food-tech industry and trends · 2017-09-19 · food-tech industry and trends ... online shopping...

TRANSCRIPT

We help to knit your dreams!

Aakanksha Aggarwal FOUNDER | CRAFT DRIVEN MARKET RESEARCH

Food-Tech Industry and Trends

A REPORT RESEARCHED BY CRAFT DRIVEN MARKET RESEARCH

CONTACT: +91-9540756743

May, 2016

We help to knit your dreams!

Aakanksha Aggarwal FOUNDER | CRAFT DRIVEN MARKET RESEARCH

Food-Tech Industry and Trends A REPORT RESEARCHED BY

CRAFT DRIVEN MARKET RESEARCH CONTACT: +91-9540756743

May, 2016

We help to knit your dreams!

Craft Driven Market Research Message

This century has come up with a new generation of entrepreneurs. Many start-ups are opening

up in India. With currently 4200 start-ups, India is globally at third position in the number. There

is no doubt that the environment is favourable for start-ups and they have become a driving

force for dynamic nature of the market. With increasing number of start-ups, there are

increasing number of investments as well and all the industries have become closely involved

with each other. This rising number of start-ups has given a way to e-commerce in different

fields. Initially it began with discounted products and apparels and soon it entered vigorously

into can service. No lately, there has been an increasing trend of food- tech based start-ups.

Currently there are more than 150 food-tech in India, out of which some are at national level

and many at regional levels. Many have got funding as well for improved operations and this

trend is giving a boost to food industry. Currently, most of the food-tech start-ups are being

operated in metro cities with few tier-1 cities but the studies depict that soon they will explore

the untapped markets of tier-2 cities. Also, there are various trends changing in the industry.

Beginning from restaurant take-outs, it has moved to home cooked food delivery and recently

to diet specific food as well. In future, it is expected to see more changes in this industry owing

to increasing competition.

Craft Driven Market Research has made an effort to bring the attention of investors towards

this industry and make their investments judicially considering the factors which are

determinants of success of a start-up in food-tech industry. The Government of India’s efforts

to launch Start-up India initiative will increase the number of start-ups in this field and thus it

becomes necessary for start-up founders as well as investors to promote only those services

which are suitable for market demands.

Craft Driven would like to thank the reviewers of this report who helped in editing it and making

it worthy of read. Craft Driven expects that food-tech industry continues to make progress and

bring India in the forefront in this domain.

Aakanksha Aggarwal

Founder

Craft Driven Market Research

Email: [email protected]

Phone: +91-9560847547

We help to knit your dreams!

Contents:

1. Consumer Segmentation

2. Key market clusters

3. Emerging categories

4. Investments and amount raised

5. Logistics

6. Role of logistics in food delivery

business

7. Popular third party delivery

companies

8. Market Penetration

9. Total orders- Projection

10. Business structure & M&A’s

11. Findings and analysis

Figures

1. City wise number of

registered stores

2. Categories of food-techs

3. Percentage of funded vs

non funded food-techs

4. Funding in specific

categories

5. Number of investments

category wise

6. Number of companies

funded 2013-18

7. Market Penetration

8. Total orders- Projection

9. Self-Preparation vs on

order

10. Table- M&A’s

11. Table-M&A’s 2

We help to knit your dreams!

About the Report

Online shopping is increasingly becoming more vital to people and this trend has been travelling developing

nations vigorously. There is an ever growing need of products and services alike with higher margins and easy

accessibility. This has led a way for online shopping and e-commerce. People look for a wide variety of goods

that includes standard as well as premium goods such as organic food, grocery, clothing, accessories,

personalised gifts and even cabs. The trend started with clothing, books, electronics and then got extended to

cabs and now recently to food delivery. In this report, we discuss comprehensive range of challenges with food

delivery start-ups in India. We will highlight where this industry is headed towards. This report will also address

several questions such as whether the market is moving in the right direction, is the market profitable enough

for investors, and why many companies in the domain are closing down. This report will also discourse on

several logistic issues associated with the industry will highlight key factors in the same industry that will

include investments, major segments and new trends.

This report has several purposes and will interest a wide audience. It will support founders of food delivery

companies to better strategize keeping in mind all the issues that are discussed in the report. The report will

support them to understand new trends and probable future outcomes out of those trends. Investors will be

benefited by getting an insight to how companies need to be evaluated for promising future. The report will

be helpful for them in avoiding futile investments. In addition to this, the report will be of tremendous support

to those who are beginning to start another food-tech company.

This report is mainly focused on current trends of food-tech industry and has been supported by various

databases, market analysis and surveys to authenticate the results. Projections have been done by author’s

understanding and knowledge of the industry.

We help to knit your dreams!

Recent decade has seen tremendous change in

the way India shops and sells. With an internet

user base of 354 million in June 2015, e-

commerce has become one of the favourite

words among the corporate society. Various

entrepreneurs, businesses and ventures are

looking into e-commerce every year with

higher scope and bringing up varied

commercial models. The whole sector has seen

extensive growth with 12.6 billion USD

revenue in 2013 (PwC, 2014). With increasing

penetration of smart phones, more online

market spaces that include F&B organizations,

retail, logistics and fashion industry, are more

focussed on increasing their online visibility. E-

commerce reduces several costs related to

physical presence of stores but at the same

time increases expectations of customers.

With increasing expectations, challenges

increase but dynamic nature of Indian market

set it apart and give a leverage to grow in

liberal manner. Although, 92% of business still

comes from the corner stores and physical

outlets, yet there is high potential of growth

for online stores (KPMG, 2014).

Consumer Segmentation

With increasing number of internet users,

online business penetration has increased

tremendously. Today, internet is accessed by

40 million Indians everyday with 58,000 new

users connecting every day (BCG, 2015). India

has the third largest internet population after

the US and Canada with a projection of 500

million users in 2018. The major reasons

behind this increase are penetration up to rural

areas, increased internet usage by older

generation, increasing infrastructure of

telecom industry and growing number of e-

commerce and other internet based service

providers. Based on the above factors, internet

online consumers can be segmented into the

following;

Rural consumers: With 68% of India’s

population living in rural areas (The World

Bank, IBRD, IDA, 2014), and many internet

based companies targeting tier-II and lower

segments of the market, the number of rural

consumers is increasing at a sharp rate. Also,

with more data enabled smart phones

We help to knit your dreams!

penetrating the market, this segment has

become more active in recent years. Many

companies like Coca Cola have penetrated this

segment in 1990s by introducing products

focussed specifically to rural market. Currently,

major consumption is in the industry of

personal care, hair care and teeth care (BCG,

2015).

