driving savings and compliance at newell rubbermaid · driving savings and compliance at newell...

TRANSCRIPT

Driving Savings and Compliance at

Newell Rubbermaid

October 27th, 2011

My Purchasing Center

Key Trends

© 2011 SAP AG. All rights reserved. 3

Demand for

Rapid

Productivity

Globalization Sustainability Economic Recovery

Focus on Efficiency

Growing

Supplier Risk

Importance of

Governance

Continued

Focus on Costs

Global Trends are Driving Change in Procurement

Practices

© 2011 SAP AG. All rights reserved. 4

Procurement Executives What does this mean for your business?

How do we continue to identify opportunities

to manage and reduce costs?

How do we maximize spend under

management, for all categories of spend?

How do we optimize contract terms and

enforce compliance?

How do we manage suppliers’ performance

and supply-based risk?

How do we improve our sourcing,

procurement and invoice management

processes?

How do we align our activities to best support

the corporate strategy?

© 2011 SAP AG. All rights reserved. 5

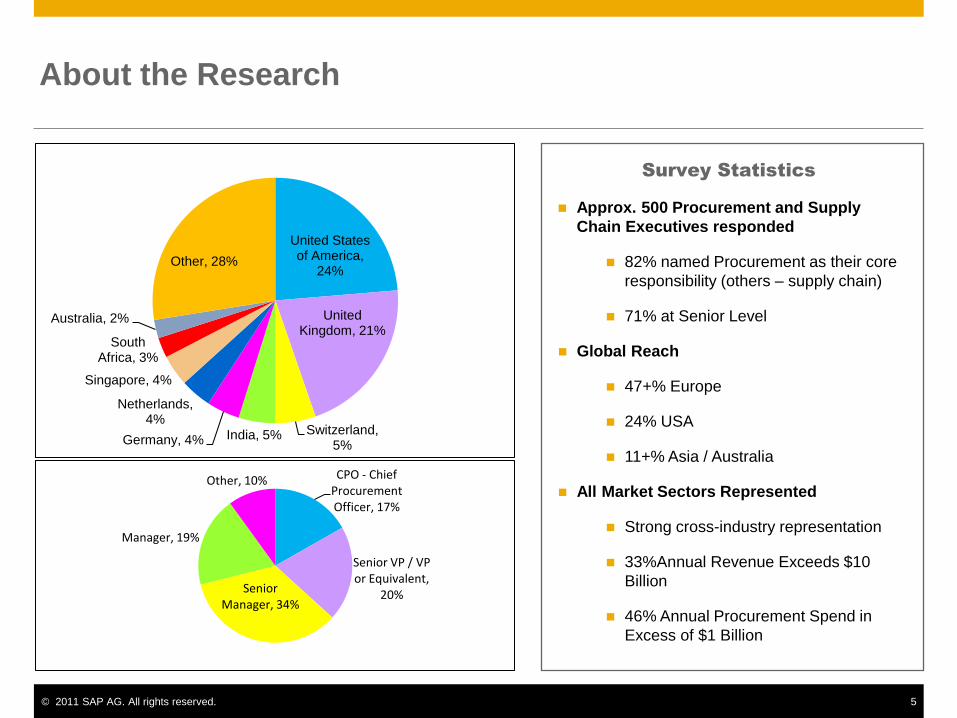

About the Research

Survey Statistics

Approx. 500 Procurement and Supply

Chain Executives responded

82% named Procurement as their core

responsibility (others – supply chain)

71% at Senior Level

Global Reach

47+% Europe

24% USA

11+% Asia / Australia

All Market Sectors Represented

Strong cross-industry representation

33%Annual Revenue Exceeds $10

Billion

46% Annual Procurement Spend in

Excess of $1 Billion

United States of America,

24%

United Kingdom, 21%

Switzerland, 5%

India, 5% Germany, 4%

Netherlands, 4%

Singapore, 4%

South Africa, 3%

Australia, 2%

Other, 28%

CPO - Chief Procurement Officer, 17%

Senior VP / VP or Equivalent,

20% Senior Manager, 34%

Manager, 19%

Other, 10%

© 2011 SAP AG. All rights reserved. 6

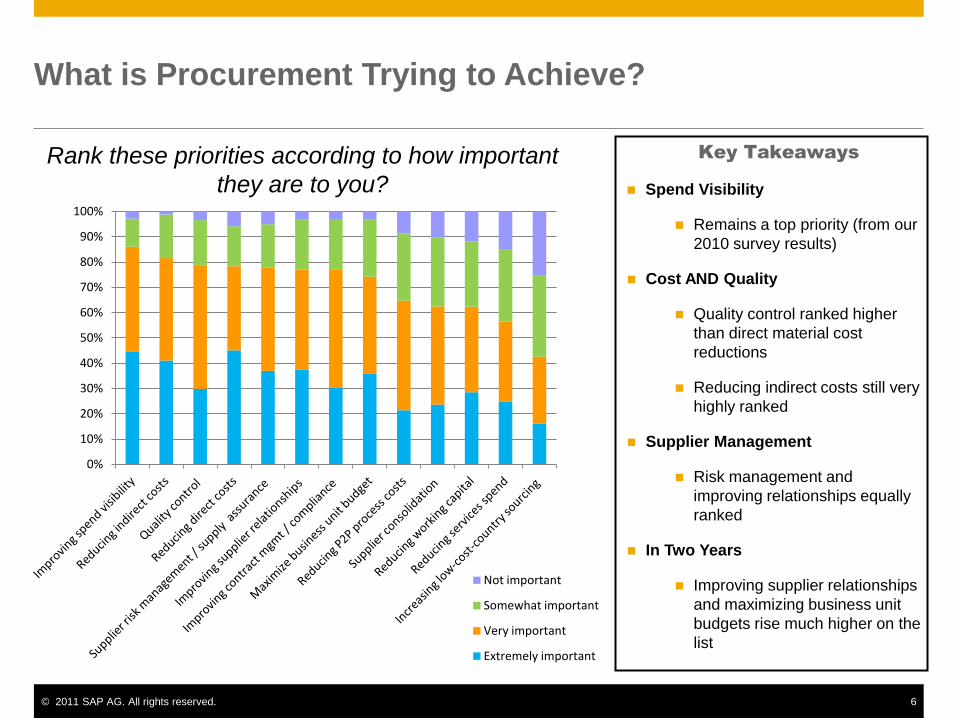

What is Procurement Trying to Achieve?

Rank these priorities according to how important

they are to you?

Key Takeaways

Spend Visibility

Remains a top priority (from our

2010 survey results)

Cost AND Quality

Quality control ranked higher

than direct material cost

reductions

Reducing indirect costs still very

highly ranked

Supplier Management

Risk management and

improving relationships equally

ranked

In Two Years

Improving supplier relationships

and maximizing business unit

budgets rise much higher on the

list

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Not important

Somewhat important

Very important

Extremely important

© 2011 SAP AG. All rights reserved. 7

Current Strategies on the CPO Agenda

In light of recent global events, what different

strategies are you adopting or do you plan to adopt?

