tax Updates –

Cont. Policy change for combined group extension payment options –Cont.

• Previous policy did not allow the 100% of prior year method if any affiliates were added to a combined group.

• Revised policy allows the 100% of prior year method regardless of any changes to the combined group from the prior year.

• Rule 3.585 amended to reflect policy change

• Change is effective for report year 2017

Texas Franchise Tax Updates –

Cont. Deadlines extended for administrative filings

• Amendments to Tax Code §111.009:

• A request for refund hearing must be filed within 60 days of the issuance of a letter denying a refund claim.

• A Petition for Redermination must be filed within 60 days of the issuance of a notification of audit results.

• Prior law required filings within 30 days

• Changes were effective September 1, 2017

State Implications of

Federal Tax Reform

Mr. Harley Duncan Managing Director

Washington National Tax

KPMG LLP

Marquee Items For States

• 20% corporate rate – no direct effect

• Reduced pass-through rate

• Deduction approach of Senate is an issue for states

• Expensing – Would not expect substantial changes in conformity

• Limitation on interest expense deduction – coordinate with addback

• NOLs – substantial nonconformity now

• Other deductions – modest broadening

• Contribution to capital rules

Business Tax Reform International Tax Reform • Shift to a territorial system

• Repatriation of deferred earnings as transition to territorial – substantial current exclusion of Subpart F

• Base erosion matters

• Minimum tax – unclear impact

• Interest disallowance – coordination with other limits

• Excise tax – limited

Overall Assessment- Structural

• From a structural standpoint, there may be less here than meets the eye; issues will be complex but (mostly) of modest impact

• Coordinating interest disallowance with addbacks

• Determining amount of repatriation and foreign inclusion and then resolving sourcing issues

• Determining conformity to international base erosion provisions and if changes are necessary/desirable

Overall Assessment- Structural

– Cont.

• Greatest structural impact will be on individual side

• Taxable income states because of proposal to double standard deduction and repeal personal exemption allowance – household size and distribution issues

• Conformity on itemized deduction – no revenue impact from repeal of state and local income tax deduction

Overall Assessment- Fiscal • As proposed, bill would reduce federal revenues by $1.5

trillion over 10 years – as provided for in the budget resolution

• Without dynamic scoring

• Question on whether all base broadening can be made to hold

• To the extent tax cuts are deficit-financed, this imposes fiscal constraints on the federal government and its ability to finance intergovernmental programs

• Stuff rolls down hill

Overall Assessment- Fiscal

– Cont.

• Certain aspects of reform may serve to constrain state tax resources

• Repeal of deduction for state and local income taxes

• Increases the after-tax costs of state and local government at a time when federal resources will be constrained

• Reducing federal rates has similar effect

• Somewhat of an incentive to favor property taxes, but many states have constitutional property tax limits

Timing is Delicate and Important

• Timing could be an issue- as it is not yet clear if federal tax reform will be enacted, when it might be enacted OR when it would be effective if enacted

• Most state legislatures convene and adjourn within a few months during the first part of the year Increases the after-tax costs of state and local government at a time when federal resources will be constrained

• Some states have very short sessions and federal tax reform may be enacted after the state legislature has adjourned

• Depending on the effective date- states may have to convene a special session to address tax reform changes or put off addressing until the following year

Timing is Delicate and Important –

Cont.

• If enacted in 2017 with a 2018 effective date, time for state analysis and changes is short in many cases.

• States may take some precautionary/protective steps in 2018 legislative sessions

What To Expect From States?

• Prospects for state reductions in rates is unclear (at best)

• Any state base broadening likely to be relatively less than at federal level because of lack of conformity and other issues

• State fiscal conditions may not allow for it, and deficit financing not allowed

• Many states experiencing fiscal difficulties at the present time

• Impact of reform is to further restrain resources and increase responsibilities

• Limited pressure for state reductions in pass-through rates unless they also reduce regular corporate rate

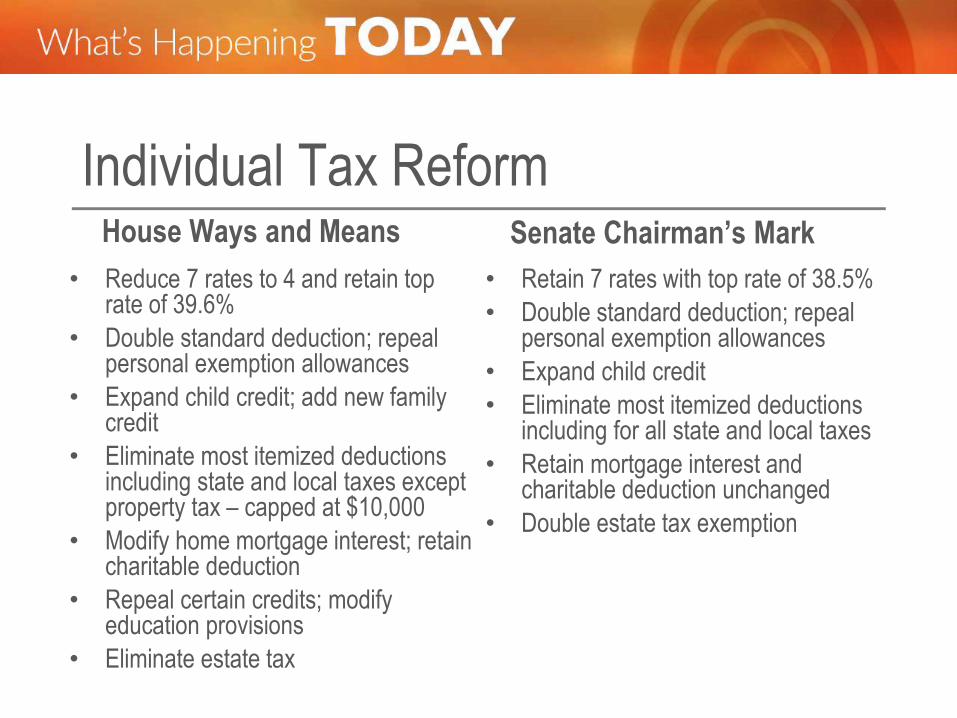

Individual Tax Reform

• Reduce 7 rates to 4 and retain top

rate of 39.6%

• Double standard deduction; repeal personal exemption allowances

• Expand child credit; add new family credit

• Eliminate most itemized deductions including state and local taxes except property tax – capped at $10,000

• Modify home mortgage interest; retain charitable deduction

• Repeal certain credits; modify education provisions

• Eliminate estate tax

House Ways and Means Senate Chairman’s Mark

• Retain 7 rates with top rate of 38.5%

• Double standard deduction; repeal personal exemption allowances

• Expand child credit

• Eliminate most itemized deductions including for all state and local taxes

• Retain mortgage interest and charitable deduction unchanged

• Double estate tax exemption

Louisiana Update

Cooking- LA Style!

Mr. Jaye A. Calhoun

Partner

Kean Miller LLP

New Orleans, LA

Louisiana Update

Cooking- LA Style!

Ms. Jaye A. Calhoun

Partner

Kean Miller LLP

New Orleans, LA

Louisiana Is Flat But… When facing a Fiscal Cliff …

What is the natural response…?

Party Time!! And what do you need for a party?

SOME GREAT FOOD!!!

Louisiana Legislative Changes

(2015 Background) • 2015 Regular Session – New/Increased taxes include:

• Changes to tax credit on business inventory

• Increased tax on utilities

• Changes to R&D credit

• Net operating loss reductions

• Deduction and credit reductions

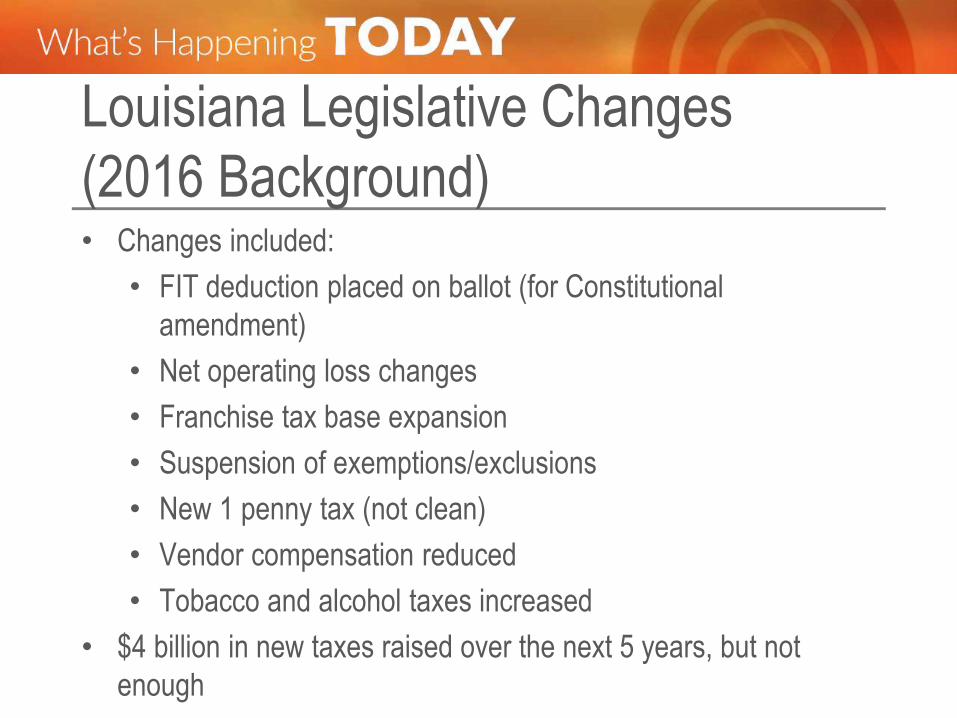

Louisiana Legislative Changes

(2016 Background) • Changes included:

• FIT deduction placed on ballot (for Constitutional

amendment)

• Net operating loss changes

• Franchise tax base expansion

• Suspension of exemptions/exclusions

• New 1 penny tax (not clean)

• Vendor compensation reduced

• Tobacco and alcohol taxes increased

• $4 billion in new taxes raised over the next 5 years, but not

enough

Louisiana Legislative Changes

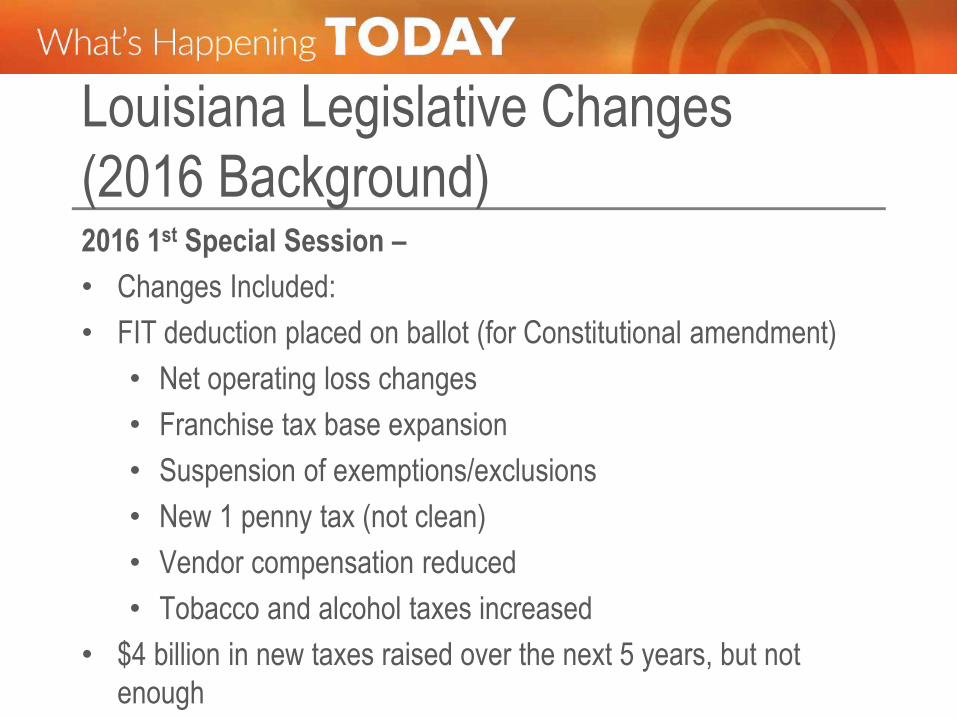

(2016 Background) 2016 1st Special Session –

• Changes Included:

• FIT deduction placed on ballot (for Constitutional amendment)

• Net operating loss changes

• Franchise tax base expansion

• Suspension of exemptions/exclusions

• New 1 penny tax (not clean)

• Vendor compensation reduced

• Tobacco and alcohol taxes increased

• $4 billion in new taxes raised over the next 5 years, but not

enough

Louisiana Legislative Changes

(2016 Background) –Cont. 2016 2nd Special Session –

• Changes, included:

• New HMO license tax

• New limitations on industrial inventory tax credits

• Limitation on interest paid on refunds

• Raised $260 million but still need about $340 million

2016 1st Special Session

Income/Franchise Tax & Incentives Changes included:

• Constitutional Amendment on Ballot – Did not Pass

• Repeal FIT/Flat CIT Rate

• Intercompany Expense Addback

• Transfer Pricing Safe Harbors

• Franchise Tax Expansion

• Credits/Incentives Reductions Extended

2016 Regular Session • Filing Extension Relief

• Payment of Claimes through Offset

• Electronic Filing of Refund Claims

• Use Tax Reporting and Notice

• BTA Jurisdiction

• Property Tax Administration

• Reform and Uniformity Efforts (including LTI)

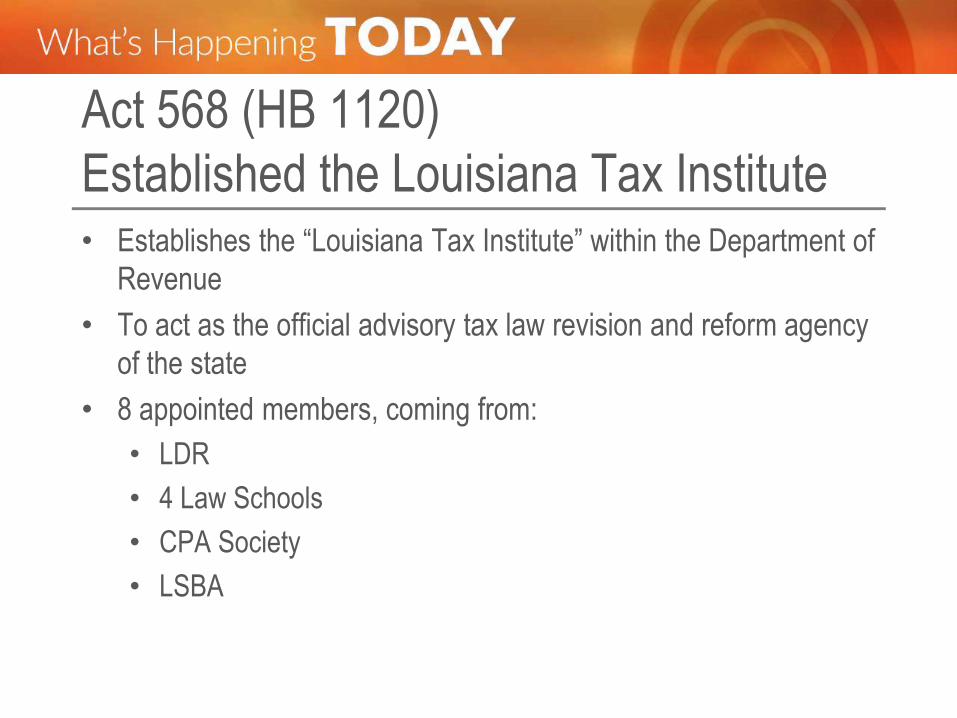

Act 568 (HB 1120)

Established the Louisiana Tax Institute • Establishes the “Louisiana Tax Institute” within the Department of

Revenue

• To act as the official advisory tax law revision and reform agency

of the state

• 8 appointed members, coming from:

• LDR

• 4 Law Schools

• CPA Society

• LSBA

2016 2nd Special Session • NOL Issue Resolved

• Individual Capital Gain Ddn Reduced

• SSF/Market Sourcing

• ITC Changes

• Interest Limitation

• SUT Exemptions/Exclusions Restored

• Further Processing

• HMOs

• Hotel Rules

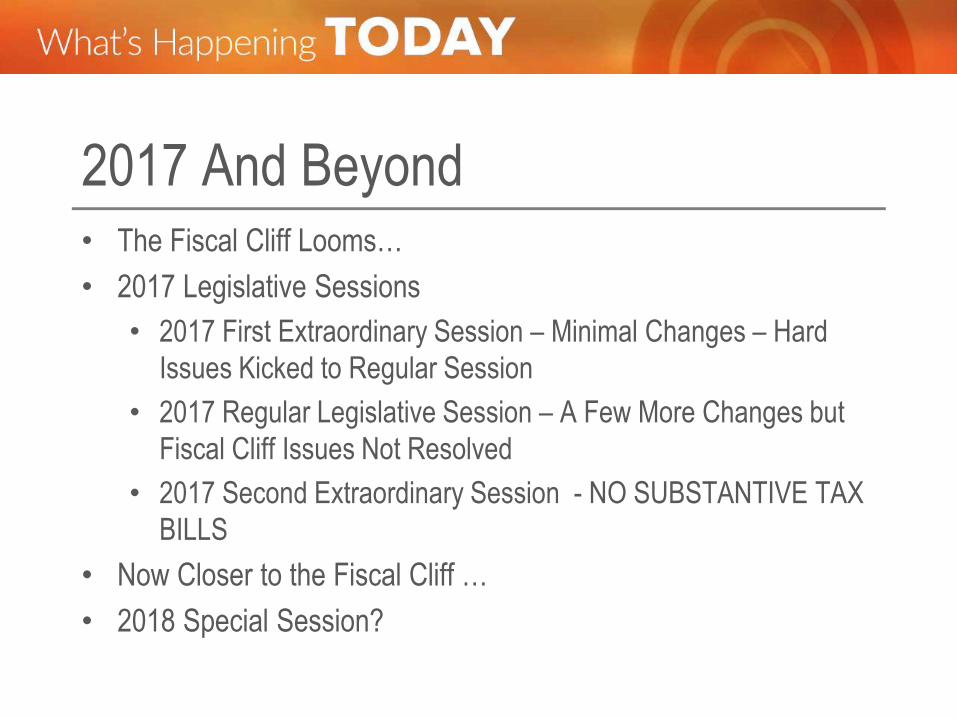

2017 And Beyond • The Fiscal Cliff Looms…

• 2017 Legislative Sessions

• 2017 First Extraordinary Session – Minimal Changes – Hard

Issues Kicked to Regular Session

• 2017 Regular Legislative Session – A Few More Changes but

Fiscal Cliff Issues Not Resolved

• 2017 Second Extraordinary Session - NO SUBSTANTIVE TAX

BILLS

• Now Closer to the Fiscal Cliff …

• 2018 Special Session?

