aup 1214 close 12-16-14 · how to analyze an automobile manufacturing company ... contacts:...

TRANSCRIPT

Please see General Disclaimers on the last page of this report.

Current Environment ............................................................................................ 1

Industry Profile .................................................................................................... 10

Industry Trends ................................................................................................... 12

How the Industry Operates ............................................................................... 22

Key Industry Ratios and Statistics ................................................................... 28

How to Analyze an Automobile Manufacturing Company .......................... 30

Glossary ................................................................................................................ 34

Industry References ........................................................................................... 36

Comparative Company Analysis ...................................................................... 37

This issue updates the one dated July 2014.

Industry Surveys Autos & Auto Parts Efraim Levy, CFA, Auto Manufacturers & Auto Parts Equity Analyst

DECEMBER 2014

CONTACTS:

INQUIRIES & CLIENT SUPPORT 800.523.4534 clientsupport@ standardandpoors.com

SALES 877.219.1247 [email protected]

MEDIA Michael Privitera 212.438.6679 [email protected]

S&P CAPITAL IQ 55 Water Street New York, NY 10041

Topics Covered by Industry Surveys

Aerospace & Defense

Airlines

Alcoholic Beverages & Tobacco

Apparel & Footwear: Retailers & Brands

Autos & Auto Parts

Banking

Biotechnology

Broadcasting, Cable & Satellite

Chemicals

Communications Equipment

Computers: Commercial Services

Computers: Consumer Services & the Internet

Computers: Hardware

Computers: Software

Electric Utilities

Environmental & Waste Management

Financial Services: Diversified

Foods & Nonalcoholic Beverages

Healthcare: Facilities

Healthcare: Managed Care

Healthcare: Pharmaceuticals

Healthcare: Products & Supplies

Heavy Equipment & Trucks

Homebuilding

Household Durables

Household Nondurables

Industrial Machinery

Insurance: Life & Health

Insurance: Property-Casualty

Investment Services

Lodging & Gaming

Metals: Industrial

Movies & Entertainment

Natural Gas Distribution

Oil & Gas: Equipment & Services

Oil & Gas: Production & Marketing

Paper & Forest Products

Publishing & Advertising

Real Estate Investment Trusts

Restaurants

Retailing: General

Retailing: Specialty

Semiconductors & Equipment

Supermarkets & Drugstores

Telecommunications

Thrifts & Mortgage Finance

Transportation: Commercial

Global Industry Surveys

Airlines: Asia

Autos & Auto Parts: Europe

Banking: Europe

Food Retail: Europe

Foods & Beverages: Europe

Media: Europe

Oil & Gas: Europe

Pharmaceuticals: Europe

Telecommunications: Asia

Telecommunications: Europe

S&P Capital IQ Industry Surveys 55 Water Street, New York, NY 10041

CLIENT SUPPORT: 1-800-523-4534

VISIT THE S&P CAPITAL IQ WEBSITE: www.spcapitaliq.com

S&P CAPITAL IQ INDUSTRY SURVEYS (ISSN 0196-4666) is published weekly. Redistribution or reproduction in whole or in part (including inputting into a computer) is prohibited without written permission. To learn more about Industry Surveys and the S&P Capital IQ product offering, please contact our Product Specialist team at 1-877-219-1247 or visit getmarketscope.com. Executive and Editorial Office: S&P Capital IQ, 55 Water Street, New York, NY 10041. Officers of McGraw Hill Financial: Douglas L. Peterson, President, and CEO; Jack F. Callahan, Jr., Executive Vice President, Chief Financial Officer; John Berisford, Executive Vice President, Human Resources; D. Edward Smyth, Executive Vice President, Corporate Affairs; and Lucy Fato, Executive Vice President and General Counsel. Information has been obtained by S&P Capital IQ INDUSTRY SURVEYS from sources believed to be reliable. However, because of the possibility of human or mechanical error by our sources, INDUSTRY SURVEYS, or others, INDUSTRY SURVEYS does not guarantee the accuracy, adequacy, or completeness of any information and is not responsible for any errors or omissions or for the results obtained from the use of such information. Copyright © 2014 Standard & Poor's Financial Services LLC, a part of McGraw Hill Financial. All rights reserved. STANDARD & POOR’S, S&P, S&P 500, S&P MIDCAP 400, S&P SMALLCAP 600, and S&P EUROPE 350 are registered trademarks of Standard & Poor’s Financial Services LLC. S&P CAPITAL IQ is a trademark of Standard & Poor’s Financial Services LLC.

INDUSTRY SURVEYS AUTOS & AUTO PARTS / DECEMBER 2014 1

CURRENT ENVIRONMENT

Corporate actions pick up

Mergers and acquisitions (M&A) activity saw a sizeable jump in the auto manufacturing industry and the auto retail market in the first 10 months of 2014.

Following Fiat SpA’s complete takeover of Chrysler Group LLC’s after buying the 41% stake for $2.9 billion in January 2014, the combined company—Fiat Chrysler Automobiles NV (FCA)—went public on October 13, forming the seventh-largest automaker in the world.

Another M&A activity is ZF Friedrichshafen AG’s buyout of TRW Automotive Holdings Corp. for $13.5 billion. The deal was announced on September 15, 2014 and is expected to be completed in the first half of 2015. While TRW Automotive will operate as a separate business division, the combined company will bring together complementary product offerings and leading technology positions that will better position the company in different markets and high-growth areas. ZF Friedrichshafen estimated that the merger will result in a business that will more than double sales in the US and China. The transaction creates the second largest auto parts supplier in the world.

We think the consolidation phase in the industry will continue in 2015, as companies want to have access to different segments, markets, and technologies.

Dealership M&A US auto retailers, though benefiting from improving domestic sales, are queuing up to acquire dealerships overseas. They believe that international markets will play a crucial role by providing potential growth even amid cyclicality of the domestic market.

In October, Lithia Motors, Inc. completed its acquisition of DCH Auto Group Inc. for $362.5 million, which is expected to result in a $2.3-billion increase in annual revenue to Lithia. The deal diversifies the combined company’s brand portfolio, reducing reliance on any one brand. For example, prior to the acquisition, Lithia had focused mainly on domestic brands and was heavily dependent on Chrysler vehicle growth, but the combined company can now expand to imported and luxury brands. There are two growth paths in store for the company—Lithia will be focusing on exclusive franchises in medium markets, while DCH will be focusing on extra-large and mega markets. The combination develops a metro market strategy for Lithia.

Meanwhile, Warren Buffet’s investment company, Berkshire Hathaway Inc., announced in October that it is entering the auto business through its decision to acquire Van Tuyl Group, the largest privately owned auto dealership in the US, with almost $8 billion in revenues. After the anticipated acquisition closes in the first quarter of 2015, Van Tuyl Group will be renamed Berkshire Hathaway Automotive. While the terms of the acquisition are undisclosed, the move shows Buffet’s confidence in car retailing, which is noteworthy as he is one of the most influential businessmen and investors in the world. Buffet has mentioned that he may buy more dealerships. We think this acquisition could stimulate other dealership M&A activity, as Buffet’s interest in dealerships indicate their value in the automotive industry.

Identifying growth opportunities in dealerships, Asbury Automotive Group Inc. announced in October 2014 that it aims to buy stores that will add $500 million in annual revenue over the next 18 months. At the end of October 2014, the company announced the acquisition of two unidentified dealerships that are expected to contribute $250 million in revenue. These transactions are expected to close by the end of 2014 or early in 2015.

There has also been movement toward international expansion among publicly traded auto dealers. For example, Group 1 Automotive is expanding its international presence. The company acquired UAB Motors Participacoes SA, a Brazilian automotive retailer, in 2013. Group 1 obtained full ownership of 18

2 AUTOS & AUTO PARTS / DECEMBER 2014 INDUSTRY SURVEYS

dealerships representing 22 franchises in the deal, which was worth about $146 million. In the same month, it also acquired four Ford dealerships from Inchcape Retail Ltd in the UK.

Penske Automotive Group Inc. has been very active on the acquisition trail. The company acquired 13 franchises in the UK that were formerly part of the Isaac Agnew dealership group in January 2012. Further, in March 2012, the company established a joint venture with Andrea Mantellini, which operates a BMW/MINI dealer group in Bologna, Italy; the joint venture acquired the Mariani BMW/MINI dealership in Monza, Italy. Penske acquired Western Star Trucks Australia Pty. Ltd. from Transpacific Industries Group Ltd. for about $200 million in August 2013. Western Star is a distributor of commercial vehicles, related spare parts, and aftermarket support across Australia, New Zealand, and parts of Southeast Asia.

Ford launches aluminum-bodied F-150 The Ford F-150 was the best-selling vehicle in the US for the past 32 years. Despite the success of this vehicle, Ford has decided to take it a notch higher, and is scheduled to begin production of its redesigned, all-aluminum body F-150, which is expected to be launched onto the market in December 2014.

While aluminum is as strong as steel, it is lighter, and hence increases fuel efficiency as well as towing and payload capacities, and improves power-to-weight ratio for faster acceleration. The use of aluminum also makes the F-150 stronger, considering that this material is more resistant to dents and dings than steel. Switching to an aluminum body adds $395 to the price. Consumers and investors will be on the lookout, even though there has been some controversy about how the F-150’s all-aluminum body will stand up to the abuse that pickup trucks often endure.

Good news for used car buyers A key indicator in the US automobile industry, the Manheim Used Vehicle Value Index, has been on a downward trend since reaching a price peak in May 2014, showing year-on-year declines in August and September of 0.4% and 1.1%, respectively. In 2013, the Mainheim Used Vehicle Value Index averaged 121.4, down 1.8% from the 2012 average. However, year to date through October, the index averaged 123.1, up 1.6% from the year-ago period. We still think the prices of used cars will continue to decline, despite the moderate increase in October. The decline in prices provides an opportunity for car shoppers, especially for those who otherwise could not afford to buy a used car in the wake of the recession. However, the used car price trend may be a threat to new-car sales, as some car shoppers may forgo buying a new car, and may have a renewed interest in owning used vehicles.

