voluntary disclosure patrick harteveld – mazars claudia c. de regt – fineco bank 1

TRANSCRIPT

1

Voluntary Disclosure

Patrick Harteveld – MazarsClaudia C. de Regt – Fineco Bank

2

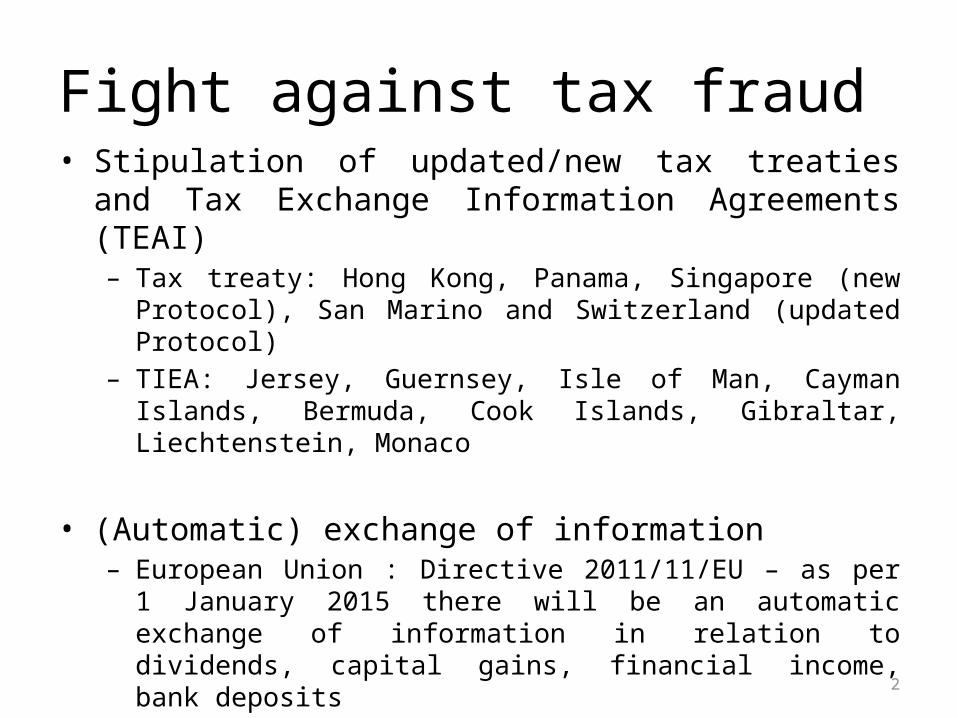

Fight against tax fraud• Stipulation of updated/new tax treaties and Tax Exchange

Information Agreements (TEAI)– Tax treaty: Hong Kong, Panama, Singapore (new Protocol), San Marino

and Switzerland (updated Protocol)– TIEA: Jersey, Guernsey, Isle of Man, Cayman Islands, Bermuda, Cook

Islands, Gibraltar, Liechtenstein, Monaco

• (Automatic) exchange of information– European Union : Directive 2011/11/EU – as per 1 January 2015 there

will be an automatic exchange of information in relation to dividends, capital gains, financial income, bank deposits

– OECD: Common Reporting Standard adopted by Global Forum on Transparency and Exchange of Information for Tax Purposes (October 2014)

3

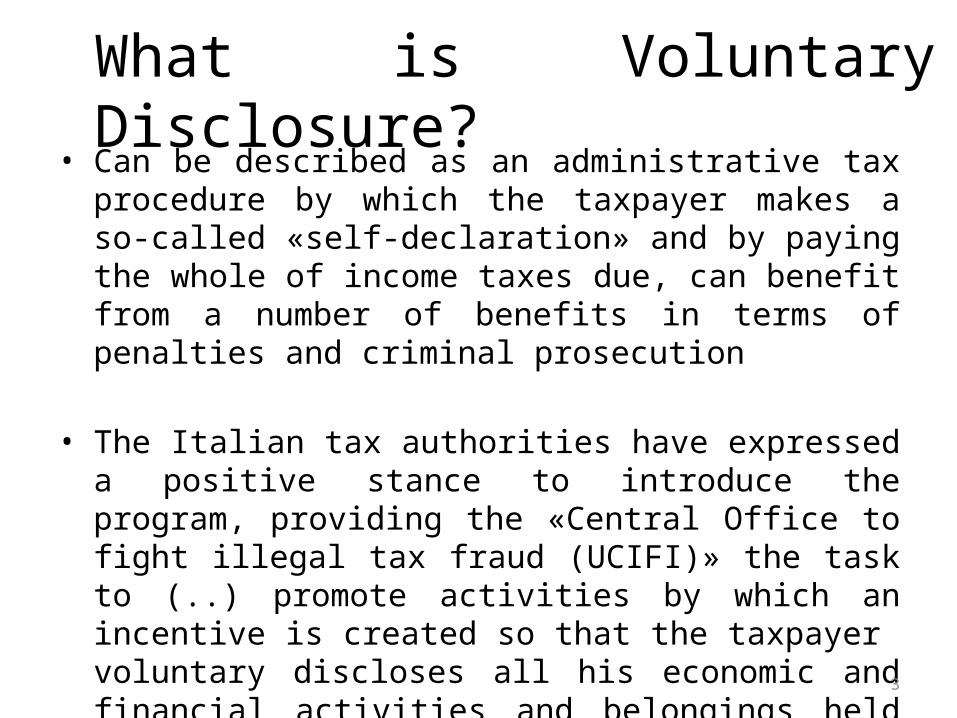

What is Voluntary Disclosure?• Can be described as an administrative tax procedure by which

the taxpayer makes a so-called «self-declaration» and by paying the whole of income taxes due, can benefit from a number of benefits in terms of penalties and criminal prosecution

• The Italian tax authorities have expressed a positive stance to introduce the program, providing the «Central Office to fight illegal tax fraud (UCIFI)» the task to (..) promote activities by which an incentive is created so that the taxpayer voluntary discloses all his economic and financial activities and belongings held abroad (cfr. par. 3.2. of Circ. 25/E/2013).

