who will be the winners in maritime satcom five years from now

TRANSCRIPT

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo

Who will be the winners in maritime satcom five years from now An Euroconsult presentation for Thor 7 customer briefing

Euroconsult presentation for Thor 7 customer briefing

Wei Li, Senior Consultant

Oslo June 3rd, 2015

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo

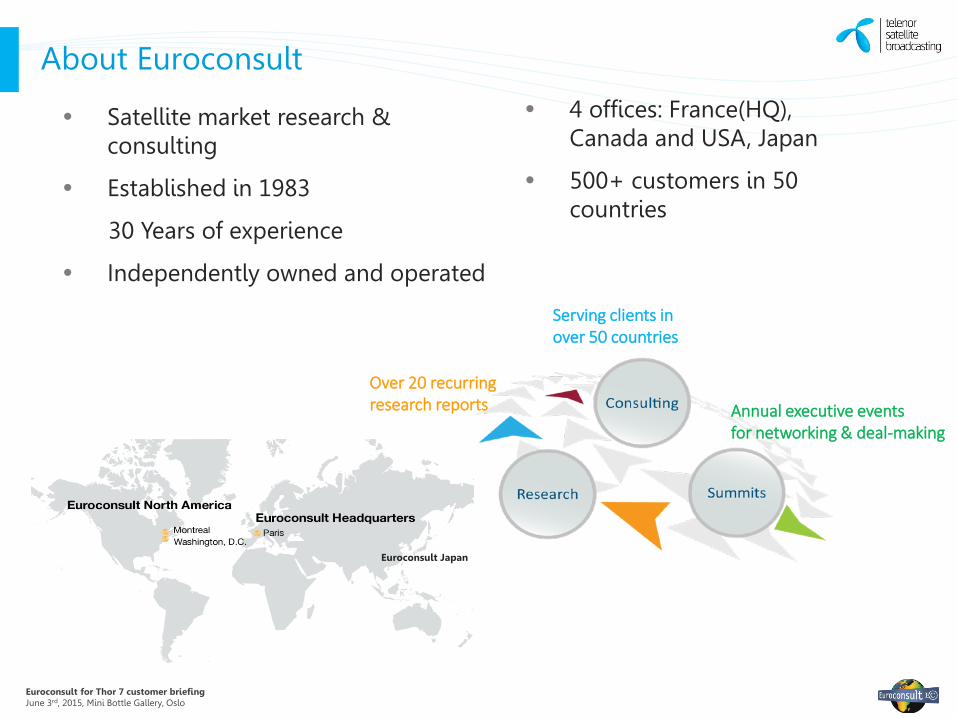

• Satellite market research & consulting

• Established in 1983

30 Years of experience

• Independently owned and operated

About Euroconsult

Euroconsult Japan

Serving clients in over 50 countries

Over 20 recurring research reports Annual executive events

for networking & deal-making

• 4 offices: France(HQ), Canada and USA, Japan

• 500+ customers in 50 countries

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo

RELATED RESEARCH REPORTS

Mobile Satellite Communications Markets Survey Prospects to 2024 2015 Edition* Comprehensive expert analysis & forecasts for the MSS sector

*Available

Prospects for In-Flight Entertainment and Connectivity Prospects to 2024 2015 Edition* Sector dynamics, analysis and forecasts addressing the IFEC market for commercial airlines and business aviation

*Release soon

High Throughput Satellite Systems Prospects to 2022 2014 Edition A vertical market analysis of major drivers, strategic issues and demand take-up for High Throughput Satellites

*Available

Maritime Telecom Solutions by Satellite Prospects to 2024 2015 Edition* Comprehensive analysis & forecasts for maritime satellite communications - Merchant Shipping, Fishing, Passenger Ships, Leisure Vessels, Offshore

