car sharing industry boston university student research and events/research challenge... · cfa...

TRANSCRIPT

Boston University Student Research This report is published for educational purposes

only by students competing in the CFA Institute

Research Challenge.

Ticker: ZIP (NASDAQ) Recommendation: BUY

Price: $14.28 (As of 12/09/11) Price Target: $19.45

Earnings/Share

(Normalized to 42.48mm weighted average diluted shares outstanding)

Mar. Jun. Sept. Dec. Year P/E Ratio

2008A $(0.17) $(0.08) $(0.04) $(0.05) $(0.34) NA 2009A (0.07) (0.04) (0.03) 0.03 (0.11) NA 2010A (0.13) (0.12) (0.06) (0.02) (0.33) NA 2011E (0.14) (0.13) 0.02 0.00 (0.26) NM

Source: CapitalIQ, Student Research

GREEN LIGHT TO BUY ZIPCAR

We initiate coverage of Zipcar with a one-year price target of $19.45, offering a 36%

upside in comparison to a ten-year standard deviation of returns of the Small Cap

S&P600 Index of 20%. ZIP will maintain its position as the world’s leader in car sharing

through aggressive expansion into markets like Europe, growing membership at a

projected CAGR of 17% through 2016.

Zipcar’s value proposition will drive membership growth, which will in turn drive

revenues. Zipcar use is about 69% less expensive than owning a car, which is a strong

incentive for new members to join, especially when coupled with increasing costs of

living. We estimate Zipcar’s total revenue growth at 21% CAGR from 2011 through

2016, as a result of new members and increased vehicle utilization.

Increased utilization and growing fee revenues will drive margin expansion which

will boost earnings. Margin expansion will be driven by higher growth in fee revenue,

which we expect to reach 15% of total revenue by 2016, up from 14% in 2011. We

forecast EBITDA margin to be 16% by 2016, in comparison to 11% in 2011.

Zipcar’s strong solvency position provides room for additional expansion. With the

latest debt-to-equity ratio of 35%, Zipcar has an estimated 3.7% after-tax cost of debt.

The Company’s asset-backed security notes allow for lower rate borrowings, which can

be utilized for vehicle purchases. Zipcar has shown its ability to obtain additional term

loans of up to $40 million to finance acquisitions.

ZIP is an emerging story which makes it hard for investors to evaluate early in its

business life cycle, similar to a venture capital company. We believe this leads to a

misunderstanding of the Company’s potential and the low market valuation; however

when all variables are well considered, we are confident that ZIP is a BUY.

Zipcar, Inc.

Car Sharing Industry

Date: Dec. 12, 2011

-50%

0%

Apr-11 Jul-11 Oct-11

ZIP vs. S&P 600(Apr. 2011 - Dec. 2011)

ZIP S&P 600

Market Profile

52-Week Price Range $31.50/$13.87

Average Daily Volume (USD mm) 0.36

Beta 1.17

Shares out (USD mm) 39.3

Market Cap (USD mm) 561.2

Institutional Holdings (USD mm) 233.1

Insider Holdings (USD mm) 19.0

Total Debt to Equity 0.35

Return on Assets (LTM, 3Q11) 0.3%

Return on Equity (LTM, 3Q11) -7.8%

Source: CapitalIQ Source: CapitalIQ

CFA Institute Research Challenge December 12, 2011

2

BUSINESS DESCRIPTION Zipcar has grown revenues and membership rapidly but has so far made slow progress towards

profitability.

Zipcar, founded in 2000 and based in Cambridge, Massachusetts, operates the world’s leading car sharing

network. Zipcar went public in April of 2011 and has 72% of the car-sharing market share, which is only a

small decrease from its 75% market share in 2005 due to its continued domination of the industry. The

Company has achieved five-year CAGR of 48% in organic membership growth and the acquisitions of

Flexcar and Streetcar in 2007 and 2011, added an additional 11% to membership to each year.

A key strength of the firm is the technology utilized in its operations.

Vehicles are reserved by phone, the internet, or through smart-phone applications and are unlocked with a

keyless entry card (Zipcard), using RFID technology. Fleet operations are supported by software that collects

real-time data on Zipsters and allows the Company to monitor vehicle usage and profitability.

As of 3Q 2011 the Company had operations in the United States, Canada, and the United Kingdom, and

about 650,000 members, 9,500 cars, 600employees, and a presence in over 130 cities including 15 major

metropolitan areas. Despite its revenue growing at a CAGR of 67% from 2005 to 2010, Zipcar is making

slow progress to profitability; net income margin of 1% was declared for the third quarter of 2011, but

guidance for 4Q2011 is for a net loss.

Services: ZIP provides an attractive value proposition for both individual and business

customers, which should encourage new members to join.

Fleet Rental: ZIP provides self-service vehicles in convenient locations for an annual fee of $60

plus an hourly rate of between $7.75 and $13.50 or a monthly fee of $50 and a 10% discount on

driving rates. Gas, insurance, and up to 180 free miles per day are included in the price. This results

in savings of about 69% versus owning a car, despite decreased convenience (see Figure 1 and

Exhibit 1 in Appendix).

FastFleet: “FastFleet” is a proprietary vehicle-on-demand software that ZIP leases to organizations

that manage their own fleet of vehicles, at a rate of $65 to $95 per car. This allows organizations to

track vehicles, analyze usage and diagnostic data, and improve efficiency, saving as much as

$1,250 a month per vehicle.

Cost Drivers: ZIP’s can distribute high fixed costs across its 650,000 members, and will increase

utilization to improve profitability.

ZIP achieves economies of scale through distribution of fixed cost such as gas, parking, and car purchases,

over its fleet (see Figure 2 and Exhibit 2 in Appendix). ZIP passes on gas price increases to customers, which

keeps its own costs down, while still offering a cheaper alternative to customers owning vehicles.

Increasing utilization per vehicle will lead to higher revenues per vehicle, which will mean higher

profitability as ZIP covers its fixed costs.

Revenue per vehicle per day is currently $65, which translates to utilization of 6.5 hours; both have

been increasing historically.

We believe this trend will continue as ZIP expands its corporate customer base, bringing more

weekday utilization (see Figure 3).

Additionally, we believe that management is capable of achieving their stated target utilization rate

of 9 hours, based on their record with past goals (see discussion of Management on page 4).

CUSTOMERS Zipcar’s plan for increasing utilization includes a new focus on business and governments.

Individuals: Zipcar has traditionally targeted middle-class customers between the ages of 20 and

35, who do not own cars and live in densely populated cities. These customers usually utilize

Zipcar for weekend trips for social gatherings and shopping.

Universities: Zipcar operates in over 150 college campuses, offering car sharing to those between

the ages of 21 and 25 without the additional charges required by traditional car rental firms. As of

September 2011, universities make up 10% of the total revenue base.

Figure 3: Historical revenue per

vehicle per day has been increasing.

Assuming a constant hourly rate of

$10, this means each car is being

used for more hours daily.

y = 0.013x - 503

R² = 0.722

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

Sep-09 Apr-11 Dec-12 Aug-14 Mar-16

Usage Revenue Per Vehicle Per Day

Actual Predicted

Car Ownership Zipcar

Private Ownership $4,733 $-

Zipcar $- $455

Public Transit $720 $720

Taxi $192 $384

Conventional Rental $- $200

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

Cost

in U

SD

Car Ownership vs. Zipcar Costs

Per Year

Figure 1: Zipsters spend an average

$1,800 a year on transportation costs,

versus $5,500 per year for car owners.

Sources: Victoria Transport Institute, US

Dept of Transportation, Office of Fair

Trading, TaxiFareFinder.com

$(1,000)

$(500)

$-

$500

$1,000

$1,500

$2,000

$2,500

Monthly Loss Per Vehicle

SG&A

R&D

Membership

ServicesDepreciation

Parking

Insurance

Gas

Maintenance

Revenue: $1,888

Loss: 18.1%

Figure 2: Zipcar currently experiences

an 11.5% loss on each vehicle without

accounting for fee revenues, a loss they

need to address through increased

utilization.

CFA Institute Research Challenge December 12, 2011

3

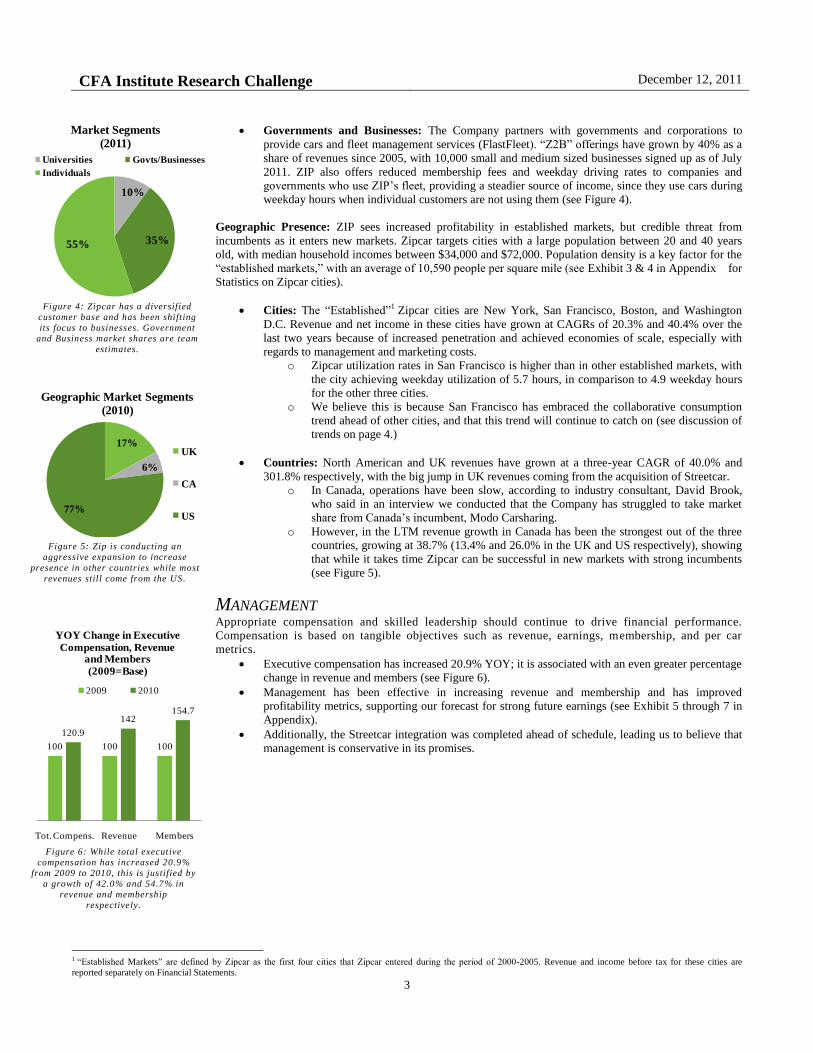

Governments and Businesses: The Company partners with governments and corporations to

provide cars and fleet management services (FlastFleet). “Z2B” offerings have grown by 40% as a

share of revenues since 2005, with 10,000 small and medium sized businesses signed up as of July

2011. ZIP also offers reduced membership fees and weekday driving rates to companies and

governments who use ZIP’s fleet, providing a steadier source of income, since they use cars during

weekday hours when individual customers are not using them (see Figure 4).

