dsm factbook 2017 · roche’s vitamins & fine chemicals division, subsequently renamed dsm...

TRANSCRIPT

HEALTH NUTRITION MATERIALS

ROYAL DSM

DSM Factbook 2017

DSM Investor Relations | Contact

Page 1

Dave Huizing – Vice President Investor Relations

t. +31 45 578 2864

Petra Volk – IR Support Officer

t. +31 45 578 2511

Sandra Segers – IR Support Officer

t. +31 45 578 2864

Marc Silvertand – IR Manager

t. +31 45 578 2348

Thijs van der Heide – IR Manager

t. +31 45 578 2282

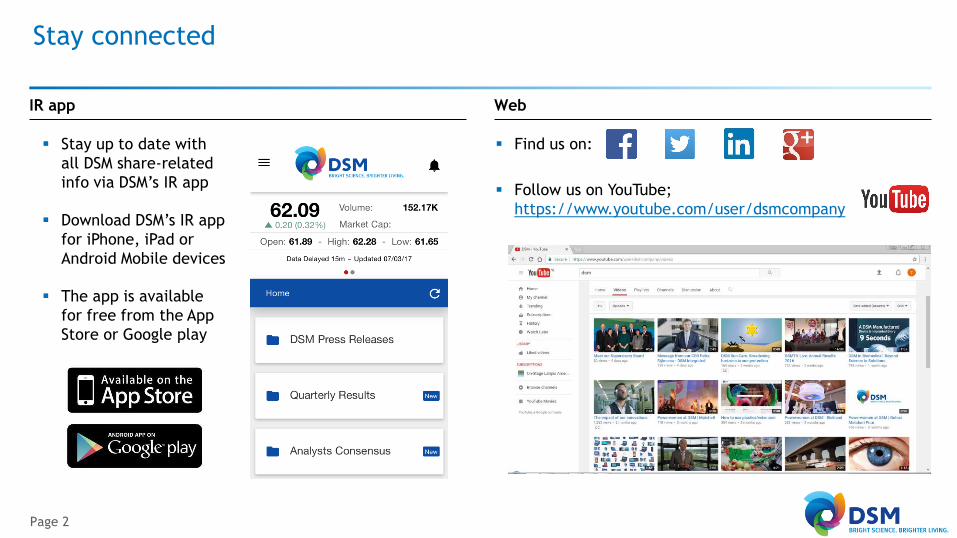

Stay connected

Page 2

WebIR app

▪ Stay up to date with

all DSM share-related

info via DSM’s IR app

▪ Download DSM’s IR app

for iPhone, iPad or

Android Mobile devices

▪ The app is available

for free from the App

Store or Google play

▪ Find us on:

▪ Follow us on YouTube;

https://www.youtube.com/user/dsmcompany

HEALTH NUTRITION MATERIALS

ROYAL DSM

DSM at a glance/Strategy 2018

Business overview

Financial data

Share-related information

1

2

3

4

DSM at a glance | People, planet, profit in 2016

Page 4

1. Continuing operations unless stated otherwise

2. See page 142 of the Integrated Annual Report 2016 for reconciliation

People Planet Profit1

Watch clip:

DSM at a glance | 2016 key financial data

Page 5

1. At 31 December

2. Income statement expense and capitalized costs (including associated IP expenditure)

1,262

931

435

MaterialsNutrition GroupCorp.

Act.

105

Innovation

Center

1

Sales Adj. EBITDA & Adj. EBITDA margin (%)

Capital Employed1 and ROCE (%) Capital Expenditure (accounting)

Adj. EBIT & Adj. EBIT margin (%)

R&D Expenditure2

18.0 17.3 15.9

7,920

5,169

2,513

GroupCorp.

Act.

71

Innovation

Center

167

MaterialsNutrition

141 791

645

311

GroupCorp.

Act.

Innovation

Center

24

MaterialsNutrition

12.5 12.4 10.0

7,889

5,5371,807

Nutrition GroupCorp.

Act.

31

Innovation

Center

576

Materials

12.0 17.6 10.4

485

331106

Corp.

Act.

16

Innovation

Center

32

MaterialsNutrition Group

426

205

75

124

MaterialsNutrition GroupCorp.

Act.

22

Innovation

Center

Watch clip:

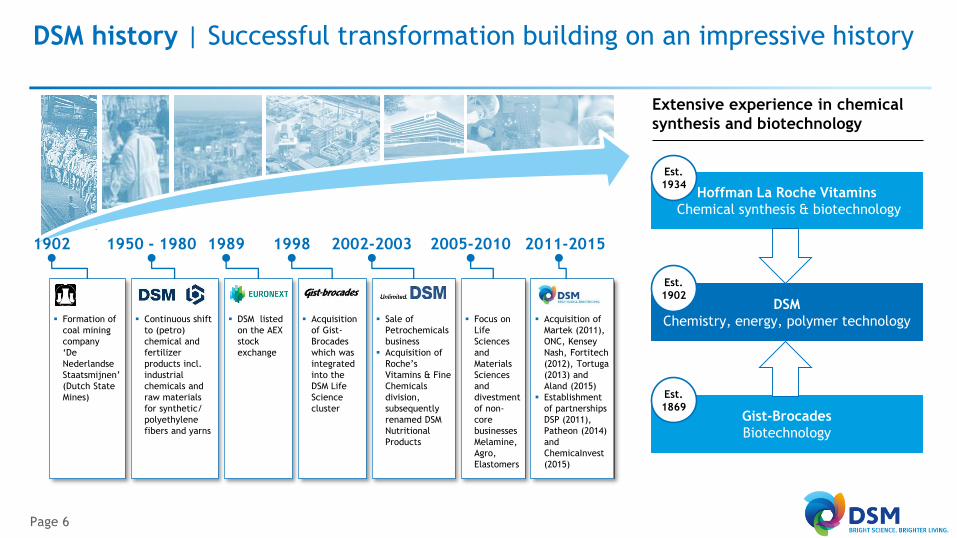

DSM history | Successful transformation building on an impressive history

Page 6

▪ Formation of

coal mining

company

‘De

Nederlandse

Staatsmijnen’

(Dutch State

Mines)

1950 - 1980

▪ Continuous shift

to (petro)

chemical and

fertilizer

products incl.

industrial

chemicals and

raw materials

for synthetic/

polyethylene

fibers and yarns

1989

▪ DSM listed

on the AEX

stock

exchange

1998

▪ Acquisition

of Gist-

Brocades

which was

integrated

into the

DSM Life

Science

cluster

2002-2003

▪ Sale of

Petrochemicals

business

▪ Acquisition of

Roche’s

Vitamins & Fine

Chemicals

division,

subsequently

renamed DSM

Nutritional

Products

2005-2010

▪ Focus on

Life

Sciences

and

Materials

Sciences

and

divestment

of non-

core

businesses

Melamine,

Agro,

Elastomers

2011-2015

▪ Acquisition of

Martek (2011),

ONC, Kensey

Nash, Fortitech

(2012), Tortuga

(2013) and

Aland (2015)

▪ Establishment

of partnerships

DSP (2011),

Patheon (2014)

and

ChemicaInvest

(2015)

Extensive experience in chemical

synthesis and biotechnology

DSM

Chemistry, energy, polymer technology

Hoffman La Roche Vitamins

Chemical synthesis & biotechnology

Gist-Brocades

Biotechnology

Est.

1934

Est.

1902

Est.

1869

1902

DSM history | Business portfolio streamlined and simplified,

creating good platform for growth

Page 7

Significant portfolio transformation (in % of DSM sales)

▪ Built a broad, deep and global

Nutrition business

▪ Upgraded Materials businesses

▪ Became a more global, innovative

and sustainable company

▪ Extensive experience in chemical

synthesis and biotechnology binds

Nutrition and Materials

▪ Created 3 new growth platforms:

– Innovative materials for

medical devices

– Clean energy (from crop

– residues) and bio-chemicals for

biomass conversion

– Yield-boosting solutions for

solar energy

2010200520001995 2015

100%

Nutrition

Innovation Center

Materials

Pharma

Polymer Intermediates & Composite Resins

Other

▪ Petrochemicals

▪ Energy

▪ Engineering

▪ Plastic

products

▪ Curver

▪ Base Chemicals

& Materials

▪ Others

▪ Petrochemicals

▪ Energy

▪ Engineering

▪ Plastic

products

▪ Base Chemicals

& Materials

▪ Others

▪ Base Chemicals

& Materials

▪ Energy

Nutrition

Materials

Innovation

DSM today | DSM expects to extract significant value from further exiting

its legacy partnerships in the coming years

Page 8

1. On 15 May 2017, DSM informed markets that it had unanimously approved the acquisition of Patheon by Thermo Fisher Scientific. Thermo Fisher will

commence a tender offer to acquire all shares for $35 per share. The transaction is expected to be completed by the end of 2017

2. Book year 1 November until 31 October. Based on continuing operations

In € million at 100% 2016

Sales 431

Adjusted EBITDA% 14%

In € million at 100% 20162

Sales 1,786

Adjusted EBITDA% 20%

In € million at 100% 2016

Sales 1,802

Adjusted EBITDA% 6%

DSM Sinochem Pharmaceuticals (50%)

Pharma - Antibiotics

Patheon (34%)1

Pharma - Contract Manufacturing

ChemicaInvest (35%)

Bulk Chemicals

▪ JV with Sinochem created in 2011

when Sinochem took a 50% interest

in DSM Anti-Infectives

▪ Global leader in generic anti-

infective

▪ Created in 2014, when DSM

combined DSM Pharmaceutical

Products with JLL Partners’ Patheon

▪ Produces a unique breadth of

offerings from finished dosage (drug

products) to active substances (APIs)

▪ Created in 2015 when CVC Capital

Partners took a 65% stake in the (bulk

chemical) activities of DSM in

caprolactam, acrylonitrile and

composite resins

DSM today | A broad, deep and global Nutrition business and a focused,

high-quality, specialty Materials portfolio

Page 9

Sales

€7,920

Adj. EBITDA

€1,262

Adj. EBITDA%

15.9%

ROCE

10.4%

Nutrition

▪ Nutrition is active in nutritional ingredients for

animal feed and food, as well as in food specialty

ingredients and performance ingredients for

personal care, serving the global feed, food &

beverage, pharmaceutical, infant nutrition,

dietary supplements and personal care industries

Sales

€5,169

EBITDA

€931

EBITDA%

18.0%

Materials

▪ Advanced materials for high-performance

components for the electrical and electronics,

automotive, (flexible food) packaging, consumer

goods, life protection, transportation and telecom

industries

Sales

€2,513

EBITDA

€435

EBITDA%

17.3%

Animal

Nutrition

Human

Nutrition

DSM Food

Specialties

Pers. Care

& Aroma Ingr.

DSM Engineering

Plastics

DSM Dyneema DSM Resins &

Functional Materials

DSM today | Emerging Business Areas provide long-term growth platforms

based on the company’s core competences

Page 10

▪ DSM Biomedical supplies innovative

biomedical materials that enable

medical device manufacturers to

make less invasive devices. These

can speed up recovery, shorten

hospital stays and minimize

reoperations, lowering health costs

and helping people to lead longer,

healthier and more active lives

▪ DSM Bio-based Products & Services is

at the forefront of building a more

sustainable, bio-based economy with

solutions for clean fuel from

agricultural residue and for

renewable chemical building blocks

such as bio-based succinic acid

▪ DSM Advanced Solar develops and

provides solutions to increase the

yield of solar panels – Same sun.