4

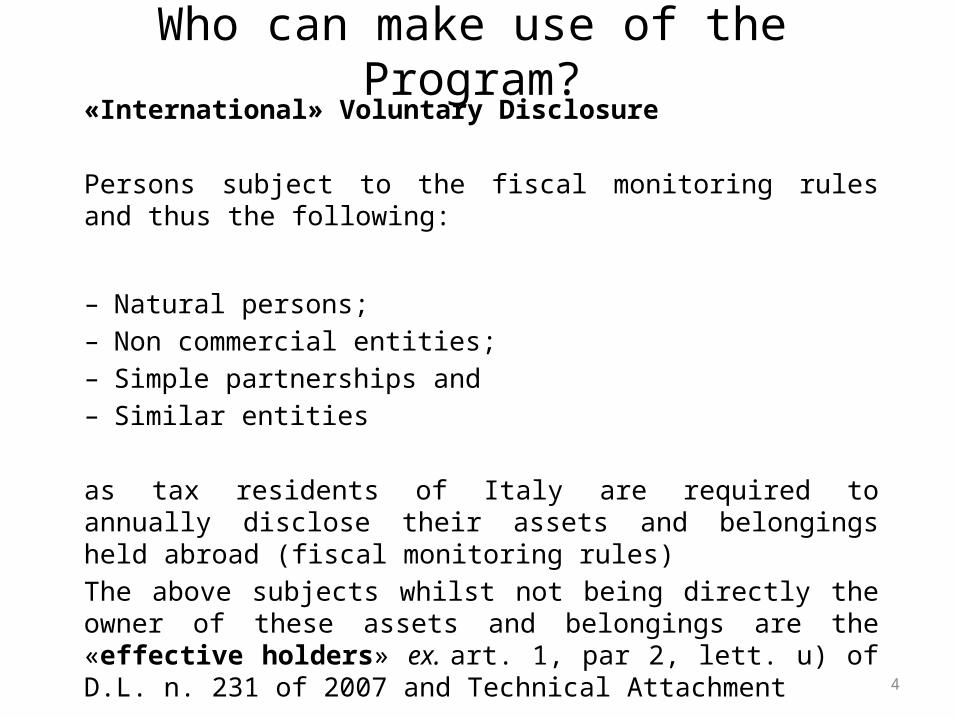

Who can make use of the Program?«International» Voluntary Disclosure

Persons subject to the fiscal monitoring rules and thus the following:

– Natural persons;– Non commercial entities;– Simple partnerships and– Similar entities

as tax residents of Italy are required to annually disclose their assets and belongings held abroad (fiscal monitoring rules)The above subjects whilst not being directly the owner of these assets and belongings are the «effective holders» ex. art. 1, par 2, lett. u) of D.L. n. 231 of 2007 and Technical Attachment

5

«International» Voluntary DisclosureTax residence of natural persons

– Sufficient to be a tax resident in just one outstanding year (Circ. AdE n. 10/E of13 March 2015)

– Art. 2, par. 2 of d.p.r. 917/1986 sets forth that a natural person is considered a tax resident of Italy if such a person – for the greatest part of the tax year (> 183 days)

• Has been registered at the Population Register (Anagrafe);• Has his centre of vital interest in Italy;• Has his habitual abode in Italy

- Art. 2, par. 2bis dpr 917/1986 sets forth that a natural persons who emigrated to a blacklisted country is deemed to be a tax resident of Italy, unless proven differently

6

«International» Voluntary Disclosure all investments and financial assets established or held abroad,

also indirectly by virtue of interposed persons, in violation of the fiscal monitoring rules;

income connected to above or income which serve to establish or purchase these belongings or financial assets as well as income pursuant to the use of these belongings or financial assets (..);

additional taxes, not connected to the belongings and financial assets illegally held abroad (..)

All-in principle; using the “international” voluntary disclosure program obliges a taxpayer to use also the “domestic” voluntary disclosure, but only limited to the years covered by the international program (cfr. Circ. 13 March 2015, n. 10/E, par. 1.2)

7

«Domestic» Voluntary Disclosure Residual and refers to other «internal» violations that cannot be

dealt with through the «international» Voluntary Disclosure

Refers to «other taxpayers», not necessarily falling within the scope of the fiscal monitoring rules

Covers essentially the following taxes:

• Personal and Corporate Income taxes;• Regional / municipal income taxes;• Substitutive taxes (imposte sostitutive)• IRAP• VAT • Violation in relation to withholding taxes

8

How can one apply?

The Voluntary Disclosure program allows a taxpayer, before 30 September 2015, to regularize violations committed up to 30 September 2014

The regularization needs to be done by:

1. Filing a digital return to UCIFI by 30 September 2015 (it is possible to integrate and correct a prior filing but needs to be done within the same deadline);

2. File, within 30 days, but in any case within 30 September 2015, the consultant’s «Export Report» (relazione) attaching all relevant documentation and information