Geographic Presence: ZIP sees increased profitability in established markets, but credible threat from

incumbents as it enters new markets. Zipcar targets cities with a large population between 20 and 40 years

old, with median household incomes between $34,000 and $72,000. Population density is a key factor for the

“established markets,” with an average of 10,590 people per square mile (see Exhibit 3 & 4 in Append ix for

Statistics on Zipcar cities).

Cities: The “Established”1 Zipcar cities are New York, San Francisco, Boston, and Washington

D.C. Revenue and net income in these cities have grown at CAGRs of 20.3% and 40.4% over the

last two years because of increased penetration and achieved economies of scale, especially with

regards to management and marketing costs.

o Zipcar utilization rates in San Francisco is higher than in other established markets, with

the city achieving weekday utilization of 5.7 hours, in comparison to 4.9 weekday hours

for the other three cities.

o We believe this is because San Francisco has embraced the collaborative consumption

trend ahead of other cities, and that this trend will continue to catch on (see discussion of

trends on page 4.)

Countries: North American and UK revenues have grown at a three-year CAGR of 40.0% and

301.8% respectively, with the big jump in UK revenues coming from the acquisition of Streetcar.

o In Canada, operations have been slow, according to industry consultant, David Brook,

who said in an interview we conducted that the Company has struggled to take market

share from Canada’s incumbent, Modo Carsharing.

o However, in the LTM revenue growth in Canada has been the strongest out of the three

countries, growing at 38.7% (13.4% and 26.0% in the UK and US respectively), showing

that while it takes time Zipcar can be successful in new markets with strong incumbents

(see Figure 5).

MANAGEMENT Appropriate compensation and skilled leadership should continue to drive financial performance.

Compensation is based on tangible objectives such as revenue, earnings, membership, and per car

metrics.

Executive compensation has increased 20.9% YOY; it is associated with an even greater percentage

change in revenue and members (see Figure 6).

Management has been effective in increasing revenue and membership and has improved

profitability metrics, supporting our forecast for strong future earnings (see Exhibit 5 through 7 in

Appendix).

Additionally, the Streetcar integration was completed ahead of schedule, leading us to believe that

management is conservative in its promises.

1 “Established Markets” are defined by Zipcar as the first four cities that Zipcar entered during the period of 2000-2005. Revenue and income before tax for these cities are

reported separately on Financial Statements.

Figure 4: Zipcar has a diversified

customer base and has been shifting

its focus to businesses. Government

and Business market shares are team

estimates.

Figure 5: Zip is conducting an

aggressive expansion to increase

presence in other countries while most

revenues still come from the US.

100 100 100

120.9

142154.7

Tot. Compens. Revenue Members

YOY Change in Executive

Compensation, Revenue and Members

(2009=Base)

2009 2010

Figure 6: While total executive

compensation has increased 20.9%

from 2009 to 2010, this is justified by

a growth of 42.0% and 54.7% in

revenue and membership

respectively.

17%

6%

77%

Geographic Market Segments

(2010)

UK

CA

US

10%

35%55%

Market Segments

(2011)

Universities Govts/Businesses

Individuals

CFA Institute Research Challenge December 12, 2011

4

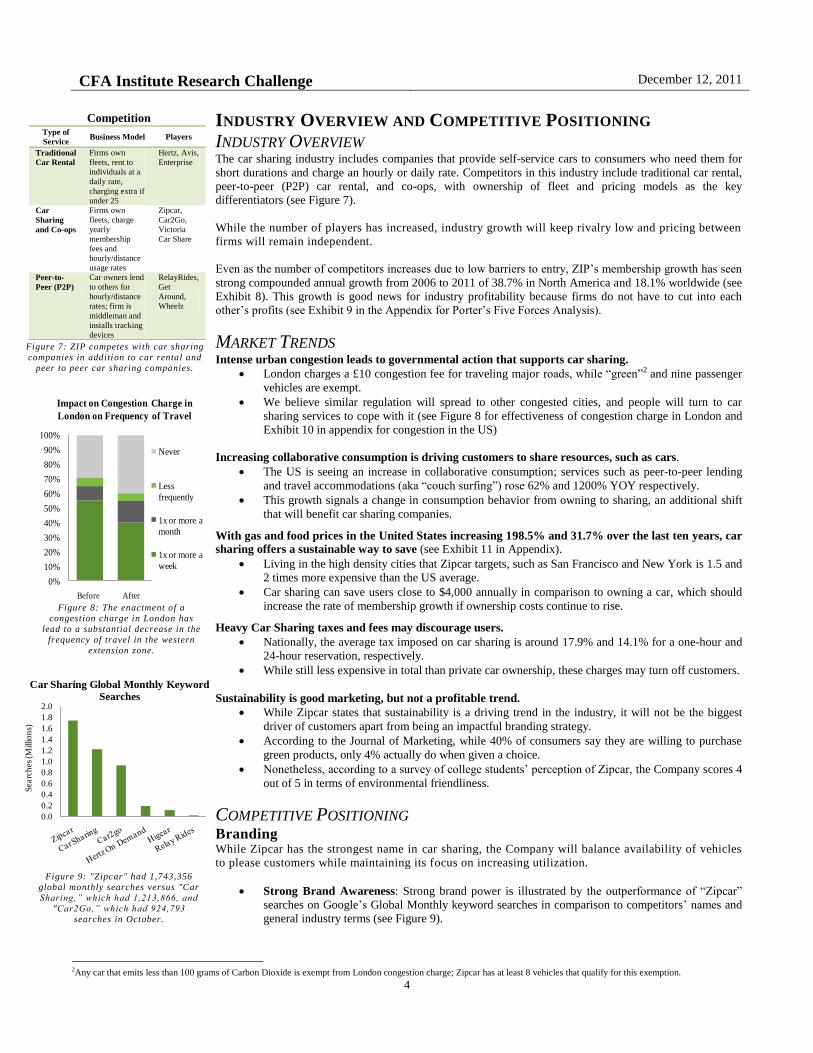

INDUSTRY OVERVIEW AND COMPETITIVE POSITIONING

INDUSTRY OVERVIEW The car sharing industry includes companies that provide self-service cars to consumers who need them for

short durations and charge an hourly or daily rate. Competitors in this industry include traditional car rental,

peer-to-peer (P2P) car rental, and co-ops, with ownership of fleet and pricing models as the key

differentiators (see Figure 7).

While the number of players has increased, industry growth will keep rivalry low and pricing between

firms will remain independent.

Even as the number of competitors increases due to low barriers to entry, ZIP’s membership growth has seen

strong compounded annual growth from 2006 to 2011 of 38.7% in North America and 18.1% worldwide (see

Exhibit 8). This growth is good news for industry profitability because firms do not have to cut into each

other’s profits (see Exhibit 9 in the Appendix for Porter’s Five Forces Analysis).

MARKET TRENDS Intense urban congestion leads to governmental action that supports car sharing.

London charges a £10 congestion fee for traveling major roads, while “green”2 and nine passenger

vehicles are exempt.

We believe similar regulation will spread to other congested cities, and people will turn to car

sharing services to cope with it (see Figure 8 for effectiveness of congestion charge in London and

Exhibit 10 in appendix for congestion in the US)

Increasing collaborative consumption is driving customers to share resources, such as cars.

The US is seeing an increase in collaborative consumption; services such as peer-to-peer lending

and travel accommodations (aka “couch surfing”) rose 62% and 1200% YOY respectively.

This growth signals a change in consumption behavior from owning to sharing, an additional shift

that will benefit car sharing companies.

With gas and food prices in the United States increasing 198.5% and 31.7% over the last ten years, car

sharing offers a sustainable way to save (see Exhibit 11 in Appendix).

Living in the high density cities that Zipcar targets, such as San Francisco and New York is 1.5 and

2 times more expensive than the US average.

Car sharing can save users close to $4,000 annually in comparison to owning a car, which should

increase the rate of membership growth if ownership costs continue to rise.

Heavy Car Sharing taxes and fees may discourage users.

Nationally, the average tax imposed on car sharing is around 17.9% and 14.1% for a one-hour and

24-hour reservation, respectively.

While still less expensive in total than private car ownership, these charges may turn off customers.

Sustainability is good marketing, but not a profitable trend.

While Zipcar states that sustainability is a driving trend in the industry, it will not be the biggest

driver of customers apart from being an impactful branding strategy.

According to the Journal of Marketing, while 40% of consumers say they are willing to purchase

green products, only 4% actually do when given a choice.

Nonetheless, according to a survey of college students’ perception of Zipcar, the Company scores 4

out of 5 in terms of environmental friendliness.

COMPETITIVE POSITIONING Branding While Zipcar has the strongest name in car sharing, the Company will balance availability of vehicles

to please customers while maintaining its focus on increasing utilization.

Strong Brand Awareness: Strong brand power is illustrated by the outperformance of “Zipcar”

searches on Google’s Global Monthly keyword searches in comparison to competitors’ names and

general industry terms (see Figure 9).

2Any car that emits less than 100 grams of Carbon Dioxide is exempt from London congestion charge; Zipcar has at least 8 vehicles that qualify for this exemption.

Type of

Service Business Model Players

Traditional

Car Rental

Firms own

fleets, rent to

individuals at a

daily rate,

charging extra if

under 25

Hertz, Avis,

Enterprise

Car

Sharing

and Co-ops

Firms own

fleets, charge

yearly

membership

fees and

hourly/distance

usage rates

Zipcar,

Car2Go,

Victoria

Car Share

Peer-to-

Peer (P2P)

Car owners lend

to others for

hourly/distance

rates; firm is

middleman and

installs tracking

devices

RelayRides,

Get

Around,

Wheelz

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Sea

rch

es (M

illio

ns)

Car Sharing Global Monthly Keyword

Searches

Figure 7: ZIP competes with car sharing

companies in addition to car rental and

peer to peer car sharing companies.