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Key Takeaways

Internal Collaboration

68% stated they are now working

much more closely with the

business

63% said they are more involved

in strategic decisions

Supplier Risk Mgmt

66% have created new

approaches to supplier risk mgmt

63% are proactive about

commodity mgmt

45% formalized a supplier mgmt

program (in addition to those who

had this already)

New Investments

Over 40% invested in technology

and intelligence

© 2011 SAP AG. All rights reserved. 8

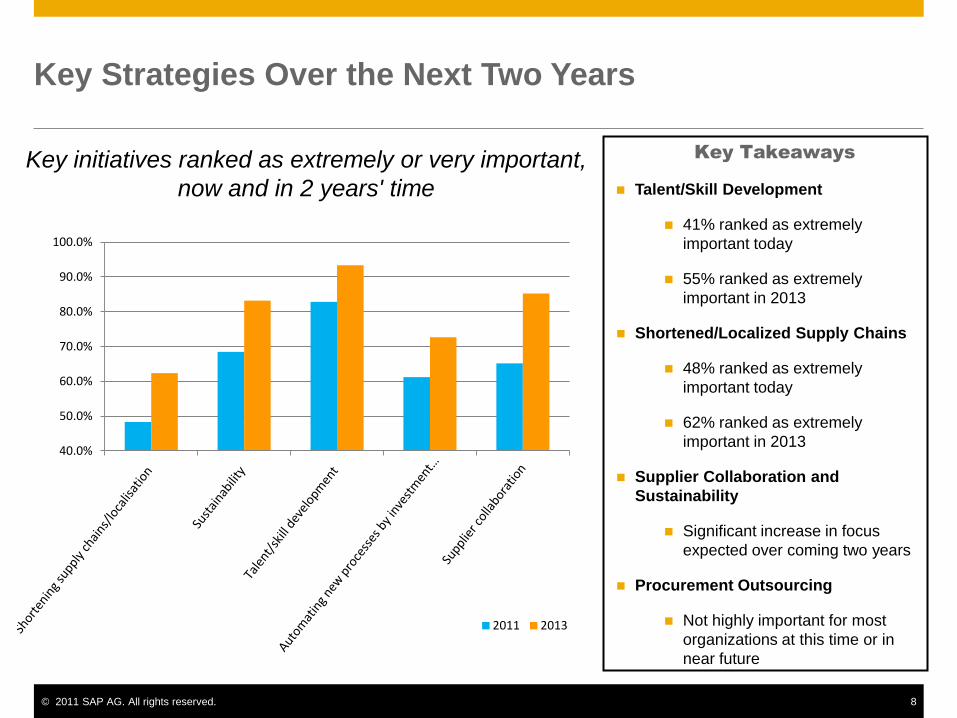

Key Strategies Over the Next Two Years

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2011 2013

Key Takeaways

Talent/Skill Development

41% ranked as extremely

important today

55% ranked as extremely

important in 2013

Shortened/Localized Supply Chains

48% ranked as extremely

important today

62% ranked as extremely

important in 2013

Supplier Collaboration and

Sustainability

Significant increase in focus

expected over coming two years

Procurement Outsourcing

Not highly important for most

organizations at this time or in

near future

Key initiatives ranked as extremely or very important,

now and in 2 years' time

© 2011 SAP AG. All rights reserved. 9

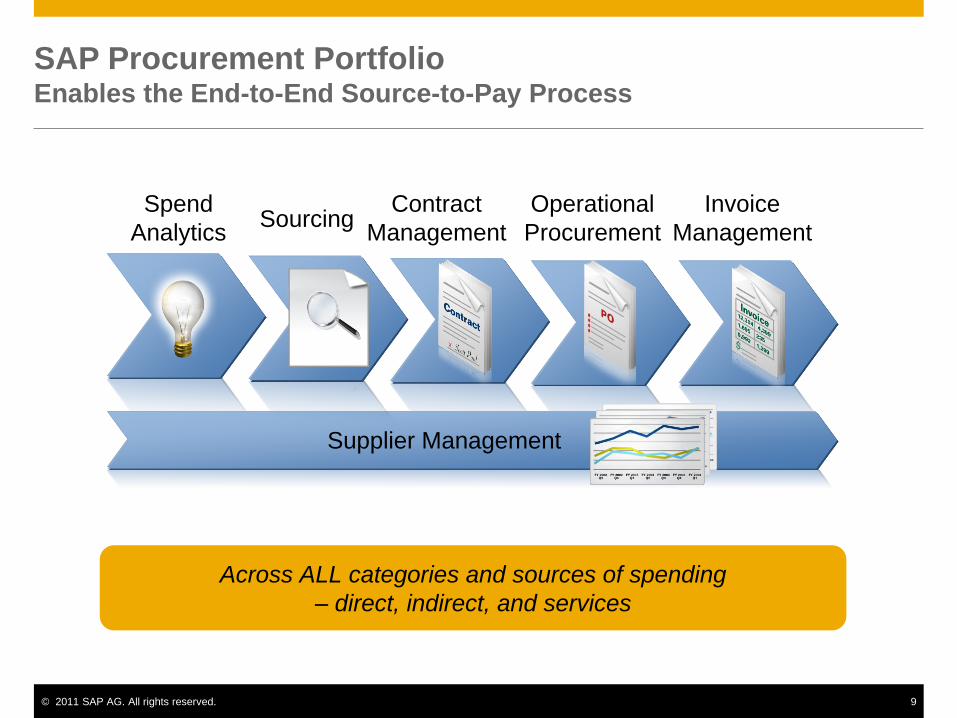

SAP Procurement Portfolio Enables the End-to-End Source-to-Pay Process

Spend

Analytics

Supplier Management

Sourcing Contract

Management

Operational

Procurement

Invoice

Management

Across ALL categories and sources of spending

– direct, indirect, and services

DRIVING THE NEXT GENERATION OF

STRATEGIC SOURCING AT NEWELL

RUBBERMAID

10

Agenda

Who is Newell Rubbermaid?

Corporate Procurement - Challenges

Indirect Sourcing – The Journey

Enabling Change and Driving Adoption

Results, Benefits, and Key Takeaways

Questions

11

We are a global marketer of consumer and commercial

products that touch the lives of people where they work, live

and play.

Headquartered in Atlanta, GA

Approximately 19,000 employees worldwide

NYSE: NWL

Who Are We?

More than 90 percent of U.S. households

have at least one Newell Rubbermaid product.

12

Our Vision

To be a global company

of Brands That Matter™

and great people,

known for best-in-class

results.