2017 Regular Session

Income/franchise Taxes • What didn’t pass (but was considered):

• Ohio style gross receipts tax

• Michigan style single business tax

• Flat tax

2017 Regular Session

Income/franchise Taxes –Cont. • What did pass:

• Solar credit relief

• Created legacy film tax credits

• Made credit reductions permanent and other modifications

• Enterprise zone and angel investor credits sunsets extended

• R&D credit reduced

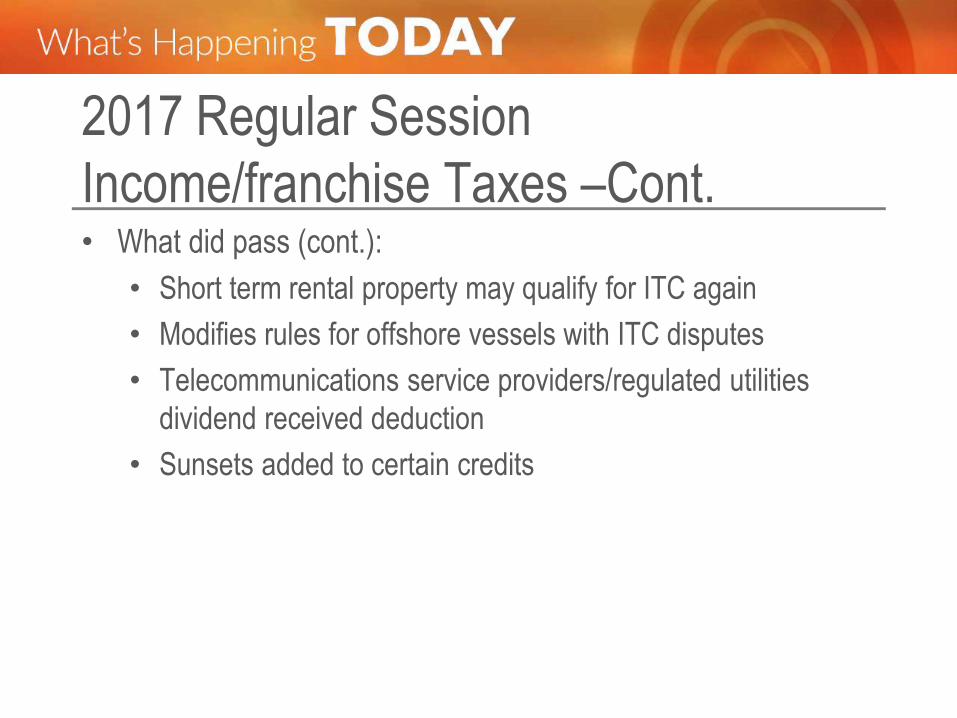

2017 Regular Session

Income/franchise Taxes –Cont. • What did pass (cont.):

• Short term rental property may qualify for ITC again

• Modifies rules for offshore vessels with ITC disputes

• Telecommunications service providers/regulated utilities

dividend received deduction

• Sunsets added to certain credits

2017 Regular Session

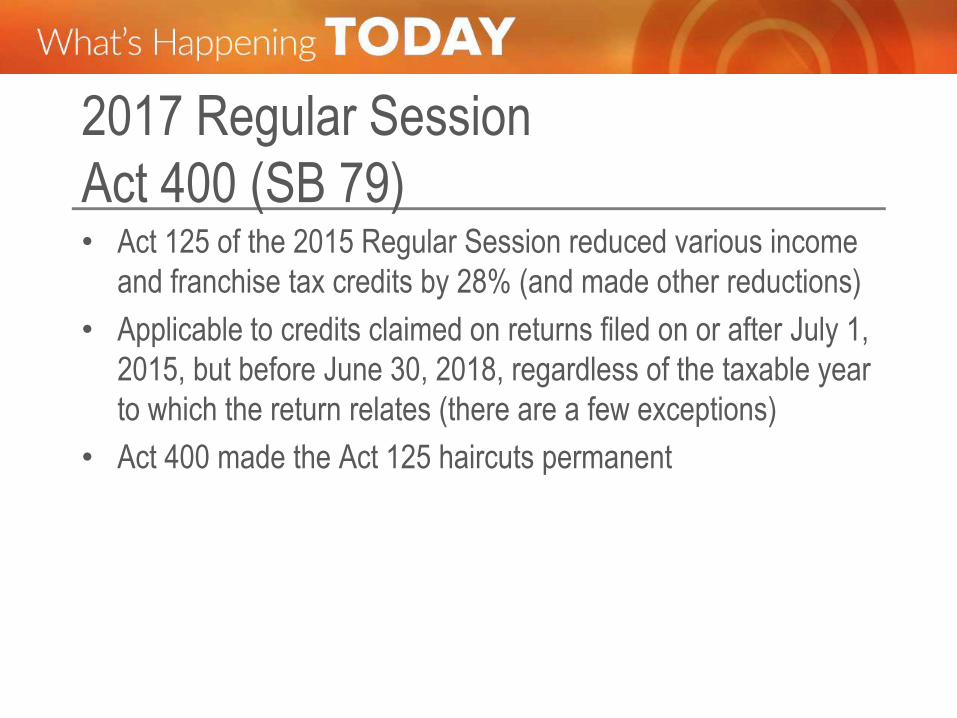

Act 400 (SB 79) • Act 125 of the 2015 Regular Session reduced various income

and franchise tax credits by 28% (and made other reductions)

• Applicable to credits claimed on returns filed on or after July 1,

2015, but before June 30, 2018, regardless of the taxable year

to which the return relates (there are a few exceptions)

• Act 400 made the Act 125 haircuts permanent

2017 Regular Session

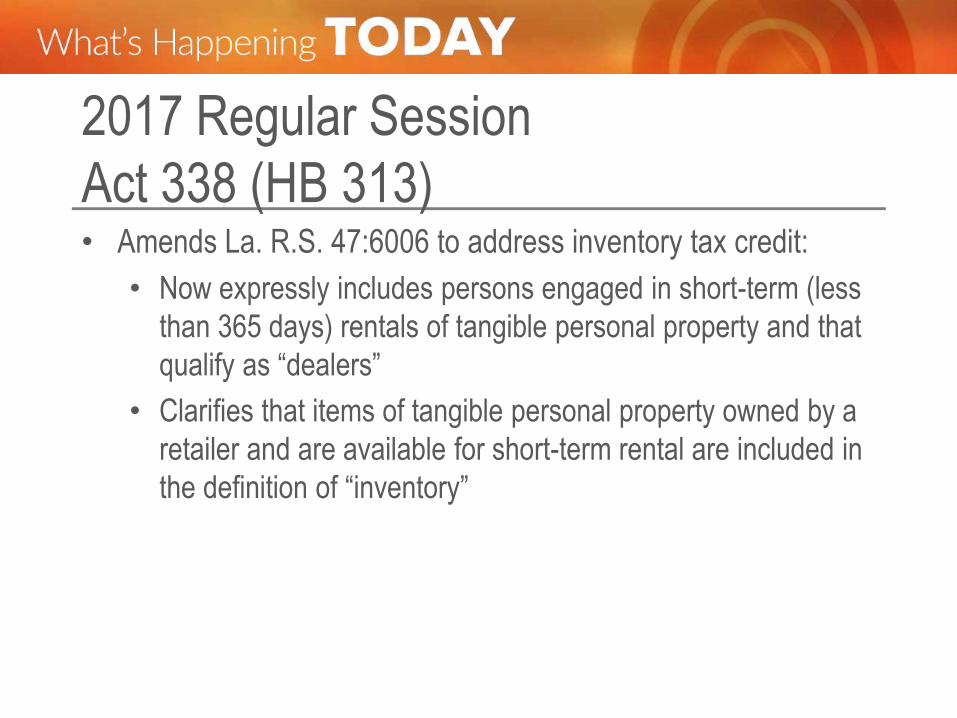

Act 338 (HB 313) • Amends La. R.S. 47:6006 to address inventory tax credit:

• Now expressly includes persons engaged in short-term (less

than 365 days) rentals of tangible personal property and that

qualify as “dealers”

• Clarifies that items of tangible personal property owned by a

retailer and are available for short-term rental are included in

the definition of “inventory”

2017 Regular Session

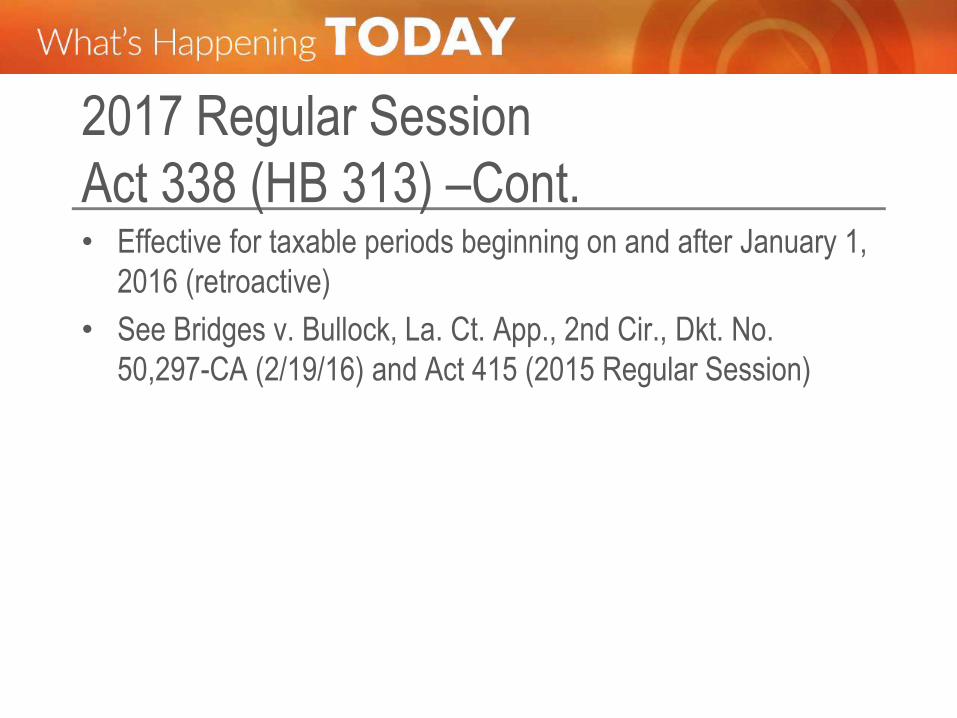

Act 338 (HB 313) –Cont. • Effective for taxable periods beginning on and after January 1,

2016 (retroactive)

• See Bridges v. Bullock, La. Ct. App., 2nd Cir., Dkt. No.

50,297-CA (2/19/16) and Act 415 (2015 Regular Session)

Proposed Regulations

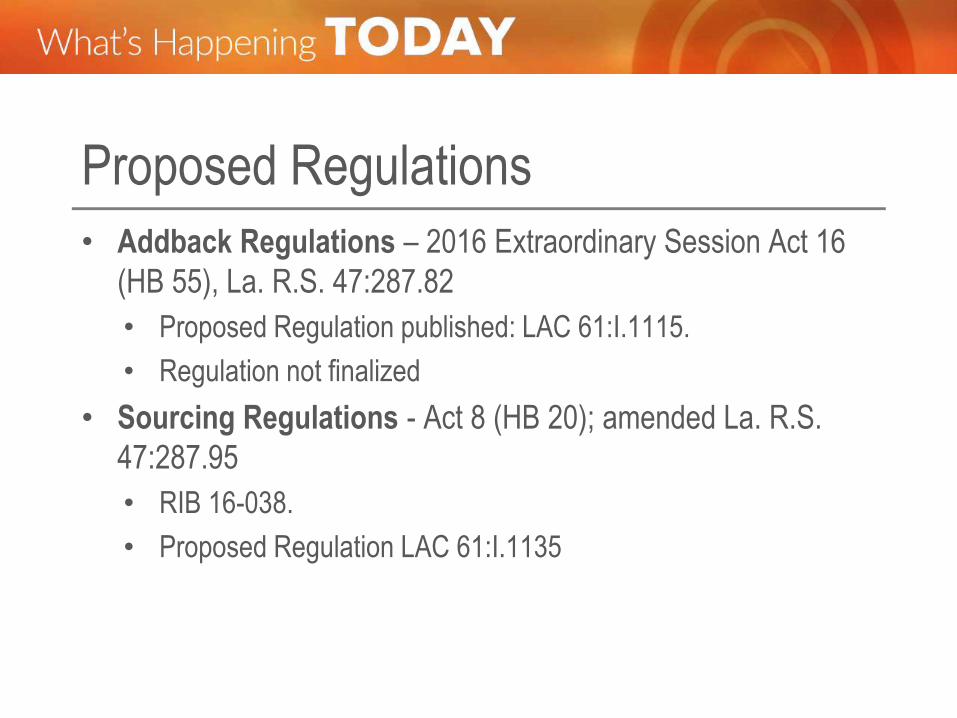

• Addback Regulations – 2016 Extraordinary Session Act 16

(HB 55), La. R.S. 47:287.82

• Proposed Regulation published: LAC 61:I.1115.

• Regulation not finalized

• Sourcing Regulations - Act 8 (HB 20); amended La. R.S.

47:287.95

• RIB 16-038.

• Proposed Regulation LAC 61:I.1135

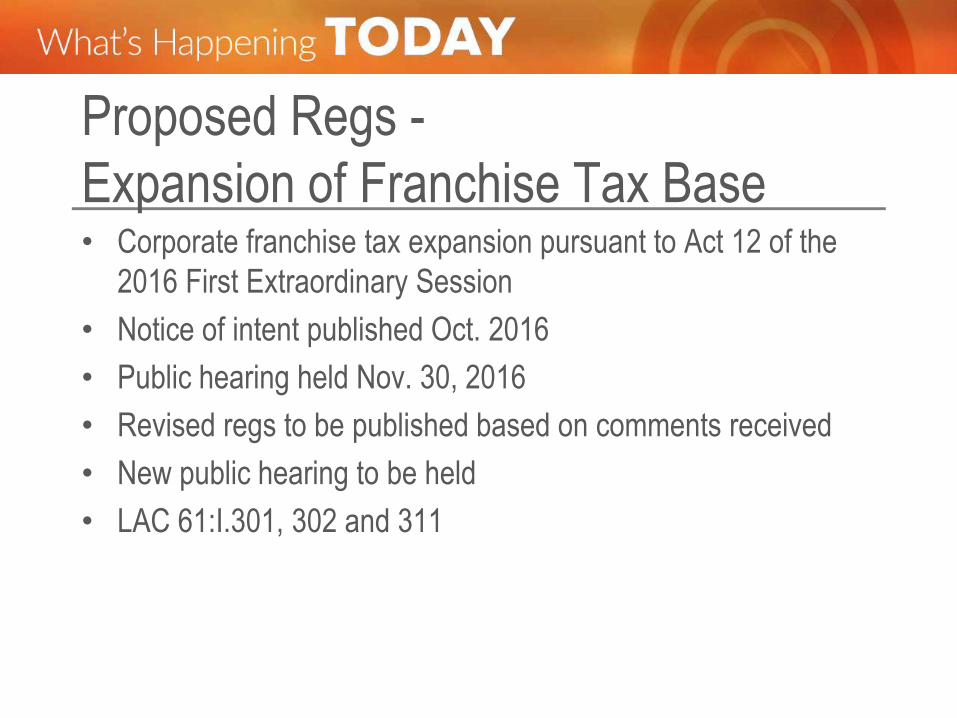

Proposed Regs -

Expansion of Franchise Tax Base • Corporate franchise tax expansion pursuant to Act 12 of the

2016 First Extraordinary Session

• Notice of intent published Oct. 2016

• Public hearing held Nov. 30, 2016

• Revised regs to be published based on comments received

• New public hearing to be held

• LAC 61:I.301, 302 and 311

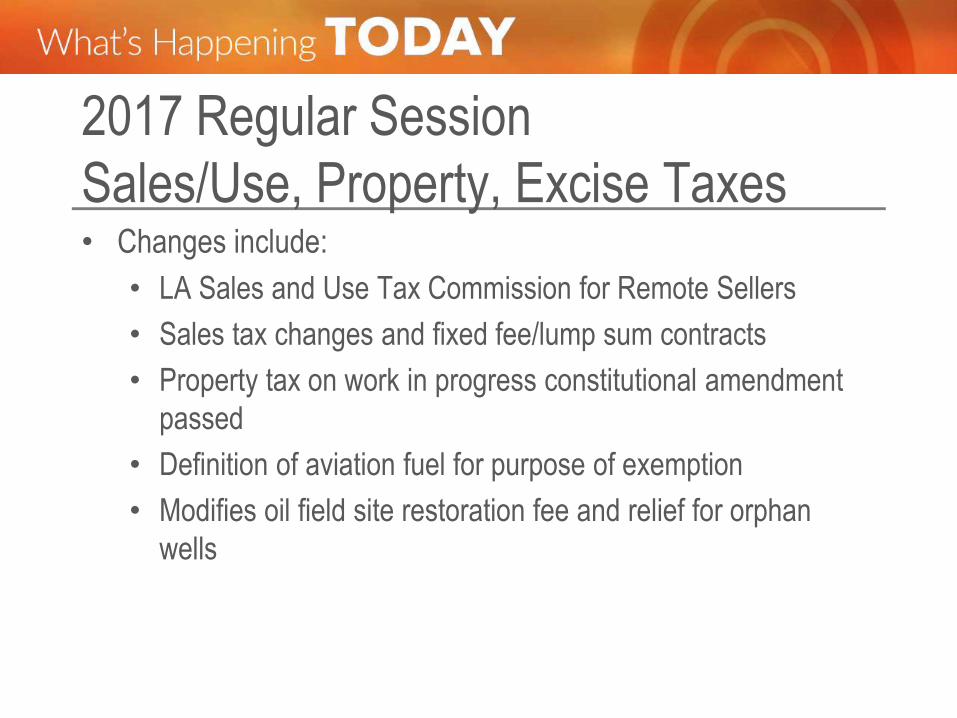

2017 Regular Session

Sales/Use, Property, Excise Taxes • Changes include:

• LA Sales and Use Tax Commission for Remote Sellers

• Sales tax changes and fixed fee/lump sum contracts

• Property tax on work in progress constitutional amendment

passed

• Definition of aviation fuel for purpose of exemption

• Modifies oil field site restoration fee and relief for orphan

wells

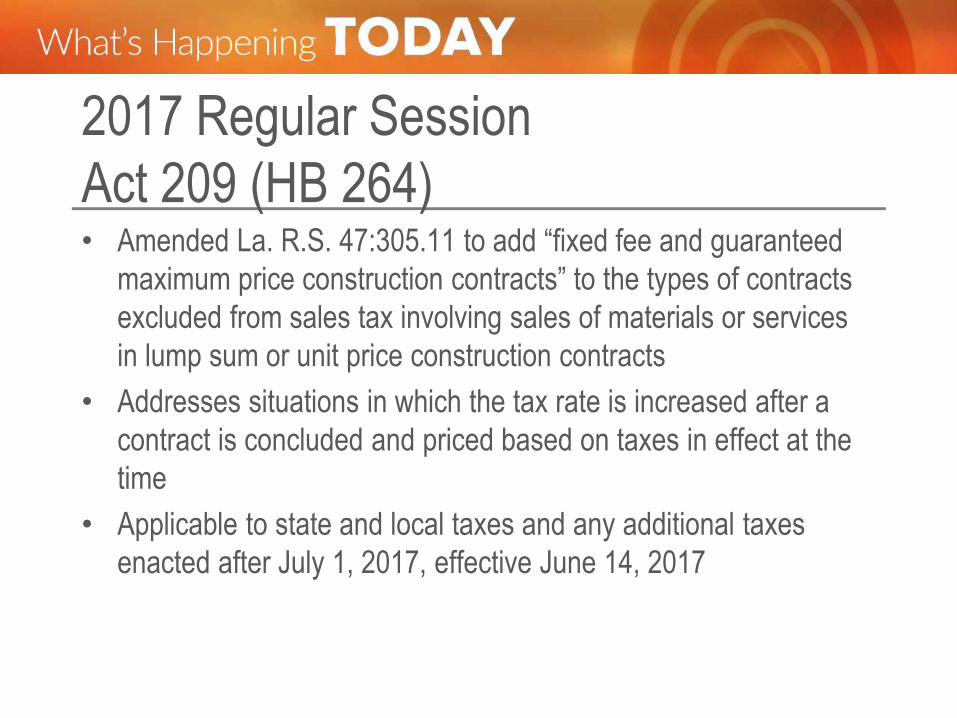

2017 Regular Session

Act 209 (HB 264) • Amended La. R.S. 47:305.11 to add “fixed fee and guaranteed

maximum price construction contracts” to the types of contracts

excluded from sales tax involving sales of materials or services

in lump sum or unit price construction contracts

• Addresses situations in which the tax rate is increased after a

contract is concluded and priced based on taxes in effect at the

time

• Applicable to state and local taxes and any additional taxes

enacted after July 1, 2017, effective June 14, 2017

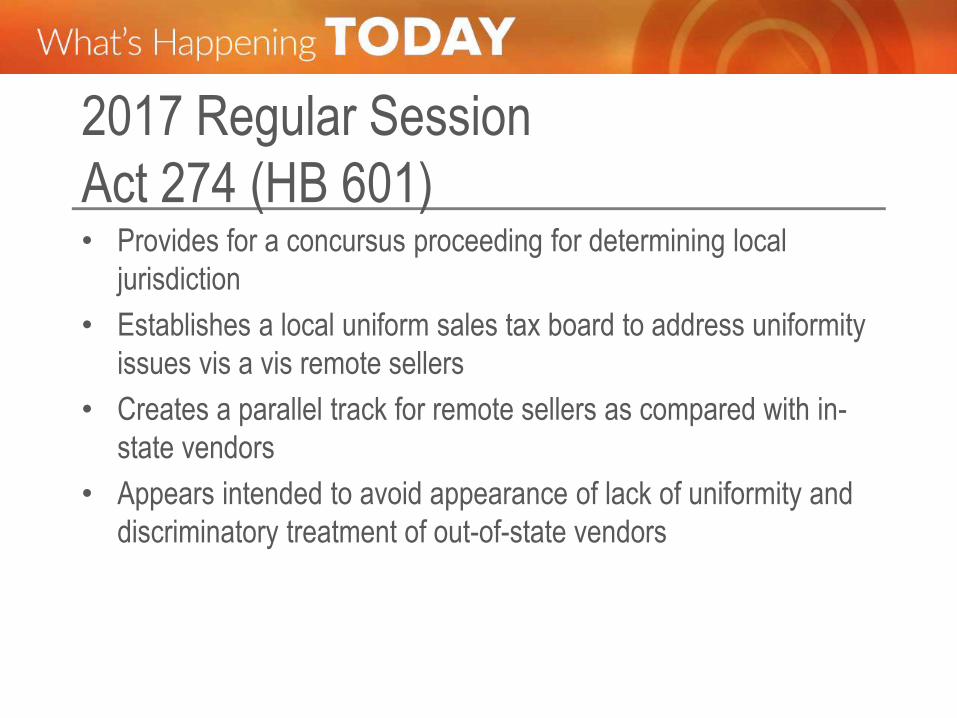

2017 Regular Session

Act 274 (HB 601) • Provides for a concursus proceeding for determining local

jurisdiction

• Establishes a local uniform sales tax board to address uniformity

issues vis a vis remote sellers

• Creates a parallel track for remote sellers as compared with in-

state vendors

• Appears intended to avoid appearance of lack of uniformity and

discriminatory treatment of out-of-state vendors

Judicial Update

Recent Cases

• Quest Diagnostics Clinical Laboratories, Inc. v. Barfield, 2015-

0926 (La. App. 1 Cir. 9/9/16), 2016 WL 4719894, unpublished

• Medtron Software Intelligence Corporation v. Barfield, BTA Doc.

