energy market simulations under climate stabilization ... · pdf fileenergy market simulations...

TRANSCRIPT

Energy Market Simulations Under Climate Stabilization Transitions

Donald Hanson, Economist, ANLJon Marano, Energy ConsultantTito Homem-de-Mello, Northwestern UniversityInternational Association for Energy EconomicsJune 21-24, 2009

2

Energy/Climate Transitions Analysis

Modeling Important Joint Production Technologies– Pricing joint-production products– Conventional and unconventional crude oil refining; biomass- and

coal-to-liquids coproduction plants: MARS – coauthor JJMarano– Vehicle choice model (AMIGA), price effects, and modeling CAFE

standards– Biomass supply and allocation: FASOM

Importance of moving quickly on CCS demonstrations-Coal gasification projects with CO2 capture-Retrofitting existing coal-fired power plants

3

What We Learned from the EMF-22 Climate Transition Scenario Runs for the U.S.

The current baseline outlook appears consistent with the U.S. holding its CO2-eq emissions from 2012 to 2050 at a constant allowance path at 2008 levels (with flexible banking and borrowing). This represents 287bmt CO2-eq cumulative emissions.A 50% reduction by 2050 (203 bmt CO2-eq cumulative from 2012 to 2050) is doable with advanced technology deploymentAn 80% reduction by 2050 (167 bmt CO2-eq cumulative) is extremely difficult. Large amounts of new nuclear capacity and renewables have to be phased in by 2030 to reduce emissions accumulations from existing coal plant and to provide electricity for PHEVs to reduce petroleum useWhat can be done to reduce demand for motor gasoline blends, and especially faster growing diesel/jet fuel will be very importantDetailed technology modeling is necessary to formulate a balanced, complementary set of actions for energy/climate security

4

General Equilibrium in Fuels Markets and Product Pricing

Joint product prices are based on both costs and demand elasticities in the different product marketsIn AEO 2009, motor gasoline blends decrease 0.8% per year from 2007 to 2030, whereas distillate demand (jet fuel, diesel, DFO) grows at 1.0% per year.This gives rise to an increasing distillate to gasoline ratio, whereas refineries are limited in capability to change this production ratio.Diesel prices will rise relative to gasoline. Biodiesel and CTL will sell at a premium. Gasoline substitutes (ethanol) will be relatively less economic to produce.There will be major implications for crude oil imports and petroleum products imports and exportsDelayed participation of non-Annex1 countries in a climate agreement will affect location of future refining capacity away from the U.S. with a CO2 emission cap