13

Our Purpose

14

Channels & Customers

Specialty Retail

Home Center “DIY”

Office Supply

Commercial

Other

Mass Merchandisers 15

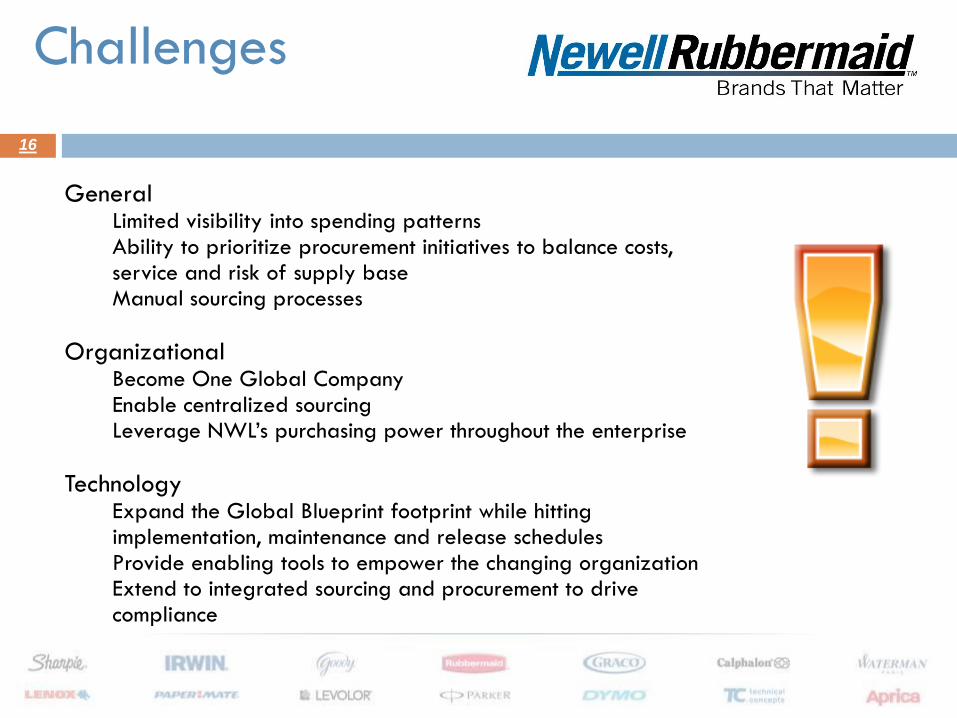

Challenges

General Limited visibility into spending patterns Ability to prioritize procurement initiatives to balance costs, service and risk of supply base Manual sourcing processes

Organizational Become One Global Company Enable centralized sourcing Leverage NWL’s purchasing power throughout the enterprise

Technology Expand the Global Blueprint footprint while hitting implementation, maintenance and release schedules Provide enabling tools to empower the changing organization Extend to integrated sourcing and procurement to drive compliance

16

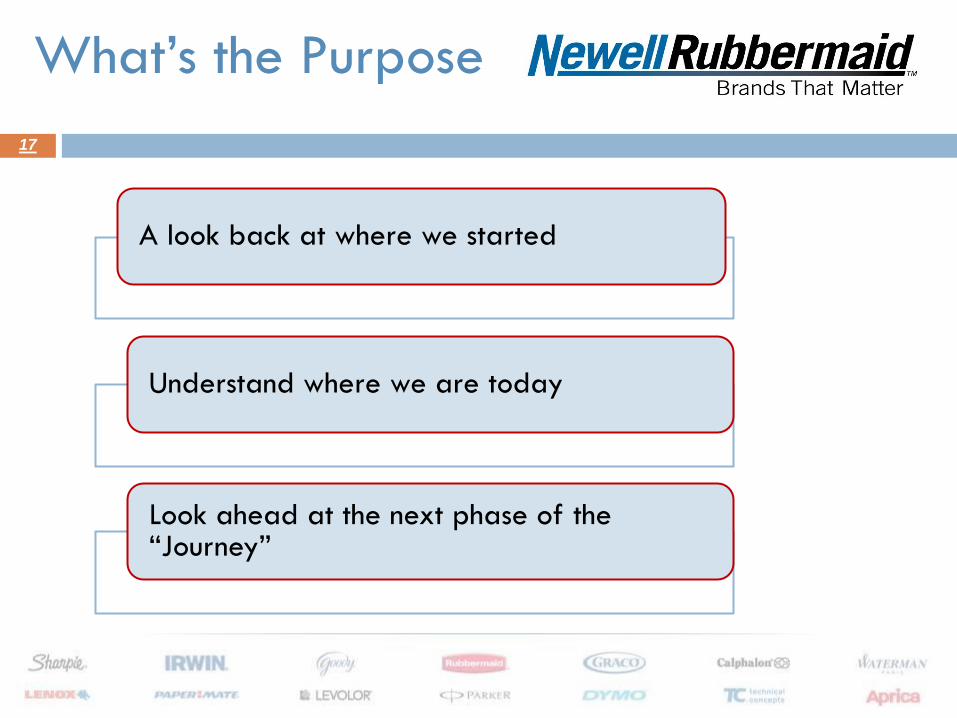

What’s the Purpose

A look back at where we started

Understand where we are today

Look ahead at the next phase of the “Journey”