No. 9527D (La. Bd. Tax App. 8/10/16)

• Turner Bros. Crane and Rigging, LLC v. Ascension Parish Sales

and Use Tax Auth., 2016-0673 (La. App. 1 Cir. 7/5/17); __ So.

3d __, 2017 WL 2875914

• Louisiana Chemical Association v. State of Louisiana, et al.,

2016-0501 (La. App. 1 Cir. 4/7/17), ___ So. 3d ___

Judicial Update – Cont.

Recent Cases – Cont.

• Red River Parish Tax Agency, et al. v. SWEPI, LP, 61-51244

(La. App. 2 Cir. 4/5/17), ___ So. 3d ___

• Cajun Indus., LLC and Cajun Constr., Inc. v. Sec’y Dep’t of

Revenue, State of Louisiana, BTA Docket No. 9898D, (La. Bd.

Tax App. 4/12/17).

• Barfield v. Diamond Construction, No. 51,291 (La. App. 2 Cir.

4/5/17), ___ So. 3d ___.

Judicial Update – Cont.

Recent Cases – Cont.

• Arrow Aviation Company, LLC v. St. Martin Parish School Board

Sales Tax Dept., 2016-1132 (La. 12/6/16), ___ So. 3d ___, 2016

WL 7118912.

• Dep’t. of Revenue, State of Louisiana v. Jazz Casino Co., LLC.,

2016-0180, (La. 2/7/17), __ So.3d __, 2017 WL 496266.

• Oldebrecht developments

• NISCO developments

Jaye’s Crystal Ball –

Hot Topics And Hot Sauce

HOT AUDIT INITIATIVES AND HOTTER PREDICTIONS!!

What’s cooking at the LDR?

HOT Audit initiatives!! • TRANSFER PRICING!!! (AND LA RS 47:287.480)

• INTERCOMPANIES!

• ADDBACKS!

• EXEMPTION CERTIFICATE DRILL DOWN!

• LA IS GETTING TO KNOW THE MTC AND…

Hot Predictions!!

• There will be audits!

• There will be higher and more taxes!

• Summer in Louisiana will be HOT!

• BUT…

• We have a festival every weekend

• We invented gumbo and beignets and jambalaya and are

happy to show you how to eat crawfish

• The good news: we are a fun place to visit if you have to work

out your audit issues so Y’ALL COME ON DOWN!

Illinois Legislation and Litigation

Updates

Mr. Jason Wyman

Partner, Deloitte Tax

Chicago, IL

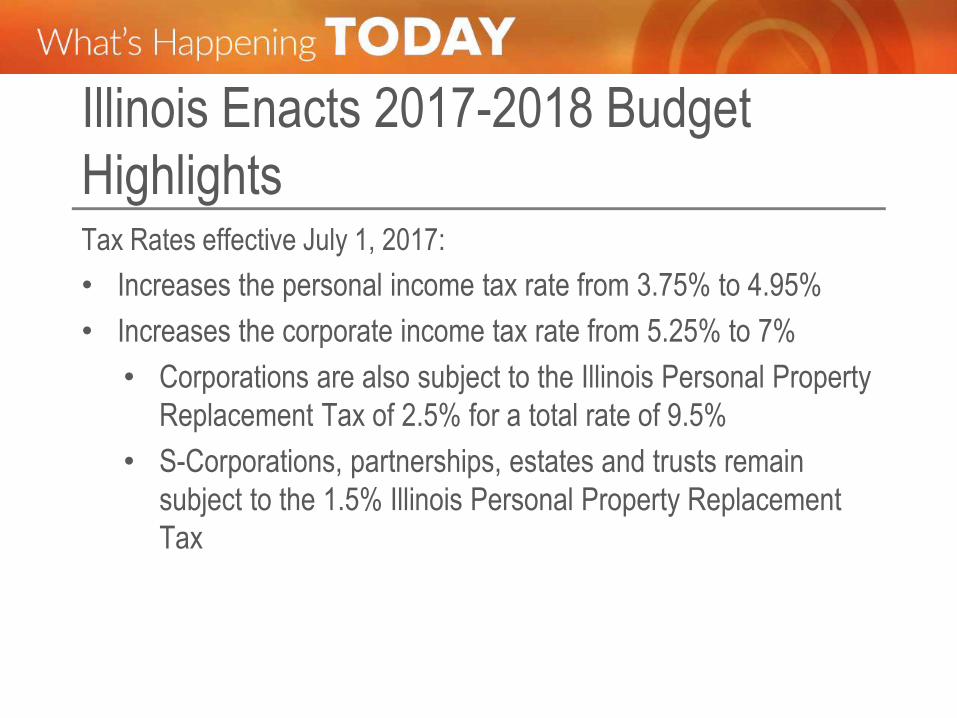

Illinois Enacts 2017-2018 Budget

Highlights Tax Rates effective July 1, 2017:

• Increases the personal income tax rate from 3.75% to 4.95%

• Increases the corporate income tax rate from 5.25% to 7%

• Corporations are also subject to the Illinois Personal Property

Replacement Tax of 2.5% for a total rate of 9.5%

• S-Corporations, partnerships, estates and trusts remain

subject to the 1.5% Illinois Personal Property Replacement

Tax

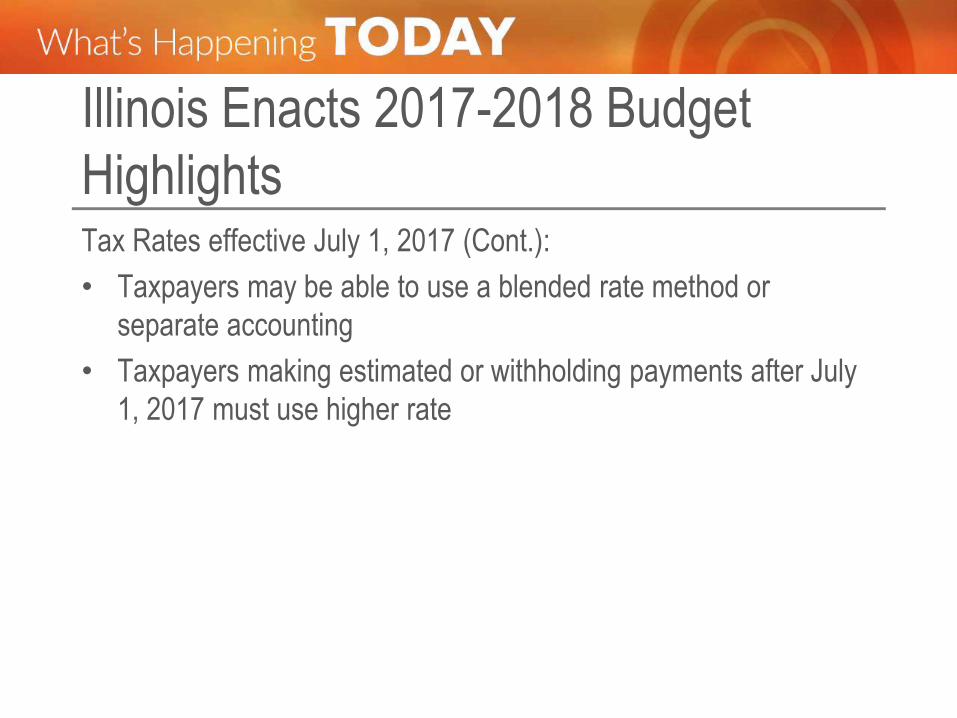

Illinois Enacts 2017-2018 Budget

Highlights Tax Rates effective July 1, 2017 (Cont.):

• Taxpayers may be able to use a blended rate method or

separate accounting

• Taxpayers making estimated or withholding payments after July

1, 2017 must use higher rate

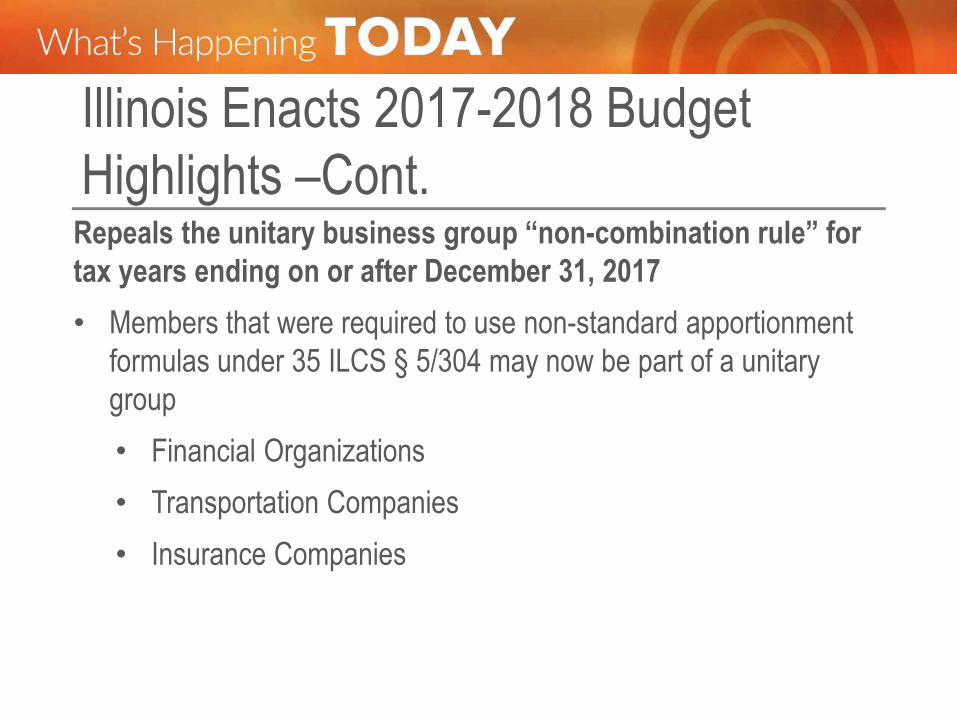

Illinois Enacts 2017-2018 Budget

Highlights –Cont. Repeals the unitary business group “non-combination rule” for

tax years ending on or after December 31, 2017

• Members that were required to use non-standard apportionment

formulas under 35 ILCS § 5/304 may now be part of a unitary

group

• Financial Organizations

• Transportation Companies

• Insurance Companies

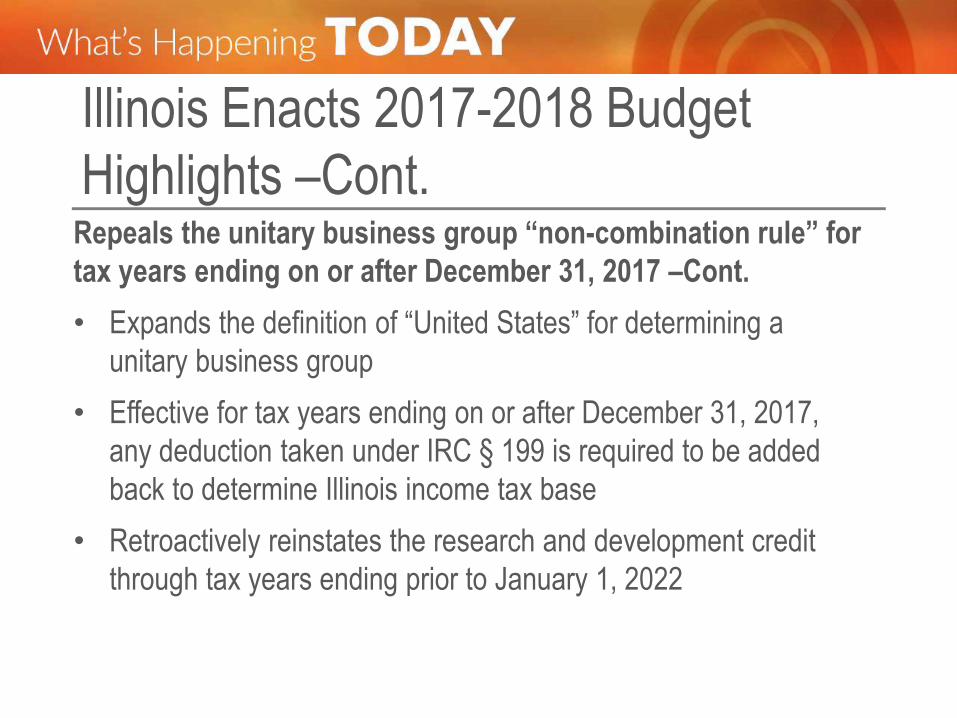

Illinois Enacts 2017-2018 Budget

Highlights –Cont. Repeals the unitary business group “non-combination rule” for

tax years ending on or after December 31, 2017 –Cont.

• Expands the definition of “United States” for determining a

unitary business group

• Effective for tax years ending on or after December 31, 2017,

any deduction taken under IRC § 199 is required to be added

back to determine Illinois income tax base

• Retroactively reinstates the research and development credit

through tax years ending prior to January 1, 2022

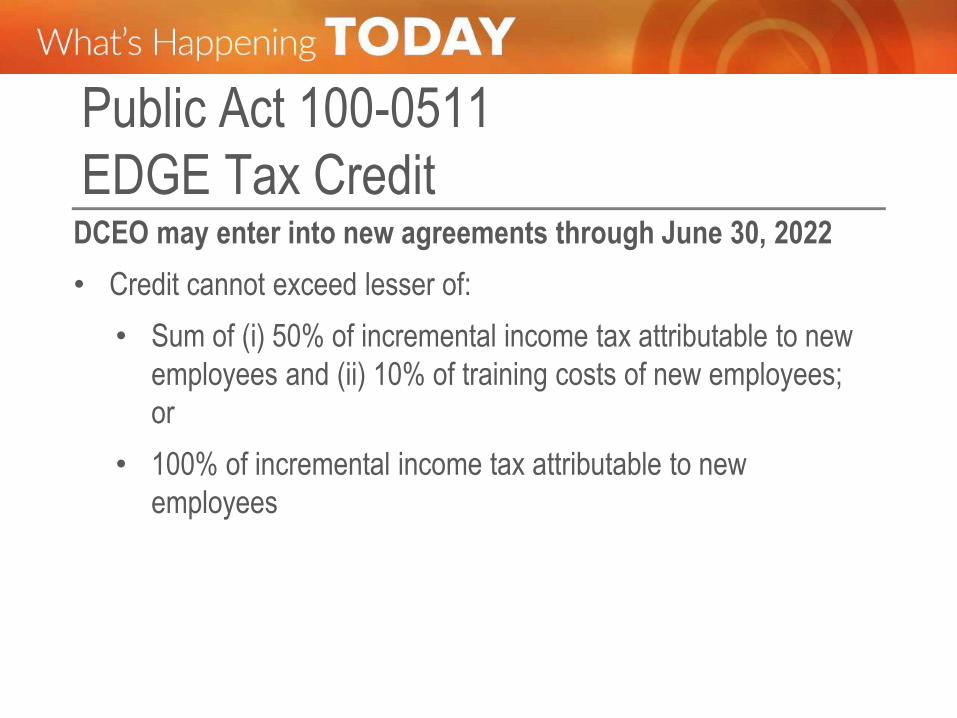

Public Act 100-0511

EDGE Tax Credit DCEO may enter into new agreements through June 30, 2022

• Credit cannot exceed lesser of:

• Sum of (i) 50% of incremental income tax attributable to new

employees and (ii) 10% of training costs of new employees;

or

• 100% of incremental income tax attributable to new

employees

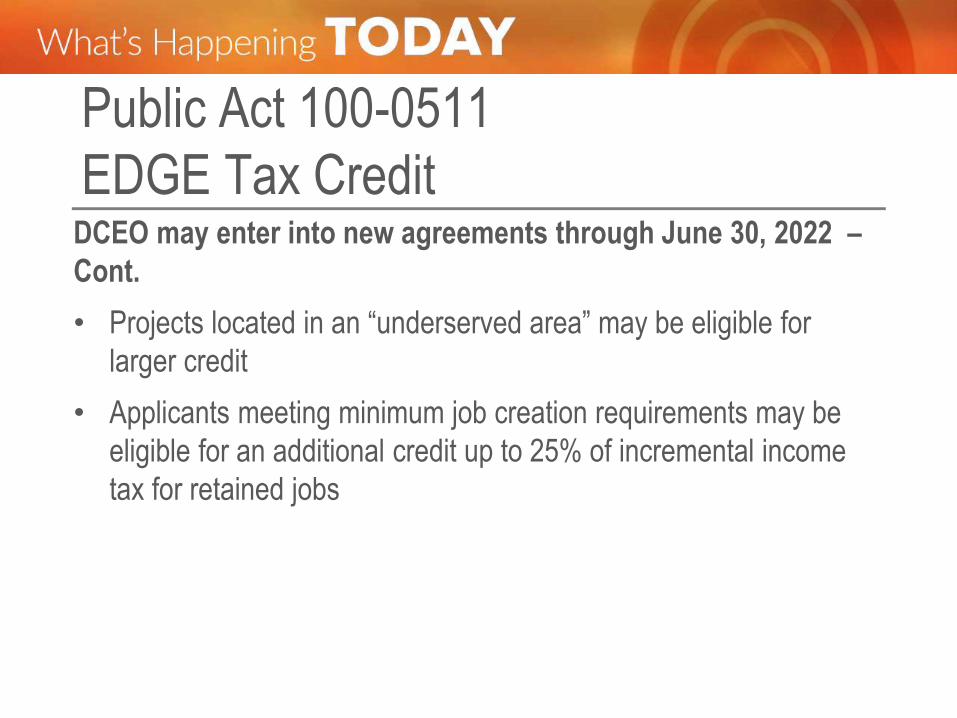

Public Act 100-0511

EDGE Tax Credit DCEO may enter into new agreements through June 30, 2022 –

Cont.

• Projects located in an “underserved area” may be eligible for

larger credit

• Applicants meeting minimum job creation requirements may be

eligible for an additional credit up to 25% of incremental income

tax for retained jobs

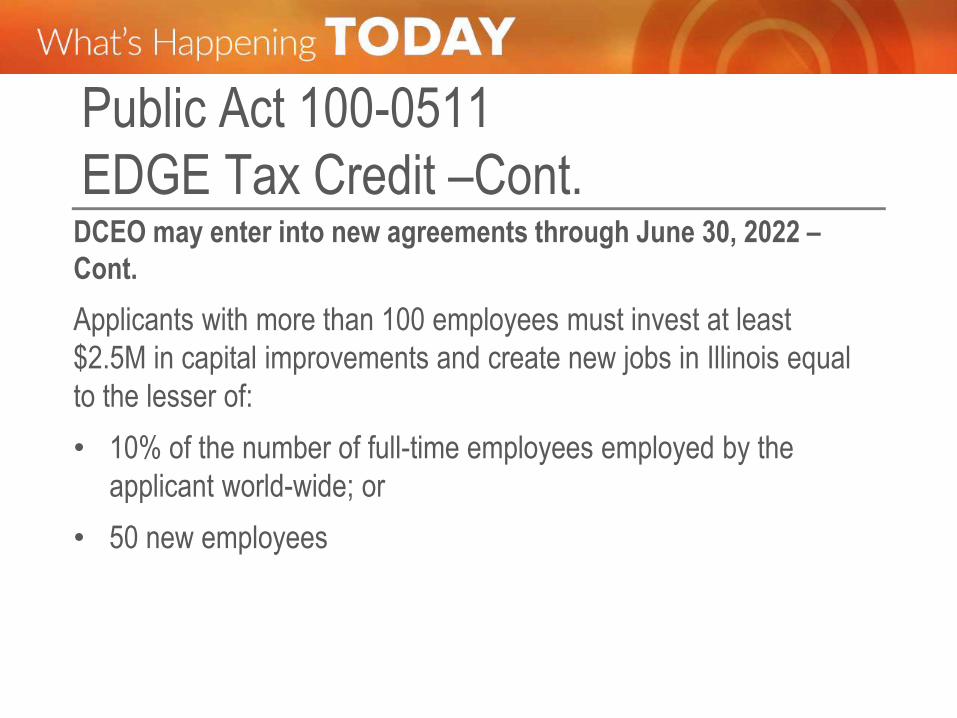

Public Act 100-0511

EDGE Tax Credit –Cont. DCEO may enter into new agreements through June 30, 2022 –

Cont.