9

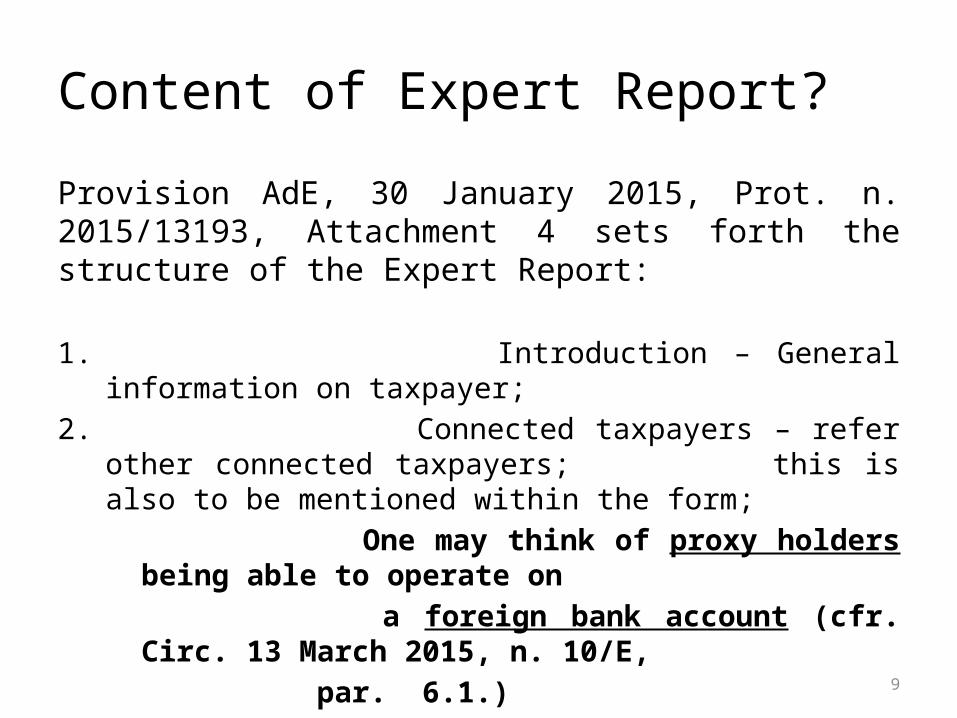

Content of Expert Report?

Provision AdE, 30 January 2015, Prot. n. 2015/13193, Attachment 4 sets forth the structure of the Expert Report:

1. Introduction – General information on taxpayer;2. Connected taxpayers – refer other connected taxpayers;

this is also to be mentioned within the form; One may think of proxy holders being able to

operate on a foreign bank account (cfr. Circ. 13 March 2015, n. 10/E, par. 6.1.)

3/4/5/6 Assets and belongings; income, etc.7 Indication on previous declarations done in relation to Tax Shield (scudo fiscale)

10

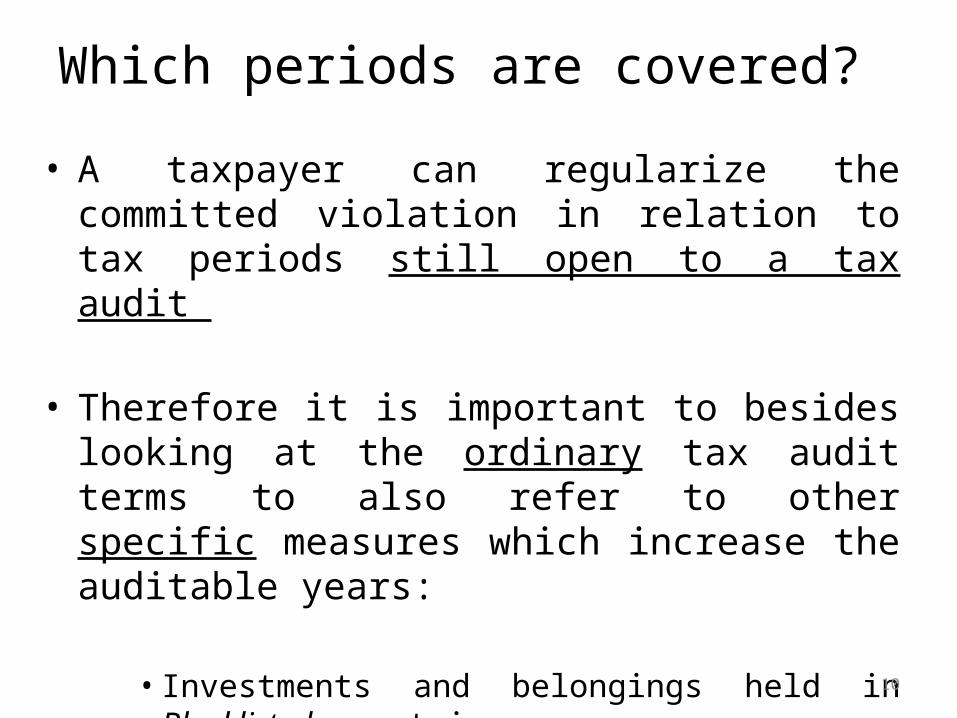

Which periods are covered?

• A taxpayer can regularize the committed violation in relation to tax periods still open to a tax audit

• Therefore it is important to besides looking at the ordinary tax audit terms to also refer to other specific measures which increase the auditable years:

• Investments and belongings held in Blacklisted countries;• Periods which fall under a criminal tax offence

