energy outlook 2035_presentation

TRANSCRIPT

© BP p.l.c. 2015

17th

February 2015

BP Energy Outlook 2035

bp.com/energyoutlook

#BPstats

© BP p.l.c. 2015

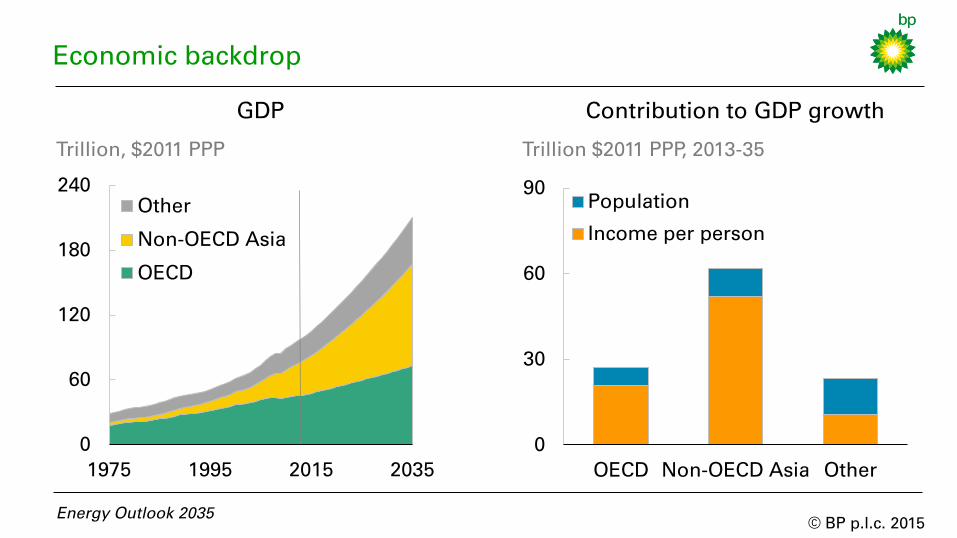

0

30

60

90

OECD Non-OECD Asia Other

Population

Income per person

0

60

120

180

240

1975 1995 2015 2035

Other

Non-OECD Asia

OECD

Trillion, $2011 PPP

GDP

Economic backdrop

Contribution to GDP growth

Energy Outlook 2035

Trillion $2011 PPP, 2013-35

© BP p.l.c. 2015

0%

2%

4%

6%

8%

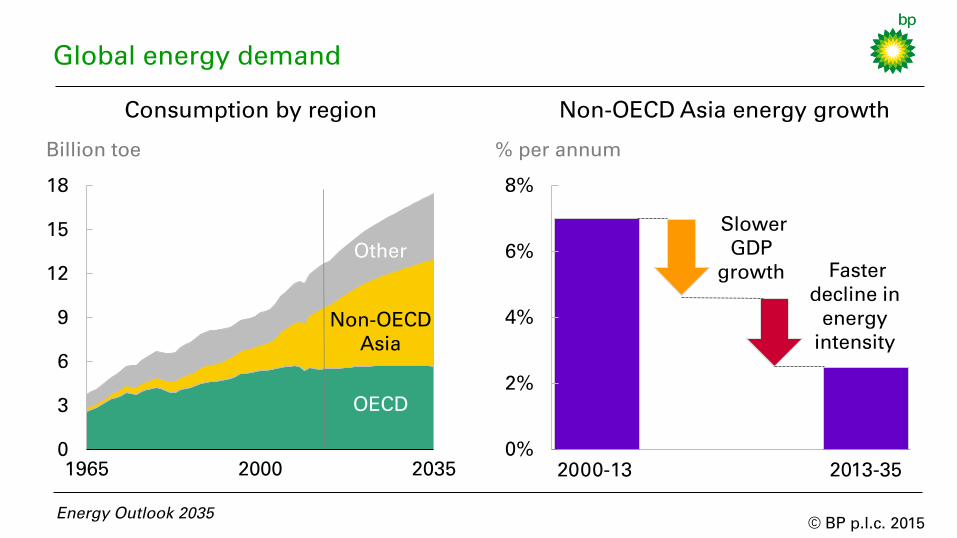

Global energy demand

Billion toe

Consumption by region

0

3

6

9

12

15

18

1965 2000 2035

Energy Outlook 2035

% per annum

Non-OECD Asia energy growth

2000-13

Slower

GDP

growth

2013-35

Faster

decline in

energy

intensity

Other

Non-OECD

Asia

OECD

© BP p.l.c. 2015

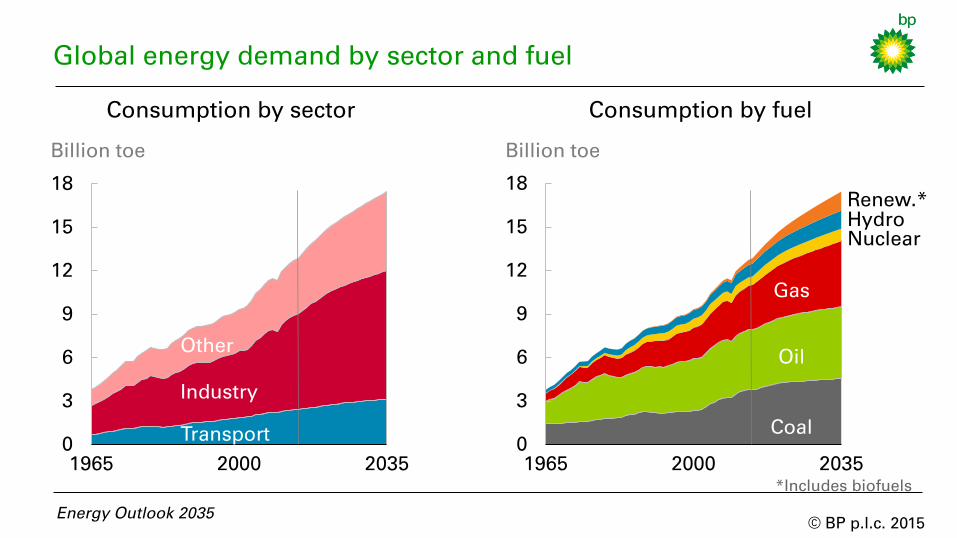