GAS PRICES DROPPING

As of November 13, 2014, gas prices in the US averaged $2.92, down 8.4% on a year-on-year basis, according to the AAA. Drivers are expected to pay less than $3 for a gallon of gas in 2015, according to the Energy Information Association (EIA), a division of the US Energy Department.

As gas price per gallon reached the below-$3 dollar mark, consumer preference is shifting from fuel-efficient and smaller cars to SUVs and other light-duty trucks. Year to date through October, total unit sales for SUV and light-duty trucks (including pickups, cross-overs, minivans, and SUVs) jumped 7.1% and 9.7%, respectively, compared with a slower growth for cars (1.4%), according to Motor Intelligence. The slow growth in car sales can largely be attributed to the decline in midsize and large-car sales. Based on WardsAuto data, year to date through October, the biggest winner for light-duty trucks was Jeep Cherokee, with unit sales increase of 144,287 from 579 units, on a year-on-year basis. Meanwhile, the Grand Cherokee’s sales grew 5.5% year to date through October, on a year-on-year basis. The best-selling light truck, the Ford F-150, declined 0.5% as buyers put off their purchasing decisions in anticipation of the 2015 F-150.

INDUSTRY SURVEYS AUTOS & AUTO PARTS / DECEMBER 2014 3

RECALLS IN THE FOREFRONT

According to the National Highway Traffic Safety Administration (NHTSA), auto manufacturers recalled 21.9 million vehicles in the US in 2013, representing a nine-year high. The highest number of recalls affected Toyota (24.1%), Chrysler (21.2%), and Honda (12.6%). Auto recalls are on an upward trend in 2014, resulting in billion-dollar penalties, e.g., the $1.2 billion penalty on Toyota in March 2014 for misleading the public and regulators, and there is a push for an independent review of safety processes in automobile companies. In the first half of 2014 alone, the NHTSA reported 37.5 million recalled vehicles, which is 71.2% more than the total recalls in full-year 2013.

General Motors Co. (GM) is facing a probe into faulty parts that have allegedly caused deaths and serious injuries. Year to date through October, GM had 77 separate recalls involving 26.6 million vehicles in the US market and 3.5 million vehicles in foreign markets, bringing the total to 30.1 million. The company has been in the hot seat over faulty ignition switches. Ignition-related vehicle recalls totaled 13.2 million (including exports), i.e., 2.6 million units of 1997–2005 Chevrolet Malibu and 1998–2002 Chevrolet HHR were recalled due to faulty ignition cylinders in April 2014. According to a November 2014 article published by Reuters, this ignition problem has resulted in 196 claims for death, 116 for catastrophic injuries, and 1,460 for other injuries since August 1, 2014, when GM’s compensation program for victims of faulty ignition switch accidents started. Overall, GM incurred recall-related charges of $2.7 billion, year to date through September.

S&P Capital IQ (S&P) expects recall activity by automakers in 2015, but at a slower pace, as manufacturers want to avoid penalties from the government and lawsuits from customers for safety defects. Evidently, Ford, Toyota, and GM, as well as other companies, seem to have realized that early, voluntary safety recalls are more to their advantage than billion-dollar penalties and prolonged public condemnation arising from defect-related accidents.

Takata massive recalls Airbag-related problems have also resulted in-vehicle recalls, particularly those manufactured by Takata Corp. In June 2014, the NHTSA received notification from BMW, Chrysler, Ford, Honda, Mazda, Nissan, Toyota, and Mitsubishi that they are conducting limited regional recalls to address possible defects of Takata air bag inflators. According to an October 22, 2014 article published by Automotive News, 7.8 million vehicles were involved in the Takata airbag recalls; Honda took the hardest hit, with a total of 5.1 million recalled vehicles manufactured between 2001 and 2007. As of November 2014, five deaths were linked to defective Takata airbags, according to The New York Times, resulting in multiple lawsuits for the company. On October 27, 2014, a class-action suit was filed with the US District Court in Florida against Takata and several automobile manufacturers. If class-action status is granted, Takata will have to pay a larger amount in a trial or settlement costs compared with individually filed lawsuits against the company.

Record fines for Hyundai and Kia US regulators have set standards in an attempt to increase product safety and environmental efficiency. In November 2014, the Environmental Protection Agency (EPA) and the US Justice Department fined Hyundai and Kia $100 million (the largest Clean Air Act penalty ever) for overstating fuel economy claims. The EPA found that 1.2 million cars sold by the Korean automobile carmaker were manufactured under false fuel economy ratings. The Agency argued that this contributed to over 5.2 million unaccounted tons of greenhouse gases. As a result, the companies will forfeit carbon credits, which are linked with the unaccounted emissions, valued at $200 million. The car models involved include Hyundai’s Accent, Elantra, Veloster, and Santa Fe as well as Kia’s Rio and Soul. In effect, Hyundai and Kia earned greater profits while also misleading consumers about the environmental impact of about one million of their 2012 and 2013 models. These penalties should serve as a warning to auto carmakers that tightening regulations in the US and other markets are being enforced to ensure that they comply with EPA requirements, and that failure to do so could blemish the company’s reputation.

4 AUTOS & AUTO PARTS / DECEMBER 2014 INDUSTRY SURVEYS

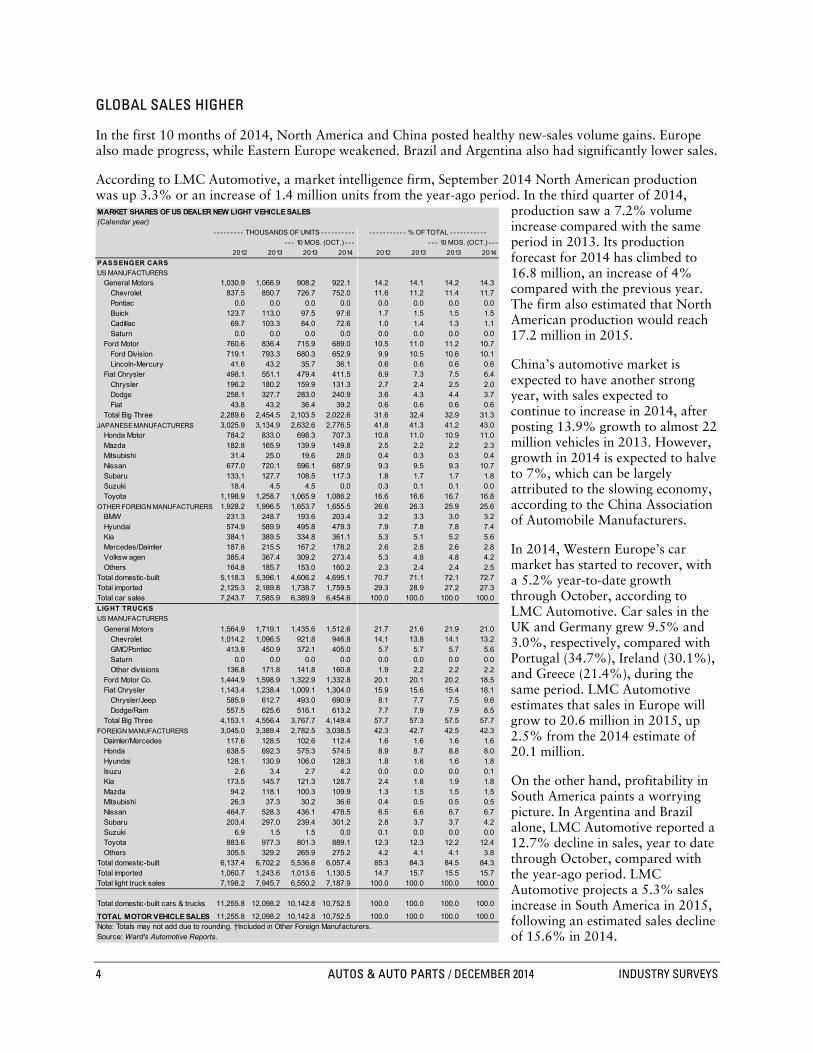

GLOBAL SALES HIGHER

In the first 10 months of 2014, North America and China posted healthy new-sales volume gains. Europe also made progress, while Eastern Europe weakened. Brazil and Argentina also had significantly lower sales.

According to LMC Automotive, a market intelligence firm, September 2014 North American production was up 3.3% or an increase of 1.4 million units from the year-ago period. In the third quarter of 2014,

production saw a 7.2% volume increase compared with the same period in 2013. Its production forecast for 2014 has climbed to 16.8 million, an increase of 4% compared with the previous year. The firm also estimated that North American production would reach 17.2 million in 2015.

China’s automotive market is expected to have another strong year, with sales expected to continue to increase in 2014, after posting 13.9% growth to almost 22 million vehicles in 2013. However, growth in 2014 is expected to halve to 7%, which can be largely attributed to the slowing economy, according to the China Association of Automobile Manufacturers.

In 2014, Western Europe’s car market has started to recover, with a 5.2% year-to-date growth through October, according to LMC Automotive. Car sales in the UK and Germany grew 9.5% and 3.0%, respectively, compared with Portugal (34.7%), Ireland (30.1%), and Greece (21.4%), during the same period. LMC Automotive estimates that sales in Europe will grow to 20.6 million in 2015, up 2.5% from the 2014 estimate of 20.1 million.

On the other hand, profitability in South America paints a worrying picture. In Argentina and Brazil alone, LMC Automotive reported a 12.7% decline in sales, year to date through October, compared with the year-ago period. LMC Automotive projects a 5.3% sales increase in South America in 2015, following an estimated sales decline of 15.6% in 2014.