17

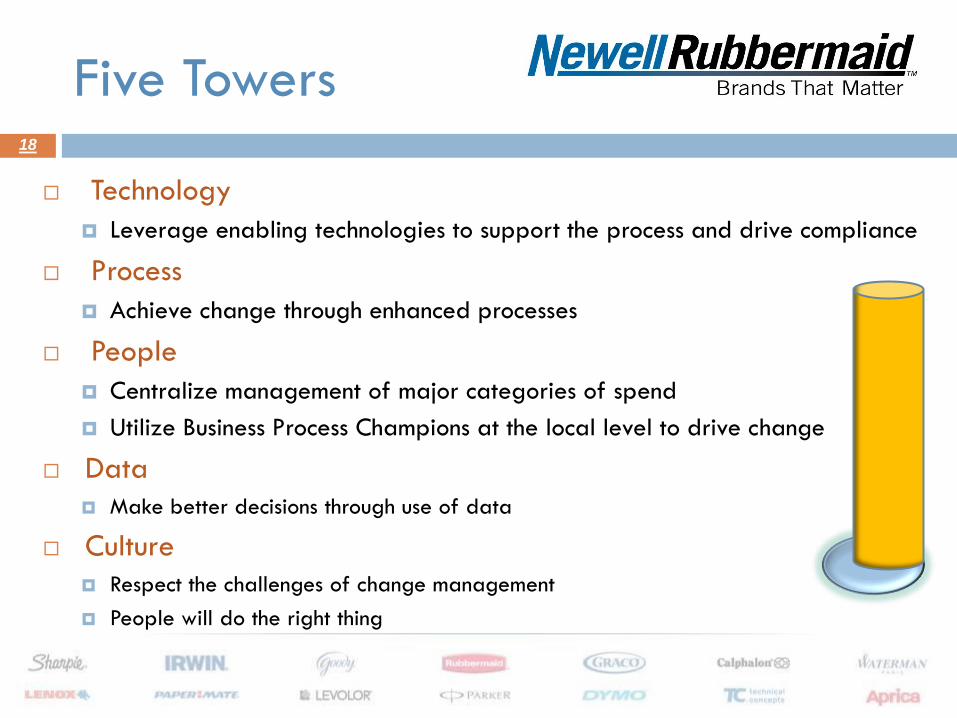

Five Towers 18

Technology

Leverage enabling technologies to support the process and drive compliance

Process

Achieve change through enhanced processes

People

Centralize management of major categories of spend

Utilize Business Process Champions at the local level to drive change

Data

Make better decisions through use of data

Culture

Respect the challenges of change management

People will do the right thing

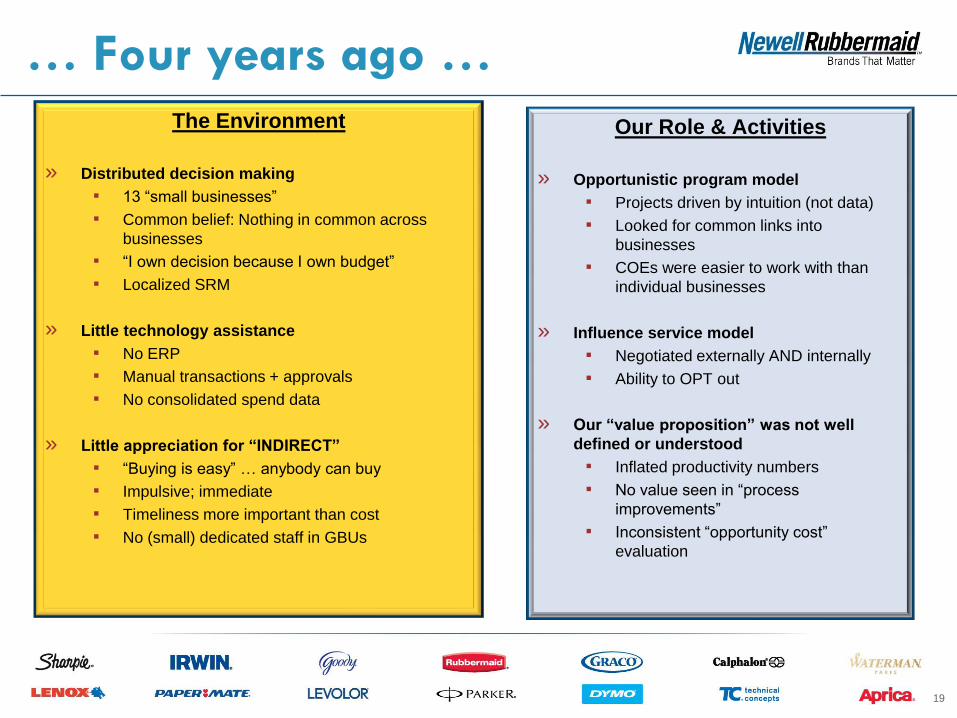

… Four years ago … The Environment

» Distributed decision making

▪ 13 “small businesses”

▪ Common belief: Nothing in common across

businesses

▪ “I own decision because I own budget”

▪ Localized SRM

» Little technology assistance

▪ No ERP

▪ Manual transactions + approvals

▪ No consolidated spend data

» Little appreciation for “INDIRECT”

▪ “Buying is easy” … anybody can buy

▪ Impulsive; immediate

▪ Timeliness more important than cost

▪ No (small) dedicated staff in GBUs

Our Role & Activities

» Opportunistic program model

▪ Projects driven by intuition (not data)

▪ Looked for common links into

businesses

▪ COEs were easier to work with than

individual businesses

» Influence service model

▪ Negotiated externally AND internally

▪ Ability to OPT out

» Our “value proposition” was not well

defined or understood

▪ Inflated productivity numbers

▪ No value seen in “process

improvements”

▪ Inconsistent “opportunity cost”

evaluation

19

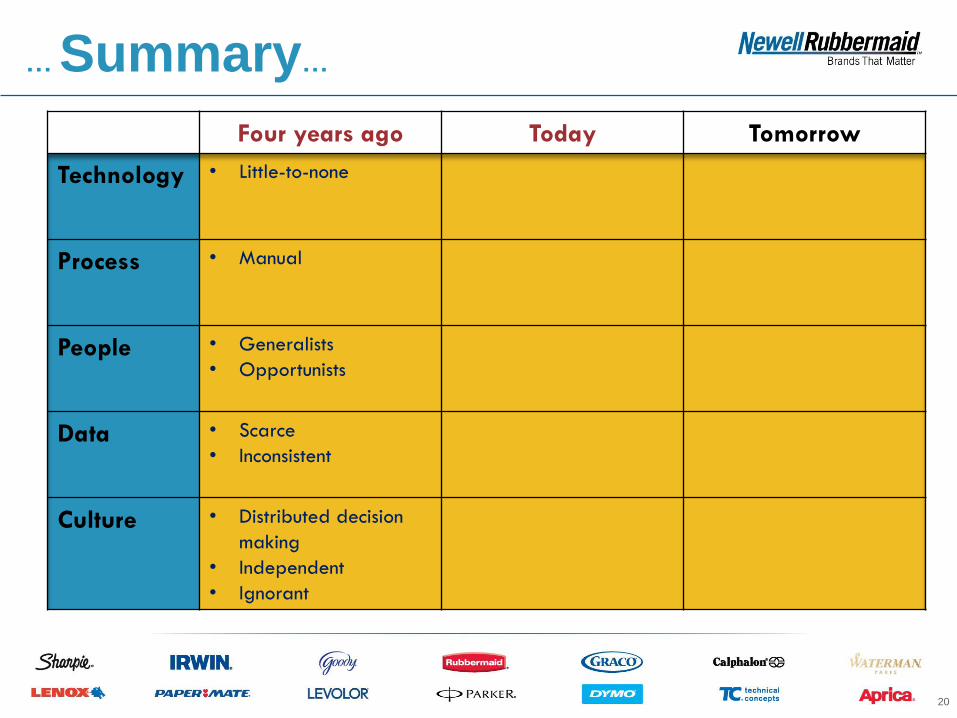

… Summary…

Four years ago Today Tomorrow

Technology

• Little-to-none

Process

• Manual

People

• Generalists

• Opportunists

Data

• Scarce

• Inconsistent

Culture

• Distributed decision

making

• Independent

• Ignorant

20

Technology

Process changes

People capacity & capabilities

Change in Culture

21

What was our Focus?

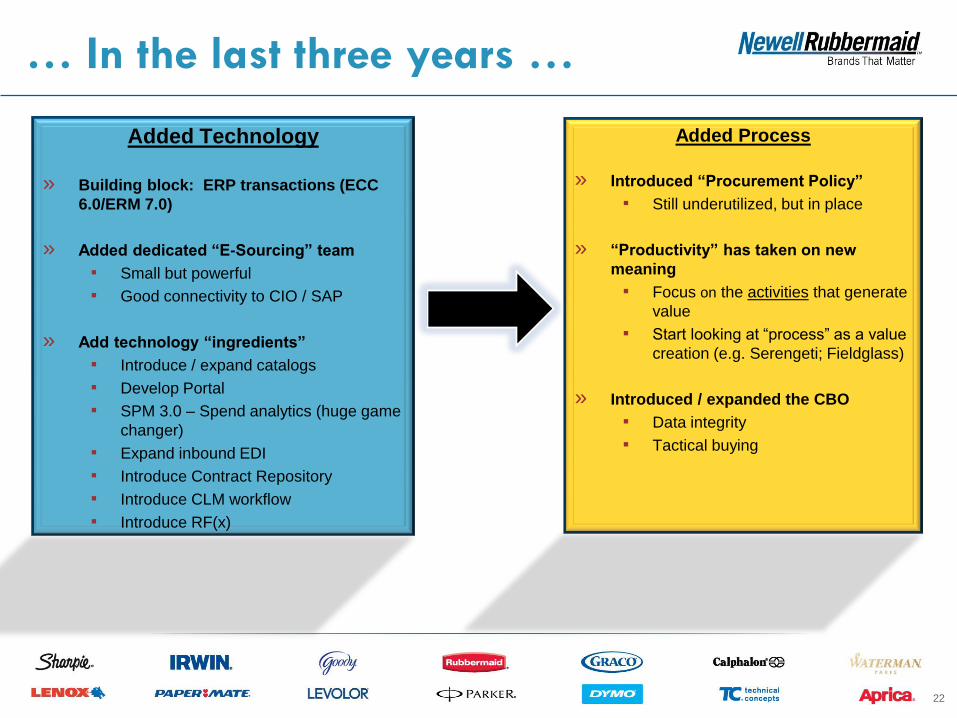

… In the last three years …

Added Technology

» Building block: ERP transactions (ECC

6.0/ERM 7.0)