11

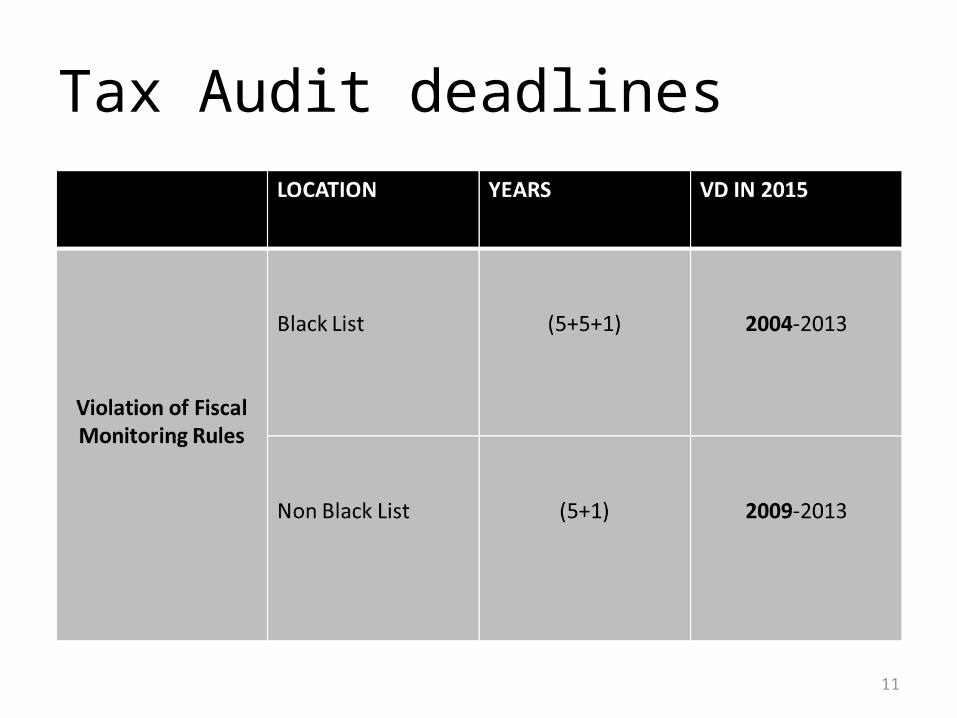

Tax Audit deadlines

12

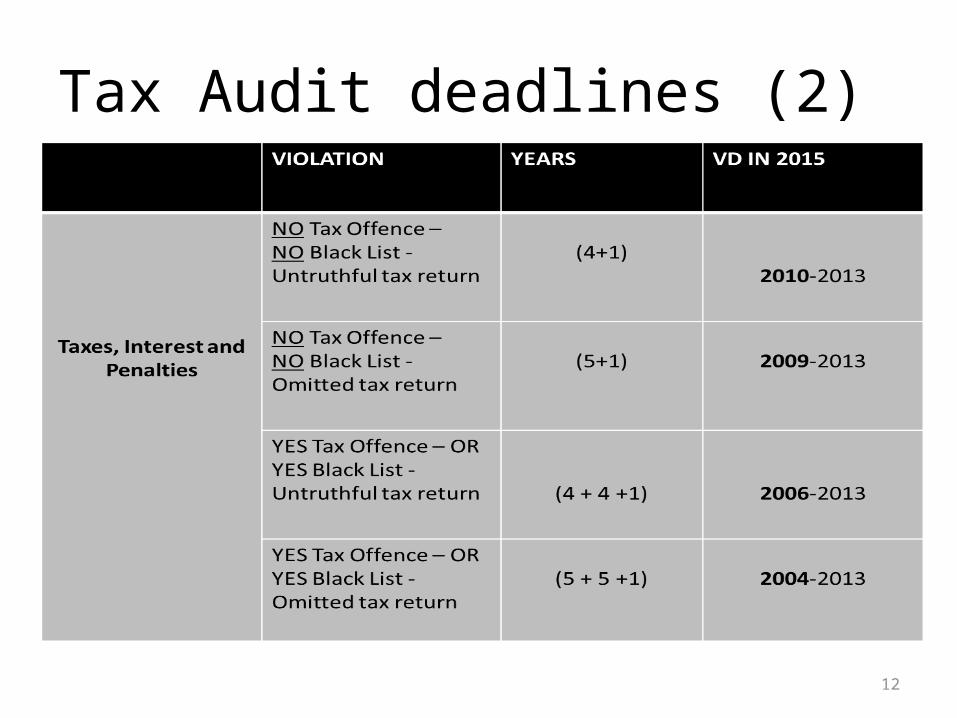

Tax Audit deadlines (2)

13

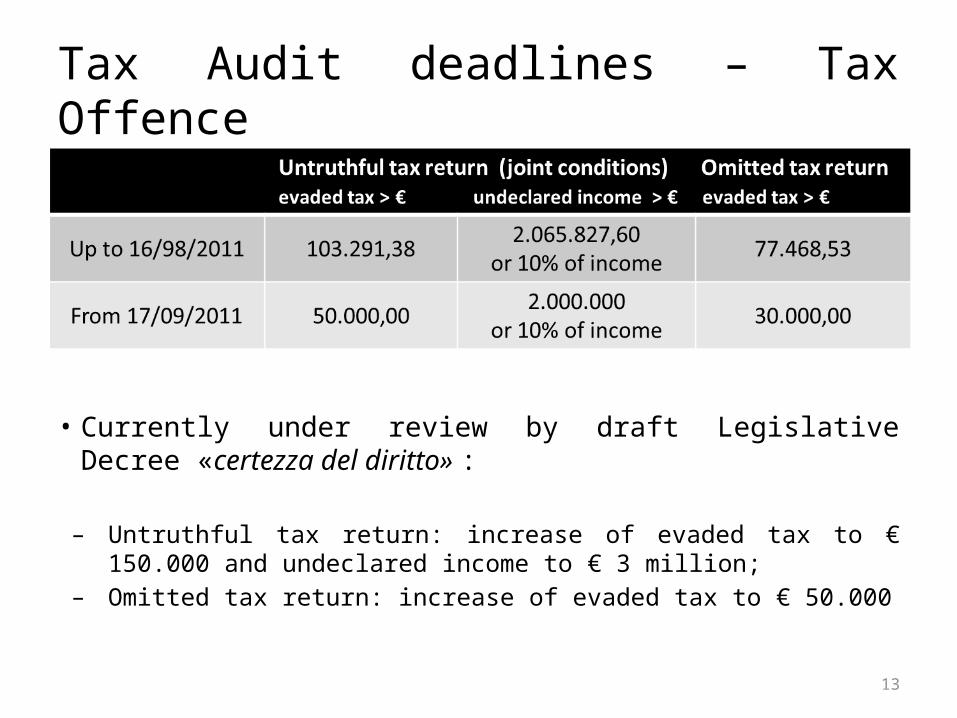

Tax Audit deadlines – Tax Offence

• Currently under review by draft Legislative Decree «certezza del diritto» :

– Untruthful tax return: increase of evaded tax to € 150.000 and undeclared income to € 3 million;

– Omitted tax return: increase of evaded tax to € 50.000

14

How Much does it cost?

The taxpayer needs to take into account:

• The total full amount of taxes payable in relation to all tax auditable years

• Payment of legal interest

• Administrative penalties due

15

Administrative Penalties – Violation of Fiscal Monitoring Rules

• This violation is punished by:

– An administrative penalty ranging from 3% to 15% of the amount of the unreported financial assets and / or belongings;

– When these financial assets and / or belongings are held in so-called blacklisted countries then penalties are ranging from 6% (5% between 2004 and 2007) to 30%

16

Administrative Penalties – Violation of Fiscal Monitoring Rules (2)

• Making use of the Voluntary Disclosure Programs means that the (minimum) penalty is reduced by 50% when the financial assets and / or belongings:a) are transferred in Italy or another country allowing an

effective exchange of information (EU, Norway, etc.);b) were or are already held in such countries;c) Whenever the taxpayer releases an authorization to its

financial intermediary to transmit all relevant documentation and / or information attaching a copy of the authorization

• In all other cases, the taxpayer can still benefit from a penalty reduction but this is limited to 25% (in relation to the minimum applied penalty).

