global commercial and civil uav market guide 2014-2015

TRANSCRIPT

2014 - 2015

Inea Consulting is a well established renewable energy advisory firm focused to emerging markets of Eastern Europe, CIS countries and MENA countries. Through its service Renewable Market WatchTM, the company provides independent renewable and commercial UAV sectors overview, customized analysis, market outlooks and sector studies. What makes us different is the quality and accuracy of information, which is interpreted in the best way to take your investment decisions. You may find relevant information our latest issued superior analysis Global Commercial and Civil UAV Market Report 2015 – 2025 here: http://renewablemarketwatch.com/country-reports

Flyver SDK enables millions of Android developers to write apps for drones... as easy as they would for a smartphone.

http://flyver.co/Drone apps platform

Tools to developMarketplace to publishPlatform to monetize

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

3

TABLE OF CONTENTS

FOREWORD ..................................................................................................................... 4

1. METHODOLOGY ..................................................................................................... 5

1.1. Methodology .............................................................................................................. 5

1.2. Limitations .................................................................................................................. 6

2. EXECUTIVE SUMMARY ........................................................................................... 7

3. WHAT IS UAV ......................................................................................................... 9

4. AVIATION REGULATIONS AND RESTRICTIONS FOR USE OF COMMERICAL AND CIVIL UAV 10

4.1. Global Legal and Regulatory Framework ................................................................. 10

4.2. European Legal and Regulatory Framework ............................................................ 11

5. GLOBAL COMMERCIAL AND CIVIL UAV MARKET ................................................... 12

5.1. Market overview ...................................................................................................... 12

5.2. Future development trends ..................................................................................... 13

6. COMPETITIVE LANDSCAPE ................................................................................... 16

6.1. Manufacturers and equipment suppliers of commercial and civil UAVs ................ 16

6.2. Software developers for commercial and civil UAVs industry ................................. 17

7. CONCLUSIONS ..................................................................................................... 18

8. LIST OF ABBREVIATIONS ...................................................................................... 21

9. REFERENCES ........................................................................................................ 22

10. DISCLAIMER ......................................................................................................... 22

LIST OF MAPS, CHARTS AND TABLES

Table 1: Classification of UAVs .................................................................................................. 9

Chart 1: Global spending on commercial and civil UAVs 2007 – 2013 (in million €) .............. 12

Chart 2: Regional breakdown of the global commercial and civil UAV market in 2013 ........ 12

Chart 3: Forecast of global spending on commercial and civil UAVs 2013 – 2015 (in million €) ................................................................................................................................................. 14

Chart 4: SWOT analysis of the global commercial and civil UAV market ............................... 14

© 2014, Inea Consulting Ltd., Manufactured in the UK; All rights reserved. Last edited on

14.10.2014

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

4

FOREWORD

Dear colleague,

It gives me great pleasure to welcome you to our latest report The Global Commercial and Civil

UAV Market Guide 2014 - 2015!

Thank you for your interest!

As we entered into an era of UAVs, international policy makers and stakeholders from all countries

must consider both the concerns and the economic potential of these new technologies. UAV

technology progressed much in the past ten years making civil and commercial applications feasible

and compelling, and the technology holds the potential to benefit citizens and industries in many

ways. In addition to its applications, UAV technology is supposed to positively impact jobs and

economic development on a global scale.

Projections of the economic impact of autonomous vehicle industries are typically generated

through the point of view of the current industry portfolios. However, similar to the Internet, UAV’s

are expected to create whole new industries. Current vehicle technologies are based on moving

people and products, whereas UAV’s will not only move people and products (and more of them),

but will perform new activities that were not feasible in the past. Most likely new activities will

involve: first responders, agricultural harvest monitoring, security, surveillance of utility grid

networks, oil and gas pipelines, heat pipelines, energy efficiency audits, wind power plant audits,

photovoltaic power plant audits, etc.

Global commercial and civil UAV industry will pressure to increase its share in the UAV global

production mix, becoming a reliable source of cost effective, energy efficient and sustainable aerial

transportation solution.

Enjoy your reading!

Yours sincerely,

Ilko Iliev

CEO

Inea Consulting Ltd.

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

5

1. METHODOLOGY

1.1. Methodology

We draw conclusions from a dataset that uses public sources, industry reports from reputable

institutions, on-site interviews, assessment from established experts and detailed review of articles

in a reputable local media, sorted by relevance and covering the last 4 years.

During the course of preparation of this analysis, most of the information was independently

verified where possible. Please note that where exact data was not available, common business

sense was applied to validate the integrity and feasibility of the information. The existing report is

in the form of a “high-level summary” quoting sources where needed. Any portion of this document

is a subject to follow-up review and further elaboration if needed. All sources, contacts, findings

and information used for the analysis have been properly identified and are available for further

work.

The methodology employed in this market study is summarized below:

1. Research and analysis of the current global political and economic climate relevant to the

development of the commercial and civil UAV industry sector;

2. Research of International and European regulations and legislative framework related to the

commercial and civil UAV industry sector;

3. Assessment of the main risks related to potential investments in the commercial and civil UAV

industry sector;

Our conclusions are based on information and data gathered through extensive industry research

including:

Industry reports from reputable institutions;

Interviews with industry stakeholders including executives and managers of companies

operating in the sector, manufacturers of UAVs, journalists and government officials;

Detailed review of articles published in the last 4 years by reputable international media.

