8.1 activity based costing (abc) · web viewdescribe and explain the activity based costing (abc)...

TRANSCRIPT

DEPARTMENT OF ACCOUNTING SCIENCE AND FINANCE

COST AND MANAGEMENT ACCOUNTING II (CUAC 203) NOTES

BSCAC 1.2 2016

COMPILED BY MUGUTI E (MR)

1 | P a g e

The Chairperson’s Office

COURSE OUTLINE 2016(Revised)

COURSE LECTURER: E.MUGUTI (MR.)

General Information

Office: Prefab Block 1 Office 6

E-mail: [email protected], [email protected] .

+263775712712

1.0 Course Title and CodeCost and Management Accounting II – CUAC 203

2.0 Time Allocation4 hours per week and 1 hour will be reserved for tutorials

2 | P a g e

CHINHOYI UNIVERSITY OF TECHNOLOGY

ACCOUNTING SCIENCE AND FINANCE DEPARTMENT

+ P. Bag 7724, CHINHOYI, ZIMBABWE

3.0 RationaleThis course develops further the costing concepts and methods introduced in Cost and Management Accounting 1(CUAC 104) and also introduce contemporary approaches in arriving at the cost of products produced or services rendered. In addition, the course discusses applications of techniques in the analysis of relevant data to provide information for managerial planning, control, divisional performance evaluation and decision making.

4.0 Purpose 4.1 To provide an understanding on how organisations accumulate, assign and analyse cost and revenue data for use within the organisation and its practical applications thereof. 4.2 To provide an understanding on how organizations use managerial information in planning, controlling, decision making and divisional performance evaluation, and to enable students to apply management accounting techniques in providing such information.

5 Main CapabilitiesBy the end of the course, students should be able to:

5.1 Apply the concept of Activity Based Costing (ABC) in product costing and profitability analysis and distinguish it from the traditional absorption costing approach. 5.2 Compile the master budget from the functional, operating budgets and other given information and use the concept of flexible budgeting in managerial control. 5.3 Explain the concept of relevant costs and revenues and apply this concept in tactical short-term decisions such as (i) make or buy decisions (ii) dropping a product, department or business unit (iii) profitability analysis (iv) acceptance/rejection of a special order and (v) limiting factor analysis5.4 Apply the linear programming model in solving problems with more than one limiting factor5.5 Use various techniques in capital investment decisions including accounting rate of return, payback; discounted payback, discounted cash flow techniques, and adjust for the effect of inflation and taxation. 5.6 Compute the profitability index and use it in capital rationing situations5.7 Incorporate motivational, behavioural and ethical issues in managerial planning, control and decision making. 5.8 Analyse management accounting information and use performance measures such as Return on Capital Employed (ROCE), Residual Income (RI), Economic Value Added (EVA) and Cash Flow Return on Investment (CFROI) in divisional performance evaluation and management control.

3 | P a g e

5.9 Critically evaluate each costing technique, method and approach used in the analysis of cost information for managerial control, decision making and performance evaluation.

6 Method of InstructionEach section of the course outline will be thoroughly demonstrated in the lecture, with comprehensive examples articulated to the students. The following methods among others will be used:

6.1 Lectures

6.2 Demonstrations

6.3 Group discussions6.4 Tests

7 Students Assessments

7.1 Coursework comprises of at least two (2) tests and one (1) assignment, which constitute 30% weight of the final mark. Questions in the tests will cover all the pertinent aspects of the course covered up to the time of the test, and will serve as mock exams, in preparation for the final exam.

7.2 Final exam constitute 70% of the final mark and will examine all the

pertinent aspect of the course.

7.3 The final mark will be a summation of course work and the exam mark.

7.4 The students will evaluate the course online on their student portals

7.5 The range of marks attained by the student will be classified as follows:

Degree Class Range of Marks Description

1 75% - 100% Distinction

2.1 65% - 74% Pass

2.2 60% - 64% Pass

3 50% - 59% Pass

4 | P a g e

F 0% - 49% Fail

8 Course Content8.1 Activity Based Costing (ABC)

Changes in cost composition and impact of the Activity-based costing (ABC) method

Treatment of costs are under Activity-Based Costing(ABC) Designing an Activity-Based Costing(ABC) system The mechanics of ABC Comparison of traditional and ABC product costs Advantages and limitations of ABC ABC in the service industry

8.2 Intermediate Budgeting and Budgetary Control

8.2.1 Master Budget

Budgeted Cash Flow Statement (Cash Budget) Budgeted Income Statement Budgeted Statement of Financial Position

8.2.2 Flexible Budgeting

Preparation of fixed budgets Preparation of flexible budgets Separation of fixed and variable costs using the high-low method. Budgetary control statements under both the fixed and flexible budgets The appropriateness of fixed and flexible budgets in different circumstances

8.3 Short-term Tactical Decision Making

8.3.1 Relevant costs and Decision Making

The concept of relevant costs and revenues for decision making Make or buy decisions Dropping a segment, department or a business unit Profitability analysis Acceptance/rejection of a special order Limiting factor analysis

8.3.2Linear programming Formulating a linear programming model with objective function,

variables and constraints

5 | P a g e

Solving a linear programming problem using (i) graphical method (ii) simultaneous equations method and (iii) simplex method

Shadow prices Slack and surplus

8.4 Investment Appraisal8.4.1 The capital budgeting process and the role of investment appraisal8.4.2 Capital investment appraisal techniques

Accounting rate of return Payback Discounted payback Net present value Internal rate of return

8.4.3 Profitability Index and capital rationing8.4.4 Effect of inflation and taxation in capital investment appraisal8.4.5 Ethical and non-financial issues in long-term decision-making

8.4 Divisional Performance Evaluation

8.4.1Responsibility centres:

Cost centre, Revenue centre, Profit centre, Investment centre8.4.2 Measures of performance:

Profit, Return On Capital Employed(ROCE), Residual Income(RI), Economic Value Added(EVA) and Cash Flow Return on Investment(CFROI)

Course Text(s) Recommended Reading

1. Drury C (2008) Management and Cost Accounting, 7 th Edition, Cengage Learning, London.

2. Horngren, C.T. etal Cost Accounting – A managerial Emphasis, 13 th Edition, Prentice Hall Inc, New Jersey.

3. Lucey T (2006) Costing, 7th Edition, DP Publications.

4. Lucey T (2006) Management Accounting, 5th Edition, DP Publications

5. Vigario F (2007) Managerial Accounting, 4th Edition, LexisNexis, Durban, South Africa.

6. CPA Australia/CIMA/ACCA modules.

7. Articles from professional journals.

6 | P a g e

1. ACTIVITY BASED COSTINGOBJECTIVESBy the end of this topic, the student should be able to; 1. Explain the shortcomings of traditional overhead absorption/allocation methods.2. Describe and explain the Activity Based Costing (ABC) approach to overhead absorption and how it overcomes the limitations of the traditional methods.3. Compute products costs using ABC approach and compare the costs with those calculated under the traditional methods.4. Comment on the reasons for the differences in costs between ABC and traditional methods.

1.0 INTRODUCTION The cost of a product or service is information that is quite often required by

management for various purposes, for example, stock valuation, profit measurement or

decision making.

Cost is simply the aggregate of all the expenses incurred in bringing a product to its

present condition and location,

Some expenses are directly traceable to the cost object (direct costs), while some are

not (indirect costs or overheads).

The problem remains that production overhead, which is not directly traceable, should

form part of the production cost of a product.

The process of allocating production overheads to cost units/cost objects is known as

overhead absorption.

There are two approaches to overhead absorption; (i) traditional approach (ii) Activity

Based Costing (ABC) approach.

1.1 TRADITIONAL COST ALLOCATION METHODS Apportions the total production overheads based on production volume.

7 | P a g e

Common absorption bases are number of units, machine hours and direct labour hours.

Under this approach, an organisation can use either a (i) plant-wide allocation method

or a (ii) departmental allocation method.

The plant-wide allocation method uses the entire plant/organisation as a cost pool.

Therefore one overhead absorption rate is calculated for the whole plant/organisation.

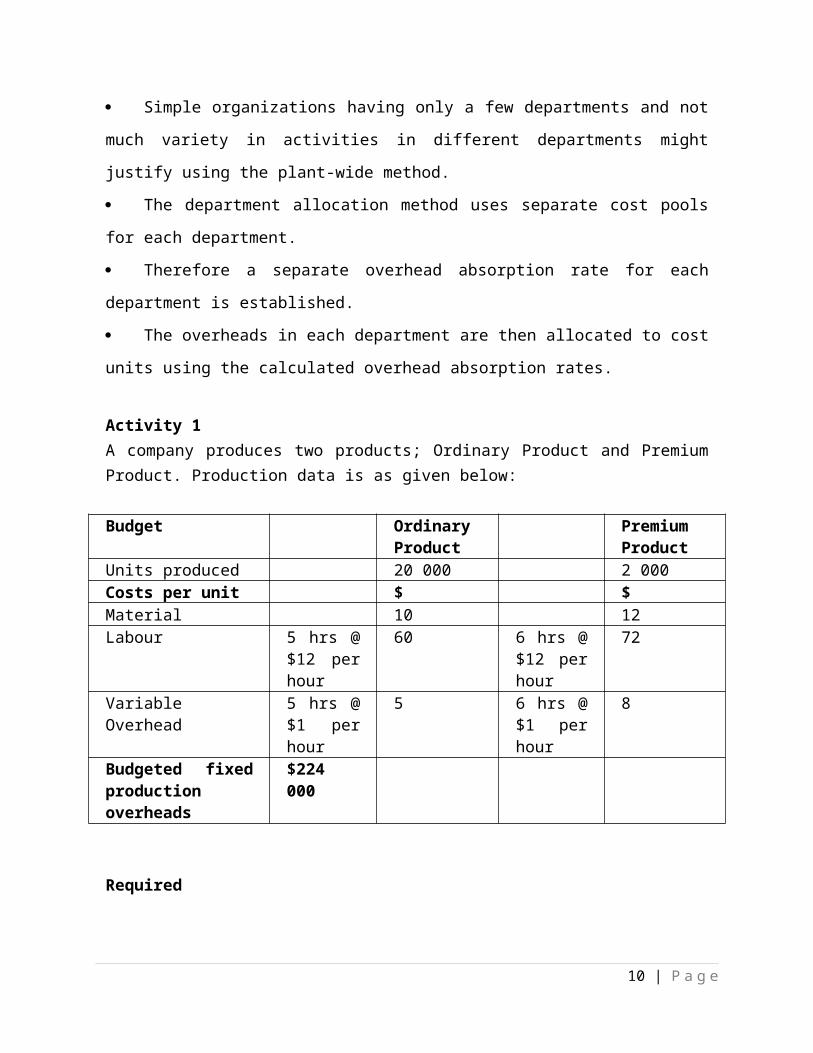

Simple organizations having only a few departments and not much variety in activities

in different departments might justify using the plant-wide method.