More power™.

DSM Biomedical

Enabling innovative medical devices

DSM Bio-based Products & Services

Enzymes/yeast for biomass conversion

DSM Advanced Solar

Efficiency-increasing products for solar

DSM today | A well-balanced and diversified portfolio

Page 11

1. Personal Care & Aroma Ingredients

Net sales by end-use market (%)Net sales by origin (%)

1%

3%

1%

1%

11%

7%

18%

2%31%

25%

Rest of the World

Rest of Asia

Japan

India

China

Latin America

North America

Eastern Europe

Rest of Western Europe

The Netherlands

6%

25%

4%3%10%

3%2%

12%

12%

23%

Eastern Europe

Rest of Western Europe

The Netherlands

Rest of the World

Rest of Asia

Japan

India

China

Latin America

North America

8%

6%

5%1%

7%

6%

Other

Packaging

Electrical & electronics

Textiles

Automotive/transport

Metal/building & construction

Nutrition and Health

1%

2%

32%

65%

Corporate Activities

Innovation Center

Materials

Nutrition

Net sales by business segment (%)Net sales by destination (%)

67%

▪ Animal Nutrition (31%)

▪ Human Nutrition (24%)

▪ Food Specialties (7%)

▪ Other (1%)

▪ PC & AI (4%)1

DSM today | Global production while offering a local approach

Page 12

1. As per 31 December 2016

2%

23%

19%1%

4%

1%

2%

22%

10%

15%

North America

Eastern Europe

Rest of Western Europe

The Netherlands

Rest of World

Rest of Asia

Japan

India

China

Latin America

Africa:

73 employees

2,447

619

4,460

13,260Corporate Activities

Innovation Center

Materials

Nutrition

Total employees | 20,786

North America

3,187

Europe

9,180

Asia

6,090

RoW

260

Latin America

2,069

Employees per business segment1

Employees per region1Global presence1

Watch clip:

DSM today | Sustainability agenda is core to DSM’s business strategy1

Page 13

1. Please see DSM’s Integrated Annual Report 2016 for definitions and additional information

GHG and Energy

Efficiency

Renewable

energy

Brighter Living Solutions: ECO+ and People+

▪ Profitable solutions better for people and planet

▪ Aspiration: 65% of DSM products by 2020

Health & Safety

Engagement

Diversity

Securing sustainable operations

Operational Aspirations

▪ Leading in reporting benchmarks Gold class DJSI

▪ GHG efficiency improvements 40-45% (2008-2025)

▪ Energy efficiency improvements >10% (2016-2025)

▪ Purchased electricity from renewables 50% by 2025

▪ Employee engagement favorable score 75% by 2020

▪ Safety: Frequency recordable index 0.25 by 2020

Gold class

23%

2%

8%

71%

0.33

Eco+ People+

Sustainability as business growth driver

Key sustainability focus areas

▪ Nutrition

▪ Climate change and renewable energy

▪ Circular and bio-based economy

2016

63%

2016

Long-term goals

DSM today | DSM and the Sustainable Development Goals

Page 14

1. Please see DSM’s Integrated Annual Report 2016, pages 12 and 13 for additional details

▪ At DSM, we believe that companies have a

crucial role to play in creating the impact

needed at scale to achieve the 17 Global

Goals for Sustainable Development

▪ We believe that our expertise in health,

nutrition and materials position DSM well

to actively contribute to the SDGs

▪ While all the Goals are important, there

are five SDGs on which we believe our

company and its businesses can be most

influential

▪ DSM collaborates with multiple partners

and stakeholders, in line with SDG 17

(Partnering for the Goals), including UN

agencies, governments, academia, NGOs

and peers (see also next page)

Main intersections between the SDGs and DSM1

SDG 2 | End hunger, achieve food security and improved nutrition and promote sustainable

agriculture. DSM works to improve nutrition via initiatives such as the Nutrition Improvement

Program and Africa Improved Foods, providing fortified food solutions and micronutrient products,

as well as through partnerships such as with WFP. We continue to support the independent

nutrition think-tank, Sight and Life

SDG 3 | Ensure healthy lives and promote well-being for all at all ages. DSM’s health, nutrition,

biomedical and high-performance materials portfolios are geared to maintaining, protecting or

regenerating health in all age groups (for example, by reducing salt and sugar levels in processed

foods, or by reducing emissions associated with chemical manufacturing processes). Our First 1,000

Days Program supports mother and child health. We employ the DSM Life Saving Rules to protect our

employees from harm and the DSM Vitality Program to promote awareness of good health and

healthy living options among our employees

SDG 7 | Ensure access to affordable, reliable, sustainable and modern energy for all

SDG 13 | Take urgent action to combat climate change and its impacts. In partnership with RE100,

we are increasing the use of renewables in our energy mix, reducing our carbon footprint. DSM

enables solar and bio-based energy solutions and supports the move toward a low-carbon economy

through solutions such as POET-DSM advanced biofuels and high-performance materials for solar

panels. Our Bright Minds Challenge is identifying innovative solutions and new materials that will

fast-track the movement toward 100% renewable energy. We advocate responsible action on

climate change in combination with our stakeholders

SDG 12 | Ensure sustainable consumption and production patterns. DSM contributes to a bio-based,

circular and low-carbon economy with products such as Akulon® oil pans and Arnite® car lighting.

DSM-Niaga enables the manufacture of carpets that can be recycled, again and again. Food waste is

reduced through DSM food solutions such as Pack-Age®. Bio-based chemicals such as bio-succinic

acid replace fossil-fuel based alternatives in applications from packaging to footwear. Through our

Brighter Living Solutions program we consider the impact of our products throughout the value chain

DSM today | Rewarding partnerships to fight malnutrition around the

world

Page 15

1. For a more extensive list and description of DSM’s other nutrition platforms and partnerships, please see our website

▪ As a leading micronutrient provider DSM develops innovative

solutions for improved nutrition. In order for these solutions to

have the broadest reach, and in line with SDG 17, we work with

partner organizations that have direct access to beneficiaries

▪ DSM’s nutrition partnerships focus on the following objectives:

– Wider base of scientific evidence and endorsement;

– Increased market for nutrition products;

– Improved employee engagement

▪ DSM’s partners range from UN agencies, governments, academia

and NGOs to industry peers

▪ We commit support through financial and non-financial means

including time, technical expertise, products and volunteers

DSM’s main cross-sector nutrition partnerships1

DSM today | External recognition1

Page 16

1. For more information please see https://www.dsm.com/corporate/about/our-company/external-recognition.html

▪ In August 2016, Fortune Magazine revealed that DSM was included in its second annual Change the World List which highlights the 50 leading

companies that are innovating to solve the world’s biggest challenges through core profit-making strategy and operations

▪ On 8 September, DSM was named the worldwide leader in the Materials industry group in the Dow Jones Sustainability World Index. DSM has

consistently been recognized for integrating sustainability into its business, having been named among the global leaders in each of the last 13 years

and holding the number one position in the sector seven times

▪ On 30 September, DSM’s Science Can Change the World campaign won in the Best Communication category at the Ethical Corporation Responsible

Business Awards 2016. DSM was also ‘highly commended’ in the Best Sustainable Company category. The Awards recognize genuine, truly innovative

and meaningful approaches to making responsible business a reality

▪ DSM has been identified as a global leader for its actions and strategies in response to climate change and has been awarded a position on the Climate

A List by CDP, the international not-for-profit that drives sustainable economies. 193 “A Listers” appear on the list, which has been produced at the

request of 827 investors with assets of US$100 trillion

▪ On 25 October 2016, DSM was reconfirmed as a constituent of the Ethibel Sustainability Index (ESI) Excellence Europe. The ESI Excellence Europe

contains shares of 200 European companies that are included in the Russell Global Index that display the best performance in terms of corporate

social responsibility (CSR)

▪ On 4 November 2016, Reverdia, the joint venture between DSM and Roquette Frères that produces Biosuccinium™ (succinic acid), the first non-fossil

feedstock derived chemical building block, topped the Biofuels Digest 40 Hottest Emerging Companies in the Advanced Bioeconomy 2016-17

▪ Each year Corporate Knights publishes their Global 100 Index of the most sustainable corporations in the world. In the 2017 Index published on 16

January, DSM was the highest ranked materials company for a second successive year and rose from 23rd place overall in 2016 to 9th in 2017. Those

featured are considered leaders in transparency, in resource productivity and on a range of other social and governance indicators

DSM today | DSM management

Page 17

DSM Managing Board

▪ Member of the Managing Board since

September 2013

▪ With DSM since 1990

Dimitri de Vreeze

Member of the Managing Board

Nationality: Dutch

▪ CEO since 1 May 2007, member of the Managing

Board since 2000

▪ With DSM since 1998 when DSM acquired Gist-

Brocades. Joined Gist-Brocades in 1987

Feike Sijbesma

CEO/Chairman of the Managing Board

Nationality: Dutch

DSM Supervisory Board DSM Executive Committee

▪ Rob Routs (Chairman)

▪ Tom de Swaan

▪ Pauline van der Meer Mohr

▪ John Ramsay

▪ Victoria Haynes

▪ Eileen Kennedy

▪ Pradeep Pant

▪ Frits van Paasschen

▪ Feike Sijbesma (CEO/Chairman)

▪ Geraldine Matchett (CFO)

▪ Dimitri de Vreeze (Materials)

▪ Chris Goppelsroeder (Nutrition)

▪ Philip Eykerman (Strategy and M&A)

▪ Peter Vrijsen (People & Organization)

▪ Rob van Leen (R&D and Innovation)

▪ CFO since December 2014, member of the

Managing Board since August 2014

▪ Prior to joining DSM, Global CFO of SGS Group,

a publicly quoted company on the SIX Swiss

stock exchange

Geraldine Matchett

Chief Financial Officer

Nationality: British, French, Swiss

Strategy 2018 | Summary and 2016 achievements

Page 18

Two headline

financial targets

High single-digit percentage

annual Adjusted EBITDA growth

2016 achievements:

▪ 17%

High double-digit basis point

annual ROCE growth

2016 achievements:

▪ 280 bps

Clear actions identified to

achieve targets

Businesses aim to outpace

market growth

2016 achievements:

Nutrition

▪ 5% organic growth

Materials

▪ 4% volume growth

€250-300m cost reduction &

efficiency improvements

2016 achievements:

▪ On track: ~€110m

cumulative savings by

year-end 2016

Consistent improvements in

capital efficiency

2016 achievements:

▪ Cash from operating

activities up 27%

▪ Capex at €475m,

<€500-550m guidance

▪ Total Working Capital

at 18.4%, better than

aspiration level

✓ ✓

✓

✓

✓

Additional items underpinning

strategy

Stepping up sustainability

aspirations

2016 achievements:

▪ On track

Global organizational and

operational adjustments

2016 achievements:

▪ On track

Extract value from Pharma and

Bulk Chemicals JVs

2016 achievements:

▪ 1st step taken with sale

of 4.8m shares in Patheon

✓

✓

✓

✓ ✓ ✓

Strategy 2018 | Driving profitable growth through science-based,

sustainable solutions

Page 19

▪ Following a period of important transformation, DSM is now focusing on ensuring that the potential of the current

business portfolio translates into improved financial results during the 2016-2018 period