Applicants with more than 100 employees must invest at least

$2.5M in capital improvements and create new jobs in Illinois equal

to the lesser of:

• 10% of the number of full-time employees employed by the

applicant world-wide; or

• 50 new employees

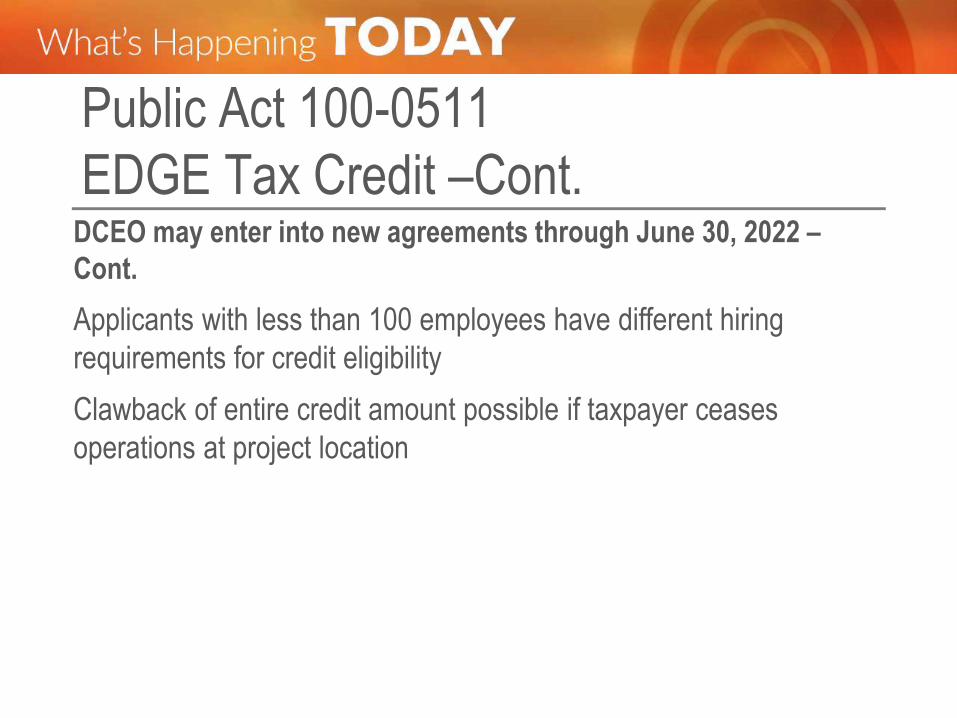

Public Act 100-0511

EDGE Tax Credit –Cont. DCEO may enter into new agreements through June 30, 2022 –

Cont.

Applicants with less than 100 employees have different hiring

requirements for credit eligibility

Clawback of entire credit amount possible if taxpayer ceases

operations at project location

Public Act 100-0465

“Invest in Kids Act” For taxable years beginning on or after January 1, 2018 and ending

before January 1, 2023, the Act provides an income tax credit for

qualified contributions made to scholarship granting organizations

• The organizations must provide scholarships for students to

attend a non-public school in Illinois

• The organizations must be approved to issue certificates of

receipt to taxpayers who make a qualified contribution

Public Act 100-0465

“Invest in Kids Act” –Cont. Credit is available to individuals, corporations, trusts, partners in

partnerships, shareholders of subchapter S corporations, owners of

limited liability companies, if the liability company is treated as a

partnership for federal and state income tax purposes, and other

taxpayers subject to Illinois income tax

Public Act 100-0465

“Invest in Kids Act” –Cont. Taxpayer is allowed a credit of 75% its qualified contributions,

limited to $1 million per taxpayer

• Illinois Department of Revenue limits credits awarded to $75

million per year

Credit may be carried forward 5 years

Credit may not be claimed for a qualified contribution for which

taxpayer claims a federal income tax deduction

• Individuals – Schedule A filers

Public Act 100-0437 “Rental Purchase

Agreement Occupation and Use Tax”

Tax goes into effect January 1, 2018

Imposes a 6.25% tax on persons in Illinois engaged in the business

of renting merchandise under a rental-purchase agreement

• Such persons must apply to the Department of Revenue for a

certificate of registration

Public Act 100-0437 “Rental Purchase

Agreement Occupation and Use Tax” –Cont.

Imposes a 6.25% tax on persons in Illinois using merchandise

rented from a merchant

• Tax is to be collected by merchant

• Consumer owes the tax to the Department if not collected by the

merchant

Use Tax and Retailer’s Occupation Tax are both amended to provide

and exception for “merchandise subject to the Rental Purchase

Agreement Occupation and Use Tax”

• Purchaser must certify that the item is purchased for the purpose

of renting

Cook County- Sweetened Beverage Tax

Update • On November 10, 2016 the Illinois Cook County Board of

Commissioners enacted the “Sweetened Beverage Tax”, a $0.01

per ounce tax imposed on the retail sale of all sweetened

beverages in Cook County. The tax became effective on July 1,

2017 and was imposed on any non-alcoholic beverage,

carbonated or non-carbonated, intended for human consumption,

contains any caloric sweetener or non-caloric sweetener, and

available for sale in a bottle or produced for sale through the use

of syrup and/or powder

Cook County- Sweetened Beverage Tax

Update –Cont. • Although the tax is ultimately born by the consumer, distributors

of the taxable bottled sweetened beverages, syrup and/or

powder used to produce a sweetened beverage were

responsible for collection of the tax on sales to retailers who

purchase bottled sweetened beverages or syrup and/or powder

used to produce a sweetened beverage, and remit that tax to

Cook County

• On October 11, 2017, the Illinois Cook County Board repealed

the Sweetened Beverage Tax Ordinance, effective December 1,

2017. The tax must continue to be paid, collected and remitted

through November 30, 2017

Income Tax Regulations 86 Ill. Admin. Code §§ 100.3380 and 100.3390

86 Ill. Admin. Code § 100.3380

• Changes to incidental or occasional sales rules

• Gross receipts from the sale of stock in a subsidiary are

excluded from the Illinois sales factor

• Creates a list of factors that may make exclusion appropriate

to a particular sale. The list includes incidental or occasional

sales not made in the market for the taxpayer’s goods or

services

Income Tax Regulations –Cont. 86 Ill. Admin. Code § 100.3380 –Cont.

• Repeal of “double-throwback” rule

• The rule required taxpayers selling tangible personal property

and that were taxable in neither the state of origin nor the state

of destination to throwback sales to Illinois if the taxpayer’s

activities in Illinois exceeded Public Law 86-272

• The regulation has been changed to limit this rule only to

taxable years ending on or before December 31, 2008

86 Ill. Admin. Code § 100.3390

• Updates to petitions for alternative apportionment to account for the

Illinois Independent Tax Tribunal and market-based sourcing

•

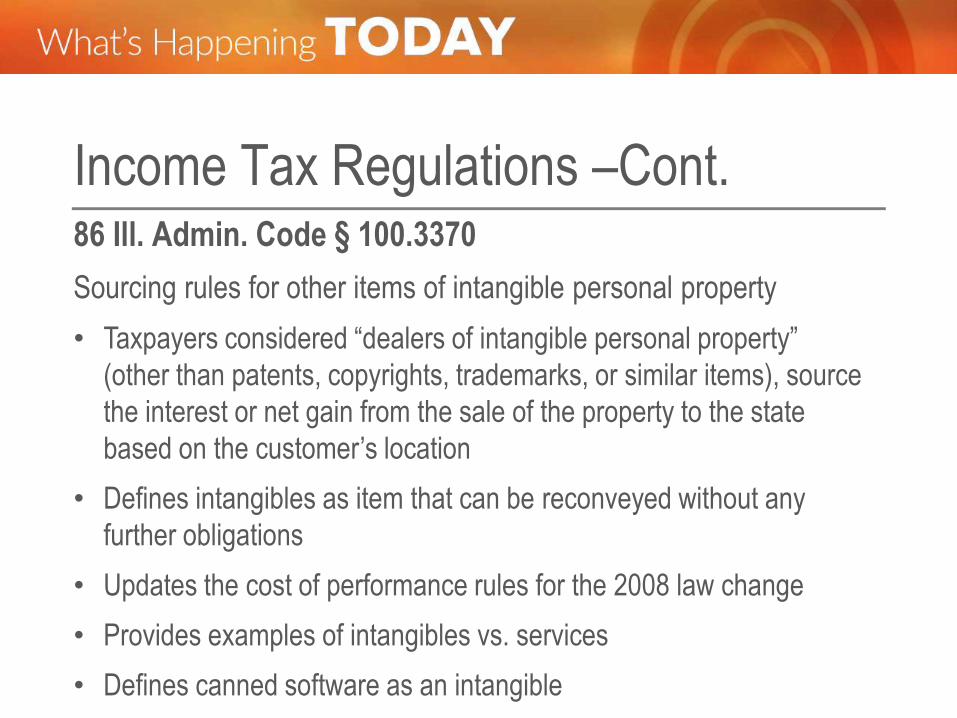

Income Tax Regulations –Cont. 86 Ill. Admin. Code § 100.3370

Sourcing rules for other items of intangible personal property

• Taxpayers considered “dealers of intangible personal property”

(other than patents, copyrights, trademarks, or similar items), source

the interest or net gain from the sale of the property to the state

based on the customer’s location

• Defines intangibles as item that can be reconveyed without any

further obligations

• Updates the cost of performance rules for the 2008 law change

• Provides examples of intangibles vs. services

• Defines canned software as an intangible

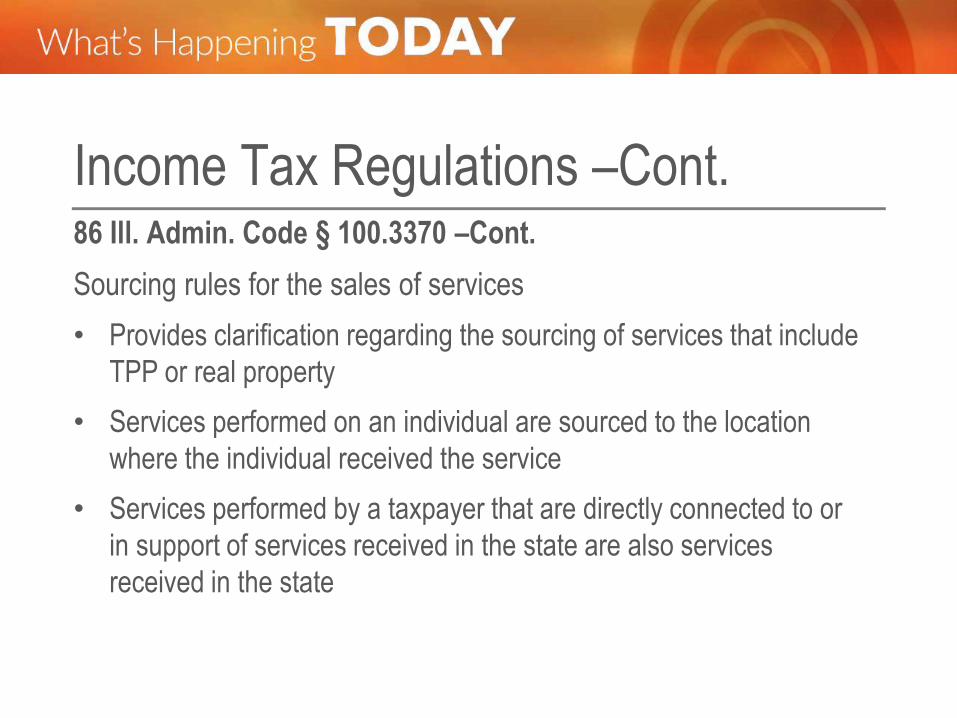

Income Tax Regulations –Cont. 86 Ill. Admin. Code § 100.3370 –Cont.

Sourcing rules for the sales of services

• Provides clarification regarding the sourcing of services that include

TPP or real property

• Services performed on an individual are sourced to the location

where the individual received the service

• Services performed by a taxpayer that are directly connected to or

in support of services received in the state are also services

received in the state

Income Tax Regulations –Cont. 86 Ill. Admin. Code § 100.3370 –Cont.

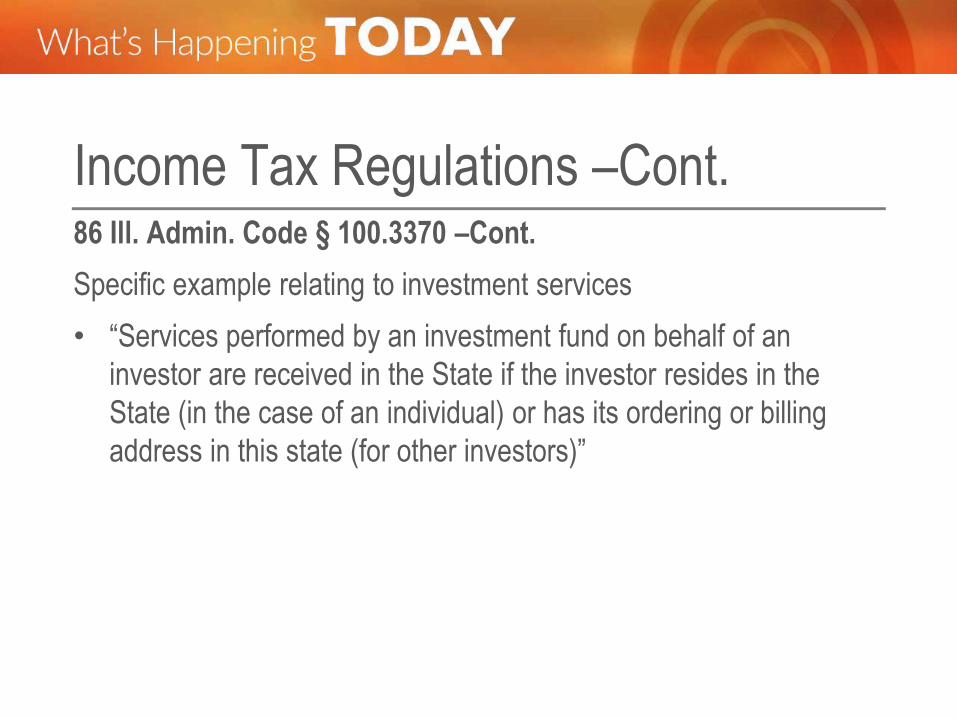

Specific example relating to investment services

• “Services performed by an investment fund on behalf of an

investor are received in the State if the investor resides in the

State (in the case of an individual) or has its ordering or billing

address in this state (for other investors)”

Income Tax Regulations –Cont. 86 Ill. Admin. Code § 100.3370 –Cont.

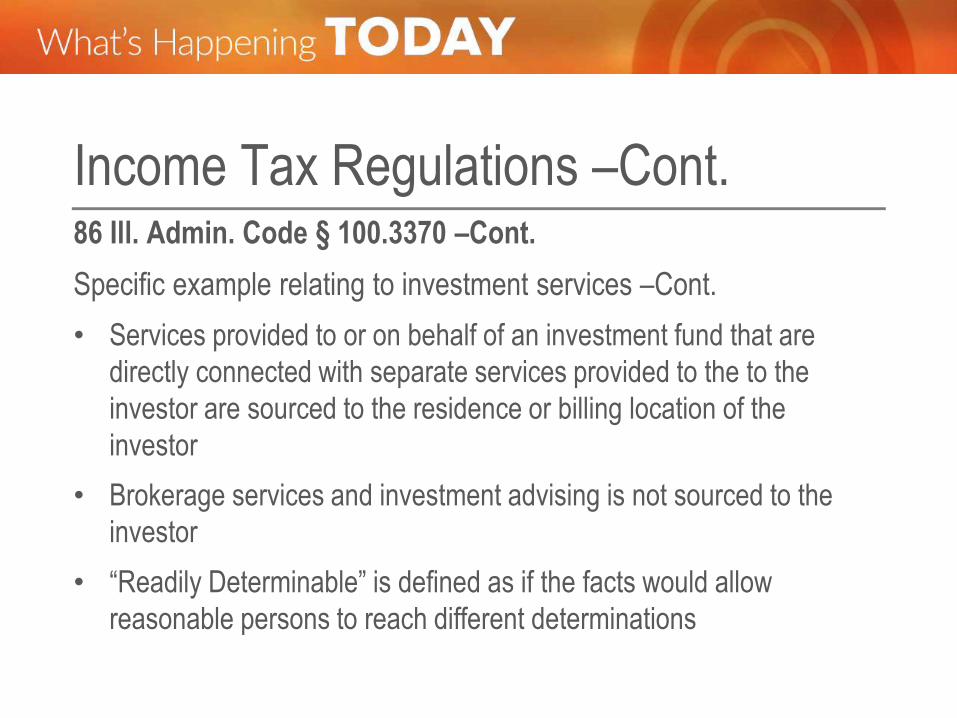

Specific example relating to investment services –Cont.

• Services provided to or on behalf of an investment fund that are

directly connected with separate services provided to the to the

investor are sourced to the residence or billing location of the

investor

• Brokerage services and investment advising is not sourced to the

investor

• “Readily Determinable” is defined as if the facts would allow

reasonable persons to reach different determinations

Income Tax Regulations –Cont. 86 Ill. Admin. Code § 100.3370 –Cont.