The department allocation method uses separate cost pools for each department.

Therefore a separate overhead absorption rate for each department is established.

The overheads in each department are then allocated to cost units using the calculated

overhead absorption rates.

Activity 1A company produces two products; Ordinary Product and Premium Product. Production data is as given below:

Budget Ordinary Product

Premium Product

Units produced 20 000 2 000Costs per unit $ $Material 10 12Labour 5 hrs @

$12 per hour

60 6 hrs @ $12 per hour

72

Variable Overhead 5 hrs @ $1 per hour

5 6 hrs @ $1 per hour

8

Budgeted fixed production overheads

$224 000

RequiredCalculate the total full production cost and the production cost per unit of each product using labour hours to absorb overheads.

The major drawback of the traditional approach to overhead absorption is that overhead

is absorbed into product cost on the basis of production volume (measured generally in

8 | P a g e

machine hours, labour hours, etc) regardless of the fact that most of the overhead expenses

may not have been the result of that production volume.

This, therefore, results in inaccurate allotment of overhead cost with a consequent effect

on product pricing and profitability or profit measurement.

The modern approach called Activity Based Costing (ABC) challenges this traditional

approach by arguing that in these days of technological advancement, different factors do

influence the overhead expense.

These factors are called cost drivers.

ABC attempts to find a causal relationship between overhead and the cost driver.

A cost driver is, therefore, any factor which causes a change in the cost of an activity.

1.2 ACTIVITY BASED COSTING (ABC)

Challenges the traditional approach but takes into consideration the real factors that

cause overhead to vary with production.

This is because, it is believed that, what is regarded as overheads is now accounting for

significant proportion of total cost and a more accurate method of apportionment is therefore,

required.

Using this approach would require a different way of classifying overhead cost, and the

use of Cost Drivers.

Activity-based costing (ABC) rest on this premise: Products require activities;

activities consume resources and acquisition of resources causes costs.

ABC therefore, assigns costs first to activities, then to the products based on each

product’s use of activities.

1.2.1 Steps in ABC Activity-based costing requires accountants to follow four steps.

1. Identify the activities that consume resources and assign costs to those activities Activity: an event, task, or unit of work with a specified purpose,

e.g. designing products, setting up machines, operating machines, procuring materials

etc. are some of the activities in a manufacturing organisation.

9 | P a g e

Activities can be classified into 4 categories namely; unit level activities, batch level

activities, product level activities, and facility level activities.

(a) Unit level activities.

The costs of these activities are strongly correlated to the number of units produced.

For example, the use of indirect materials/ consumables tends to increase in proportion

to the number of units produced. Another example is; the inspection or testing of every item

produced

(b)Batch level activities. The costs of these activities are driven by the number of batches of units produced.

Examples of this are:

1. Material ordering – where an order is placed for every batch of production.

2. Machine set-up costs – where machines need resetting between each different batch of

production.

3. Inspection of products – where the first item in every batch is inspected rather that

every item.

(c)Product level activities. The costs of these activities (often once only activities) are driven by the creation of a

new product line and its maintenance,

For example, designing the product, producing parts specifications and keeping

technical drawings of products up to date. Advertising costs fall into this category if

individual products are advertised rather than the company’s name.

(d)Facility level activities. These costs are not related to a particular product line; instead they are related to

maintaining the buildings and facilities.

Examples are the maintenance of buildings, plant security, business rates, production

manager’s salary and advertising to promote the whole organisation.

The first and last categories above are the same as those in traditional absorption costing

and so if an organisation’s costs are mainly made up of these two categories ABC will not

improve the overhead analysis greatly.

10 | P a g e

But if the organisation’s costs fall mainly in the second and third categories an ABC

analysis will provide a different and more accurate analysis.

2. Identify the cost driver(s) associated with each activity. A cost driver is a factor that causes, or ‘‘drives,’’ an activity’s costs.

For the activity ‘‘purchasing materials,’’ the cost driver could be ‘‘number of

orders.’’(Each activity could have multiple cost drivers.)

How do managers decide which cost driver to use? The primary criterion for selecting a

cost driver is causal relation. Choose a cost driver that causes the cost.

Activity 2

Match the following costs with their appropriate cost drivers and also identify volume based and non volume based cost drivers:

COSTS COST DRIVERS1. Depreciation A. No. of set ups2. Indirect labour cost B. No. of purchases3. Machine set up cost C. No. of product design4. Order placing cost D. No. of inspections5. Inspection cost E. Machine hours6. Design cost F. Direct labour hours

3. Compute a cost driver rate for each cost driver. Cost driver rate=Indirect cost or Overheads for each activity/Cost driver volume

4. Assign costs to products using the cost driver rate Multiply the cost driver rate by the volume of cost drivers consumed by the product.

For example, the cost per purchase order times the number of orders required for

Product X for the month of December would measure the cost of the purchasing activity for

Product X for December.

11 | P a g e

1.2.2 Activity Analysis ABC starts with activity analysis.

An activity is a unit of work, a task or an event, it involves action words, for example,

purchasing raw materials, setting up machinery, machining and inspecting finished goods.

Activity Analysis has 4 steps;

1. Chart, from start to finish, the activities used to complete the product or service.2. Classify activities as value-added or non–value-added.3. Eliminate non–value-added activities.4. Continuously improve and reevaluate the efficiency of value-added activities or replace them with more efficient activities. Activity analysis provides a systematic way for organizations to evaluate the processes

that they use to produce goods and services for their customers.

Such an analysis can identify and eliminate activities that add costs but not value to the

product.

Non–value-added costs are costs of activities that the company can eliminate without

reducing product quality, performance, or value.

The following activities are candidates for elimination because they do not add value to

the product; (i) storage of materials, (ii) moving items and (iii) waiting for work.

The traditional method of cost allocation is criticized as being too simplistic and

inaccurate; the dinner example

There is the trade-off that accountants and managers face: the less expensive, less

accurate, traditional method versus the more expensive, more accurate, activity analysis.

Managers must make a cost-benefit call whether the added benefits of activity-based

information justify the additional costs of obtaining that information.

Cost pools are groups of costs.

Activity 3Continuing from data in Activity 2 above, the following additional information is provided;

1. The examination of the fixed overheads of $224,000 shows that they consist of:$Machine set-up costs 90,000Material handling costs 92,000Packaging costs (manual) 42,000

12 | P a g e

Total 224,000

2. Activity Levels are as follows;

Product Ordinary PremiumNumber of set ups 10 20Number of material movements 400 000 60 000

Required(a)Calculate the total full production cost and the production cost per unit using ABC principles(b) Compare the cost per unit under the Traditional approach and ABC approach and comment on why there are differences.

Activity 3Two products X and Y are made using similar equipment and methods.The data for last period are:

X YUnits produced 6,000 8,000Labour hours per unit 1 2Machine hours per unit 4 2Set-ups in period 15 45Orders handled in the period 12 60Overheads for period $Relating to production set-ups 89,500Relating to order handling 15,000Relating to machine activity 27,500

Required:Calculate the overheads to be absorbed per unit of each product based on:(a) Conventional absorption costing using a labour absorption rate(b) An ABC approach using suitable cost drivers.(c) Compare the overhead cost per unit in (a) and (b) above and comment on why ABC is considered to be superior to the traditional approach.

END OF TOPIC NOTES

13 | P a g e

2. INTERMEDIATE BUDGETING AND BUDGETARY CONTROL

OBJECTIVESAfter studying this topic, the student should be able to:1. Compile master budgets (Statement of Comprehensive Income, Statement of Financial Position and Budgeted Cash Flow Statement (Cash budget)2. Explain the importance of preparing cash budgets3. Explain and prepare fixed, flexible and flexed budgets and justify the circumstances under which each type of budget is appropriate.4. Prepare budgetary control operating statements under both fixed and flexed budgets and suggest reasons for the causes of variances.

1.1 MASTER BUDGET This is the summary of all the operating and financial budgets and it consists of a Budgeted

Income Statement, a Budgeted Statement of Financial Position and a Budgeted Cash flow

statement.

The master budget is, therefore, an overall budget.

1.11 Cash Budget Provides an estimate of all receipts and payments and the manner and period in which they will

be received or employed.