Table B02: MARKET SHARES OF US DEALER NEW LIGHT VEHICLE SALES

MARKET SHARES OF US DEALER NEW LIGHT VEHICLE SALES(Calendar year)

2012 2013 2013 2014 2012 2013 2013 2014

PASSENGER CARS

US MANUFACTURERS

General Motors 1,030.9 1,066.9 908.2 922.1 14.2 14.1 14.2 14.3Chevrolet 837.5 850.7 726.7 752.0 11.6 11.2 11.4 11.7Pontiac 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0Buick 123.7 113.0 97.5 97.6 1.7 1.5 1.5 1.5Cadillac 69.7 103.3 84.0 72.6 1.0 1.4 1.3 1.1Saturn 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Ford Motor 760.6 836.4 715.9 689.0 10.5 11.0 11.2 10.7Ford Division 719.1 793.3 680.3 652.9 9.9 10.5 10.6 10.1Lincoln-Mercury 41.6 43.2 35.7 36.1 0.6 0.6 0.6 0.6

Fiat Chrysler 498.1 551.1 479.4 411.5 6.9 7.3 7.5 6.4Chrysler 196.2 180.2 159.9 131.3 2.7 2.4 2.5 2.0Dodge 258.1 327.7 283.0 240.9 3.6 4.3 4.4 3.7Fiat 43.8 43.2 36.4 39.2 0.6 0.6 0.6 0.6

Total Big Three 2,289.6 2,454.5 2,103.5 2,022.6 31.6 32.4 32.9 31.3JAPANESE MANUFACTURERS 3,025.9 3,134.9 2,632.6 2,776.5 41.8 41.3 41.2 43.0

Honda Motor 784.2 833.0 698.3 707.3 10.8 11.0 10.9 11.0Mazda 182.8 165.9 139.9 149.8 2.5 2.2 2.2 2.3Mitsubishi 31.4 25.0 19.6 28.0 0.4 0.3 0.3 0.4Nissan 677.0 720.1 596.1 687.9 9.3 9.5 9.3 10.7Subaru 133.1 127.7 108.5 117.3 1.8 1.7 1.7 1.8Suzuki 18.4 4.5 4.5 0.0 0.3 0.1 0.1 0.0Toyota 1,198.9 1,258.7 1,065.9 1,086.2 16.6 16.6 16.7 16.8

OTHER FOREIGN MANUFACTURERS 1,928.2 1,996.5 1,653.7 1,655.5 26.6 26.3 25.9 25.6BMW 231.3 248.7 193.6 203.4 3.2 3.3 3.0 3.2Hyundai 574.9 589.9 495.8 479.3 7.9 7.8 7.8 7.4Kia 384.1 389.5 334.8 361.1 5.3 5.1 5.2 5.6Mercedes/Daimler 187.8 215.5 167.2 178.2 2.6 2.8 2.6 2.8Volksw agen 385.4 367.4 309.2 273.4 5.3 4.8 4.8 4.2Others 164.8 185.7 153.0 160.2 2.3 2.4 2.4 2.5

Total domestic-built 5,118.3 5,396.1 4,606.2 4,695.1 70.7 71.1 72.1 72.7Total imported 2,125.3 2,189.8 1,738.7 1,759.5 29.3 28.9 27.2 27.3Total car sales 7,243.7 7,585.9 6,389.9 6,454.6 100.0 100.0 100.0 100.0LIGHT TRUCKS

US MANUFACTURERS

General Motors 1,564.9 1,719.1 1,435.6 1,512.6 21.7 21.6 21.9 21.0Chevrolet 1,014.2 1,096.5 921.8 946.8 14.1 13.8 14.1 13.2GMC/Pontiac 413.9 450.9 372.1 405.0 5.7 5.7 5.7 5.6Saturn 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0Other divisions 136.8 171.8 141.8 160.8 1.9 2.2 2.2 2.2

Ford Motor Co. 1,444.9 1,598.9 1,322.9 1,332.8 20.1 20.1 20.2 18.5Fiat Chrysler 1,143.4 1,238.4 1,009.1 1,304.0 15.9 15.6 15.4 18.1

Chrysler/Jeep 585.9 612.7 493.0 690.9 8.1 7.7 7.5 9.6Dodge/Ram 557.5 625.6 516.1 613.2 7.7 7.9 7.9 8.5

Total Big Three 4,153.1 4,556.4 3,767.7 4,149.4 57.7 57.3 57.5 57.7FOREIGN MANUFACTURERS 3,045.0 3,389.4 2,782.5 3,038.5 42.3 42.7 42.5 42.3

Daimler/Mercedes 117.6 128.5 102.6 112.4 1.6 1.6 1.6 1.6Honda 638.5 692.3 575.3 574.5 8.9 8.7 8.8 8.0Hyundai 128.1 130.9 106.0 128.3 1.8 1.6 1.6 1.8Isuzu 2.6 3.4 2.7 4.2 0.0 0.0 0.0 0.1Kia 173.5 145.7 121.3 128.7 2.4 1.8 1.9 1.8Mazda 94.2 118.1 100.3 109.9 1.3 1.5 1.5 1.5Mitsubishi 26.3 37.3 30.2 36.6 0.4 0.5 0.5 0.5Nissan 464.7 528.3 436.1 478.5 6.5 6.6 6.7 6.7Subaru 203.4 297.0 239.4 301.2 2.8 3.7 3.7 4.2Suzuki 6.9 1.5 1.5 0.0 0.1 0.0 0.0 0.0Toyota 883.6 977.3 801.3 889.1 12.3 12.3 12.2 12.4Others 305.5 329.2 265.9 275.2 4.2 4.1 4.1 3.8

Total domestic-built 6,137.4 6,702.2 5,536.6 6,057.4 85.3 84.3 84.5 84.3Total imported 1,060.7 1,243.6 1,013.6 1,130.5 14.7 15.7 15.5 15.7Total light truck sales 7,198.2 7,945.7 6,550.2 7,187.9 100.0 100.0 100.0 100.0

Total domestic-built cars & trucks 11,255.8 12,098.2 10,142.8 10,752.5 100.0 100.0 100.0 100.0

TOTAL MOTOR VEHICLE SALES 11,255.8 12,098.2 10,142.8 10,752.5 100.0 100.0 100.0 100.0Note: Totals may not add due to rounding. †Included in Other Foreign Manufacturers.Source: Ward's Automotive Reports.

- - - 10 MOS. (OCT.) - - -

- - - - - - - - - THOUSANDS OF UNITS - - - - - - - - - - - - - - - - - - - - - % OF TOTAL - - - - - - - - - - -

- - - 10 MOS. (OCT.) - - -

INDUSTRY SURVEYS AUTOS & AUTO PARTS / DECEMBER 2014 5

Pickups picking up US pickup sales gained momentum throughout 2014, and we expect further growth in 2015. The Detroit Three—the three biggest US automakers, which are based in Detroit, Michigan—reported combined year-over-year double-digit sales gains in 2013, mainly due to the rising demand for pickup trucks. Year to date through October, the Detroit Three reported growth of 5.2%, which can largely be attributed to a 0.6% drop in Ford sales, a 3.9% sales growth of GM vehicles, and the double-digit growth of Fiat Chrysler vehicles at 15.3%.

According to WardsAuto, year to date through October, sales of large pickup trucks rose 5.4%, year over year. Chrysler Group LLC sales of Ram pickup trucks rose 22.9%, while Ford’s F-series truck sales declined 0.5%, as buyers wait for the 2015 F-150. Sales of GM’s Silverado and GMC Sierra climbed 6.4% and 9.0%, respectively. In 2013, sales of large pickup trucks rose 10% on a year-on-year basis. Year to date through October, truck sales grew 9.8%.

We think that economic growth and steady gasoline prices will support expansion in the highly profitable light truck segment. Furthermore, new and refreshed pickup trucks—whether available or soon-to-be for sale—should boost overall truck sales, especially when improving construction, housing, and contractor activities are ongoing.

According to the US Census Bureau, housing starts reached a seasonally adjusted annual rate (SAAR) of nearly 9,839,000 units in year to date through October, up 9.1% from 9,017,000 in the same period in 2013. As of October, Standard & Poor’s Economics (which operates separately from S&P Capital IQ) forecast housing starts to reach 1.02 million in 2014 and 1.28 million in 2015, both up from the 930,000 units in 2013.

Detroit Three market share relatively stable in 2014 According to WardsAuto, US sales in light vehicles reached 13.6 million units year to date through October, which is a 5.4% increase from the year-ago period. Of these units sold, GM contributed 2.3 million units with a 3.9% sales increase. Ford’s sales dropped 0.8% to 2.0 million units, and Fiat Chrysler increased 15.3% to 1.5 million units.

The market share of the Detroit Three in the light truck category is up to 57.7%, year to date through October, from 57.5% recorded a year ago. The slow market share growth can be attributed to a decline in GM’s and Ford’s market share, from 21.9% and 21.0% as of October to 20.2% and 18.5%, respectively.

China to remain the world’s largest vehicle market Sales of new vehicles in China reached a record 21.98 million units in 2013, according to WardsAuto. This made China the first country to exceed 20 million deliveries in a year. The huge market also overtook the 20-million benchmark in auto production, with 22.12 million units manufactured in 2013. Year to date through October, China’s vehicle sales grew 8.1%, reaching 19.2 million sales, according to LMC. China had a 28.2% share in global vehicle sales as of October, outperforming the US, which had a 17.5% share.

In 2009, China overcame the US’ decades-long run as sales champ, years earlier than we had expected. China remains an under-penetrated market and S&P thinks that the country is likely to continue to lead in the future, given its large population. In our view, this development represents a shift in the center of the automotive world from Detroit to Asia. We expect more and more automotive trends and technologies to originate in Asia, as that market grows even larger in size and importance. Asia and other emerging markets already account for the majority of new vehicle growth. Nevertheless, the US and Europe will remain important and competitive markets for automotive products.