Working Population- Women: This segment

comprises of working women population in the

age range 24-54 years. India has one of the

lowest female labour force participation rates

(FLFP), it is currently at 33% (2012) and still

growing every year (IMF, 2014). Their

increasing number is a major factor for

increasing online shopping and their increased

spending power has also supported several

online stores. Major kick has been given to

online stores in clothing and food.

Working Population-Non women: This

segment also comprises the population in the

age range of 24-54 years. This customer

segment is the highest spender on online

transactions. According to Census 2011, more

than 40% of India’s population comes under

this segment. Their major spending is on food

and beverages closely followed by luxury

products (BCG, 2015).

Figure1. City wise start-ups

Youth: This segment comprises of population

below 25 years of age and this segment makes

18.1% of total Indian population (CIA World

Book facts). They are the key drivers of

increasing sales of online services and

products. Most of the e-commerce websites

are designed based on their interests. Their

major spending area is of packaged food which

is followed by apparels, accessories, gadgets

and mobiles.

Middle income and lower middle income:

According to NCAER, in 2016, India’s middle

income population would be 267 million. This

segment is important for e-commerce

websites selling discounted products such as

Flipkart, Amazon, Snapdeal but does not quite

appeal to providers selling food or other luxury

items. Their increased spending capacity has

boosted online market in India.

Key market clusters for online food delivery

market:

A study done on 70 food tech start-ups

operational in 2016 reveals that most of the

food tech companies are based in metro cities

Bangalore, Delhi and NCR region. Very few

City No. of registered companies

Ahmedabad 1

Bangalore 12

Rajasthan 1

Chandigarh 1

Chennai 2

Cochin 1

Delhi 1

Faridabad 1

Gurgaon 6

Hyderabad 2

Mumbai 4

New Delhi 10

Pune 2

Unknown 28

We help to knit your dreams!

companies have targeted tier-2 cities

The presence seems to be directly related to

high consumer base in these cities along with

presence of industries and thus online ordering

customers. Major proportion of customers are

based in corporate sector

It is to be noted that North East India has no or

minimum presence of similar companies and

this happens to be a great opportunity to

explore an untapped market.

Certain tier-2 cities such as Ahmedabad,

Chandigarh and Pune have also got start-up

presence and they offer certain advantages

such as low office rents and lower wages.

Emerging categories for online food techs

A unique selling proposition (USP) is something

that differentiates different brands in any

industry. In food-tech industry, a sound USP

can contribute to success of the organization

and similarly a poor and lack of novelty in USP

can on one hand can increase competitiveness

and on the other, make it difficult to make a

presence in the market.

Elements of USP:

Unique food quality

Price

Special menu or special dishes

Food Delivery

Money back procedures

Factors that impact in the background:

Logistics

Technical know how

Market Penetration

Reviews

Growth with respect to funding

USP value

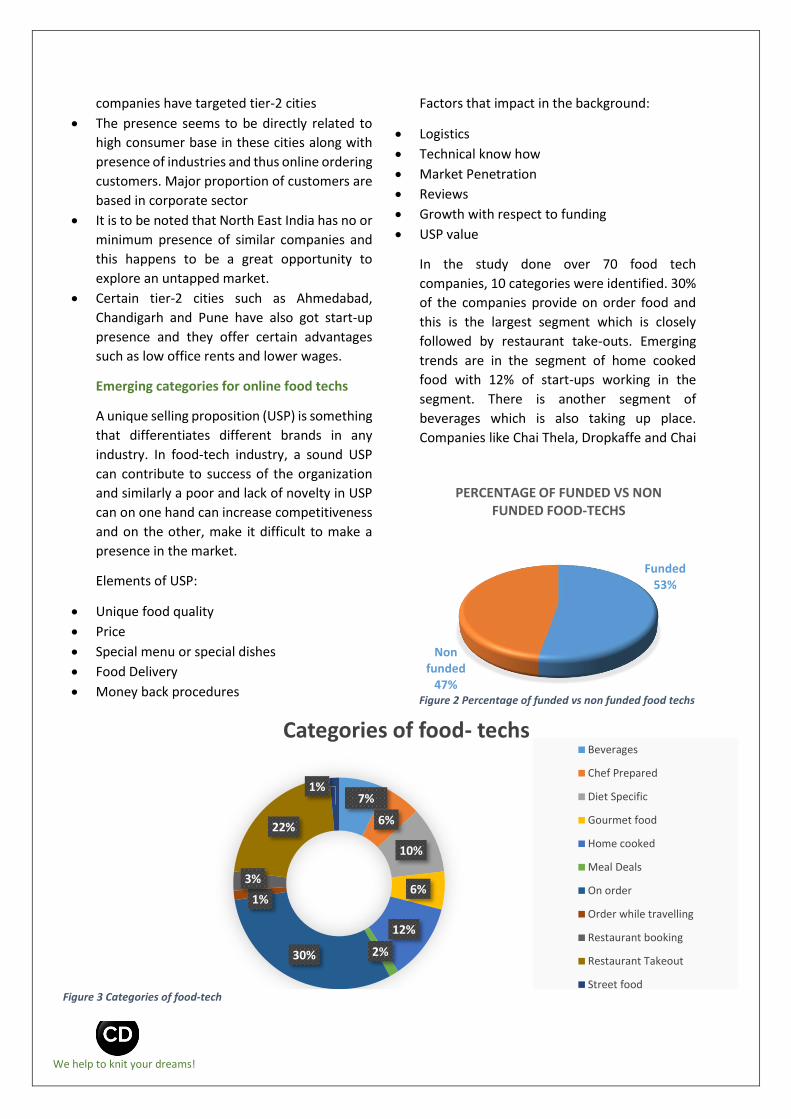

In the study done over 70 food tech

companies, 10 categories were identified. 30%

of the companies provide on order food and

this is the largest segment which is closely

followed by restaurant take-outs. Emerging

trends are in the segment of home cooked

food with 12% of start-ups working in the

segment. There is another segment of

beverages which is also taking up place.