*Release soon

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo

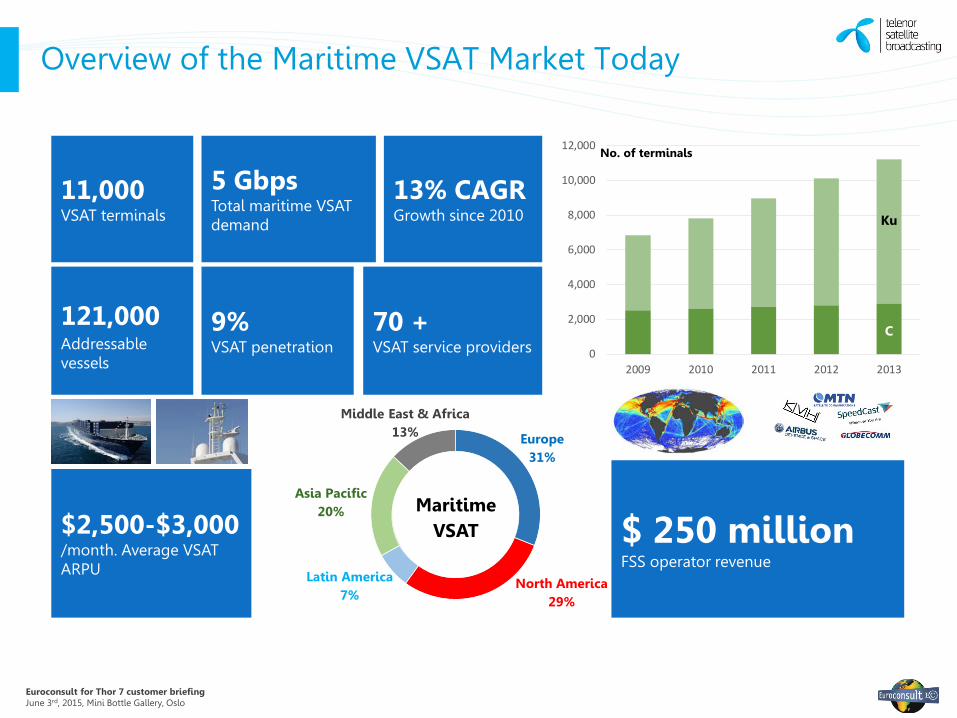

Overview of the Maritime VSAT Market Today

70 + VSAT service providers

121,000 Addressable vessels

$2,500-$3,000 /month. Average VSAT ARPU

9% VSAT penetration

$ 250 million FSS operator revenue

11,000 VSAT terminals

5 Gbps Total maritime VSAT demand

13% CAGR Growth since 2010

0

2,000

4,000

6,000

8,000

10,000

12,000

2009 2010 2011 2012 2013

No. of terminals

C

North America 29%

Europe 31%

Asia Pacific

20%

Latin America 7%

Maritime VSAT

Middle East & Africa 13%

Ku

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo

5

Maritime vertical review

MERCHANT

FISHING

PASSENGER

LEISURE

OFFSHORE O&G

Drivers

68,000

46,000

6,500

6,600

1,200

• Fuel cost reduction • Operation optimization • Crew retention

• Passenger entertainment & communications

Addressable vessels Penetration ARPU

MSS >100%

source: Euroconsult research.