Our forecasts for future development of the global commercial and civil UAV industry sector are

built on the basis of the following scenarios:

The “Moderate case” scenario assumes rather pessimistic market behaviour with no major

reinforcement or adequate replacement of existing national and international aviation

regulations.

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

6

The “Optimal case” scenario assumes rather realistic market behaviour with some

reinforcement or adequate replacement of existing national and international aviation

regulations. This scenario has higher probability compared to “Moderate case” and “Best case”

scenarios.

The “Best case” scenario assumes the continuation, adjustment or introduction of adequate

national and international aviation regulations, accompanied by a strong political will to

consider commercial and civil UAV industry segment as viable and important one in the

coming years. Achieving this will also require removing unnecessary administrative barriers

and streamlining aviation regulations and procedures.

Under these three scenarios, this report analyses the historical development of the global

commercial and civil UAV industry and its potential for the future.

In this bottom-up approach, consolidated forecasts should be understood as a range of possible in

global commercial and civil UAV industry market developments, with a high probability between

the “Moderate case” scenario as the lower boundary and the “Best case” scenario as the higher

one. Lower or higher forecasts are of course possible, but with a lower probability.

Currency exchange levels used in this report are as follows:

EUR/USD – 1.26894

1.2. Limitations

This market guide report does not contain descriptions of each reviewed documents. We have only

identified and discussed those documents and issues, which we regard as being material in the

context of the global commercial and civil UAV industry. The accuracy of this report is dependent

on the Reviewed Documents being true, complete, accurate and not misleading. This report is a key

issues market outlook and does not purport to provide a very detailed description of all the facts

that we have established in the course of global commercial and civil UAV industry development. It

is important to mention that we consider in our analysis only global commercial and civil UAV

industry, thus we exclude military UAV market segment from this market guide.

We have not sought or received confirmation, information or clarifications from the counterparties

to the agreements, arrangements or documents provided to us, nor from any other third party, as

to the status of such agreement, arrangement or document, the relationship between the parties

thereto or otherwise.

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

7

2. EXECUTIVE SUMMARY

This report reveals current state and future trends about global commercial and civil UAV industry.

It is intended to provide the reader with an overview on the economics and regulation of the

industry.

Aviation regulations and restrictions: Currently, the development and expansion of the UAV

market is showing that adequate regulatory framework established on a global level does not exist.

Some countries have already adopted legislation and relevant bylaws to enable operation of small

UAV’s on their territory. Canada, Australia and Brazil voted their first regulations for UAV’s between

2007 and 2011, UK in 2011, France and USA in 2012. Of course these regulations should not be

considered like fixed. They will change along with the progress and development of UAV industry.

Civil aviation has to this point been based on the notion of a pilot operating the aircraft from within

the aircraft itself and more often than not with passengers on board. Removing the pilot from the

aircraft raises important technical and operational issues, the extent of which is being actively

studied by the aviation community and addressed by ICAO regulations and guides regarding UAVs.

Current market trends: After many years of growth and innovation mainly in military segment, the

global UAV industry is now going through a challenging period, with possible increasing of market

dynamics towards wider use of UAVs for commercial and civil purposes. The current levels of

dependence on fossil fuels, the need of reducing the carbon emissions and footprint associated

with energy use and the prospects of developing a new and extremely innovative technology

sectors, make commercial and civil UAVs increasingly attractive. Small UAV’s costs are becoming

more and more competitive.

A stronger effort towards further development and technological innovation will make the

commercial and civil UAV sector more productive and competitive, and accelerate its evolution.

Nevertheless of increased competition in the last few years, the global UAV market is currently

continue to be highly compacted and consolidated with a small number of companies dominating

global sales. It is necessary to point out those positions of the current market leaders are

increasingly under pressure from newcomers and existing competitors offering a range of cost-

effective UAV capabilities and cutting edge innovative technologies.

Regional breakdown shows that North America (mainly USA) like in the past decade continues to be

leading global UAV market for 2013 with 61 % followed by Asia Pacific (APAC) with 20 %, Europe

with 17% and MENA with 2%.

Risks and challenges associated with UAVs: The inevitable global expansion of UAV’s creates some

challenges and risks: In order to operate in the national airspace of any country in the world, UAV

systems must have documentation and analysis to show that it can operate at a satisfactory level of

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

8

safety. UAV systems have higher accident rate than manned aircraft. UAV’s manufacturers and

service providers have to ensure that will not endanger security and privacy of citizens.

Development of unified international standards for licensing and medical qualification of UAV’s

crew is necessary to ensure safety operation of UAV’s in national and international air space.

Catastrophic control failure prevention and procedures especially for UAV’s operated in populated

areas should be developed in order to avoid disasters and negative impact in general. Points of

impact from catastrophic failure should be calculated reduce probability of bystander injuries and

other related damages. Legislation for operation of UAVs is missing and/or is complicated in many

countries and inadequate communication between government stakeholders’ results in

investments outflow and present obstacle for UAV industry development in those countries.

Environmentalists and community-based organizations, despite generally being in favor of

endeavors for UAV industry development, at times have radically different opinions from UAV

operators, mainly because of hazardous waste generated by UAVs.

Future market trends: Commercial and civil UAV industry is gaining positive image globally in the

recent years and enjoys increased attention and sympathy by the general public. In order to ensure

the continued wide public and political acceptance of commercial and civil UAVs, it is essential that

the UAV industry reinforces its communication on its advantages and carbon reduction credentials,

but also on its social contribution as an industry generating sustained and sustainable socio-

economic development.

