inventory control 1 copyright 1999 prentice hall publishing company managing inventory

TRANSCRIPT

Inventory ControlInventory Control 11Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Managing InventoryManaging Inventory

Inventory ControlInventory Control 22Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Managing Inventory Involves...Managing Inventory Involves...

Developing an accurate sales forecast.Developing an accurate sales forecast. Developing a plan to make inventory Developing a plan to make inventory

available when and where customers want available when and where customers want it.it.

Building relationships with quality Building relationships with quality suppliers.suppliers.

Setting realistic inventory turnover Setting realistic inventory turnover objectives.objectives.

Inventory ControlInventory Control 33Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Managing Inventory Involves...Managing Inventory Involves...

Computing the cost of carrying inventory.Computing the cost of carrying inventory. Using the most timely and accurate Using the most timely and accurate

information system the business can information system the business can afford to provide everyone with vital afford to provide everyone with vital inventory information.inventory information.

Teaching employees how inventory Teaching employees how inventory control systems work so they can help control systems work so they can help manage inventory on a daily basis.manage inventory on a daily basis.

Inventory ControlInventory Control 44Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Pareto’s LawPareto’s Law Business owners must recognize the Business owners must recognize the

importance of Pareto’s Law (the 80/20 importance of Pareto’s Law (the 80/20 Rule): About 80% of a firm’s sales are Rule): About 80% of a firm’s sales are generated by about 20% of the items in generated by about 20% of the items in its inventory. its inventory.

The goal of inventory control is to focus The goal of inventory control is to focus the majority of the effort on that 20% of the majority of the effort on that 20% of the inventory. the inventory.

Inventory ControlInventory Control 55Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Inventory Control SystemsInventory Control Systems Perpetual inventory systemsPerpetual inventory systems

Point-pf-sale (POS) systemsPoint-pf-sale (POS) systems Sales ticket methodSales ticket method Sales stub methodSales stub method Punch card methodPunch card method Floor sample methodFloor sample method

Visual inventory systemsVisual inventory systems Partial inventory systemsPartial inventory systems

ABC methodABC method "Just-In-Time" techniques"Just-In-Time" techniques

Inventory ControlInventory Control 66Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

ABC MethodABC Method

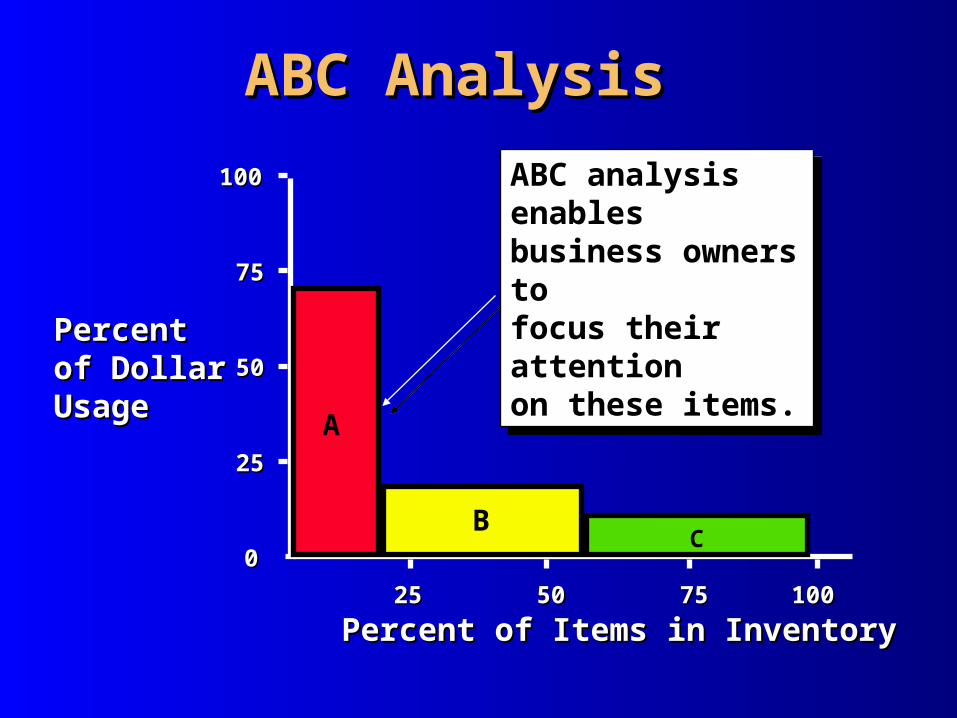

The ABC technique focuses inventory control efforts on The ABC technique focuses inventory control efforts on the small percentage of items that account for the the small percentage of items that account for the majority of the firm’s sales.majority of the firm’s sales.