5

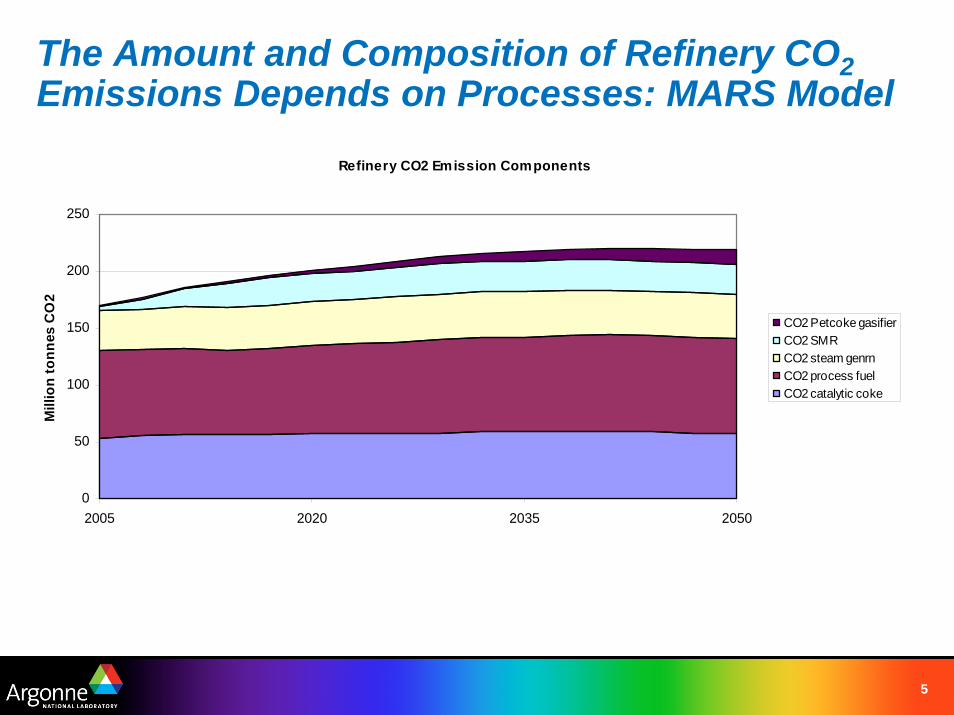

The Amount and Composition of Refinery CO2Emissions Depends on Processes: MARS Model

Refinery CO2 Emission Components

0

50

100

150

200

250

2005 2020 2035 2050

Mill

ion

tonn

es C

O2

CO2 Petcoke gasifierCO2 SMRCO2 steam genrnCO2 process fuelCO2 catalytic coke

6

Some Features of Our SystemU.S. focus and rest-of-world global focus

Bottom-up investment requirement calculations (capital scarce)– Energy technology capacity expansion– Transportation technologies– End use buildings and industry investments in energy efficiency

Average energy prices must be sufficient to sustain investment –economic condition for entry and investment by firms

John Marano’s work with NREL and EIA in characterizing current, next generation, and mature cellulosic biomass technologies, including pyrolysis

7

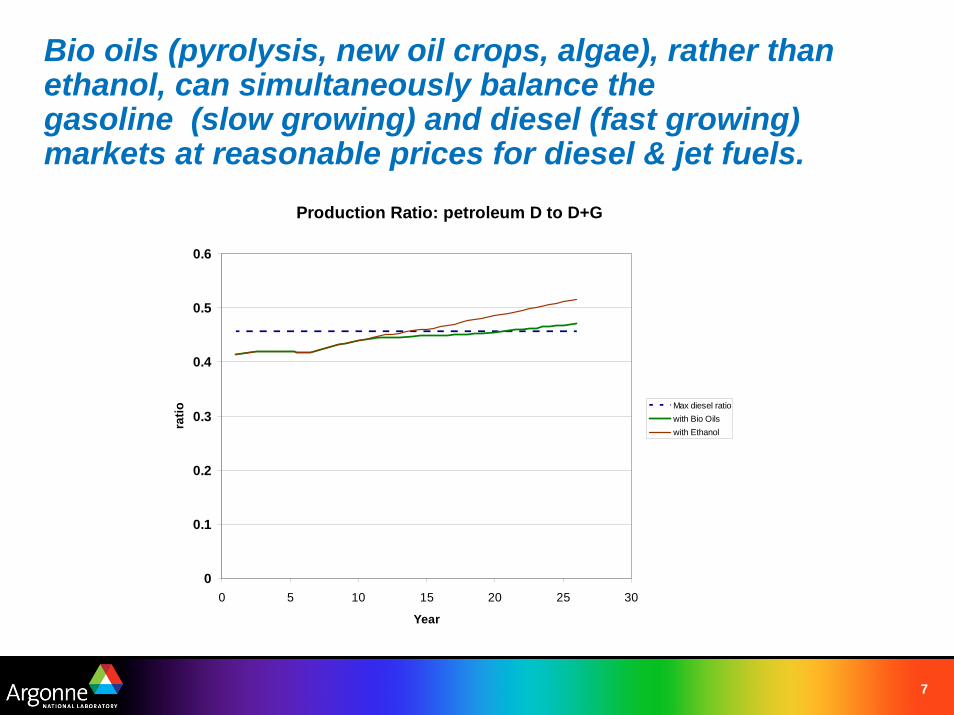

Bio oils (pyrolysis, new oil crops, algae), rather than ethanol, can simultaneously balance the gasoline (slow growing) and diesel (fast growing) markets at reasonable prices for diesel & jet fuels.