• Data intensive exploration and monitoring applications

• Crew retention

• Passenger entertainment & communications

• Regulation • Crew retention

MSS >100%

MSS >100%

MSS >100%

VSAT <5%

VSAT >10%

VSAT >15%

VSAT<20%

MSS >50%

VSAT <10%

MSS <$500

VSAT ~$2,500

MSS <$300

VSAT ~$10,000

MSS <$1,000

VSAT ~$20,000

MSS ~$1,000

VSAT ~$2,000

MSS <$500

VSAT ~$2,000

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo

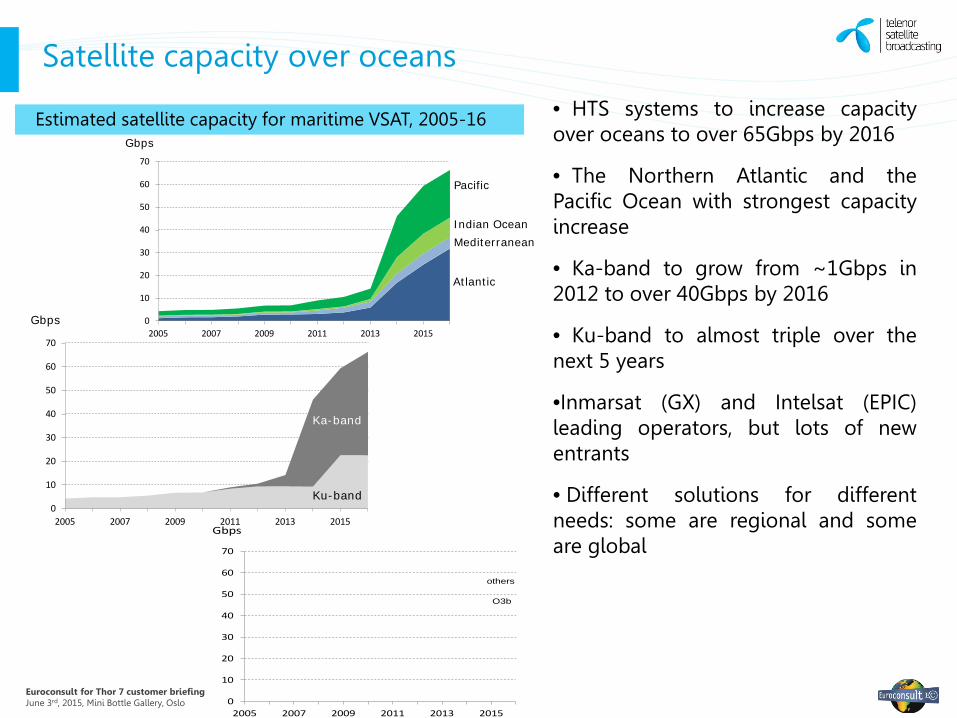

• HTS systems to increase capacity over oceans to over 65Gbps by 2016

• The Northern Atlantic and the Pacific Ocean with strongest capacity increase

• Ka-band to grow from ~1Gbps in 2012 to over 40Gbps by 2016

• Ku-band to almost triple over the next 5 years

•Inmarsat (GX) and Intelsat (EPIC) leading operators, but lots of new entrants

• Different solutions for different needs: some are regional and some are global

Satellite capacity over oceans

Estimated satellite capacity for maritime VSAT, 2005-16

Gbps

Pacific

Indian OceanMediterranean

Atlantic

0

10

20

30

40

50

60

70

2005 2007 2009 2011 2013 2015Gbps

0

10

20

30

40

50

60

70

2005 2007 2009 2011 2013 2015

Ku-band

Ka-band

0

10

20

30

40

50

60

70

2005 2007 2009 2011 2013 2015

Intelsat

Inmarsat

O3b

others

Gbps

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo

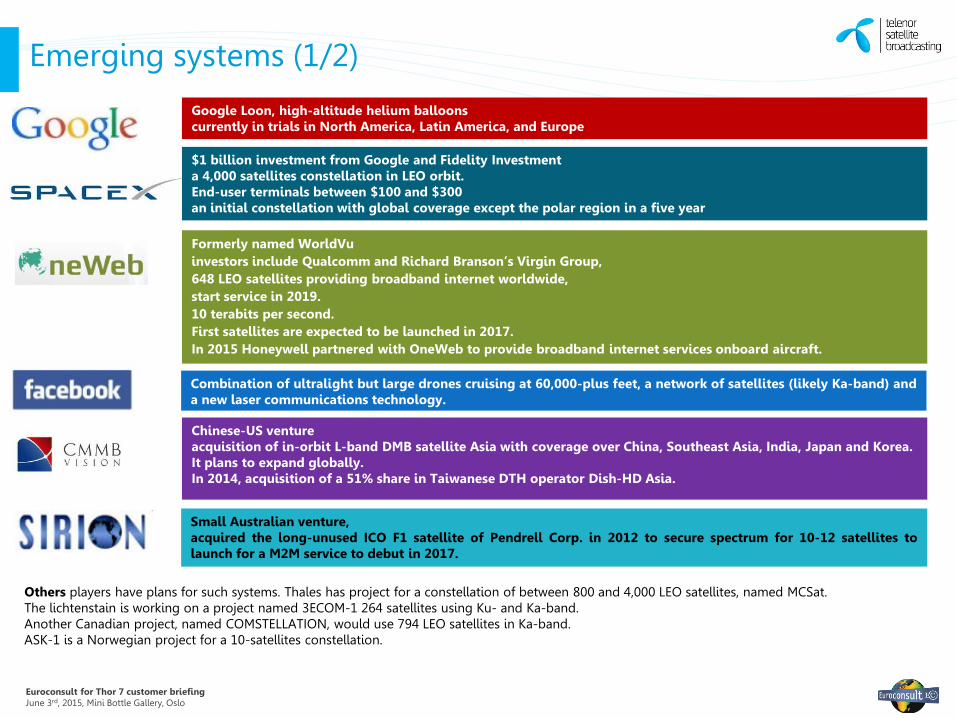

Google Loon, high-altitude helium balloons currently in trials in North America, Latin America, and Europe

Emerging systems (1/2)

Formerly named WorldVu investors include Qualcomm and Richard Branson’s Virgin Group, 648 LEO satellites providing broadband internet worldwide, start service in 2019. 10 terabits per second. First satellites are expected to be launched in 2017. In 2015 Honeywell partnered with OneWeb to provide broadband internet services onboard aircraft.