A items A items - items accounting for a large dollar usage - items accounting for a large dollar usage volumevolume (Approximately the top 15% of items). (Approximately the top 15% of items).

B items B items - items accounting for a moderate dollar usage - items accounting for a moderate dollar usage volume (Approximately the next 35% of items).volume (Approximately the next 35% of items).

C items C items - items accounting for a low dollar usage - items accounting for a low dollar usage volume (Approximately the remaining 50% of items).volume (Approximately the remaining 50% of items).

100100

5050

00

PercentPercentof Dollarof DollarUsageUsage

7575

2525

Percent of Items in InventoryPercent of Items in Inventory

A

BC

2525 5050 7575 100100

ABC analysis enables business owners to focus their attentionon these items.

ABC analysis enables business owners to focus their attentionon these items.

ABC AnalysisABC Analysis

Inventory ControlInventory Control 88Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

ABC Inventory ControlABC Inventory ControlThe purpose of classifying items (A, B, or C) is to establish The purpose of classifying items (A, B, or C) is to establish

the proper degree of control over each item in inventory.the proper degree of control over each item in inventory. A items A items - Strict control; Perpetual inventory control - Strict control; Perpetual inventory control

systems.systems. B items B items - Moderate control; Periodic control systems - Moderate control; Periodic control systems

using EOQ and reorder point analysis.using EOQ and reorder point analysis. C items C items - Minimal control; Simple, inexpensive control - Minimal control; Simple, inexpensive control

systems such as the two-bin or tag systems. Many systems such as the two-bin or tag systems. Many businesses carry large levels of safety stock of C items businesses carry large levels of safety stock of C items where carrying costs are low.where carrying costs are low.

Inventory ControlInventory Control 99Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Just-In-Time TechniquesJust-In-Time Techniques JIT attempts to reduce the investment JIT attempts to reduce the investment

required in inventory because it drains a required in inventory because it drains a company’s cash and hides a multitude of company’s cash and hides a multitude of problems managers need to address.problems managers need to address.

The goal is to achieve a smooth flow of The goal is to achieve a smooth flow of materials and inventory through the business.materials and inventory through the business.

Rather than build up costly stockpiles of Rather than build up costly stockpiles of inventory, JIT seeks to get items where they inventory, JIT seeks to get items where they are needed “just in time.”are needed “just in time.”

Inventory ControlInventory Control 1010Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Benefits of JITBenefits of JIT

Lower investment in inventory.Lower investment in inventory. Reduced inventory carrying and handling Reduced inventory carrying and handling

costs.costs. Reduced costs resulting from obsolete Reduced costs resulting from obsolete

inventory.inventory. Smaller investment in inventory storage space.Smaller investment in inventory storage space. Reduced manufacturing costs as a result of Reduced manufacturing costs as a result of

improved coordination among departments.improved coordination among departments.

Inventory ControlInventory Control 1111Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

JIT IIJIT II JIT II techniques focus on creating a closer, more JIT II techniques focus on creating a closer, more

harmonious relationship with a company’s harmonious relationship with a company’s suppliers so that both benefit from increased suppliers so that both benefit from increased efficiency. efficiency.

JIT II is “empowerment of the supplier within the JIT II is “empowerment of the supplier within the customer’s organization.” --Lance Dixoncustomer’s organization.” --Lance Dixon

In a retail environment, JIT II principles are called In a retail environment, JIT II principles are called Efficient Consumer Response Efficient Consumer Response (ECR), which enable (ECR), which enable retailers to replenish their inventories constantly retailers to replenish their inventories constantly and on an as-needed basis. and on an as-needed basis.

Inventory ControlInventory Control 1212Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Protecting Inventory from Protecting Inventory from TheftTheft

Businesses lose an estimated $400 billion Businesses lose an estimated $400 billion annually to criminals.annually to criminals.

Small businesses are more susceptible t Small businesses are more susceptible t crime than large companies. crime than large companies.

Two biggest criminal threats to small Two biggest criminal threats to small businesses are employee theft and businesses are employee theft and shoplifting. shoplifting.