This budget is prepared after all other budgets are complete. Attention must be paid to the

following aspects:

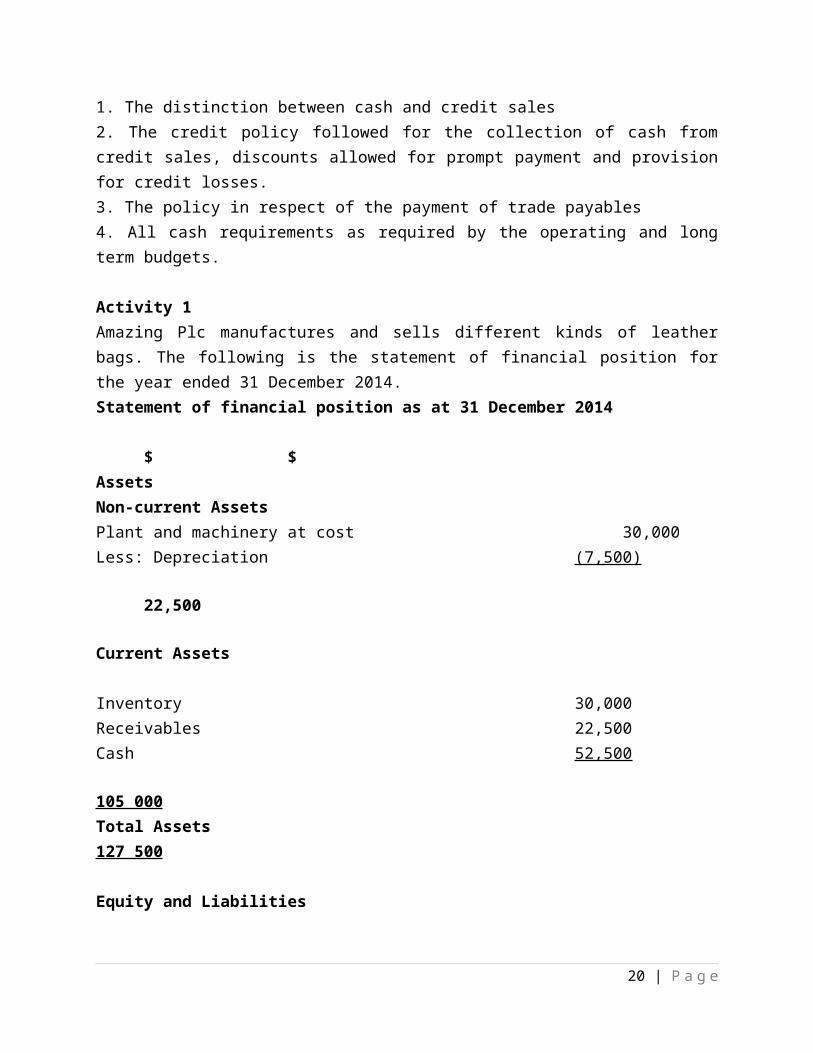

1. The distinction between cash and credit sales2. The credit policy followed for the collection of cash from credit sales, discounts allowed for prompt payment and provision for credit losses.3. The policy in respect of the payment of trade payables4. All cash requirements as required by the operating and long term budgets.

Activity 1Amazing Plc manufactures and sells different kinds of leather bags. The following is the statement of financial position for the year ended 31 December 2014.Statement of financial position as at 31 December 2014

$ $AssetsNon-current Assets

14 | P a g e

Plant and machinery at cost 30,000Less: Depreciation (7,500)

22,500 Current Assets

Inventory 30,000Receivables 22,500Cash 52,500

105 000 Total Assets 127 500

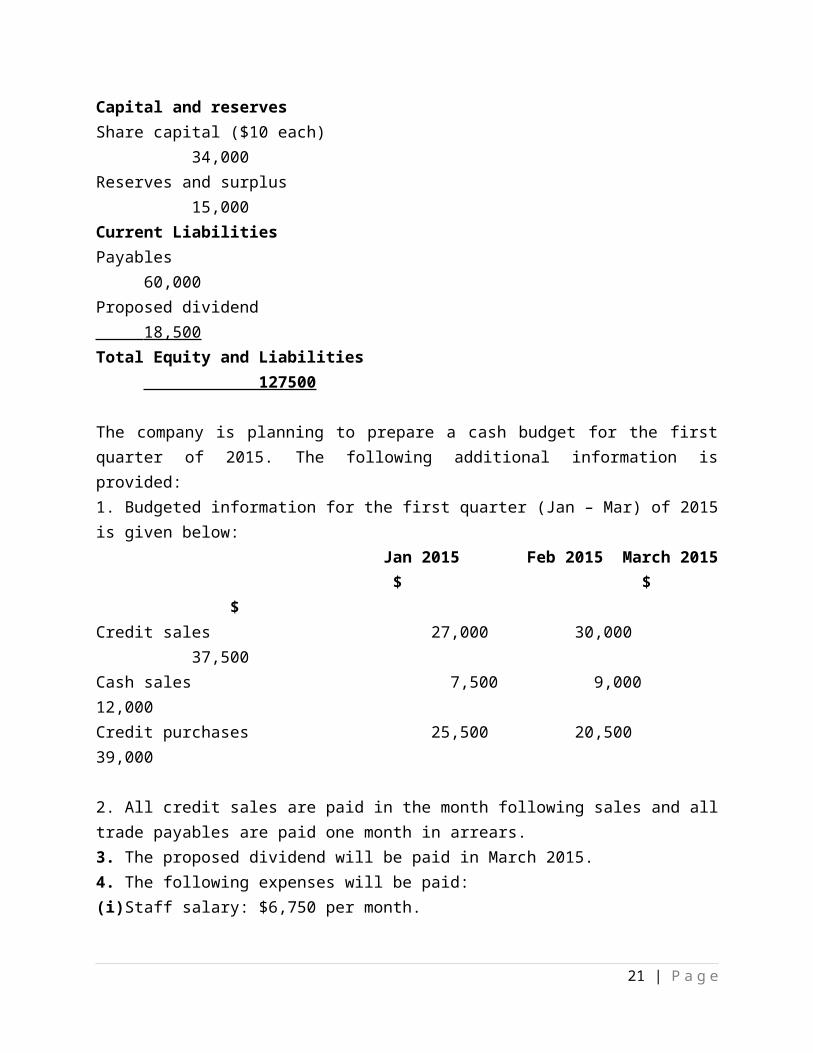

Equity and Liabilities

Capital and reservesShare capital ($10 each) 34,000Reserves and surplus 15,000Current LiabilitiesPayables 60,000Proposed dividend 18,500 Total Equity and Liabilities 127500

The company is planning to prepare a cash budget for the first quarter of 2015. The following additional information is provided:1. Budgeted information for the first quarter (Jan – Mar) of 2015 is given below:

Jan 2015 Feb 2015 March 2015 $ $ $Credit sales 27,000 30,000 37,500Cash sales 7,500 9,000 12,000Credit purchases 25,500 20,500 39,000

2. All credit sales are paid in the month following sales and all trade payables are paid one month in arrears.3. The proposed dividend will be paid in March 2015.4. The following expenses will be paid:(i)Staff salary: $6,750 per month.(ii) Rent of $15,400 for the first quarter of 2015 will be paid in January 2015.5. Depreciation on the plant and machinery will be provided @10% per annum.

RequiredPrepare a cash budget for the first quarter of 2015

15 | P a g e

1.12 Budgeted Statement of Comprehensive Income (BSOCI) It is prepared after the various operating budgets have been drawn up.

It includes the sales budget, purchases budget, production budget and expenses budget.

It shows the projected profit according to the estimates for the planned period.

1.13 Budgeted Statement of Financial Position (BSOFP) This budget exercises control over the accuracy of all the other budgets.

It shows the closing balances of all assets, liabilities and shareholders’ funds as reflected in the

budgets prepared by different departments.

Once the BSOCI and BSOFP are complete, ratios for analysis and interpretation purposes can be

calculated.

ACTIVITY 2

MASTER BUDGET-QUESTION

Company XYZ commences trading on 1 June 2014 with a capital of $240 000. The following estimates have been made.

(a) Plant and Equipment costing $160 000 will be purchased and installed prior to the commencement of business. The plant and equipment is payable in June 2014 and will be depreciated on a straight line basis over 8 years.

(b)On 1 June 2014 an initial inventory of goods will be purchased for $96 000 payable in July. All goods sold from 1 June will be replaced immediately. Purchases will be on 2 months credit.

(c)Gross Profit will be 331/3% of cost of goods.

(d)Forecast sales for the first three months are;

June $92 000, July $108 000, August $124 000

Sales are on credit payable in the month following sale.

(e) Rent and rates of $32 000 for 12 months from 1 June are payable in July.

(f) Wages and other Overheads commencing in June are estimated at $24 000 per month. 50% will be paid in the month incurred with the balance payable in the following month.

Required

16 | P a g e

(a) A Cash Budget for each of the 3 months June, July and August 2014(b) A Budgeted Income Statement for the 3 months ending 31 August 2014.(c) A budgeted Statement of Financial Position as at 31 December 2014.

1.2 FIXED AND FLEXIBLE BUDGETSFixed budgets remain unchanged regardless of the level of activity. Flexible budgets are designed to change with the level of activity. Flexible budgets are prepared using marginal costing and so mixed costs must be split into fixed and variable components (possibly using the high –low method).

1.2.1 Fixed Budgets The master budget prepared before the beginning of the budget period is known as the fixed

budget.

The term fixed means the following:

1. The budget is prepared on the basis of an estimated volume of production and estimated volume of sales but no plans are made for the event that actual volumes of production and sales may differ from budgeted volumes.2. When actual volumes of production and sales during a control period are achieved, a fixed budget is not adjusted in retrospect to represent a new target for the new levels of activity.

The major purpose of a fixed budget lies in its use at the planning stage, when it seeks to define

the broad objectives of an organization.

It is also used for controlling any fixed costs and particularly non-production fixed costs such as

advertising because such costs should be unaffected by changes in the levels of activity (within a

certain range).

A disadvantage of fixed budgets is that they are not adjusted for changes in activity levels.

Thus where budgeted output differs from actual output, a meaningful comparison cannot be

made between actual and budgeted expenditure to establish variances for control purposes.

A fixed budget is however useful for controlling costs where the objective is to limit the level of

expenditure.

1.2.2 Flexible Budgets Comparison of a fixed budget with actual results for a different level of activity is of little use for

budgetary control purposes.

Flexible budgets should be used to show what costs and revenues should have been for the actual

level of activity.

17 | P a g e

Differences between the flexed budget figures and the actual results are variances.

A flexible budget shows costs, revenues and resources for more than one level of activity so that

costs, etc can be predicted for other activity levels.