Global energy demand by sector and fuel

Energy Outlook 2035

Billion toe

Consumption by sector

Consumption by fuel

Billion toe

0

3

6

9

12

15

18

1965 2000 2035

Transport

Other

Industry

0

3

6

9

12

15

18

1965 2000 2035

Th

ou

sa

nd

s

Oil

Gas

Coal

Hydro

Nuclear

Renew.*

*Includes biofuels

© BP p.l.c. 2015

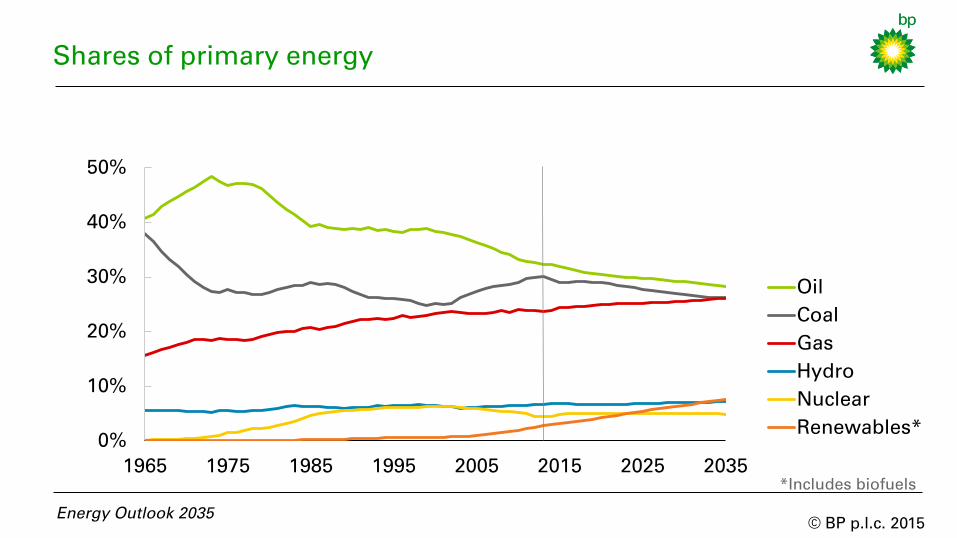

0%

10%

20%

30%

40%

50%

1965 1975 1985 1995 2005 2015 2025 2035

Oil

Coal

Gas

Hydro

Nuclear

Renewables*

Shares of primary energy

Energy Outlook 2035

*Includes biofuels

© BP p.l.c. 2015

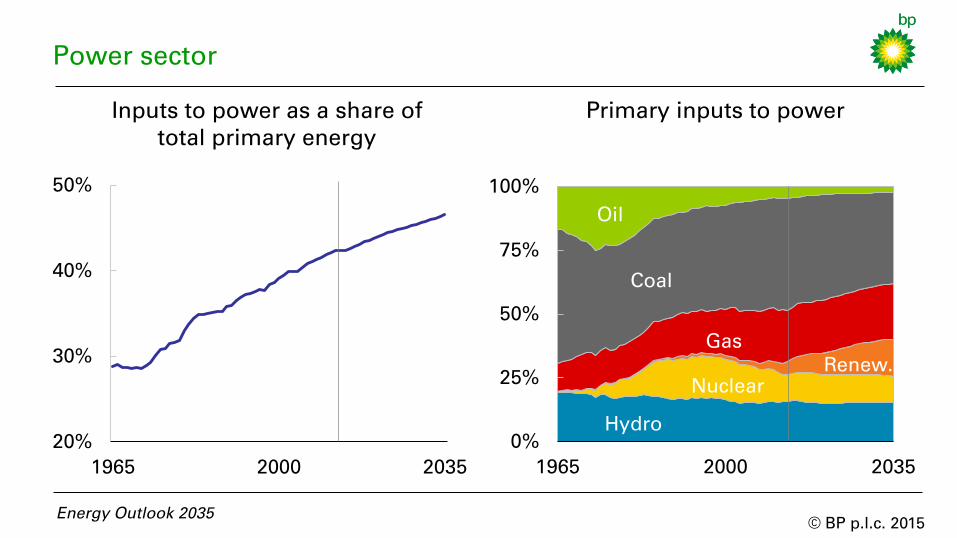

Power sector

0%

25%

50%

75%

100%

1965 2000 2035

Inputs to power as a share of

total primary energy

Primary inputs to power

20%

30%

40%

50%

1965 2000 2035

Energy Outlook 2035

Coal

Gas

Oil

Hydro

Nuclear

Renew.

