june july 2015 ceri commodity report — natural gas ... · ceri commodity report – natural gas...

TRANSCRIPT

Relevant • Independent • Objective

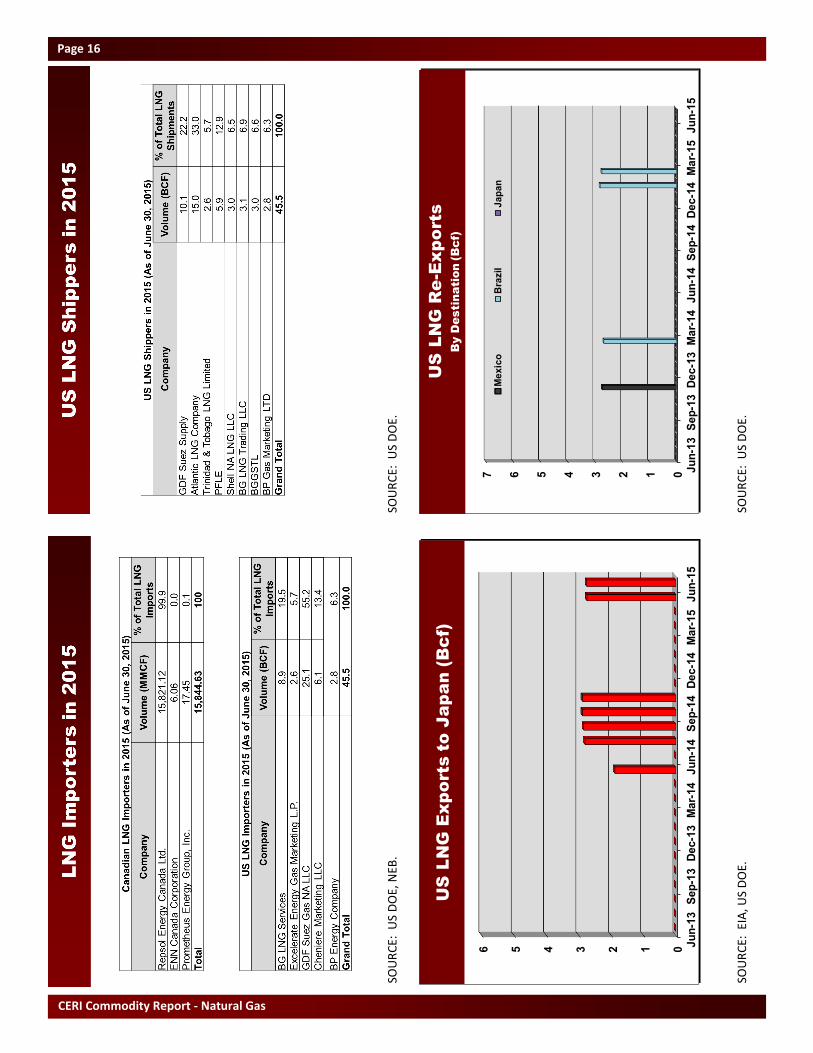

are under the jurisdiction of the United States Maritime Administration (MARAD) and the United States Coast Guard (USCG). Table 1 illustrates the existing import and export LNG terminals in the US, their company name, location and capacity. It is important to note that Freeport LNG, Sabine Pass LNG and Sempra-Cameron LNG are authorized to re-export delivered LNG. Re-exports of LNG occur when foreign shipments are offloaded in US storage tanks and are then subsequently reloaded onto tankers for delivery to other countries.2 This lets marketers and suppliers wait for price signals before delivering the LNG to higher-paying markets.3 Thus far, in 2015 only two shipments totaling 5.54 Bcf were re-exported from Freeport, Texas to Brazil. Table 1: Existing US LNG Terminals4