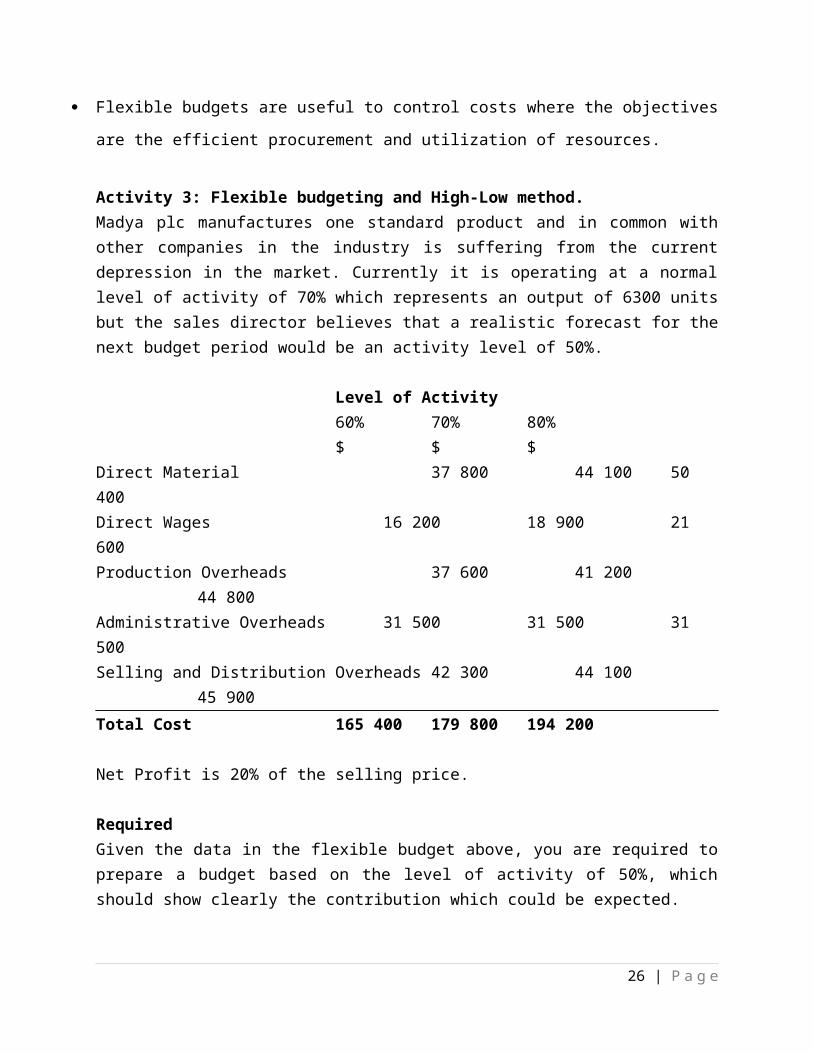

They are useful to control costs where the objectives are the efficient procurement and utilization

of resources.

It is designed to change as volume of activity changes.

1.2.2.1 Uses of flexible budgets1. Planning stage

A flexible budget can be prepared for different levels of activity and the possible outcomes

assessed.

2. Budgetary control At the end of each control period, flexible budgets are used to compare actual results achieved

with what the results should have been under the circumstances.

This is essential since businesses are dynamic and actual volumes of output cannot be expected

to conform exactly to the fixed budget.

Comparing actual costs directly with the fixed budget costs is meaningless.

Flexible budgets are useful to control costs where the objectives are the efficient procurement

and utilization of resources.

Activity 3: Flexible budgeting and High-Low method.Madya plc manufactures one standard product and in common with other companies in the industry is suffering from the current depression in the market. Currently it is operating at a normal level of activity of 70% which represents an output of 6300 units but the sales director believes that a realistic forecast for the next budget period would be an activity level of 50%.

Level of Activity60% 70% 80%$ $ $

Direct Material 37 800 44 100 50 400Direct Wages 16 200 18 900 21 600Production Overheads 37 600 41 200 44 800Administrative Overheads 31 500 31 500 31 500Selling and Distribution Overheads 42 300 44 100 45 900Total Cost 165 400 179 800 194 200

18 | P a g e

Net Profit is 20% of the selling price.

RequiredGiven the data in the flexible budget above, you are required to prepare a budget based on the level of activity of 50%, which should show clearly the contribution which could be expected.

END OF TOPIC NOTES

3. SHORT TERM TACTICAL DECISION MAKING

19 | P a g e

OBJECTIVESBy the end of the topic, the student should be able to:1. Identify and explain the term ‘relevant costs and revenues’ for short term decision making, giving practical examples.2. Apply relevant costing principles to compute costs and revenues and chose the appropriate alternatives under different decision making situations, including;(a)Make or buy decisions(b)Dropping a department or segment(c) Accepting or rejecting a special order(d)To decide on further processing decision particularly in relation joint product costs.(c) To determine product profitability3. Apply limiting factor analysis to determine the optimum production mix and calculate the resultant profit where there is only one limiting factor. 4. Formulate linear programming models and determine optimum production mix where there is more than one constraint using the following techniques:(a) Graphical method(c)Simultaneous equations method(d) Simplex method.5. Interpret the output of a computer programme under the simplex method.6. Explain and compute shadow prices, surpluses and slack in a linear programming solution.

1.0 RELEVANT COST Any cost that is useful for decision making is often referred to as a relevant cost.

A cost is said to be relevant provided there is a future cash flow arising from a direct

consequence of a decision.

(a) Relevant costs are future costs: A decision is about the future; it cannot alter what has been done already.

Therefore all historic costs/sunk costs are irrelevant for decision making.

Costs that are the subject of legally binding contracts, even if payments due under the

contract have not yet been made are also irrelevant (committed costs).

Past costs are only useful as long as they provide information for forecasting.

(b) Relevant costs are cash flows: Only cash flow information is required.

In essence, any cost or charge that fails to reflect additional cash spending should be

excluded.

20 | P a g e

These include: Depreciation as a fixed overhead incurred, Notional rent or interest, as

fixed overhead incurred and all overheads absorbed.

Fixed overhead absorption is always irrelevant, since it is overheads to be incurred which

affect decisions.

(c) Relevant costs are incremental or differential costs A relevant cost is one which arises as a direct consequence of a decision

Thus, only costs which will differ under some or all of the available opportunities should

be considered.

Thus, relevant costs are sometimes referred to as incremental or differential costs.

A differential cost is the difference between the incremental costs of the different options

(d) Relevant costs are opportunity costs

An opportunity cost is the benefit of the next best alternative that is forgone:

1.2 CLOSING DOWN A PRODUCT LINE OR BUSINESS The general decision criteria, on financial grounds, are that;

1. If a product or a division is making a positive contribution towards common (general)

fixed costs, then it should not be closed.

2. If there are fixed costs specifically incurred for a division or a product, then those fixed

costs become relevant costs and net contribution should be calculated.

ACTIVITY 1

The following information, organised on departmental basis, has been gathered from the accounts of Chika-Chika Engineering Limited Departments X Y Z $ $ $Variable costs 90,000 100,000 150,000Fixed costs:(apportioned on the 20,000 30,000 50,000basis of sales)Total Costs 110,000 130,000 200,000Sales 100,000 150,000 250,000Profit (Loss) (10,000) 20,000 50,000

21 | P a g e

With the object of doing away with departments incurring a loss, the management asks for your opinion on:(a) The closure of Department X on the basis of the above information.(b) The comparative profitability of different departments if specific fixed costs are ascertained to be $5,000 for Department X, $55,000 for Department Y and $30,000 for Department Z, the remaining $10,000 being general fixed costs.

Required:Prepare appropriate statements so as to help management in arriving at a decision on the above points. Also give your comments, explaining the position presented in the statements.

1.3 MAKE OR BUY DECISIONS This type of situation arises when a manufacturer is faced with the decision as to

whether:

(a) to manufacture one of its components in-house, or(b) to buy such components from an outside supplier.

The decision maker will be interested in the difference between the suppliers quotation

and the cost of producing in-house.

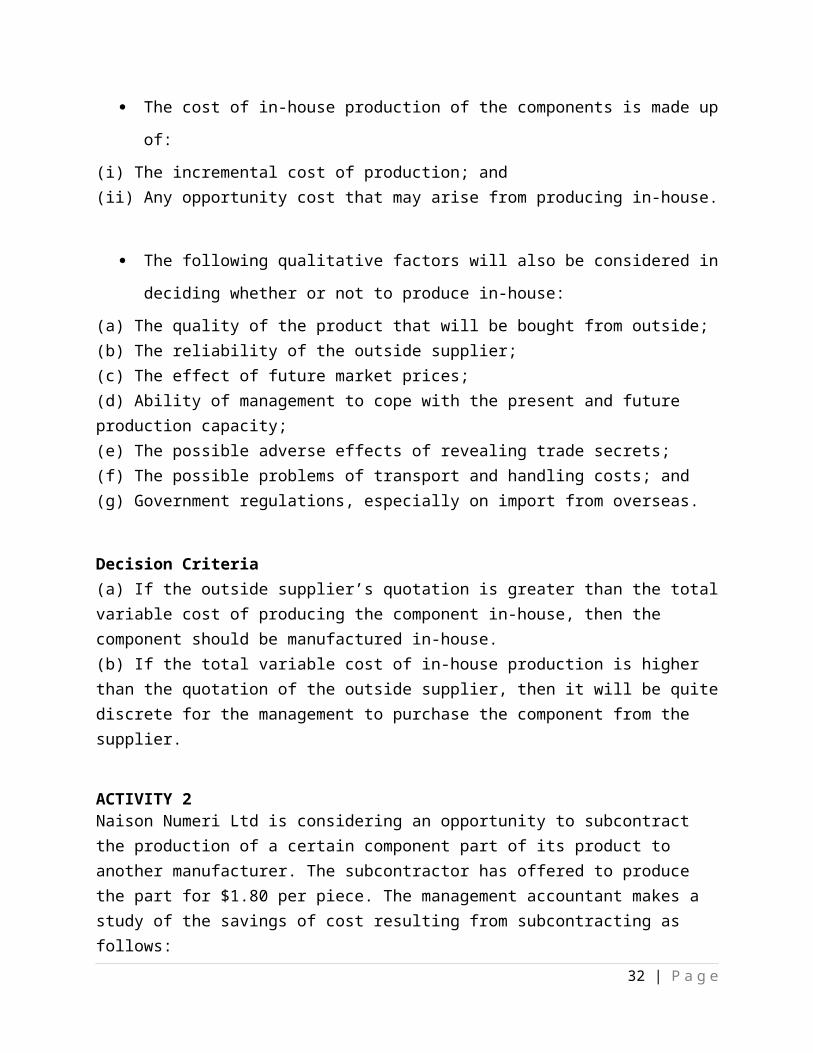

The cost of in-house production of the components is made up of:

(i) The incremental cost of production; and(ii) Any opportunity cost that may arise from producing in-house.