© BP p.l.c. 2015

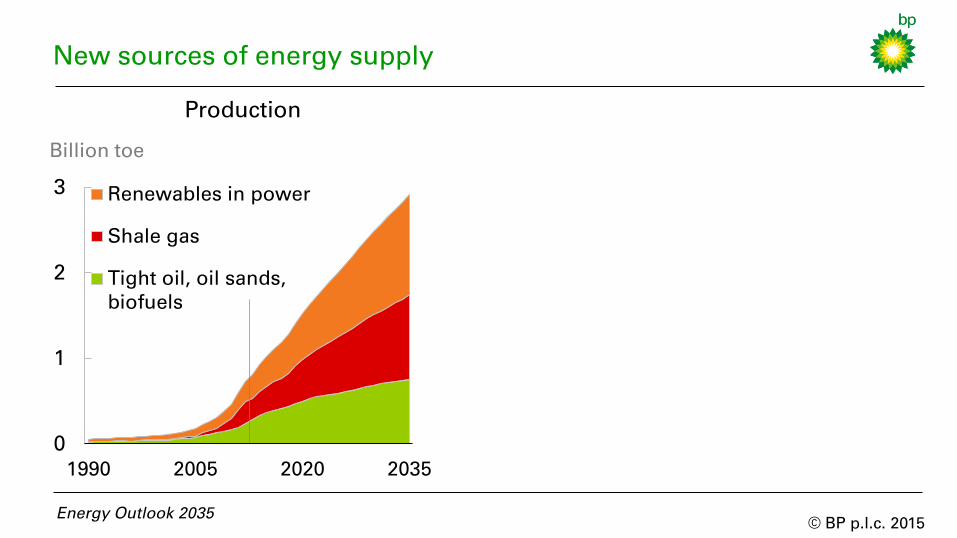

New sources of energy supply

Energy Outlook 2035

0

1

2

3

1990 2005 2020 2035

Renewables in power

Shale gas

Tight oil, oil sands,

biofuels

Production

Billion toe

© BP p.l.c. 2015

0 20 40 60

Middle East

Europe & Eurasia

Africa

S & C America

North America

Asia Pacific

Tight oil

Shale gas

New sources of energy supply

Energy Outlook 2035

0

1

2

3

1990 2005 2020 2035

Renewables in power

Shale gas

Tight oil, oil sands,

biofuels

Billion toe Billion toe

Technically recoverable resources

Source: © OECD/IEA 2014

Production

© BP p.l.c. 2015

0 20 40 60

Middle East

Europe & Eurasia

Africa

S & C America

North America

Asia Pacific

Tight oil

Shale gas

New sources of energy supply

Energy Outlook 2035

0

1

2

3

1990 2005 2020 2035

Renewables in power

Shale gas

Tight oil, oil sands,

biofuels

Billion toe Billion toe

Technically recoverable resources

Source: © OECD/IEA 2014

Production

© BP p.l.c. 2015

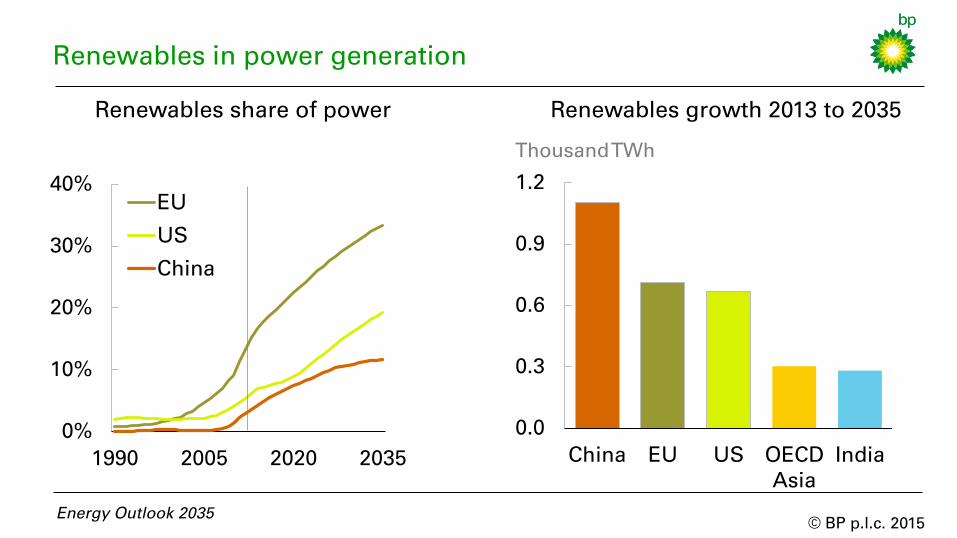

Renewables in power generation

Energy Outlook 2035

Renewables share of power