Competition

Figure 9: "Zipcar" had 1,743,356

global monthly searches versus "Car

Sharing,” which had 1,213,866, and

"Car2Go,” which had 924,793

searches in October.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Before After

Impact on Congestion Charge in

London on Frequency of Travel

Never

Less

frequently

1x or more a

month

1x or more a

week

Figure 8: The enactment of a

congestion charge in London has

lead to a substantial decrease in the

frequency of travel in the western

extension zone.

CFA Institute Research Challenge December 12, 2011

5

Online Reviews are good, not great: Out of a sample of 633 Yelp.com ratings across the

established markets, Boston, NY, San Francisco, and Chicago, 57.8% of reviewers gave Zipcar 4+

stars (see Figure 10 and Exhibit 12 in Appendix). Most negative reviewers complained about the

unavailability of cars, which is a problem management has stated it will focus on as markets mature

and more members share the same fleet.

Over 90% of customers recommend ZIP: We conducted an anonymous survey in October with

141 respondents, 35% of which were either current or past users of Zipcar. Our results indicate that

over 90% of current and past Zipcar users would recommend Zipcar and its services to a family or

friend. This number, better known as the Net Promoter Score, is a critical metric Zipcar

management uses to measure customer satisfaction (see Exhibit 13 in Appendix).

Competition ZIP’s market leadership and competitive positioning should enable it to enter new markets with ease.

ZIP holds 72% of the car sharing market share in 2011 (by membership), with the next biggest competitor

holding only 5%. While Car2Go, Connect by Hertz, and RelayRides are often cited as threats to Zipcar, it is

apparent that they have not made a significant dent in the market and should not pose a credible threat to

Zipcar’s leadership. The rest of the industry is made up of smaller players with 5,000 or fewer members (see

Figure 11).

Zipcar has positioned itself as a broad market differentiator, targeting a large market and charging premium

prices while offering more services. Zipcar has the largest fleet in the most number of locations and uses

advanced technology, enabling it to provide better service than competitors. Zipcar plans to maintain this

position via aggressive expansion plans.

While competitors may take members, they are unable to impact utilization, the main

determinant of profitability.

Connect by Hertz and Relay Rides pose the greatest threats in terms of competitive pricing. Hertz

offers a no membership or enrollment fee plan with One Way trips available. Relay Rides also offers

free membership and rates start at $5; in addition, cars generate an average of $250 per month with the

owners keeping 65% of revenues.

However, these players are competing on price while Zipcar is focusing on service. Moreover, the key driver

of profitability is utilization of cars, and while a loss in market share may decrease membership, we believe

Zipcar can sustain utilization rates, thus competition should not present a credible threat to company

performance (see Figure 3 on page 2).

INVESTMENT SUMMARY We initiate coverage of Zipcar with a BUY rating and a one-year target price of $19.45, offering a

36% upside from its closing stock price as of December 9, 2011.

The Company’s future earnings will be driven by growth in capacity utilization coupled with an increase in

share of revenue from fees:

Future Cash Inflows = ƒ(Number of vehicles*Usage revenue per vehicle, Fee Revenue)

Implied capacity utilization growth will be driven by membership growth coupled with higher

weekday usage from business customers.

We project that Zipcar’s membership will grow at a 17.0% CAGR over the next five years, in

comparison to 53.3% CAGR from 2006 to 2011.

In addition, ZIP’s Z2B offerings increased 40% as a share of revenue since 2005 and are projected

to grow further, which will boost weekday usage hours.

Membership growth per vehicle and higher weekday utilization from business customers result in

increased usage revenue per the vehicle (see Figure 13 for forecasts).

While Zipcar may enter Asia in the long-term, we do not see Asia as target market for the next five

years.

The Company’s international strategy focuses on congested cities with average GDP per capita of

$34,000 to $71,000.

Figure 12: ZIP is positioned as a broad

market differentiator; Car2Go seems to

be trying to edge into this space while

Connect by Hertz is concentrating on

maintaining cost leadership.

DifferentiationCost Leadership

Bro

ad

Mark

etN

arr

ow

Mark

et

Competitive Positioning Map

0%

10%

20%

30%

40%

50%

60%

70%

Zipcar Yelp Ratings

Great (4+ Stars) Neutral (3 Stars)

Negative (2- Stars)

Figure 10: Zipcar Yelp ratings show

an overall positive perception of the

Company in its top established

markets.

Zipcar

72.2%

Car2Go

5.0%

Connect by Hertz

3.3%

RelayRides, Cityzen

Cars, Higear,

Livop, Greenwheels,

Tamyca, and

Enterprise WeCar

1.9% Others

17.6%

Car Sharing Market Share by Members

(2011)

Figure 11: Zipcar has72.2% of the car

sharing market share, as measured in

members.

Source: tfl.gov.uk

CFA Institute Research Challenge December 12, 2011

6

Although Asian cities such as Tokyo, Singapore, and Hong Kong currently have these

characteristics, they are too far apart geographically to achieve the scale efficiencies that are

possible in Europe (see Exhibit 14).

Entrance into Asia also requires special regulatory relationships. Thus, Zipcar will prioritize

expansion into Europe and only enter Asia once these operations are under control, in five to ten

years.

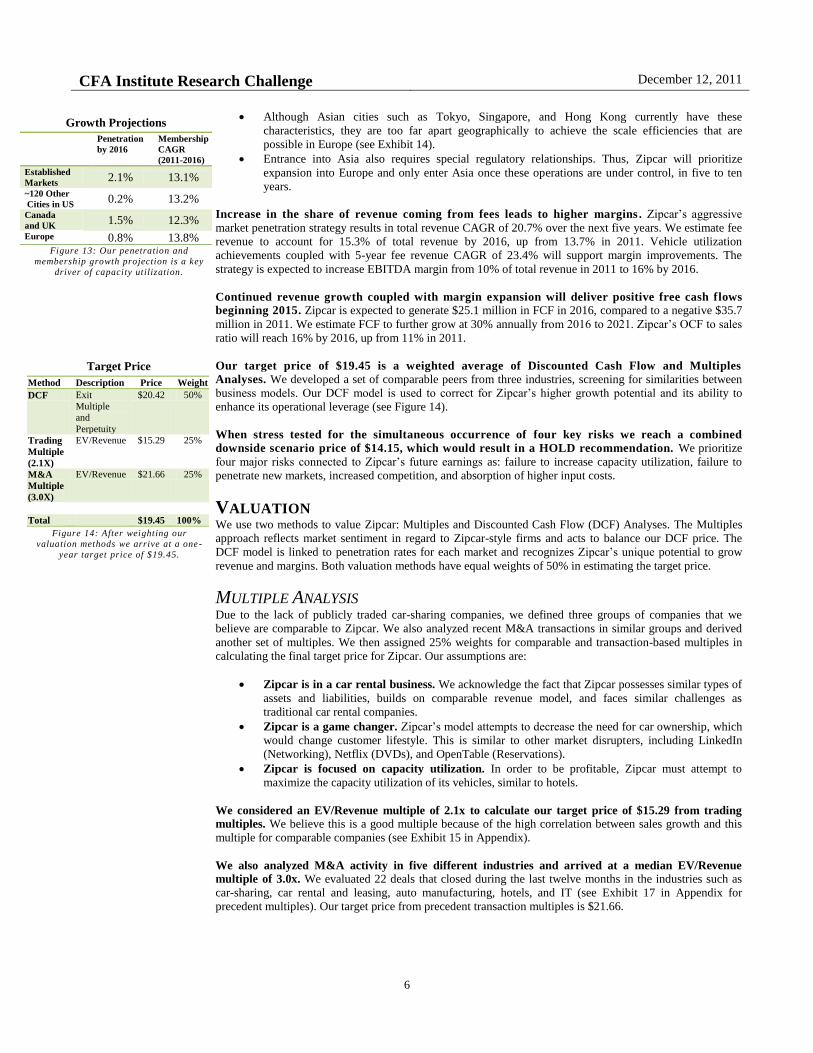

Increase in the share of revenue coming from fees leads to higher margins . Zipcar’s aggressive

market penetration strategy results in total revenue CAGR of 20.7% over the next five years. We estimate fee

revenue to account for 15.3% of total revenue by 2016, up from 13.7% in 2011. Vehicle utilization

achievements coupled with 5-year fee revenue CAGR of 23.4% will support margin improvements. The

strategy is expected to increase EBITDA margin from 10% of total revenue in 2011 to 16% by 2016.

Continued revenue growth coupled with margin expansion will deliver positive free cash flows

beginning 2015. Zipcar is expected to generate $25.1 million in FCF in 2016, compared to a negative $35.7

million in 2011. We estimate FCF to further grow at 30% annually from 2016 to 2021. Zipcar’s OCF to sales

ratio will reach 16% by 2016, up from 11% in 2011.

Our target price of $19.45 is a weighted average of Discounted Cash Flow and Multiples

Analyses. We developed a set of comparable peers from three industries, screening for similarities between

business models. Our DCF model is used to correct for Zipcar’s higher growth potential and its ability to

enhance its operational leverage (see Figure 14).

When stress tested for the simultaneous occurrence of four key risks we reach a combined

downside scenario price of $14.15, which would result in a HOLD recommendation. We prioritize

four major risks connected to Zipcar’s future earnings as: failure to increase capacity utilization, failure to

penetrate new markets, increased competition, and absorption of higher input costs.

VALUATION We use two methods to value Zipcar: Multiples and Discounted Cash Flow (DCF) Analyses. The Multiples

approach reflects market sentiment in regard to Zipcar-style firms and acts to balance our DCF price. The

DCF model is linked to penetration rates for each market and recognizes Zipcar’s unique potential to grow

revenue and margins. Both valuation methods have equal weights of 50% in estimating the target price.

MULTIPLE ANALYSIS Due to the lack of publicly traded car-sharing companies, we defined three groups of companies that we

believe are comparable to Zipcar. We also analyzed recent M&A transactions in similar groups and derived

another set of multiples. We then assigned 25% weights for comparable and transaction-based multiples in

calculating the final target price for Zipcar. Our assumptions are:

Zipcar is in a car rental business. We acknowledge the fact that Zipcar possesses similar types of

assets and liabilities, builds on comparable revenue model, and faces similar challenges as

traditional car rental companies.