FORD CHINA SALES TAKING OFF

Ford China sold 906,613 units year to date through October, posting a strong year-on-year growth of 22.2%. This steady growth in sales is significant in the overall growth of the Chinese market. Ford has increased its focus on the Chinese market, as it expects that this market will have the highest growth rates in

6 AUTOS & AUTO PARTS / DECEMBER 2014 INDUSTRY SURVEYS

both revenue and profits over the next few years. In 2013, wholesale volume was up 30% to 935,813 vehicles, while revenue rose 17%, compared with 2012.

Ford is a late entrant in the Chinese market compared with its peers. It primarily concentrates its operations in the US and Europe and has a small market share in China—around 5%, versus nearly 15% each for Volkswagen and GM. Ford began producing cars in a Chinese joint venture in 2003, four years after GM and 18 years after Volkswagen (Forbes, March 19, 2014). To make up for its late entry, the company plans to increase its market share to 6% by 2015 through expanding its production capacity, marketing and distribution network, and introducing new products.

Global sales forecast In 2015, the rising prosperity in emerging markets, led by China, is expected to drive global demand growth, and European demand is expected to rise slightly, partly offset by declines in some emerging markets. S&P thinks that higher volume in the US and abroad will help increase corporate profit and cash flow, but this could be partly offset by difficulties coming from intense competition in Europe. Overall, we expect auto sales to increase in 2015, helped in part by rising wealth, pent-up demand, and the improved availability of credit.

Europe stabilizing In the third quarter of 2014, Eurozone gross domestic product (GDP) rose only 1.0%, slightly higher than the previous quarter’s 0.9% growth. Europe has pressured GM and Ford in the troubled regions, but we think the European demand should rise slightly, partly offset by declines in some emerging markets. According to Ford, the industry’s SAAR of vehicles was 14.5 million units in the third quarter of 2014, for the 20 European markets it tracks.

Ford Europe’s sales grew 7.8% year to date through September, on a year-on-year basis. The company’s European market share increased to 8.1%, up from 2013. In addition, Ford’s European operations reported a pre-tax loss of $619 million, year to date through September, an improvement over the $913 million loss of a year earlier, and revenues of $22.7 billion, up from $20.3 billion in 2013.

GM Europe reported an operating loss before income taxes of $976 million year to date through September, versus a $504 million loss in the prior-year period. Overall, GM Europe’s total net sales and revenue in the first nine months of 2014 reached $16.8 billion, up 3.5% from $16.3 billion in the same period in 2013.

BATTLE FOR THE MIDSIZED VEHICLE

Demand for the latest models with dramatic styling and interior is what fuels the battle in family-sedan sector. Companies usually wait five years to redesign their vehicles, but fierce competition in the midsized vehicles is driving automakers to restyle sedans faster. For instance, in May 2014, Toyota launched redesigns of the current version of Camry that has been around for only two years, and Hyundai debuted the redesign of its 2011 Sonata model. Camry has been leading the race in this segment for 12 years now, but keeping up with the pace and closing the lead are Ford’s Fusion, Nissan’s Altima, and Honda’s Accord. Year to date through October, Camry sold 368,006 units (up 5.8% from the year-ago period); Honda Accord, 331,167 units (up 8.0%); Ford Fusion, 263,431 units (up 6.2%); and Nissan Altima, 280,479 units (up 3.4%).

The demand for affordable midsized vehicles, the biggest segment of the car market, is at a historically high level, sparking competition among car manufacturers to get the biggest piece of the pie. Hyundai’s strategy lies in Sonata’s below-industry-average pricing and “fluidic sculpture,” the company’s design philosophy that centers on a flowing and dynamic form.

Automakers are in a race to offer the best deals and discounts. With the looming threat of Accord overtaking Camry, Toyota’s sales incentives averaged about $3,200 in the first three months of 2014, which is almost $500 more than the industry’s average for midsized cars. In October Toyota was offering 0% financing for 72 months with a $500 rebate for 2014 models, Honda was offering 0% for 60 months with $1,500 rebate.

INDUSTRY SURVEYS AUTOS & AUTO PARTS / DECEMBER 2014 7

BANKS’ AUTO LENDING INCREASES

Rising vehicle sales of vehicles has led to an increase in overall auto lending by banks and other financial institutions and auto finance companies. According to the latest “National Consumer Credit Trends Report” published by Equifax (a consumer credit reporting agency), balances on outstanding auto loans in August 2014 totaled $924.2 billion, an all-time high and a 10.8% increase from the year-ago period. While the auto finance companies were the first to start lending after the financial crisis, banks and other financial institutions have increased their lending recently. According to Experian, automotive delinquency rate has been improving since the crisis, and auto finance lenders have been granting longer-term loans. In its “State of the Automotive Finance Market Second Quarter 2014”, Experian reported that recent automotive 30-day delinquency decreased to 1.9% in banks, but increased to 5.1% in financial institutions during the second quarter of the year. We think this decline in delinquency rates will continue in 2014.

The average monthly payment through the second quarter of 2014 was $407, slightly lower than the $408 a year ago. On the other hand, average interest rate for new cars and used cars was 4.6% and 8.8%, respectively, compared with 4.4% and 8.6% a year ago. In the second quarter of 2014, the average loan term was 66 months for new cars (up from 65 months a year earlier) and 61 months for used cars (flat from year earlier).

Auto prices rise, but monthly loan payments remain flat Attractive deals are making it easier for more buyers to get their hands on new-car purchases. According to Kelley Blue Book, a vehicle valuation and automotive research company, the average transaction price of new cars has increased from $25,500 in 2008 to an estimated $33,361 in October 2014, a moderate increase from $33,176 in the prior-year period. Even though this represents a 30.8% increase in transaction prices over the last six years, average monthly payments on car loans have declined 2% from $464 in 2008 to an estimated $455 in 2014. Therefore, more middle-class car buyers can afford more expensive vehicles despite flat wages. Consumers need to be aware, however, of lease contract limitations and longer-term debts.

Several reasons explain why car loan payments have remained essentially flat, including record low interest rates, loans with longer repayment schedules, subsidized loans, and a strong market for used cars. According to J.D. Power and Associates, loans with a tenure of 72 and more months were used to finance an estimated 31% of all car purchases in 2014, versus 22% in 2009. Furthermore, the market for used cars has been strong as the average transaction price of used cars has increased from $15,900 in 2008 to an estimated $19,300 in 2014, according to J.D. Power.

AUTO RETAILERS: IMPROVED OPERATING EFFICIENCIES

Auto retailers cut their operating costs in order to survive in the environment of declining sales during the economic recession. However, as the economy gradually improved and auto sales picked up in 2013, we see a discipline among auto retailers to contain operating costs. Some of the largest auto retailers have seen their selling, general and administrative (SGA) costs as a percentage of gross profit improve considerably over time. For instance, AutoNation’s SGA as percentage of gross profit declined from 75.3% in 2008 to 70.1% in 2013. During the first nine months of 2014, the company saw this figure at 70.2%, slightly lower than 70.6% from a year ago due to increased sales and effective management of costs.

Replacement market still strong The US replacement parts market continued to grow strongly in 2013 as thrifty consumers repaired aging vehicles. According to Autocare Association, a trade group, the aftermarket industry’s revenues totaled $317.2 billion in 2013, up 3.1% from 2012. These figures include all automotive aftermarket sales (including medium and heavy-duty vehicle parts). We expect improved market demand for US automotive replacement parts for the following reasons: vehicle longevity has crossed 11 years, thrifty consumers continue to hold on to and repair their aging vehicles, and more than 261 million vehicles are expected to be on the road by 2017, according to Autocare Association.

Many auto parts suppliers are increasing their revenues generated outside the US, and emerging markets are becoming more attractive to parts manufacturers due to lower labor costs. Tenneco Inc., which produces

8 AUTOS & AUTO PARTS / DECEMBER 2014 INDUSTRY SURVEYS

ride control and exhaust systems for original equipment manufacturers (OEMs) and the aftermarket, is expected to see continued growth in its partnerships with OEMs in North America and Europe. Most of the company’s cost cutting has been aimed at shifting manufacturing overseas. We expect Tenneco’s revenue to advance about 9% in 2014 to $8.7 billion and a further 10% increase in 2015.

TIRES: ORIGINAL EQUIPMENT SHOULD DRIVE TIRE SALES HIGHER

With the expected rise in global vehicle production in 2015 comes an expanding global demand for tires. Replacement demand could also improve in the US as the economy starts to pick up. At some point soon, we think that consumers will start spending to replace tires and purchase items they have deferred.

Modern Tire Dealer, a monthly trade publication, reported in “Facts Issue 2014” that original equipment (OE) shipments of passenger tires rose about 9% to 44.0 million in 2013 from 40.5 million units in 2012, while light truck tires rose about 5% to 4.4 million in 2013 from 4.2 million in 2012. Total replacement passenger tire units shipped in 2013 amounted to 201.6 million units, up 5% from 192.0 in 2012, and nearing the record 205.8 million in 2005. Sales for replacement passenger tires reached $25.0 billion, truck tires $6.3 billion, and light truck tires $4.9 billion. Tire imports from China increased markedly by 57.5% to 51.2 million units in 2013 from 32.5 million in 2012.

About three-quarters of the tire shipments for the automotive industry are for replacement tires, with one-quarter for new vehicles. Margins on replacement tires are typically higher than for original equipment tires, as automakers receive discounts for high volume buying.

Costs have been more favorable than we expected in terms of raw materials. Tire manufacturers, which have been dealing with high raw material costs for a long time, witnessed a decline in prices recently. A noteworthy raw material is rubber, which reached a five-year low in October 2014. While the price trend of rubber hurts farmers in countries like Thailand and Vietnam, it has helped boost revenues for tire manufacturers, such as Cooper Tire & Rubber Co. and Goodyear Tire & Rubber Co. Year to date through September, Goodyear’s sales in North America dipped 8.7% on a year-on-year basis. Nonetheless, Goodyear’s operating income in North America increased 16.7%. Similarly, Cooper Tire’s net revenues increased 2.0% year to date through September, whereas its operating profit increased 23.7%. This indicates that low rubber prices have helped trim down the operating costs of both Goodyear and Cooper Tire, allowing the companies to post favorable operating income.