0%

10%

20%

30%

40%

1990 2005 2020 2035

EU

US

China

0.0

0.3

0.6

0.9

1.2

China EU US OECD

Asia

India

Renewables growth 2013 to 2035

Thousand TWh

© BP p.l.c. 2015

Oil and other liquid fuels

Energy Outlook 2035

© BP p.l.c. 2015

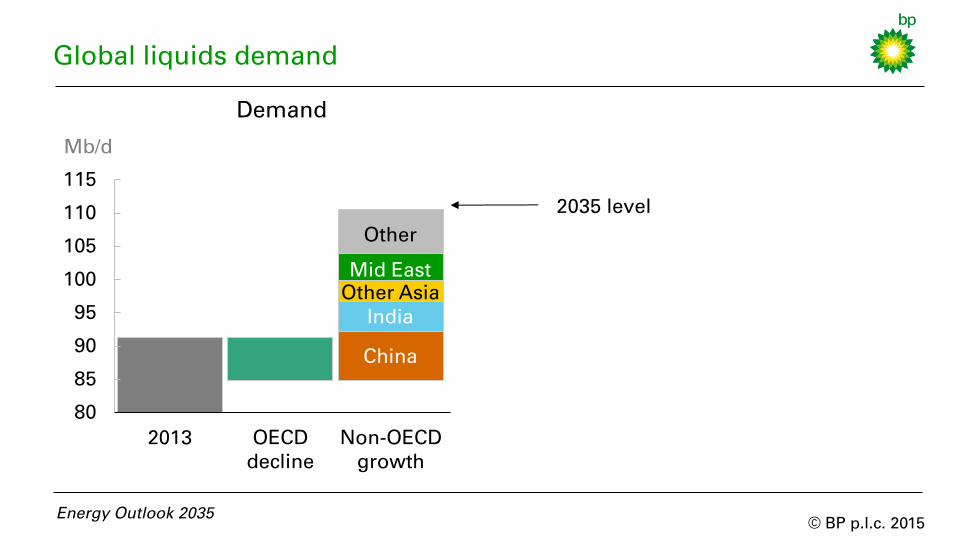

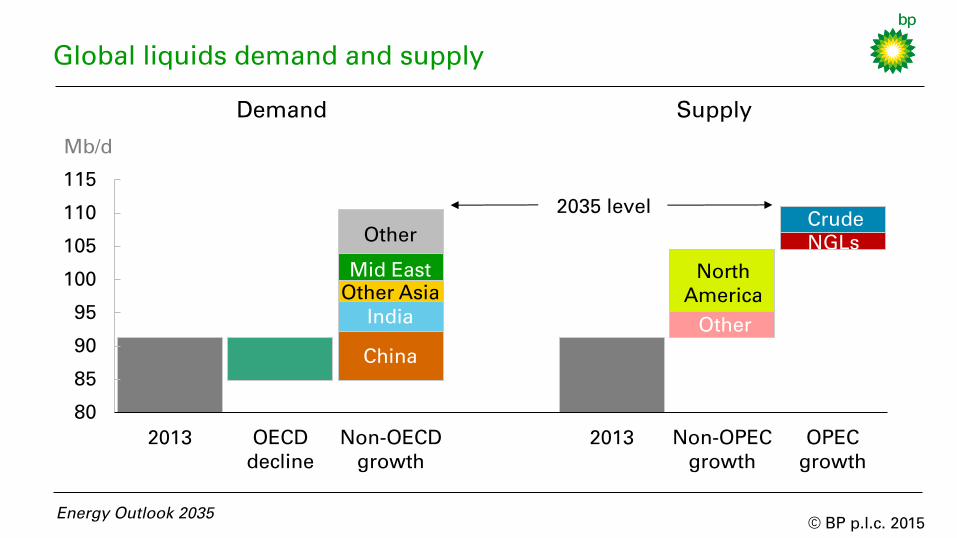

Global liquids demand

Mb/d

Energy Outlook 2035

80

85

90

95

100

105

110

115

2013 OECD

decline

Non-OECD

growth

2013 Non-OPEC

growth

OPEC

growth

India

Mid East

China

NGLs*

Crude

Other

Other Asia

2035 level

North

America

Other

Demand Supply

2035 level

© BP p.l.c. 2015

Global liquids demand and supply

Mb/d

Energy Outlook 2035

80

85

90

95

100

105

110

115

2013 OECD

decline

Non-OECD

growth

2013 Non-OPEC

growth

OPEC

growth

India

Mid East

China

NGLs

Crude

Other

Other Asia

2035 level

North

America

Other

Demand Supply

© BP p.l.c. 2015

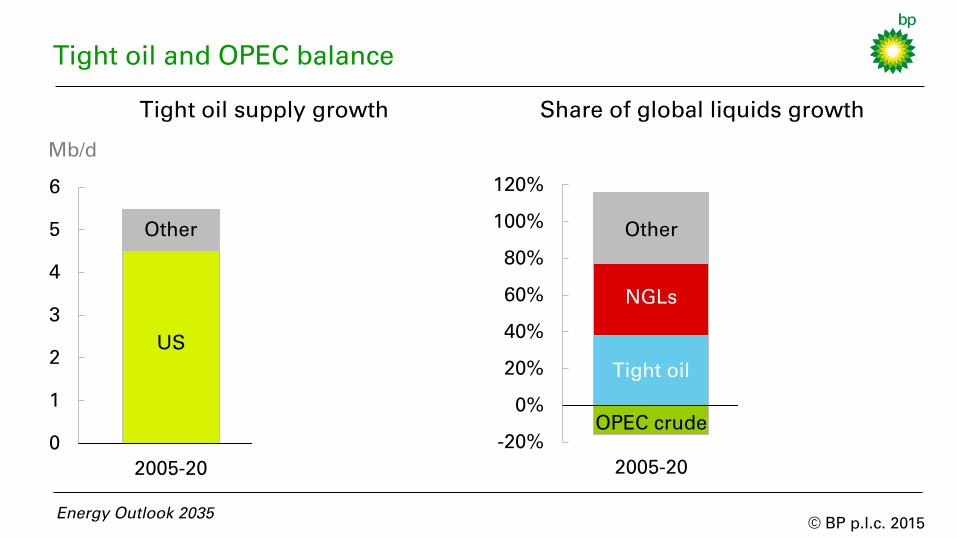

Tight oil and OPEC balance

0

1

2

3

4

5

6

2005-20 2020-35

Russia

S & C America

China

Canada & Mexico

US

US

Other

Tight oil supply growth

Mb/d

-20%