The following qualitative factors will also be considered in deciding whether or not to

produce in-house:

(a) The quality of the product that will be bought from outside;(b) The reliability of the outside supplier;(c) The effect of future market prices;(d) Ability of management to cope with the present and future production capacity;(e) The possible adverse effects of revealing trade secrets;(f) The possible problems of transport and handling costs; and(g) Government regulations, especially on import from overseas.

Decision Criteria(a) If the outside supplier’s quotation is greater than the total variable cost of producing the component in-house, then the component should be manufactured in-house.

22 | P a g e

(b) If the total variable cost of in-house production is higher than the quotation of the outside supplier, then it will be quite discrete for the management to purchase the component from the supplier.

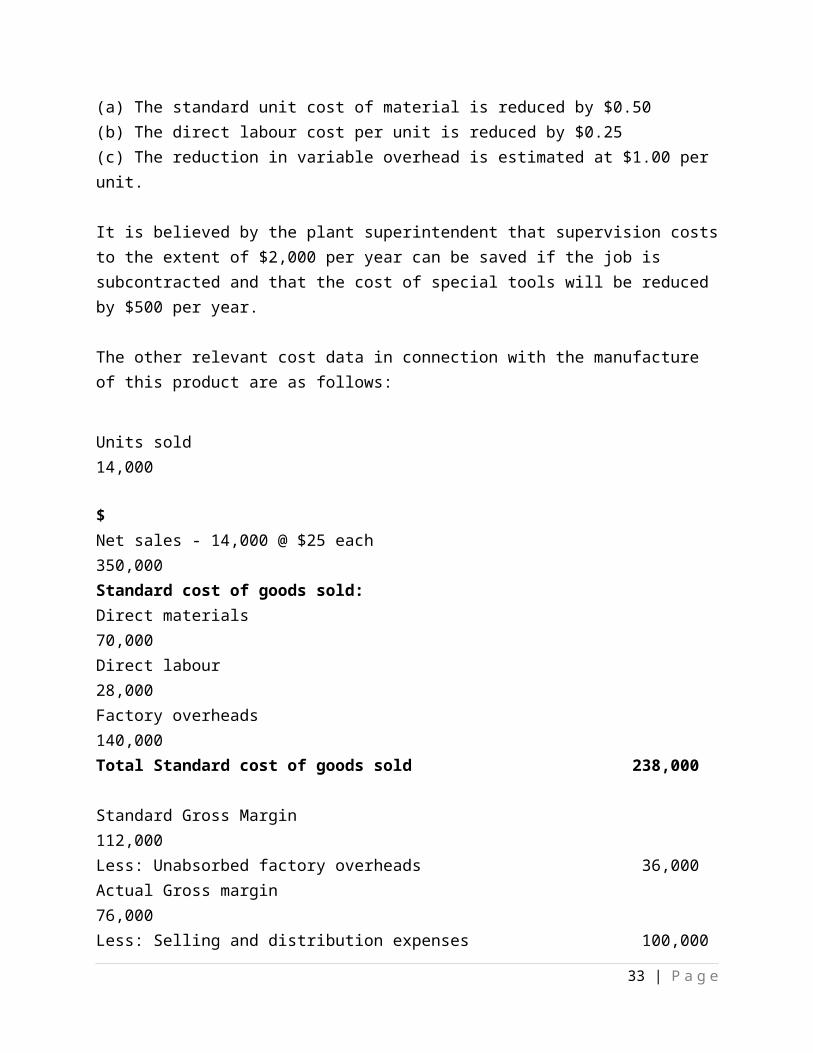

ACTIVITY 2Naison Numeri Ltd is considering an opportunity to subcontract the production of a certain component part of its product to another manufacturer. The subcontractor has offered to producethe part for $1.80 per piece. The management accountant makes a study of the savings of cost resulting from subcontracting as follows:(a) The standard unit cost of material is reduced by $0.50(b) The direct labour cost per unit is reduced by $0.25(c) The reduction in variable overhead is estimated at $1.00 per unit.

It is believed by the plant superintendent that supervision costs to the extent of $2,000 per year can be saved if the job is subcontracted and that the cost of special tools will be reduced by $500 per year.

The other relevant cost data in connection with the manufacture of this product are as follows:

Units sold 14,000 $Net sales - 14,000 @ $25 each 350,000Standard cost of goods sold:Direct materials 70,000Direct labour 28,000Factory overheads 140,000Total Standard cost of goods sold 238,000

Standard Gross Margin 112,000Less: Unabsorbed factory overheads 36,000Actual Gross margin 76,000Less: Selling and distribution expenses 100,000Net Loss (24,000)

The break-up of factory overheads into their fixed and variable components at normal capacity level of 20,000 units is as follows: Per Unit Total $ $

Variable 4 80,000Fixed 6 120,000

23 | P a g e

10 200,000

The company is working at less than normal capacity which is manufacture of 20,000 units of this product.

You are required to advise management on whether to subcontract the production of the component or to produce it internally.

1.4 ACCEPTANCE/REJECTION OF A SPECIAL ORDER

This type of situation arises when a company receives an order from a customer at a price

lower than its normal selling price.

The company, if working below capacity, may be advised to accept the offer after taking

into consideration the marginal cost of its production.

Therefore if the answer to the following questions are in affirmative, the special price

quoted by the customer should be accepted:

(a) Does the price quoted by the special customer cover the marginal cost of production?

(b) Does the company have excess capacity?

ACTIVITY 3Chaka Limited manufactures a special product for ladies called ‘the slimming stick‟. A stick sells for $0.20 per unit. Current output is 400,000 sticks which represents 80% level of activity. A customer Gwaya Stores Limited, recently, placed an order for 100,000 sticks at $0.13 per unit. The total cost for the period were $56,000 of which $16,000 were fixed costs. This represents a total cost of $0.14 per slimming stick.

Required:(a) Based on the above information, advise Chaka Limited whether or not to accept the offer.(b) What other factors may be taken into consideration in taking this type of decision?

ACTIVITY 4 Basket Ltd which manufactures rubber soles for use in its production cycle has the following unit cost for production of 40,000 units. $Director labour 30 Direct material 8 Manufacturing overheads 36 74

75% of the manufacturing overhead is fixed. Best Ltd has offered to sell 40,000 units of the rubber soles to Basket Ltd for $55 per unit. If Basket accepts the offer, part of the facilities

24 | P a g e

presently used to manufacture the rubber shoes could be rented to Karima Ltd at a rent of $72,000. Also, $10 per unit of the fixed overhead costs applied to the rubber shoes would be avoided.

The Managing Director, Munya Dexter has called you to advise him on whether or not to accept the offer. You are also required to state other matters that should be noted before taking the decision.

1.5 ALLOCATION OF SCARCE RESOURCES/LIMITING FACTOR ANALYSIS If management is faced with scarcity of a factor of production (termed a limiting or key

factor), it must ensure that the affected factor of production is used in such a way that profits per

unit of the factor automatically secure maximum profit.

In order to maximise profit, contribution should be maximised. In order to maximise

contribution, products should be produced in the order of their contribution per limiting factor.

ACTIVITY 5Dadirai Kasi Ltd manufactures and sells three products: P, Q and R. For the period ended 31 December, 2014, the following data were obtained from the company: P Q ROutput/Sales volume 4,000 units 3,000 units 3,000unitsSelling Price/unit $50 $30 $20Variable cost/unit $15 $20 $15Fixed cost of $100,000 are absorbed on the basis of labour hours which were: P ($2,000), Q ($1,500) and R ($1,500).

Assuming the company is faced with reduced machine hours since its plant is getting old. It has been estimated that it takes:5 machine hours to produce a unit of P, 2 machine hours to produce a unit of Q and 0.5 machine hour to produce a unit of R

The company is planning to replace its plant with a new one, but this can only be ready for operation in January, 2015. Before then the plant can only be used for 30 hours in a week instead of the normal 45 hours per week. Management wants to reconsider the allocation of this scarce resource. Advise management.

1.6 LINEAR PROGRAMMING

1.6.0 Introduction

25 | P a g e

Key budget factors sometimes known as a limiting factor or principal budget factor. This is a factor which is a binding constraint upon the organization, that is, the factor which restricts indefinite expansion or unlimited profits. It may be sales, availability of finance, skilled labour, supplies of material or lack of space. The 'maximizing contribution per unit of the limiting factor' rule can be of value, but can only work when there is one limiting factor. Where more than one limiting factor (constraint) exists, a mathematical technique known as linear programming can be used to establish the optimal solution. It is a method of solving equations and can be programmed for computer so that difficult and multi-constraint problems will show how scarce resources in a firm can best be utilized. It is a procedure to optimize the value of some objectives, for example, maximize profits or minimize costs when the factors involved (for example, labour or machine hours) are subject to some constraints. A general statement of a Linear Programming Model consists of three basic components or elements. These elements are the Decision variables, Objective function and constraints.

1.6.1 Assumptions of LP The basic assumptions underlying the operation of the technique are: (a) Certainty: It is believed that all relevant information relating to a problem situation are known, for example, the resources available. (b) Linearity: It is believed that there is a proportional relationship between the resources utilized and the contribution or the cost incurred. (c) Non-Negativity: There is no negative output that will be produced, that is, at worst we achieve zero level of production. (d) Single-Objective: There is an assumption of only one economic objective, which is maximization of profit or minimization of costs. (e) Divisibility: It is generally believed that fractional output could be produced, that is, all the variables are assumed to be completely divisible.