Companies like Chai Thela, Dropkaffe and Chai

Funded53%

Non funded

47%

PERCENTAGE OF FUNDED VS NON FUNDED FOOD-TECHS

7%

6%

10%

6%

12%

2%30%

1%

3%

22%

1%

Categories of food- techsBeverages

Chef Prepared

Diet Specific

Gourmet food

Home cooked

Meal Deals

On order

Order while travelling

Restaurant booking

Restaurant Takeout

Street foodFigure 3 Categories of food-tech

Figure 2 Percentage of funded vs non funded food techs

We help to knit your dreams!

Point are stringly making their place in the

industry.

Among all the companies present in the

industry, there is a slight change in the USPs

provided. Some of the companies are heavily

focused on providing home cooked food while

others on gourmet food from the chefs. 2 years

back, most of the companies in food-tech

domain were based out of restaurant take-

outs but the trend is slowly changing and many

new themes are emerging.

Investments and amount raised

To fulfil customers’ expectations, many new

food-tech companies are entering into the

market. As the number of start-ups is

increasing, there are more investments in the

industry. We studied 70 running companies in

food-tech industry and most of them have

received seed funding. Some have also gone

beyond 2 rounds of funding. Bigger players like

Zomato have got 8 rounds of funding with 4

investors involved in the process.

So far, maximum amount of equity funding has

been invested in Zomato which is not a

surprise due to the reason that it is among the

forerunners in the domain. Among the 70

companies studied, 29 companies have

disclosed the amount of funding received and

19 have received more than $1 million funding.

Even when new trends are emerging,

restaurant take-outs have got the maximum

funding and this includes a list of big players

such as Zomato, FoodPanda and Swiggy. This is

for the reason that these companies are old

players and certainly the companies in the

segment of emerging trends will follow the

suit. It is highly noticeable that home cooked,

beverages and diet specific food delivery

businesses are coming into lime light and

taking up investors’ attention. Major home

cooked start-ups include Fresh Menu and Bite

Club; beverage start-ups include Chai Point and

Dropkaffe while diet specific food providers

include FRSH and iTiffin. These are slowly

gaining market space and getting increased

amount of funding currently.

The trend of food delivery business is fast

catching up in India and so as the investment

in the industry. This is attracting several

players to widen their USPs and come up with

new and innovative ideas. Some provide

attractive coupons and deals; others have

started distributing freebies. Increasing

competition is a win-win situation for both the

organizations and the customers in terms of

innovation and increasing investment. New

categories have also evolved out of

0.0050.00

100.00150.00200.00250.00300.00350.00400.00450.00500.00

497.45

94.22

22.60 10.32 3.60 3.42 3.00 1.00 0.70

Funding in specific categories ($m)

Figure 4 Funding in specific categories ($m)

We help to knit your dreams!

competition such as Travel Khana which

provides food while customers commute.

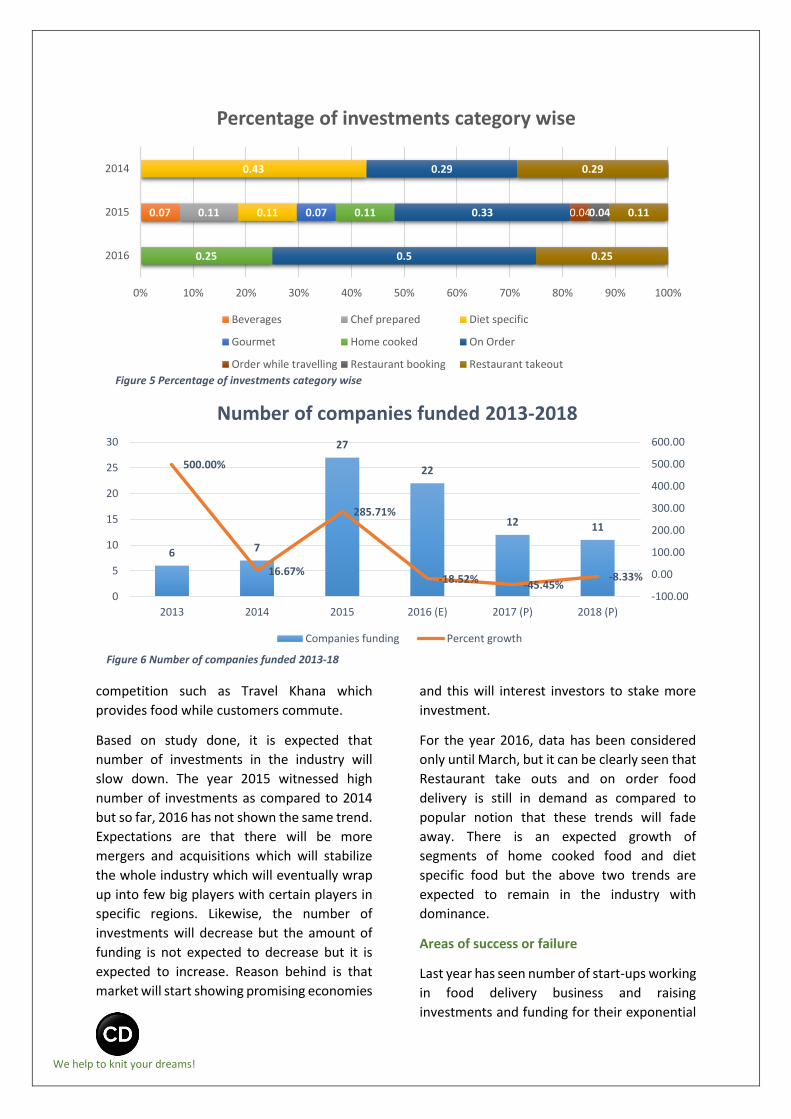

Based on study done, it is expected that

number of investments in the industry will

slow down. The year 2015 witnessed high

number of investments as compared to 2014

but so far, 2016 has not shown the same trend.