▪ Two headline financial targets

– High single-digit percentage annual Adjusted EBITDA growth & high double-digit basis point annual ROCE growth

HEALTH . NUTRITION . MATERIALS

IMPROVING

FINANCIAL RESULTS

Growth

Cost & Productivity

Capital

Efficiency

2018 TARGETS

annual Adj. EBITDA growth:

high single-digit percentage

- - -

annual ROCE growth:

high double-digit bps

Global shifts &

Digitization

Climate &

Energy

Health &

Wellness

Result-driven organization

& culture

BRIGHT SCIENCES

Strategy 2018 | Well-identified initiatives to drive Strategy 2018 targets

Page 20

1. Savings as of 2015

▪ DSM is confident it has the right business strategies in place to meet the needs of its customers and succeed in its

markets, providing innovative and sustainable solutions

▪ Aims to accelerate growth and outpace market growth in all its key segments

▪ In addition to its growth initiatives, self-help programs will further help delivery of the Strategy 2018 targets

2015

EBITDA

2018

EBITDA

~€100-125m1

~€130-150m

InflationSupport

functions& services program

Nutrition program Sales above

market growth

Strategy 2018 | Nutrition growth strategy

Page 21

▪ Annual EBITDA growth:

high single-digit percentage

▪ Annual ROCE growth:

high double-digit bps

▪ EBITDA margins: 18-20% over the period

▪ Above-market sales growth (at stable

prices)

Nutrition strategy 2018 Aspirations underlying Group targets

Excellence in execution

2

143

▪ Profitable growth via:

▪ Expanding the core

▪ New products and solutions

▪ Growing in underpenetrated

categories/regions

▪ Accessing new segments/new

business models

▪ Reducing costs and increasing

productivity

▪ Driving cash generation

▪ Increasing capital efficiency

1

2

3

4

Strategy 2018 | Growth projects in Nutrition are delivering

Page 22

Excellence in execution

2

143

▪ Expand the core

– New vitamin B6 plant and

expansion of the gellan-gum

and pectin facilities all in

China;

▪ Add new products and solutions

– Product offering broadened

e.g. eubiotics for antibiotic-

free poultry;

– Good progress in the ‘Green

Ocean’ and ‘Clean Cow’

projects;

1

2

2016

▪ Organic growth: 5%

▪ EBITDA growth: 13.3%

▪ ROCE up 170 bps

Nutrition Strategy 2018 and 2016 milestones

Watch clip:

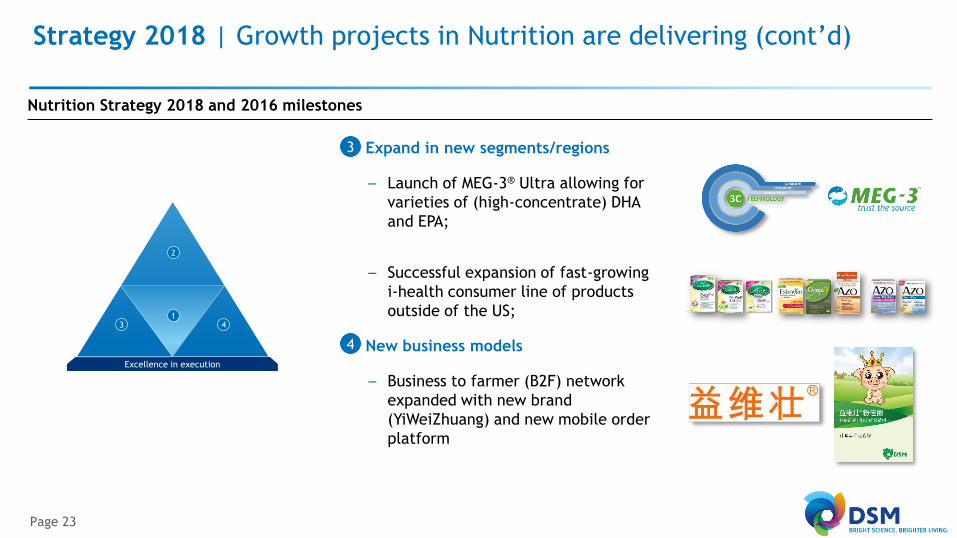

Strategy 2018 | Growth projects in Nutrition are delivering (cont’d)

Page 23

Nutrition Strategy 2018 and 2016 milestones

Excellence in execution

2

143

▪ Expand in new segments/regions

– Launch of MEG-3® Ultra allowing for

varieties of (high-concentrate) DHA

and EPA;

– Successful expansion of fast-growing

i-health consumer line of products

outside of the US;

▪ New business models

– Business to farmer (B2F) network

expanded with new brand

(YiWeiZhuang) and new mobile order

platform

3

4

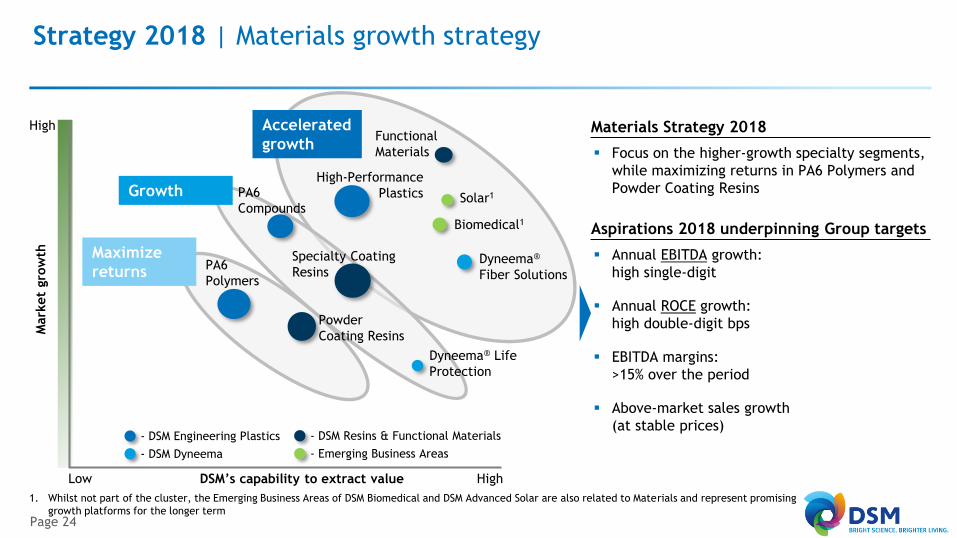

Strategy 2018 | Materials growth strategy

Page 24

1. Whilst not part of the cluster, the Emerging Business Areas of DSM Biomedical and DSM Advanced Solar are also related to Materials and represent promising

growth platforms for the longer term

▪ Annual EBITDA growth:

high single-digit

▪ Annual ROCE growth:

high double-digit bps

▪ EBITDA margins:

>15% over the period

▪ Above-market sales growth

(at stable prices)

Aspirations 2018 underpinning Group targets

High Low

High-Performance

Plastics

Biomedical1

Functional

Materials

Specialty Coating

Resins

DSM’s capability to extract value

Mark

et

gro

wth

Solar1

Dyneema® Life

Protection

Growth

Accelerated

growth

Powder

Coating Resins

PA6

Polymers

PA6

Compounds

- DSM Engineering Plastics

- DSM Dyneema

- DSM Resins & Functional Materials

- Emerging Business Areas

High

Maximize

returnsDyneema®

Fiber Solutions

Materials Strategy 2018

▪ Focus on the higher-growth specialty segments,

while maximizing returns in PA6 Polymers and

Powder Coating Resins

High Low

High-Performance

Plastics

Biomedical

Functional

Materials

Specialty Coating

Resins

DSM’s capability to extract value

Mark

et

gro

wth

Solar

Dyneema® Life

Protection

Growth

Accelerated

growth

Powder

Coating Resins

PA6

Polymers

PA6

Compounds

- DSM Engineering Plastics

- DSM Dyneema

- DSM Resins & Functional Materials

- Emerging Business Areas

High

Maximize

returnsDyneema®

Fiber Solutions

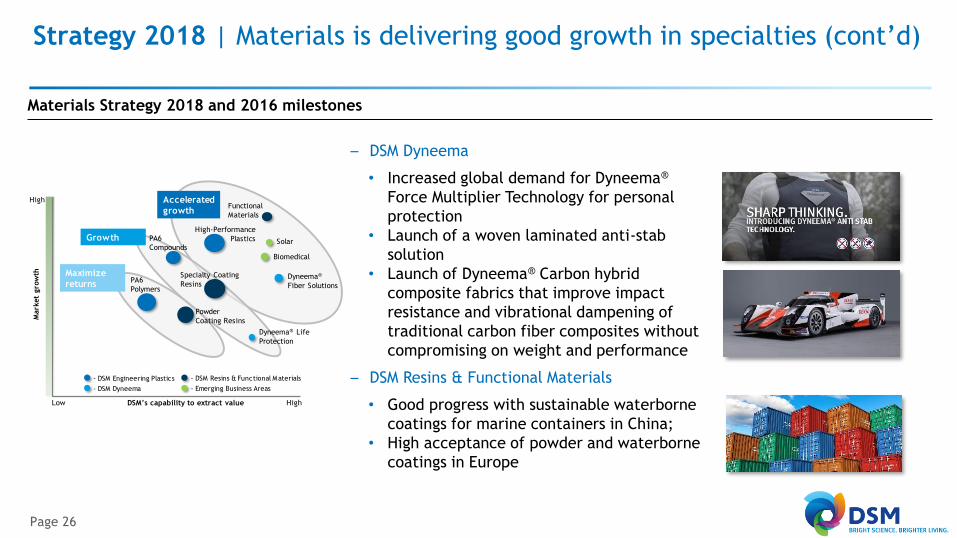

Strategy 2018 | Materials is delivering good growth in specialties

Page 25

▪ For DSM’s specialty materials, DSM is using new

technologies and (sustainable) customer solutions

to accelerate growth:

– DSM Engineering Plastics

• Used in new ultra-thin USB Type-C

connectors

• Launch of next-generation high-

temperature polyamides

• New high-performance thermoplastic

copolyester

2016

▪ Volume growth: 4%

▪ EBITDA growth: 13.3%

▪ ROCE up 320 bps

Materials Strategy 2018 and 2016 milestones

ForTii®

PA6, PA66

PA410

PA46

PPS

PA4T

High Low

High-Performance

Plastics

Biomedical

Functional

Materials

Specialty Coating

Resins

DSM’s capability to extract value

Mark

et

gro

wth

Solar

Dyneema® Life

Protection

Growth

Accelerated

growth

Powder

Coating Resins

PA6

Polymers

PA6

Compounds

- DSM Engineering Plastics

- DSM Dyneema

- DSM Resins & Functional Materials

- Emerging Business Areas

High

Maximize

returnsDyneema®

Fiber Solutions

Strategy 2018 | Materials is delivering good growth in specialties (cont’d)