Despite declining rubber prices, producers may shrink their supply, which could increase the prices for this commodity once again. While we think volume will rise in 2015, potentially higher raw materials costs could restrict profitability.

NEW LIGHT VEHICLE SALES FORECASTS

S&P projects that US light vehicle sales volume would reach 16.4 million units in 2014, a 5.5% increase compared with a year-ago period. In 2015, we expect this sales volume to further increase to 16.8 million As of October 2014, Standard & Poor’s Economics was forecasting a 2.2% increase in real GDP for 2014 and a 3.0% increase for 2015. We see the industry in the early stages of a multiyear uptrend in demand.

As of October 2014, J.D. Power and Associates and LMC Automotive were forecasting that North American production would reach 16.8 million, up 4% from the year-ago period. LMC also adjusted its forecast for light vehicle retail sales to 13.6 million units this year, while estimated total light vehicle units were raised to 16.4 million.

SUB-INDUSTRY REVIEWS & OUTLOOK

As of November 2014, our fundamental outlook for the automobile manufacturers sub-industry for the next 12 months was positive. We see US automotive demand trending higher on a year-over-year basis, and while we expect to see uneven geographic progress, we look for global demand to rise in 2014. Also, despite the risks we perceive, we forecast steady improvement overall. Europe has pressured GM and Ford in the

INDUSTRY SURVEYS AUTOS & AUTO PARTS / DECEMBER 2014 9

troubled region, but the companies have shown progress, and we see slightly higher volume sales there after years of declines. Russia and parts of South America still look likely to be challenged areas.

We estimate US light vehicle sales in 2014 rising 5.5% to 16.4 million units, and reaching 16.8 million in 2015. In 2014, we expect gains in most other regions too, including emerging markets led by China, leading to a global demand growth and slight rise in European demand. However, this is also partly offset by declines in some emerging markets.

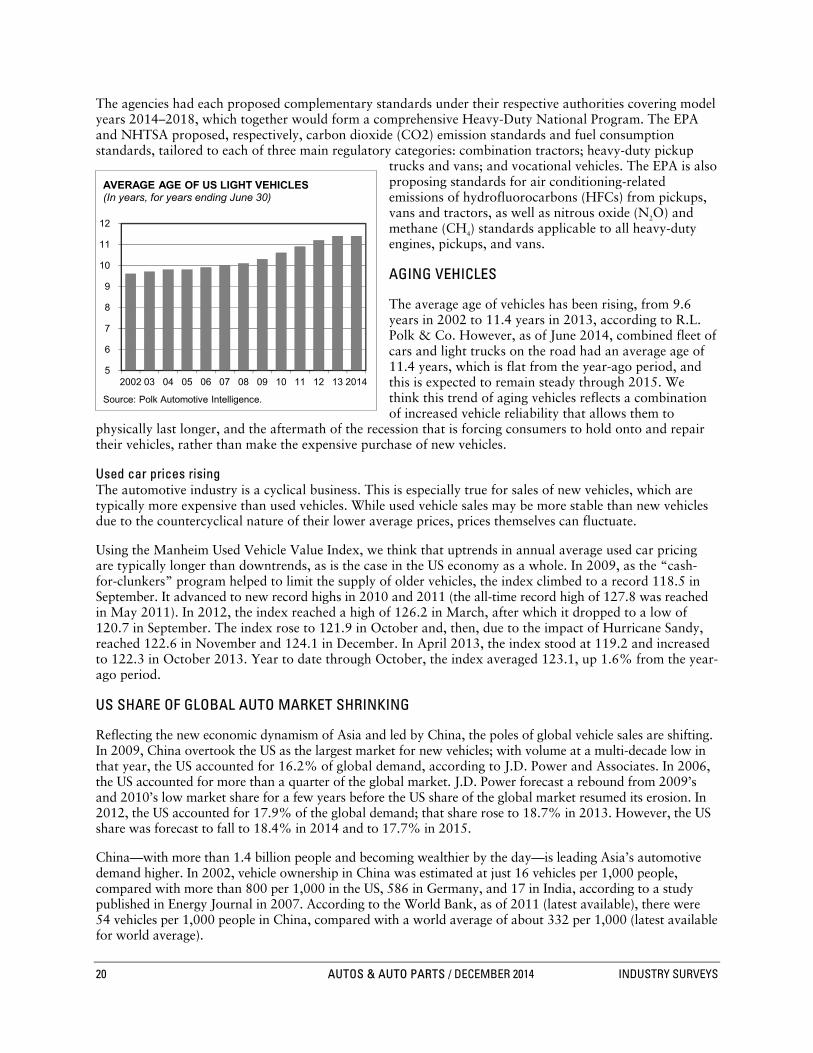

We think higher volume in the US and abroad versus 2013 will help corporate profits and cash flows. European difficulties, including competitive pressures, should be partly offsetting factors. Positive factors we see in the US include pent-up demand and widely available access to consumer credit. The average vehicle is now more than 11 years old, an industry record. We think lower gasoline prices are a positive for sales.

We also think recently lower gasoline prices and economic growth will support expansion in the highly profitable light truck segment. Also, new and refreshed pickup trucks—available and soon-to-be for sale—combined with improved construction, as well as housing and contractor activity, should boost overall truck sales. Luxury vehicle sales in the US, which were also restrained by economic weakness, should show improvement, in our view, as wealthy consumers become more confident. Luxury sales should be strong in China.

We think GM’s and Chrysler’s respective bankruptcy filings allowed the automakers to shed billions of dollars in liabilities and lower their operating costs. Overall, we see this makes the companies more cost-competitive and focused, but they still face competitive challenges. Chrysler has merged with Fiat SpA of Italy.

As for the auto parts and equipment sub-industry, our outlook is also positive, reflecting our expectations for rising demand and volume in the US and abroad, including China. Many auto parts suppliers are increasing their revenues generated outside the US. Emerging markets are becoming more attractive to manufacturers of auto parts due to lower labor costs for manufacturing and engineering and/or due to growing demand in local and regional markets. Over time, we expect some domestic parts suppliers to increase penetration of import brands, which are shifting more of their production to the US.

We think the worst has passed for Europe, but it will likely remain relatively weak during 2015. We expect profits should benefit from higher global vehicle production and higher production in Asia, despite a likely decline in Japan. Lastly, we expect improved market demand for US automotive replacement parts in 2014 and 2015.

Year to date through November 11, 2014, the S&P Automobile Manufacturers Index was down 10.8% while the S&P Auto Parts & Equipment Index rose moderately to 1.8%, versus the 9.8% gain for the S&P 1500 Index. In 2013, the Automobile Manufacturers Index and Auto Parts & Equipment Index surged 27.8% and 62.4%, respectively, compared with a 30.1% gain for the S&P 1500.

10 AUTOS & AUTO PARTS / DECEMBER 2014 INDUSTRY SURVEYS

INDUSTRY PROFILE

Competition in overdrive

Based on dollar value, the US is the world’s largest consumer market for light vehicles, a category that comprises passenger cars and light trucks. According to the National Automobile Dealers Association’s “NADA Data 2014”, revenues (including sales of new and used vehicles, as well as service and other items)

for dealers in the US totaled $730 billion in 2013, up 8.8% from in the previous year.

Year to date through October, new light vehicle sales in the US reached 13.6 million (up from 12.9 million in 2013), whereas US vehicle sales reached 14.0 million (up from 13.2 million in the year-ago period). For 2013, new light vehicle sales in the US advanced to 15.5 million, compared with 14.5 million in 2012 and 12.7 million in 2011. In 2013, US vehicle sales reached 15.9 million units, up 7.4% from 14.8 million in

2012. S&P Capital IQ (S&P) expects volume to increase to 16.4 million in 2014, fueled by replacement demand as American consumers replace their aging vehicles.

In recent years, light trucks have been popular passenger vehicles. In terms of units sold, light trucks (less than 14,000 pounds gross vehicle weight, or GVW) accounted for almost 96% of the truck market as of October 2014.

Approximately 335,000 medium- and heavy-duty trucks were sold in the US year to date through October, up from 288,000 in the year-ago period. In 2013, about 352,000 medium- and heavy-duty trucks were sold, up from

346,000 in 2012, but still sharply lower than the high of 545,000 in 2006. (Medium-duty trucks weigh 14,001 to 33,000 pounds; heavy-duty trucks exceed 33,000 pounds). S&P estimates that sales of medium- and heavy-duty trucks will advance about 14% in 2014.

Table B18: US MOTOR VEHICLE SALES & PRODUCTION

US MOTOR VEHICLE SALES & PRODUCTION(In thousands)

MED. & TOTAL MED. & TOTAL

PASSENGER LIGHT HEAVY MOTOR PASSENGER LIGHT HEAVY MOTOR

YEAR CARS TRUCKS TRUCKS VEHICLES CARS TRUCKS TRUCKS VEHICLES

2014ʬ 6,455 7,188 335 13,977 3,606 6,055 246 9,9082013ʬ 6,390 6,550 288 13,228 3,709 5,455 214 9,378

2013 7,586 7,946 352 15,884 4,369 6,446 251 11,0662012 7,244 7,198 346 14,788 4,109 5,959 268 10,3362011 6,089 6,645 306 13,041 2,978 5,441 243 8,6622010 5,635 5,919 218 11,772 2,732 4,866 146 7,7442009 5,401 5,001 200 10,601 2,196 3,382 132 5,7102008 6,813 6,381 298 13,493 3,731 4,671 225 8,6272007 7,618 8,471 371 16,460 3,867 6,549 279 10,6952006 7,821 8,684 545 17,049 4,312 6,431 462 11,2052005 7,667 9,281 497 17,444 4,266 7,203 422 11,8912004 7,506 9,361 432 17,299 4,166 7,373 386 11,9242003 7,610 9,029 328 16,967 4,453 7,319 268 12,040NOTE: Totals may not add due to rounding. *Total US sales, including foreign models produced bothinside and outside the United States, as w ell as domestic models produced in Canada and Mexico.†Foreign and domestic models produced inside the United States. ʬData through October.Source: Ward's Automotive Reports.