17

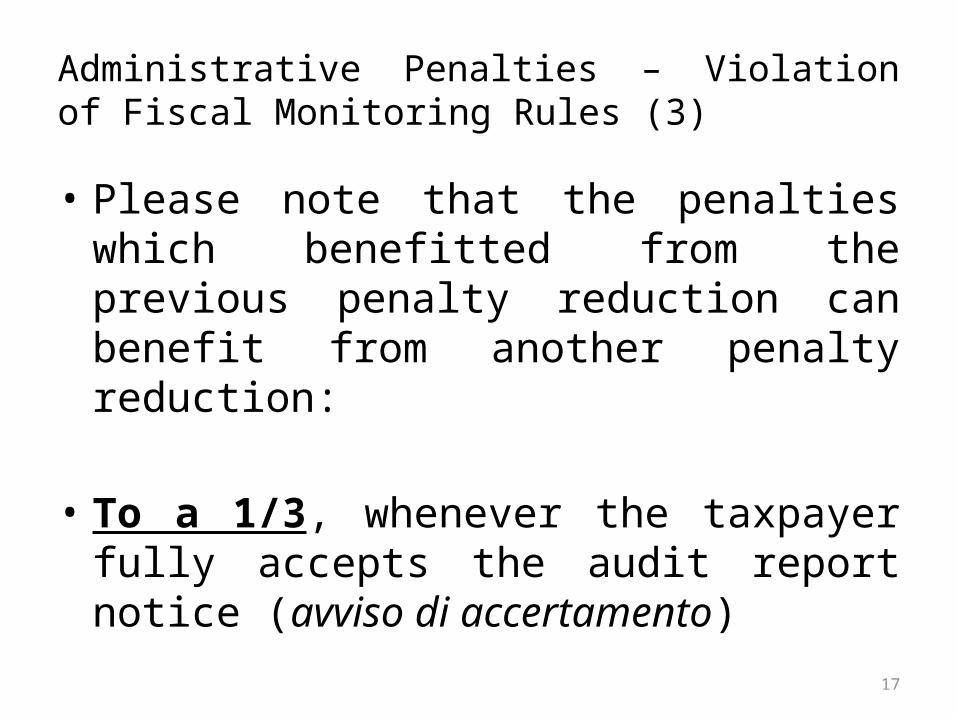

Administrative Penalties – Violation of Fiscal Monitoring Rules (3)

• Please note that the penalties which benefitted from the previous penalty reduction can benefit from another penalty reduction:

• To a 1/3, whenever the taxpayer fully accepts the audit report notice (avviso di accertamento)

18

Summary sheet of penalties due in relation to violation of fiscal monitoring rules (from 2008)

Original location of belongings and assets prior to VD

General penalty

Destination of belongings / assets after VD Penalty

reductionFurther reduction

to a 1/3

Italy or «White list» 3% - 15%Italy/EU/EEA (Iceland and Norway)

or in presence of an authorization signed by foreign intermediary

1,50% 0,50%

Italy or «White List» 3% - 15%Other countries than Italy/EU/EEA in lack of

an authorization signed by foreign intermediary

2,25% 0,75%

«Black list» with exchange of

information (e.g. Switzerland)

3% - 15%Italy/EU/EEA (Iceland and Norway)

or in presence of an authorization signed by foreign intermediary

1,50% 0,50%

«Black list» with exchange of

information (e.g. Switzerland)

3% - 15%Other countries than Italy/UE/SEE in lack of

an authorization signed by foreign intermediary 2,25% 0,75%

«Black list» without exchange of information

6%-30%Italy/UE/SEE (Iceland and Norway)

or in presence of an authorization signed by foreign intermediary

3% 1%

«Black list» exchange of information 6%-30%

Other countries than Italy/EU/EEA in lack of an authorization signed by foreign

intermediary 4,5% 1,5%

19

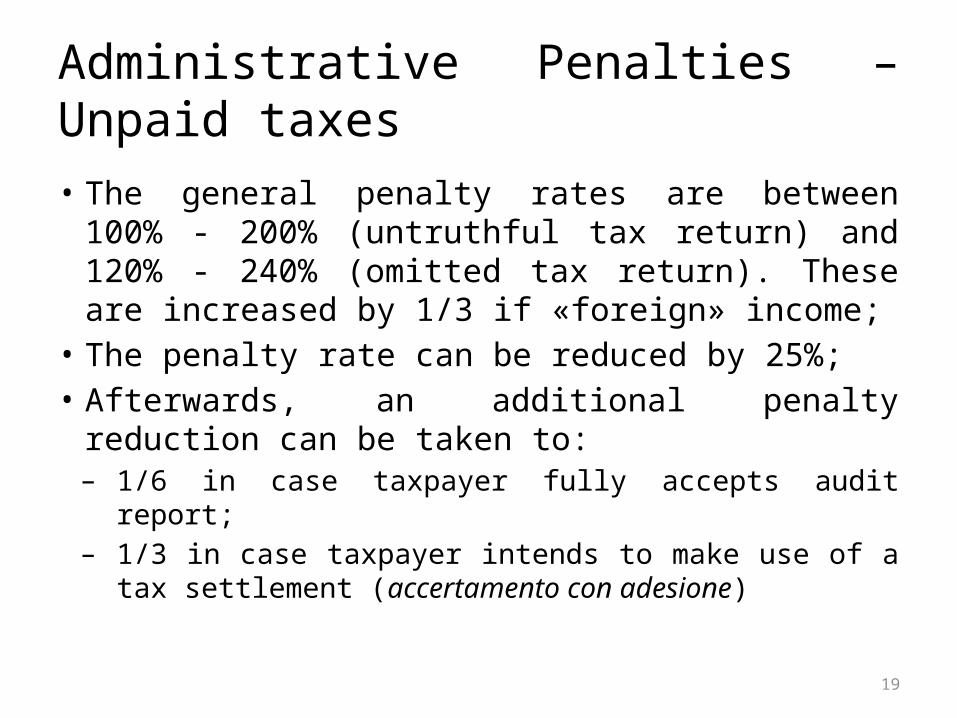

Administrative Penalties – Unpaid taxes

• The general penalty rates are between 100% - 200% (untruthful tax return) and 120% - 240% (omitted tax return). These are increased by 1/3 if «foreign» income;