» Added dedicated “E-Sourcing” team

▪ Small but powerful

▪ Good connectivity to CIO / SAP

» Add technology “ingredients”

▪ Introduce / expand catalogs

▪ Develop Portal

▪ SPM 3.0 – Spend analytics (huge game

changer)

▪ Expand inbound EDI

▪ Introduce Contract Repository

▪ Introduce CLM workflow

▪ Introduce RF(x)

Added Process

» Introduced “Procurement Policy”

▪ Still underutilized, but in place

» “Productivity” has taken on new

meaning

▪ Focus on the activities that generate

value

▪ Start looking at “process” as a value

creation (e.g. Serengeti; Fieldglass)

» Introduced / expanded the CBO

▪ Data integrity

▪ Tactical buying

22

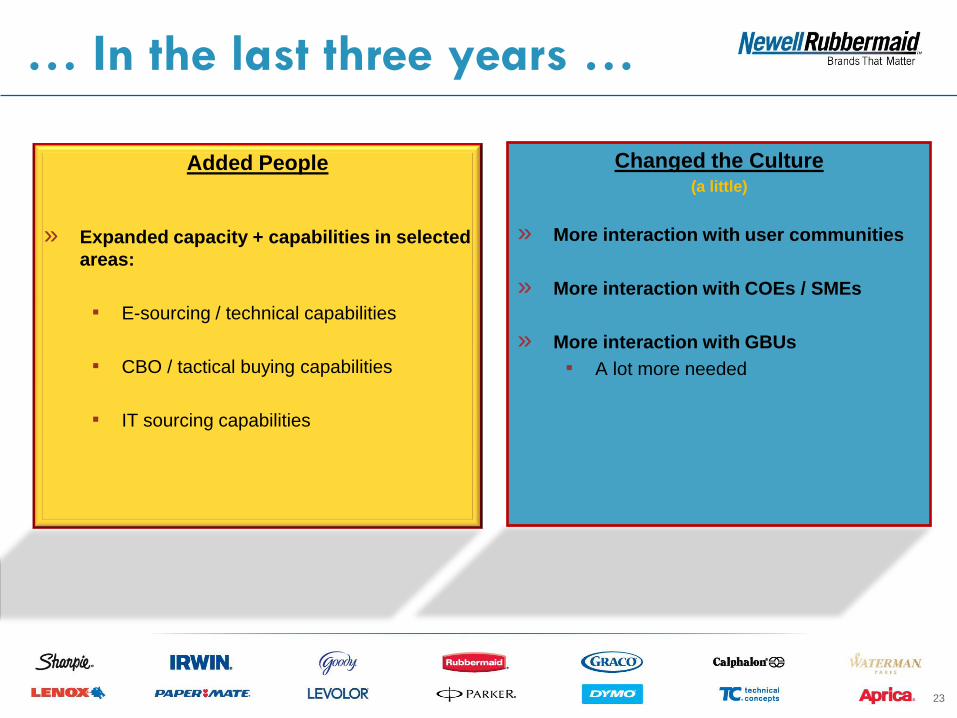

… In the last three years …

Added People

» Expanded capacity + capabilities in selected

areas:

▪ E-sourcing / technical capabilities

▪ CBO / tactical buying capabilities

▪ IT sourcing capabilities

Changed the Culture (a little)