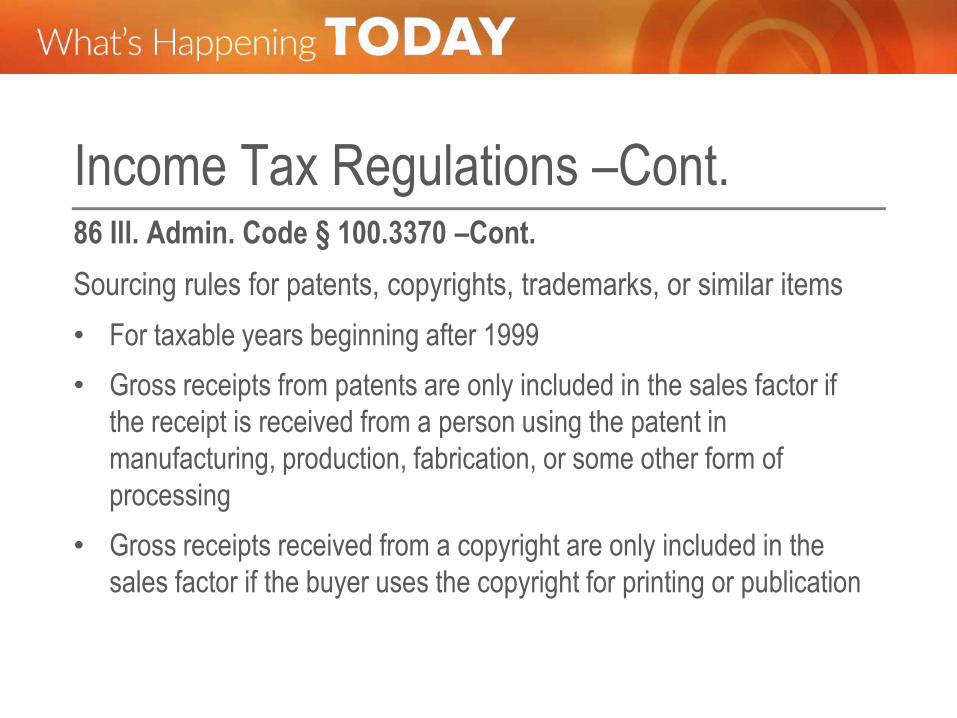

Sourcing rules for patents, copyrights, trademarks, or similar items

• For taxable years beginning after 1999

• Gross receipts from patents are only included in the sales factor if

the receipt is received from a person using the patent in

manufacturing, production, fabrication, or some other form of

processing

• Gross receipts received from a copyright are only included in the

sales factor if the buyer uses the copyright for printing or publication

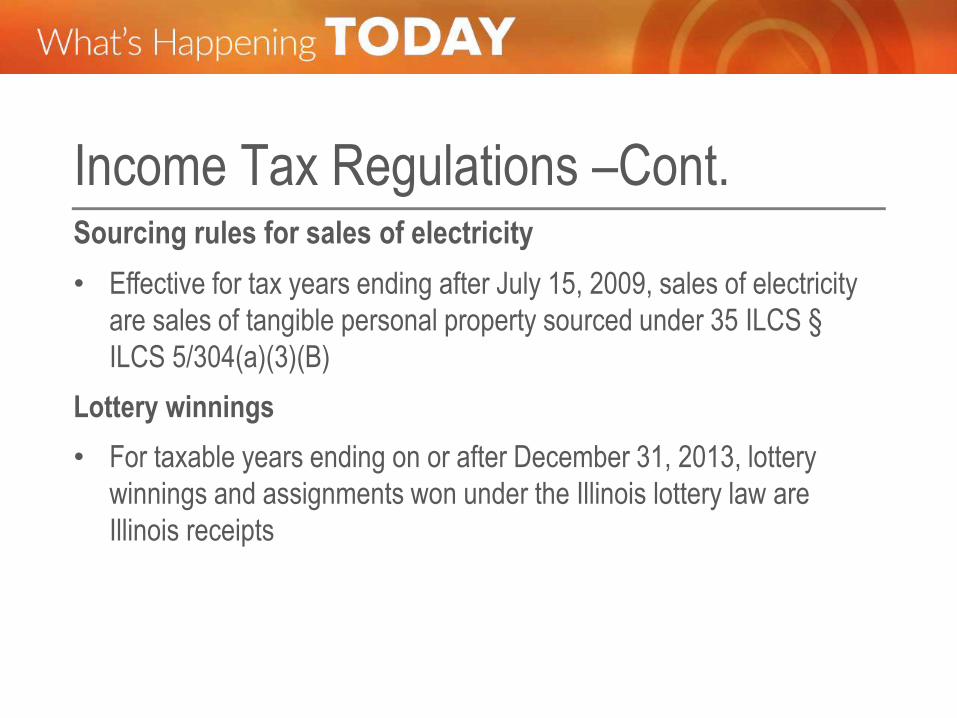

Income Tax Regulations –Cont. Sourcing rules for sales of electricity

• Effective for tax years ending after July 15, 2009, sales of electricity

are sales of tangible personal property sourced under 35 ILCS §

ILCS 5/304(a)(3)(B)

Lottery winnings

• For taxable years ending on or after December 31, 2013, lottery

winnings and assignments won under the Illinois lottery law are

Illinois receipts

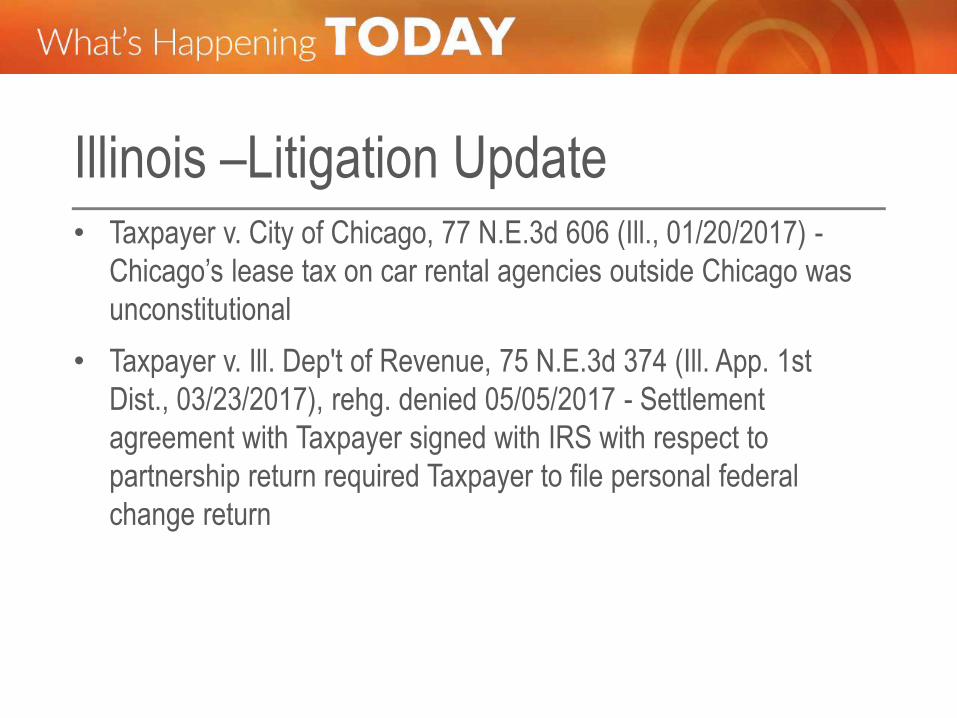

Illinois –Litigation Update • Taxpayer v. City of Chicago, 77 N.E.3d 606 (Ill., 01/20/2017) -

Chicago’s lease tax on car rental agencies outside Chicago was

unconstitutional

• Taxpayer v. Ill. Dep't of Revenue, 75 N.E.3d 374 (Ill. App. 1st

Dist., 03/23/2017), rehg. denied 05/05/2017 - Settlement

agreement with Taxpayer signed with IRS with respect to

partnership return required Taxpayer to file personal federal

change return

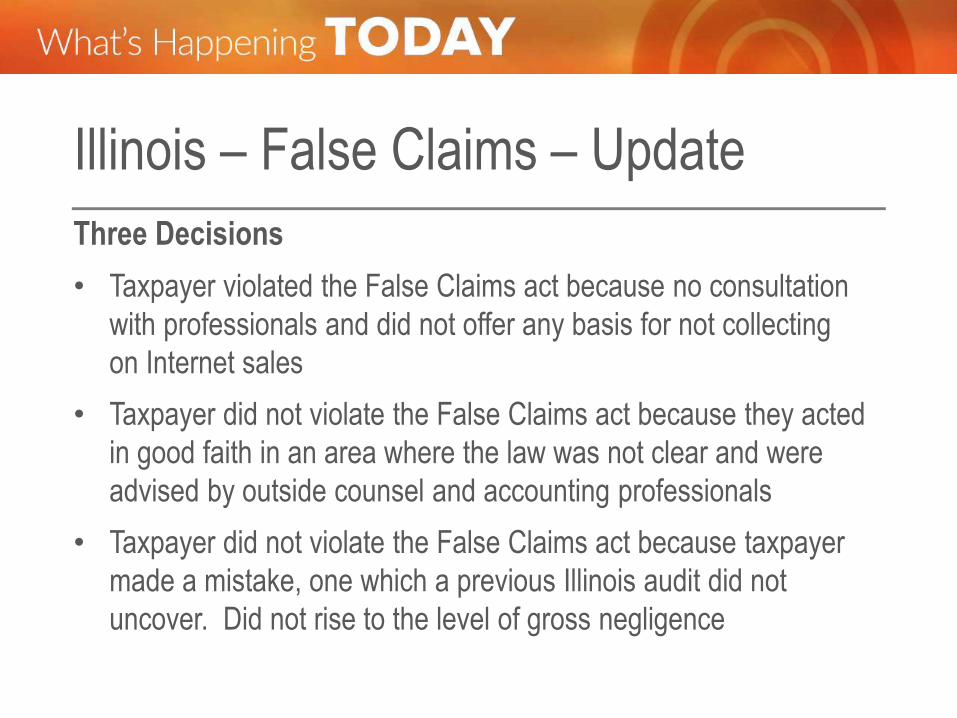

Illinois – False Claims – Update

Three Decisions

• Taxpayer violated the False Claims act because no consultation

with professionals and did not offer any basis for not collecting

on Internet sales

• Taxpayer did not violate the False Claims act because they acted

in good faith in an area where the law was not clear and were

advised by outside counsel and accounting professionals

• Taxpayer did not violate the False Claims act because taxpayer

made a mistake, one which a previous Illinois audit did not

uncover. Did not rise to the level of gross negligence

FEATURING SPECIAL GUESTS:

Mr. John Coalson

Partner

Alston & Bird LLP

Atlanta, GA

Ms. Diann Smith

Counsel

McDermott Will & Emery LLP

Washington, DC

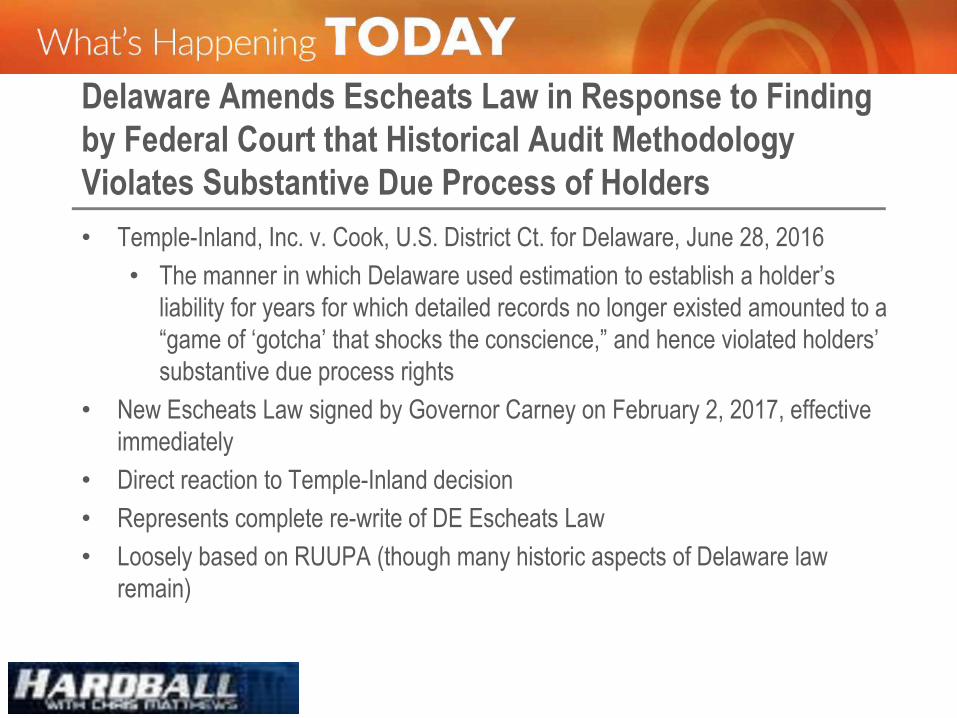

Delaware Amends Escheats Law in Response to Finding

by Federal Court that Historical Audit Methodology

Violates Substantive Due Process of Holders

• Temple-Inland, Inc. v. Cook, U.S. District Ct. for Delaware, June 28, 2016

• The manner in which Delaware used estimation to establish a holder’s

liability for years for which detailed records no longer existed amounted to a

“game of ‘gotcha’ that shocks the conscience,” and hence violated holders’

substantive due process rights

• New Escheats Law signed by Governor Carney on February 2, 2017, effective

immediately

• Direct reaction to Temple-Inland decision

• Represents complete re-write of DE Escheats Law

• Loosely based on RUUPA (though many historic aspects of Delaware law

remain)

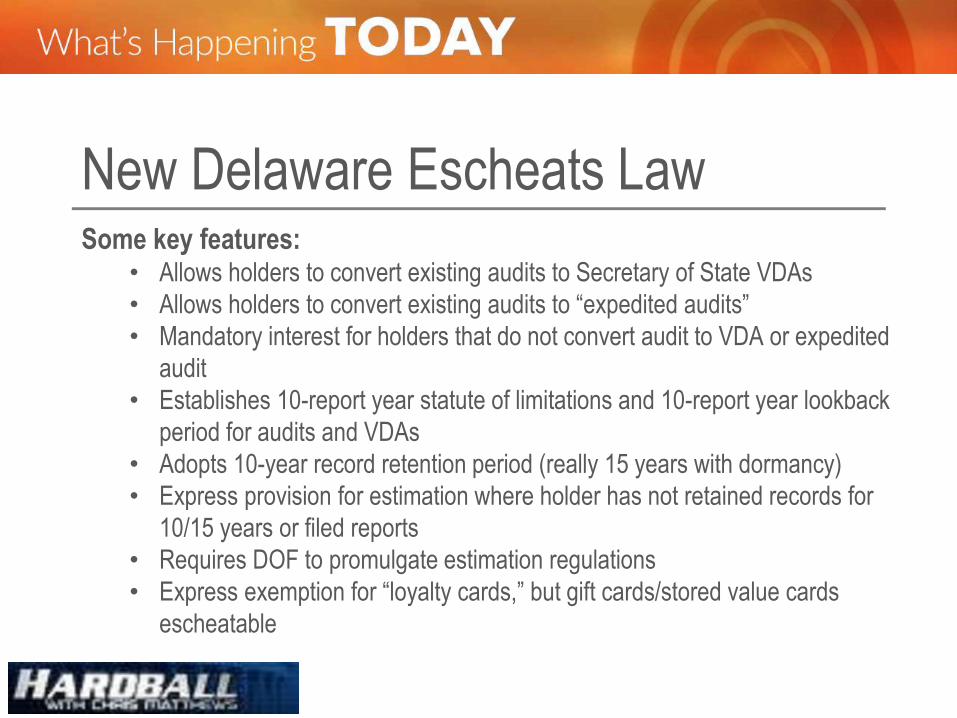

New Delaware Escheats Law Some key features:

• Allows holders to convert existing audits to Secretary of State VDAs

• Allows holders to convert existing audits to “expedited audits”

• Mandatory interest for holders that do not convert audit to VDA or expedited

audit

• Establishes 10-report year statute of limitations and 10-report year lookback

period for audits and VDAs

• Adopts 10-year record retention period (really 15 years with dormancy)

• Express provision for estimation where holder has not retained records for

10/15 years or filed reports

• Requires DOF to promulgate estimation regulations

• Express exemption for “loyalty cards,” but gift cards/stored value cards

escheatable

New Delaware Escheats Law –Cont. Conversion of pending audit to Voluntary Disclosure:

• Must have received audit notice on/before July 22, 2015

• Must file Notice of Intent to Convert within 60 days of DoF’s

adoption of estimation regulation (Monday December 11)

• No audit workpapers to be transferred, and no coordination or

consultation with DoF or any third-party audit firm

• However, holders are expected to utilize same audit scope and

are not expected to “start over”

• Clear that estimation will be required using DE’s historical

estimation methodology

Delaware Expands Its Attack on Retail/Hospital

Industries and Other Issuers of Gift Cards

• CardFact qui tam litigation

• Kelmar audits of gift card structures and special purpose entities

• Kelmar audits of loyalty programs

• Implications of Plains All-American Pipeline, Marathon/Speedway,

and Office Depot decisions

• Computation of “maximum cost” per new DOF audit regulations

• New Section 1147(a): “A holder may not assign or otherwise

transfer its obligation to hold for or pay or deliver property or to

comply with the duties of this chapter, other than to a parent,

subsidiary, or affiliate of the holder”

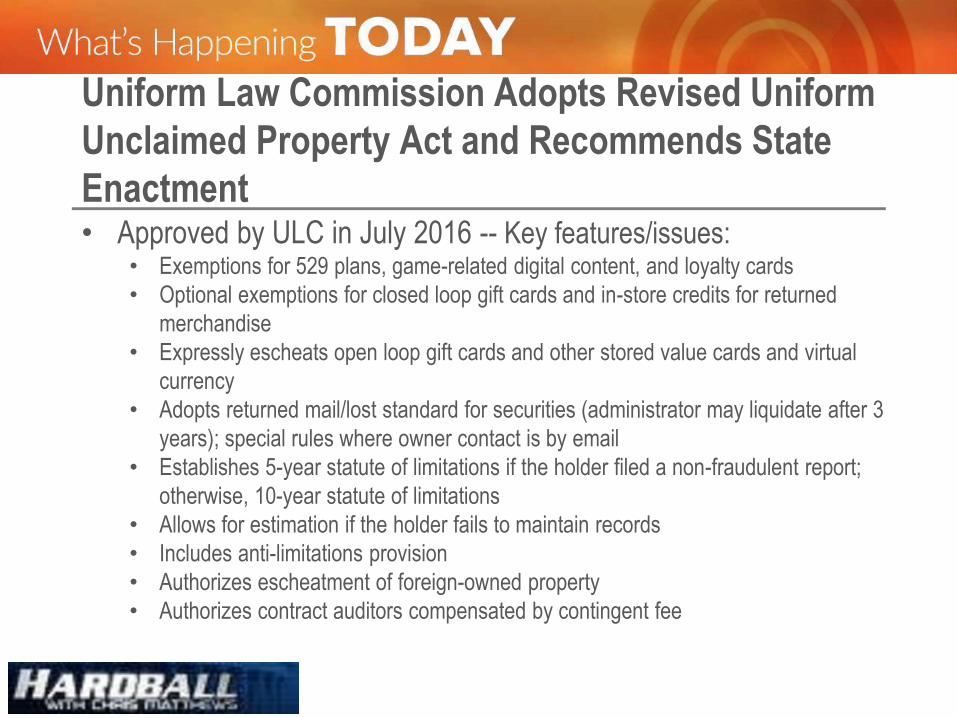

Uniform Law Commission Adopts Revised Uniform

Unclaimed Property Act and Recommends State

Enactment • Approved by ULC in July 2016 -- Key features/issues:

• Exemptions for 529 plans, game-related digital content, and loyalty cards

• Optional exemptions for closed loop gift cards and in-store credits for returned

merchandise

• Expressly escheats open loop gift cards and other stored value cards and virtual

currency

• Adopts returned mail/lost standard for securities (administrator may liquidate after 3

years); special rules where owner contact is by email

• Establishes 5-year statute of limitations if the holder filed a non-fraudulent report;

otherwise, 10-year statute of limitations

• Allows for estimation if the holder fails to maintain records

• Includes anti-limitations provision

• Authorizes escheatment of foreign-owned property

• Authorizes contract auditors compensated by contingent fee

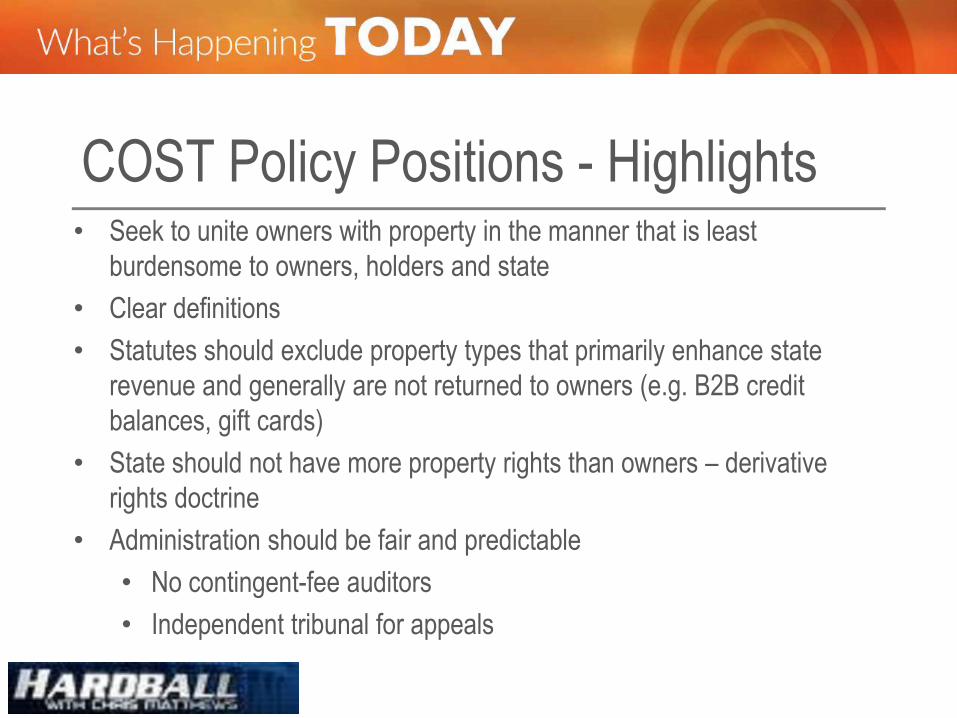

COST Policy Positions - Highlights • Seek to unite owners with property in the manner that is least

burdensome to owners, holders and state

• Clear definitions

• Statutes should exclude property types that primarily enhance state

revenue and generally are not returned to owners (e.g. B2B credit

balances, gift cards)