Combination of ultralight but large drones cruising at 60,000-plus feet, a network of satellites (likely Ka-band) and a new laser communications technology.

Chinese-US venture acquisition of in-orbit L-band DMB satellite Asia with coverage over China, Southeast Asia, India, Japan and Korea. It plans to expand globally. In 2014, acquisition of a 51% share in Taiwanese DTH operator Dish-HD Asia.

$1 billion investment from Google and Fidelity Investment a 4,000 satellites constellation in LEO orbit. End-user terminals between $100 and $300 an initial constellation with global coverage except the polar region in a five year

Small Australian venture, acquired the long-unused ICO F1 satellite of Pendrell Corp. in 2012 to secure spectrum for 10-12 satellites to launch for a M2M service to debut in 2017.

Others players have plans for such systems. Thales has project for a constellation of between 800 and 4,000 LEO satellites, named MCSat. The lichtenstain is working on a project named 3ECOM-1 264 satellites using Ku- and Ka-band. Another Canadian project, named COMSTELLATION, would use 794 LEO satellites in Ka-band. ASK-1 is a Norwegian project for a 10-satellites constellation.

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo

Emerging systems (2/2)

Most of the emerging systems are using low-earth orbit (LEO) constellations of hundreds of small satellites with lower latency than geostationary satellite systems. Some of them have inter-satellite links which reduce the dependence on ground segment and reduce latency. Three challenges for such systems: • The development time, which has ultimately taken up to 8-10 years for all LEO

constellations including regulatory process to access spectrum, design issues with the constellation, time required to launch satellites to orbit etc.

• The need to develop a likely dedicated ground segment that is cost effective, • Constellations are global by nature: they need to obtain landing rights/access in all

countries where they want to provide capacity from their day of launch.

Large capex required at the start for satellites that usually have a short lifetime (less than 10 years) and the time needed to develop their business have so far made the economic model extremely challenging.

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo

• Capacity prices per Mbps will go down

• New maritime markets and end-users will become addressable for satellite broadband

• Services will allow for new, more bandwidth intense applications (e.g. high-speed internet, streaming, cloud computing, etc.)

• The growth of ARPU is however not expected to be in line with bandwidth

• End users and service providers are becoming increasingly technology agnostic with the abundance choice of networks

• When bandwidth is not anymore a limitation, the market will become application and service driven

Impacts from HTS capacity over the oceans

Supply

Demand

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo 10

• Engine manufacturers and other vendors are building their systems with sensors in vessels and run algorithms to interpret that data, for maintenance, remote diagnostic, customer support and product improvement purpose

• In most cases shipping company’s IT will take care of the data transmissions

• In average, one IT engineer takes care of 15-20 ships

• Yards, vendors, owners, ship managers, regulators, need to agree what data should be there, and what format it should be in

• There are many standards and the data all needs to have the same protocol to be transferred over a single centralized system

• Autonomous vessel will be the next step as result from big Data

Big Data

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo 11

• Trend of more and more automation onboard the vessel with an increasing amount of data to be tracked

• Regulation and safety applications (LRIT, AIS, etc.)

• Condition based/performance monitoring (engine, etc.)

• Cargo monitoring (containers, etc.)

• Requirements for M2M applications onboard vessels growing and diversifying

• Need for interoperability of multiple technologies and systems (GSM, RFID, satellite, etc.)

M2M – the internet of things

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo 12

• ‘Cloud computing’ can help shipping companies to reduce IT investment, and improve efficiency.

• However it has yet struggled to gain acceptance within the conservative maritime industry

• Ship owners generally have strong concern about data security over cloud infrastructure

• Some major companies have started to move in this direction

• The majority of the cloud projects are still with company-wide or ship-wide cloud infrastructures.

• Ship-wide cloud is by far mostly used for entertainment for crew or passengers (e.g. VAVE system from MCP for Corsica Ferries)

• Internet-wide cloud infrastructures have been recently started to adopt by a few shipping companies for business purpose (e.g. Orange Business Services for Columbia Ship Management).

Cloud applications

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo 13

• For long the telecommunications in ships are only available in the bridge via wired and fix devices

• Crew call room and Internet café are adopted by a shipping companies

• The crew and passenger communications have been significantly increasing along with the trends in terrestrial telecom

• The majority of new communication needs are data

• BYOD is becoming popular and communication become wireless onboard

• Wireless communications basically include Wi-Fi and cellular. Wi-Fi is easier to realize and cellular is of more complexity and require roaming agreements.