Expectations are that there will be more

mergers and acquisitions which will stabilize

the whole industry which will eventually wrap

up into few big players with certain players in

specific regions. Likewise, the number of

investments will decrease but the amount of

funding is not expected to decrease but it is

expected to increase. Reason behind is that

market will start showing promising economies

and this will interest investors to stake more

investment.

For the year 2016, data has been considered

only until March, but it can be clearly seen that

Restaurant take outs and on order food

delivery is still in demand as compared to

popular notion that these trends will fade

away. There is an expected growth of

segments of home cooked food and diet

specific food but the above two trends are

expected to remain in the industry with

dominance.

Areas of success or failure

Last year has seen number of start-ups working

in food delivery business and raising

investments and funding for their exponential

6 7

27

22

12 11

500.00%

16.67%

285.71%

-18.52% -45.45%-8.33%

-100.00

0.00

100.00

200.00

300.00

400.00

500.00

600.00

0

5

10

15

20

25

30

2013 2014 2015 2016 (E) 2017 (P) 2018 (P)

Number of companies funded 2013-2018

Companies funding Percent growth

0.07 0.11 0.11

0.43

0.07

0.25

0.11

0.5

0.33

0.29

0.040.04

0.25

0.11

0.29

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2016

2015

2014

Percentage of investments category wise

Beverages Chef prepared Diet specific

Gourmet Home cooked On Order

Order while travelling Restaurant booking Restaurant takeout

Figure 5 Percentage of investments category wise

Figure 6 Number of companies funded 2013-18

We help to knit your dreams!

growth. When the whole food industry is

expected to grow at a rate of 28%, food

delivery business shows tremendous scope

with a growth of over 40% y-o-y basis. Unlike

other e-commerce businesses, food delivery

offers highly perishable products and thus

needs to be extremely precocious of several

contexts.

There are various segments which determine

the success or failure of food-tech industry.

Major determinants are logistics, technical

investment and market penetration. This

report will mainly focus on logistics and market

penetration of various players. For logistic,

third party service providers have come

upfront and become a major success driver for

many start-ups.

Logistics:

The rise in use of smart phones and thus e-

commerce has resulted in the emergence of

world class logistics systems in the country.

Growth of e-commerce has attracted

numerous investments in the Indian logistics

sector and made it a highly technology

dependent system in the industry. In food

delivery business, some have invested in

building their own logistics software systems

and others have outsourced their

requirements to expert logistics based

organizations. The whole system is quite

complex which involves high service levels,

cash on delivery system and supply chain

security and regulations involved. The logistics

requirements make supply chain management

more complex and also increase costs in carrier

fleet operations.

Role of logistics in food delivery

business

Logistics is the key enabler of all the food

delivery start-ups and their success highly

depend upon the efficiency of their logistics.

Logistics contributes greatly to customer

satisfaction through successful delivery. Most

of the delivery businesses operate a

centralised logistic system that can manage all

the chefs or restaurants on board and adjust

delivery system taking into account all the

participants. Currently, all the successful food

delivery businesses manage it through their

apps which connects headquarters to delivery

points. Controlling the whole process through

software adds to the USP of the system and

may cut costs up to 30%.

Overview of complete process

Food ordered online undergo various steps of

the logistics process in a span of very short

duration. The process has been outlined as

follows:

First interaction with delivery: As the food is

ordered online an alert is send to the kitchen

as well as the delivery staff so as to start

preparing for the delivery and subsequently

the food. The process takes only a few seconds

as it is automated using software and

centralized system. As soon as the order is

placed, raw material for cooking is collected

and preparation of food takes place. In the

meantime, delivery is assigned to the

concerned keeping it in mind that minimum

time takes place to deliver the food.

Fulfilment: Post first interaction, second stage

of fulfilment comes up. This stage comprises of

very fast processing that includes preparing

food as per the order, packing it in a way that

it reaches safely and with the same taste to the

customer and finally transferring the packed

and labelled food to the delivery staff which

will continue the further processing.

Final step: The step involves final dispatch of

the prepared food to the customer. This could

be directly from the kitchen of the site from

where the food has been order or from the

kitchen of a restaurant which has tied up with

the site. The delivery can be either connected

to the ordering site or the ordering restaurant

or through any third party which handles

delivery for the ordering site.

We help to knit your dreams!

Food delivery business is highly perishable and

often involves no time for anything else

beginning from when the order is placed and

then finally delivered to the customer. There is

no scope of return or change of order unless

there is a mistake by the seller end. Cash on

delivery (COD) and online payment both are

prevalent in the market.

Popular third part delivery companies

With the advancements in e-commerce and

build-up of strong online community, many

delivery businesses have started in last two

years in India. Initially, they focussed on e0-

retail but with the growth of food delivery

business, many food -techs have tied up with

these companies so as to get rid of logistics and

get an expert for higher satisfaction of

customers. Some of the popular companies in

food- delivery business that provide logistics

solutions are:

Roadrunnr: The company is intended to

become Uber for food delivery. It is

headquartered in Kormangala, Karnataka. The

founders are ex-employees of Flipkart, Ola and

Amazon; and have a good experience of

logistic based environment. The company has

already received 3 rounds of investments even

when it was founded in 2015 only. In June,

2015, it received Series A funding of $11

million, and then again in October, 2015,

received funding from 3 investors where one

has made an undisclosed amount of

investment and the other two invested $10

million. The list of investors includes Blume

Ventures (Series A), Nexus Venture Partners

(Series A), Sequoia Capital (Series A) and Yuri

Milner (Venture). The company is highly

focussed on developing a strong technology

platform to make scalability and operations

easier. They have clients from merchants,

restaurants and e-commerce companies. The

company has operations in Bangalore, Mumbai

and Delhi/ NCR region and is slowly expanding

to other cities as well. Currently they follow an

order base of more than 25,000 per day.

The company’s business model is similar to

Uber since it partners with drivers, students

and part time workers which give them a

leverage of having no assets and warehouses.

Their pricing is similar to courier services which

is based on size of shipment. Their client base

ranges from older chains like KFC, Pizza Hut to

start ups like Brekkie, Bhukkad, Ammi’s Biryani

and Grab Eat.