• The penalty rate can be reduced by 25%;• Afterwards, an additional penalty reduction can be

taken to:– 1/6 in case taxpayer fully accepts audit report;– 1/3 in case taxpayer intends to make use of a tax

settlement (accertamento con adesione)

20

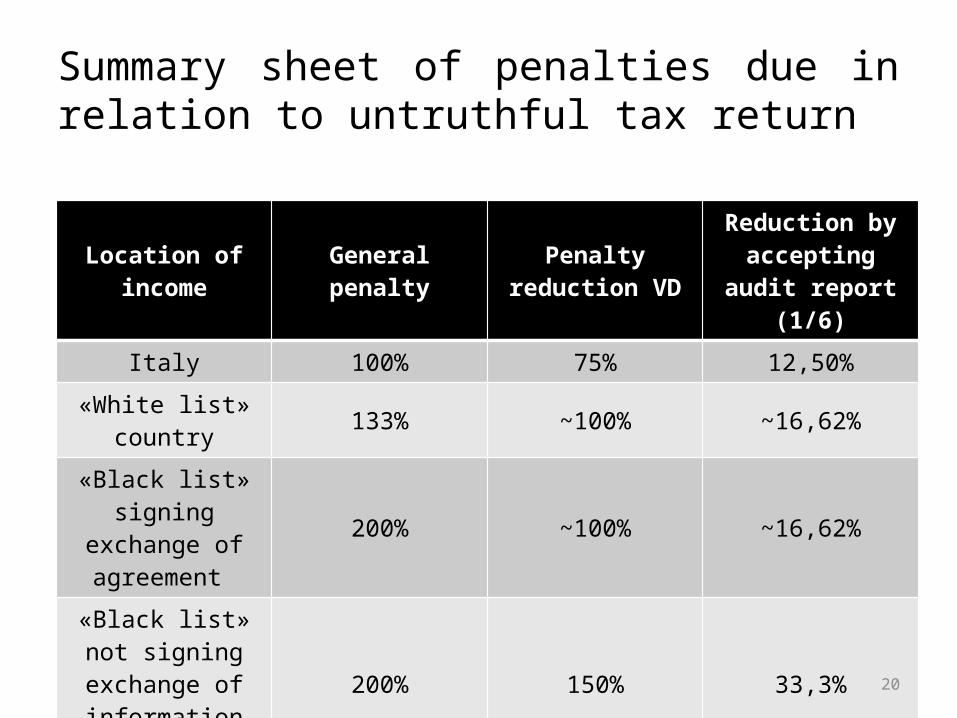

Summary sheet of penalties due in relation to untruthful tax return

Location of income General penalty Penalty reduction VD

Reduction by accepting audit

report (1/6)Italy 100% 75% 12,50%

«White list» country 133% ~100% ~16,62%

«Black list» signing exchange of agreement

200% ~100% ~16,62%

«Black list» not signing exchange of

information agreement

200% 150% 33,3%

21

Reconstruction of foreign assets and belongings• In order for a correct reconstruction it is necessary that

the consultant acquires from its client:– copies of bank statements in relation to the tax auditable

years;– contracts and other documents indicating the origin of the

«foreign» financial assets and belongings and related movements (withdrawals and / or contributions);

– Possible mandates given to fiduciaries and effective beneficiaries;

– A so-called self-declaration by which the client declares that all information and documents provided to the consultant are conform the truth

22

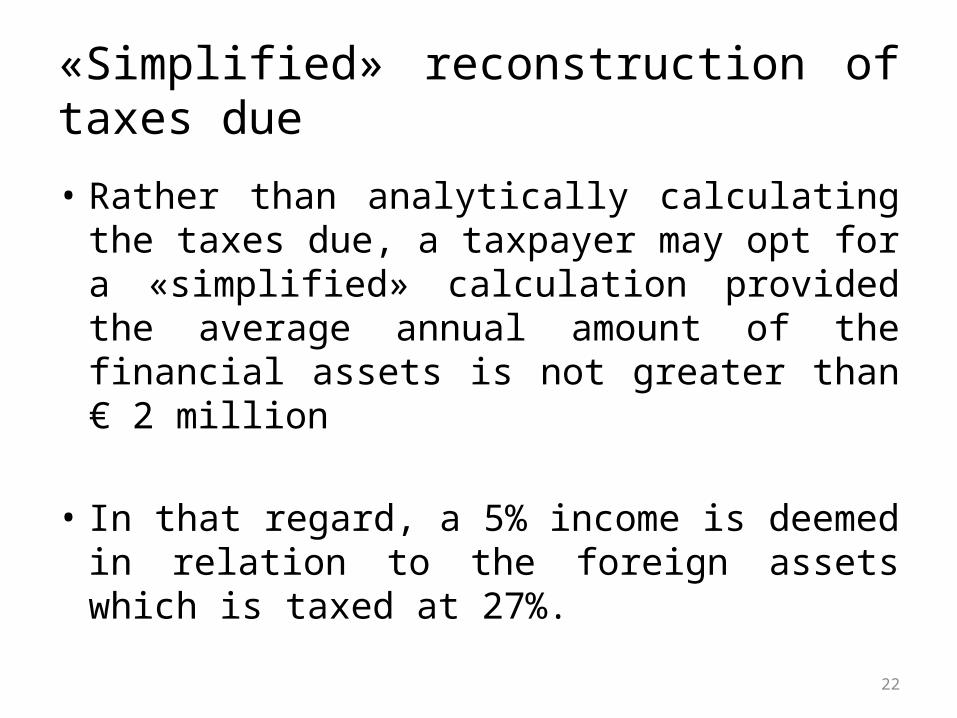

«Simplified» reconstruction of taxes due

• Rather than analytically calculating the taxes due, a taxpayer may opt for a «simplified» calculation provided the average annual amount of the financial assets is not greater than € 2 million

• In that regard, a 5% income is deemed in relation to the foreign assets which is taxed at 27%.