Zipcar is a game changer. Zipcar’s model attempts to decrease the need for car ownership, which

would change customer lifestyle. This is similar to other market disrupters, including LinkedIn

(Networking), Netflix (DVDs), and OpenTable (Reservations).

Zipcar is focused on capacity utilization. In order to be profitable, Zipcar must attempt to

maximize the capacity utilization of its vehicles, similar to hotels.

We considered an EV/Revenue multiple of 2.1x to calculate our target price of $15.29 from trading

multiples. We believe this is a good multiple because of the high correlation between sales growth and this

multiple for comparable companies (see Exhibit 15 in Appendix).

We also analyzed M&A activity in five different industries and arrived at a median EV/Revenue

multiple of 3.0x. We evaluated 22 deals that closed during the last twelve months in the industries such as

car-sharing, car rental and leasing, auto manufacturing, hotels, and IT (see Exhibit 17 in Appendix for

precedent multiples). Our target price from precedent transaction multiples is $21.66.

Growth Projections

Target Price

Method Description Price Weight

DCF Exit

Multiple

and

Perpetuity

$20.42 50%

Trading

Multiple

(2.1X)

EV/Revenue $15.29 25%

M&A

Multiple

(3.0X)

EV/Revenue $21.66 25%

Total $19.45 100%

Figure 14: After weighting our

valuation methods we arrive at a one -

year target price of $19.45.

Figure 13: Our penetration and

membership growth projection is a key

driver of capacity utilization.

Penetration

by 2016

Membership

CAGR

(2011-2016)

Established

Markets 2.1% 13.1%

~120 Other

Cities in US 0.2% 13.2%

Canada

and UK 1.5% 12.3%

Europe 0.8% 13.8%

CFA Institute Research Challenge December 12, 2011

7

DCF ANALYSIS We estimated Zipcar’s value at $20.42 per share based on our DCF model. The driving metrics in our

model are the membership growth and vehicle utilization rates, which feed into revenue growth and

profitability.

Membership growth: Market specific penetration rates indicate that United States will account for 65% of

total members by 2016 with the other 19% coming from United Kingdom and Canada. The remaining 16% of

total members will come from expansion into new markets in Europe (see Exhibit 18 in Appendix for

detailed membership projections). We do not believe that Zipcar will enter Asia within the next five years as

explained earlier.

Revenue will grow at a CAGR of 20.7% through 2011-2016 based on growing usage revenue

combined with increasing share of fee revenue, a trend supported by Zipcar’s historical performance.

Usage revenue reaches $525.4 million by 2016, a 20.3% CAGR over the next five years. Fee

revenue grows to 15.3% of total revenue by 2016, up from 13.7% in 2011. Membership growth

coupled with increase in business customers leads to higher usage revenue as well as increase in

fees.

Revenue growth combined with efficient cost control leads to expanding EBIT margin, which

drives consistently improving free cash flow. Free cash flow turns positive by 2015, and grows at a

30% CAGR through 2016-21.

Our WACC is estimated at 8.7% based on equity, debt, and minority interest. We further used three different

methods to estimate beta for Zipcar (see Exhibit 19).

Our DCF price: We calculated the DCF price of $20.42 using a combination of two methods: perpetual

growth rate and exit multiples method.

We apply two stage growth rates when calculating the terminal value. We computed 30% yearly

FCF growth through 2016-21. We further use a 3.0% perpetual growth after 2021 to reflect the

industry’s significant growth potential. That results in a target price of $20.61, which is weighted

50% into our DCF price.

We also applied an EV/Revenue exit multiple of 2.1x to FCF in 2016, based upon our trading

multiples analysis, which gives a target price of $20.23, also weighted 50% into our DCF Price.

SENSITIVITY Zipcar’s ability to control expenses via operating leverage enhancements (capacity utilization)

and fleet optimization is a critical factor in our model. Historically, expenses (as % of sales) have

declined by 150 bps/year. To stress test our analysis, we apply a 75 bps upswing in expenses (as % of

sales) which results in a -45% change to our target price.

Sensitivity tests are also applied to valuation analysis inputs such as WACC, the perpetuity growth factor,

EV/Revenue multiples and operational drivers such as revenue and expenses. On a stand-alone basis, our

BUY recommendation holds under every test except for expenses (+ 75bps). Zipcar’s ability to gradually

enhance operational leverage as they increase market penetration will be crucial to translating top-line

revenue into EPS (see Exhibit 20)

Though unlikely, our ultimate best/worst case scenarios which are driven by the simultaneous occurrence of

all five sensitivities result in share prices of $34.65/$8.21.

FINANCIAL ANALYSIS After performing a sanity check through the analysis of historical figures using 2008-11 experience we

strongly believe that our projections are achievable.

Revenue Growth: Our projections are conservative in relation to historical numbers and recent

developments provide compelling support for projections (see Figure 16).

Domestic revenue reached record $136.8 million for the nine months period ended September 30,

2011, presenting a 26.7% YOY. Established markets account for 75.3% of US revenue as of the

last reported date, and remain a main driver for the total US revenue with a 22.8% growth

compared to the same nine months period in 2010.

CAGR Historical 2008- 2011

Projected 2012-2016

Revenue 31.7% 20.7%

Usage

Revenue

29.3% 20.3%

Fee

Revenue

54.7% 24.7%

Membership 37.7% 17.0%

Figure 16: Our projected growth is

consistently lower than historical growth

in order to remain conservative.

Conservative Projections

Item

%

Risk Premium 6.49%

Beta Estimate 1.17

Risk Free:

30 Yr Treasury 2.92%

After-tax

Cost of debt 3.70%

Weight

25.90%

Cost of Equity 10.51%

Weight

73.90%

Cost of

Minority

Interest

0.00%

Weight

0.20%

WACC

8.73%

Figure 15: We estimated our

WACC to be 8.7%.

Weighted Average Cost of

Capital

CFA Institute Research Challenge December 12, 2011

8

Zipcar’s revenue from international operations increased $15.9 million, or 61.2%, for the

comparable nine months ended periods, driven by $2.7 million increase in revenue from Canada

and $13.2 million increase in revenue from United Kingdom.

Margins: ZIP has improved operational efficiency historically, which should lead to positive EBIT margins

by 2012. In addition, higher utilization rates coupled with an increase in fee revenue result in margin

improvements. We believe historical numbers are consistent with our projections, where EBIT reaches

positive margin by 2012, and equals 4% by 2016.

Cash Flows: Cash flow growth has remained strong up to 2011, a trend which we expect to continue. Cash

flows from operating activities turned positive in 2009 and reached $17.8 million for the nine months ending

September 30, 2011. We foresee this number will keep growing as the Company starts turning higher returns

on each of the vehicles. Unlevered free cash flow, however, is not expected to turn positive until 2015.

Balance Sheet and Financing: ZIP has a strong balance sheet, which places it in a favorable position for

expansion in the future. As 3Q2011, Zipcar had $88 million in cash, which is an adequate source of funding

for future expansions.

Historically, the Company was able to secure additional term loans for the total amount of $40

million to fund its acquisitions. However, Zipcar paid off those term loans after its initial public

offering, and its latest outstanding principal amount of debt equals to $75.3 million. It is comprised

of $50.0 million under ABS facility, and $25.3 million under Capital Lease Obligations (see

Exhibit 21for debt structure).

Based on a leverage coverage ratio analysis of comparable companies in the traditional car rental

industry, ZIP is in a better position to service its debt; its Debt/EBITDA ratio is 3.0x compared to

an industry median of 7.1x (see Exhibit 22 for leverage ratio analysis).

MARKET’S PERCEPTION While the market has celebrated good news like a government contract, we believe the market has

discounted ZIP’s share price too heavily due to worries about profitability.

In October, ZIP’s stock increased with the news of a secured government contract. The

market recognized that this partnership would increase weekday utilization, a key to profitability.

In November, ZIP offered negative net income guidance for Q4, and the share price dropped

by 21%. This announcement only reinforced concerns about Zipcar’s ability to produce positive

earnings. However, we believe that near term losses does not negate future sustainable profitability.

Zipcar’s launch of its Zipvan service was received with doubts. The market demonstrated a

concern with Zipcar’s attempt to directly compete with U-Haul, the leader in the moving space. We

believe that this service will be appreciated by Zipsters, who responded in our survey saying that

moving was among their top motivations for using Zipcar.

Figure 18: Zipcar has generally underperformed the market due to investor worries about future

profitability.

Historical

2008-2011 Projected 2012-2016

EBIT

Margin

Average

(3%) 3%

Fleet Costs

as % of

Rev

79% - 66% 64% - 60%

Figure 17: Our projected margins are

in line with historical numbers.

Margin Projections

CFA Institute Research Challenge December 12, 2011

9

INVESTMENT RISKS The combined effect of four downside risks brings the target price to $14.15, a 27% decrease from the

one-year target price of $19.45, which would result in a HOLD recommendation (see Exhibit 23).

Failure to Increase Capacity Utilization, High Risk – 35%

The key driver to improving profitability is ZIP’s ability to increase capacity utilization rates.

We estimate a 35% probability that ZIP will fail in its attempt to increase member usage and

optimize pricing. To accurately estimate these effects, we put a ceiling on revenue per vehicle per

day at $65, which was originally projected to be $90 by 2016.

Marketing expenses under SG&A also increased at an addition .025%, assuming that ZIP’s

marketing strategies would fail in increasing awareness for established markets.

This stress-test decreases the target price by 36% to $12.48, resulting in a SELL recommendation.

Failure to Penetrate New Markets, High Risk – 30%

To estimate the effects of an unsuccessful entrance into the European markets, we discounted the total

number forecasted members in Europe by 90% and increased the loss on sale cars, which still resulted in a

BUY recommendation with a new target price at $15.95, a decrease of 18%.

Increased Competition, Moderate Risk – 20%

New players are entering the car sharing industry at a rapid rate, with about 3 players entering into the

industry every year since 2000.

These firms pose a threat to Zipcar’s market share and future member growth.

We quantified this risk by decreasing total membership base by 15% and increasing SG&A

expenses by .5% every year.

This results in a SELL recommendation with a 30% decrease in the price to $13.70.

Absorption of Input Costs, Low Risk – 15%

Zipcar relies on partnerships and 3rd party vendors such as vehicle manufacturers, insurance companies, and

other maintenance providers to offer its car-sharing services at a competitive price.

An unfavorable turn in economic forces that affect these suppliers could increase ZIP’s fleet

operation expense growth by an additional .9% annually.