» More interaction with user communities

» More interaction with COEs / SMEs

» More interaction with GBUs

▪ A lot more needed

23

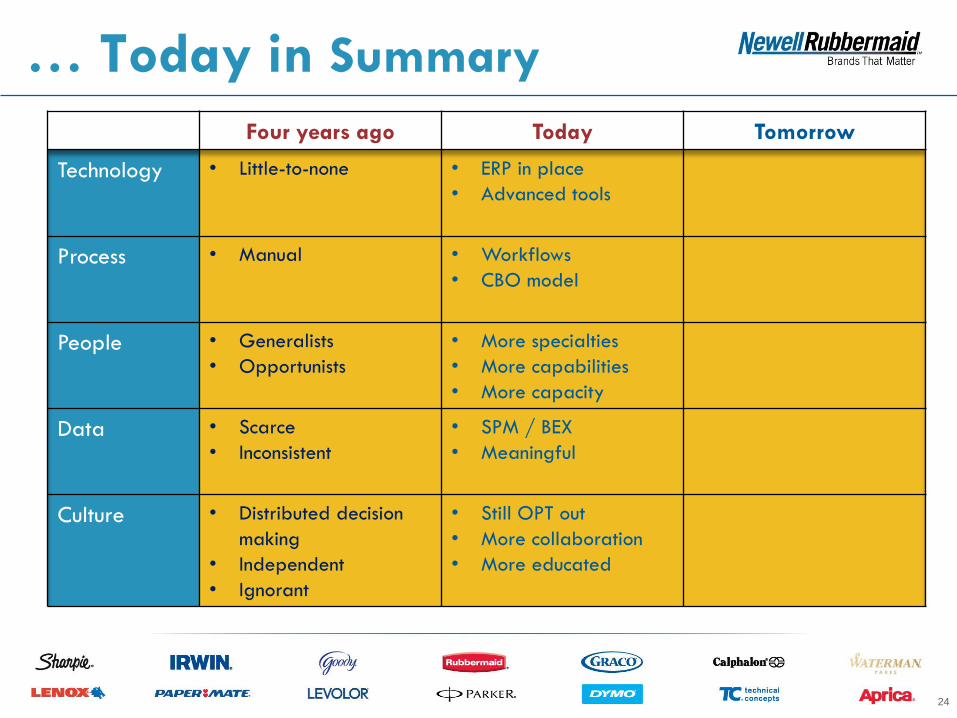

… Today in Summary

Four years ago Today Tomorrow

Technology

• Little-to-none

• ERP in place

• Advanced tools

Process

• Manual

• Workflows

• CBO model

People

• Generalists

• Opportunists

• More specialties

• More capabilities

• More capacity

Data

• Scarce

• Inconsistent

• SPM / BEX

• Meaningful

Culture

• Distributed decision

making

• Independent

• Ignorant

• Still OPT out

• More collaboration

• More educated

24

Technology

Process changes

People capacity & capabilities

Change in Culture

25

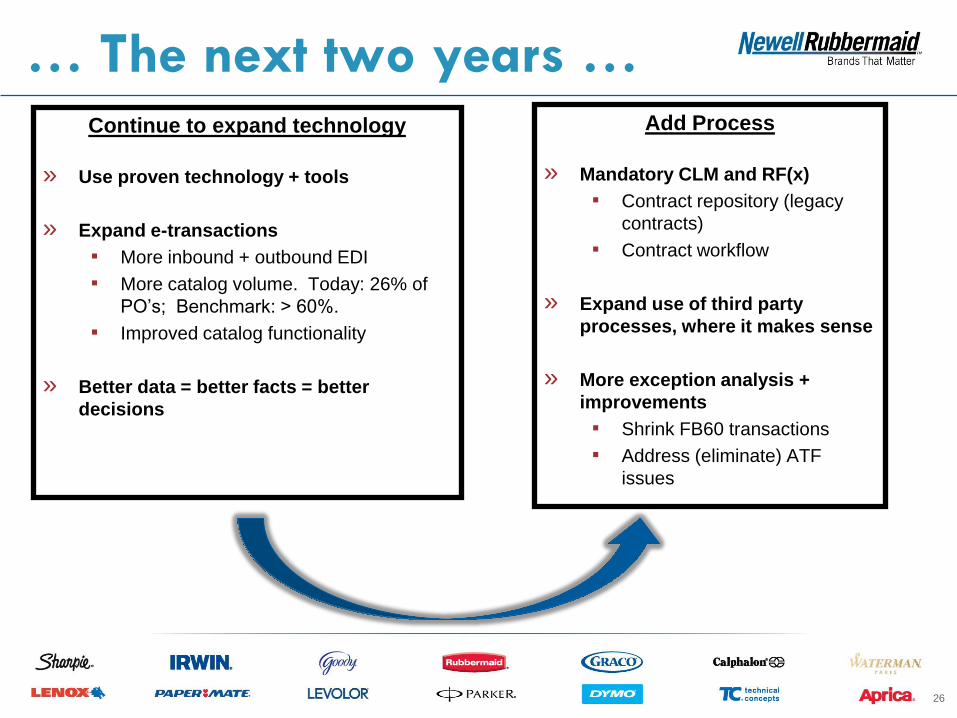

Looking Ahead... Add

… The next two years … Continue to expand technology

» Use proven technology + tools

» Expand e-transactions

▪ More inbound + outbound EDI

▪ More catalog volume. Today: 26% of

PO’s; Benchmark: > 60%.

▪ Improved catalog functionality

» Better data = better facts = better

decisions

Add Process

» Mandatory CLM and RF(x)

▪ Contract repository (legacy

contracts)

▪ Contract workflow

» Expand use of third party

processes, where it makes sense

» More exception analysis +

improvements

▪ Shrink FB60 transactions

▪ Address (eliminate) ATF

issues

26

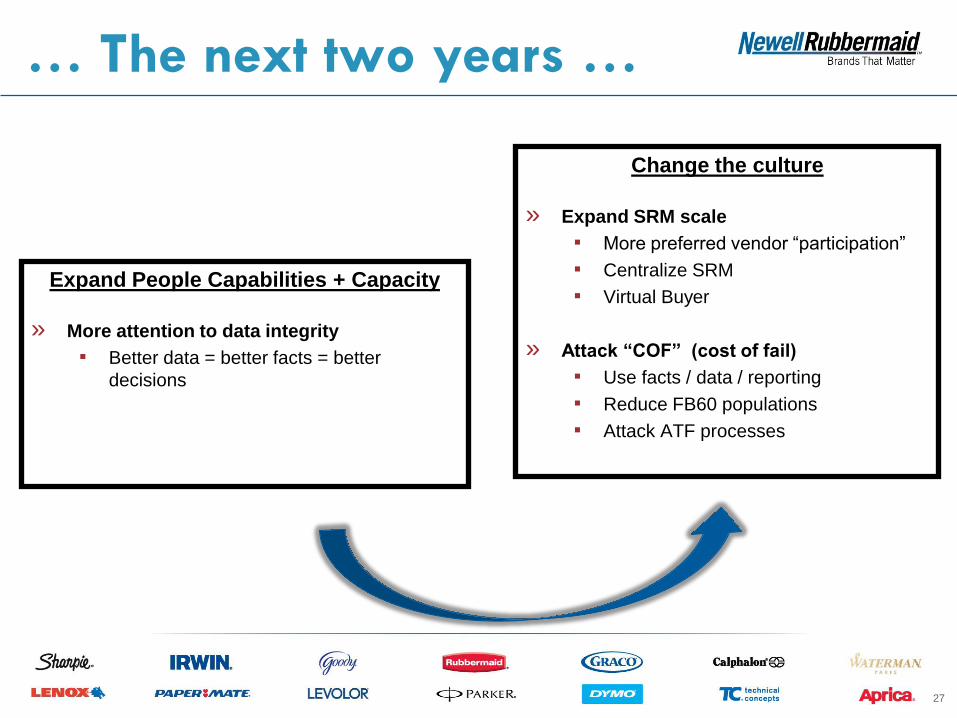

… The next two years …

Expand People Capabilities + Capacity

» More attention to data integrity

▪ Better data = better facts = better

decisions

Change the culture

» Expand SRM scale

▪ More preferred vendor “participation”

▪ Centralize SRM

▪ Virtual Buyer

» Attack “COF” (cost of fail)

▪ Use facts / data / reporting

▪ Reduce FB60 populations

▪ Attack ATF processes

27

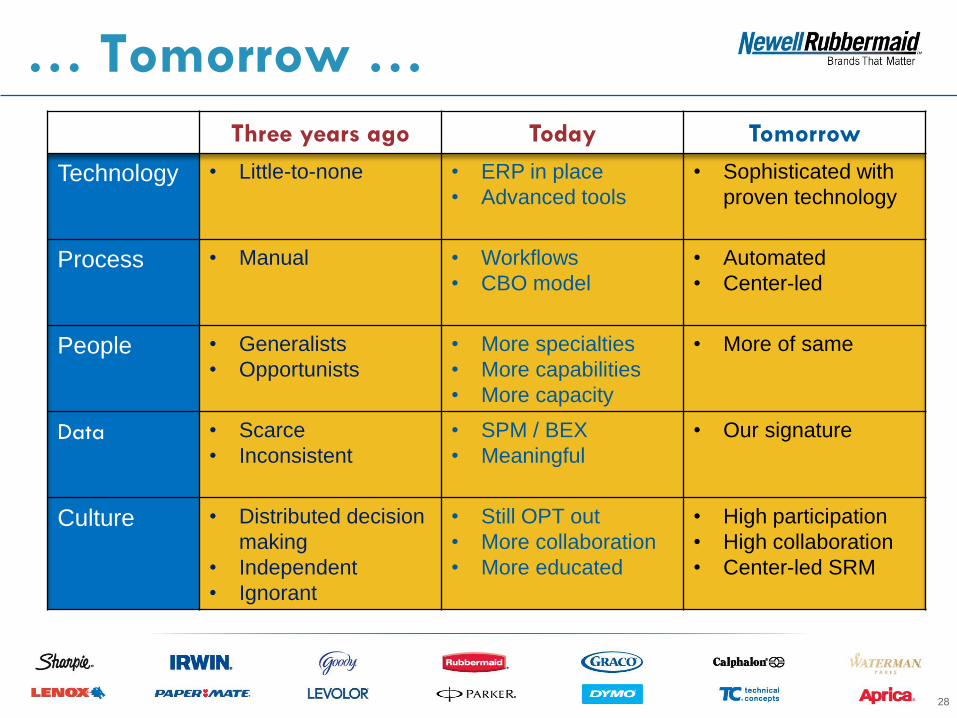

… Tomorrow …

Three years ago Today Tomorrow

Technology

• Little-to-none

• ERP in place

• Advanced tools

• Sophisticated with

proven technology

Process

• Manual

• Workflows

• CBO model

• Automated

• Center-led

People

• Generalists

• Opportunists

• More specialties

• More capabilities

• More capacity

• More of same

Data

• Scarce

• Inconsistent

• SPM / BEX

• Meaningful

• Our signature

Culture

• Distributed decision

making

• Independent

• Ignorant

• Still OPT out

• More collaboration

• More educated

• High participation

• High collaboration

• Center-led SRM

28

Summary....