Bring-your-own-device (BYOD)

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo 14

• Increasing use of video applications with high data rate requirements

• Real time video streaming from the vessel for remote monitoring and diagnostics

• E-learning and crew training

• Update of weather charts, maps, shipping documents, manuals

• Video conferencing

• Quality and resolution of videos and images improving

• Trend towards HD with video streams that can require 2-8Mbps

• More efficiency systems and better compression needed

Video – “Pictures worth a thousand words”

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo 15

• The market, especially high end market is approaching the saturation in terms of satcom penetration

• SP are looking for new opportunities to increase ARPU

• Content is considered to be the most important and easy to do add on to get incremental revenue from existing customers

• KVH and Inmarsat are the pioneers among service provider to provide contents to ships

• By far most contents are entertainment and news related

• Tele-education and business related contents are in development and are expected to be online in the coming months

Content is king

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo

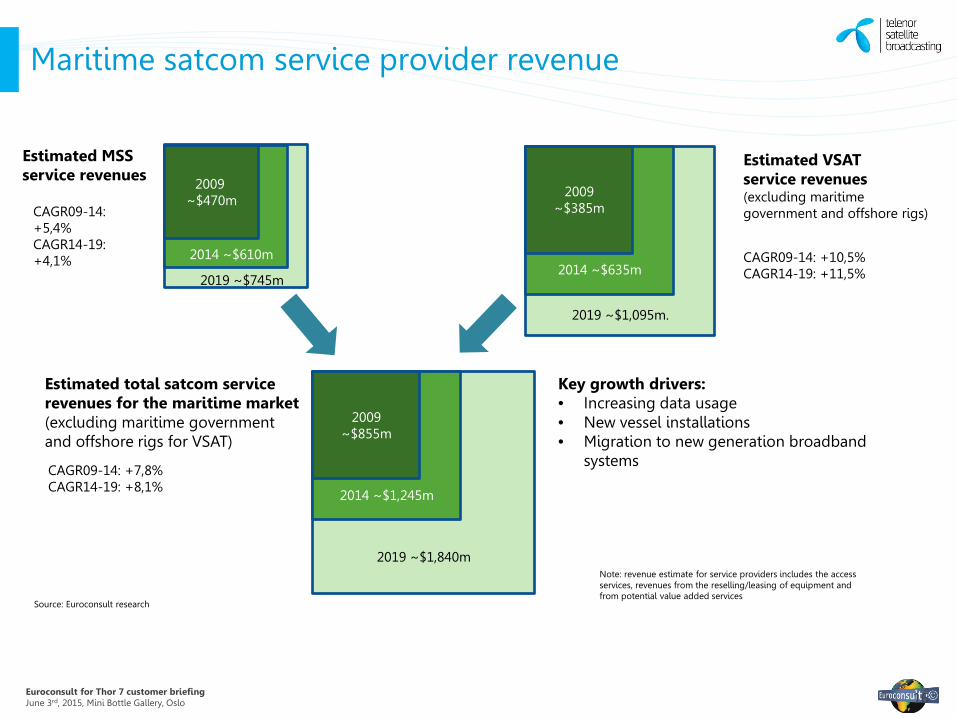

2009 ~$470m

16

Maritime satcom service provider revenue

2019 ~$1,095m.

2014 ~$635m

2009 ~$385m

Estimated VSAT service revenues (excluding maritime government and offshore rigs)

Estimated MSS service revenues

2014 ~$610m

2019 ~$745m

Estimated total satcom service revenues for the maritime market (excluding maritime government and offshore rigs for VSAT)

2019 ~$1,840m

2014 ~$1,245m

2009 ~$855m

Source: Euroconsult research

Note: revenue estimate for service providers includes the access services, revenues from the reselling/leasing of equipment and from potential value added services

CAGR09-14: +5,4% CAGR14-19: +4,1% CAGR09-14: +10,5%

CAGR14-19: +11,5%

CAGR09-14: +7,8% CAGR14-19: +8,1%

Key growth drivers: • Increasing data usage • New vessel installations • Migration to new generation broadband

systems

Euroconsult for Thor 7 customer briefing June 3rd, 2015, Mini Bottle Gallery, Oslo

CONTACTS

Wei LI [email protected]

www.euroconsult-ec.com

17

Paris Office 86 Blvd de Sébastopol 75003 Paris - France T: +33 (0)1 49 23 75 30 - F: +33 (0)1 48 05 54 39