1.6.2 Methods of Linear Programming Three main methods of solving linear programming problem are: (a) Graphical solution method. (b) Algebraic or Simultaneous Solution method. (c) Simplex Solution method.

1.6.3 Formulating the problem

Steps in Linear Programming

The steps involved are as follows.1. Define variables2. Construct objective function3. Establish constraints

26 | P a g e

4. Graph constraints5. Establish feasible region6. Add iso-profit/contribution line7. Determine optimal solution

ACTIVITY 6

Brunel manufactures plastic-covered steel fencing in two qualities, standard and heavy gauge. Both products pass through the same processes, involving steel-forming and plastic bonding.

Standard gauge fencing sells at $18 a roll and heavy gauge fencing at $24 a roll. Variable costs per roll are $16 and $21 respectively. There is an unlimited market for the standard gauge, but demand for the heavy gauge is limited to 1,300 rolls a year. Factory operations are limited to 2,400 hours a year in each of the two production processes.

Processing hour per rollGauge Steel-forming Plastic-bondingStandard 0.6 0.4Heavy 0.8 1.2

What is the production mix which will maximize total contribution and what would be the total contribution?

ACTIVITY 7Minimisation problems

Although decision problems with limiting factors usually involve the maximisation of contribution, there may be a requirement to minimise costs. A graphical solution, involving two variables, is very similar to that for a maximisation problem, with the exception that instead of finding a contribution line touching the feasible area as far away from the origin as possible, we look for a total cost line touching the feasible area as close to the origin as possible.

Claire Speke has undertaken a contract to supply a customer with at least 260 units in total of two products, X and Y, during the next month. At least 50% of the total output must be units of X. The products are each made by two grades of labour, as follows.

X YHours Hours

Grade A labour 4 6Grade B labour 4 2Total 8 8

27 | P a g e

Although additional labour can be made available at short notice, the company wishes to make use of 1,200 hours of Grade A labour and 800 hours of Grade B labour which has already been assigned to working on the contract next month. The total variable cost per unit is $120 for X and $100 for Y.

Claire Speke wishes to minimise expenditure on the contract next month. How much of X and Y should be supplied in order to meet the terms of the contract?

1.6.4 SLACK AND SURPLUSSlack occurs when maximum availability of a resource is not used. Surplus occurs when more than a minimum requirement is used.

If, at the optimal solution, the resource used equals the resource available there is no spare capacity of a resource and so there is no slack.If a resource which has a maximum availability is not binding at the optimal solution, there will be slack.

ACTIVITY 8

A machine shop makes boxes (B) and tins (T). Contribution per box is $5 and per tin is $7. A box requires 3 hours of machine processing time, 16kg of raw materials and 6 labour hours. A tin requires 10 hours of machine processing time, 4kg of raw materials and 6 labour hours. In a given month, 330 hours of machine processing time are available, 400kg of raw material and 240 labour hours. The manufacturing technology used means that at least 12 tins must be made every month. The constraints are:

3B + 10T ≤ 33016B + 4T ≤ 4006B + 6T ≤ 240T ≥ 12

The optimal solution is found to be to manufacture 10 boxes and 30 tins.Required:Determine the slack/surplus in the constraints above.

1.6.5 SHADOW PRICES

The shadow price or dual price of a limiting factor is the increase in value which would

be created by having one additional unit of the limiting factor at the original cost.

The shadow price is the increase in contribution created by the availability of an

extra unit of a limited resource at its original cost.

ACTIVITY 9

28 | P a g e

Let us suppose that WX manufactures two products, A and B. Both products pass through two production departments, mixing and shaping. The organisation's objective is to maximise contribution to fixed costs.

Product A is sold for $1.50 whereas product B is priced at $2.00. There is unlimited demand for product A but demand for B is limited to 13,000 units per annum. The machine hours available in each department are restricted to 2,400 per annum. Other relevant data are as follows.

Machine hours required Mixing ShapingHrs Hrs

Product A 0.06 0.04Product B 0.08 0.12

Variable cost per unit $Product A 1.30Product B 1.70

The objective function is:Contribution (C) = 0.2x + 0.3y

The constraints are:0.06x + 0.08y ≤ 2,4000.04x + 0.12y ≤ 2,4000 ≤ y ≤ 13,0000 ≤ x

RequiredDetermine the shadow price for shaping time in the scenario above.

1.6.6 SIMPLEX METHOD A linear programming problem with more than two decision variables (e.g. more than two products) cannot be plotted on the two axes of a graph. Therefore, we need a different method of solving the problem: the Simplex method. The Simplex method begins in the same way, by setting up equations for the objective function and the constraints. You should be able to formulate the problem for the exam but will not be expected to solve it.

ACTIVITY 10Wood Ltd is a furniture company that specialises in high-quality products. The company can manufacture four different types of coffee table (small, medium, large and ornate). Each type of table requires time for the cutting of the component parts, for assembly and for finishing. The data in the table below has been collected for the year now being planned.

Hours per table

29 | P a g e

Table Cutting Assembly Finishing Contribution per table($)

Small 2 5 1 60Medium 2 4 4 123Large 1 3 5 135Ornate 6 2 3 90Capacity in hours 3000 9000 4950Owing to other commitments, no more than a total of 1,800 coffee tables can be made in any given year. Also, market analysis reveals that the annual demand for the company’s small coffee table is at least 800.

Required:

Determine how many of each type of coffee table it should produce in the coming year to maximise contribution.

Simplex solution for Wood

Objective function variable (z): 168,750.0000

Variable Value Relative loss

a 950.0000 0.0000

b 250.0000 0.0000

c 3 600.0000 0.0000

d 4 0.0000 48.0000

Constraint Slack/surplus Worth

1 0.0000 9.0000

2 1,450.0000 0.0000

3 0.0000 21.0000

4 0.0000 21.0000

5 150.0000 0.0000

30 | P a g e

Although you will not have to solve a Simplex problem you should be able to interpret the results:

Required:

Interpret the simplex solution for Wood above

END OF TOPIC NOTES

31 | P a g e

4. CAPITAL INVESTMENT DECISIONS

OBJECTIVES

By the end of the topic, students should be able to:

1. Describe the capital budgeting process and explain the role of investment appraisal in that process.

2. Evaluate and use non-discounted cash flow methods to choose between alternative projects i.e. Accounting Rate of Return (ARR) and Payback method.

3. Explain the concept of relevant cash flows, giving practical examples and calculate relevant cash flows in given capital investment decision scenarios.

4. Evaluate and use discounted cash flow methods to choose between alternative projects i.e. Net Present Value method(NPV), Internal Rate of Return method(IRR) and Discounted Payback method.

5. Compare the NPV method and IRR method and justify why the NPV method is considered to be superior.

6. Adjust cash flows for inflation in capital investment decisions.

7. Adjust cash flows for the effect of tax in capital investment decisions.

8. Compute the Profitability Index (PI) and use it to allocate capital between different projects in capital rationing situations under the following scenarios;

(a) Single period capital rationing

(b) Divisible and non-divisible projects

(d) Dependent and mutually exclusive projects.

1.0 INTRODUCTION

Capital budgeting can be explained in the context of a firm's decision to invest its current funds in long term activities in anticipation of an expected flow of future benefits over a number of years.

However, the investment decisions could be in the form of acquisition of additional fixed assets, replacements and modifications of activities and expansion of plant.

1.1 CAPITAL AND REVENUE EXPENDITURE Investment is any expenditure in expectation of future benefits.

32 | P a g e

It can be divided into two categories namely; revenue expenditure and capital expenditure.

Capital expenditure is expenditure that results in the acquisition of a non-current asset or improvement of the earning capacity of a non-current asset.

The expenditure appears as a non-current asset in the statement of financial position. Revenue expenditure refers to the expenditure that is incurred in the day to day running

of a business. It includes expenditure that is classified as selling and distribution expenses,

administration expenses and finance charges. It is thus expenditure incurred in order to maintain the existing earning capacity of a non-

current asset. It appears as an expense in the income statement.

ACTIVITY 1Suppose that a business purchases a building for $30,000. It then adds an extension to the building at a cost of $10,000. The building needs to have a few broken windows mended, its floors polished and some missing roof tiles replaced. These cleaning and maintenance jobs cost $900.Required:Determine the amount of capital expenditure and revenue expenditure

Investment can be made in non-current assets or working capital. Investment in non-current assets involves a significant time lag between the commitment

of funds and the recoupment of the investment. Thus, money is paid out in order to acquire resources that will be used on a continuing

basis within the organisation. Investment in working capital arises from the need to pay out money for resources before

it can be recovered from the sale of the finished product or service. The funds are therefore only committed for a short period of time.

1.2 THE CAPITAL BUDGETING PROCESS

Capital budgeting is the process of identifying, analyzing and selecting investment projects whose returns are expected to extend beyond one year.

The capital budget should therefore be based on the current production budget, future expected levels of production and the long-term development of the organisation, and industry, as a whole.

Such a capital budget therefore shows the expected investment in non-current assets and other long term investments.

The administration of the capital budget is usually separate from that of the other budgets.

Overall responsibility for authorisation and monitoring of capital expenditure is, in most large organisations, the responsibility of a committee.

Capital expenditure often involves the outlay of large sums of money, and that any expected benefits may take a number of years to accrue.

33 | P a g e

For these reasons it is vital that capital expenditure is subject to a rigorous process of appraisal and control.

A typical model for investment decision making/capital budgeting process has a number of distinct stages which are as follows:

(i)Origination of proposals(ii)Project screening(iii)Analysis and acceptance(iv)Monitoring and review

1.2.1 Origination of proposals New project ideas usually come from a system of environmental scanning or from

various departments within the organisation. They may also come from the top management who usually have a strategic view of the

organisation’s direction and greater knowledge of the competitive environment.