Market evolution over the next few years will depend mainly on developments in USA followed by

Asia Pacific and Europe and the ability of policymakers responsive for international and national

aviation regulations to maintain market conditions at an acceptable level. A lot of new jobs are

expected to be created in the leading UAV markets. The countries where commercial and civil UAV

market has not developed until now will be interesting to follow in the coming years, because of

their untapped potential but also for the unique opportunity to witness a different market

development than what was experienced until now in the global leader USA and several European

and Asian countries.

According to analysis conducted by Inea Consulting Ltd., the current global market value of

commercial and civil UAVs under best case scenario will reach € 563.7 million in 2014 and is

expected to continue its growth to € 612.9 million in 2015.

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

9

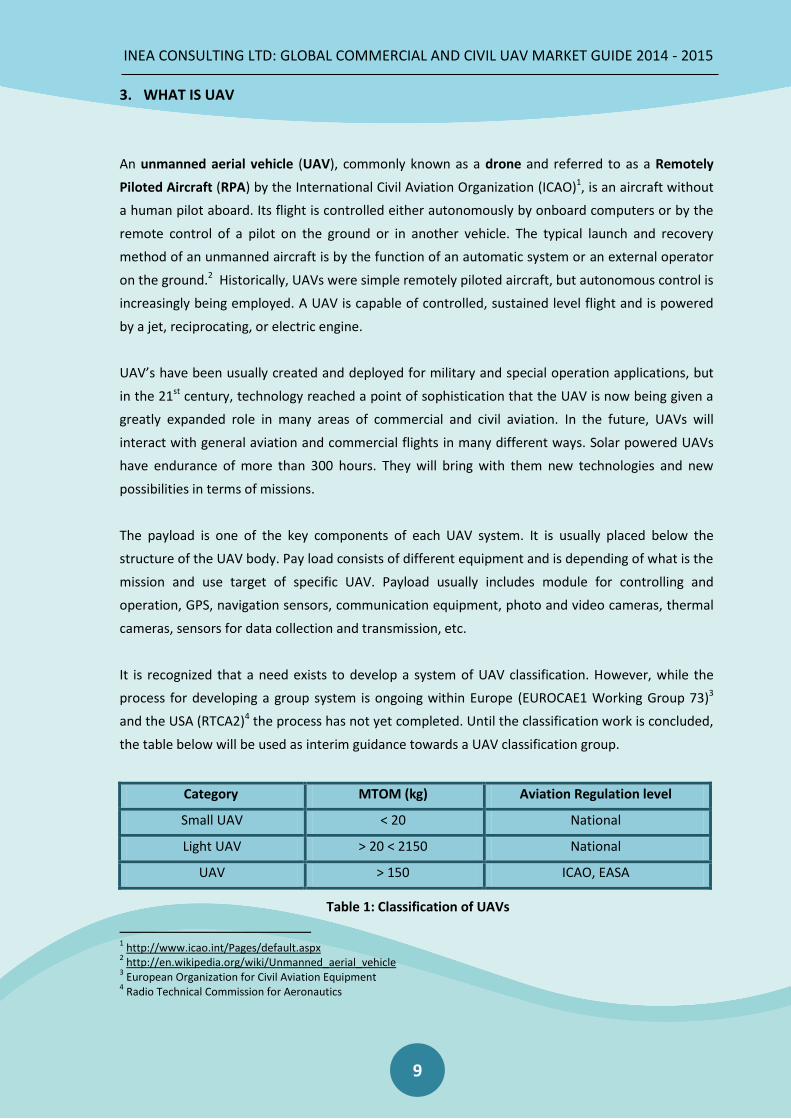

3. WHAT IS UAV

An unmanned aerial vehicle (UAV), commonly known as a drone and referred to as a Remotely

Piloted Aircraft (RPA) by the International Civil Aviation Organization (ICAO)1, is an aircraft without

a human pilot aboard. Its flight is controlled either autonomously by onboard computers or by the

remote control of a pilot on the ground or in another vehicle. The typical launch and recovery

method of an unmanned aircraft is by the function of an automatic system or an external operator

on the ground.2 Historically, UAVs were simple remotely piloted aircraft, but autonomous control is

increasingly being employed. A UAV is capable of controlled, sustained level flight and is powered

by a jet, reciprocating, or electric engine.

UAV’s have been usually created and deployed for military and special operation applications, but

in the 21st century, technology reached a point of sophistication that the UAV is now being given a

greatly expanded role in many areas of commercial and civil aviation. In the future, UAVs will

interact with general aviation and commercial flights in many different ways. Solar powered UAVs

have endurance of more than 300 hours. They will bring with them new technologies and new

possibilities in terms of missions.

The payload is one of the key components of each UAV system. It is usually placed below the

structure of the UAV body. Pay load consists of different equipment and is depending of what is the

mission and use target of specific UAV. Payload usually includes module for controlling and

operation, GPS, navigation sensors, communication equipment, photo and video cameras, thermal

cameras, sensors for data collection and transmission, etc.

It is recognized that a need exists to develop a system of UAV classification. However, while the

process for developing a group system is ongoing within Europe (EUROCAE1 Working Group 73)3

and the USA (RTCA2)4 the process has not yet completed. Until the classification work is concluded,

the table below will be used as interim guidance towards a UAV classification group.