Opinio: The company is focussed on last mile

delivery is providing services to food

businesses, grocery, bakery, peer to peer and

many more. Founded by Mayank Kumar and

Lokesh Jangid, its operations started in 2015

but has gained quite a lot of momentum with

2 rounds of investments. It claims to have more

than 4800 merchants in areas of Bengaluru and

3 of Delhi with 30% growth. The company has

an opinion that all the problems with logistics

can be solved by integrating technology at

different levels that includes payments,

optimisation merchant database,

NewOrder

Raw Material

collection/ Delivery

Alert

Food preparati

on

Packaging/

labelling/ billing

Food send to delivery

team

Figure 7 Logistics process

We help to knit your dreams!

requirements, feedbacks etc. Charging is done

per order basis.

The company website boasts of having covered

10 cities. The company is doing 20,000

deliveries per day. The client base ranges from

Tiny Owl, Faasos, ammi’s Biryani, California

Burrito, Khan Saheb etc.

Grab.in: Majorly focussed on food delivery

businesses, this B2B was launched earlier as

Grab a Grub. The company has received seed

funding of $1 million from Haresh Chawla, an

independent investor and Oliphans Capital.

Company is based in Mumbai and is headed by

trio of Nishant Vohra, Pratish Sanghvi, Jignesh

Patel. Currently operating in 10 cities, the

company has a team of more than 800 riders

who pick up a delivery within 15 minutes of

order. Company has a strong base of 1030

merchants with more than 1,5000,000 orders

finished till the time of writing this report.

The company understands the challenges of

last mile delivery and how it can impact a food

delivery business. Thus, Grab heavily relies on

technology to make the whole process

seamless. Their effectiveness has led them to

join hands with the famous Dabbawallas of

Mumbai. Also, Zomato has invested in Grab to

cover its last mile delivery including for those

restaurants which have only dine-in option.

Swiggy: Although it’s a food delivery platform

but it can be very well placed in the list of those

providing logistics solution. It focusses on

delivering food from the restaurants which are

registered on its portal. Its operations are

mainly concentrated in the areas of Bengaluru.

Founded in 2014 by a trio of Sriharsha Majety,

Rahul Jamini and Nandan Reddy; the company

has been backed up by VCs in 4 rounds. Till

date, it has received $53.5 million in 4 rounds

of funding.

The company has its own fleet of delivery men

having their smartphones equipped with

Swiggy app which contains a routing algorithm.

What differentiates them is that they have no

minimum order policy and their technology

driven service allows everything to be tracked

and managed from the restaurants’

perspective to be done online.

Quickli: Another delivery based start-up which

is based in Gurgoan. The logistics company pick

up and deliver from restaurants as well as

stores. Founded in 2015, the company is

headed by Rohan Diwan and Sudhanshu

Aggarwal. The company got a seed funding of

an undisclosed amount in September, 2015.

Similar to other same domain apps, the

company provides an option of using iOS and

Android platforms, Web dashboard, API

integration to the merchants. The company

achieves an edge by adding miss call

functionality to request a runner. Real time

tracking is provided which improves

transparency in the system.

Shadowfax: Started by IIT alumni- Abhishek

Bansal and Vaibhav Khandelwal, the company

claims to deliver 95% of its delivery to be

finished within 15 minutes of pick up. The

company has a fleet of more than 700 delivery

boys. The company has raised $350k in the

seed round led by Snapdeal’s founders Kunal

Nehl and Rohit Bansal. The client base of the

company ranges from Pind Baluchi, Faasos to

Chhayos and Yo China.

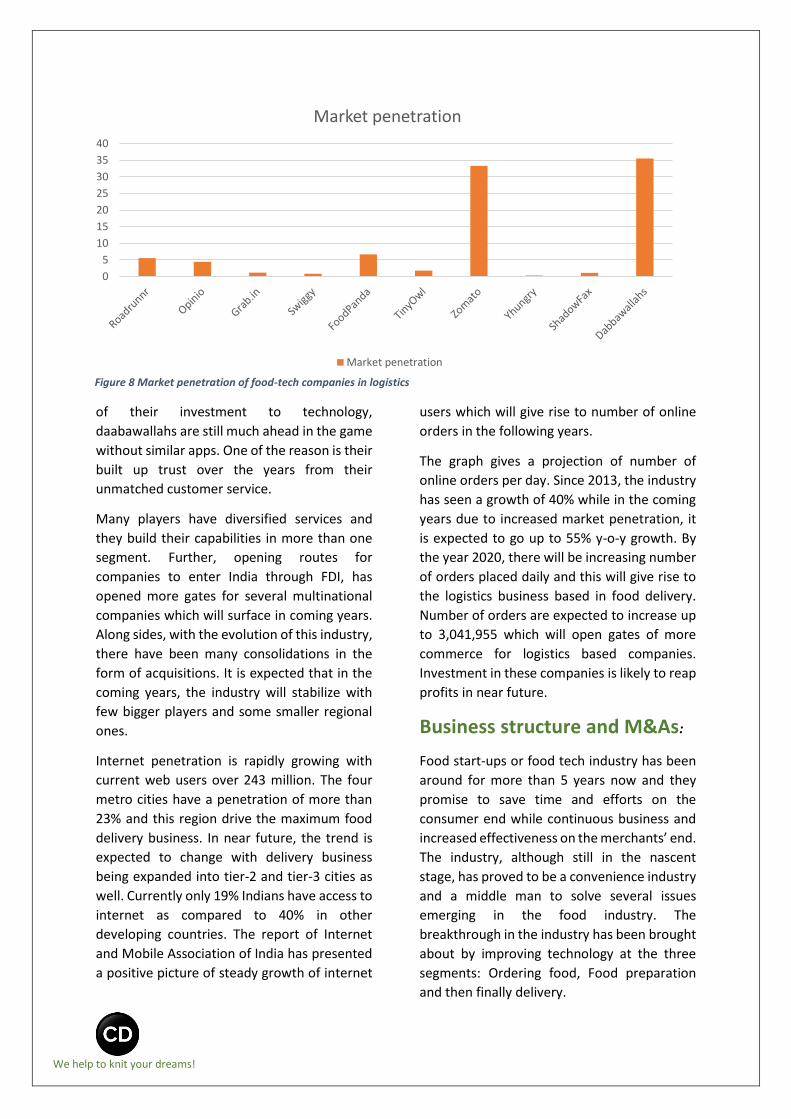

Considering market penetration of certain top

companies, in the field of logistics, there is an

interesting fact that comes up. Mumbai

Dabbawallahs beat all the Indian Startups. Only

Zomato has the potential to compete with

them, remaining fall short of penetration when

Dabbawallahs are included. Dabbawallahs

have been deliberately ncluded in the graph

for the reason that they fulfil all the criteria for

the list. All these companies provide logistics to

restaurants or individual food preparers.