Page 26

Materials Strategy 2018 and 2016 milestones

– DSM Dyneema

• Increased global demand for Dyneema®

Force Multiplier Technology for personal

protection

• Launch of a woven laminated anti-stab

solution

• Launch of Dyneema® Carbon hybrid

composite fabrics that improve impact

resistance and vibrational dampening of

traditional carbon fiber composites without

compromising on weight and performance

– DSM Resins & Functional Materials

• Good progress with sustainable waterborne

coatings for marine containers in China;

• High acceptance of powder and waterborne

coatings in Europe

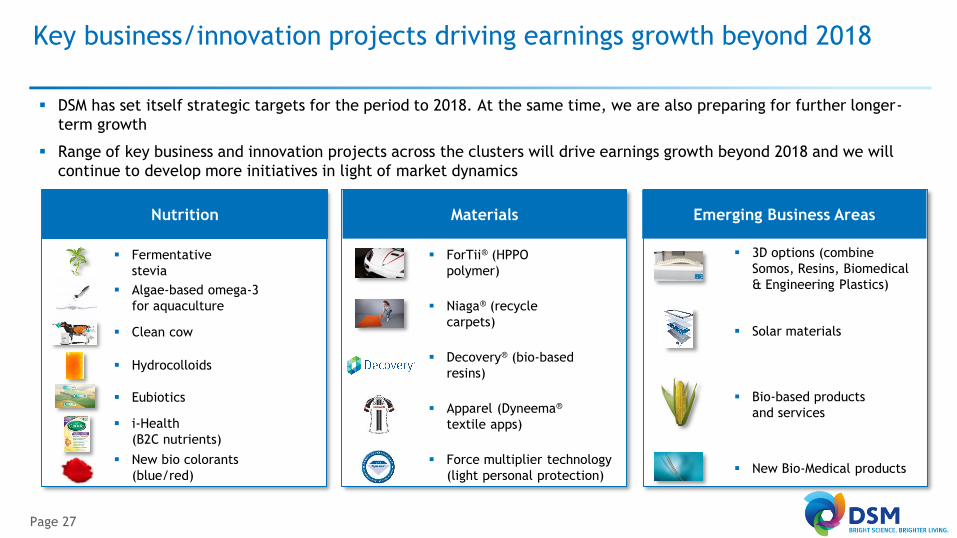

Key business/innovation projects driving earnings growth beyond 2018

Page 27

▪ DSM has set itself strategic targets for the period to 2018. At the same time, we are also preparing for further longer-

term growth

▪ Range of key business and innovation projects across the clusters will drive earnings growth beyond 2018 and we will

continue to develop more initiatives in light of market dynamics

Nutrition Emerging Business AreasMaterials

▪ Force multiplier technology

(light personal protection)▪ New Bio-Medical products

▪ Fermentative

stevia

▪ Algae-based omega-3

for aquaculture

▪ Clean cow

▪ New bio colorants

(blue/red)

▪ i-Health

(B2C nutrients)

▪ Eubiotics

▪ Hydrocolloids

▪ ForTii® (HPPO

polymer)

▪ Niaga® (recycle

carpets)

▪ Decovery® (bio-based

resins)

▪ Apparel (Dyneema®

textile apps)

▪ 3D options (combine

Somos, Resins, Biomedical

& Engineering Plastics)

▪ Solar materials

▪ Bio-based products

and services

Strategy 2018 | Driving profitable growth supported by cost reduction

and efficiency improvement programs

Page 28

▪ DSM is rigorously executing its ambitious cost reduction and efficiency improvement programs across the company

▪ Cost reduction/efficiency improvement programs target overall savings of €250-300m by 2018

▪ The plans are firmly on track by end of 2016

Cost savings: total €250-300m by 2018 Timing of cumulative cost savings

~€m

~25

~110

0

100

200

300

400

2015 2016 2017 2018

Realized Forecast

DSM-wide

support

functions

€125-150m(by end 2017)

Nutrition

Program

€130-150m(by 2018)

Materials

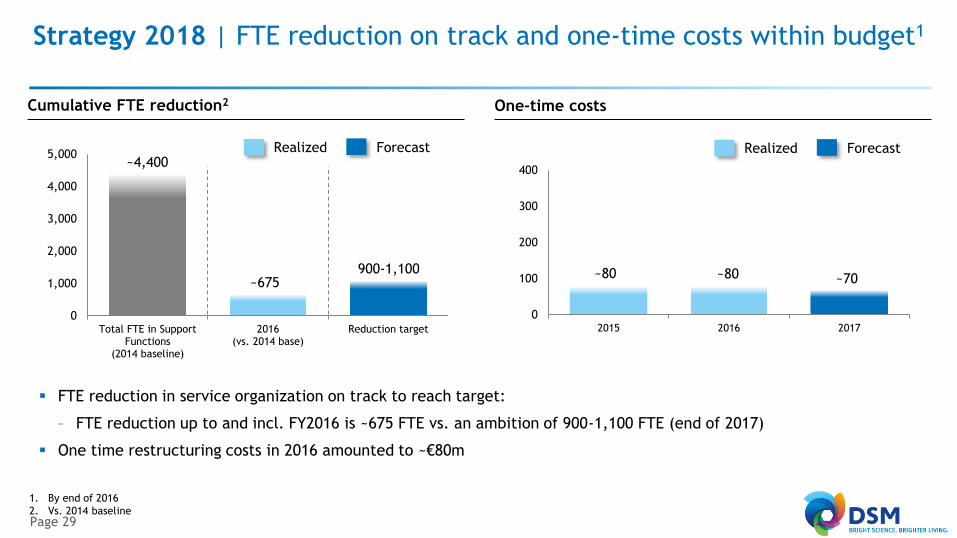

Strategy 2018 | FTE reduction on track and one-time costs within budget1

Page 29

1. By end of 2016

2. Vs. 2014 baseline

▪ FTE reduction in service organization on track to reach target:

– FTE reduction up to and incl. FY2016 is ~675 FTE vs. an ambition of 900-1,100 FTE (end of 2017)

▪ One time restructuring costs in 2016 amounted to ~€80m

0

100

200

300

400

2015 2016 2017

Realized Forecast

~80 ~70

0

1,000

2,000

3,000

4,000

5,000

Total FTE in SupportFunctions

(2014 baseline)

2016(vs. 2014 base)

Reduction target

~4,400

900-1,100~675

~80

Realized Forecast

Cumulative FTE reduction2 One-time costs

Strategy 2018 | Strong progress made with globally leveraging support

functions, saving DSM-wide support functions & staff costs

Page 30

1. Vs. 2014 baseline

2. By end of 2016

Savings: €125-150m1

Support

Funct.

Regions

Funct.

Excell.

▪ Shared Services Improvement Plan completed, incl. shift of most activities to Global Service Centre in

India

▪ Finance Regions (EMEA, North America, Asia) staffed and operational in Financial, Commercial &

Operations Control

▪ Shared Services operational and payroll outsourced

▪ Updated processes and tools for talent development, career review, recruitment, learning & development

▪ IT Operating Model defined and related FTE reductions announced, implementation has started

▪ Standardization/outsourcing of personal workplaces and other saving initiatives realized

▪ Supplier base rationalization, FTE reduction and related savings in external spend progressing well

▪ Global external & internal Communications function fully operational across regions and business groups

▪ Supplier rationalization in (Marketing-)Communications progressing well

▪ One Shared Services Organization with Global Delivery Centre in India and satellite in China live

▪ One multi-functional Service Desk and Portal in development

▪ Operating Models implemented (FTE reduction of ~40%); good progress in implementing new mandates

▪ Regional organizations brought in line with new DSM Operating Model; Finance, HR implementing Functional Operating Models

65 35Finance

85 15HR

50 50IT

75 25Ind. Sourcing

85 15Comms

30 70Shared Services

RemarksProgress (%)2 Achieved by end of 2016 Remaining 2017/ Run Rate EoY

Strategy 2018 | Nutrition-specific improvement program running well

with purchasing savings ahead of plan and cost-reductions on track

Page 31

1. Vs. 2015

Savings: €130-150m1

Cost improvements Work streams closely monitored and on track

Purchasing

Fixed cost

reduction

(~100 FTE)

Throughput gain in sold-out units

Efficiency

gains

(Yield &

Energy)

Purchasing ▪ Purchasing savings so far

exceeding target, helped by low

commodity prices

Fixed cost

reduction

▪ Cost reduction programs are

being executed. Remaining part

will be captured in the upcoming

period

Throughput

gains

▪ Program on track, planned

benefits end of 2016 realized.

Target gains are expected to be

secured

Efficiency

gains

▪ Program on track, planned

benefits end of 2016 realized.

Target gains are expected to be

secured

Actions Financial benefitsCurrent status as per end of 2016:

Strategy 2018 | Disciplined approach to capital allocation

Page 32

1. 2014 figure added for comparison only: based on non-audited, restated estimates adjusting for divestitures, acquisitions and other non-recurring items

▪ Capital efficiency is a key driver of cash generation; in 2016 we undertook a number of improvement projects in this

area throughout DSM

– One of these has been to take a more integrated approach to business planning, in particular in our Nutrition cluster

– Holistically addressing processes instead of approaching them as a series of individual steps has resulted in clear

improvements in inventory management, production and distribution efficiencies.

Driving financial performance

1,018

800

663

201620152014

▪ Cash from operating activities up 27%

2016

18.6%

2015

20.7%

2014

▪ Average Total Working Capital better

than aspiration level <20%

▪ Cash capex at €475m below

€500-550m per annum guidance

475

20162015

536

2014

628

Reducing working capital1 Strict capital allocation

Discontinued operations

Strategy 2018 | Organization adjustments to deliver

Page 33

▪ A new -strengthened- top structure:

Executive Committee aligns finance, business, innovation, strategy

& people, enabling faster strategic alignment & operational

execution

▪ A new operating model:

Business Groups: focus on M&S, Operations, Sourcing, R&D

Support Functions: globally leveraged: Finance, HR, Legal,

Comms, IT, Business Services & Corporate

Departments

▪ A new way of working:

Focus on Accountability (delivering) and Collaboration

(trust/speed)

Examples: reduction internal meetings, reducing demand,

increased speed, feedback loops, clearer expectations and

engagement with more skills, supported by incentives

HEALTH NUTRITION MATERIALS

ROYAL DSM

DSM at a glance/Strategy 2018

Business overview

Financial data

Share-related information

1

2

3

4

HEALTH NUTRITION MATERIALS

ROYAL DSM

Nutrition

Nutrition | A unique, global and broad portfolio in food/feed nutritional

ingredients with increased solutions offering capabilities

Page 36

▪ Global leader in nutrition, with broadest portfolio of

specialty nutritional ingredients

▪ DSM serves the global industries for animal feed, food and

beverages, pharmaceuticals, infant nutrition, dietary

supplements and personal care

▪ DSM is uniquely positioned in all steps of the feed and food

value chains: the production of pure active ingredients, their

incorporation into sophisticated forms, and the provision of

tailored premixes and forward solutions

Sales by end-market (%)

Sales by region (%)

Nutrition - Overview

4%

25%

18%22%

31%

10%

35%

46%

7%1%

Human Nutrition & Health

Food Specialties

Animal Nutrition & Health

Personal Care & Aroma Ingredients

Other

Sales | €5,169m

Sales | €5,169m

Rest of the World

Asia

North America

Europe

Latin America

Nutrition | 2016 key financial data (continuing operations)1

Page 37

1. 2012-13 figures added for comparison only. Figures are based on non-audited, restated estimates adjusting for divestitures, acquisitions and other non-

recurring items

Sales and organic sales growth (%) Adj. EBITDA & Adj. EBITDA margin (%)

ROCE (%) Capital employed (at 31 Dec.)