Category MTOM (kg) Aviation Regulation level

Small UAV < 20 National

Light UAV > 20 < 2150 National

UAV > 150 ICAO, EASA

Table 1: Classification of UAVs

1 http://www.icao.int/Pages/default.aspx

2 http://en.wikipedia.org/wiki/Unmanned_aerial_vehicle

3 European Organization for Civil Aviation Equipment

4 Radio Technical Commission for Aeronautics

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

10

4. AVIATION REGULATIONS AND RESTRICTIONS FOR USE OF COMMERICAL AND CIVIL UAV

4.1. Global Legal and Regulatory Framework

Currently, the development and expansion of the UAV market is showing that adequate regulatory

framework established on a global level does not exist. Some countries have already adopted

legislation and relevant bylaws to enable operation of small UAV’s on their territory.

Canada, Australia and Brazil voted their first regulations for UAV’s between 2007 and 2011, UK in

2011, France and USA in 2012. Of course these regulations should not be considered like fixed.

They will change along with the progress and development of UAV industry.

Civil aviation has to this point been based on the notion of a pilot operating the aircraft from within

the aircraft itself and more often than not with passengers on board. Removing the pilot from the

aircraft raises important technical and operational issues, the extent of which is being actively

studied by the aviation community and addressed by ICAO regulations and guides regarding UAVs.

The International Civil Aviation Organization (ICAO) is a UN specialized agency, created in 1944

upon the signing of the Convention on International Civil Aviation (Chicago Convention). ICAO

works with the Convention’s 191 Member States and global aviation organizations to develop

international Standards and Recommended Practices (SARPs) which States reference when

developing their legally-enforceable national civil aviation regulations.

UAV’s are a new component of the aviation system, one which ICAO, countries in the world and the

aerospace industry are working to understand, define and ultimately integrate. These systems are

based on cutting edge developments in aerospace technologies, offering advancements which may

open new and improved civil/commercial applications as well as improvements to the safety and

efficiency of all civil aviation. The safe integration of UAV’s into non-segregated airspace will be a

long-term activity with many stakeholders adding their expertise on such diverse topics as licensing

and medical qualification of UAV’s crew, technologies for detect and avoid systems, frequency

spectrum (including its protection from unintentional or unlawful interference), separation

standards from other aircraft, and development of a robust regulatory framework.

The goal of ICAO in addressing unmanned aviation is to provide the fundamental international

regulatory framework through Standards and Recommended Practices (SARPs), with supporting

Procedures for Air Navigation Services (PANS) and guidance material, to underpin routine operation

of UAV’s throughout the world in a safe, harmonized and seamless manner comparable to that of

manned operations. This circular is the first step in reaching that goal. ICAO anticipates that

information and data pertaining to UAV’s will evolve rapidly as States and the aerospace industry

advance their work. This circular therefore serves as a first snapshot of the subject.

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

11

4.2. European Legal and Regulatory Framework

In December2013, the European Council asked the European Commission to develop a framework

for the safe integration of drones into civil air space as from 2016.

EC Regulation 216/2008 (the Basic EASA Regulation) establishes the European Aviation Safety

Agency (EASA) and makes provision for Implementing Rules dealing with airworthiness certification,

continuing airworthiness, operations, pilot licensing, air traffic management and aerodromes.

Neither the Basic EASA Regulation nor the Implementing Rules apply to aircraft carrying out

military, customs, police, search and rescue, firefighting, coastguard or similar activities or services

(State aircraft). EU Member States must, however, ensure that such services have due regard as far

as practicable to the objectives of the EASA Regulation.

Certain categories of civil aircraft are also exempt from the need to comply with the Basic EASA

Regulation and its Implementing Rules. These exempt categories are listed in Annex II to the Basic

EASA Regulation (Annex II aircraft). The exempt categories which are of relevance for UAV are:

aircraft specifically designed or modified for research, experimental or scientific purposes and

likely to be produced in very limited numbers;

ex-military aircraft; and

unmanned aircraft (UAV) with an operating mass of 150 kg or less.

Any aircraft which is subject to the Basic EASA Regulation and Implementing Rules (e.g. an

unmanned aircraft more than 150 kg which is neither experimental nor used for State purposes)

will be required to have an EASA airworthiness certificate. An aircraft which is not required to

comply with the Basic EASA Regulation, either because it is a State aircraft or because it comes

within one of the exempt categories, remains subject to national regulation so far as airworthiness

certification and continuing airworthiness are concerned.

Implementing Rules for airworthiness certification and continuing airworthiness have been in force

for some years. Implementing Rules for operations, pilot licensing, air traffic management and

aerodromes came into force during the course of 2012 and 2013. EC Regulation 785/2004 came

into force on 30 April 2005 requiring most operators of aircraft, irrespective of the purposes for

which they fly, to hold adequate levels of insurance in order to meet their liabilities in the event of

an accident. This EC Regulation specifies amongst other things the minimum levels of third party

accident and war risk insurance for aircraft operating in to, over or within the EU (including UAS)

depending on their Maximum Take-Off Mass (MTOM). The EC Insurance Regulation does not apply

to State aircraft or to model aircraft with an MTOM of less than 20 kg.