A differential aspect of today’s start-ups with

dabbawallahs is their distinctive ability to

expedite information exchange through

technology driven apps and web systems. The

above graph clearly depicts that even though

these companies are spending a major portion

We help to knit your dreams!

of their investment to technology,

daabawallahs are still much ahead in the game

without similar apps. One of the reason is their

built up trust over the years from their

unmatched customer service.

Many players have diversified services and

they build their capabilities in more than one

segment. Further, opening routes for

companies to enter India through FDI, has

opened more gates for several multinational

companies which will surface in coming years.

Along sides, with the evolution of this industry,

there have been many consolidations in the

form of acquisitions. It is expected that in the

coming years, the industry will stabilize with

few bigger players and some smaller regional

ones.

Internet penetration is rapidly growing with

current web users over 243 million. The four

metro cities have a penetration of more than

23% and this region drive the maximum food

delivery business. In near future, the trend is

expected to change with delivery business

being expanded into tier-2 and tier-3 cities as

well. Currently only 19% Indians have access to

internet as compared to 40% in other

developing countries. The report of Internet

and Mobile Association of India has presented

a positive picture of steady growth of internet

users which will give rise to number of online

orders in the following years.

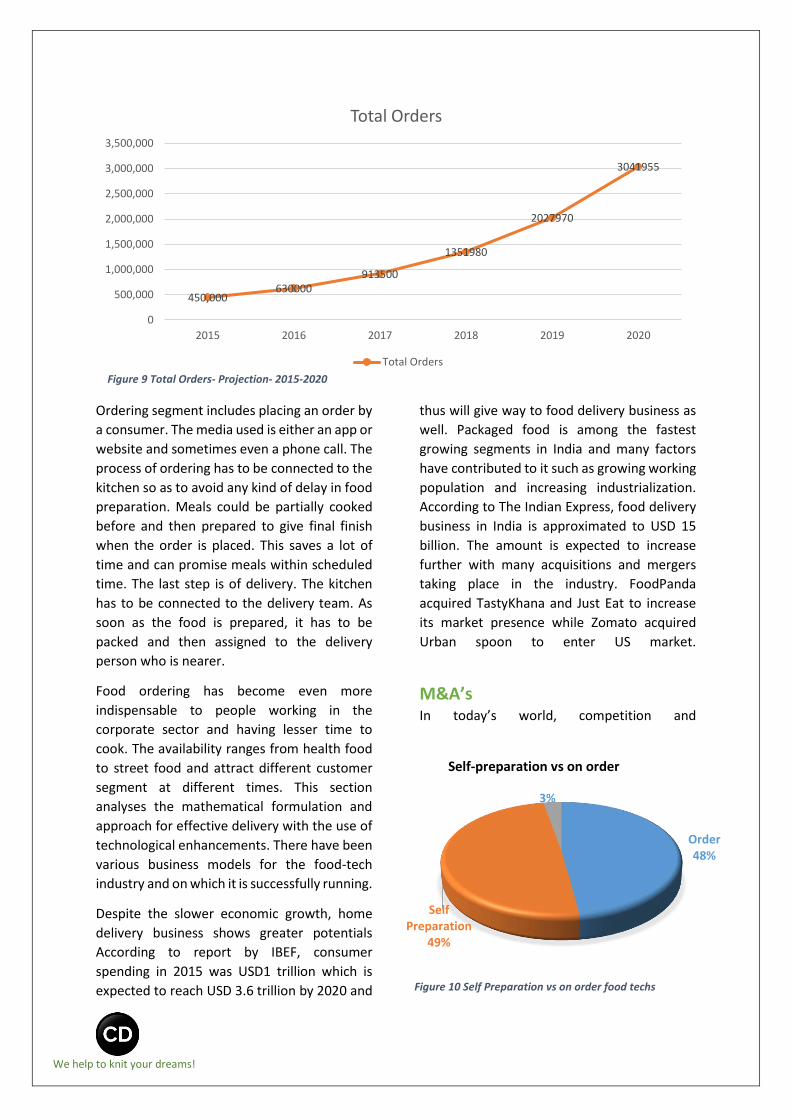

The graph gives a projection of number of

online orders per day. Since 2013, the industry

has seen a growth of 40% while in the coming

years due to increased market penetration, it

is expected to go up to 55% y-o-y growth. By

the year 2020, there will be increasing number

of orders placed daily and this will give rise to

the logistics business based in food delivery.

Number of orders are expected to increase up

to 3,041,955 which will open gates of more

commerce for logistics based companies.

Investment in these companies is likely to reap

profits in near future.

Business structure and M&As:

Food start-ups or food tech industry has been

around for more than 5 years now and they

promise to save time and efforts on the

consumer end while continuous business and

increased effectiveness on the merchants’ end.

The industry, although still in the nascent

stage, has proved to be a convenience industry

and a middle man to solve several issues

emerging in the food industry. The

breakthrough in the industry has been brought

about by improving technology at the three

segments: Ordering food, Food preparation

and then finally delivery.

0

5

10

15

20

25

30

35

40

Market penetration

Market penetration

Figure 8 Market penetration of food-tech companies in logistics

We help to knit your dreams!

Ordering segment includes placing an order by

a consumer. The media used is either an app or

website and sometimes even a phone call. The

process of ordering has to be connected to the

kitchen so as to avoid any kind of delay in food

preparation. Meals could be partially cooked

before and then prepared to give final finish

when the order is placed. This saves a lot of

time and can promise meals within scheduled

time. The last step is of delivery. The kitchen

has to be connected to the delivery team. As

soon as the food is prepared, it has to be

packed and then assigned to the delivery

person who is nearer.