This stress-test still results in a BUY recommendation of $16.55, a decrease 15% from the one-year

target price.

RECOMMENDATION After considering all risk scenarios, we reiterate our BUY recommendation. Looking toward the horizon, we

believe ZIP will continue to accelerate, leaving its competition in the rear view mirror.

These fundamentals, combined with attractive valuation, indicate a 36% upside to the stock.

CFA Institute Research Challenge December 12, 2011

10

APPENDIX

Exhibit 1: While car sharing is more cost effective than private car ownership, it is still not as convenien t as having a car

available at one’s disposal. Combining car sharing with other forms yields similar convenience to private ownership.

Source: Victoria Transport Policy Institute.

Exhibit 2: Zipcar partners with both local and national suppliers and is able to achieve cost savings from volume

purchases and logistical efficiency.

Supplier Cost

Car Manufacturers ZIP partners with major car manufacturers to yield savings on fleet (average cost of $20k per car).

Parking ZIP pays for parking spots from local parking facilities and major parking companies such as Interpark, Inc.

(monthly parking per car averages around $600). Some municipalities and universities offer Zipcar free parking in

an effort to promote sustainable behavior.

Labor Zipcar’s 593 employees are compensated based on their departmental functions (wages averages around $26k to

$60k).

Gas ZIP absorbs the majority of fluctuations in gas prices, occasionally passing on increases to customers via higher

fees. ZIP partners with Wright Express, a business payment processor, to supply its vehicles with gas cards (for a

monthly fee of $2 per card).

Insurance Liberty Mutual provides car insurance to ZIP (for a cost of about $150 per car per month).

Third Party Service

Providers

ZIP uses third party service providers for services such as maintenance ($33 per car per month) and data centers.

Exhibit 3: A correlation matrix run on number of cars Zipcar has in its top ten cities and nationally agai nst population

characteristics suggests that Zipcar targets dense urban populations.

Cities Characteristics vs. Number of Zipcar Cars Top 10 Cities All US Cities Cars 1.00 1.00

Population 0.65 0.67

Number of Universities 0.37 0.56

Number of College Students 0.47 0.46

Median HH Income 0.54 0.10

Population Density (per sq mile) 0.90 0.11

20 to 24 years 0.64 0.49

25 to 29 years 0.65 0.53

30 to 34 years 0.65 0.51

35 to 39 years 0.65 0.47

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Public Transit Car Sharing Conventional

Rental

Taxi Private

Ownership

Convenience of Different Transportation Modes(1 = Least Convenient 3= Most Convenient)

CFA Institute Research Challenge December 12, 2011

11

Exhibit 4: Zipcar city statistics show that Zipcar targets cities with median incomes between $34,400 and $71,745 and

high population density.

Top 10 US Cities Min Max Median All US Cities Min Max Median

Population 66,194 8,175,133 619,278 Population 1,357 8,175,133 71,943

Population Density

(people/sq mile) 3,153 27,016 10,590

Population Density

(people/sq mile) 62 228,330 3,263

Number of Universities 12 45 18 Number of Universities 0 45 3

Median Income ($USD) 34,400 71,745 47,134 Median Income ($USD) 13,385 200,001 39,427

People between 20 and 39 160,206 2,622,437 245,390 People between 20 and 39 420 2,944,154 33,485

Exhibit 5: Zipcar is led by experienced executives whose compensation is directly tied to firm performance. The CFO, Ed

Goldfinger, has experience with data analytics, which he can apply to the decade of data Zipcar has collected. The COO,

Mark Norman, has experience with highly rapid growth in his prior car sharing company, which he may apply to Zipcar in

managing its expansion. Source: Zipcar Form 424-B4

Name and Title Background Leadership Examples Individual Compensation Objectives in 2010 (20% of

total bonus)

Scott Griffith

Chairman & CEO Boeing

Information

America

The Parthenon

Group

In 2009, anticipated growth of 15-25% over the next five years and so far ZIP has achieved

41.9% and 36.0% YOY growth in revenues

and 54.7% and 20.4% membership growth in

2010 and 2011.

Source: FastCompany.com

General oversight of the senior management team

IPO readiness and execution

Increasing brand awareness

Received a $360,000 bonus

Mark Norman

President & COO Flexcar

DaimlerChrysler

Ford

Mr. Norman was previously the CEO of

Flexcar, which was acquired by Zipcar in 2007.

Flexcar, a problematic company that expanded

too quickly before operations were finalized (20 cities in five years) and had technology

implementation setbacks.

Source: Zipcar Form 424-B4 and David Brook’s “Car Sharing in North America”

Establishing and maintaining initiatives regarding operational excellence

Improving the field operations structure

Management of our ongoing efforts to improve

the customer experience

Received a $159,670 bonus

Ed Goldfinger

CFO KPMG

PepsiCo

Spotfire

Empirix

Sapient

Mr. Goldfinger was the CEO of Empirix, a

company that provided corporations “with

products and solutions in the areas of

functional and regression testing, load

testing, monitoring and management.” This makes him a good fit for analyzing data

collected by Zipcar and implementing

appropriate actions. Source: Frost and Sullivan, Movers and

Shakers Interview, September 2005.

IPO readiness

Obtaining and maintaining debt facilities

Establishing a public- company level finance team

Received a bonus of $119,753

CFA Institute Research Challenge December 12, 2011

12

Exhibit 6: Management has been consistent with reaching performance targets that drive the top line and have been

focusing on improving profitability. 2010 Target vs. Attained: Revenue $187.9mm vs. $187.5mm, EBITDA $15.5mm vs.

$16.1mm, Operating Income $5.2mm vs. $4.9mm.

Exhibit 7: Profitability has seen a significant improvement historically and should continue to improve as management

focuses on these performance metrics, which are tied to their compensation.

88%

90%

92%

94%

96%

98%

100%

102%

104%

106%

Revenue EBITDA Operating Income

2010 Performance Targets vs. Attained

(Target = 100%)

Target Attained

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

2005 2006 2007 2008 2009 2010 2011E

Profitability Margins

(2005-2011E)

Operating Income Margin EBITDA margin Net Income Margin

CFA Institute Research Challenge December 12, 2011

13

Exhibit 8: Car sharing companies launches have increased significantly over the last decade (ZIP was founded in 2000).

Exhibit 9: Porter's Five Forces Analysis suggests that the car sharing industry is currently a profitable industry for

incumbents, but these forces may change for the worse as industry rivalry increases with the entrance of more players.

Buyer power will also increase as customers will have more car sharing companies to choose from. Additionally, the high

threat of substitution demands that car sharing companies keep pricing from getting too high. Nonetheless, being an early

mover is an important advantage because while entry costs are low, brand and reach are important factors to customers.

0

0.5

1

1.5

2

2.5

3

3.5

1985 1990 1995 2000 2005 2010 2015

Number of Car Companies Launched Per Year

(1990-2011)

Abroad US

CFA Institute Research Challenge December 12, 2011

14

Exhibit 10: The average delay per traveler in the US per year has increase drastically, especially in cities with larger

population sizes. As city governments attempt to address this problem, car sharing seems like a viable option. Source: US

Department of Transportation

Exhibit 11: Food and gas prices have increased 198.5% and 31.7% respectively since 1990, increasing the cost of living

and making car sharing an attractive cost saving proposition

Exhibit 12: Yelp ratings from top Zipcar cities show a generally favorable perception about company, but about 30% of

customers are dissatisfied with its services, suggesting that management must lower this number in order to retain

members who may now go to one of the many other car sharing companies.

City 5 Stars 4 Stars 3 Stars 2 Stars 1 Star Total Ratings

Boston 41 24 11 6 23 105

39.0% 22.9% 10.5% 5.7% 21.9% 100.0%

NY 21 18 16 11 15 81

25.9% 22.2% 19.8% 13.6% 18.5% 100.0%

San Francisco 123 68 43 22 78 334

36.8% 20.4% 12.9% 6.6% 23.4% 100.0%

Chicago 41 30 10 17 15 113

36.3% 26.5% 8.8% 15.0% 13.3% 100.0%

Total 226 140 80 56 131 633

35.7% 22.1% 12.6% 8.8% 20.7% 100.0%

0

10

20

30

40

50

60

70

Small Medium Large Very Large

Ho

urs

Yearly Hours of Delay per Traveler by City Population Size

(1982-2002)

1982 1992 2002

0

0.5

1

1.5

2

2.5

3

3.5

0

50

100

150

200

250

1990 2000 2010

Ca

rs

to N

um

ber o

f P

eo

ple

an

d G

as

Pric

e (

$)

Fo

od

Pric

e I

nd

ices

Fuel and Food Prices

(1990-2010)

Food Price Indices Gas Prices

CFA Institute Research Challenge December 12, 2011

15

Exhibit 13: We conducted a survey with 141 respondents, which enabled us to determine key metrics and assumptions,

such as net promoter scores, user utilization rates, and preferences.

Key Statistics from Zipcar Survey Total Percentage

Total Completed Surveys 129 141 91.49%

Total Zipsters 45 129 34.88%

NPS (Net Promoter Score) 41 44 93.18%

Exhibit 14: Europe is the best market for Zipcar to enter in the near future, as it is full of countries and cities with

favorable characteristics adjacent to each other. In comparis on, Asia only has three cities with these important

characteristics, and they are not geographically close, which would make achieving economies of scale more difficult. Top

locations were chosen based on income (ideal range in current cities is between $3 4,000 and $70,000, based on data in

Exhibit 4) and large presence of cars. Source: World Data Bank and NYC.gov.

4-5

times/week

0%

Less than 1

time/month

58%

5+

times/week

3%

Once a week

2%

No longer

use

21%

2-3

times/week

0%

1-3

times/month

16%

Frequency of Use

1-2 hours

18%

2-4 hours

64%

4-6 hours

2%

6-8 hours

7%

Whole day

9%Average Usage

Toyota

Hybrid

36.4%

BMW

Sedan

36.4%

Nissan

Sedan

18.2%

Mini

Cooper

9.1%

Most Popular Cars

0

100

200

300

400

500

600

700

800

900

$-

$10

$20

$30

$40

$50

$60

$70

Cars

/Th

ou

san

d o

f P

eop

le

GD

P/C

ap

. (U

SD

Th

ou

san

ds)

Potential Countries for Zipcar

(2008)

GDP per capita (current US$) Motor vehicles (per 1,000 people)

0

100

200

300

400

500

600

700

$0

$10

$20

$30

$40

$50

$60

$70

$80

Cars

/Th

ou

san

d o

f P

eop

le

GD

P/C

ap

. (U

SD

Th

ou

san

ds)

Potential Cities for Zipcar

(2008)

GDP per capita (current US$) Motor vehicles (per 1,000 people)

CFA Institute Research Challenge December 12, 2011

16

Exhibit 15: We used the EV/Revenue multiple because of the high correlation between sales growth and this multipl e.