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

12

5. GLOBAL COMMERCIAL AND CIVIL UAV MARKET

5.1. Market overview

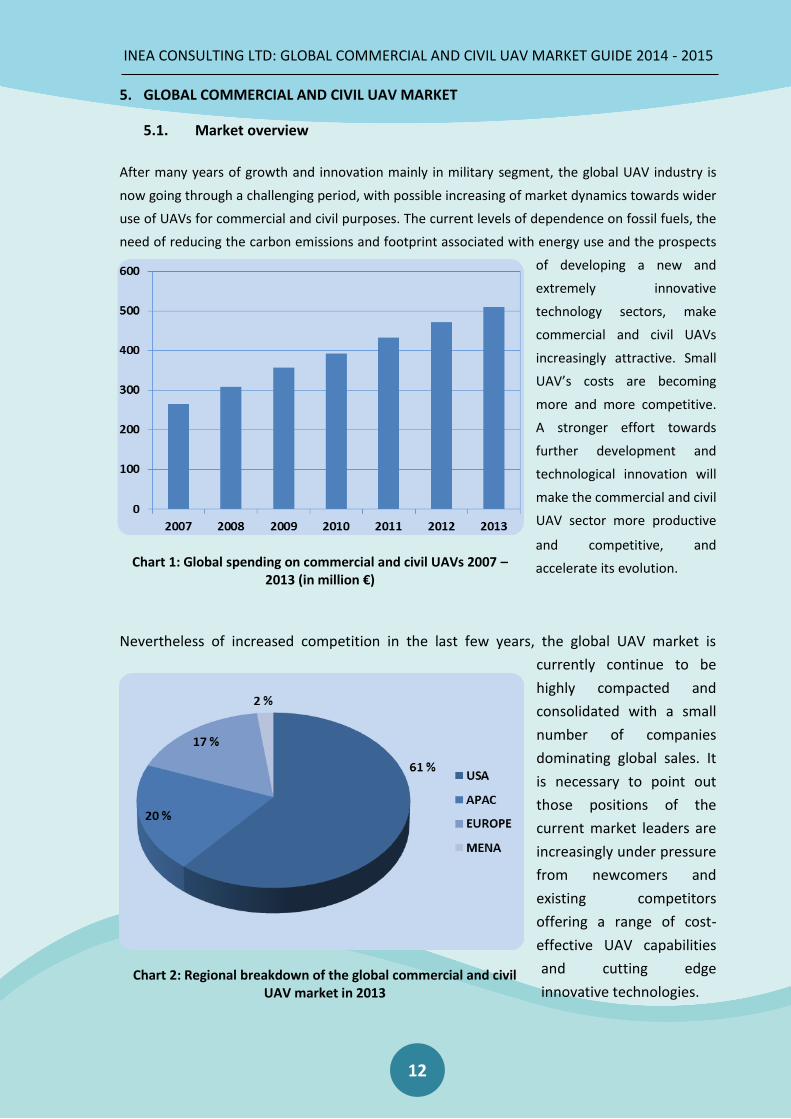

After many years of growth and innovation mainly in military segment, the global UAV industry is

now going through a challenging period, with possible increasing of market dynamics towards wider

use of UAVs for commercial and civil purposes. The current levels of dependence on fossil fuels, the

need of reducing the carbon emissions and footprint associated with energy use and the prospects

of developing a new and

extremely innovative

technology sectors, make

commercial and civil UAVs

increasingly attractive. Small

UAV’s costs are becoming

more and more competitive.

A stronger effort towards

further development and

technological innovation will

make the commercial and civil

UAV sector more productive

and competitive, and

accelerate its evolution.

Nevertheless of increased competition in the last few years, the global UAV market is

currently continue to be

highly compacted and

consolidated with a small

number of companies

dominating global sales. It

is necessary to point out

those positions of the

current market leaders are

increasingly under pressure

from newcomers and

existing competitors

offering a range of cost-

effective UAV capabilities

and cutting edge

innovative technologies.

Chart 1: Global spending on commercial and civil UAVs 2007 – 2013 (in million €)

Chart 2: Regional breakdown of the global commercial and civil UAV market in 2013

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

13

Regional breakdown for 2013 shows that North America (mainly USA) like in the past decade

continues to be leading global commercial and civil UAV market for 2013 with 61 % followed by Asia

Pacific (APAC) with 20 %, Europe with 17% and MENA with 2%.

However there are only two known cases of commercial drone licenses having been granted in the

USA. One is for oil British Petroleum and the other for six film companies based in Hollywood,

California. Both were the result of heavy lobbying. One from BP themselves and the other from the

Motion Picture Association of America on behalf of its subcontractors. Otherwise, commercial use

of drones is largely inaccessible to small and medium-sized business owners in the USA, because of

limiting legislation.

Canada is one of the leaders in commercial applications for drones, largely because of its

progressive legislation. Drones are already being used in Canada for monitoring of piping and power

lines, as well as various other uses including crop monitoring.

The UK was also one of the first countries to pass drone legislation and this has given it an

advantage in implementing drones for commercial uses. It is being sued there as well in order to

monitor various public and private properties.

Commercial and civil UAV industry is gaining positive image globally in the recent years and enjoys

increased attention and sympathy by the general public. The rapid development of the industry has

recently put UAVs increasingly under the spotlight and, on many occasions, competing interests

have challenged the commercial and civil UAV industry in many respects. In order to ensure the

continued wide public and political acceptance of commercial and civil UAVs, it is essential that the

UAV industry reinforces its communication on its advantages and carbon reduction credentials, but

also on its social contribution as an industry generating sustainable socio-economic development.

The multi-faceted value of UAV technology resulting from the multiple applications and services it

can provide must also be communicated to the wider public and deny emerging misconceptions

about its limitations.