Production Ratio: petroleum D to D+G

0

0.1

0.2

0.3

0.4

0.5

0.6

0 5 10 15 20 25 30

Year

ratio

Max diesel ratiowith Bio Oilswith Ethanol

8

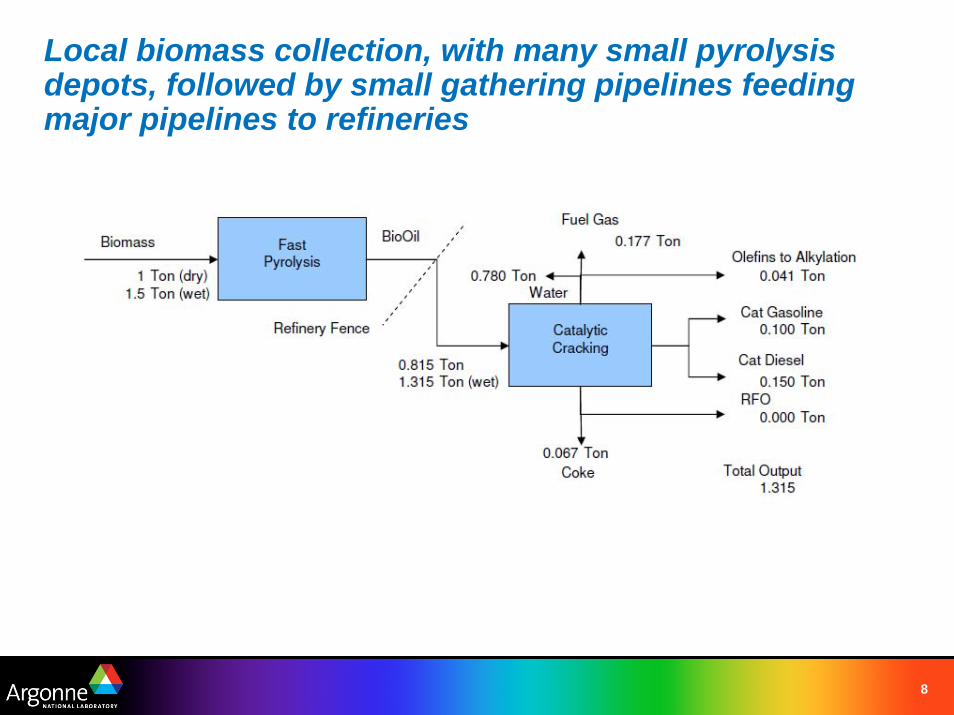

Local biomass collection, with many small pyrolysis depots, followed by small gathering pipelines feeding major pipelines to refineries