» In three years, we’ve seen a major shift from “tolerated” to “engaged”

▪ Major technology- and process-enabled changes

▪ Tremendous change in our capabilities + capacity

▪ Modest changes in “culture”

» Change will accelerate

▪ Expecting a tremendous change in our level of sophistication

▪ The INDIRECT sourcing model will evolve from “influence” to more “center-led”

… and it won’t be easy

▪ The business will catch-up through technology, process, people, data and

cultural changes

» It is our role (job) to help the business adjust and accelerate the

savings from INDIRECT

29

LESSONS LEARNED

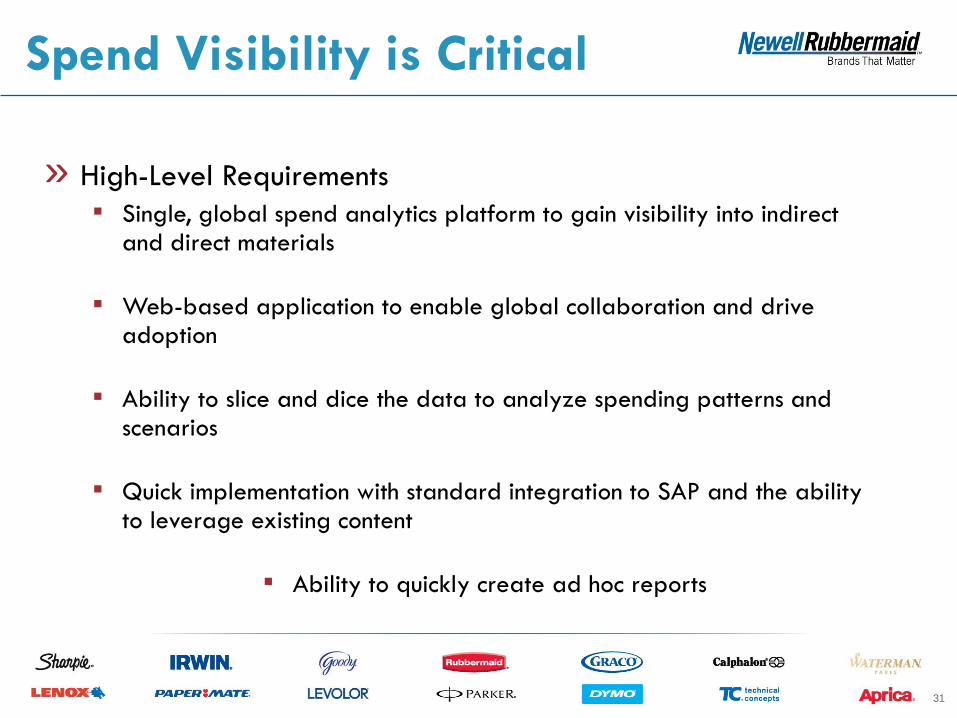

Spend Visibility is Critical

31

» High-Level Requirements

▪ Single, global spend analytics platform to gain visibility into indirect and direct materials

▪ Web-based application to enable global collaboration and drive adoption

▪ Ability to slice and dice the data to analyze spending patterns and scenarios

▪ Quick implementation with standard integration to SAP and the ability to leverage existing content

▪ Ability to quickly create ad hoc reports

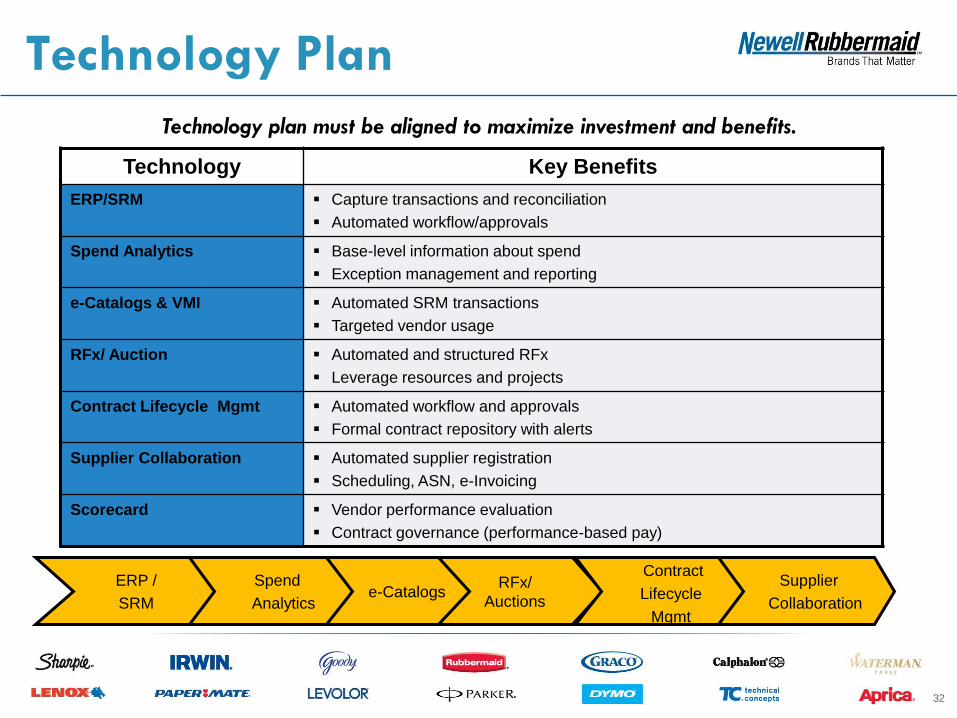

Technology Plan

32

Supplier

Collaboration

ERP /

SRM

RFx/

Auctions

Contract

Lifecycle

Mgmt

e-Catalogs Spend

Analytics

Technology Key Benefits

ERP/SRM Capture transactions and reconciliation

Automated workflow/approvals

Spend Analytics Base-level information about spend

Exception management and reporting

e-Catalogs & VMI Automated SRM transactions

Targeted vendor usage

RFx/ Auction Automated and structured RFx

Leverage resources and projects

Contract Lifecycle Mgmt Automated workflow and approvals

Formal contract repository with alerts

Supplier Collaboration Automated supplier registration

Scheduling, ASN, e-Invoicing

Scorecard Vendor performance evaluation

Contract governance (performance-based pay)

Technology plan must be aligned to maximize investment and benefits.