5.2. Future development trends

Market evolution over the next few years will depend mainly on developments in USA followed by

Asia Pacific and Europe and the ability of policymakers responsive for international and national

aviation regulations to maintain market conditions at an acceptable level. A lot of new jobs are

expected to be created in the leading UAV markets. The countries where commercial and civil UAV

market has not developed until now will be interesting to follow in the coming years, because of

their untapped potential but also for the unique opportunity to witness a different market

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

14

development than what was experienced until now in the global leader USA and several European

and Asian countries.

Chart 3: Forecast of global spending on commercial and civil UAVs 2013 – 2015 (in million €)

According to analysis conducted by Inea Consulting Ltd., the current global market value of

spending on commercial and civil UAVs under best case scenario will reach € 563.7 million in 2014

and is expected to continue its growth to € 612.9 million in 2015. Global UAV market, which is

dominated by its military segment, is possible to face pressure for structural and competitive

changes as a result of the emerging commercial and civil UAV market.

Chart 4: SWOT analysis of the global commercial and civil UAV market

Some of the current leading players in the global UAV market (including military segment) will

specialize within the commercial and civil UAV market, concentrating on key technologies, features

and services to maximize sales and increase their share in this increasingly competitive market

segment. Newcomers and start-up companies bringing technological innovations and know-how,

€ 509.5 2013 € 563.7 F 2014 € 612.9 F 2015

STRENGHTS

- Cost effective aerial transportation

- Carbon footprint reduction

- Access to remote areas

- Technological innovations driven market

WEAKNESSES

- Global aviation regulations need improvement

- Lack of unified international standards about crew certification, medical qualification ,etc.

- High R & D cost of UAVs equipped with the necessary specialized equipment

OPPORTUNITIES

- New emerging market

- Development of new UAV based services

- Market place for UAV software and SDK

- Flight endurance increase with solar power

THREATS

- Slow harmonizarion process of global aviation regulations for UAV operation

- New technology, which is not well tested and may have higher failure rate

- Strong influence of NGO's and social organizations

SWOT

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

15

will also threat positions of the current market leaders, who will have to adapt their business

models and strategies to rapidly shifting market dynamics of commercial and civil UAV industry.

Therefore the global commercial and civil UAV market is estimated to grow in 2014 – 2015.

However strong political willpower is needed to build confidence in market players and industry

participants, to establish solid ground for future growth, remove bottlenecks and maintain a

reliable but dynamic national and international regulatory framework for development and

commercial and civil use of UAV systems. Global commercial and civil UAV market will be volatile in

the near future, mostly influenced by the uncertain legal and regulatory framework governing

commercial and civil UAVs use.

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

16

6. COMPETITIVE LANDSCAPE

6.1. Manufacturers and equipment suppliers of commercial and civil UAVs

In this chapter we present brief selection about some of the most important manufacturers and

equipment suppliers of commercial and civil UAVs.

3D Robotics5 develops innovative, flexible and reliable personal drones and UAV technology for

everyday exploration and business applications. DR’s UAV platforms capture breathtaking aerial

imagery for consumer enjoyment and data analysis, enabling mapping, surveying, 3D modeling and

more. Our technology is currently used across multiple industries around the world, including

agriculture, photography, construction, search and rescue and ecological study.

senseFly Ltd6 is a Swiss company based in Cheseaux-Lausanne. senseFly develops, assembles and

markets autonomous mini-drones and related software solutions for civil professional applications

such as accurate mapping of mining sites, quarries, forests, construction sites, crops, etc. Since

summer 2012 senseFly is a member of the Parrot group.7

Aibotix8 since February 2014 is part of Hexagon (NASDAQ OMX Stockholm: HEXA B), a leading

global provider of integrated design, measurement and visualization technologies. As part of this

global network, it benefits from the expertise of other renowned brands such as Leica Geosystems,

Intergraph and Tridicon, with whom it works closely and jointly develops solutions.

DJI Innovations9 is the global leader in developing and manufacturing high performance, reliable,

and easy to use small UAV systems, for commercial and recreational use. The company has over

500 employees, and is among the largest in the commercial UAV market. It is dedicated to making

aerial photography and videography accessible to professional photographers, cinematographers

and hobbyists anywhere. Global company operations span to North America, Europe and Asia.

Walkera with the concept of "Walking in Era and Towing the Trend", replying on its strong research

& development ability, and manufacturing capacity, Guangzhou Walkera Technology CO., LTD. has

become a professional commercial UAV manufacturer that unifies product research &

development, production, marketing, and service.10

5 http://3drobotics.com/about-us/

6 https://www.sensefly.com/about/company-profile.html

7 http://www.parrot.com/usa/

8 http://www.aibotix.com/about-aibotix.html

9 http://www.dji.com/company

10 http://www.walkera.com/en/article.php?id=5&cat_id=2

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

17

6.2. Software developers for commercial and civil UAVs industry

In this chapter we present a brief selection of some of the most important software developers and

for the commercial and civil UAVs industry.

Proprietary software

Many companies create proprietary software like controllers for their own devices. Most of it is not

accessible by third parties and developers. Industry shows first signs of open software and open

interfaces for drones.

DroneDeploy11 is a company focusing on developing software that adapts drones for businesses

and industrial purposes. It enables cloud control for drones by connecting them to LTE and 3G

networks. The main sectors it focuses on are construction, agriculture and surveying.

Airware12 is a combination of software running on a hardware unit controlling the main functions of

the drone, providing connectivity to a third party sensors and external devices.

Open software

Flyver13 is among the first companies providing open interface to drones aimed to developers. It

enables them to write designated apps for drones. Flyver announced its public marketplace for

drone apps developed by independent developers where drone owners can download and run

Android based apps created for drones.