9

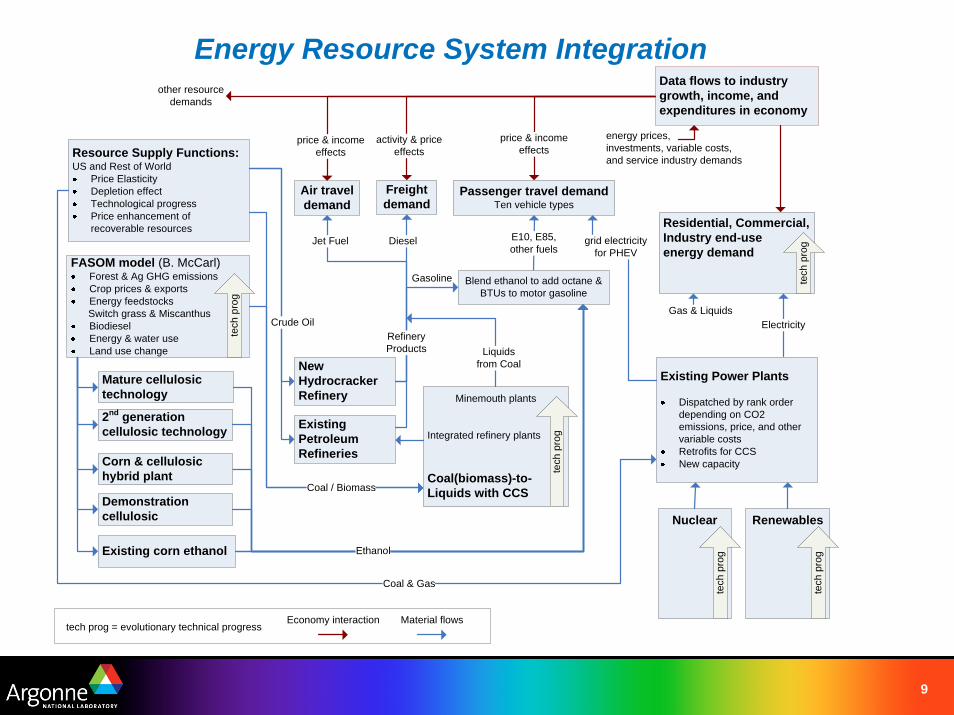

Energy Resource System Integration

Resource Supply Functions:US and Rest of World

Price ElasticityDepletion effectTechnological progressPrice enhancement of recoverable resources

FASOM model (B. McCarl)Forest & Ag GHG emissionsCrop prices & exportsEnergy feedstocks Switch grass & MiscanthusBiodieselEnergy & water useLand use change

Mature cellulosic technology

2nd generation cellulosic technology

Corn & cellulosic hybrid plant

Demonstration cellulosic

Existing corn ethanol

Air travel demand

Freight demand

Passenger travel demandTen vehicle types

New Hydrocracker Refinery

Existing Petroleum Refineries

Minemouth plants

Integrated refinery plants

Coal(biomass)-to-Liquids with CCS

tech

pro

g

Residential, Commercial, Industry end-use energy demand

Existing Power Plants

Dispatched by rank order depending on CO2 emissions, price, and other variable costs Retrofits for CCSNew capacity