1.2.2 Project Screening Each proposal must be subject to detailed screening. So that a qualitative evaluation of a proposal can be made, a number of key questions

such as those below might be asked before any financial analysis is undertaken.

(i)What is the purpose of the project?(ii)Does it 'fit' with the organisation's long-term objectives?(iii)Is it a mandatory investment, for example to conform with safety legislation?(iv)What resources are required and are they available, eg money, capacity, labour?(v)Do we have the necessary management expertise to guide the project to completion?(vi) Does the project expose the organisation to unnecessary risk?(vii)How long will the project last and what factors are key to its success?(viii)Have all possible alternatives been considered?

Only if the project passes this initial screening will more detailed financial analysis begin.

1.2.3 Analysis and Acceptance. This stage involves submitting an investment proposal in the form of financial

information about a project. Such financial information includes the cost of the investment and the expected cash

inflows over the life of the project. The project is then classified into either high risk or low risk investment and a financial

analysis is carried out. The financial analysis will involve the use of one or more of the investment appraisal

techniques that will be discussed later. The results of the financial analysis are then compared to the predetermined acceptance

criteria.

34 | P a g e

If the project qualifies, it is then assessed in the light of the capital budget for the current and future operating periods in deciding whether to carry on with the project or to abandon it. This is a stage known as investment appraisal.

Before the final decision is made additional qualitative factors might need to be considered and these include the following;

(a) What are the implications of not undertaking the investment, eg adverse effect on staff morale, loss of market share?(b) Will acceptance of this project lead to the need for further investment activity in future?(c) What will be the effect on the company's image?(d) Will the organisation be more flexible as a result of the investment, and better able to respond to market and technology changes?

Once a decision is made to accept a project, the organisation is committed to the project, and the decision maker must accept that the project’s success or failure reflects on his or her ability to make sound decisions.

1.2.4 Monitoring the progress of the project

During the project's progress, project controls should be applied to ensure the following.(i)Capital spending does not exceed the amount authorised.(ii)The implementation of the project is not delayed.(iii)The anticipated benefits are eventually obtained.

1.3 INVESTMENT APPRAISAL TECHNIQUES

Are the techniques used to determine whether to accept or reject a project based on financial grounds?

They are classified into two categories namely; non-discounted cash flow techniques (ARR and Payback) and the discounted cash flow techniques (NPV, IRR and the Discounted Payback).

1.3.1 ACCOUNTING RATE OF RETURN (ARR)

It is the only investment appraisal technique which uses accounting profits. It is also called the ROCE or ROI. It is used to estimate the accounting rate of return that a project should yield. It is calculated as follows;

ROCE = Estimated average annual accounting profits/Estimated average investment x100%

Average investment = (Capital cost+disposal value)/2

Unfortunately, there are several different definitions of 'return on capital employed.

35 | P a g e

Others include;:ROCE =Estimated total profits/Estimated initial investmentx100%

ROCE =Estimated Average profits/Estimated initial investmentx100%

There are arguments in favour of each of these definitions. The most important point is, however, that the method selected should be used

consistently. For examination purposes we recommend the first definition unless the question clearly

indicates that some other one is to be used.

Decision criteria A project should be accepted if its estimated ARR is greater than the hurdle or target

ARR For mutually exclusive projects, the project with the highest ROCE would be selected

(provided that the expected ROCE is higher than the company's target ROCE).

ACTIVITY 2A company has a target return on capital employed of 20% (using the first definition from the paragraph above), and is now considering the following project.Capital cost of asset $80,000Estimated life 4 yearsEstimated profit before depreciationYear 1 $20,000Year 2 $25,000Year 3 $35,000Year 4 $25,000The capital asset would be depreciated by 25% of its cost each year, and will have no residual value. You are required to assess whether the project should be undertaken.

ACTIVITY 3

Asante wants to buy a new item of equipment which will be used to provide a service to customers of the company. Two models of equipment are available, one with a slightly higher capacity and greater reliability than the other. The expected costs and profits of each item are as follows.

Equipment item X Equipment item YCapital cost $80,000 $150,000Life 5 years 5 yearsProfits before depreciation $ $Year 1 50,000 50,000Year 2 50,000 50,000Year 3 30,000 60,000Year 4 20,000 60,000Year 5 10,000 60,000

36 | P a g e

Disposal value 0 0

ROCE is measured as the average annual profit after depreciation, divided by the average net book value of the asset. You are required to decide which item of equipment should be selected, if any, if the company's target ROCE is 30%

Advantages of ARR as a capital investment appraisal method

(a) It is a quick and simple calculation.(b) It involves the familiar concept of a percentage return.(c) It looks at the entire project life.

Disadvantages of the ARR(aa)It does not take into account the timing of the profits from an investment(a) It is based on accounting profits and not cash flows. Accounting profits are subject to a number of different accounting treatments.(b) It is a relative measure rather than an absolute measure and hence takes no account of the size of the investment.(c) It takes no account of the length of the project.(d) Like the payback method, it ignores the time value of money.

Since all other capital investment appraisal methods use cash flows it is important to look closely at the concept of relevant cash flow.

1.3.2 RELEVANT CASH FLOW

The relevant costs for decision making are those costs that are affected or affect the decision at hand.

Thus relevant costs are 1. Cash flows 2. Incremental cash flows 3. Differential cash flows.

This means that past costs (sunk costs), committed costs, centrally allocated overheads are irrelevant costs because they won’t change as a result of undertaking a project.

Non-cash items like depreciation are also irrelevant because no cash is involved. Relevant costs for an investment also include opportunity costs. These are the costs incurred or revenues lost from diverting existing resources from their

best use.

ACTIVITY 4A salesman, who is paid an annual salary of $30,000, is diverted to work on a new project and as a result existing sales of $50,000 are lost. What is the relevant cost of the new project?

Relevant benefits from investments include increased cash flows, cost savings and better relationships with customers and employees.

37 | P a g e

ACTIVITY 5Tamuka is considering the manufacture of a new product which would involve the use of both a new machine (costing $150,000) and an existing machine, which cost $80,000 two years ago and has a current net book value of $60,000. There is sufficient capacity on this machine, which has so far been under-utilised.

Annual sales of the product would be 5,000 units, selling at $32 per unit. Unit costs would be as follows.

$Direct labour (4 hours at $2 per hour) 8Direct materials 7Fixed costs including depreciation 9

24

The project would have a five-year life, after which the new machine would have a net residual value of $10,000. Because direct labour is continually in short supply, labour resources would have to be diverted from other work which currently earns a contribution of $1.50 per direct labour hour. The fixed overhead absorption rate would be $2.25 per hour ($9 per unit) but actual expenditure on fixed overhead would not alter. Working capital requirements would be $10,000 in the first year, rising to $15,000 in the second year and remaining at this level until the end of the project, when it will all be recovered. The company's cost of capital is 20%. Ignore taxation.

Required Identify the relevant cash flows for the decision as to whether or not the project is worthwhile.

1.3.3 PAYBACK METHOD

Payback period is the time it takes the cash inflows from a capital investment project to equal the cash outflows, usually expressed in years.

Since earlier cash flows are better than later cash flows, projects with shorter payback periods are preferred.

Decision criteria Accept a project with a payback period that is less than the targeted payback.

ACTIVITY 6: A project with an exact number of years in payback

$Initial outlay 700Cash inflows Year 1 400

2 3003 2004 100

ACTIVITY 7: A project with inexact number of years in payback

38 | P a g e

P=E+B/C-where P stands for payback period E stands for number of years immediately preceding the year of final recovery B stands for the balance amount still to the recovered C stands for cash flow during the year of final recovery

$Initial outlay 700Cash inflows Year 1 400

2 2003 2004 100

Advantages of Payback

(a) It is simple to calculate and simple to understand.(b) It uses cash flows rather than accounting profits.(c) It can be used as a screening device as a first stage in eliminating obviously inappropriate projects prior to more detailed evaluation.(d) It helps to improve an organisation’s liquidity and cash flow since it favours projects with a shorter payback.(e) It can be used when there is a capital rationing situation to identify those projects which generate additional cash for investment quickly.Disadvantages(a) It ignores the timing of cash flows within the payback period.(b) It ignores the cash flows after the end of payback period and therefore the total project return.(c) It ignores the time value of money (a concept incorporated into more sophisticated appraisalmethods). This means that it does not take account of the fact that $1 today is worth more than $1 in one year's time. An investor who has $1 today can either consume it immediately or alternatively can invest it at the prevailing interest rate, say 10%, to get a return of $1.10 in a year's time.(d) Payback is unable to distinguish between projects with the same payback period.(e) The choice of any cut-off payback period by an organisation is arbitrary.(f) It may lead to excessive investment in short-term projects.(g) It takes account of the risk of the timing of cash flows but not the variability of those cash flows.

1.3.4 DISCOUNTED CASH FLOW (DCF) TECHNIQUES

There are two common methods of using DCF to evaluate capital investments, the NPV method and the IRR method.

DCF techniques are investment appraisal techniques that have the following features;1. They use cash flows rather than profits

39 | P a g e

2. They take into account the time value of money/the timing of cash flows. This concepts acknowledges that earlier cash flows have more value than later cash flows

because; they can be invested to earn returns, they are less affected by inflation, they are more

certain and are less risky. 1.3.4.1 Compounding

Suppose that a company makes an investment of $10 000 and expects to earn a return of 10% compound interest , the investment will build up as follows;

………… This process of finding the future value of an investment plus the accumulated interest

after n number of years is known as compounding and is done using the following formula:

FV=PV (1+r) ^n

Where FV is the future value of the investment with interestPV is the initial or 'present' value of the investmentr is the compound rate of return per time period, expressed as a proportion (so 10% = 0.10, 5% = 0.05 and so on)n is the number of time periods.

1.3.4.2 Discounting

While compounding starts with the present value and converts it into a future value by using the targeted rate of return, discounting starts with the future value of an investment and converts it into the present value.

Present value is the cash equivalent now of a sum of money receivable or payable at a stated future date, discounted at a specified rate of return.