- - - - - - - - - - - - - - - - - - SALES* - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - PRODUCTION† - - - - - - - - - - - - - - -

Table B12: US RETAIL SALES OF MOTOR VEHICLES, BY WEIGHT CLASS

US RETAIL SALES OF MOTOR VEHICLES, BY WEIGHT CLASS

- - - - - - - 2013 - - - - - - -

UNITS % OF UNITS % OF UNITS % OF

CATEGORY (THOUS.) TOTAL (THOUS.) TOTAL (THOUS.) TOTAL

PASSENGER CARS 7,586 49.2 6,390 48.3 6,455 46.2Domestic 5,396 35.0 4,606 34.8 4,695 33.6Import 2,190 14.2 1,784 13.5 1,759 12.6

TRUCKS 7,848 50.8 6,838 51.7 7,522 53.8Light trucks, total 7,496 48.6 6,550 49.5 7,188 51.4

0-6,000 lbs. 5,165 33.5 4,636 35.0 5,126 36.76,001-10,000 lbs. 2,077 13.5 1,708 12.9 1,851 13.210,001-14,000 lbs. 254 1.6 207 1.6 211 1.5

Medium-duty trucks, total 167 1.1 138 1.0 154 1.114,001-26,000 lbs. 119 0.8 98 0.7 109 0.826,001-33,000 lbs. 48 0.3 40 0.3 45 0.3

Heavy-duty trucks 185 1.2 151 1.1 180 1.3(over 33,000 lbs.)

Total US sales 15,434 100.0 13,228 100.0 13,977 100.0*Data through October.Source: Ward's Automotive Reports.

- - - - - - - - - - - - - - - OCTOBER - - - - - - - - - - - - - - -

- - - - - - 2013* - - - - - - - - - - - - - 2014* - - - - - - -

INDUSTRY SURVEYS AUTOS & AUTO PARTS / DECEMBER 2014 11

Participants in the medium- and heavy-duty commercial truck markets include Daimler AG, Freightliner Corp. (a subsidiary of Daimler that makes Freightliner brand trucks), Volvo Trucks North America Inc., PACCAR Inc., Navistar International Transportation Corp., and Mack Trucks Inc. (acquired by Volvo in 2001).

THE DETROIT THREE SEE DWINDLING MARKET SHARE

The “Detroit Three” (formerly known as the “Big Three”) US automakers—General Motors Co. (or GM, the new name of General Motors Corp. following its emergence from bankruptcy in 2009), Ford Motor Co., and Chrysler Group LLC—accounted for 31.3% of passenger cars sold in the US year to date through October. Their market shares were 14.3%, 10.7%, and 6.4%, respectively. Year to date through October, the top three foreign companies had a combined US car market share of 38.4%: Toyota Motor Corp. (16.8%), Honda Motor Co. Ltd. (11.0%), and Nissan Motor Co. Ltd. (10.7%).

In the light truck category, however, the Detroit Three still dominates the US market. Ford, GM (maker of Chevrolet and GMC trucks), and Chrysler (maker of Dodge trucks and Jeep SUVs and recreational vehicles) accounted for 57.7% of light truck sales year to date through October. Among foreign automakers expanding in the US light truck market are Toyota (12.4%), Honda (8.0%), and Nissan (6.7%).

In the overall US light vehicle market (a category that comprises passenger cars and light trucks), Detroit Three brands had a 44.9% share in 2013, according to industry publication Ward’s Automotive Reports, up from 44.6% in 2012 and down from 46.9% in 2011. Market share for the Detroit Three brands in October 2014 was 45.2% slightly down from 45.4% a year ago.

Auto parts sector highly fragmented The auto parts sector of the US auto industry is highly fragmented, consisting of thousands of parts suppliers that range in size from small shops to large multinational corporations. It comprises four lines of business: original equipment manufacturing, replacement parts manufacturing, replacement parts distribution, and rubber fabrication.

Table B01: NORTH AMERICAN MOTOR VEHICLE PRODUCTION

NORTH AMERICAN MOTOR VEHICLE PRODUCTION(Calendar year)

2013 2013* 2014* 2013 2013* 2014* 2013 2013* 2014* 2013 2013* 2014*

General Motors 1,249 1,045 1,032 17.6 17.2 17.2 2,036 1,726 1,835 21.7 21.8 21.0Ford Motor 952 923 781 13.4 15.2 13.1 2,032 1,723 1,742 21.6 21.7 19.9Fiat Chrysler 641 546 446 9.1 9.0 7.4 1,868 1,539 1,921 19.9 19.4 22.0

Total Big Three 2,841 2,514 2,259 40.1 41.4 37.7 5,936 4,987 5,498 63.2 62.9 62.8Auto Alliance 117 ... ... 1.7 ... ... ... ... ... ... ... ... BMW ... ... ... ... ... ... 297 255 295 3.2 3.2 3.4Honda Motor 949 815 811 13.4 13.4 13.5 832 708 724 8.9 8.9 8.3Hyundai 399 348 337 5.6 5.7 5.6 ... ... ... ... ... ... Isuzu ... ... ... ... ... ... 4 4 5 0.0 0.0 0.1Kia 134 114 122 1.9 1.9 2.0 236 203 196 2.5 2.6 2.2Mazda ... ... 77 ... ... ... ... ... ... Mercedes ... ... 22 ... ... 0.4 186 159 160 2.0 2.0 1.8Mitsubishi ... ... ... ... ... ... 67 57 59 0.7 0.7 0.7Nissan 1,038 884 977 14.7 14.5 16.3 433 362 513 4.6 4.6 5.9Subaru 138 119 128 1.9 2.0 2.1 128 109 113 1.4 1.4 1.3Tesla ... 20 27 ... 0.3 0.5Toyota 815 690 719 11.5 11.4 12.0 945 810 861 10.1 10.2 9.8Volksw agen 652 570 509 9.2 9.4 8.5 ... ... ... ... ... ... Others ... ... ... ... ... ... 328 278 324 3.5 3.5 3.7

Total transplants 4,243 3,560 3,728 59.9 58.6 62.3 3,458 2,946 3,250 36.8 37.1 37.2Grand total 7,084 6,074 5,987 100.0 100.0 100.0 9,394 7,933 8,748 100.0 100.0 100.0

Note: Totals may not add due to rounding. *Data through October.Source: Ward's Automotive Reports.

CARS TRUCKS

THOUSANDS OF UNITS - - - - - - % OF TOTAL - - - - - - THOUSANDS OF UNITS - - - - - - % OF TOTAL - - - - - -

12 AUTOS & AUTO PARTS / DECEMBER 2014 INDUSTRY SURVEYS

Original equipment manufacturers (OEM). These manufacturers produce parts and components that automakers use in the assembly of new vehicles. Thousands of OEMs are independent firms; among the largest independents are Dana Holding Corp., Delphi Automotive PLC, Goodyear Tire & Rubber Co., Johnson Controls Inc., Magna International Inc., Superior Industries International Inc., Tenneco Inc., TRW Automotive Holdings, and Visteon Corp. Other OEMs are subsidiaries of large diversified companies, such as AlliedSignal Inc., Eaton Corp., General Electric Co., 3M Co., PPG Industries, Textron Inc., and United Technologies Corp.

Replacement parts manufacturing. Participants in the replacement market, also known as the aftermarket, produce parts and components to replace or supplement parts that were included in a vehicle’s original assembly. Among the field’s important players are Meritor Inc., Cooper Tire & Rubber Co., Dana Holding Corp., and Federal-Mogul Corp. As in the original equipment segment, aftermarket parts suppliers and distributors may be independent companies or subsidiaries of larger companies. Some firms, like Dana, participate in both the original equipment and replacement sectors.

Replacement parts distribution. Companies in this category distribute automotive accessories and parts, such as air filters, light bulbs, and fuses, which replace or supplement original vehicle parts. Sales are primarily to automotive parts retail stores and fleet owners.

Genuine Parts Co. (GPC) is by far the largest independent distributor of auto parts, and its largest division is The Automotive Parts Group. The Group operates four Balkamp distribution centers, six Rayloc facilities, 12 Johnson industries facilities, and 58 distribution centers associated with the National Automotive Parts Association (NAPA), a leading US franchiser of auto/parts accessories stores and distribution centers. GPC also operates 900 co-owned NAPA auto parts stores, and its major products include access to more than 300,000 items such as heavy-duty parts, farm and marine supplies, and refinishing supplies. The company serves approximately 5,800 NAPA auto parts stores in the US, according to GPC’s 2013 annual report.

Rubber fabricating. Rubber fabricators manufacture the tires, belts, hoses, and other rubber products used in vehicles. Approximately 60% of rubber production for the auto industry is tire-related.

About half of worldwide tire production is estimated to come from three companies: Compagnie Générale des Établissements Michelin (France), Goodyear Tire & Rubber (US), and Bridgestone/Firestone Inc. (Japan). Foreign-based tire manufacturers now own a substantial portion of US domestic capacity. Only two publicly traded US tire companies remain: Cooper and Goodyear.

In January 2014, the Modern Tire Dealer reported that 298 million tires (for both original equipment and replacement) were shipped in 2013 (latest available), more than the 284 million tires in 2012. Of these shipments, 245.6 million tires were for replacement, up from 236.3 million tires in 2012. S&P thinks economic growth should cause industry tire sales to improve in the remainder of 2014 and into 2015, primarily driven by new vehicle production and better results in 2013 due to an improving global economy.

INDUSTRY TRENDS

In the luxury automobile market trend, new buyers take center stage. According to a report published by the National Automobile Dealers Association (NADA) in its April 2014 “NADA Market Review: Shifting Luxury Vehicle Preferences”, luxury sales, which includes luxury cars and utility vehicles, soared to more than 62% between 2009 and 2013, and climbed to 12.8% of the total market in 2013. Year to date through September, luxury car sales increased 5.9%, according to WardsAuto.