Nuclear

tech

pro

g

Renewables

tech

pro

g

price & incomeeffects

activity & priceeffects

price & incomeeffects

E10, E85, other fuels

Blend ethanol to add octane & BTUs to motor gasoline

grid electricityfor PHEV

Crude Oil

Liquidsfrom Coal

DieselJet Fuel

Ethanol

Electricity

tech prog = evolutionary technical progress

Data flows to industry growth, income, and expenditures in economy

Gas & Liquids

Coal & Gas

tech

pro

g

tech

pro

g

RefineryProducts

Gasoline

Coal / Biomass

Economy interaction Material flows

energy prices, investments, variable costs,and service industry demands

other resourcedemands

10

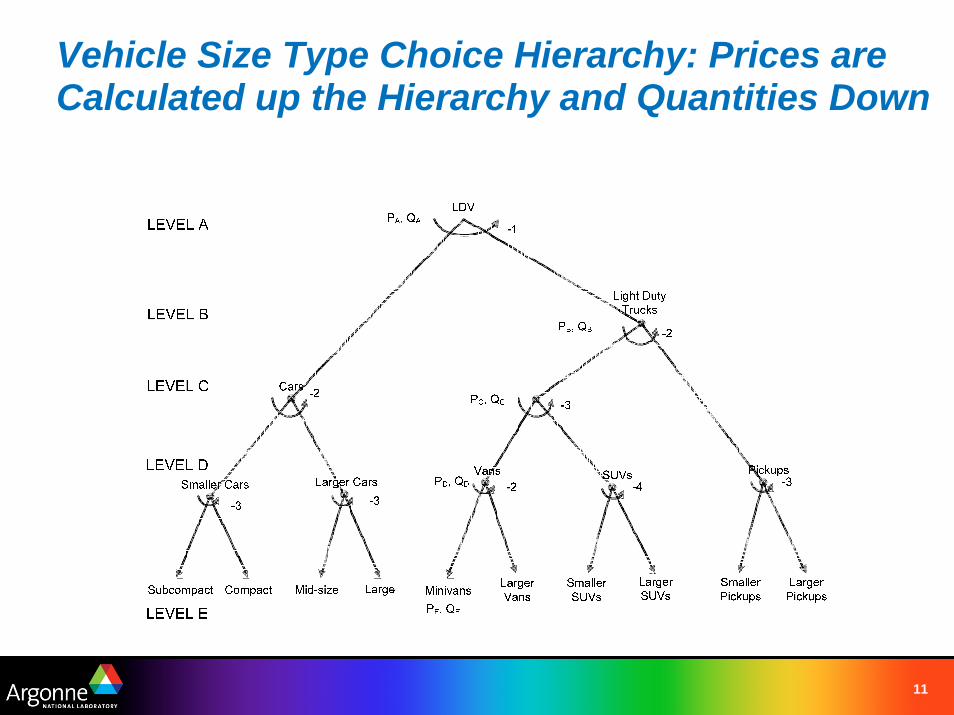

Dimensions along which Vehicle Markets Adjust. These Are Responses that we Model.

Substitution of capital (first cost of vehicle) for energy efficiency technologies (our data is based on Effectiveness and Impact of Corporate Average Fuel Economy Standards by David Greene et.al., NRC, 2002)Choice of more or less vehicle performance (income and price effects)Substitution among vehicle sizes (we model ten size types)Shift in household budget shares to other goods, services, and transportation modes away from personal vehicle-related expenditures (price effects)General changes in economic conditions (income effects)Driving existing vehicles more or less (price effects)Accelerating the rate of turnover to newer efficient vehicles

11

Vehicle Size Type Choice Hierarchy: Prices are Calculated up the Hierarchy and Quantities Down

12

Change in size categories for a doubling in gasoline price.

Pvehj = Cvehj + lambda*(GPMvehj – GPMavg)

13

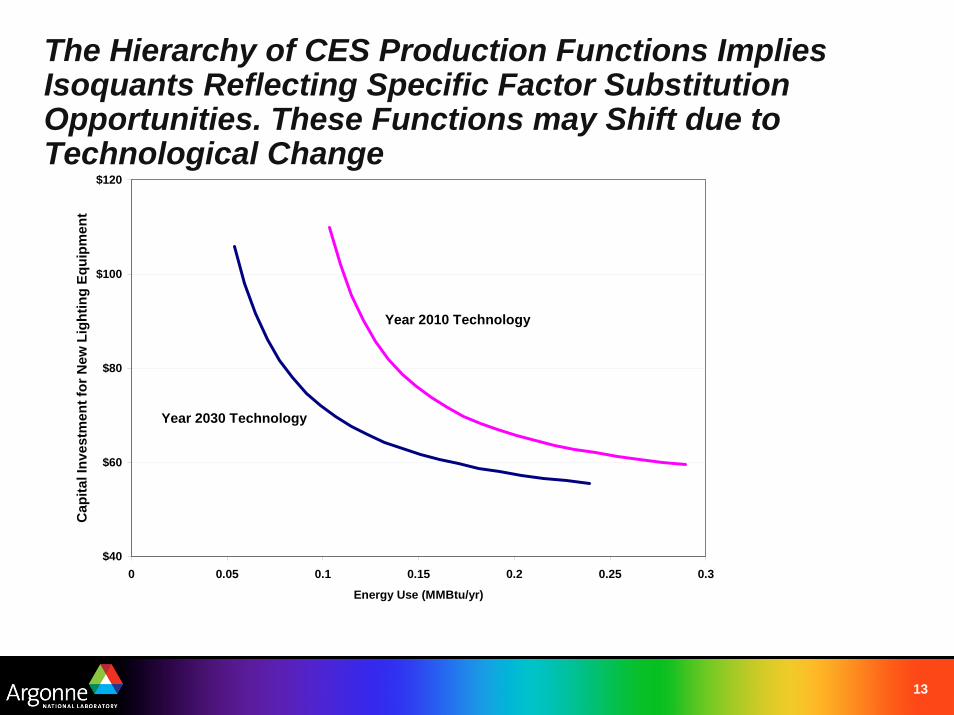

The Hierarchy of CES Production Functions Implies Isoquants Reflecting Specific Factor Substitution Opportunities. These Functions may Shift due to Technological Change