0%

20%

40%

60%

80%

100%

120%

2005-20 2020-35

Share of global liquids growth

Energy Outlook 2035

Other

NGLs

Tight oil

OPEC crude

© BP p.l.c. 2015

Tight oil and OPEC balance

0

1

2

3

4

5

6

2005-20 2020-35

Russia

S & C America

China

Canada & Mexico

US

US

Other

Tight oil supply growth

Mb/d

-20%

0%

20%

40%

60%

80%

100%

120%

2005-20 2020-35

Share of global liquids growth

Energy Outlook 2035

Other

NGLs

Tight oil

OPEC crude

© BP p.l.c. 2015

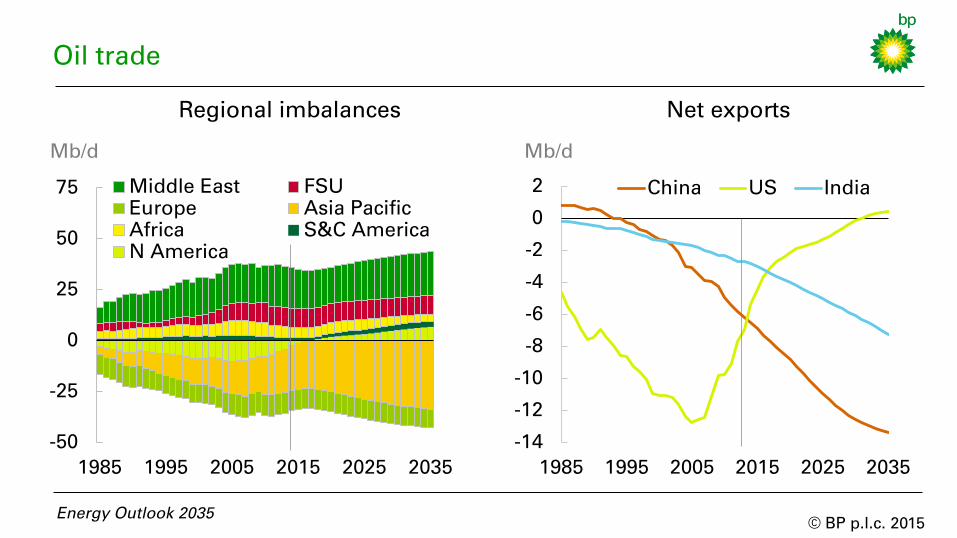

-14

-12

-10

-8

-6

-4

-2

0

2

1985 1995 2005 2015 2025 2035

China US India

Oil trade

Energy Outlook 2035

Mb/d

Net exports

-50

-25

0

25

50

75

1985 1995 2005 2015 2025 2035

Middle East FSU

Europe Asia Pacific

Africa S&C America

N America

Regional imbalances

Mb/d

© BP p.l.c. 2015

Natural gas

Energy Outlook 2035

© BP p.l.c. 2015

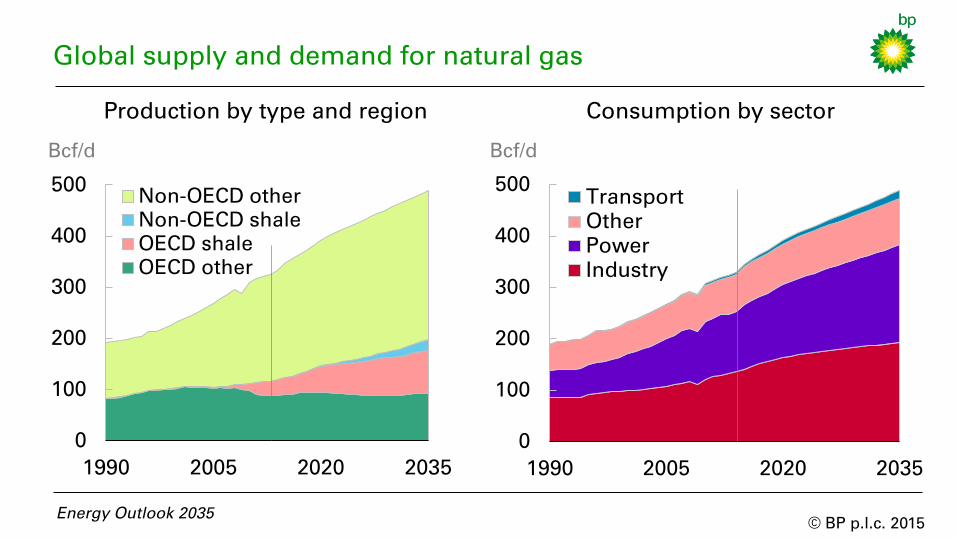

0

100

200

300

400

500

1990 2005 2020 2035

Non-OECD other

Non-OECD shale

OECD shale

OECD other

Energy Outlook 2035

Production by type and region

Bcf/d

0

100

200

300

400

500

1990 2005 2020 2035