• State should not have more property rights than owners – derivative

rights doctrine

• Administration should be fair and predictable

• No contingent-fee auditors

• Independent tribunal for appeals

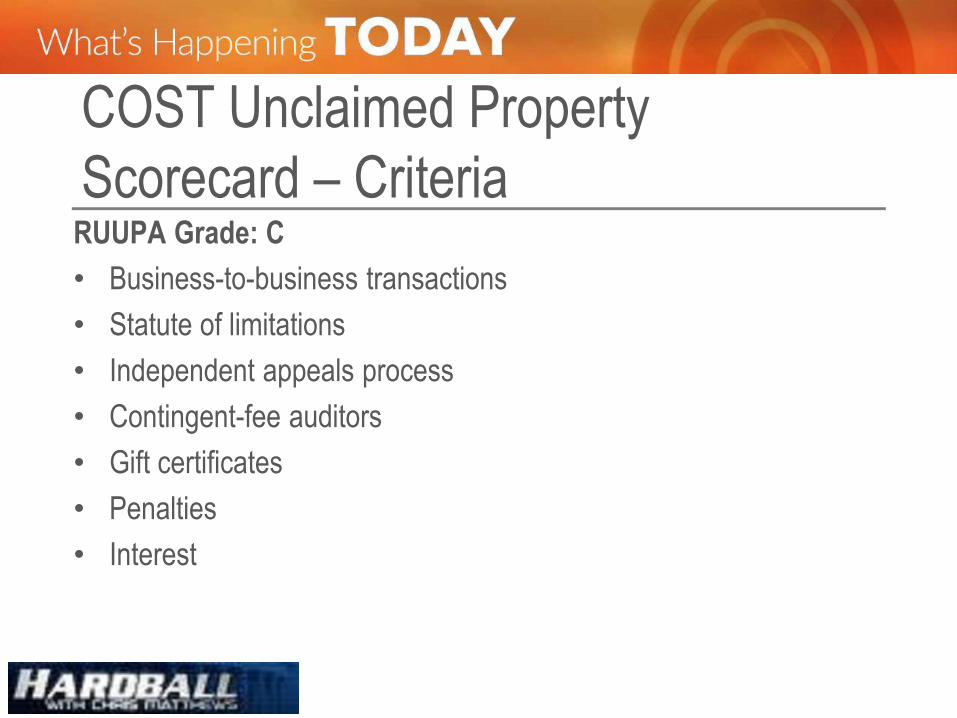

COST Unclaimed Property

Scorecard – Criteria RUUPA Grade: C

• Business-to-business transactions

• Statute of limitations

• Independent appeals process

• Contingent-fee auditors

• Gift certificates

• Penalties

• Interest

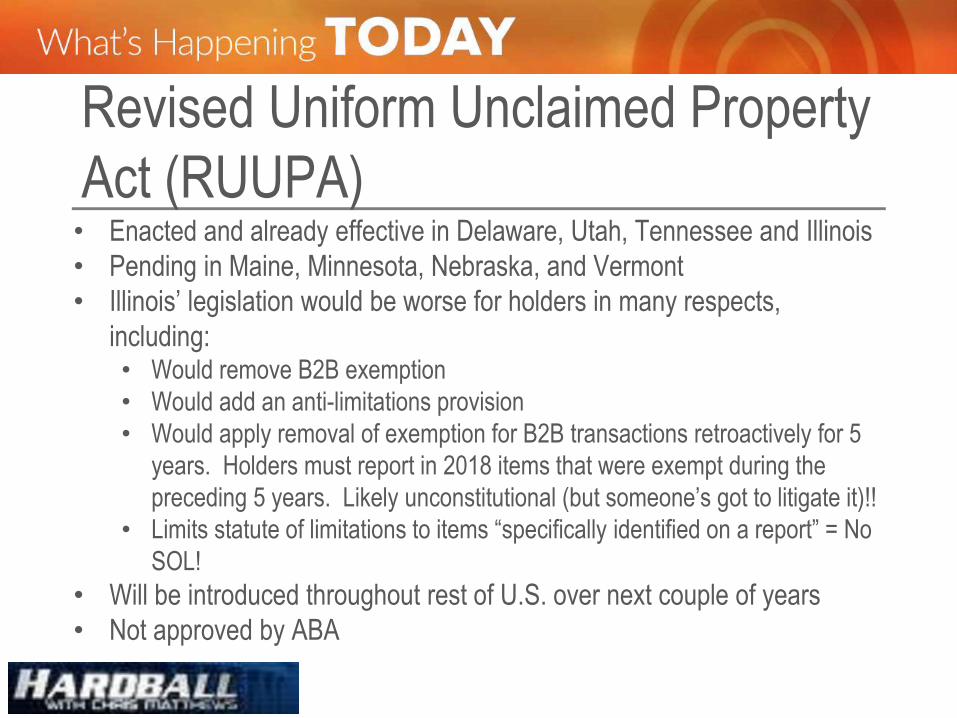

Revised Uniform Unclaimed Property

Act (RUUPA) • Enacted and already effective in Delaware, Utah, Tennessee and Illinois

• Pending in Maine, Minnesota, Nebraska, and Vermont

• Illinois’ legislation would be worse for holders in many respects,

including: • Would remove B2B exemption

• Would add an anti-limitations provision

• Would apply removal of exemption for B2B transactions retroactively for 5

years. Holders must report in 2018 items that were exempt during the

preceding 5 years. Likely unconstitutional (but someone’s got to litigate it)!!

• Limits statute of limitations to items “specifically identified on a report” = No

SOL!

• Will be introduced throughout rest of U.S. over next couple of years

• Not approved by ABA

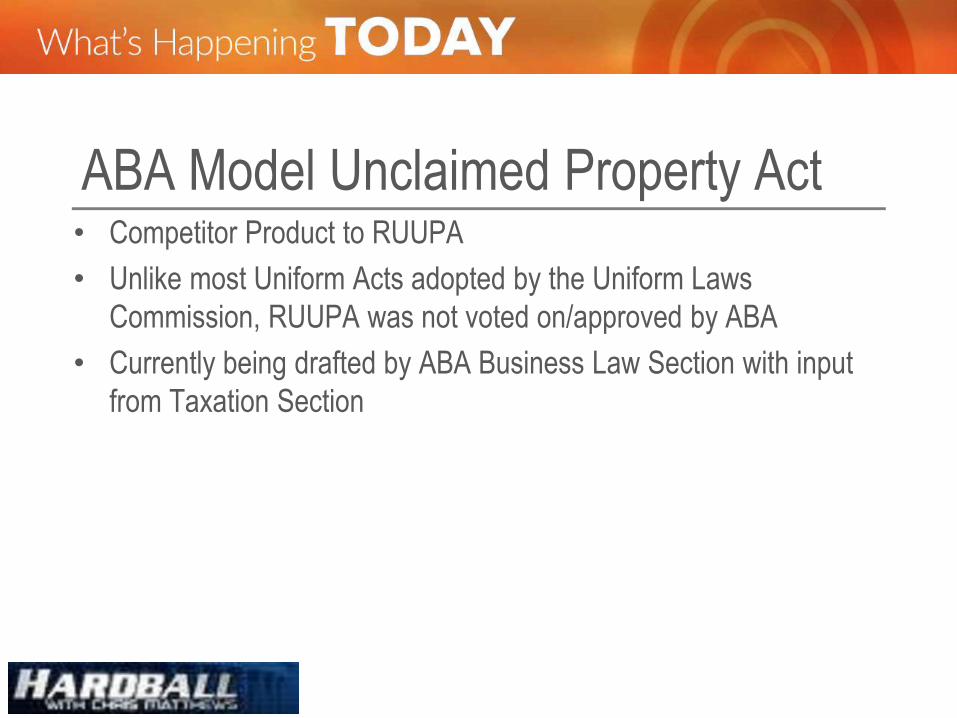

ABA Model Unclaimed Property Act • Competitor Product to RUUPA

• Unlike most Uniform Acts adopted by the Uniform Laws

Commission, RUUPA was not voted on/approved by ABA

• Currently being drafted by ABA Business Law Section with input

from Taxation Section

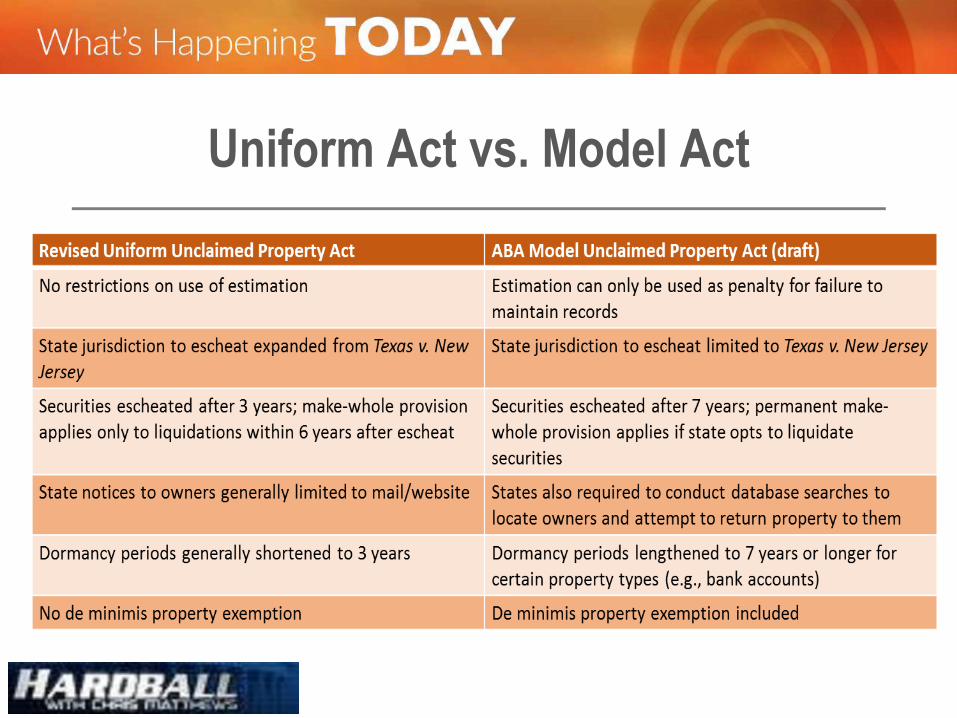

Uniform Act vs. Model Act

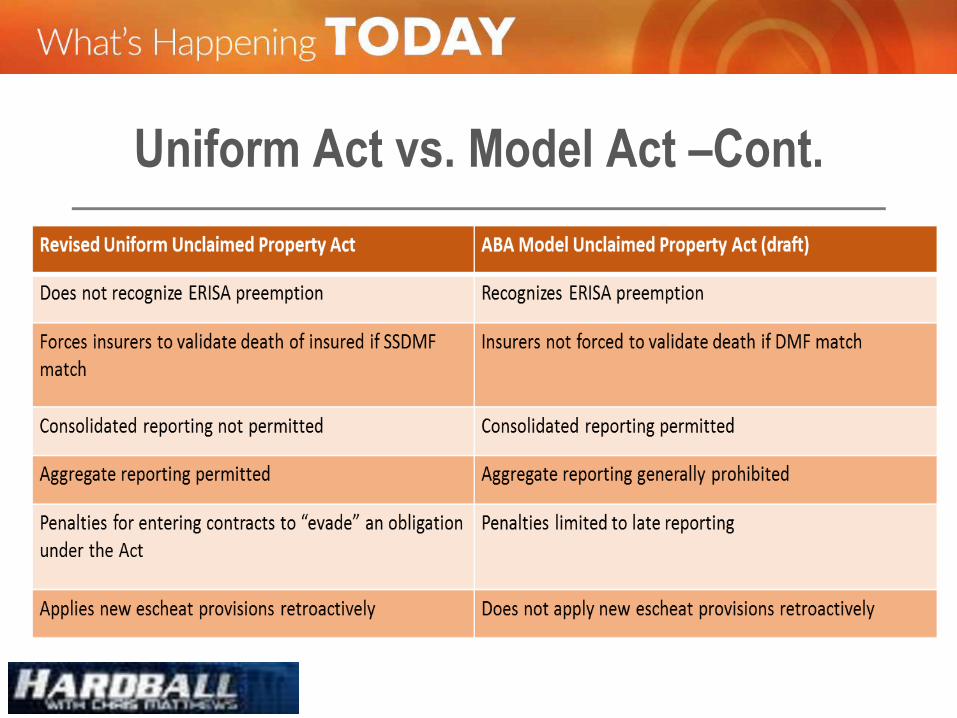

Uniform Act vs. Model Act –Cont.

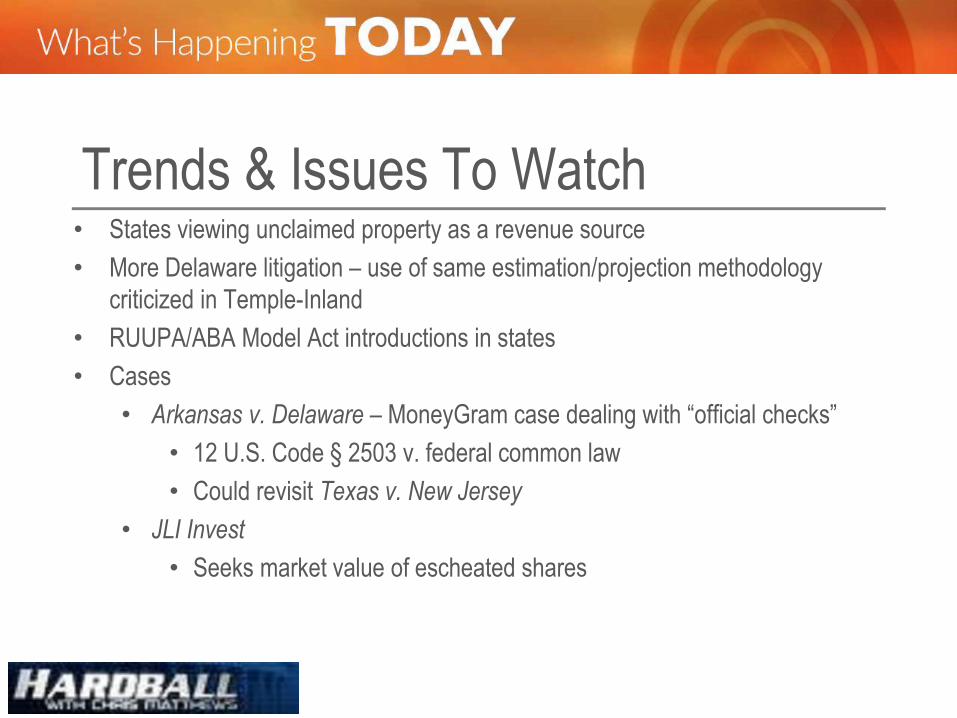

Trends & Issues To Watch • States viewing unclaimed property as a revenue source

• More Delaware litigation – use of same estimation/projection methodology

criticized in Temple-Inland

• RUUPA/ABA Model Act introductions in states

• Cases

• Arkansas v. Delaware – MoneyGram case dealing with “official checks”

• 12 U.S. Code § 2503 v. federal common law

• Could revisit Texas v. New Jersey

• JLI Invest

• Seeks market value of escheated shares

California’s New Tax Agencies and

Procedures

Mr. Edwin P. Antolin

Antolin Agarwal LLP

California’s New Tax Agencies

• Board of Equalization Reform

• What prompted the Legislature and Governor to push for reform in 2017?

• State Controller issued a critical report in November 2015

• Series of highly critical newspaper articles in the Sacramento Bee and Los Angeles Times in the first half of 2017

• Department of Finance issued another critical report in March 2017

California’s New Tax Agencies –Cont.

• What prompted the Legislature and Governor to push for reform in 2017? –Cont.

• April 2017 – Governor Brown intervened:

• Directed the Department of Human Resources and Department of Justice to investigate BOE employee complaints

• Suspended the BOE’s delegated authority for personnel, contracting, and technology

• Called on Legislature to address the BOE problems and enact changes by June 2017

The Taxpayer Transparency and Fairness

Act of 2017 (Assembly Bill 102) –Cont. • Signed into law on June 27, 2017; effective July 1, 2017 (only 4

days after enactment)

• Divests BOE of authority to administer taxes and fees imposed by statutes (as of July 1, 2017) and authority to hear and decide tax appeals (as of January 1, 2018)

• The BOE will continue perform duties granted under the California Constitution, including property tax equalization, assessment of state assessed properties, administration of insurance tax, and assessment of excise taxes on alcoholic beverages

The Taxpayer Transparency and Fairness

Act of 2017 (Assembly Bill 102) –Cont. • Prohibits ex parte communications with Board members as of

July 1, 2017

• AB 102 did not change the duties of the Franchise Tax Board, which administers the corporate franchise tax and personal income tax

The Taxpayer Transparency and

Fairness Act of 2017 (Assembly Bill 102) • AB 102 Established Two New Tax Agencies–

• The California Department of Tax and Fee Administration (CDTFA) took over the duties to assess and collect the statutory taxes and fees previously administered by the BOE on July 1, 2017

• The taxes administered by the CDTFA include the sales/use tax, tobacco taxes and fuel taxes

The Taxpayer Transparency and Fairness

Act of 2017 (Assembly Bill 102) –Cont. • The Office of Tax Appeals (OTA) will take over the BOE’s tax

appeals function beginning January 1, 2017

• OTA will hear taxpayer appeals of business tax assessments (i.e., sales/use taxes and various other taxes and fees) and appeals of corporation franchise tax and personal income tax assessments

California Department of Tax and Fee

Administration • CDTFA is under the Governor’s authority. The Governor

appoints the director, chief deputy director, and chief counsel

• Governor Brown appointed Nicolas Maduros as CDTFA’s first director. He is an attorney. He was chief of staff at the U.S. Small Business Administration and worked for a government relations firm in D.C.

• Governor Brown appointed Tad Egawa as chief counsel. He was general counsel of the California Department of Housing an Community Development, and also worked at the California Bureau of Real Estate, the California Department of Justice, and in private practice

Office of Tax Appeals • The OTA is under the Governor’s authority. The Governor

appoints the director, chief deputy director, and chief counsel

• Governor Brown appointed Kristen Kane as chief counsel. She also will serve as the acting director. She was with the deputy director of the California Competes Tax Credit Program, and prior to that was an FTB attorney

• November 22, 2017 – Mark Ibele appointed Director of OTA

• The OTA will hear most state tax appeals in California. (Payroll tax appeals will continue to be heard by the California Unemployment Insurance Appeals Board)

• Tax appeals will be heard by 3 judge panels of administrative law judges

Office of Tax Appeals –Cont. • The new ALJs must have the following qualifications:

• An active bar membership for at least 5 years, and

• Knowledge and experience with regard to the administration and operation of the tax and fee laws of the United States and of California

• OTA announced that the ALJ panels will begin hearing appeals in January 2018

• OTA plans to arrange ALJ training sessions

Office of Tax Appeals –Cont. • The ALJ panels will hear cases in Fresno, Sacramento and Los

Angeles

• 12 ALJs will be based in Sacramento and 6 will be based in Los Angeles. ALJs will travel to Fresno for hearings

• OTA is planning to hire 18 ALJs

• Assembly Bill 102 provides that appeals will be conducted pursuant to the APA except as provided in the bill

Office of Tax Appeals –Cont. • “To the extent possible” regulations adopted to carry out the

purpose of the OTA shall be consistent with the Model State Administrative Tax Tribunal Act dated August 2006 adopted by the American Bar Association

• Key provisions of the ABA Model State Administrative Tax Tribunal Act provide that a “taxpayer shall have the right to have his case heard by the Tax Tribunal prior to the payment of any of the amounts asserted as due . . . and prior to the posting of any bond.”

• A taxpayer “shall be entitled to judicial review of a final decision of the Tax Tribunal . . . in accordance with the procedure for appeal from a decision of a [general trial] court.”

Office of Tax Appeals –Cont. • “To the extent possible” regulations adopted to carry out the

purpose of the OTA shall be consistent with the Model State Administrative Tax Tribunal Act dated August 2006 adopted by the American Bar Association. –Cont.

• Appearances in proceedings conducted by the Tax Tribunal may be by the taxpayer, by an attorney admitted to practice in the state (including an attorney who is a partner or member of, or is employed by, an accounting or other professional services firm), by an accountant licensed in this State, or by an enrolled agent authorized to practice before the IRS

• Prohibits ex parte communications with ALJs

Office of Tax Appeals –Cont. • Assembly Bill 131 – Clean Up Legislation

• Clarifies that sales/use tax appeals conferences will be conducted by the CDTFA, and a taxpayer may request a hearing before the OTA if it disagrees with the appeals conference.