NADA also reported that luxury car share went up 0.4 percentage points in 2013 as automakers successfully competed to attract new buyers entering the market. Among luxury utility vehicles, the consumer preferences for the crossover utility vehicle (CUV) increased 0.9 percentage points, while the sport utility vehicles’ (SUVs) consumer preference points were down 0.3 percentage points. Buyers appear to be leaning more toward the lower, lighter, and economical CUVs than the roomy, fuel-thirsty SUVs. However,

INDUSTRY SURVEYS AUTOS & AUTO PARTS / DECEMBER 2014 13

according to WardsAuto data, there was a shift to SUVs in the first nine months of 2014—sales of luxury SUVs (16.9%) outperformed luxury CUVs (10.7%), thanks to lower gas prices.

NADA’s April 2014 report also highlighted that the luxury compact car segment has retained about 49% of its perceived value—more than the luxury midsize and large-car segments. Thus, luxury compact cars, which cost less than the midsized and large cars, are becoming more popular due to their superior value retention. In fact, the new lower-luxury cars market share is 5%, substantially higher than the 3% share of the other luxury car segments. Since retention value for luxury compact cars is high, used cars in this segment are in high demand. Similarly, the luxury compact utility vehicle and the luxury large SUVs have retained their value at 60%. Buyers, who are becoming more value conscious, prefer the cost-effective and better-value luxury CUVs to the more expensive SUVs.

Luxury compact utilities volume was 70,000 in 2013 and this is forecast to climb 51% by 2015, according to NADA, resulting in lower prices expected for used luxury CUVs in 2014 and 2015. On the other hand, luxury large SUVs are forecast to increase by only 17% by 2015, which shows declining consumer demand for these vehicles since 2013. Despite this small rise in supply, prices in this segment are expected to decline, partly because of steep depreciation curves.

Other industry trends include the increasing prevalence of smaller-sized cars, particularly in the developing world; improved repayment rates on vehicle loans; rising vehicle rental revenues; and the growing phenomenon of car sharing.

Exogenous factors are also having an impact on the industry. Higher oil prices, as well as expectations that any lull in these prices is only temporary, are spurring demand for smaller, more fuel-efficient gasoline-powered vehicles, and encouraging investment in alternative fuel technologies. In addition, efforts to reduce US energy dependence and the negative impact of fossil fuels are forces driving regulatory demands for higher fuel efficiency.

Notwithstanding these cost pressures, consumers still want vehicles that are safe and fun. Demand for the latest technology—including entertainment systems and communications devices—continues to drive growth in automotive electronics. In addition, demand for safety continues to increase. We note that greater use of safety equipment has helped reduce vehicle fatality rates in the US.

Economically expanding emerging markets are becoming a key source of growth for today’s global auto industry. Companies in developing markets are looking for opportunities in the US, while US manufacturers are looking to expand sales and production in other areas. In the US, challenges from import brands mean that the top US automakers, Detroit Three—General Motors Co. (GM), Ford Motor Co., and Chrysler (now Fiat Chrysler Automobiles) —have long seen reduced share in their domestic market. At the same time, growth in global demand means that the US market is accounting for a shrinking share of worldwide industry volume. For US auto parts companies, automaker demand for larger global suppliers has contributed to industry consolidation, as has profit margin pressure from rapidly rising costs.

THE ROLE OF INTERNET IN PURCHASE DECISIONS

Millennials, also known as Generation Y consumers (born 1977–1994) have outpaced their older Generation X counterparts (born 1965–1976) in new-car sales. In July, J.D. Power and Associates reported that Millennials accounted for 25% of total car sales year to date through June, whereas Gen X accounted for 24% of sales. Compact cars were the most popular choice for Millennials, whereas compact SUVs were more popular for Gen X buyers.

With the shifting share of the different generations on the US car market, understanding how they make their car purchase decisions is worth noting. The Multi-Device Car Shopping Study published by AutoTrader.com in October 2013 revealed that the PC or laptop is still the primary device used for car shopping, although a rapid adoption of mobile devices can be seen. The study found that 23% of car shoppers use two or more devices when purchasing a car. According to the study, 80% of consumers think that multi-device usage enhances the vehicle shopping process.

14 AUTOS & AUTO PARTS / DECEMBER 2014 INDUSTRY SURVEYS

LEASE RETURNS ON THE RISE

Another trend in the automobile market is the release of pent-up demand through an increasing number of lease returners. According to Edmund.com’s “Q3 2014 Used Vehicle Report”, lease returns are increasing, which resulted in greater concentration of newer used vehicles sold in the quarter. The report cited that one out of five vehicles sold in the third quarter of 2014 were between one and two years old.

Overall, an increase in lease returns can provide benefits for dealers and automakers. When a car lease expires, a lease return could present an opportunity for a dealer to sell a customer another car or to offer another car lease. The more cars dealers sell, the greater the manufacturing expansion for automakers.

Leasing makes a comeback Consumers, who are willing to spend on more expensive vehicles, believe that the market has been stabilizing and that leasing is becoming more desirable. According to Edmunds.com, easing credit conditions make new-car leasing easier for consumers and put lease penetration at an all-time high. Lease penetration hit a record high of 25.6% during the second quarter of 2014, up from the same period in 2013, according to Experian Automotive, a source of auto industry information. The average loan term for new vehicles reached 66 months in the second quarter, up from 65 months a year ago. For used vehicles, the term reached 61 months, flat from the prior-year period.

Leasing is becoming more attractive, despite the fact that the average monthly lease payment for new vehicles increased to $467 in the first quarter of 2014 from $457 a year ago. By leasing a new vehicle, many shoppers are able to get a car for less the price than if they had bought it. Leasing peaked in 1999 with 3.7 million units. About a decade later, GM and Chrysler ended their leasing programs due to losses stemming from poor residuals on returned vehicles. By 2009, overall leasing plunged to 1.1 million units, but since 2012, it grew steadily from 2.5 million to 3.0 million in 2013. Among young buyers, average lease penetration rose to 23% in 2013 from a record low of 13% in 2009, according to J.D. Power.

According to Auto Remarketing, a news media of pre-owned industry, leasing has a high penetration in the luxury segments, but in recent years, the mainstream segments are becoming more popular. Subcompact cars saw a 187% increase in the lease share of sales between 2008 and 2013 (latest available), while compact cars’ leasing share saw a 131% increase. This resulted in the drop of leasing share of new luxury vehicles from 30% in 2008 to 24% in 2013.

RISING DEMAND FOR DIESEL-POWERED VEHICLES

Consumers are seeking eco-friendly cars more than ever before. Hence, diesel-powered vehicles have become more common. In addition, the Motor & Equipment Manufacturers Association published on November 25, that the average price of diesel has fallen to $3.60. However, according to a November 2014 Forbes article, diesel fuel is not as widely available as gasoline.

According to the National Association of Convenience Stores, an international trade association of retail and supplier company members, US diesel car sales increased 25%, year to date through June, compared with the year-ago period. This sales growth is more than the overall US car market, which increased 4.2%.

With the potential sales of this type of vehicle, GM, Porsche, and Volkswagen are just some of the automakers that have expressed interest in producing diesel cars. GM’s Vice President Steve Kiefer thinks that diesel cars could make up 10% share of the US market by 2020. As of August, Chevrolet Cruz and some heavy-duty pickups have a diesel-engine option, and the company plans to introduce more diesel-powered vehicles in 2016. In October, Porsche announced that it plans to introduce a diesel-powered Macan crossover in the US by late 2015 or early 2016. Finally, Volkswagen is still one of the biggest players in the diesel vehicle segment, with diesel-powered cars accounting for 10% to 30% of the company’s sales.

INDUSTRY SURVEYS AUTOS & AUTO PARTS / DECEMBER 2014 15

FUEL EFFICIENCY RISING

The fuel efficiency of vehicles is on the rise in the US. The University of Michigan’s Transportation Research Institute (UMTRI) reports the average sales-weighted fuel economy of light vehicles (calculated from the monthly sales of individual models and published fuel economy ratings for city and highway combined). UMTRI reported that fuel economy increased by 25.9% from October 2007 through October 2014. Year to date through October, the index averaged 25.4 miles per gallon (mpg) in, from the 20.4 mpg average in the same period in 2013. UMTRI’s Eco-Driving Index, which estimates the average monthly emissions generated by an individual US driver, showed a 24% improvement in August 2014 compared with October 2007, when UMTRI started tracking this data.

The US Environment Protection Agency (EPA) has been imposing stringent regulations on vehicles. It has taken steps to reduce greenhouse gas (GHG) emissions in heavy-duty engines and vehicles. Fuel efficiency will increase further because of the new Corporate Average Fuel Economy (CAFE) enacted in 2011. According to the new CAFE, automakers have to increase the fuel economy of light vehicles to 35.5 mpg by 2016 and then to 54.5 mpg by 2025.

The EPA have put forward these regulations to encourage production of cleaner vehicles, reduce energy consumption by increasing the fuel economy of vehicles, and dissuade buying or manufacturing of fuel-inefficient vehicles.

ELECTRONICS IN VEHICLES

There is undoubtedly an increasing use of electronics in vehicles, from power windows to power sockets. The advancement of technology has allowed automakers to add more features to their vehicles. For example, starting in June 2014 with Chevrolet Malibu, GM is offering OnStar 4G Long Term Evolution (LTE) capability over a range of its vehicles. OnStar with 4G LTE brings a built-in Wi-Fi hotspot into and around the vehicle that can be paired with a laptop, smartphone, videogame console, and other electronic gadgets.

One use of electronics that is particularly worth noting is the development of self-driving cars. Automakers and technology companies are in a race to introduce the first self-driving car. Interestingly, Google Inc. has been developing self-driving cars and aims to introduce this technology to the market by 2017. GM also plans to introduce a self-driving Cadillac model in 2017, according to a Bloomberg article published in September. Not to be outdone, Huawei Technologies is currently designing self-driving cars that will be connected to the Internet, which the company expects to be commercially available by 2020.