Transport

Other

Power

Industry

Consumption by sector

Bcf/d

Global supply and demand for natural gas

© BP p.l.c. 2015

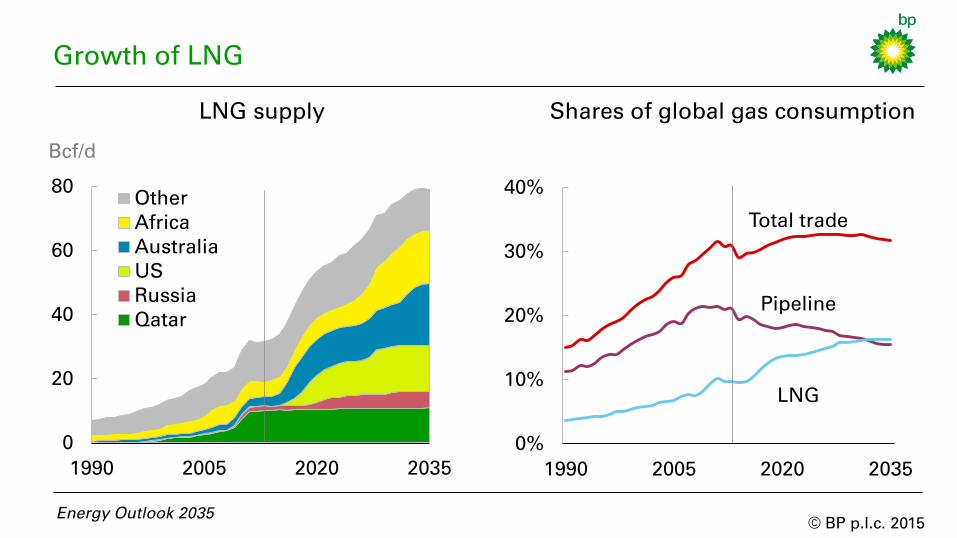

Energy Outlook 2035

Bcf/d

LNG supply

0

20

40

60

80

1990 2005 2020 2035

Other

Africa

Australia

US

Russia

Qatar

0%

10%

20%

30%

40%

1990 2005 2020 2035

Total trade

Pipeline

LNG

Shares of global gas consumption

Growth of LNG

© BP p.l.c. 2015

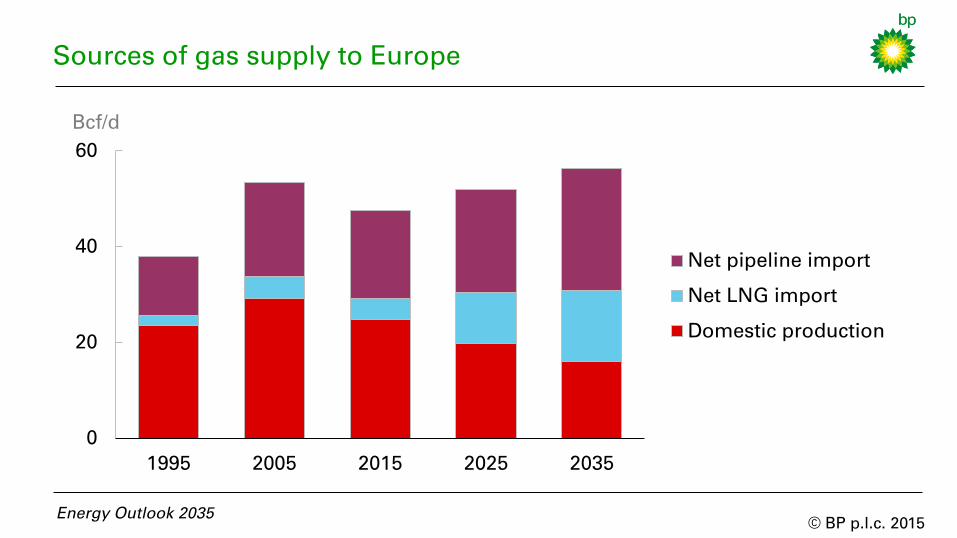

Sources of gas supply to Europe

Bcf/d

Energy Outlook 2035

0

20

40

60

1995 2005 2015 2025 2035

Net pipeline import

Net LNG import

Domestic production

© BP p.l.c. 2015

Low GDP growth

- what if growth in China and India

slows more rapidly than assumed?

Climate policies

- what if policymakers take more

actions to reduce emissions?

Geopolitics

- what are the implications of

heightened geopolitical risks?

China’s electrification

- what if China’s electricity use

follows a different path?

Key uncertainties

Energy Outlook 2035

© BP p.l.c. 2015

Low GDP growth

what if growth in China and India

slows more rapidly than assumed?