• Directs that the OTA establish a procedure for closed hearings

• Clarifies that the OTA is not a tax court. Thus, non-attorneys may appear before the OTA.

Office of Tax Appeals –Cont. • Assembly Bill 131 – Clean Up Legislation –Cont.

• Transitional Rule – The BOE shall continue to have the legal authority to hear, determine, decide, or take any other action with respect to an appeal regarding matters for which the duties, powers, and responsibilities are transferred to the Office of Tax Appeals only if both of the following are satisfied:

• (A) The hearing, determination, decision, or any other action with respect to an appeal is placed on the calendar of a meeting of the State Board of Equalization to be held before January 1, 2018.

• (B) The appeal is heard, determined, decided, or is otherwise final before January 1, 2018.

Office of Tax Appeals –Cont. • Emergency Draft Regulations issued on October 23, 2017

• Provides guidelines for how to file an appeal and instructions on filing briefs

• Allows prehearing conferences with OTA

• Requires a written request for an oral hearing

• In order to exercise the right to an oral hearing, the appellant must submit a written request no later than the date of the appellant’s reply brief and must timely respond to any request by OTA for confirmation that the appellant still seeks an oral hearing. A request for an oral hearing may be included in appellant’s appeal letter or briefing and should indicate whether the appellant prefers a hearing in Sacramento, Los Angeles, or Fresno

Office of Tax Appeals –Cont. • Emergency Draft Regulations issued on October 23, 2017

–Cont.

• Provides written options for each appeal. However, only opinions designated as “precedential” will be binding precedent.

• Declares that BOE published opinions are not binding authority. They are merely persuasive authority. This provision may be in conflict with Rev. & Tax. Code § 40, which provides that any formal BOE opinion may be cited as precedent before the BOE.

Office of Tax Appeals –Cont. • Emergency Draft Regulations issued on October 23, 2017

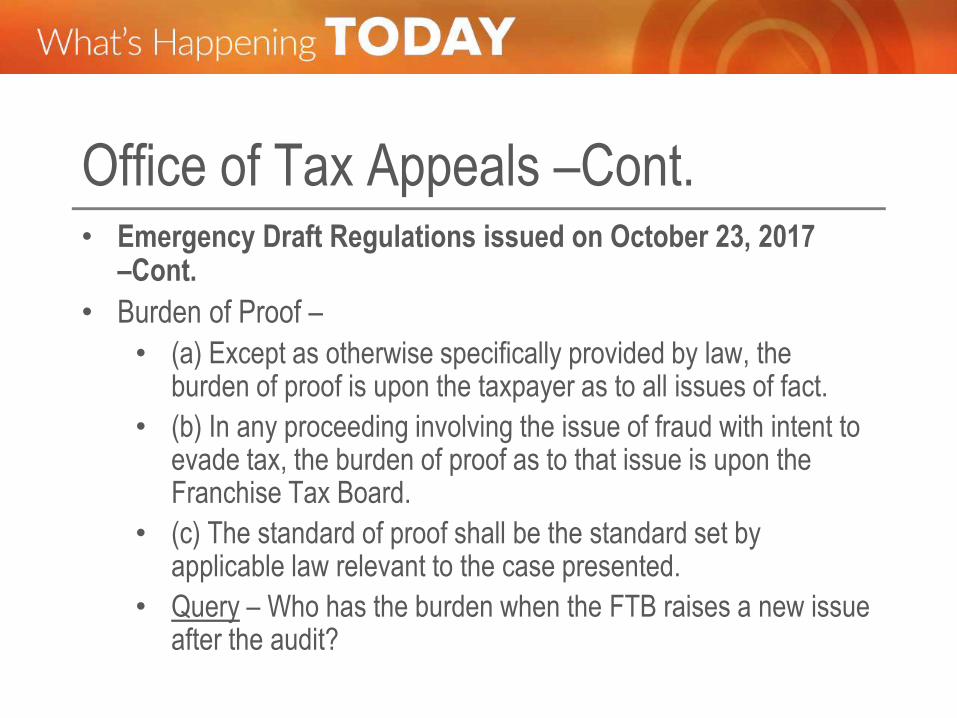

–Cont.

• Burden of Proof –

• (a) Except as otherwise specifically provided by law, the burden of proof is upon the taxpayer as to all issues of fact.

• (b) In any proceeding involving the issue of fraud with intent to evade tax, the burden of proof as to that issue is upon the Franchise Tax Board.

• (c) The standard of proof shall be the standard set by applicable law relevant to the case presented.

• Query – Who has the burden when the FTB raises a new issue after the audit?

Office of Tax Appeals –Cont. • Emergency Draft Regulations issued on October 23, 2017

–Cont.

• Provides for deferral of appeal if CDFTA and taxpayer are engaged in settlement negotiations.

• There is no deferral provision if FTB and taxpayer are engaged in settlement negotiations. However, the draft regulations generally provide for deferral based on reasonable cause.

Office of Tax Appeals –Cont. • Emergency Draft Regulations issued on October 23, 2017

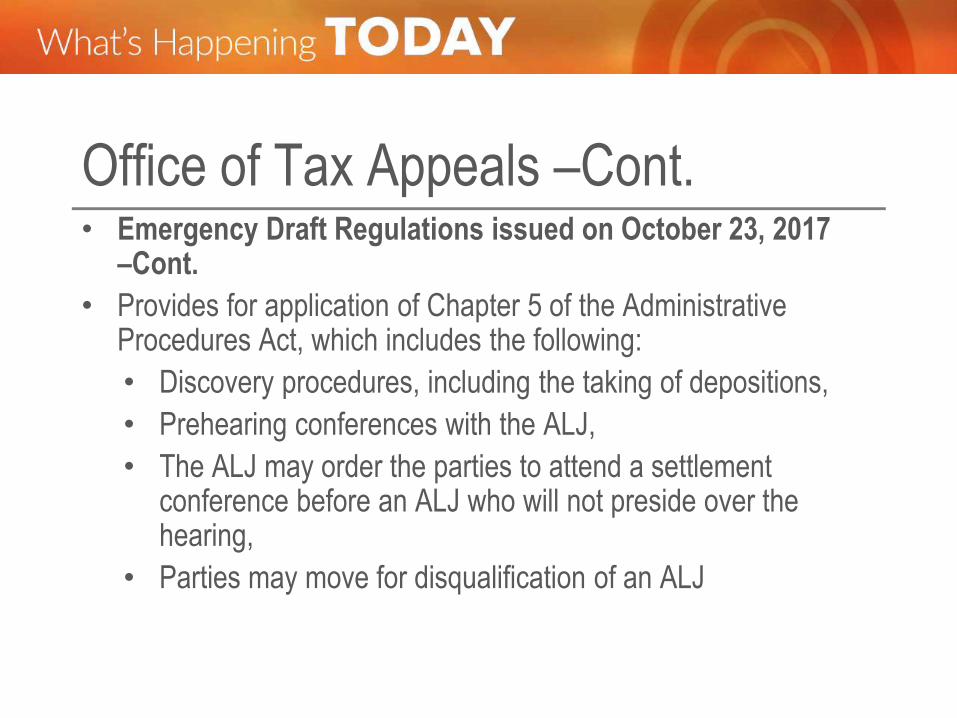

–Cont.

• Provides for application of Chapter 5 of the Administrative Procedures Act, which includes the following:

• Discovery procedures, including the taking of depositions,

• Prehearing conferences with the ALJ,

• The ALJ may order the parties to attend a settlement conference before an ALJ who will not preside over the hearing,

• Parties may move for disqualification of an ALJ

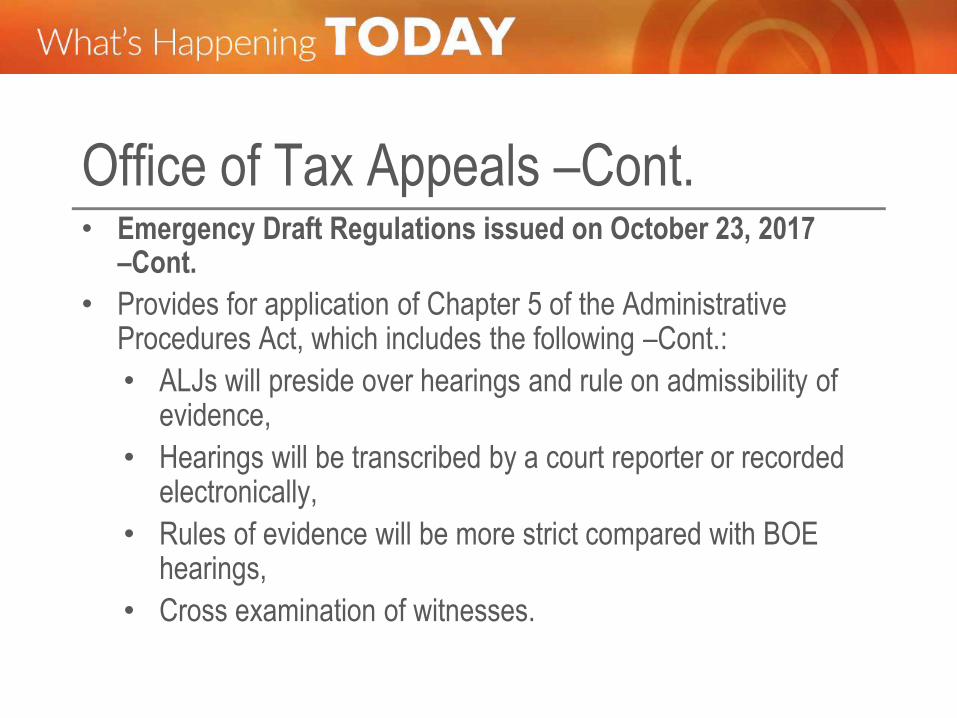

Office of Tax Appeals –Cont. • Emergency Draft Regulations issued on October 23, 2017

–Cont.

• Provides for application of Chapter 5 of the Administrative Procedures Act, which includes the following –Cont.:

• ALJs will preside over hearings and rule on admissibility of evidence,

• Hearings will be transcribed by a court reporter or recorded electronically,

• Rules of evidence will be more strict compared with BOE hearings,

• Cross examination of witnesses.

Office of Tax Appeals: Issues • Pending cases will be transferred by the BOE to OTA.

Taxpayers will not need to refile briefs and evidence.

• What is the process for making formal BOE opinions non-precedential?

• Do all or just a portion of the Administrative Procedures Act apply to OTA hearings?

• AB 102 and AB 131 provide that hearings will be conducted in accordance with the APA.

• However, OTA’s draft emergency regulations provide that only a portion of the APA’s provisions apply to OTA hearings and only to the extent not in conflict with the regulations.

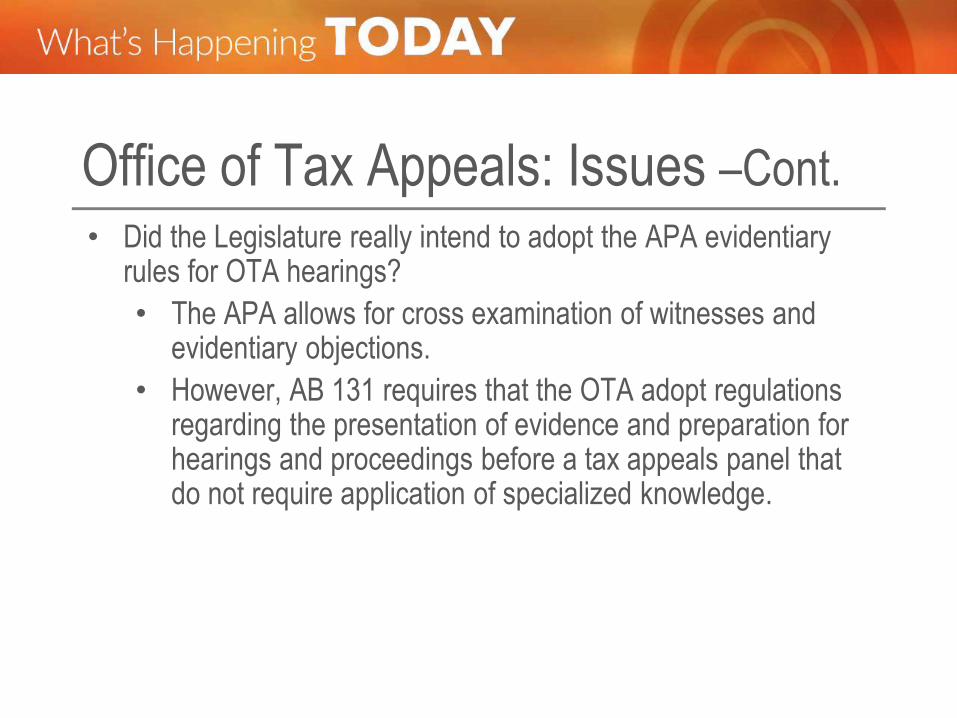

Office of Tax Appeals: Issues –Cont.

• Did the Legislature really intend to adopt the APA evidentiary rules for OTA hearings?

• The APA allows for cross examination of witnesses and evidentiary objections.

• However, AB 131 requires that the OTA adopt regulations regarding the presentation of evidence and preparation for hearings and proceedings before a tax appeals panel that do not require application of specialized knowledge.

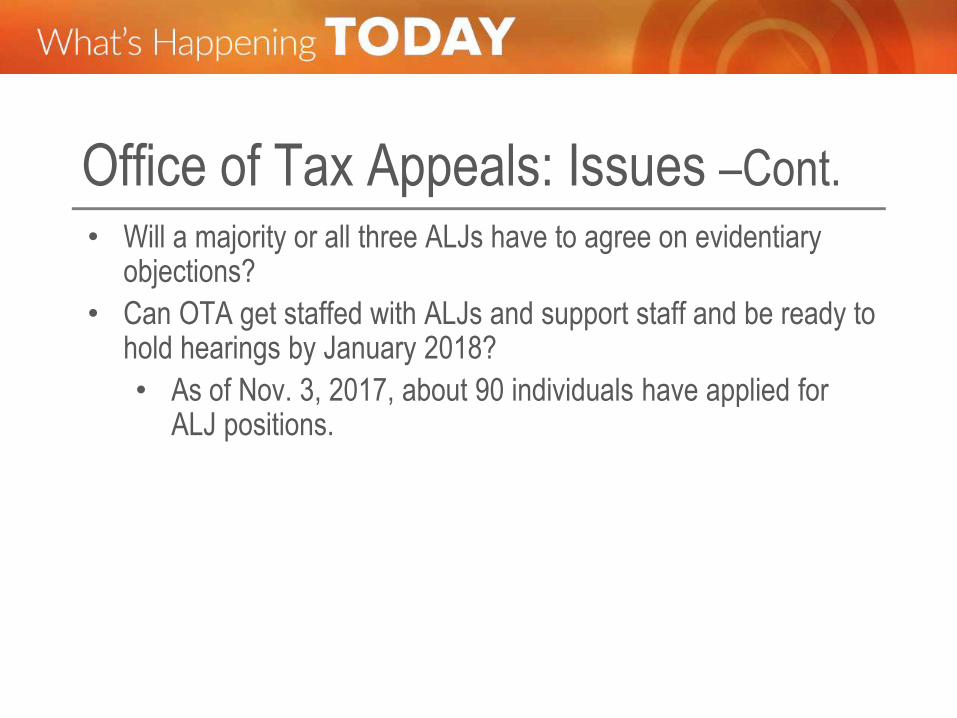

Office of Tax Appeals: Issues –Cont.

• Will a majority or all three ALJs have to agree on evidentiary objections?

• Can OTA get staffed with ALJs and support staff and be ready to hold hearings by January 2018?

• As of Nov. 3, 2017, about 90 individuals have applied for ALJ positions.

Today in Pennsylvania

David J. Shipley, Esq.

McCarter & English, LLP

Newark, New Jersey

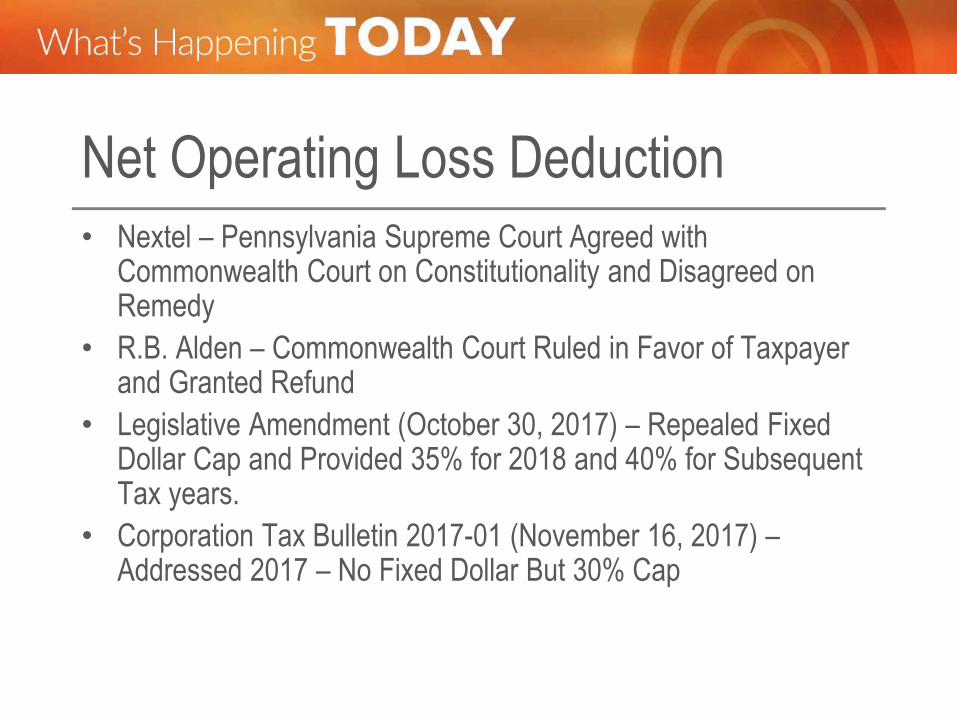

Net Operating Loss Deduction

• Nextel – Pennsylvania Supreme Court Agreed with Commonwealth Court on Constitutionality and Disagreed on Remedy

• R.B. Alden – Commonwealth Court Ruled in Favor of Taxpayer and Granted Refund

• Legislative Amendment (October 30, 2017) – Repealed Fixed Dollar Cap and Provided 35% for 2018 and 40% for Subsequent Tax years.