Adj. EBIT & Adj. EBIT margin (%)

Capital expenditure (accounting)

5,1694,9634,335

201620132012 20152014

931822850

2015 20162012 20142013

19.6 16.6 18.0562

645

535596

2013 20162012 20152014

13.7 10.8 12.5

12.010.3

12.5

20142013 20162012 2015

5,5375,3095,034

2015 20162012 20142013

331322330

20142013 20162012 2015

22 2222 1617

Nutrition | Broad portfolio is providing resilience with limited exposure to

single product lines or customers

Page 38

Sales split over value chain steps (%)Portfolio of ingredients (%)

Sales per customer (top 10)Profit contribution per product line (%)

Active ingredients

Forms

Premixes

i-Health/B2C

Fat soluble vitamins (e.g. A,D,E)

Water soluble vitamins (e.g. B,C)

Carotenoids

Marine PUFAs

Microbial PUFAs

Enzymes & cultures

Minerals & dicalcium phosphates

Savory / yeast extracts

Nutraceutical ingredients

Aroma intermediates

Other blend ingredients

Other

▪ Top-10 represent <50% of Nutrition

profit in 2016

▪ Product range includes ~100 product

lines

▪ Largest profit contributor less than

10% of Nutrition profit

▪ Several products have a strong IP

position

▪ Largest customer

represents less than 3%

of Nutrition sales

Nutrition | Product portfolio overview

Page 39

Value chain positioning

Active IngredientsForms/delivery

systems

Premix and

nutritional solutions

Feed,

Food,

Cosmetics,

Pharma

Retail/end

consumer

Raw

Materials

▪ Vitamins – Essential ingredients required for growth and well-being ranging from fat-soluble vitamins (A, D, E, K) to water-

soluble vitamins (C, all B vitamins, folic acid and pantothenic acid)

▪ Carotenoids – Essential ingredients that are important in nutrition and reproduction. Providing sufficient carotenoids

increases animal performance across species. Carotenoids also ensure consistent pigmentation of eggs and fish such as

salmon

– Key carotenoids are beta carotene, lutein, canthaxanthin, astaxanthin and zeaxanthin

▪ Nutritional Lipids – Polyunsaturated fatty acids (‘PUFAs’) play a critical role in the development and maintenance of proper

brain function, cardiovascular and eye health, immune and inflammatory responses and the production of hormone-like

molecules. Omega-3 and omega-6 are used in food, dietary supplements and infant nutrition and are manufactured from

algae, fungi as well as fish oil

▪ Enzymes & Cultures for food and feed – Adding enzymes to animal feed improves feed conversion leading to a reduction of

the cost of feed while at the same time improving the ecological impact of animal protein production by reducing the

amount of raw materials needed and by reducing pollutants in the manure. In food & beverage, enzymes and cultures

enhance taste, texture or act as processing aids functioning as a catalyst for biochemical reactions

Nutrition | Product portfolio overview (cont’d)

Page 40

Value chain positioning

Active IngredientsForms/delivery

systems

Premix and

nutritional solutions

Feed,

Food,

Cosmetics,

Pharma

Retail/end

consumer

Raw

Materials

▪ (Trace) minerals & Dicalcium Phosphates (DCP) – Minerals that are needed in very small amounts. As minerals they

come from soil and water and cannot be made by living organisms. Most of the trace elements in our diets come

directly from plants or indirectly from animal sources

▪ Savory/yeast extracts – Extracts and process flavors to enhance taste while reducing salt in snacks, ready-meals,

sauces, soups and meat

▪ Natural anti-microbials - Fermentation based anti-microbial solutions, effective to protect foodstuffs and beverages

from microbial spoilage, extending shelf life and improving flavor

▪ Nutraceutical ingredients – Deliver the optimal balance of microflora in the gastrointestinal tract of livestock animals

optimizing nutrient absorption, while in human nutrition, nutraceutical ingredients enable consumers to perform at

their peak, as well as helping cope with future health concerns such as cardiovascular disease and weight

management

▪ Aroma intermediates - Products of the highest purity and quality, from authentic foods packed with taste to aromatic

scents and perfumes

▪ UV-filters – Range of high performing UV-A and UV-B filters for skin and hair applications

▪ Skin Bio-actives – Range of vitamins, synthetic peptides and natural extracts for skin care markets

Nutrition | Product portfolio overview (cont’d)

Page 41

Value chain positioning

Active IngredientsForms/delivery

systems

Premix and

nutritional solutions

Feed,

Food,

Cosmetics,

Pharma

Retail/end

consumer

Raw

Materials

▪ A broad range of technologies transform the

active ingredients into a different state of

presentation, e.g. a fat-soluble vitamin oil

into a powder form

▪ Allows for maximum differentiation in terms

of stability, shelf-life, heat resistance, bio-

availability, physical properties

▪ Through customized blending of active

ingredients and/or forms, DSM offers its

clients regional and segment-specific

finished products solutions

▪ A broad network of around 60 premix plants

allows DSM to offer tailor-made, customer-

driven solutions, i.e. global products & local

solutions

Spray

dried

Multi-layer

micro

encapsulate

Beadlet Flavor

flake

Examples of forms

Nutrition | Global presence and unparalleled local network

Page 42

1. Excl. DSM(-wide) Research & Development locations

Unique global network1

HEALTH NUTRITION MATERIALS

ROYAL DSM

Animal Nutrition & Health

Animal Nutrition | DSM has the broadest portfolio in the industry

Page 44

Core

Vitamins

Carotenoids

Enzymes

Eubiotics

Premixes

Tortugaminerals

Provide antioxidants

& pigmentation

HEALTH

Required for growth

and well-being

PRODUCTIVITY

Improve digestion

Strengthen gut

health

Animal Nutrition | Focused on sustainable animal nutrition

Page 45

• Advocate science-based knowledge

about balanced diets; the right

amount and quality of proteins are

essential

• Improved end-product quality and

food safety

• Support small-scale farmers with

training and services

• Reduce use of scarce resources

• Reduce greenhouse gas

emissions from livestock

• Reduce food waste

• Capture the opportunities of new,

emerging technologies

• Combat antibiotic resistance

• Improved gut health

• Find and develop new sources of

protein and marine omega–3 oils

• Care for safe and controlled

production, including animal

welfare

• continuous drive to increase

animal health

Animal Nutrition | Serving global feed ingredients markets with local

solutions

Page 46

▪ Animal Nutrition & Health serves the global feed ingredients

markets for poultry, swine, aquaculture, ruminants and pets

with a focus on the nutritional ingredients and additives

segments (€2,399m in sales in 2016)

– These markets are spurred by population growth and rising

standards of living

▪ The global animal nutrition market is driven by the need to

improve production efficiency in response to the growing global

demand for animal protein while at the same time reducing the

environmental impact of farming

– This results in feed with higher nutritional content (i.e.

higher degree of nutritional ingredients)

▪ Increased focus on alternatives to antibiotic growth promoters

▪ Few global players in feed/premix and animal protein, next to

many mid-size, local and/or regional feed/premix companies

and animal protein producers

▪ DSM is uniquely positioned, offering a complete portfolio of

targeted feed ingredients, while competitors cover only part(s)

of the value chain

Global ingredients market for animal feed (%)

Amino Acids(4-6%)

Carotenoids(2-3%)

Water soluble vitamins(2-3%)

Fat soluble vitamins(4-6%)

Enzymes(5-6%)

Eubiotics4-5%)

Minerals & chelates(4-6%)

(x) = Growth rate 2015-18 (CAGR, %)

Total

potential

market:

€10bn

DSM active in colored parts with

market share of ~30%

Overview

Compound feed

Premix

Additives

Other

€350bn

(~2%)

€9bn (~4%)

€10bn (~4%)

€2bn (0.1%)

DSM is active in the ~€10bn

additives and ~€9bn premix

segments

~370bn (~2%)

Animal Nutrition | Value chain

Page 47

Compound feed - €198bn

Premix

Processors/farmers -

>€1,200bn

Specialty feed

additives

>€10bn

Feed ingredients

(soy, corn, etc.)

~€140bn

Nutrition serv.

& consultants

Medical feed

additives

>€10bn

Additives for pasture

raised animals

Chinese

players

Various

consultants

A full chain player, providing active ingredients globally and (tailored) premix solutions at a local level

Animal Nutrition | Overview

Page 48

Sales by active ingredients (%)Sales by region (%)

Sales by differentiated segment (%)Sales by application landscape (%)

Forms

Straight actives

Premix

Feed enzymes

Carotenoids

Water-soluble vitamins

Fat-soluble vitamins

Other

Other blending ingredients

Minerals/DCP

Pet

Aqua

Ruminant

Poultry

Swine

North America

Europe

Rest of the World

Asia

Latin America

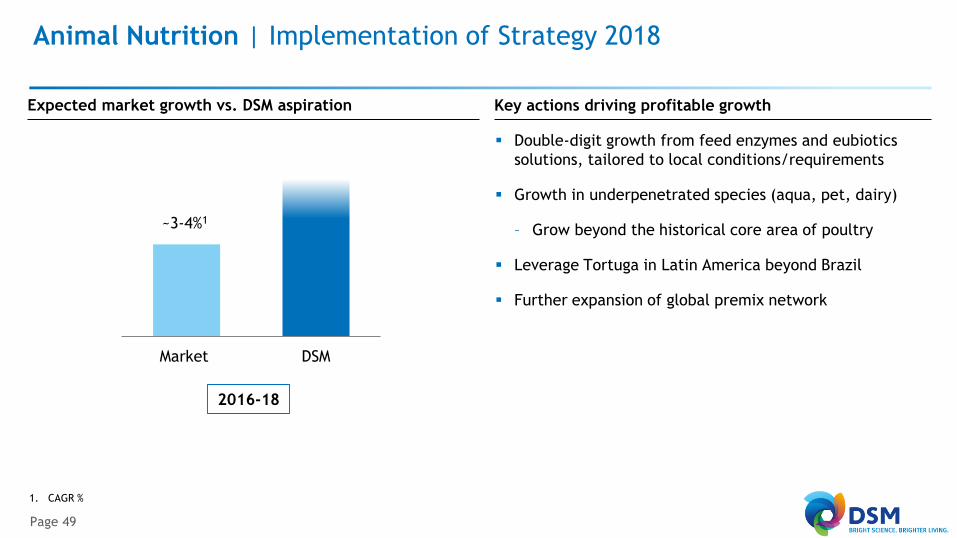

Animal Nutrition | Implementation of Strategy 2018

Page 49

1. CAGR %

▪ Double-digit growth from feed enzymes and eubiotics

solutions, tailored to local conditions/requirements

▪ Growth in underpenetrated species (aqua, pet, dairy)