Food ordering has become even more

indispensable to people working in the

corporate sector and having lesser time to

cook. The availability ranges from health food

to street food and attract different customer

segment at different times. This section

analyses the mathematical formulation and

approach for effective delivery with the use of

technological enhancements. There have been

various business models for the food-tech

industry and on which it is successfully running.

Despite the slower economic growth, home

delivery business shows greater potentials

According to report by IBEF, consumer

spending in 2015 was USD1 trillion which is

expected to reach USD 3.6 trillion by 2020 and

thus will give way to food delivery business as

well. Packaged food is among the fastest

growing segments in India and many factors

have contributed to it such as growing working

population and increasing industrialization.

According to The Indian Express, food delivery

business in India is approximated to USD 15

billion. The amount is expected to increase

further with many acquisitions and mergers

taking place in the industry. FoodPanda

acquired TastyKhana and Just Eat to increase

its market presence while Zomato acquired

Urban spoon to enter US market.

M&A’s

In today’s world, competition and

450,000630000

913500

1351980

2027970

3041955

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

2015 2016 2017 2018 2019 2020

Total Orders

Total Orders

Order48%

Self Preparation

49%

No knowledge

3%

Self-preparation vs on order

Figure 9 Total Orders- Projection- 2015-2020

Figure 10 Self Preparation vs on order food techs

We help to knit your dreams!

competitiveness are two major keywords for

measuring any company’s success. To increase

competitiveness, merger and acquisitions have

taken their way and many start-ups are now

being targeted by bigger corporates. F&B

industry is looking towards many strategic

acquisitions within India and abroad. In order

to combat unhealthy competition and to drive

more profits, M&As will become a driving force

for many companies in the segment. It will

provide consolidation to the whole market.

Food delivery business today is one of the

growing industry with increasing number of

start-ups joining the force every year. Alliance

of varied start-ups into one big corporate will

provide global competition opportunities,

rapid innovations and increasingly beneficial

services to the customers.

M&As is a general response to the strategic

movement of the industry. With the

availability of several players in the market,

union of some players will provide better

strategic movement to the industry. This will

help the companies to invest less in order to

combat competitors and provide more to the

customer through increased number of

resources. The trend is that most of the food

delivery businesses start with a focused item

but later on due to competition diversify their

portfolio. This instead of providing them a

bigger market share, takes away their USP

value as well. This can be made counter-

productive with more mergers and

acquisitions in the industry.

There have been acquisitions since 2014. The

report discusses acquisitions carried out by

two biggest players Zomato and Foodpanda.

The study done clearly demonstrates that all

the acquisitions have been done focused on

strategic expansion of the firms. Both the

companies vigorously acquired various

companies in different countries and

expanded their areas of operations through

taking over the restaurant listings.

Prior to e-commerce boom, these companies

survived by sticking to a particular region or

area but now with the advent of the boom, a

global platform has become accessible to many

firms through merger and acquisitions in

extended territories. M&As also give way to

new technologies which can increase

competitiveness of the firms. Also, for smaller

firms, it becomes profitable to merge with

larger firms, one they get an exposure and

second they get a stability in their operations.

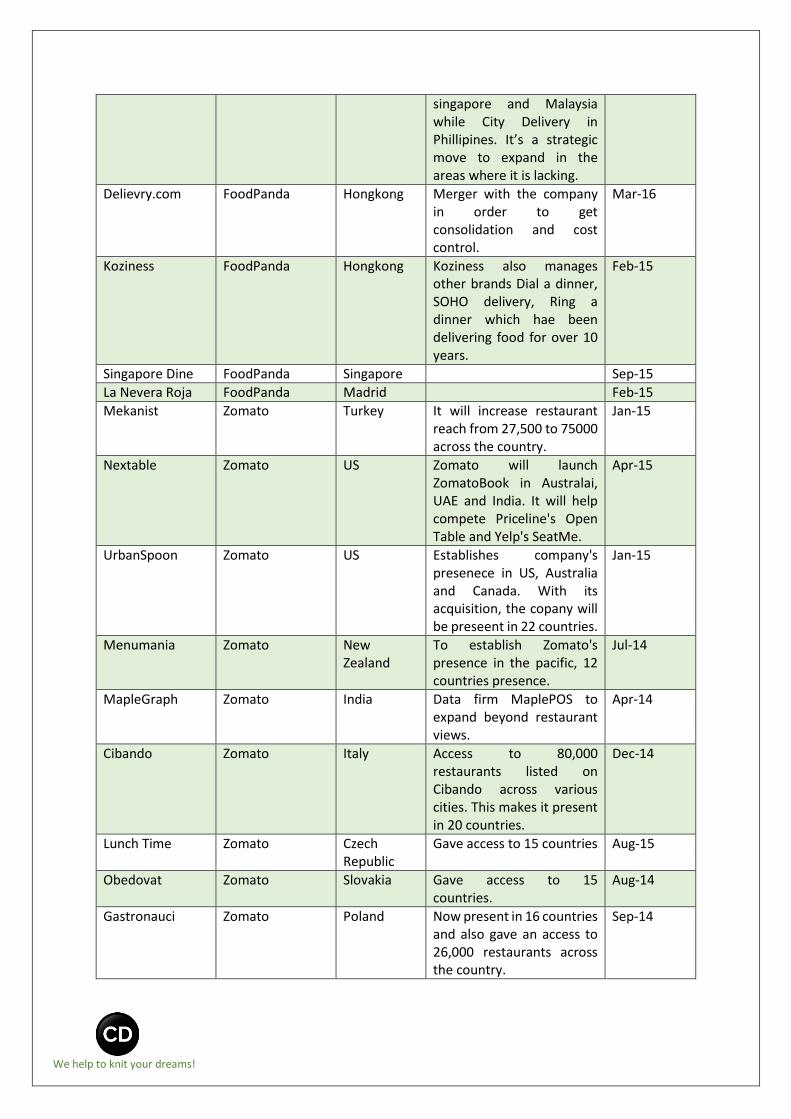

Target Acquirer Country of target

Strategy Month-Year

Just Eat India FoodPanda India Expanding market leadership.