• Corporation Tax Bulletin 2017-01 (November 16, 2017) – Addressed 2017 – No Fixed Dollar But 30% Cap

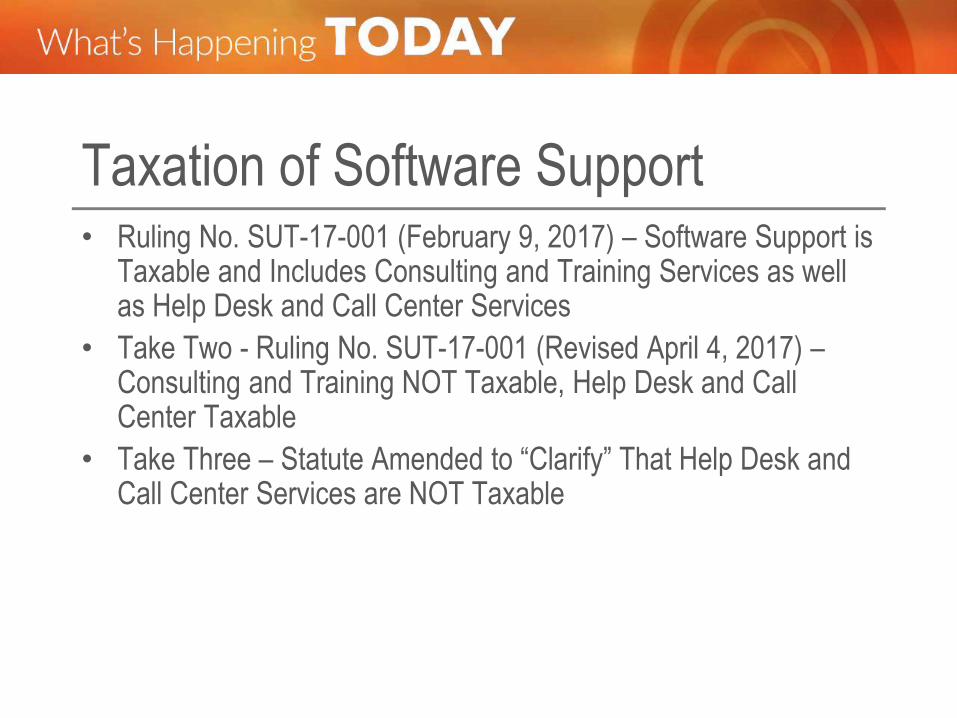

Taxation of Software Support • Ruling No. SUT-17-001 (February 9, 2017) – Software Support is

Taxable and Includes Consulting and Training Services as well as Help Desk and Call Center Services

• Take Two - Ruling No. SUT-17-001 (Revised April 4, 2017) – Consulting and Training NOT Taxable, Help Desk and Call Center Taxable

• Take Three – Statute Amended to “Clarify” That Help Desk and Call Center Services are NOT Taxable

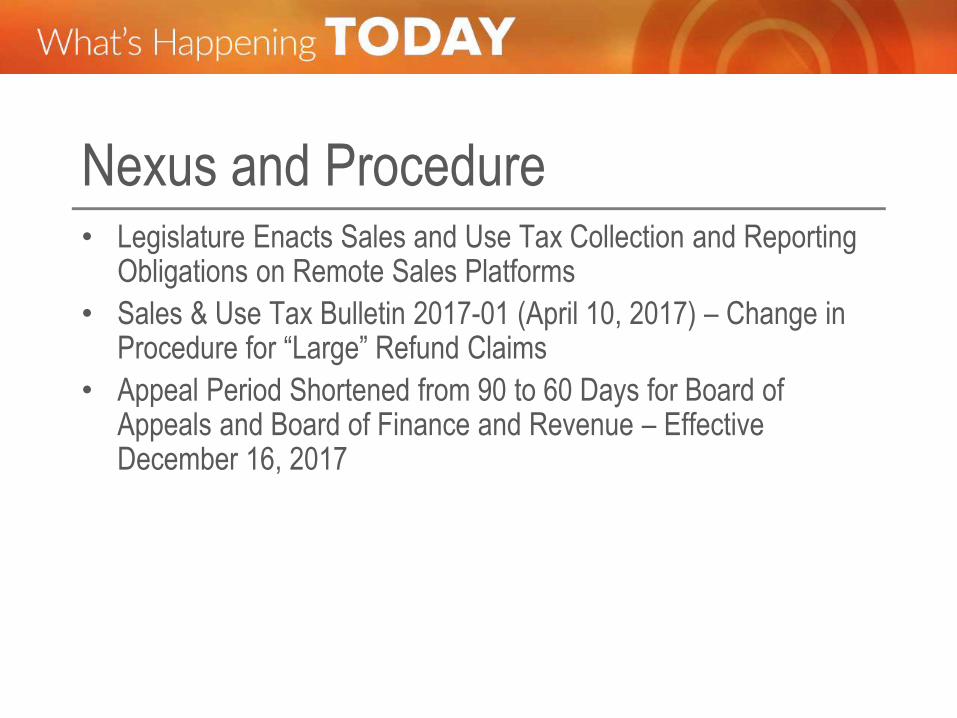

Nexus and Procedure • Legislature Enacts Sales and Use Tax Collection and Reporting

Obligations on Remote Sales Platforms

• Sales & Use Tax Bulletin 2017-01 (April 10, 2017) – Change in Procedure for “Large” Refund Claims

• Appeal Period Shortened from 90 to 60 Days for Board of Appeals and Board of Finance and Revenue – Effective December 16, 2017

Other Sales Tax Issues

• Taxation of Information Retrieval Products – Ruling No. SUT-17-002 (May 17, 2017)

• Going Nuts - Green Acres Contracting

• Beer Kegs Exempt as Wrapping Supplies

Kentucky Tax Developments- 2017 Year In Review

Mr. Mark F. Sommer

Member

Frost Brown Todd LLC

Louisville, Kentucky

Legislative Developments • HB 50 provides sunsets to all Administrative Regulations,

requiring them to expire seven years after its last effective date,

unless Executive Branch agencies (e.g., KDOR) demonstrate to

the General Assembly sufficient reasons for not letting a

regulation expire.

• HB 245 amends KRS 131.130 to give KDOR the ability to

publish more guidance on various complex tax issues without

going through a formal process for the promulgation of an

administrative regulation (e.g., similar to the Revenue Circular

Program, long since terminated.)

Administrative Developments • Just In…Issued on Friday, December 1, 2017:

• Kentucky Revenue Procedure (KY-RP-17-01)

• Details process and procedures concerning information requests

and rulings

Judicial Developments Circuit Court Finds Consolidated Filing Inappropriate

• In World Acceptance Corporation, et al. v. Commonwealth of

Kentucky, Finance & Administration Cabinet, Department of

Revenue1, an out-of-state corporation and its wholly owned

Kentucky subsidiary filed amended the separate returns initially

filed by the companies to instead utilize a consolidated filing

method, which generated refund claims. Notably, the Taxpayers

relied upon a letter ruling issued by the Department advising World

Acceptance Corporation (“WAC”) to file a consolidated return.

However, this ruling was issued on an anonymous basis.

1File No. K13-R-18, Order No. K-24682 (KBTA August 29, 2014), appealed to Franklin Circuit Court, Civil Action No.

2014-CI-1193 (August 14, 2015), vacated and reversed (November 10, 2015), appealed to Kentucky Court of

Appeals, Case No. 2015-CA-001852 (pending).

Judicial Developments –Cont. Circuit Court Finds Consolidated Filing Inappropriate –Cont.

• The taxpayers appealed the Department’s denial of their refund

claims to the KBTA, which ruled in favor of the Department. On

appeal, the Department claimed the facts in the letter request were

materially different from reality and that the taxpayer failed to

disclose that management services were performed outside

Kentucky. Thus, the Department argued that WAC was not an

“includible corporation” and consolidated filing was not appropriate.

(…)

Judicial Developments –Cont. Circuit Court Finds Consolidated Filing Inappropriate –Cont.

• …The Court agreed, and held that the Department was not bound

by its letter ruling. Further, the Court held that KRS 141.200(9)(e)

sets the definition of “includible corporation.” WAC did not meet the

definition because WAC fell within the exceptions in KRS

141.200(9)(e)(7) or (8) because its KY property, payroll and sales

factors were either zero or de minimis.

Judicial Developments –Cont. Another Win for Tax Transparency: The Kentucky Court of

Appeals Requires the Department to Provide Case Pleadings Put

Into the Public Records to the Requesting Party Under the Open

Records Act

• In Dep’t of Revenue v. Sommer6, an Open Records Act case, Tax

Attorney Mark Sommer and Tax Analysts Publishers sought

redacted copies of final rulings from the Protest stage that had been

issued by the Department pursuant to KRS 131.110. Specifically at

issue were final rulings issued but not appealed to the Kentucky

Board of Tax Appeals (now the Kentucky Claims Commission).

62015-CA-001128 (Ky. App. Jan. 13, 2017), discretionary review granted, 2017-SC-00041 (Ky. Aug. 16,

2017).

Judicial Developments –Cont. Another Win for Tax Transparency: The Kentucky Court of

Appeals Requires the Department to Provide Case Pleadings Put

Into the Public Records to the Requesting Party Under the Open

Records Act –Cont.

• The Department’s position is that these unappealed final rulings

(i.e., not already in public record) constituted confidential

information that it is forbidden from disclosing by KRS

131.190(1)(a). See also KRS 131.081(15); 131.990(2); 61.878(1)(k)

and (1); Maysville Transit Co. v. Ort, 177 S.W.2d 369 (1943). (…)

Judicial Developments –Cont. Another Win for Tax Transparency: The Kentucky Court of

Appeals Requires the Department to Provide Case Pleadings Put

Into the Public Records to the Requesting Party Under the Open

Records Act –Cont.

• …Sommer and Tax Analysts believe that the Department is

required to provide properly redacted final rulings, and that proper

redaction preserves taxpayer rights. In a published (i.e.,

binding/precedential) decision, the Court of Appeals ruled that these

final rulings should nevertheless be divulged by KDOR after suitable

redactions are made. On August 16, 2017, the Kentucky Supreme

Court granted discretionary review in this matter

Additional Resources KBTA Holds that Fees for Waiver Provisions Are Not Subject to

Sales Tax

• In Rent-A-Center East v. Dep’t of Revenue7, the KBTA held that

waivers are not tangible personal property and thus fees paid to

obtain waivers are not subject to sales tax.

• As part of the rental agreement utilized by the taxpayer, the

customer has the option to purchase an optional damage waiver

designed to cover much of the consumer’s potential liability for

losses under the rental agreement. If the consumer desires to

purchase the waiver, an additional separately stated waiver fee is

paid in additional to the rental payment.

7File No. K14-R-17, Order No. K-25136 (KBTA Sept. 6, 2016).

Additional Resources –Cont. KBTA Holds that Fees for Waiver Provisions Are Not Subject to

Sales Tax –Cont.

• The Department determined these waivers were taxable, despite

not taxing the waivers in two previous audits of RAC. RAC argued

that the waivers were intangible property and thus the fees were not

subject to sales tax. The Kentucky Claims Commission issued an

order on September 6, 2016 holding the waiver fees were not

subject to sales tax because the waiver is an intangible.

• The Department appealed this matter to the Franklin Circuit Court,

which affirmed the Claims Commission decision on September 11,

2017. The Department has appealed this decision to the Court of

Appeals, where it is currently pending in Case No. 2017-CA-01653.

Additional Resources –Cont. Kentucky Court of Appeals Finds Turn Key, Built to Suit Pharmacy

Property was not Overvalued

• In Wilgreens, LLC and Walgreen Co. v. David O’Neill, Fayette

County PVA8, property with a Walgreen’s on the premises was

valued using the income approach. The property was subject to a

triple net lease. Additionally, the property had been previously sold

and had been recently listed for sale prior to the valuation. The

taxpayer presented expert witnesses to argue that the income

approach was not a valid method of valuation in the secured lease

setting.

8Order No. K-24624 (KBTA Mar. 26, 2014), Civ. Action No. 14-CI-1566 (Fayette Cir. Ct., Feb. 18, 2015), on

appeal Case No. 2015-CA-000407 (Ky. App., Sept. 23, 2016).

Additional Resources –Cont. Kentucky Court of Appeals Finds Turn Key, Built to Suit Pharmacy

Property was not Overvalued –Cont.

• When the case reached the Court of Appeals, the Court noted that

Walgreens attempted to show the property was overvalued by

relying on properties very different from the property at issue. The

Court noted that the failure to produce competent, substantive

evidence “in and of itself justified the Board’s conclusion.” The Court

further noted that even setting aside the proof issue, it could find no

outright fault with the PVA’s application of the assessment statutes,

as the PVA is permitted to use the income generation approach to

estimate fair cash value. (…)

Additional Resources –Cont. Kentucky Court of Appeals Finds Turn Key, Built to Suit Pharmacy

Property was not Overvalued –Cont.

• …Additionally, consideration of the leasehold was acceptable. A

motion for discretionary review was ultimately denied; however, the

Supreme Court de-published the Court of Appeals’ Opinion.

Additional Resources –Cont. Circuit Court Rules on 911 Taxes

• In Virgin Mobile USA, L.P. v. Commonwealth of Kentucky ex rel.

Commercial Mobile Radio Service Emergency Telecommunications

Board9, Virgin Mobile USA, LP (“Virgin Mobile”) challenged the

imposition of the CMRS service charge imposed under KRS

65.7629 prior to July 2006. Virgin Mobile remitted the charge, but

instead of collecting the tax from its customers, it remitted the tax

from its general revenues. Virgin Mobile ultimately stopped paying

the tax and then requested refunds on the belief the service charge

did not apply to prepaid wireless services

9448 S.W.3d 241 (Ky. 2014), remanded and final judgment entered, Jeff. Cir. Ct. No. 08-CI-010857 (July 29,

2015), appealed to Kentucky Court of Appeals, Case No. 2015-CA-001312 (July 14, 2017).

Additional Resources –Cont. Circuit Court Rules on 911 Taxes –Cont.

• At the Court of Appeals, the Court determined that Virgin Mobile

was a CMRS provider subject to the tax. The Kentucky Supreme

Court granted cross-motions for discretionary review. The Supreme

Court found that Virgin Mobile was not required to collect from its

prepaid customers prior to July 2016 because it was not a “billing

provider.” However, because Virgin Mobile “repaid itself” by set-off,

refunds were not appropriate. (…)

Additional Resources –Cont. Circuit Court Rules on 911 Taxes –Cont.

• …On remand, Virgin Mobile argued that it was entitled to a refund,

but the Jefferson Circuit Court denied the claim based on the law of

the case doctrine. Virgin Mobile satisfied the judgment and

appealed the issue of whether it was entitled to a refund of the pre-

July 2006 CMRS charges it mistakenly paid. The Court of Appeals

affirmed the decision of the Jefferson Circuit Court, and this

decision is now final.

Additional Resources –Cont. KBTA Determines Netflix Streaming Services are not Taxable as

Video Programming or Cable Services

• In Netflix Inc. v. Dep’t10

, Netflix requested refunds of gross receipts

taxes, excise taxes, and utility gross receipts license taxes imposed

on taxable multichannel video programming services or cable

services, claiming its streaming services do not meet the definition

of multichannel video programming services in KRS 136.602(8).

The Department argued that Netflix’s streaming services are

generally considered comparable to programming provided by a

television broadcast system. (…)

10File Nos. K13-R-31; K13-R-32; Order No. K-24900 (KBTA Sept. 23, 2015), appealed Civ. Action No. 15-CI-

01117 (Franklin Cir. Ct. Aug. 21, 2016), on appeal, Case No. 2016-CA-001405 (Ky. App. Sept. 20, 2016)

(pending).

Additional Resources –Cont. KBTA Determines Netflix Streaming Services are not Taxable as

Video Programming or Cable Services –Cont.

• …Netflix argued that the non-linear nature of its programming and

the fact that programming is not live distinguishes it from broadcast

stations. Netflix also argued that “multichannel video programming”

was an FCC term of art which no other jurisdiction interpreted to

include Netflix’s services.

Additional Resources –Cont. KBTA Determines Netflix Streaming Services are not Taxable as

Video Programming or Cable Services –Cont.

• The Franklin Circuit Court affirmed the decision of the KBTA,

holding that Netflix’s streaming services are not sufficiently similar to

cable services to meet the definition of multichannel video

programming services. The services were also not generally

comparable to television broadcast programming. Thus, Netflix does

not provide taxable multichannel video programming services, and

Netflix was entitled to refunds. The Department appealed this

decision, but the appeal was ultimately dismissed by agreement and

the case became final in March 2017

Additional Resources –Cont. Taxable Leasehold Found in Residential Communities for the

Elderly

• In Grand Lodge F & A.M. v. Kenton County PVA11

, the KBTA held

mere possession of a residential unit in a retirement community was

not a taxable real property leasehold interest. The PVA attempted to

tax the interest because the underlying property was exempt by

Section 170 of the Kentucky Constitution. Section 170 exempts real

property owned and occupied by institutions of purely public charity.

(…)

11File No. K12-S-69, Order No. K-24714 (November 19, 2014), appealed to Kenton Circuit Court, Civil Action

No. 2014-CI-02367 (October 9, 2015), appealed to Kentucky Court of Appeals, Case No. 2015-CA-001617

(February 10, 2017), motion for discretionary review filed, Kentucky Supreme Court, No. 2017-SC-122-D

(March 10, 2017) (Pending).

Additional Resources –Cont. Taxable Leasehold Found in Residential Communities for the

Elderly –Cont.

• …The owner of the underlying real property had been a recognized

charity in Kentucky since at least 1970. However, a non-profit

affiliate built and owned Springhill Retirement Community on the

underlying property. The PVA recognized that the real property

owner, Grand Lodge of Kentucky, Free & Accepted Masons, and

the affiliate were both purely public charities. However, the PVA

assessed the leasehold interests in the residential units to the

residents as non-exempt possessors.

Additional Resources –Cont. Taxable Leasehold Found in Residential Communities for the

Elderly –Cont.

• The Kentucky Court of Appeals held that possession of a residential

unit in a retirement community constitutes a taxable leasehold

interest. The Court adopted the Kenton Circuit Court’s legal

analysis, holding the residents are responsible for property tax on

the value of their “interests,” which the Court categorized as a

leasehold interest. However, the Court found the PVA’s valuation of

the residents’ property erroneous, and thus the assessments were

vacated. (…)

Additional Resources –Cont. Taxable Leasehold Found in Residential Communities for the

Elderly –Cont.

• …The Court instructed the PVA to follow the “well-settled” Kentucky

law for determining the fair market value of a leasehold interest for

tax purposes (the difference between the fair market value of the

real property with the leasehold and the fair market value of the real

property without the leasehold). The charities and residents have

filed a motion for discretionary review with the Kentucky Supreme

Court.

Additional Resources –Cont. Circuit Court Finds Fuel Tax Pre-Purchase Refund Requirement

Unconstitutional

• In Revelation Energy LLC v. Department of Revenue12

, the

Department denied refund claims for special fuel taxes paid prior to

a refund permit being issued by the Department, which claims it

argued were in violation of statute. Revelation argued that the

refund permit requirement violated the due process and equal

protection clauses of the United States and Kentucky constitutions.

12Civil Action No. 14-CL-00799 (Pike Cir. Ct. May 19, 2015), on appeal 2015-CA-000930

Additional Resources –Cont. Circuit Court Finds Fuel Tax Pre-Purchase Refund Requirement

Unconstitutional –Cont.

• The Pike Circuit Court determined that the state requirement to

obtain a refund permit for motor fuel tax before purchasing any fuel

in order to get a refund violates the U.S. Constitution’s due process

clause because it eliminates post-deprivation remedies for

taxpayers that overpay the tax before getting a refund permit. The

Court noted that the collection of a state tax is a deprivation of

property, and as a result the Due Process clause requires states to

provide sufficient procedural safeguards against erroneous or

unlawful exactions of tax. (…)

Additional Resources –Cont. Circuit Court Finds Fuel Tax Pre-Purchase Refund Requirement

Unconstitutional –Cont.

• …In order to satisfy this requirement, the government must provide

the taxpayer with either a pre-deprivation remedy which permits the

taxpayer a meaningful opportunity to withhold the tax and to dispute

the amount owed, a post-deprivation remedy which allows the

taxpayer to challenge the amount paid and obtain a refund if it is

determined that the tax was wrongfully collected, or a combination

of both that allows the taxpayer to challenge their tax liability. (…)

Additional Resources –Cont. Circuit Court Finds Fuel Tax Pre-Purchase Refund Requirement

Unconstitutional –Cont.

• …The Court found that the refund permit requirement under KRS

134.580(8) and KRS 138.345 effectively eliminates any meaningful

form of post-deprivation remedy under KRS 134.580 for taxpayers

like Revelation Energy who determine that they have overpaid the

motor fuels tax before obtaining a permit.

• The Department has appealed the Pike Circuit Court’s Opinion and

Order to the Kentucky Court of Appeals. The case has been

submitted for a decision without oral argument.

Additional Resources –Cont. No Excessive Entanglement Found by Providing Incentives to

Religious Theme Park

• In Ark Encounter, LLC v. Parkinson13

, the taxpayer was building a

religious theme park. The Kentucky Tourism, Arts and Heritage

Cabinet denied the Park sales tax incentives under the Kentucky

Tourism Development Act (“KDTA”) on the basis the program would

violate the constitutional prohibition against religious establishment.

13Civil Action No. 15-13-GFVT (E.D. Ky. Jan. 25, 2016).

Additional Resources –Cont. No Excessive Entanglement Found by Providing Incentives to

Religious Theme Park – Cont.

• The U.S. District Court for the Eastern District of Kentucky held a

religious-themed tourist attraction, even one advancing religion,

meeting the neutral criteria for tax incentives offered by the

Commonwealth of Kentucky cannot be denied those incentives,

based upon the Establishment Clause of the U.S. and Kentucky

Constitutions. The Court focused on the KTDA’s secular legislative

purpose of relieving unemployment by preserving and creating jobs

through tourism projects and also creating sources of tax revenue

through the projects and their attraction of out-of-state tourists. (…)

Additional Resources –Cont. No Excessive Entanglement Found by Providing Incentives to

Religious Theme Park – Cont.

• …Specifically, the Court noted, nothing in the KDTA indicates its

purpose is to aid or give preference to a particular religion.

Furthermore, the Court held that the requested exclusion of the park

would cause entanglement, while participation would not. All

programs meeting the neutral requirements of the incentive program

should be approved. The Cabinet’s exclusion also violated the

taxpayer’s First Amendment rights. This case is now final.

Additional Resources –Cont. • HB 284 allows the County PVA to: (i) extend the filing date for filing