Exhibit 16: Upon analyzing trading multiples of companies that are comparable to Zipcar in different areas, we computed

a median EV/Revenue multiple of 2.1x. This median is a conservative estimate since companies demonstra ting our 21%

revenue growth forecast trade at levels over 3.0x, selecting a target multiple appropriate for Zipcar’s revenue growth (see

Exhibit 15). Numbers below are as of 12/09/11.

Company Price Market

Cap

Total

EV

LTM

Revenue

EBITDA

Margin

1Yr Sales

Growth

EV/

Revenue

Zipcar, Inc. (NasdaqGS: ZIP) $14.28 561 549 231 10.8% 36.0% 2.4x

Traditional Car Rental

AMERCO (NasdaqGS: UHAL) $83.24 1,632 2,577 2,365 25.2% 11.0% 1.1x

Avis Budget Group (NasdaqGS: CAR) $11.70 1,229 8,862 5,495 15.5% 7.3% 1.6x

Dollar Thrifty Automotive Group (NYSE:

DTG)

$69.58 2,020 2,849 1,544 21.5% 0.7% 1.8x

Hertz Global Holdings (NYSE: HTZ) $11.57 4,821 16,936 8,120 15.2% 8.7% 2.1x

Traditional Car Rental Median 1.7x

Hotels & Time share

HomeAway, Inc. (NasdaqGS: AWAY) $25.11 2,023 1,851 217 16.6% 39.6% 8.5x

Choice Hotels International (NYSE: CHH) $37.44 2,193 2,321 628 29.2% 7.9% 3.7x

Morgans Hotels Group (NasdaqGM:

MHGC)

$5.99 184 666 220 9.3% -5.9% 3.0x

Starwood Hotels & Resorts (NYSE: HOT) $48.37 9,295 11,492 5,433 16.0% 9.2% 2.1x

Hotels Median 3.4x

Market Disrupters

LinkedIn (NYSE: LNKD) $71.89 7,013 6,626 436 12.2% 117.3% 15.2x

Netflix (NasdaqGS: NFLX) $70.89 3,925 3,793 2,925 14.8% 45.4% 1.3x

OpenTable (NasdaqGS: OPEN) $35.73 849 769 133 28.1% 52.3% 5.8x

Market Disrupters Median 5.8x

Trading Multiples Median 2.1x

ZIP

UHALDTGHTZ

AWAY

CHHMHGC

LNKD

NFLX

OPEN

R² = 0.7154

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

-20% 0% 20% 40% 60% 80% 100% 120% 140%

EV

/Rev

en

ue m

ult

iple

Sales growth

EV/Revenue and Sales growth relationship

CFA Institute Research Challenge December 12, 2011

17

Exhibit 17: We analyzed 22 precedent transactions to market premiums paid for companies which we believe are similar

to Zipcar in different ways. This resulted in a median multiple of 30x.

Announced

Date

Close Date Target Buyer Seller Size

(USD

mm)

Implied

EV

Implied

Equity

Value

Total

Consider

ation

Implied

EV/Rev.

Hotels

29-Mar-11 15-Apr-11 One Park Boulevard Sunstone Hotel

Partnership

Hilton Worldwide 422 475 231 174 4.7x

16-May-11 1-Jun-11 Radisson Lexington

Hotel

Diamondrock

Hospitality Co.

Several financial

holdings

435 430 335 335 8.5x

4-Apr-11 23-May-11 Royalton & Morgans

Hotels

FelCor Lodging

Trust Inc.

Morgans Hotel

Group

140 140 140 140 NA

4-May-11 10-May-11 W Chicago City

Center

Chesapeake Lodging

Trust

Starwood Hotels &

Resorts

129 129 128 128 4.2x

28-Mar-11 6-Apr-11 The Westin Gaslamp

Quarter

Pebblebrook Hotel

Trust

Starwood CMBS I,

LLC

110 110 110 110 4.0x

10-May-11 27-May-11 Westin Pasadena

Hotel

HEI Hospitality MPG Office Trust 92 92 92 92 4.5x

28-Feb-11 30-Jun-11 NJA Hotel, LLC Chesapeake Lodging

Trust

Sagamore Capital,

LLC

67 67 29 29 5.3x

Median 4.6X

Car rental and

Leasing

3-Dec-11 31-Dec-10 JJ Motorcars, Inc Tourism Holdings

Ltd.

D. Schneider & H.

Hagner

16 16 9 9 0.8x

16-Dec-10 28-Jan-11 Scully

Transportation

Ryder System, Inc. NA 86 86 71 71 0.5x

17-Jul-11 1-Sep-11 Donlen Corporation The Hertz

Corporation

G. Rappeport, N.

Liace, etc.

947 947 NA NA 2.7x

14-Jun-11 3-Oct-11 Avis Europe plc Avis Budget Car

Rental

D Ieteren Car Rental,

etc.

1,325 1,209 636 636 0.9x

Median 0.8x

Auto

Manufacturers

3-May-11 6-Jun-11 Wheeler Bros., Inc VSE Corp Wheeler Family and

others

220 182 162 162 1.2x

21-Jul-11 21-Jul-11 Chrysler Group LLC Fiat North America

LLC

additional 12.31% 625 7,305 5,077 625 0.2x

7-Mar-11 1-Apr-11 Classic Fire LLC Spartan Motors Inc NA 5 5 5 5 0.5x

Median 0.5x

IT Market

Disrupters

10-May-11 13-Oct-11 Skype Global Microsoft

Corporation

Group of investors 9,225 9,082 8,500 8,500 10.6x

27-Apr-11 15-Jul-11 SAVVIS, Inc CenturyLink, Inc Investment fund 3,084 2,963 2,301 2,301 3.0x

24-Mar-11 12-Apr-11 Mortgagebot, LLC Davis + Handerson

Corp

Spectrum Equity

Investors

232 232 232 232 6.1x

1-Feb-11 21-Apr-11 NaviSite, Inc Time Warner Cable

Inc

Group of investors 332 327 208 208 2.5x

5-Jul-11 7-Nov-11 Travelex Global

Business

Western Union Co. Travelex Group

Limited

606 606 606 606 4.3x

28-Mar-11 17-Jun-11 GSI Commerce, Inc eBay Inc. NA 2,381 2,139 2,215 2,215 1.6x

20-Jul-11 10-Nov-11 Insider Guides, Inc Quepasa Corp Group of investors 100 100 NA NA 3.7x

Median 3.7x

Zipcar

20-Apr-10 20-Apr-10 Streetcar Limited Zipcar, Inc. Group of investors 50 50 50 50 2.2x

3.7x

CFA Institute Research Challenge December 12, 2011

18

Exhibit 18: We determined membership growth by analyzing the markets that Zipcar is in and the ones that it plans to enter. For European

cities, we assume that the Company will enter two cities per year, based on previously established metrics (such as income), starting with

the cities with the highest population. We also used historical penetrations rates at a declining rate for established markets and constant

penetration rates for the remaining markets. Total membership is forecasted to grow at a CAGR of 17.0%.

United States

Established markets

Greater Boston Area 4,552,402 0.4% NM NM NM NM NM NM NM

New York City 18,897,109 0.3% NM NM NM NM NM NM NM

San Francisco Bay Area 4,335,391 0.5% NM NM NM NM NM NM NM

Washington Metro Area 5,582,170 1.5% NM NM NM NM NM NM NM

Established Total 33,367,072 0.5% +0.25% 389,134 474,892 550,946 617,187 673,507 719,795

Other ~120 Zipcar Cities 113,078,131 0.5% +0.02% 130,110 152,302 174,605 197,019 219,546 242,185

Total US members 519,244 627,194 725,551 814,207 893,053 961,980

Annual Decrease in Penetration Rate 0.03%

2011E US members 519,244

5yr Organic Growth CAGR (US) 13.1%

*Market penetration rates as well as membership by segments are proprietory estimates of Boston University team.

Canada

Toronto 5,741,419 1.8% NM NM NM NM NM NM NM

Vancouver 2,391,252 2.3% NM NM NM NM NM NM NM

Total Canada members 8,132,671 2.0% +0.15% 40,444 53,026 65,859 78,946 92,293 105,905

2011E US members 40,444

5yr Organic Growth CAGR (US) 21.2%

*Market penetration rates as well as membership by segments are proprietory estimates of Boston University team.

United Kingdom

Brighton 155,919 1.7% NM NM NM NM NM NM NM

Bristol 441,300 0.5% NM NM NM NM NM NM NM

Cambridge 125,700 1.1% NM NM NM NM NM NM NM

Edinburgh 486,120 1.4% NM NM NM NM NM NM NM

Greater London 7,825,200 1.0% NM NM NM NM NM NM NM

Maidstone 91,042 0.2% NM NM NM NM NM NM NM

Oxford 165,000 2.3% NM NM NM NM NM NM NM

Total UK members 9,290,281 1.0% +0.12% 115,393 126,623 137,967 149,424 160,997 172,686

2011E US members 115,393

5yr Organic Growth CAGR (US) 8.4%

*Market penetration rates as well as membership by segments are proprietory estimates of Boston University team.