ACTIVITY 8

If a company expects to earn a (compound) rate of return of 10% on its investments, how much would it need to invest now to have the following investments?(a) $11,000 after 1 year(b) $12,100 after 2 years(c) $13,310 after 3 years

The present value is calculated by using the formulae below;

PV=FV/((1+r)^n

Discounting can be applied to both money receivable and also to money payable at a future date. By discounting all payments and receipts from a capital investment to a present value, they can be compared on a common basis at a value which takes account of when the various cash flows will take place.

40 | P a g e

ACTIVITY 9

Spencer expects the cash inflow from an investment to be $40,000 after 2 years and another $30,000 after 3 years. Its target rate of return is 12%. Calculate the present value of these future returns, and explain what this present value signifies.

1.3.4.3 COST OF CAPITAL

The cost of capital has two aspects to it.(a) It is the cost of funds that a company raises and uses.(b) The return that investors expect to be paid for putting funds into the company.

It is therefore the minimum return that a company should make from its own investments, to earn the cash flows out of which investors can be paid their return.

The cost of capital can therefore be measured by studying the returns required by investors, and used to derive a discount rate for DCF analysis and investment appraisal.

1.3.5 THE NET PRESENT VALUE METHOD (NPV)

The NPV method compares the present value of all the cash inflows from an investment with the present value of all the cash outflows from an investment.

The NPV is thus calculated as the PV of cash inflows minus the PV of cash outflows. Thus the Net present value or NPV is the value obtained by discounting all cash

outflows and inflows of a capital investment project by a chosen target rate of return or cost of capital.

Decision criteria NPV positive MEANS Return from investment's cash inflows in excess of cost of capital

THEREFORE undertake project NPV negative MEANS Return from investment's cash inflows below cost of capital

THEREFORE don't undertake project NPV= 0 MEANS Return from investment's cash inflows same as cost of capital-

indifferentACTIVITY 10

A company is considering a capital investment, where the estimated cash flows are as follows.Year Cash flow

$0 (ie now) (100,000)1 60,0002 80,0003 40,0004 30,000The company's cost of capital is 15%. You are required to calculate the NPV of the project and to assess whether it should be undertaken.

41 | P a g e

1.3.5.1 Timing of cash flows: Conventions used in DCF

(a) A cash outlay to be incurred at the beginning of an investment project ('now') occurs in year 0. The present value of $1 now, in year 0, is $1 regardless of the value of r.(b) A cash outlay, saving or inflow which occurs during the course of a time period (say, one year) is assumed to occur all at once at the end of the time period (at the end of the year). Receipts of $10,000 during year 1 are therefore taken to occur at the end of year 1.(c) A cash outlay or receipt which occurs at the beginning of a time period (say at the beginning of one year) is taken to occur at the end of the previous year. Therefore a cash outlay of $5,000 at the beginning of year 2 is taken to occur at the end of year 1.

ACTIVITY 11

Makamba manufactures product X which it sells for $5 per unit. Variable costs of production are currently $3 per unit, and fixed costs 50c per unit. A new machine is available which would cost $90,000 but which could be used to make product X for a variable cost of only $2.50 per unit. Fixed costs, however, would increase by $7,500 per annum as a direct result of purchasing the machine. The machine would have an expected life of 4 years and a resale value after that time of $10,000. Sales of product X are estimated to be 75,000 units per annum. Makamba expects to earn at least 12% per annum from its investments.

Ignore taxation.

You are required to decide whether Makamba should purchase the machine.

1.3.5.2 Present value annuity factor

Where there is a constant cash flow from year to year, we can calculate the present value by adding together the discount factors for the individual years or by using the formula……….(present value annuity factor).

ACTIVITY 12

a) What is the present value of $1,000 in contribution earned each year from years 1-10, when the required return on investment is 11%?(b) What is the present value of $2,000 costs incurred each year from years 3-6 when the cost ofcapital is 5%?

Solution

(a) The PV of $1,000 earned each year from year 1-10 when the required earning rate of money is 11% is calculated as follows.$1,000 x 5.889 = $5,889(b) The PV of $2,000 in costs each year from years 3-6 when the cost of capital is 5% per annum is calculated as follows.

42 | P a g e

1.3.5.3 Annual cash flows in perpetuity

When the cost of capital is r, the cumulative PV of $1 per annum in perpetuity is $1/r.

ACTIVITY 13

An organisation with a cost of capital of 14% is considering investing in a project costing $500,000 that would yield cash inflows of $100,000 per annum in perpetuity.

RequiredAssess whether the project should be undertaken.

1.3.5.4 NPV and shareholder wealth maximisation

If a project has a positive NPV it offers a higher return than the return required by the company to provide satisfactory returns to its sources of finance.

This means that the company's value is increased and the project contributes to shareholder wealth maximisation.

1.3.6 THE INTERNAL RATE OF RETURN METHOD

The IRR method of investment appraisal is to accept projects whose IRR (the rate at which the NPV is zero) exceeds a target rate of return.

The IRR is calculated using interpolation. Without a computer or calculator program, the calculation of the internal rate of return is

made using a hit-and-miss technique known as the linear interpolation method.Step 1 Calculate the net present value using the company's cost of capital.Step 2 Having calculated the NPV using the company's cost of capital, calculate the NPV using asecond discount rate.(a) If the NPV is positive, use a second rate that is greater than the first rate(b) If the NPV is negative, use a second rate that is less than the first rateStep 3 Use the two NPV values to estimate the IRR. The formula to apply is as follows.

IRR=a+(NPVa/(NPVa-NPVb)X(b-a))

where a = the lower of the two rates of return usedb = the higher of the two rates of return usedNPVa = the NPV obtained using rate aNPVb = the NPV obtained using rate bNote. Ideally NPVa will be a positive value and NPVb will be negative. (If NPVb is negative, then in the equation above you will be subtracting a negative, ie treating it as an added positive).

ACTIVITY 14

A company is trying to decide whether to buy a machine for $80,000 which will save costs of $20,000 per annum for 5 years and which will have a resale value of $10,000 at the end of year

43 | P a g e

5. If it is the company's policy to undertake projects only if they are expected to yield a DCF return of 10% or more, ascertain whether this project be undertaken.

1.3.7 EVALUATION OF DCF TECHNIQUES AS A METHOD OF INVESTMENT APPRAISAL

Advantages

DCF is a capital appraisal technique that is based on a concept known as the time value of money: the concept that $1 received today is not equal to $1 received in the future.

Given the choice between receiving $100 today, and $100 in one year's time, most people would opt to receive $100 today because they could spend it or invest it to earn interest. If the interest rate was 10%, you could invest $100 today and it would be worth ($100 x 1.10) = $110 in one year's time.

There are, however, other reasons why a present $1 is worth more than a future $1.(a) Uncertainty. Although there might be a promise of money to come in the future, it can never be certain that the money will be received until it has actually been paid.(b) Inflation also means $1 now is worth more than $1 in the future because of inflation. The time value of money concept applies even if there is zero inflation but inflation obviously increases the discrepancy in value between monies received at different times. Taking account of the time value of money (by discounting) is one of the principal advantages of the DCF appraisal method. Other advantages are as follows.(i)The method uses all relevant cash flows relating to the project(ii)It allows for the timing of the cash flows(iii)There are universally accepted methods of calculating the NPV and the IRR

Disadvantages

Although DCF methods are theoretically the best methods of investment appraisal, you should be aware of their limitations.

(a) DCF methods use future cash flows that may be difficult to forecast. Although other methods use these as well, arguably the problem is greater with DCF methods that take cash flows into the longer-term.(b) The basic decision rule, accept all projects with a positive NPV, will not apply when the capital available for investment is rationed.(c) The cost of capital used in DCF calculations may be difficult to estimate.(d) The cost of capital may change over the life of the investment.

1.3.8 ADJUSTING FOR INFLATION

So far we have not considered the effect of inflation on the appraisal of capital investment proposals.

44 | P a g e

As the inflation rate increases so will the minimum return required by an investor. For example, you might be happy with a return of 5% in an inflation-free world, but if inflation were running at 15% you would expect a considerably greater yield.

The nominal interest rate is the interest rate that has not been adjusted for inflation while the real interest rate is one that has been adjusted for inflation.

The relationship between real and nominal rates of interest is given by the Fisher formula:

(1 + i) = (1 + r)(1 + h)Where h = rate of inflationr = real rate of interesti = nominal (money) rate of interest

ACTIVITY 15

A company is considering investing in a project with the following cash flows.Time Actual cash flows

$0 (15,000)1 9,0002 8,0003 7,000

The company requires a minimum return of 20% under the present and anticipated conditions. Inflation is currently running at 10% a year, and this rate of inflation is expected to continue indefinitely. Should the company go ahead with the project?

Let us first look at the company's required rate of return. Suppose that it invested $1,000 for one year on 1 January, then on 31 December it would require a minimum return of $200. With the initial investment of $1,000, the total value of the investment by 31 December must therefore increase to $1,200. During the course of the year the purchasing value of the dollar would fall due to inflation. We can restate the amount received on 31 December in terms of the purchasing power of the dollar at 1 January as follows. Amount received on 31 December in terms of the value of the pound at 1 January = $1,200/1.10 = $1,091

In terms of the value of the dollar at 1 January, the company would make a profit of $91 which represents a rate of return of 9.1% in 'today's money' terms. This is the real rate of return. The required rate of 20% is a nominal rate of return (sometimes called a money rate of return). The nominal rate measures the return in terms of the dollar which is, of course, falling in value. The real rate measures the return in constant price level terms.

Do we use nominal discount rate or real discount rate in investment appraisal?The rule is as follows.(a) If the cash flows are expressed in terms of the actual number of dollars that will be received or paid on the various future dates, we use the nominal rate for discounting.

45 | P a g e

(b) If the cash flows are expressed in terms of the value of the dollar at time 0 (that is, in constant price level terms), we use the real rate.

1.3.8.1 Costs and benefits which inflate at different ratesNot all costs and benefits will rise in line with the general level of inflation. In such cases, we can apply the nominal rate to inflated values to determine a project's NPV.