Energy Outlook 2035

© BP p.l.c. 2015

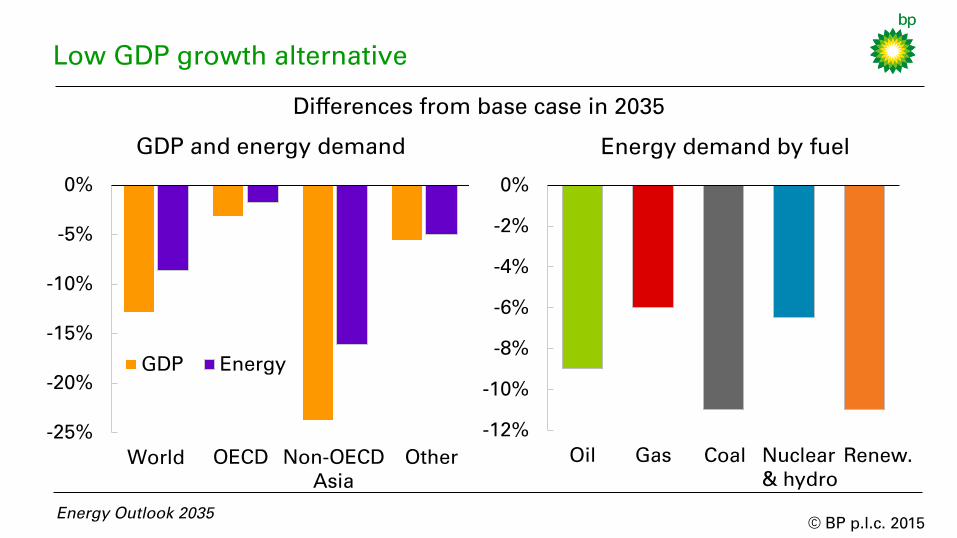

-25%

-20%

-15%

-10%

-5%

0%

World

GDP Energy

Low GDP growth alternative

Energy Outlook 2035

OECD

GDP and energy demand

Other

-12%

-10%

-8%

-6%

-4%

-2%

0%

Oil Gas

Energy demand by fuel

Nuclear

& hydro

Renew. Coal Non-OECD

Asia

Differences from base case in 2035

© BP p.l.c. 2015

Climate policies

what if policymakers take more

actions to reduce emissions?