Europe - New markets 2 cities per year

Year 5 penetration target 1.0%

Annual population growth 0.5%

Density

City Country (per sq. mile)

Paris France 54,300 10,354,675 56,000$ 20,917 42,043 63,380 84,929 106,692

Berlin Germany 10,082 3,471,756 32,000$ 7,013 14,096 21,250 28,475 35,772

Madrid Spain 13,994 3,273,049 40,000$ NA 6,645 13,356 20,134 26,980

Barcelona Spain 41,417 3,218,071 49,000$ NA 6,533 13,132 19,796 26,527

Rome Italy 5,565 2,761,477 34,000$ NA NA 5,634 11,325 17,072

Vienna Austria 10,707 1,714,142 41,000$ NA NA 3,497 7,030 10,597

Munich Germany 11,290 1,353,186 44,000$ NA NA NA 2,775 5,577

Milan Italy 19,010 1,334,077 47,000$ NA NA NA 2,736 5,498

Brussels Belgium 16,857 1,089,538 43,000$ NA NA NA NA 2,245

Basel Switzerland 19,301 169,536 42,000$ NA NA NA NA 349

Total Europe members 27,930 69,317 120,250 177,199 237,311

2010A 2011E 2012P 2013P 2014P 2015P 2016P

Total Zipsters 540,484 675,081 834,774 998,693 1,162,826 1,323,542 1,477,882

YoY Growth 25% 24% 20% 16% 14% 12%

5yr CAGR 17.0%

2010 Population

1YR

penetration

2011P

members

10yr Pop

CAGR

2010 Population

1YR

penetration

2011P

members

3yr Pop

CAGR2010 Population

1YR

penetration

2011P

members

9yr Pop

CAGR

2012P

members

2016P

members

2013P

members

2014P

members

2015P

members

2010

Population

Median

Income

2015P

members

2012P

members

2013P

members

2014P

members

2015P

members

2014P

members

2012P

members

2013P

members

2016P

members

2016P

members

2015P

members

2016P

members

2012P

members

2013P

members

2014P

members

CFA Institute Research Challenge December 12, 2011

19

Exhibit 19: We calculated the beta for Zipcar by using an average of three different betas versus the S&P500. We used a

levered beta based on comparable companies, a BARRA Beta, and a regression beta based on Zipcar’s historical prices

starting from its IPO date in April. Source: BARRA and CapitalIQ.

Levered Beta 1.19

BARRA Beta 1.35

Regression Beta 0.97

Average 1.17

Exhibit 20: Our sensitivity analysis shows that Zipcar's forecasted share price is most sen sitive to changes in expenses,

reflecting the fact that the Company has such high operating leverage.

Exhibit 21: The Company can easily access more credit to support expansion and operations plans through its large

revolving credit line.

Outstanding Principle Amount as of

Description Type Effective

From

FYE2009 FYE2010 Mar-

31-

2011

Jun-

30-

2011

Sep-

30-

2011

Coupon/Base

rate

Adjusted

Rates

Floating

Rate

Maturity

ABS Note A Revolving

Credit

May-10 - 18,867 16,275 43,000 50,000 2% + 30-day

Commercial

Paper

3.50% Yes --

ABS Note B Revolving

Credit

May-10 - 10,000 10,000 - - 9.00% 9.00% No --

Capital Leases Capital

Lease

NA 3,249 27,604 23,421 26,342 25,343 3.80 - 13.50% 10.00% Yes 2015

Loan and

Security

Agreement

Term Loans May-08 8,216 4,984 10,000 - - 11.20% 11.20% No Jun-12

Loan and

Security

Agreement

Term Loans Jun-09 4,000 8,534 10,000 - - 16.80% 16.80% No Jul-13

Loan and

Security

Agreement

Term Loans Mar-10 - 20,000 20,000 - - 15.80% 15.80% No 2013

Notes Payable Bonds and Notes

Apr-10 - 5,000 5,000 - - 12.20% 12.20% No 2013

Total Principal

Amount

15,465 94,989 94,696 69,342 75,343

Interest rate on ABS facility is 2% plus 30-day Commercial Paper conduit interest rate. The lender charges additional 1% on

undrawn amount of the $50.0 million credit line. Zipcar annually buys a 3.5% interest rate cap.

Interest rates under Capital Lease Obligations are floating, and estimated to be in the range of 3.8 to 13.5%. We analyzed

Zipcar’s historical debt structure, and concluded that the average of interest rates should be close to 10.0%.

$18.19

$19.08

$18.40

$17.85

$10.78

$8.21

$21.19

$19.89

$20.50

$21.03

$26.43

$34.65

$6.00 $11.00 $16.00 $21.00 $26.00 $31.00

WACC (+/-100 bps)

Perpetuity Growth (+/-50 bps)

EV/Revenue (+/-0.25x)

Revenue (+/-150 bps)

Expenses (+/- 75 bps)

Best/Worst Case (Assumes all

of above)

ZIP Price per Share

Sensitivity Analysis on Weighted Valuation

Current Price Forecasted Price

CFA Institute Research Challenge December 12, 2011

20

Exhibit 22: In order to analyze ZIP’s ability to repay debt, we used the traditional car rental industry as the closest industry comparable to

assess Zip’s DEBT/EBITDA, which is calculated at 3.0x. Since the industry’s leverage coverage ratio is 7.1x, we believe Zipcar is more

than capable of paying off its current debt relative to the industry and achieve a cheaper cost of debt in the future from better credit

ratings.

Exhibit 23: The biggest risk to our target price is the failure to increase capacity utilization, which could lead to a target

price of $12.48.

$12.48

$13.70

$15.95

$16.55

$14.15

$19.45

$19.45

$19.45

$19.45

$19.45

$12.00 $14.00 $16.00 $18.00 $20.00

Failure to Increase Capacity

Utilization (35%)

Increased Competition (30%)

Failure to Penetrate New Markets

(EU) (20%)

Input Costs (15%)

Reference Range

ZIP Price per Share

Current Price Forecasted Price

Investment Risks for Weighted Valuation

Leverage Coverage Ratios Latest LTM DEBT/

Company Name Debt EBTIDA EBTIDA

Zipcar, Inc. (NasdaqGS:ZIP) 75.3 25.0 3.0

Traditional Car Rental Industry

AMERCO (NasdaqGS:UHAL) 1,545.4 595.5 2.6x

Avis Budget Group, Inc.

(NasdaqGS:CAR)

8,635.0 852.0 10.1x

Dollar Thrifty Automotive Group

Inc. (NYSE:DTG)

1,329.4 331.7 4.0x

Hertz Global Holdings, Inc.

(NYSE:HTZ)

12,507.2 1,233.4 10.1x

Median 7.1x

CFA Institute Research Challenge December 12, 2011

21

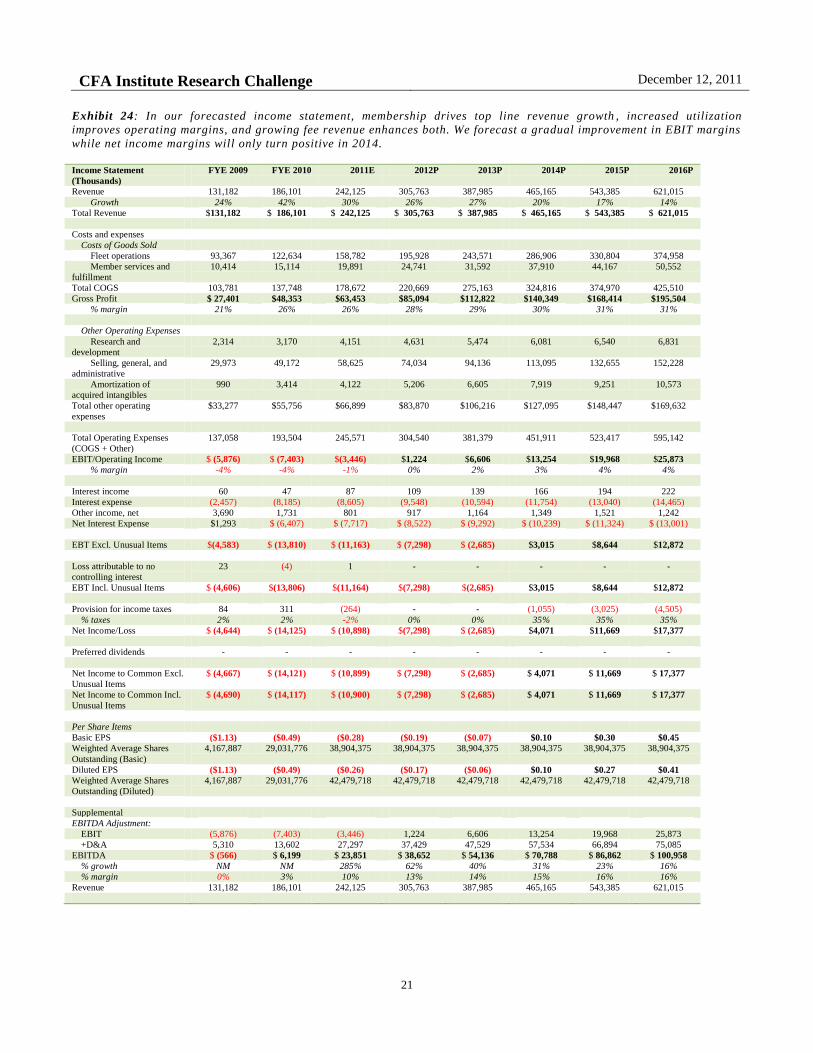

Exhibit 24: In our forecasted income statement, membership drives top line revenue growth , increased utilization

improves operating margins, and growing fee revenue enhances both. We forecast a gradual improvement in EBIT margins

while net income margins will only turn positive in 2014.

Income Statement

(Thousands)

FYE 2009 FYE 2010 2011E 2012P 2013P 2014P 2015P 2016P

Revenue 131,182 186,101 242,125 305,763 387,985 465,165 543,385 621,015

Growth 24% 42% 30% 26% 27% 20% 17% 14%

Total Revenue $131,182 $ 186,101 $ 242,125 $ 305,763 $ 387,985 $ 465,165 $ 543,385 $ 621,015

Costs and expenses

Costs of Goods Sold

Fleet operations 93,367 122,634 158,782 195,928 243,571 286,906 330,804 374,958

Member services and

fulfillment

10,414 15,114 19,891 24,741 31,592 37,910 44,167 50,552

Total COGS 103,781 137,748 178,672 220,669 275,163 324,816 374,970 425,510

Gross Profit $ 27,401 $48,353 $63,453 $85,094 $112,822 $140,349 $168,414 $195,504

% margin 21% 26% 26% 28% 29% 30% 31% 31%

Other Operating Expenses

Research and

development

2,314 3,170 4,151 4,631 5,474 6,081 6,540 6,831

Selling, general, and

administrative

29,973 49,172 58,625 74,034 94,136 113,095 132,655 152,228

Amortization of

acquired intangibles

990 3,414 4,122 5,206 6,605 7,919 9,251 10,573

Total other operating

expenses

$33,277 $55,756 $66,899 $83,870 $106,216 $127,095 $148,447 $169,632

Total Operating Expenses

(COGS + Other)

137,058 193,504 245,571 304,540 381,379 451,911 523,417 595,142

EBIT/Operating Income $ (5,876) $ (7,403) $(3,446) $1,224 $6,606 $13,254 $19,968 $25,873

% margin -4% -4% -1% 0% 2% 3% 4% 4%

Interest income 60 47 87 109 139 166 194 222

Interest expense (2,457) (8,185) (8,605) (9,548) (10,594) (11,754) (13,040) (14,465)

Other income, net 3,690 1,731 801 917 1,164 1,349 1,521 1,242

Net Interest Expense $1,293 $ (6,407) $ (7,717) $ (8,522) $ (9,292) $ (10,239) $ (11,324) $ (13,001)

EBT Excl. Unusual Items $(4,583) $ (13,810) $ (11,163) $ (7,298) $ (2,685) $3,015 $8,644 $12,872

Loss attributable to no

controlling interest

23 (4) 1 - - - - -

EBT Incl. Unusual Items $ (4,606) $(13,806) $(11,164) $(7,298) $(2,685) $3,015 $8,644 $12,872

Provision for income taxes 84 311 (264) - - (1,055) (3,025) (4,505)

% taxes 2% 2% -2% 0% 0% 35% 35% 35%

Net Income/Loss $ (4,644) $ (14,125) $ (10,898) $(7,298) $ (2,685) $4,071 $11,669 $17,377

Preferred dividends - - - - - - - -

Net Income to Common Excl.