While the production of self-driving vehicles may be costly, experts at the Los Angeles Auto Show in November 2014 highlighted that self-driving vehicles may reduce accidents, which together with increased productivity, would increase cost savings. In November 2013, Morgan Stanley reported that autonomous cars could contribute $1.3 trillion in annual savings to the US economy, due to reduction in fuel consumption and accidents, and $507 billion in productivity gains, as people could work while commuting.

EMERGING MARKETS STILL SHAKY

While the automotive industry in China is the largest in the world, growth of the industry in this country has been slowing. Year to date through October, China’s vehicle sales increased 8.1% compared with the year-ago period, according to LMC Automotive, slower compared with the double-digit growth experienced over the past few years. Fragile demand is holding back India from any serious growth, which is reflected in its 3.8% decline, year to date through October. Meanwhile, Western Europe is slowly rebounding, posting a 5.7% growth, year to date through October. France, however, has been left behind with a 1.4% growth, substantially lower than the growth of other large European markets such as Germany (3.0%), Italy (4.2%), Spain (18.1%), and the UK (9.5%). On the other hand, Eastern Europe’s vehicle sales saw a 9.4% decline, which mirrors Russia’s 12.7% decline year to date through October.

In South America, Brazil has been lagging in regaining the rapid economic growth it had previously exhibited, thus stalling vehicle sales, delaying future expansions, and jeopardizing profitability in the region.

16 AUTOS & AUTO PARTS / DECEMBER 2014 INDUSTRY SURVEYS

Based on LMC Automotive data, year to date through September, South America’s sales dropped 13.9%. In addition, Argentina and Brazil saw a 12.7% sales decline year to date through October.

Overall, LMC data shows that the global industry rose 3.1% year to date through October, thanks to continuing sales growth in North America; US and Canada rose 5.5% and 5.8%, respectively.

SUPPLIERS: ARE CAPACITY CONSTRAINTS A RISK?

The auto industry’s supply chain consolidated operations and reduced plant capacity by about 30% during the financial crisis, according to IRN Inc., a consulting firm. However, as sales figures improved in 2014, US auto manufacturers ramped up their production to meet demand. For instance, Ford Motor Co. has stepped up production at every plant in 2013 after raising plant capacity by 3% in 2012. Further, in 2013, the company announced plans to hire 3,000 salaried workers in 2014 and increase hourly employment by 12,000 by 2015. According to a Bloomberg article published in October 2014, Ford has hired 23,000 employees since 2011. The company also added 850 workers to help meet the demand for the 2015 F-150. This has brought Ford’s hourly employment total to 14,000, exceeding its earlier pledge of 12,000.

As automakers increase their production, it is becoming increasingly difficult for suppliers to keep up. According to the Original Equipment Suppliers Association (OESA), a trade group, the median running capacity of suppliers was at 90% in May 2014, up slightly from 89% from the year-ago period. In the same survey, suppliers cited engineering talent and production capacity as the top two significant new product launches. The trade group also highlighted that suppliers remain cautious in adding incremental capacity, which can be attributed to issues such as return on investment, excess capitalization, and risk sharing. Year to date through November, the OESA Automotive Supplier Sentiment Index averaged 58, down 4.4% from the year-ago period.

The industry faced disruptions due to material shortages, troubled suppliers, and quality issues. For instance, Chrysler’s launch of the 2014 Jeep Cherokee was delayed from an expected launch in July 2013 to the end of October, while the all-new Lincoln MKZ finally made its debut in November 2013 after months of delay.

Ford’s shrinking supplier base In October 2013, Ford, which buys about $100 billion worth of parts annually, announced a long-term plan to reduce its number of suppliers to 750 (from 1,260 in 2012). Cutting the supplier base by 40% will allow the company to reduce production costs and complexity. Under then CEO Allan Mulally, Ford’s global platform count has dropped from 27 in 2007 to 15 as of June 2014.

MANUFACTURING RETURNING TO THE US (AND MEXICO)

With billions of dollars lined up for investments, auto manufacturers are shifting operations to North America, mainly the US and Mexico. In May 2013, GM announced plans to invest $16 billion in the US by 2016. In December 2012, Ford announced plans to invest $6.2 billion by 2015, which would add 12,000 jobs (subsequently raised to 14,000). This trend is being driven by the shrinking wage gap between the US and China, company restructurings of unproductive markets, and the federal government’s efforts to increase domestic jobs. Furthermore, riding on a weaker yen, Japanese automakers manufactured 3.7 vehicles in the US in fiscal year ended March 2014 compared with 3.4 million in the year-ago period. More than a million cars and light trucks were exported from US auto plants in 2012, according to the US International Trade Commission. Companies like Chrysler and Honda are hoping to export even greater number of cars from North America (particularly from the US) in 2014.

Mexico is witnessing an upswing in its automotive industry. Year to date through September, Mexico’s auto production increased 7.5% to about 2.4 million units, whereas its exports increased 8.7% to almost 2.0 million units. The Wall Street Journal reported in October that recently announced investments in the country include the building of Kia Motors Corp’s $1.5-billion assembly plant near the Mexico border. In 2013, the Mexican auto industry looked promising with plans for $10 billion plant investments from various automakers. BMW, Toyota Motor Corp., and Daimler AG’s Mercedes-Benz are expected to announce at least $2 billion plant deals in the next year or two, following the plans also announced last year

INDUSTRY SURVEYS AUTOS & AUTO PARTS / DECEMBER 2014 17

that Nissan, Honda, Mazda, and Volkswagen would invest a total of $6 billion in Mexican plants in 2014. Mexico stands to benefit from its geographical position, lower wages, and free trade agreements (NAFTA), pushing up its share of production in North America.

ASIAN PRODUCTION SHARE OF INDUSTRY RISING

With Asia in the lead, the global automotive industry is increasingly shifting its focus to the emerging markets. Asia contributed 40.9% of global automobile production in 2012 and about 42.9% in 2013.The number is expected to rise to 44.9% in 2014 and 47.2% by 2015, according to LMC Automotive. Countries in the region are trying to develop their automobile sector through innovative policies, government influence (direct or indirect), and trade liberalization programs.

According to LMC Automotive, China will lead the expansion in Asia and is expected to open around 22 net new plants in 2015, with 75% of these new plants belonging to foreign players. India is second with seven net new light vehicle plants expected to open in 2015, followed by Indonesia and Thailand, which are expected to open five and three net new light vehicle plants, respectively.

HISPANIC BUYERS: A GROWING DEMOGRAPHIC

The Hispanic population is the fastest growing ethnic group in the US. According to the US Census Bureau, the US Hispanic population represented 17% of the country’s total population as of July 2013.

According to “State of the Hispanic Consumer—The Hispanic Market Imperative”, a second-quarter 2012 (latest available) report by Nielsen, a global consumer information and measurement firm, Hispanics are expected to account for most of the US population’s future growth. Their population is expected to rise by 167% from 2010 to 2050, versus 42% growth in the US population in the same period. In addition, according to the Nielsen report, the purchasing power of Hispanics is set to increase by 50% to $1.5 trillion in 2015 (from $1 trillion in 2010), thereby making them an important consumer segment.

Polk, the automotive research firm, reported that Hispanic consumer purchases increased in 2013, and that the top 10 brands that Hispanics preferred were Toyota, Honda, Nissan, Chevrolet, Ford, Hyundai, Dodge, Kia, VW, and Jeep. Among these brands, Toyota accounted for 17.5% of Hispanic sales in 2013 while Honda and Nissan represented 12.4% and 11.7%, respectively. According to the “2013 Hispanic Business Automotive Report” (latest available), car sales to Hispanics, particularly with the top 20 US Hispanic-owned dealerships, increased 21.1% to $4.0 billion compared with $3.3 billion from the 2011–2012 report.

DEALERSHIPS SEE RISING SALES PER STORE

Automotive dealership consolidation has long been an important trend. The number of franchised outlets in the US has declined over the past three decades, from approximately 24,725 in 1983 to 17,838 as of January 1, 2014, a slight decrease from 17,851 in the year-ago period, according to Urban Science, an auto industry consulting firm. During the period mentioned, the number of US dealerships trended steadily downward, with closures (mostly domestic brands) outweighing openings (mostly Asian brands).

Over the past five years though, the dealership network has been maintaining a conservative rate, setting a new normal pattern of increasing sales per dealer, leading to slighter decreases compared with sharp decreases in prior years. Moreover, based on the vehicle sales of 15.6 million (which is slightly different from Ward’s Automotive Reports), Urban Science shows that US new vehicle sales rose to an average of 874 sales per dealership, up 7.1% from the prior-year average of 812. S&P Capital IQ expects 2014 sales of new vehicles to reach 16.4 million units, with further gains to 16.8 million in 2015.

Higher sales per store have a huge impact on dealer profitability. The top 125 dealers—ranked based on retail unit sales of new cars and light trucks—continue to take a larger share of the US sales pie. These top groups sold more than 3.14 million new cars and light trucks in 2013, or 20% of the industry’s total sales in these categories, according to Automotive News (March 17, 2014). The 2013 sales of the top 125 dealers

18 AUTOS & AUTO PARTS / DECEMBER 2014 INDUSTRY SURVEYS

represent a 19% increase compared with 2012 sales. Sixty-five of these groups added at least one dealership last year, and only 15 of the 125 groups had a reduced net in their rooftop total.

CHANGE IN GLOBAL RANKINGS

The dominance of North America is gradually declining, and the Asia-Pacific region is strengthening its presence in the industry on the back of supportive demographic trends. The automotive market is shifting toward a new order in terms of ranking of geographies by sales and production. The middle-income population segment that can afford a vehicle is growing at a rapid rate in the Asia-Pacific region, causing this restructuring of the automotive industry, along with various other factors.