$40

$60

$80

$100

$120

0 0.05 0.1 0.15 0.2 0.25 0.3

Energy Use (MMBtu/yr)

Cap

ital I

nves

tmen

t for

New

Lig

htin

g Eq

uipm

ent

Year 2010 Technology

Year 2030 Technology

14

According to the National Academy’s Report, There Are Opportunities to Improve Both/Either Vehicle Efficiency and Performance (with strong price and income effects)

)/1,(0 yzeeffcyzyzyz MPGVehpricfPerform κ=

⎟⎟⎠

⎞⎜⎜⎝

⎛⋅⎟⎟⎠

⎞⎜⎜⎝

⎛=⎟⎟

⎠

⎞⎜⎜⎝

⎛hyz

hyz

he

tE

K

E

NVVMT

rP

ff

0

0,'

'

ζζζ

τω

1

/1−

−−

⎥⎥

⎦

⎤

⎢⎢

⎣

⎡

⎟⎟⎠

⎞⎜⎜⎝

⎛Φ+⎟

⎟⎠

⎞⎜⎜⎝

⎛Θ=

yz

yzyz

yz

eeffcyz

yzyz

MPGVehpricf

Isoquants move out with higher performance

ςς

ωτ

+

⎟⎟⎠

⎞⎜⎜⎝

⎛⋅⎟

⎟⎠

⎞⎜⎜⎝

⎛⋅⎟⎟⎠

⎞⎜⎜⎝

⎛

Θ

Φ=

1

'

'

/1 MPGVehpric

ff eeffc

yz

yz

yz

yz

yz

K

E

Mathematically the functions and optimal choice are described as follows:

15

Phasing-in Carbon prices

The optimal carbon price path is one which balances the risk of rapid or “built in” climate change with the cost advantage of postponing emission reduction measures. Environmental damages may be worsened by delay in mitigation.It can be shown that necessary conditions in optimal control theory imply that the efficient carbon price will grow at the difference in rates between the environmental time preference, “a,” for earlier emission reductions and the money time preference, “r”: dλ/dt = (r - a)λIf (r - a) were smaller, the Carbon Price path would be flatter.This might make sense from a technology cost/adoption perspective.Therefore, it is my conclusion that the phasing-in of an initial carbon price will be dictated by adjustment costs and political feasibility considerations, but should be ramped up as soon as is feasible.Future work: Monte Carlo sampling over uncertain parameters

16

Appendices

The AMIGA/MARS Integrated System

17

The Modeling System Integrates Energy Supply Systems and Environmental Emissions Within an Economy-wide Model

1818

MARS: Representation of Joint Production TechnologiesUS Coking RefineriesAtmospheric DistillationVacuum DistillationAtmospheric DesulfurizationDelayed CokerFischer-Tropsch liquids

upgradingGasoil HydrotreatingFluidized Catalytic CrackerGasoline DesulfurizationLo/Hi Severity Distillate HTKerosene hydrotreaterNaphtha hydrotreaterDehexanizerLow pressure reformerC6 isomerizationAlkylationC4 isomerizationsteam methane reformingSteam generation & CHP

Future US Hydrocracking RefineriesAtmospheric DistillationVacuum DistillationResid hydrocrackerGasoil hydrocrackerLo/Hi severity distillate HTKerosene hydrotreaterNaptha hydrotreaterDehexanizerLow pressure reformerC6 isomerizationSteam methane reformingSteam generation & CHP