Parrot is among the companies providing documented interface to certain parts of their software

allowing users to develop their own applications for Parrot’s flagship drone product – Parrot

Ar.Drone.

ArduPilot/APM a project by 3D Robotics is an open source autopilot system supporting multi-

copters, traditional helicopters, fixed wing aircraft and rovers. The Project clone APM:Copter is

designated specifically for rotary wing multicopter vehicles.

OpenDroneControl is an open source software platform for developing interactive artworks and

research projects with aerial robotics. ODC was developed to be a community-supported

framework for connecting commercially available quadcopter platforms to a common programming

interface. The framework provides access to platform specific sensors and optionally allows for

additional functionality such as navigation and tracking.

11

https://www.dronedeploy.com 12

http://airware.com 13

http://flyver.co/

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

18

7. CONCLUSIONS

This report analyzed the economics, the public policy, and the regulatory risks in the global

commercial and civil UAV sector, which remains the promising industry for the period 2014 - 2015.

Uncertainty about new and expanding markets for UAV technology makes it difficult to predict

economic impact by extrapolating data from existing related industries. The brief economic analysis

presented here is preliminary and conservative, but provides pretty enough insight regarding

growth potential of global UAV market. Our analysis based on primary-source information,

interviews, case studies, and desk research finds the following advantages and problems:

The Importance of Balanced Global Regulation Policy about UAVs

While UAV’s have evolved into a technology that can serve a variety of industries, many

stakeholders have operated without a clear understanding of regulatory policy—partially because

the policy is underdeveloped. Now that the technology is moving into the public consciousness,

many believe that law enforcement on international level is the critical focal point, and requires the

most attention because of privacy concerns. In reality, there are also many commercial interests

attention. Across the nations in different countries, law enforcement is calling for clear and

appropriate guidelines concerning when they can and cannot use this important, potentially life-

saving technology, in the pursuit of suspects.14

For all the above reasons is important international policy makers and stakeholders from all

countries to organize meetings, workshops and conferences and to develop finally clear and

reliable legislation for UAV that will not change frequently. Therefore today’s policy decisions and

their adequacy to the UAV industry requirements could have an enormous impact on economy of

UAV market in the next few years and beyond. Aviation administrations in many countries currently

allows UAV’s to fly in their national airspace only by exception, however plans to move from

accommodation of UAV’s to integration, enabling a variety of new commercial and civil applications

are existing in USA, UK, France, Germany, Canada and other countries.

The production and use of UAVs are increasing every day throughout the world. While the United

States and Israel were the sole producers of UAVs only 15 years ago, today China, Russia, Iran,

Australia, Brazil, Germany, Turkey, and Canada have stepped up their development programs and

have begun exporting systems internationally. Commercially successful platforms such as Northrop

Grumman’s Global Hawk, General Atomics’ Predator, AAI’s Shadow, and Boeing/Insitu’s ScanEagle

and Firescout UAS have been joined by a host of foreign-developed platforms. These include

Turkey’s Anka, Europe’s nEUROn, Australia’s Campcopter-S, and South Africa’s Seeker 400, which

14

Darryl Jenkins & Bijan Vasigh, The Economic Impact of Unmanned Aircraft Systems Integration in the United States,

Association for Unmanned Vehicle Systems (2013)

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

19

offer similar capabilities at lower costs regionally.15 As developers and prospective customers seek

to deploy autonomous aerial transportation in useful new ways, then policy makers have to take

decisions that can accelerate the pace of innovation and growth in UAV industry. This will result in

attracting new companies to engage with production in UAV industry and creating many jobs.

The attractive economics of the investment. Competition continues to grow as the countries

looking to develop high paying, high-tech manufacturing jobs see unmanned aircraft as a unique

opportunity to enter into both commercial and military environments—offering products that can

be used in multiple roles for domestic and international missions.

Future market trends

Because UAV’s have captured the public’s imagination, striving to a leadership position in this

industry will fit well on a technological and economic progress in the countries, which have

developed national strategies to support UAV industry development.

Commercial and civil UAV industry is gaining positive image globally in the recent years and enjoys

increased attention and sympathy by the general public. In order to ensure the continued wide

public and political acceptance of commercial and civil UAVs, it is essential that the UAV industry

reinforces its communication on its advantages and carbon reduction credentials, but also on its

social contribution as an industry generating sustained and sustainable socio-economic

development.

Market evolution over the next few years will depend mainly on developments in USA followed by

Asia Pacific and Europe and the ability of policymakers responsive for international and national

aviation regulations to maintain market conditions at an acceptable level. A lot of new jobs are

expected to be created in the leading UAV markets. The countries where commercial and civil UAV

market has not developed until now will be interesting to follow in the coming years, because of

their untapped potential but also for the unique opportunity to witness a different market

development than what was experienced until now in the global leader USA and several European

and Asian countries.

Projections of the economic impact of autonomous vehicle industries are typically generated

through the point of view of the current industry portfolios. However, similar to the Internet, UAV’s

are expected to create whole new industries. Current vehicle technologies are based on moving

people and products, whereas UAV’s will not only move people and products (and more of them),

but will perform new activities that were not feasible in the past. Most likely new activities will

involve: first responders, agricultural harvest monitoring, security, surveillance of utility grid

15

HIS Jane’s UAVs 2012

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

20

networks, oil and gas pipelines, heat pipelines, energy efficiency audits, wind power plant audits,

photovoltaic power plant audits, etc.