Energy Outlook 2035

© BP p.l.c. 2015

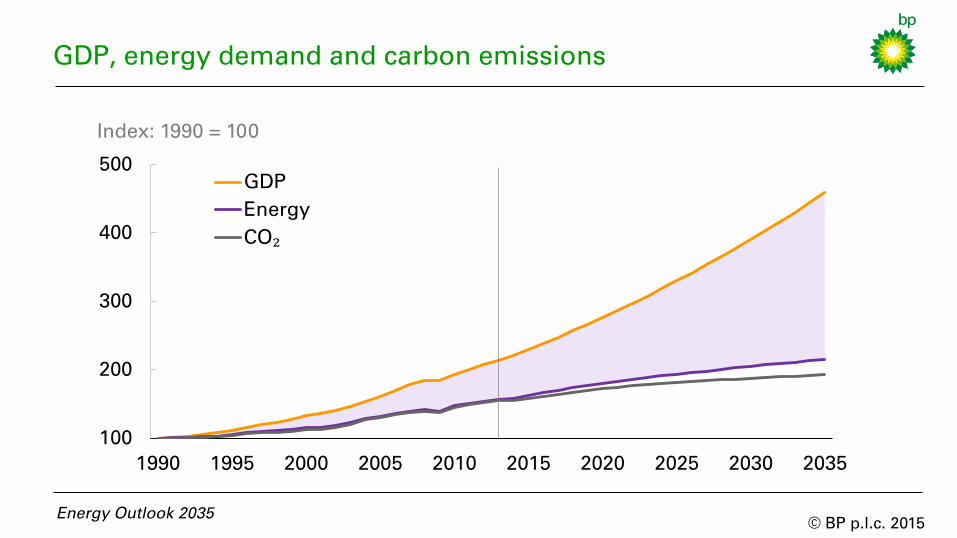

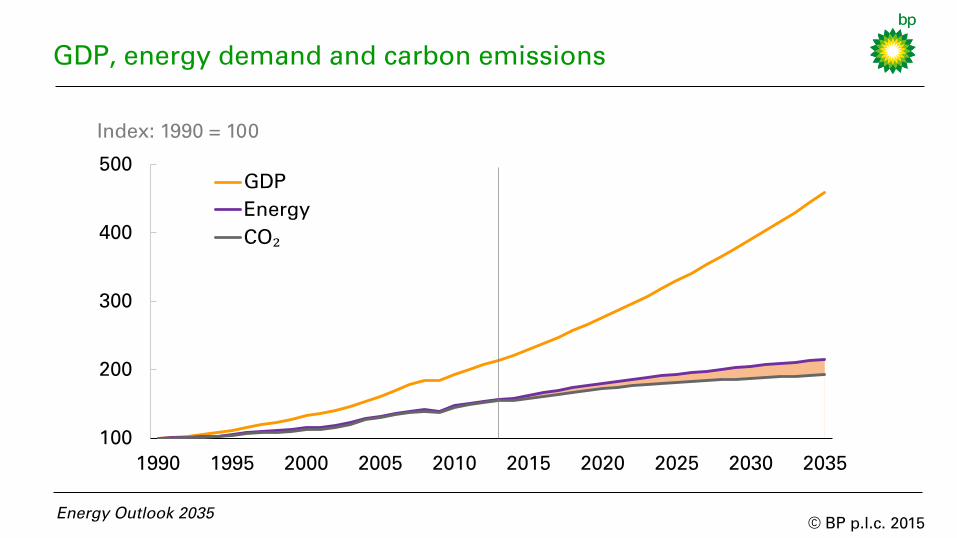

GDP, energy demand and carbon emissions

100

200

300

400

500

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

GDP

Energy

CO₂

Index: 1990 = 100

Energy Outlook 2035

© BP p.l.c. 2015

GDP, energy demand and carbon emissions

100

200

300

400

500

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

GDP

Energy

CO₂

Index: 1990 = 100

Energy Outlook 2035

© BP p.l.c. 2015

GDP, energy demand and carbon emissions

100

200

300

400

500

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

GDP

Energy

CO₂

Index: 1990 = 100

Energy Outlook 2035

© BP p.l.c. 2015

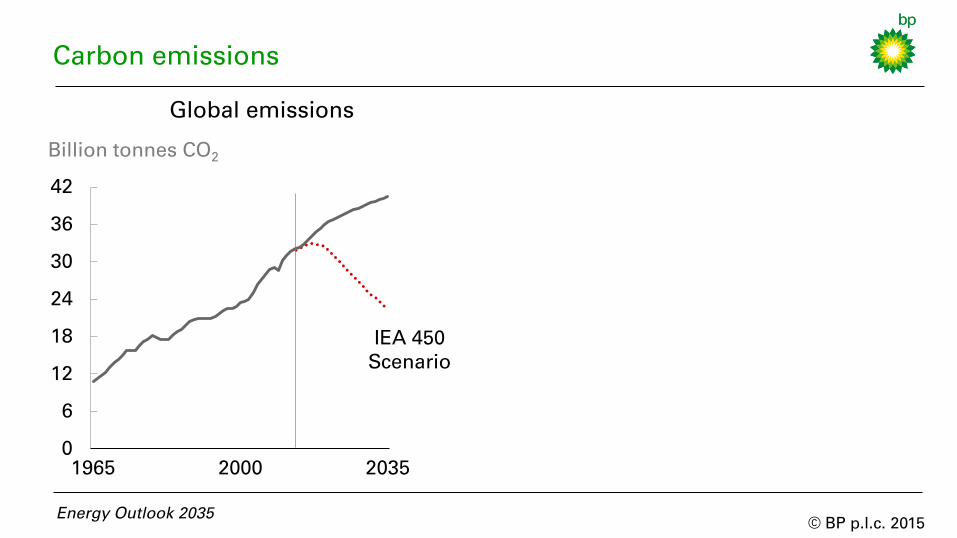

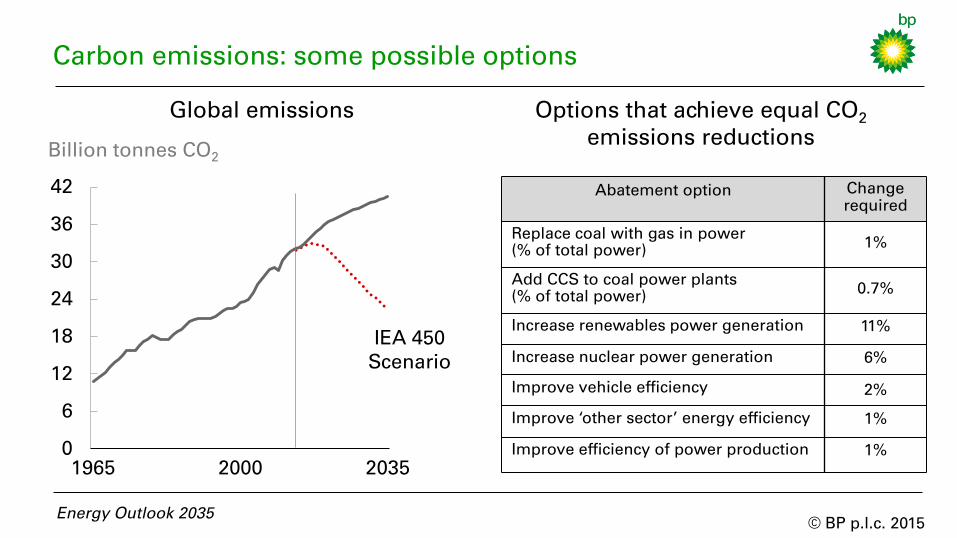

Carbon emissions

Options that achieve equal CO2

emissions reductions* Billion tonnes CO

2

Global emissions

0

6

12

18

24

30

36

42

1965 2000 2035

IEA 450

Scenario

Abatement option Change

required

Replace coal with gas in power

(% of total power) 1%

Add CCS to coal power plants

(% of total power) 0.7%

Increase renewables power generation 11%

Increase nuclear power generation 6%

Improve vehicle efficiency 2%

Improve ‘other sector’ energy efficiency 1%

Improve efficiency of power production 1%

* Normalised for a 1% swing in the coal/gas mix in power generation,

equivalent to 110 Mt CO2. Estimates are based on energy shares in 2013.

Energy Outlook 2035

© BP p.l.c. 2015

Carbon emissions: some possible options

Options that achieve equal CO2

emissions reductions Billion tonnes CO

2

Global emissions

0

6

12

18

24

30

36

42

1965 2000 2035

IEA 450

Scenario

Abatement option Change

required

Replace coal with gas in power

(% of total power) 1%

Add CCS to coal power plants

(% of total power) 0.7%

Increase renewables power generation 11%

Increase nuclear power generation 6%

Improve vehicle efficiency 2%

Improve ‘other sector’ energy efficiency 1%

Improve efficiency of power production 1%

Energy Outlook 2035

© BP p.l.c. 2015

Conclusion

Energy Outlook 2035

Changing energy mix

− gas fastest growing fossil fuel, coal the slowest

− continued rapid growth in renewables

Continuous change is the norm for energy markets

Changing energy trade patterns

− increasingly flowing from West to East

Changing the carbon emissions path?

− no silver bullet, need action on many fronts

− let the market pick the winners

© BP p.l.c. 2015

17th

February 2015

BP Energy Outlook 2035

bp.com/energyoutlook

#BPstats