33

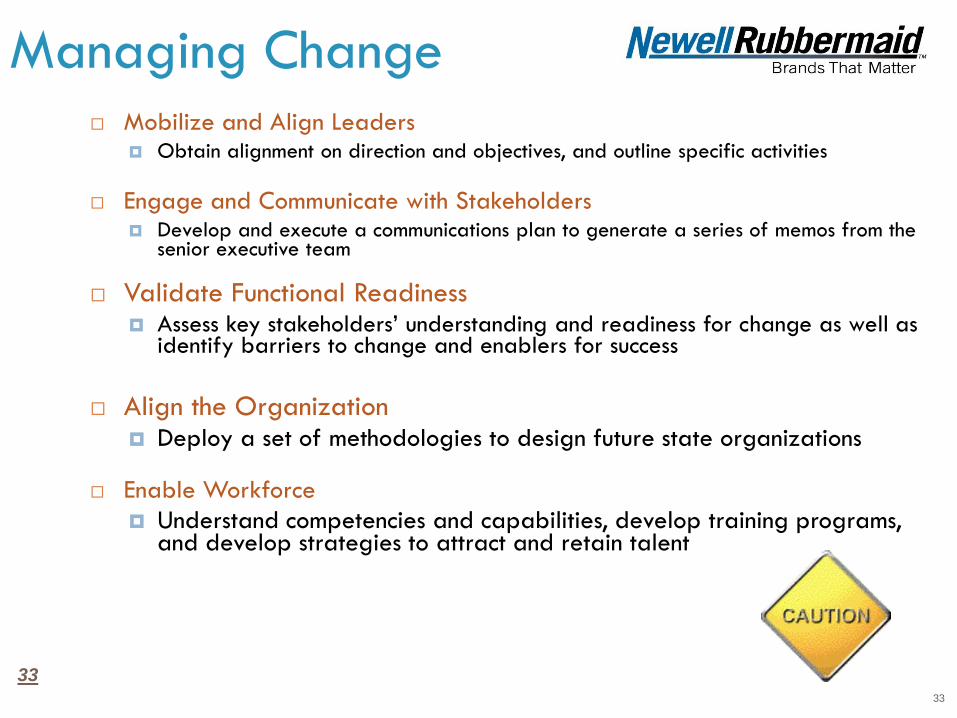

Managing Change Mobilize and Align Leaders

Obtain alignment on direction and objectives, and outline specific activities

Engage and Communicate with Stakeholders Develop and execute a communications plan to generate a series of memos from the

senior executive team

Validate Functional Readiness Assess key stakeholders’ understanding and readiness for change as well as

identify barriers to change and enablers for success

Align the Organization Deploy a set of methodologies to design future state organizations

Enable Workforce

Understand competencies and capabilities, develop training programs, and develop strategies to attract and retain talent

33

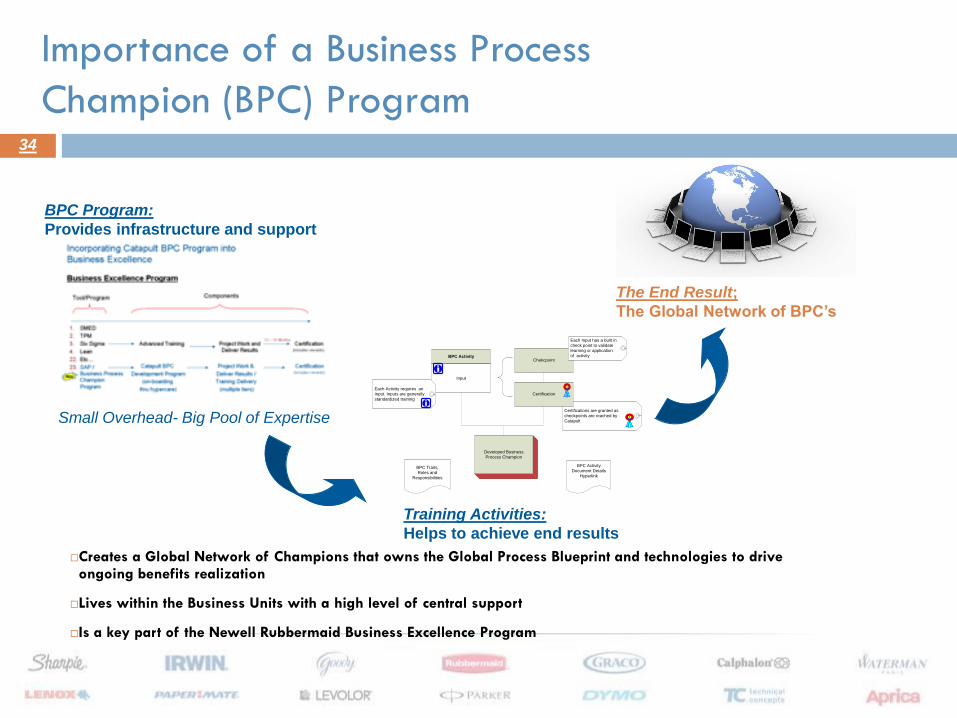

Importance of a Business Process

Champion (BPC) Program

Creates a Global Network of Champions that owns the Global Process Blueprint and technologies to drive ongoing benefits realization

Lives within the Business Units with a high level of central support

Is a key part of the Newell Rubbermaid Business Excellence Program

Certifications are granted as

checkpoints are reached by

Catapult

BPC ActivityChekcpoint

Certification

Input

Each Activity requires an

Input. Inputs are generally

standardized training

Each Input has a built in

check point to validate

learning or application

of activity

Developed Business

Process Champion

BPC Activity

Document Details

Hyperlink

BPC Traits,

Roles and

Responsibilities

Training Activities:

Helps to achieve end results

The End Result;

The Global Network of BPC’s

BPC Program:

Provides infrastructure and support

Small Overhead- Big Pool of Expertise

34

»Understands functional area and acts as a Subject Matter Expert

»Delivers results that affect bottom line and company strategies

»Able to garner project support throughout the business

»Displays energy and passion for the job

»Excites, mobilizes, and influences others

»Understand the importance of working cross functionally

»Builds and maintains working relationships

»Ability to translate technology into real world experiences

The Right BPC Enables Change and Drives Results

Selecting the Right BPC

35

RESULTS, BENEFITS, AND KEY

TAKEAWAYS

Results 37

Reduction in overall Indirect Spend by between 100-150 basis points

$10 -15mm

Standardized view of Indirect Spend

Standard workflow

UNSPSC

Increasingly standardized processes (CLM, RFx, Catalogs)

Scale, terms (cash flow)

More thought (less impulse or last minute) into local needs and alternatives

Demand destruction and better use of dollars

Creation of sourcing pipeline to drive ongoing achievement of best

value

38

Key Takeaways

A strong change management program can not be

underestimated

Configurability and flexibility are important to enable

adaptation to evolving and changing business needs

Enabling the strategic sourcing process is important to

sourcing more category spend in shorter cycle times

Technology can help to drive standard and repeatable

processes as well as enable collaboration and visibility

39

Questions?

Paula Cushing (Newell Rubbermaid) Emily Rakowski

Manager, eSourcing Global Head of Procurement Solutions Marketing

[email protected] [email protected]

Phone: 770-418-7551 Phone: 202-386-1102