23

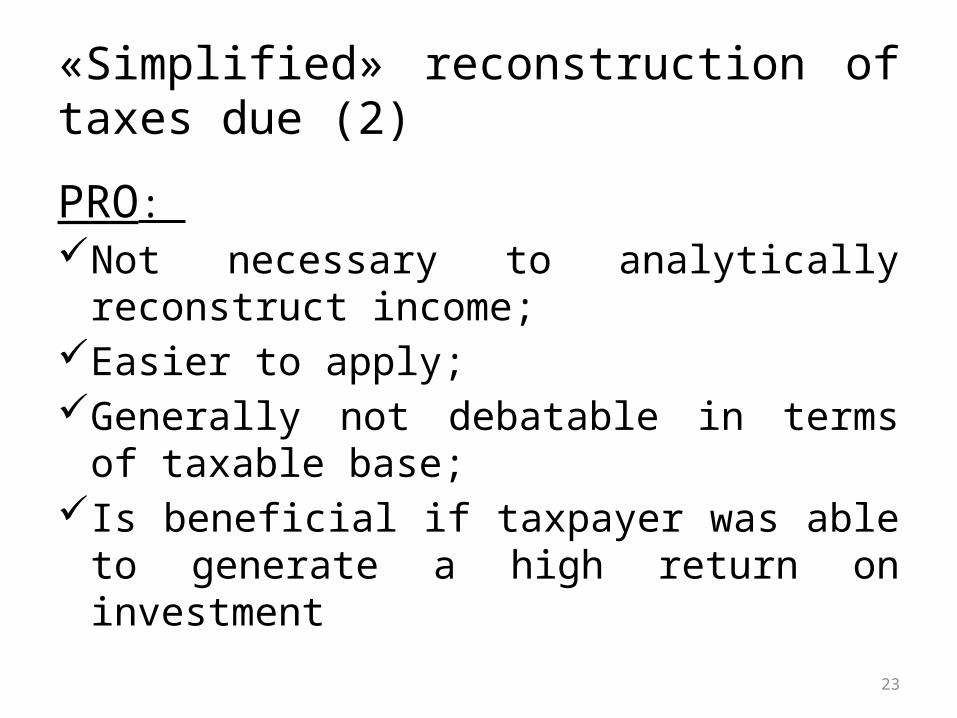

«Simplified» reconstruction of taxes due (2)

PRO: Not necessary to analytically reconstruct

income;Easier to apply;Generally not debatable in terms of taxable

base;Is beneficial if taxpayer was able to generate a

high return on investment

24

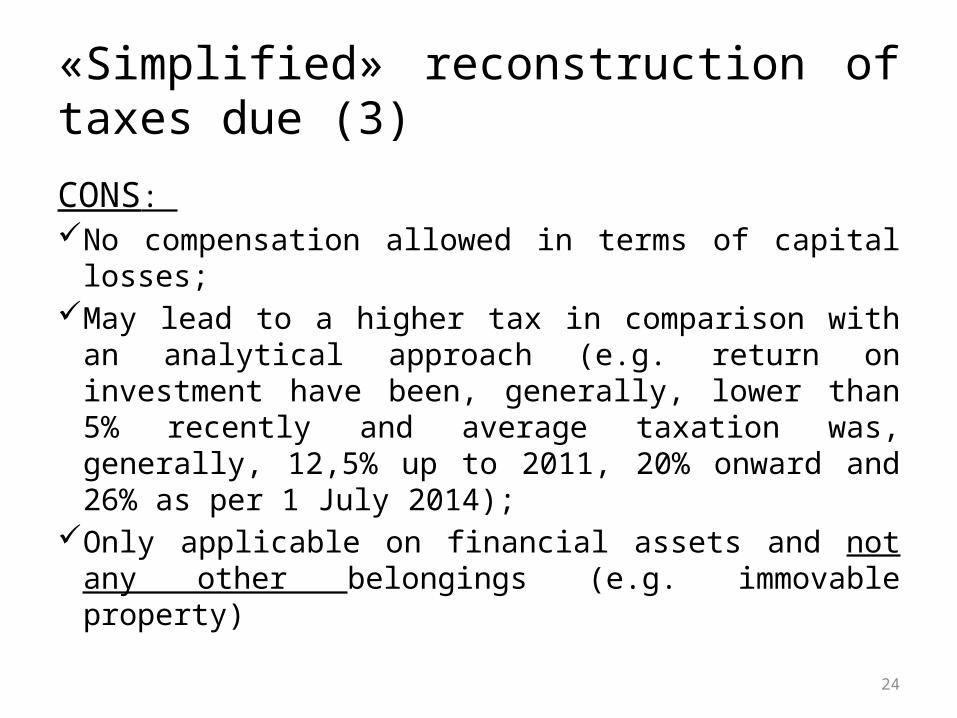

«Simplified» reconstruction of taxes due (3)

CONS: No compensation allowed in terms of capital losses;May lead to a higher tax in comparison with an

analytical approach (e.g. return on investment have been, generally, lower than 5% recently and average taxation was, generally, 12,5% up to 2011, 20% onward and 26% as per 1 July 2014);

Only applicable on financial assets and not any other belongings (e.g. immovable property)