– Grow beyond the historical core area of poultry

▪ Leverage Tortuga in Latin America beyond Brazil

▪ Further expansion of global premix network

Key actions driving profitable growthExpected market growth vs. DSM aspiration

2016-18

Market DSM

~3-4%1

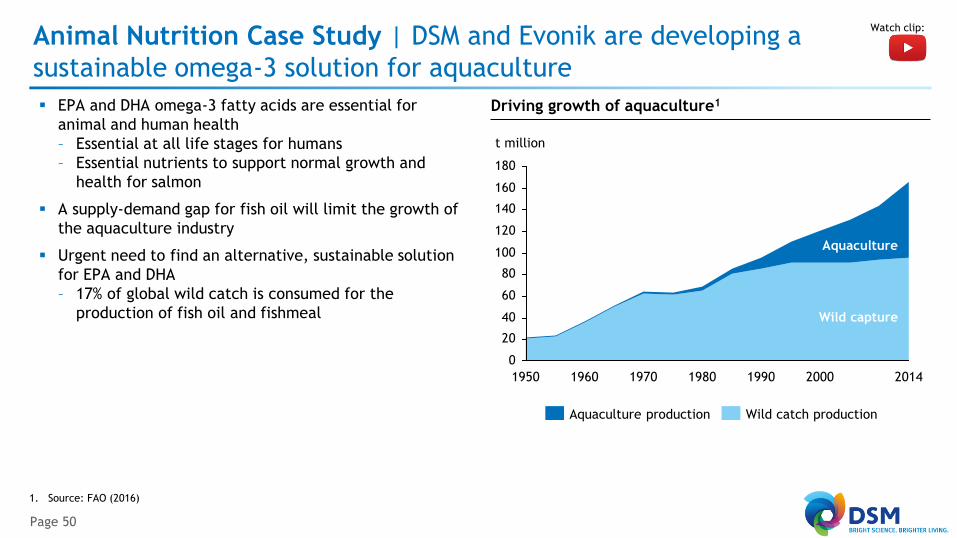

Animal Nutrition Case Study | DSM and Evonik are developing a

sustainable omega-3 solution for aquaculture

Page 50

1. Source: FAO (2016)

▪ EPA and DHA omega-3 fatty acids are essential for

animal and human health

– Essential at all life stages for humans

– Essential nutrients to support normal growth and

health for salmon

▪ A supply-demand gap for fish oil will limit the growth of

the aquaculture industry

▪ Urgent need to find an alternative, sustainable solution

for EPA and DHA

– 17% of global wild catch is consumed for the

production of fish oil and fishmeal

Driving growth of aquaculture1

0

20

40

60

80

100

120

140

160

180

1970 19901950 19801960 2000 2014

Wild capture

Aquaculture

t million

Wild catch productionAquaculture production

Watch clip:

Animal Nutrition Case Study | Algal oil as a high-quality source of

omega 3 for the use in animal nutrition

Page 51

1. Sources: IFFO, FAO

▪ Joint development between DSM and Evonik started in

2015 to find a sustainable solution for aquaculture

– Produce omega-3 fatty acids for animal nutrition

without using fish oil from wild-caught fish

▪ In March 2017, parties announced their intention to

jointly (50/50) produce omega-3 fatty acids (EPA and

DHA) from natural marine algae:

– Build new facility in the US, scheduled to open in

2019

– Total capex in the facility will amount to ~$200m

▪ Initial annual production capacity will meet ~15% of

total current annual demand for EPA and DHA by the

salmon aquaculture industry

Market size of fish oil and alternatives

Volu

me

present future

Supply/demand gap

will emerge in the

near future

Approx. 1 million tons per

year limited supply of fish oil

as source of omega-3 fatty

acids

Animal Nutrition Case Study | Project Clean Cow - Tackling methane

emissions from cows

Page 52

1. Source: S. Kirschke et al., Nature Geosci. 2013, 6, 813-823

▪ Ruminants are a significant source of methane

– Studies have shown that a cow emits 500l of methane

per day, which is equivalent to 10% of the energy it

would otherwise use for performance and milk

production

▪ Within Project Clean Cow, a special feed solution has

been developed that:

– Reduces enteric methane emissions from cow/cattle by

at least 30% (indicated by published studies)

▪ Focused on markets with highly developed dairy and beef

production

▪ Potential: triple-digit sales (€ million)

▪ Launch after 2018

Anthropogenic methane sources (%)1

Rice fields 10%

Ruminants27%

Biomass burning &

biofuel11%

Waste decomposition

23%

Fossil fuels29%

Watch clip:

HEALTH NUTRITION MATERIALS

ROYAL DSM

Human Nutrition & Health

Human Nutrition | Providing local nutritional solutions on a global scale

Page 54

1. Total specialty food ingredients market, excluding ~€20bn of commodity ingredients, e.g., soy proteins

▪ Human Nutrition & Health provides (local) nutritional solutions

for the food and beverage, dietary supplements and early-life

and clinical nutrition markets, with a parallel focus on

solutions for the pharmaceutical industry for the use of

vitamins, nutritional lipids (ARA/EPA/DHA) and carotenoids as

Active Pharmaceutical Ingredients (APIs) (€1,823m in sales in

2016)

▪ Fundamental growth driver for DSM is the link between

nutrition & health, supported by a number of global

megatrends:

– Macro-economic: Nutritional ingredients/products with

health benefits for an aging population or local solutions for

processed foods for new customers in emerging economies;

– Behavioral trends: Nutritional solutions that lead to

healthier, safer and more sustainable foods that can be

customized to local taste and preference

– Structural trends: Reforming the retail landscape by creating

a shift to modern trade, by being the only integrated

premix, vitamin and nutraceutical manufacturer capable of

creating and delivering tailor-made formulations anywhere

Global specialty food ingredients market (%)Overview

(x) = Growth rate 2016-18 (CAGR, %)

Preservation (2%)

Processing aids(3%)

Nutritional ingredients

(3-4%)

Taste(4%)

Texture(4%)

Color(5%)

Total

potential

market:

€36bn1

Main segment is

Nutritional

Ingredients but

DSM is active in all

segments

DSM market

share in

Nutritional

Ingredients

~20%

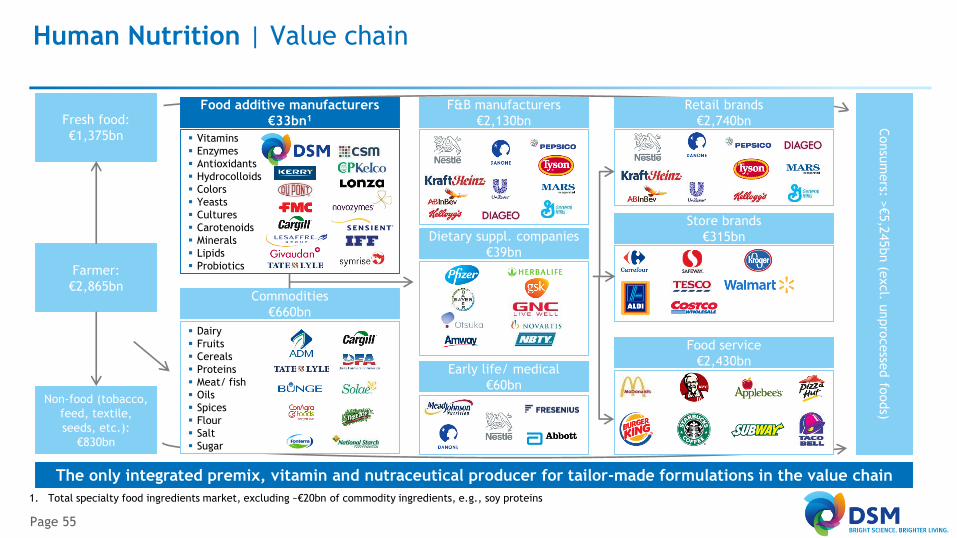

Human Nutrition | Value chain

Page 55

1. Total specialty food ingredients market, excluding ~€20bn of commodity ingredients, e.g., soy proteins

Fresh food:

€1,375bn

Farmer:

€2,865bn

Non-food (tobacco,

feed, textile,

seeds, etc.):

€830bn

▪ Vitamins

▪ Enzymes

▪ Antioxidants

▪ Hydrocolloids

▪ Colors

▪ Yeasts

▪ Cultures

▪ Carotenoids

▪ Minerals

▪ Lipids

▪ Probiotics

▪ Dairy

▪ Fruits

▪ Cereals

▪ Proteins

▪ Meat/ fish

▪ Oils

▪ Spices

▪ Flour

▪ Salt

▪ Sugar

Food additive manufacturers

€33bn1

Commodities

€660bn

F&B manufacturers

€2,130bn

Dietary suppl. companies

€39bn

Retail brands

€2,740bn

Store brands

€315bn

Food service

€2,430bn

Consu

mers: >

€5,2

45bn (e

xcl. u

npro

cesse

dfo

ods)

Early life/ medical

€60bn

The only integrated premix, vitamin and nutraceutical producer for tailor-made formulations in the value chain

Human Nutrition | Overview

Page 56

Sales by active ingredient (%)Sales by region (%)

Sales by differentiated segment (%)Sales by application landscape (%)

Other blend ingredients

Nutraceutical ingredients

Microbial PUFAs

Marine PUFAs

Carotenoids

Water-soluble vitamins (e.g. B,C)

Other

Fat-soluble vitamins (e.g. A,D,E)

B2C

Premix

Forms

Straight actives

Rest of the World

Asia

Latin America

North America

Europe

Food and Beverage

Dietary supplements

Infant

Human Nutrition | Implementation of Strategy 2018

Page 57

1. CAGR %

▪ From product to segment marketing with segment-

specific local solutions and an aligned front-end operating

model

▪ Repair growth in North America, returning Dietary

Supplements (vitamins, omega-3) and F&B to growth

▪ Continue double-digit growth of i-Health business

– Continue strong growth from base brands and expand

in category (e.g. bladder control, cough & cold, etc.)

and channels (e.g. medical, natural, digital, etc.)

▪ Accelerating forward solutions and premix globally

– Have stepped up our efforts to truly create a global

premix business with best in class systems and

processes

▪ Capture new business in nutritional ingredients for

Pharma, Clinical, and Sports Nutrition applications

Key actions driving profitable growthExpected market growth vs. DSM aspiration

2016-18

Market DSM

~3%1

Human Nutrition Case Study | Culturelle®, a probiotic megabrand

in the broader health and wellness space

Page 58

▪ The global dietary supplements probiotics market is

predicted to grow at around 7% per year (2015-19)

– New product innovation is helping to fuel this growth

▪ The market is highly segmented and extremely

competitive: product differentiation supported by

authenticated health claims is vital for success

▪ Culturelle® is currently the #1 selling consumer dietary

supplement probiotic brand in the US

▪ Top-line growth has been achieved by creating consumer

demand for Culturelle®

– Important to understand and validate consumers’

health and wellness needs

– Delivered on those needs across three growth

platforms (Digestive Health, Everyday Wellness, and

Kids) based around Lactobacillus GG − the leading

clinically-studied probiotic strain

– Positioned Culturelle® as the proven probiotic brand in

the broader health and wellness space.