Inventory ControlInventory Control 1313Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Employee Theft...Employee Theft... The greatest criminal threat to small The greatest criminal threat to small

businesses comes from businesses comes from insideinside. . 30 percent of all employees are “hard-core 30 percent of all employees are “hard-core

pilferers.”pilferers.” Is more common in small companies, Is more common in small companies,

where control and security measures are where control and security measures are less stringent. less stringent.

Is more pervasive than most owners think.Is more pervasive than most owners think.

Inventory ControlInventory Control 1414Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Reasons For Employee Reasons For Employee TheftTheft

The trusted employeeThe trusted employee Disgruntled employeesDisgruntled employees Organizational atmosphereOrganizational atmosphere Physical breakdownsPhysical breakdowns Improper cash controlImproper cash control

Inventory ControlInventory Control 1515Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Factors Encouraging Factors Encouraging Employee TheftEmployee Theft

The need or desire to steal.The need or desire to steal. A rationalization for the act.A rationalization for the act. The opportunity to steal.The opportunity to steal. The perception that there is a low The perception that there is a low

probability of being caught.probability of being caught.

Inventory ControlInventory Control 1616Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Preventing Employee TheftPreventing Employee Theft

Screen employees carefully.Screen employees carefully. Create an environment of honesty.Create an environment of honesty. Establish a system of internal controls.Establish a system of internal controls.

Creating proper checks and balances.Creating proper checks and balances. Keep records up-to-date.Keep records up-to-date. Demonstrate zero tolerance for theft. Demonstrate zero tolerance for theft.

Inventory ControlInventory Control 1717Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

ShopliftingShoplifting

The most frequent business crime.The most frequent business crime. Businesses, especially retailers, lose $17 Businesses, especially retailers, lose $17

to $20 billion per year to shoplifters.to $20 billion per year to shoplifters. Shoplifting losses add approximately 3 Shoplifting losses add approximately 3

percent to the average price tag. percent to the average price tag.

Inventory ControlInventory Control 1818Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Types of ShopliftersTypes of Shoplifters

Juveniles.Juveniles. Impulse shoplifters.Impulse shoplifters. Alcoholics, vagrants, and drug addicts.Alcoholics, vagrants, and drug addicts. Kleptomaniacs.Kleptomaniacs. Professionals.Professionals.

Inventory ControlInventory Control 1919Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Deterring ShopliftersDeterring Shoplifters

Resources are best spent on Resources are best spent on preventionprevention.. Train employees to spot shoplifters.Train employees to spot shoplifters. Create a store layout that discourages Create a store layout that discourages

shoplifting.shoplifting. Consider using mechanical devices such Consider using mechanical devices such

as cameras and electronic tags to make as cameras and electronic tags to make shoplifters’ job more difficult. shoplifters’ job more difficult.

Inventory ControlInventory Control 2020Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Apprehending ShopliftersApprehending Shoplifters

Catching shoplifters is difficult; about 98 Catching shoplifters is difficult; about 98 percent of the time, shoplifters are percent of the time, shoplifters are successful.successful.

The chance that a shoplifter will actually The chance that a shoplifter will actually go before a judge is just 1 in 100.go before a judge is just 1 in 100.

Inventory ControlInventory Control 2121Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Making a CaseMaking a Case

To make shoplifting charges stick , a business To make shoplifting charges stick , a business owner must:owner must:

See the person take or conceal the merchandise.See the person take or conceal the merchandise. Identify the merchandise as belonging to the Identify the merchandise as belonging to the

store.store. Testify that it was taken with the intent to steal.Testify that it was taken with the intent to steal. Prove that the merchandise was not paid for.Prove that the merchandise was not paid for.

Inventory ControlInventory Control 2222Copyright 1999 Prentice Hall Publishing CompanyCopyright 1999 Prentice Hall Publishing Company

Preventing ShopliftingPreventing Shoplifting

Principle 1Principle 1: Sharpen the shoplifter's : Sharpen the shoplifter's awareness that he is being watched.awareness that he is being watched.

Principle 2Principle 2: Remove opportunity by : Remove opportunity by minimizing the shoplifter's unattended minimizing the shoplifter's unattended access to merchandise.access to merchandise.

Principle 3Principle 3: If principles 1 and 2 fail, : If principles 1 and 2 fail, prosecute the shoplifter.prosecute the shoplifter.