25

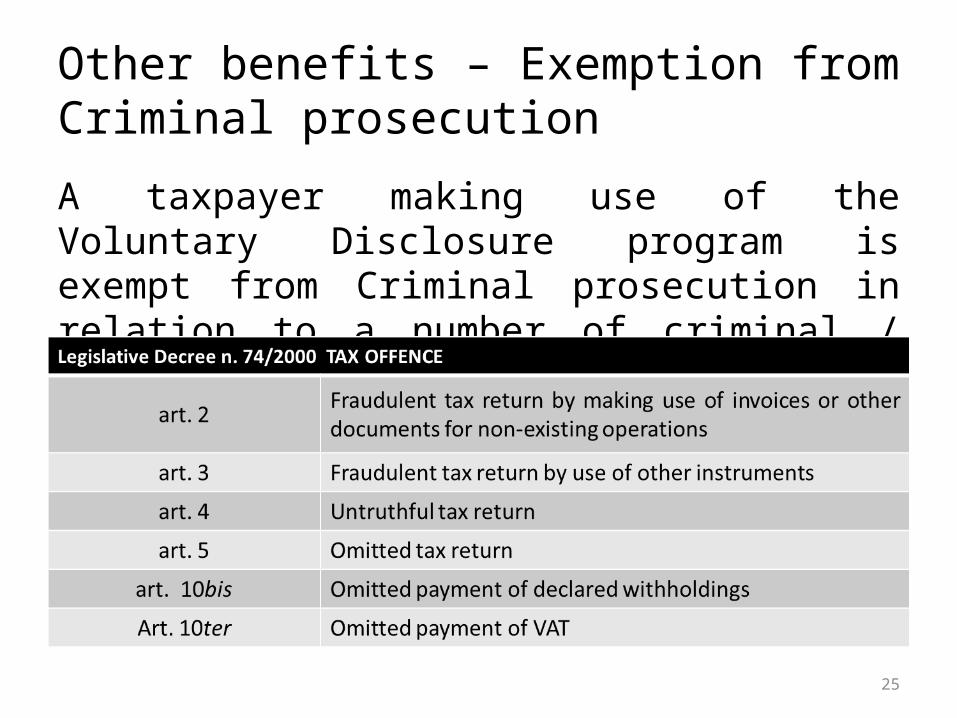

Other benefits – Exemption from Criminal prosecution

A taxpayer making use of the Voluntary Disclosure program is exempt from Criminal prosecution in relation to a number of criminal / tax offences, being

26

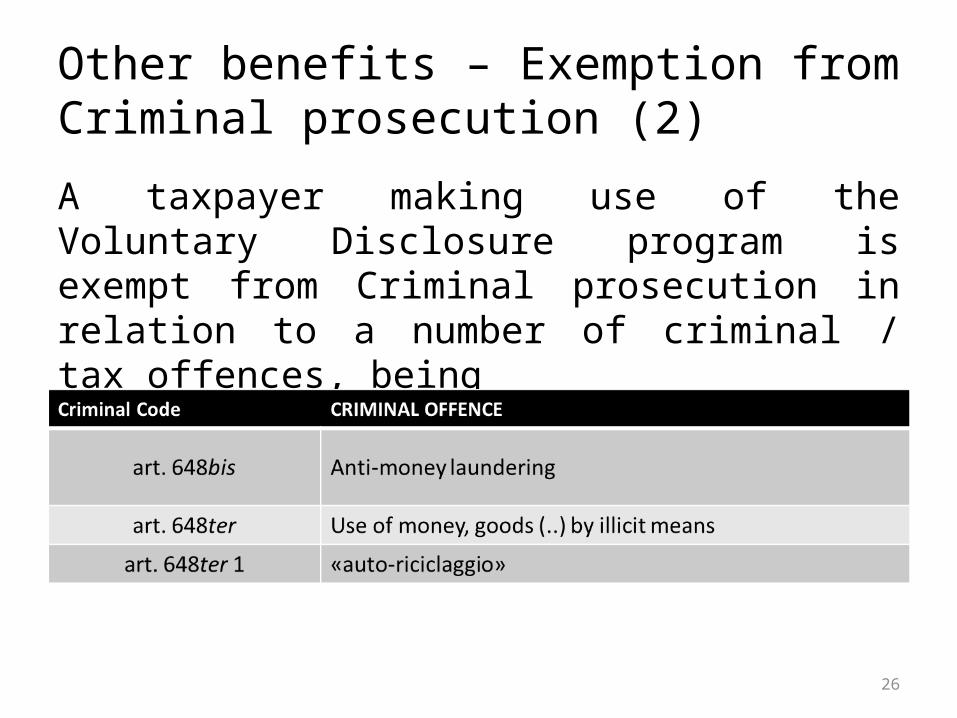

Other benefits – Exemption from Criminal prosecution (2)

A taxpayer making use of the Voluntary Disclosure program is exempt from Criminal prosecution in relation to a number of criminal / tax offences, being

27

New offence of «auto-riciclaggio»

The new art. 648ter 1 of the Italian Criminal Code foresees that:«whoever, having committed or taken part in committing with intent a crime, uses substitutes or transfers the money, goods or other items deriving from the illicit activities in economic, financial, entrepreneurial or speculative activities, such to concretely hinder the identification of their illicit origin (..), will be punished (..)»

28

Impediments• A taxpayer may not use the Voluntary Disclosure program whenever he, or

another person jointly responsible, is formally aware of access, inspections, verifications or any other kind of audit activity from the Italian tax authorities (e.g. the receipt of merely questionnaire is sufficient);

• Nonetheless, if a taxpayer is subject to an audit and has finalized the procedure in relation to a tax period, it may re-open the relevant tax period for the purpose of the Voluntary Disclosure; also the audit in relation to a specific tax does not preclude the use of the Voluntary Disclosure program in relation to other relevant tax years or other taxes (Cfr. Circ. 13 March 2015, n. 10/E, par. 3);

• In any case, whenever the Voluntary Disclosure Program cannot be used, the taxpayer may still use the voluntary settlement program (ravvedimento operoso)

29

Finalization of the procedure

The taxpayer needs to pay in a single instalment (or in three equal instalments), all amounts due in relation to the unpaid taxes and violations of the fiscal monitoring rules

The taxpayer may not make use of compensation mechanism as of art. 17 of D.L. 241/1997 not may it pay in additional instalments

The procedure is correctly finalized upon payment of all sums due; therefore failure to pay just one of the due instalments means that the Voluntary Disclosure Program is not correctly concluded

This means that the Italian tax authorities will recalculate the administrative penalties due (no reduction) and the taxpayer cannot benefit from the exemption of criminal prosecution

30

Thank you for your attention

Patrick HarteveldMazars S.p.A. – Studio Associato

Legale e Tributario Via Ludovisi 16, 00187 Roma

Email: [email protected]: +39 06 6976301

Claudia C. de RegtPersonal Financial Advisor

Fineco BankVia degli Scipioni 260

00192 RomaEmail: [email protected]

Tel: +39 337 869926