Feb-2015

Tasty Khana FoodPanda India Together they will partner over 10,000 restaurants in India covering 173 cities.

Nov-14

Tiny Owl FoodPanda India To establish itself as a market leader in a particular region.

Aug-15

Eat Oye FoodPanda Pakistan Acquisition of rival and it will boost the number of restaurants listed on FoodPanda.

Feb-15

Delivery Club FoodPanda Moscow Acquires Russian competitor, Combination will make over 25,000 restaurants on the list.

Jun-14

Food Runner FoodPanda Manila Acquisiton of its one of the service Room Service in

Feb-15

We help to knit your dreams!

singapore and Malaysia while City Delivery in Phillipines. It’s a strategic move to expand in the areas where it is lacking.

Delievry.com FoodPanda Hongkong Merger with the company in order to get consolidation and cost control.

Mar-16

Koziness FoodPanda Hongkong Koziness also manages other brands Dial a dinner, SOHO delivery, Ring a dinner which hae been delivering food for over 10 years.

Feb-15

Singapore Dine FoodPanda Singapore Sep-15

La Nevera Roja FoodPanda Madrid Feb-15

Mekanist Zomato Turkey It will increase restaurant reach from 27,500 to 75000 across the country.

Jan-15

Nextable Zomato US Zomato will launch ZomatoBook in Australai, UAE and India. It will help compete Priceline's Open Table and Yelp's SeatMe.

Apr-15

UrbanSpoon Zomato US Establishes company's presenece in US, Australia and Canada. With its acquisition, the copany will be preseent in 22 countries.

Jan-15

Menumania Zomato New Zealand

To establish Zomato's presence in the pacific, 12 countries presence.

Jul-14

MapleGraph

Zomato India Data firm MaplePOS to expand beyond restaurant views.

Apr-14

Cibando

Zomato Italy Access to 80,000 restaurants listed on Cibando across various cities. This makes it present in 20 countries.

Dec-14

Lunch Time Zomato Czech Republic

Gave access to 15 countries Aug-15

Obedovat

Zomato Slovakia

Gave access to 15 countries.

Aug-14

Gastronauci

Zomato Poland

Now present in 16 countries and also gave an access to 26,000 restaurants across the country.

Sep-14

We help to knit your dreams!

Large companies at many places compete with

smaller ones and in order to combat the

competition, acquire or merge these regional

players. For Example, Foodpanda acquired Just

Eat India to finish its rival competition. The

unique acquisition among the above ones is

that of MapleGraph. It is basically a technology

data based firm. Zomato took a totally

strategic move and acquired it to strengthen its

technology base. The strategic drivers include

product expansion, technology expansion,

geography expansion, innovation acquisition,

consolidation and accessing capabilities.

Findings and Analysis:

In a study done over 70 food tech companies,

we shortlisted the companies on various

factors. The factors included

Number of daily orders

Social media coverage of the said company

Reviews given by customers.

General knowledge of the company among

customers

Out of 70 companies, 28 were shortlisted and

plotted on a graph to understand potential

acquirers and targets and which companies are

safe and far away from any acquisition. From

the study, it came out that Zomato and

FoodPanda are clear leaders and winners in

this game. Faasos and Travel Khana compete

them strongly and can be potential leaders.

Apart from this, companies such as Box8, Imly,

Tiny Owl and Chai Point are strong runners and

they are on the way to beat competition. If

leaders try to acquire them, it will be a costly

affair but definitely a good one since they have

a strong customer reach. Next series is of the

companies which prove to be potential targets

for acquisition. They have good customer

reach, are easy to be acquired, and can provide

growing attitude to the acquirer company.

Companies which come under this list are Bite

Club, spoon joy, FRSH, Hello Curry, Yhungry,

Holachef, Inner Chef, iTiffin and Calorie Care.

These companies hold strong position in the

market and growing rapidly since their

inception. The last category comes out to be of

the companies that are in the growing stage

and are comparatively slower in achieving the

targets. The company that belong to this list

are Bhukkad, Boibanit, FoodPort, Fitgo,

Cookaroo, iChef, Dropkaffe, Masalabox,

Mealhopper and Chai Thela.

Figure 11 Potential M&A's players table

We help to knit your dreams!

----------------------------References------------------------------------------------------------------------------------------

1. BCG, 2015, “India@Digital. Bharat”, [Available at]: <http://www.bcgindia.com/documents/file180687.pdf>

[Accessed on 28th March, 2016]

2. IBEF, 2016, “Food Processing”, [Available at]: <http://www.ibef.org/download/Food-Processing-January-

2016.pdf> [Accessed on 30th March, 2016]

3. IMF, 2014, “Women Workers in India: Why so few Among so Many?”, [Available at]:

<https://www.imf.org/external/pubs/ft/wp/2015/wp1555.pdf> [Accessed on: 28th March, 2016]

4. PwC, 2014, “Evolution of e-commerce in India- Creating the bricks behind the clicks”, [Available at]:

<https://www.pwc.in/assets/pdfs/publications/2014/evolution-of-e-commerce-in-india.pdf> [Accessed on: 21st

March, 2016]

5. KPMG, 2014, “The Indian Retail, The Next Growth Story”. [accessed on 28th March, 2016]

6. Tactful Management Research Journal, “Merger and Acquisition in e- commerce”, Available online at:

<http://tmgt.lsrj.in/UploadedArticles/189.pdf> [Accessed on: 26th April, 2016]

We help to knit your dreams!

Data Classification:

The publication does not guarantee the information provided, nor it constitutes any professional guidance. Craft Driven has put in efforts to provide most reliable information but it does not hold responsibility of the information provided. Opinions and estimates presented in the publication are subject to change with time and without notice.

Craft Driven Market Research refers to Craft Driven Technologies Pvt Ltd.

You can connect with us on:

Mobile: +91-9560847547

Email:

We help to knit your dreams!

Craft Driven Market Research Aakanksha Aggarwal

Founder Sec-10, Noida, India

Mobile: +91-9560847547 E-mail: [email protected]

We help to knit your dreams!