Risks and challenges associated with UAVs. The inevitable global expansion of UAV’s creates some

challenges and risks: In order to operate in the national airspace of any country in the world, UAV

systems must have documentation and analysis to show that it can operate at a satisfactory level of

safety. UAV systems have higher accident rate than manned aircraft. UAV’s manufacturers and

service providers have to ensure that will not endanger security and privacy of citizens.

Development of unified international standards for licensing and medical qualification of UAV’s

crew is necessary to ensure safety operation of UAV’s in national and international air space.

Catastrophic control failure prevention and procedures especially for UAV’s operated in populated

areas should be developed in order to avoid disasters and negative impact in general. Points of

impact from catastrophic failure should be calculated reduce probability of bystander injuries and

other related damages. Legislation for operation of UAVs is missing and/or is complicated in many

countries and inadequate communication between government stakeholders’ results in

investments outflow and present obstacle for UAV industry development in those countries.

Environmentalists and social community-based organizations, despite generally being in favor of

endeavors for UAV industry development, at times have radically different opinions from UAV

operators, mainly because of hazardous waste generated by UAVs and because of privacy

protection of citizens.

Geopolitical environment. One of the key issues for the UAV industry is the global geopolitical

situation. Geographical location of countries, their economic development and historical traditions

often result in conflicts of interests. Development, progress and penetration of UAV is inevitable,

but the findings of this report suggest that all participants in this industry are currently expecting

predictable legislative and administrative regulations on their national level and on the

international level as well. It is obvious that governments of some countries like Australia, Canada,

Brazil, France, UK and USA are taking more effective steps towards regulations of UAV industry.

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

21

8. LIST OF ABBREVIATIONS

Some of the following abbreviations and definitions are used throughout this market guide:

Aircraft (ICAO) Any machine that can derive support in the atmosphere from the

reactions of the air other than the reactions of the air against the

Earth’s surface

AGL Above Ground Level

AUVSI Association for Unmanned Vehicle Systems International

CAA Civil Aviation Authorities

GPS Global Positioning System

GIS Geographic Information System

HALE High Altitude Long Endurance

MAV Micro Air Vehicle

MTOM (MTOW) Maximum Take-Off Mass/Weight

MALE Medium altitude long endurance

EASA European Aviation Safety Agency

EUROCONTROL European Organisation for the Safety of Air Navigation

ICAO International Civil Aviation Organisation

R&D Research and development

RPV Remotely Piloted Vehicles

SUAV Small unmanned aerial vehicle

UAS Unmanned Aircraft System

UAV Unmanned Aerial Vehicle

INEA CONSULTING LTD: GLOBAL COMMERCIAL AND CIVIL UAV MARKET GUIDE 2014 - 2015

22

9. REFERENCES

1. Transnational Institute (NL) and Statewatch UK 2014. Report about Eurodrones.

2. STIMSON 2014. Report of the task force on USA drone policy.

3. Uncork-It Communications 2014. The future of unmanned vehicle systems in Virginia

4. AUVSI 2013. The economic impact of unmanned aircraft systems integration in the USA

5. Strategy for European Union 2012. Towards the development of civil applications of

unmanned aircraft systems (UAS)

6. ICAO Cir 328, ICAO 2011. Unmanned Aircraft Systems (UAS), ISBN 978-92-9231-751-5

7. Commercial Aviation Authority of UK 2011. CAP 722 - Unmanned Aircraft System Operations in

UK Airspace – Guidance

8. European Commission/EASA 2008. UAV Task-Force Final Report

9. European Commission 2005. European Civil Unmanned Air Vehicle Roadmap

10. DISCLAIMER

This market guide contains important information. Please read it carefully before investing and

keep it for future reference. No financial adviser, dealer, salesperson or any other person has been

authorized to give any information or to make any representations, other than those contained in

this document, in connection with the contents of this market guide and, if given or made, such

other information or representations must not be relied on as having been authorized by official

representatives of Inea Consulting Ltd. The information contained herein has been obtained from

sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, we

cannot guarantee it. No responsibility is assumed for any inaccuracies. All used pictures, trademarks

and data sources belong to their owners. Readers and investors are encouraged to consult their

professional advisors prior to acting on any of the material contained in this document. With the

progress of the global commercial and civil UAV market development, this publication is supposed

to have new editions. Please contact officials of Inea Consulting Ltd. in order to be sure you read

the latest document version.

© 2014, Inea Consulting Ltd., Manufactured in the UK; All rights reserved. Last edited on 14.10.2014

UK

4, Lowndes street

London, SW1X 9ET

+44 (0) 203 60 80 138

FRANCE

30, Avenue des Alpes

Roquefort Les Pins, 06330

+33 (0) 681 477 658

AUSTRIA

10 b, St. Peter Gurtel 8042 Graz +43 (0) 664 2233 449 [email protected]

ITALY

39, Corso Don Giovanni Minzoni

00045 Genzano di Roma (RM)

+39 (0) 340 4124 602

BULGARIA

9, Maria Louisa Blvd., 3rd floor

9000 Varna

++359 (0) 896 833 044

NETHERLANDS

21, Bezuidenhoutseweg

2594AB The Hague

++31 (0) 684 488 601

GERMANY

9, Randsiedlung, 09235 Burkhardtsdorf

++49 (0) 173 261 4462

OAE, Dubai

Sheikh Zayed Road

Umm Suqaem Building, office 116