Watch clip:

2013-2014 2015-2016

Culturelle Digestive

Health Ex. Strength

Providing growth

from more

committed loyal

consumer base

Culturelle Kids

Regularity

Expands Kids line

with new benefits

Culturelle Pro-Well

Expands probiotic

benefits to heart

health with Omega-

3s

Culturelle

Adult Chewables

New form

expands

consumer base

Human Nutrition Case Study | Focus now on global expansion and

footprint

Page 59

▪ Global expansion strategy focused on distribution and

consumer brand-building in Asia first and Europe later

– Different local market characteristics require new

routes to market

– Currently building expertise in these new segments

▪ Aggressive marketing support deployed to drive growth,

yet operation still in its infancy

– First signs of successful launch

▪ International marketing supporting ongoing bran-

building

HEALTH NUTRITION MATERIALS

ROYAL DSM

DSM Food Specialties

DSM Food Specialties | A leading global supplier of food enzymes,

cultures, yeast extracts, flavors and other specialties

Page 61

1. Total specialty food ingredients market, excluding ~€25bn of commodity ingredients, e.g., soy proteins

▪ DSM Food Specialties is a leading global supplier of food

enzymes, cultures, bio-preservation, hydrocolloids, taste and

health ingredients (€536m in sales in 2016)

▪ DSM helps make existing diets healthier and more sustainable,

giving increasing numbers of people access to affordable,

quality food – ‘enabling better food for everyone’ - driven by:

–

▪ Customer proximity and the ability to deliver highly tailored

products are the basis for our continually expanding portfolio

of innovative fermentation-based product solutions

Global food ingredients market (%)Overview

(x) = Growth rate 2016-18 (CAGR, %)

DSM’s main segments

in food specialty

ingredients include,

amongst others,

processing aides

(enzymes, cultures)

and taste (savoury)

DSM typically has

number 1-3

positions in the

segments where

active

Sugar, salt, fat reduction without compromise on taste &

mouthfeel Health

Convenience and taste are key purchase driversConvenience

and taste

Strong consumer demand for ‘kitchen cabinet’ ingredients,

removal of undesired chemicals, clean and clear labelsClean label

More and

faster

Rapidly growing world population, food production more

than 8 times more efficient since 1940

Diverse cultures, eating habits and taste/flavor preference,

localized solutions key despite globalisation

1bn new

consumers

Preservation (2%)

Processing aids(3%)

Nutritional ingredients

(Human Nutrition)

(3-4%)

Taste(4%)

Texture(4%)

Color(5%)

Total

potential

market:

€36bn1

DSM Food Specialties | Value chain

Page 62

1. Total specialty food ingredients market, excluding ~€25bn of commodity ingredients, e.g., soy proteins

▪ Enzymes

▪ Antioxidants

▪ Hydrocolloids

▪ Colors

▪ Cultures

▪ Flavors

▪ Dairy

▪ Fruits

▪ Cereals

▪ Proteins

▪ Meat/ fish

▪ Oils

▪ Spices

▪ Flour

▪ Salt

▪ Sugar

F&B manufacturers

€2,130bn

Retail brands

€2,740bn

Store brands

€315bn

Food service

€2,430bn

Consu

mers: >

€5,4

85bn (e

xcl. u

npro

cesse

dfo

ods)

Commodities

€790bn

Food additive

manufacturers

€36bn1

Playing a pivotal role in the value chain offering healthier solutions that enhance taste and texture

DSM Food Specialties | Enabling better food through advanced

fermentation and biotechnology

Page 63

Sugar Reduction

Digestive Health

Taste Experience

Food Chain Efficiency

Bio Preservation

BIOTECHNOLOGY & FERMENTATION

DairyBrewing

Baking

Beverages

Savory

Watch clip:

DSM Food Specialties | Technology plays a key role in finding solutions

Page 64

▪ Biotechnology in

food

development

▪ Efficiency in

traditional food

production

systems, e.g.

robotics

▪ Innovative

production

methods, e.g.

urban farming

▪ Disruptive

production

methods, e.g. 3D

printing

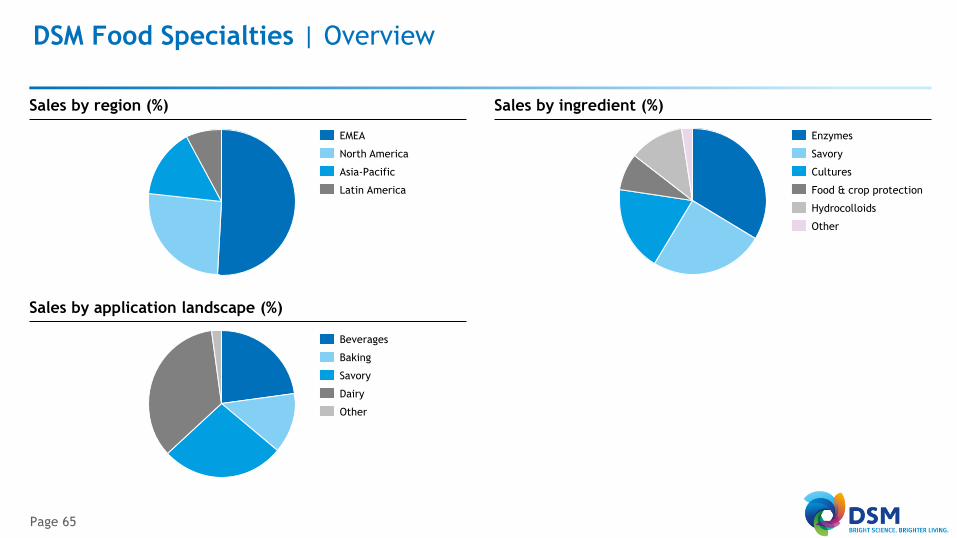

DSM Food Specialties | Overview

Page 65

Sales by ingredient (%)Sales by region (%)

Sales by application landscape (%)

Latin America

North America

EMEA

Asia-Pacific

Hydrocolloids

Cultures

Other

Food & crop protection

Enzymes

Savory

Savory

Other

Baking

Dairy

Beverages

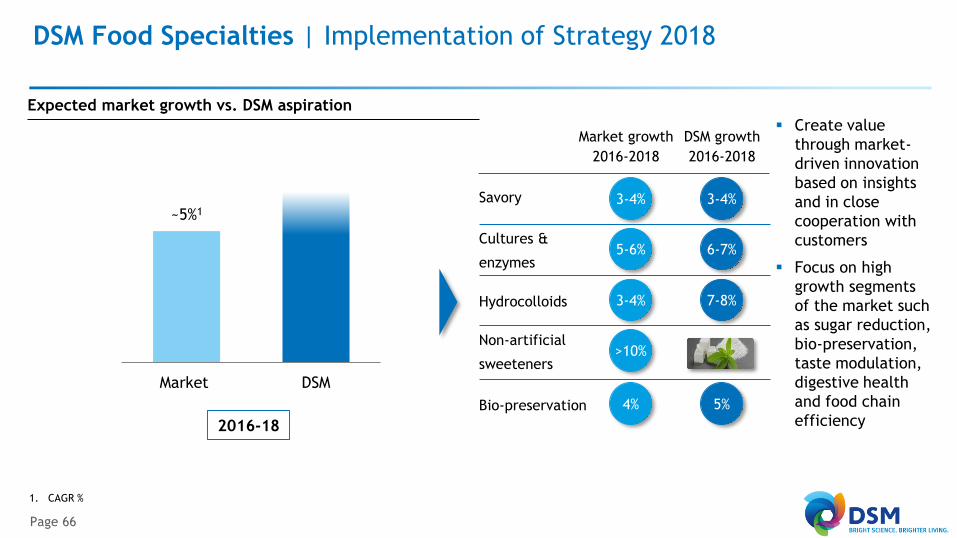

DSM Food Specialties | Implementation of Strategy 2018

Page 66

1. CAGR %

Expected market growth vs. DSM aspiration

2016-18

Market DSM

~5%1

Savory

Market growth

2016-2018

DSM growth

2016-2018

3-4%

5-6%

3-4%

>10%

3-4%

6-7%

7-8%

Cultures &

enzymes

Hydrocolloids

Non-artificial

sweeteners

▪ Create value

through market-

driven innovation

based on insights

and in close

cooperation with

customers

▪ Focus on high

growth segments

of the market such

as sugar reduction,

bio-preservation,

taste modulation,

digestive health

and food chain

efficiency4% 5%Bio-preservation

DSM Food Specialties Case Study | Consumers and governments globally

moving away from sugar

Page 67

DSM Food Specialties Case Study | Sugar reduction offers big opportunity

for fermentative stevia

Page 68

▪ Sugar is ~80% of current sweetener market

▪ Stevia is the only viable and large scale new alternative in

the foreseeable future

▪ Fermentative stevia is the future for:

– Sustainable production

– Several relevant sweetener molecules, e.g.:

• Reb A -Available in plants

• Reb M - The most potent rebaudioside, but availability

in plants is limited

• Potentially Reb D

▪ DSM has developed a unique cost effective technology to

produce Reb A and Reb M

▪ Development program for stevia well on track

– Regulatory submissions as well as FTO/IP work streams

ongoing

– Launch plans in close cooperation with major customers

– Commercial availability projected by end of 2018

DSM Food Specialties Case Study | Maxilact® offers dairy

producers opportunities for sugar reduction and digestibility

Page 69

▪ ‘Lactose-free’ and ‘no added sugar’ are two of the

fastest growing segments in dairy, driven by increasing

awareness of lactose-intolerance and health & wellness

▪ DSM was the first company to commercialize lactase and

has been innovating ever since

▪ DSM’s Maxilact® lactase breaks down lactose in dairy

products, making them suitable for lactose-intolerant

consumers

▪ Maxilact® meets the needs of lactose-intolerant

customers worldwide. Its natural sweetness also enables

dairy producers to achieve a 20 to 50% sugar reduction in

dairy products

Watch clip:

HEALTH NUTRITION MATERIALS

ROYAL DSM

Personal Care & Aroma Ingredients

Personal Care & Aroma Ingredients | Providing active, performance and

technical ingredients for cosmetic products

Page 71

▪ Personal Care & Aroma Ingredients provides innovative

solutions for some of the world’s best-selling beauty products

for sun, skin and hair care as well as aroma ingredients to the

flavor and fragrance industries which are used in many of the

world’s best-known consumer brands (€337m in sales in 2016)

▪ DSM’s extensive portfolio of key ingredients includes peptides,

natural bio-actives, UV filters, hair polymers, vitamins and

(specialty) aroma ingredients (such as lavender fragrance)

– The product portfolio is complemented by a unique range of

services in the areas of formulation expertise, sensory

competence, technical support, quality assurance, and

regulatory approval

▪ The business is driven by global megatrends, local consumer

beauty regime insights, and growth opportunities presented by

emerging markets

Global personal care market (%)Overview

Total

potential

market

€11.5bn

Surfactants (0-1%)

▪ Fatty alcohols, FA sulphates/

ethoxylates/ ethersulphates,

betaines, amphoacetates, etc.

Technical ingredients (2-3%)

▪ (Co) emulsifiers, thickeners &

rheology control agents,

emollients, solubilizers, etc.