Chemical processesGasifiactionPyrolysisFermentation

Biomass – current techBiomass – next generationBiomass – mature tech

LPGMotor GasolineJet FuelDiesel FuelDist. FOResid. FOPetro CokeAsphaltNathpha feedstockKerosene feedstockLubricants

Power Plant Biomass Co-firingConventional Markets

Rest of World - ExistingCracking Refineries

Rest of World - FutureHydrocracking Refineries

Ethanol and Biodiesel production from sugar, starch, and oil crops

US & Rest of World demand for products

Biomass & Coal based

Conventional & Unconventional Crude OilsProduct Imports/Exports

Future hydrocracking refinery locations

US Rest of World

Biomass Allocation

19

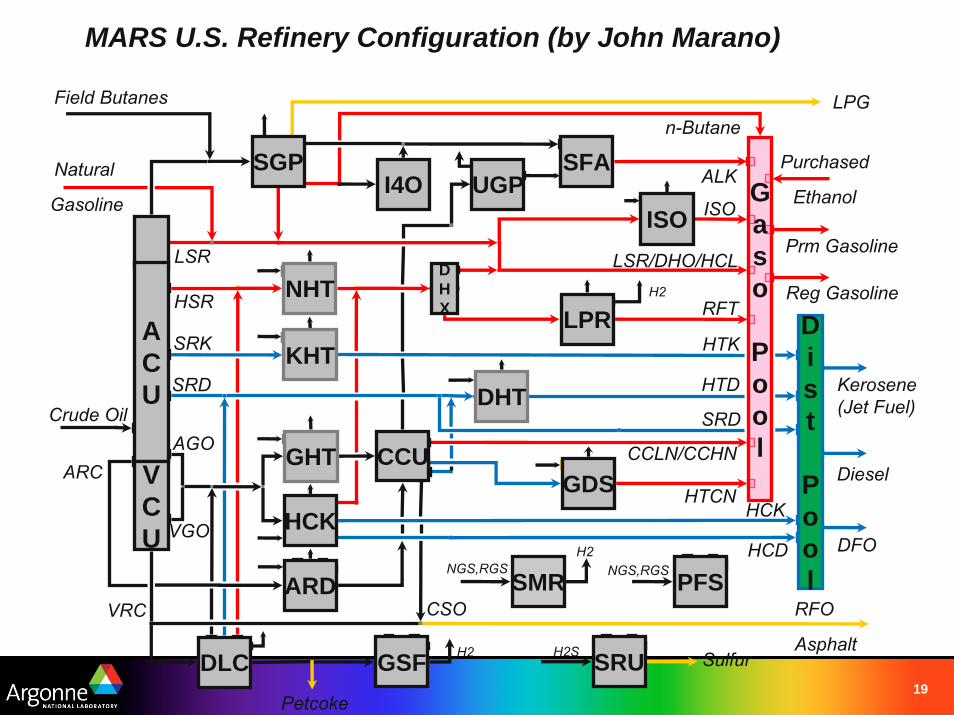

SMR

MARS U.S. Refinery Configuration (by John Marano)

Crude Oil

DLC

Prm Gasoline

Reg Gasoline

Field Butanes

Natural

Gasoline

Purchased

EthanolI4O

GSF

LPG

Kerosene(Jet Fuel)

DFO

Petcoke

RFO

Asphalt

Diesel

SRU

PFS

Sulfur

SGPUGP

SFA

Dist

Pool

ISO

NHTDHX

KHTACU

VCU

LPR

DHT

GHT

HCK

CCU

ARD

GDS

HSR

LSR

SRK

SRD

AGO

VGO

VRC

n-Butane

LSR/DHO/HCL

RFT

ISO

ALK

CCLN/CCHN

CSO

HTCN

HTK

SRD

HTD

HCK

HCD

H2

H2

H2

NGS,RGS

H2S

NGS,RGS

ARC

Gaso

Pool