Unusual Items

$ (4,667) $ (14,121) $ (10,899) $ (7,298) $ (2,685) $ 4,071 $ 11,669 $ 17,377

Net Income to Common Incl.

Unusual Items

$ (4,690) $ (14,117) $ (10,900) $ (7,298) $ (2,685) $ 4,071 $ 11,669 $ 17,377

Per Share Items

Basic EPS ($1.13) ($0.49) ($0.28) ($0.19) ($0.07) $0.10 $0.30 $0.45

Weighted Average Shares

Outstanding (Basic)

4,167,887 29,031,776 38,904,375 38,904,375 38,904,375 38,904,375 38,904,375 38,904,375

Diluted EPS ($1.13) ($0.49) ($0.26) ($0.17) ($0.06) $0.10 $0.27 $0.41

Weighted Average Shares

Outstanding (Diluted)

4,167,887 29,031,776 42,479,718 42,479,718 42,479,718 42,479,718 42,479,718 42,479,718

Supplemental

EBITDA Adjustment:

EBIT (5,876) (7,403) (3,446) 1,224 6,606 13,254 19,968 25,873

+D&A 5,310 13,602 27,297 37,429 47,529 57,534 66,894 75,085

EBITDA $ (566) $ 6,199 $ 23,851 $ 38,652 $ 54,136 $ 70,788 $ 86,862 $ 100,958

% growth NM NM 285% 62% 40% 31% 23% 16%

% margin 0% 3% 10% 13% 14% 15% 16% 16%

Revenue 131,182 186,101 242,125 305,763 387,985 465,165 543,385 621,015

CFA Institute Research Challenge December 12, 2011

22

Exhibit 25: Zipcar is well positioned to build strong asset base while maintain ing healthy levels of capitalization.

Balance Sheet

(Thousands) FYE 2009 FYE 2010 2011E 2012P 2013P 2014P 2015P 2016P

ASSETS

Current Assets

Cash and cash equivalents 19,228 43,005 48,497 35,368 30,730 40,698 68,515 114,400

ST marketable securities - - 32,152 32,152 32,152 32,152 32,152 32,152

Accounts receivable, net 2,816 4,223 5,640 6,727 8,536 10,234 11,954 13,662

Restricted cash 48 900 1,800 1,103 1,376 1,624 1,875 2,128

Inventory - - - - - - - -

Prepaid expenses and other

current assets

5,037 9,905 11,104 12,610 16,510 19,489 22,498 25,531

Total current assets 27,129 58,033 99,193 87,960 89,303 104,196 136,995 187,873

Non-Current Assets

PPE 18,604 77,288 147,630 202,424 264,193 328,946 393,720 455,328

Depreciation 9,178 6,371 33,668 71,097 118,626 176,160 243,054 318,139

Property and equipment, net 9,426 70,917 113,962 131,327 145,567 152,787 150,666 137,189

Goodwill 41,871 99,750 102,826 108,627 109,153 108,425 104,808 97,785

Intangible assets 1,385 8,527 5,668 5,951 6,249 6,561 6,889 7,234

Restricted cash 5,750 3,503 4,115 3,001 2,608 3,453 5,814 9,707

Deposits and other non-

current assets

4,346 8,198 4,743 3,459 3,005 3,980 6,701 11,188

LT marketable securities - - 5,042 - - - - -

TOTAL ASSETS 89,907 248,928 335,548 340,325 355,885 379,404 411,873 450,976

LIABILITIES

Current Liabilities

Accounts payable 3,953 6,247 8,266 10,209 12,731 15,028 17,348 19,687

Accrued expenses and other

liabilities

8,207 16,594 18,807 22,729 26,691 31,507 36,372 41,274

Deferred revenue 9,763 14,261 12,983 11,832 14,755 17,417 20,106 22,816

Current portion of capital

lease obligations and other

debt

6,984 26,041 15,796 21,125 20,578 23,074 26,133 28,018

Total current liabilities 28,907 63,143 55,853 65,896 74,754 87,026 99,959 111,795

Non-current liabilities

Capital lease obligations and

other debt, net of current

portion

8,228 68,022 59,547 61,752 70,587 77,208 84,177 93,323

Deferred revenue, net of

current portion

3,145 3,651 2,516 2,341 2,822 3,201 3,840 4,305

Redeemable convertible

preferred stock warrants

400 478 - - - - - -

Other liabilities 764 1,975 2,456 2,578 2,649 2,825 3,084 3,364

Total Liabilities 41,444 137,269 120,370 132,567 150,812 170,260 191,060 212,787

SHAREHOLDER'S

EQUITY

Redeemable non-controlling

interest

111 277 492 492 492 492 492 492

Redeemable convertible

preferred stock

95,715 116,683 - - - - - -

Total Stockholder's Equity 95,826 116,960 492 492 492 492 492 492

SHAREHOLDER'S

DEFICIT

Common stock 4 6 39 39 39 39 39 39

APIC 4,017 59,647 290,519 290,519 290,519 290,519 290,519 290,519

Accumulated deficit/income (51,093) (65,380) (76,493) (83,792) (86,477) (82,406) (70,737) (53,360)

Accumulated other

comprehensive loss

(291) 426 621 500 500 500 500 500

Total Stockholder's Deficit (47,363) (5,301) 214,686 207,266 204,581 208,652 220,321 237,698

Total Stockholder's

Equity/Deficit

48,463 111,659 215,178 207,758 205,073 209,144 220,813 238,190

Accrued expenses

TOTAL LIABILITIES AND

STOCKHOLDER'S

DEFICIT

$89,907 $248,928 $335,548 $340,325 $355,885 $379,404 $411,873 $450,976

TOTAL ASSETS $89,907 $248,928 $335,548 $340,325 $355,885 $379,404 $411,873 $450,976

ASSETS

CFA Institute Research Challenge December 12, 2011

23

Exhibit 26: Zipcar’s margin expansions will help fuel out growth projections.

Statement of Cash Flows

(USD in thousands) FYE 2009 FYE 2010 2011E 2012P 2013P 2014P 2015P 2016P

Operating Activities

Net Income/Loss ($4,690) ($14,117) ($10,900) ($7,298) ($2,685) $4,071 $11,669 $17,377

D&A 5,310 13,602 27,297 37,429 47,529 57,534 66,894 75,085

Stock-based compensation expense 1,692 2,774 3,627 2,500 2,500 2,500 2,500 2,500

Other operating cash flows 586 1,400 4,610 1,500 1,500 1,500 1,500 1,500

Changes in Net Working Capital

Accounts receivable (633) (516) (1,382) (1,087) (1,809) (1,698) (1,721) (1,708)

Prepaid expenses and other assets (1,429) (3,776) (1,725) (1,507) (3,899) (2,979) (3,009) (3,032)

Accounts payable 785 891 2,015 1,943 2,521 2,297 2,320 2,338

Accrued expenses and other liabilities 1,864 8,000 3,757 3,922 3,962 4,816 4,865 4,902

Deferred revenue 2,906 4,956 (134) (1,150) 2,922 2,662 2,689 2,710

Net Cash flow from operating activities $6,391 $13,214 $27,165 $34,131 $48,844 $65,604 $82,563 $96,462

Investing activities

Proceeds from sale of PPE 2,009 8,424 12,299 15,531 19,708 23,628 27,601 31,545

Purchases of PPE (6,755) (42,376) (69,310) (70,326) (81,477) (88,381) (92,375) (93,152)

Other investing activities (3,973) (6,625) (41,259) - - - - -

Net Cash flow from investing activities ($8,719) ($40,577) ($98,270) ($54,794) ($61,769) ($64,753) ($64,774) ($61,608)

Financing activities

Proceeds from issuance of debt, net of principal payments 250 29,833 (36,099) 7,534 8,288 9,117 10,028 11,031

Proceeds from sale of Series G redeemable convertible pref stock - 20,935 - - - - - -

Other financing activities 83 298 113,291 - - - - -

Net Cash flow from financing activities $333 $51,066 $77,192 $7,534 $8,288 $9,117 $10,028 $11,031

Net increase/decrease in cash and cash equivalents (1,995) 23,703 6,087 (13,129) (4,637) 9,968 27,817 45,885

Cash and cash equivalents

Beginning of period 21,351 19,356 43,059 48,497 35,368 30,730 40,698 68,515

End of period 19,356 43,059 48,497 35,368 30,730 40,698 68,515 114,400

Exhibit 27: Zipcar is an aggressively expanding company in an industry that is still in the growth stage, thus it will

continue to see aggressive growth numbers in the near future before achieving a perpetual stable growth rate. We

assumed a two-stage growth model utilizing 30% free cash flow growth for the first five years after 2016 and 3%

perpetual growth thereafter to calculate the terminal value. It should be noted that the terminal value given by this two -

stage perpetuity model is in line with the exit multiple terminal value, despite d epressed current market conditions.

Intrinsic DCF Analysis

(USD in thousands) 2009A 2010A 2011E 2012P 2013P 2014P 2015P 2016P

EBIT (5,876) (7,403) (3,446) 1,224 6,606 13,254 19,968 25,873

- Taxes - - - 428 2,312 4,639 6,989 9,055

Tax Effected EBIT (5,876) (7,403) (3,446) 795 4,294 8,615 12,979 16,817

+ D&A 5,310 13,602 27,297 37,429 47,529 57,534 66,894 75,085