Performance ingredients (3-4%)

▪ Hair conditioning & styling

polymers, skin sensory modifiers &

enhancers, pigments & dyes

Active ingredients (3-6%)

▪ UV-filters, vitamins, skin care

actives (natural extracts,

synthetic peptides, biotech ingr.13%

21%

30%

35%

DSM

active in

colored

parts

(x) = Growth rate 2015-18 (CAGR, %)

Personal Care & Aroma Ingredients | Value chain

Page 72

Sele

cte

d S

pecia

lty

Ingre

die

nts

segm

ents

Technical

Ingredients

(€3.5bn)

Performance

Ingredients

(€2.5bn)

Active and UV

Ingredients

(€1.5bn)

Surfactants

(€4.0bn)

Base Chemicals

(€14.obn)

Chinese

players

Cosmetic brand companies

and Private Label

Consumer products value at

manufacturer level: €240bn

Fast Moving Consumer

Goods

Consumer products value at

manufacturer level: €380bn

Leading position in selected key ingredients for cosmetic companies

Personal Care & Aroma Ingredients | Overview

Page 73

Sales by region (%)

Sales by segment (%)

China

Asia Pacific excl. China

Latin America

North America

Europe

Aroma Ingredients

Skin

Vitamins

Sun

Other

Watch clip:

Personal Care & Aroma Ingredients | Aroma Ingredients provides

lavenders and ionones to the fragrance and flavor industry

Page 74

▪ The aroma ingredients portfolio consists of lavenders and

ionones that are sold to the world’s leading fragrance and

flavor companies

▪ Products find their use mainly in home and personal care

products fine fragrances as well as food in the food

industry

▪ DSM product range includes:

– Ionones

• Beta-Ionone

• Methyl-Ionone

• Irone

– Lavender

• Linelool

• Linalyl Acetate

• Tetrahydrolinalool

Overview of the fragrance and flavor industry (€m)

F&F ingredients

4.5bn

2.4

0.2

Musk

1.0

Benzoids

1.1

Terpenes

Synthetic Essential oil/natural

1,1bn

Terpenes

Pinene

Menthol

350

Citrus

Lavender &

Ionones

Personal Care & Aroma Ingredients Case Study | An innovative

inorganic UV filter suitable for a wide range of products

Page 75

▪ Titanium dioxide finds extensive applications in the personal

care sector, being used as a pigment, sunscreen and thickener

– Its high refractive index, strong UV light-absorbing

properties and resistance to discoloration under UV light

make this the fastest-growing technology segment in the UV

filters market

▪ DSM offers a unique grade of titanium dioxide: PARSOL® TX, an

inorganic UV filter with excellent formulation compatibility,

which makes it suitable for a wide range of product

applications

▪ PARSOL® TX became the first titanium dioxide UV filter to

comply with the amended EC Regulation on Cosmetic Products

– Speedy compliance with the amended EC regulation offered

us a significant competitive advantage, establishing

PARSOL® TX as the global number one product grade in

titanium dioxide technology

▪ As a direct result of our regulatory expertise and dedicated

customer support, sales of PARSOL® TX increased by 55% in

2016

Watch clip:

Personal Care & Aroma Ingredients Case Study | Revealing the power of

beautiful skin with responsible and natural ingredients

Page 76

▪ “Health and Wellness” societal trend encourages

customers and consumers to search for more sustainable

solutions in personal care

▪ ALPAFLOR® line is a pioneer in the organic market:

– Standardized high altitude organic cultivation

contributing to Alpine flora diversity

– Quality, efficacy, and traceability from seed to

bioactive

▪ Green production principles

– 100% renewable energy

– 40% water reduction

– No production of chemical waste

– Vegetable waste used in compost

– Extraction solvent recycled

▪ Focused on all major skin care applications

▪ Potential: triple-digit sales

HEALTH NUTRITION MATERIALS

ROYAL DSM

Materials

Materials | A high-quality portfolio focused on well-defined, higher-

growth specialty segments

Page 78

▪ The Materials cluster comprises DSM Engineering Plastics,

DSM Dyneema and DSM Resins & Functional Materials

▪ The cluster consists of a high-quality portfolio of specialty

materials serving global automotive, electrical & electronics,

building & construction, consumer goods, flexible food-

packaging, high-performance textiles and life protection

industries

▪ Key trend is substitution; customers are looking to replace

existing parts and materials with newer, more sustainable

alternatives

– Through its materials, DSM is a leading provider of these

sustainable innovations, meeting demands for greater

efficiency, safer materials and improved environmental

performance

Sales by region (%)

Sales by end-market (%)

Materials - Overview

Sales | €2,513m

Sales | €2,513m 1%

36%

21%

2%

40%Asia

Rest of the World

Latin America

Europe

North America

23%

17%

15%

18%

27% Automotive & Transport

Building & Construction

Other

(Food) Packaging

Electrics & Electronics

Materials | ‘Silent’ transformation of the Materials portfolio toward

higher-value, more sustainable specialty products continues

Page 79

1. Whilst not part of the cluster, the Emerging Business Areas of Biomedical and Advanced Surfaces are also related to Materials and represent promising

growth platforms for the longer term

High Low

High-Performance

Plastics

Biomedical1

Functional

Materials

Specialty Coating

Resins

DSM’s capability to extract value

Mark

et

gro

wth

Solar1

Dyneema® Life

Protection

Growth

Accelerated

growth

Powder

Coating Resins

PA6

Polymers

PA6

Compounds

- DSM Engineering Plastics

- DSM Dyneema

- DSM Resins & Functional Materials

- Emerging Business Areas

High

Maximize

returnsDyneema®

Fiber Solutions

Materials | Implementation of Strategy 2018

Page 80

1. CAGR %

DSM Engineering Plastics

▪ Highly specified application development for global

customers in high-performance plastics ‘winning’

segments

▪ Continue to grow by leveraging global footprint of

commercial and technical resources to lead the PA6 and

high-performance polyamides markets in innovative

growth

DSM Dyneema

▪ Development of new application segments and product

solutions in existing segments for Fiber Solutions

▪ Continue re-focus on growing Life Protection segment

DSM Resins & Functional Materials

▪ Grow customer base profiting from fiber-to-home trend

▪ Drive substitution from solvent to water and other

sustainable solutions in coatings

Key actions driving profitable growthExpected market growth vs. DSM aspiration

2016-18

Market DSM

~3-4%1

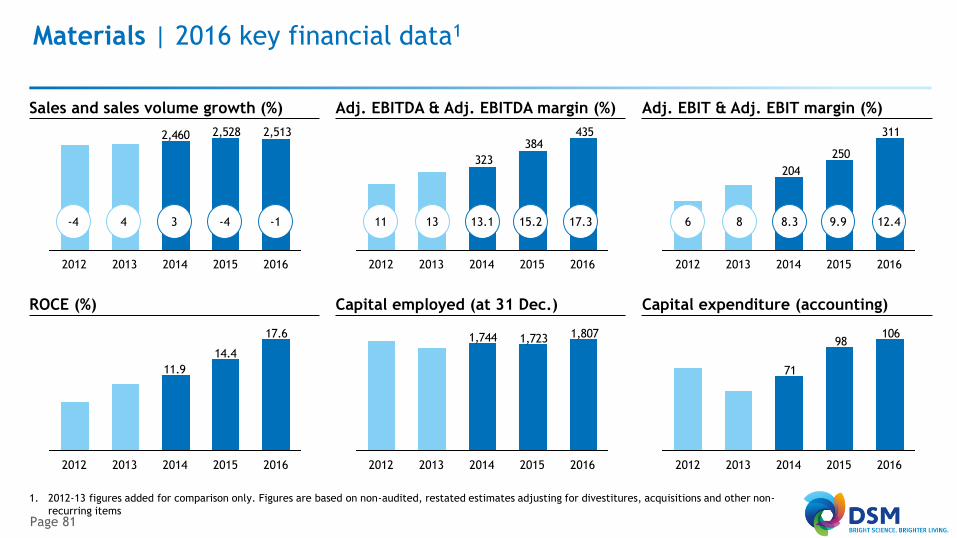

Materials | 2016 key financial data1

Page 81

1. 2012-13 figures added for comparison only. Figures are based on non-audited, restated estimates adjusting for divestitures, acquisitions and other non-

recurring items

Sales and sales volume growth (%) Adj. EBITDA & Adj. EBITDA margin (%)

ROCE (%) Capital employed (at 31 Dec.)

Adj. EBIT & Adj. EBIT margin (%)

Capital expenditure (accounting)

2,5132,5282,460

20162014 20152012 2013

435384

323

20142012 2013 2015 2016

15.2 17.3-1-4

311

250

204

2014 20152012 2013 2016

9.9 12.4

17.6

14.4

11.9

20132012 2014 2015 2016

1,8071,7231,744

20152012 2013 2014 2016

10698

71

20162012 2013 20152014

34-4 13.11311 8.386

Materials | End-market segments offer growth options enhanced by

substitution based on application development capabilities

Page 82

Automotive ElectronicsLife

Protection

Fiber

Solutions

Sustainable Coatings

Functional Materials

Replace metals &

hazardous materialsReplace steel/aluminum & aramids Environmentally friendly solutions

DSM Engineering Plastics1 DSM Dyneema DSM Resins & Functional Mat.DSM

Biomedical

Replace traditional

solutions

Regenerative

Biomaterials

DSM Advanced

Surfaces

Fossil fuel

replacement

Solar

Growth via end markets and substitution based on application development

Materials | Locations

Page 83

Global presence in R&D and production supporting preferred partnerships in winning segments

HEALTH NUTRITION MATERIALS

ROYAL DSM

DSM Engineering Plastics

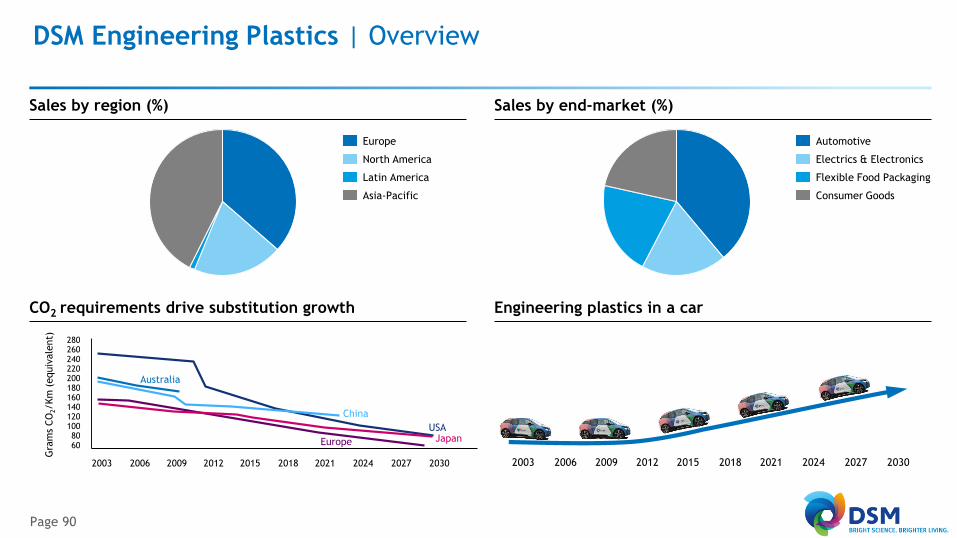

DSM Engineering Plastics | A global engineering plastics player with a

broad range of value-adding polyamides and polyesters

Page 85

▪ DSM Engineering Plastics is a global engineering plastics

player with a broad range of value-adding, high

performance polyamides and polyesters (€1,312m in sales

in 2016)

▪ DSM targets three key industries: automotive, electrical

and electronics and flexible food packaging:

– In automotive, focus is on lower fuel consumption and

emissions reduction via weight and friction reduction