Source: FERC5 Approved (and Proposed) LNG Export Terminals in the US As of August 2015, five export facilities have been approved by the US Department of Energy and FERC and are already under construction: Sabine (Cheniere-Sabine Pass LNG), Hackberry (Sempra-Cameron LNG), Freeport (Freeport LNG), Cove Point (Dominion-Cove Point LNG) and Corpus Christi (Cheniere-Corpus Christi LNG).6 A sixth export facility, the Sabine Pass Liquefaction LLC (a subsidiary of Cheniere Energy Partners) has been approved but is not yet under construction.7 The US DOE issued a final authorization on June 26, 2015 to Sabine Pass Liquefaction to export domestically produced

June-July 2015

CERI Commodity Report — Natural Gas

The Changing LNG Landscape in the US Paul Kralovic While plunging oil prices have taken the lion's share of the spotlight on energy-related news, a monumental shift in the liquefied natural gas (LNG) landscape in the US is underway and has gone relatively unnoticed. Despite the fact that the first LNG facility in the US was the Kenai LNG export terminal located in the Cook Inlet area in Alaska, it is historically defined as a net importer of LNG. That, however, will change as early as late-2015. Fueled by advances in drilling and hydraulic fracturing technology and techniques, the production of shale gas is a game changer for the US, increasing production from 1.5 TCF in 2007 to 10.7 TCF in 2013.1 The shale gas boom is not only having a profound effect on natural gas production in the Lower-48, but also on how the US views energy and its role in a rapidly changing world. This article reviews the current LNG situation in the US, from a brief overview of existing facilities to reviewing approved export LNG facilities to the flood of proposed export LNG facilities awaiting their fates in various stages of the application process. With plummeting crude oil prices and changing economics, particularly for crude oil-inked LNG contracts, the situation is, however, dynamic. Existing LNG Import/Export Terminals in the US Currently, there are twelve liquefaction or regasification facilities in the US. Aside from the Kenai LNG export terminal, the remaining eleven terminals are import or regasification terminals. Nine terminals are under the Federal Energy Regulatory Commission (FERC) jurisdiction, responsible for the regulation of natural gas pipelines, storage and LNG, while two offshore facilities

Location Company Name Capacity (Bcfpd)

Everett, MA GDF SUEZ - DOMAC 1.035

Cove Point, MD Dominion – Cove Point LNG 1.8

Elba Island, GA El Paso – Southern LNG 1.6

Lake Charles, LA Southern Union – Trunkline LNG 2.1

Offshore Boston Excelerate Energy – Northeast Gateway 0.8

Freeport, TX Cheniere/Freeport LNG Dev. 1.5

Sabine, LA Cheniere/Sabine Pass LNG 4.0

Hackberry, LA Sempra – Cameron LNG 1.8

Offshore Boston, MA GDF SUEZ – Neptune LNG 0.4

Sabine Pass, TX ExxonMobil – Golden Pass (Phase I & II) 2.0

Pascagoula, MS El Paso/Creast/Sonangol – Gulf LNG Energy 1.5

Kenai, AK ConocoPhillips 0.2

CERI Commodity Report – Natural Gas Editorial Committee: Paul Kralovic, Dinara Millington, Megan Murphy, Jon Rozhon, Allan Fogwill About CERI The Canadian Energy Research Institute is an independent, not-for-profit research establishment created through a partnership of industry, academia, and government in 1975. Our mission is to provide relevant, independent, objective economic research in energy and related environmental issues. For more information about CERI, please visit our website at www.ceri.ca or contact us at [email protected].

Relevant • Independent • Objective

Page 2

natural gas to countries that do not have a free trade agreement with the US.8 With the exception of the 2.14 Bcfpd ‘greenfield’ export terminal in Corpus Christi, the remaining export terminals under construction are former import or regasification terminals. These ‘brownfield’ liquefaction projects hold a significant capital cost advantage because many engineering and infrastructure costs were sunk in years past when these sites were being built for regasification purposes. Of the five export facilities under construction, Sabine Pass LNG is leading the way, operational as early as 2015. Cheniere began construction of Trains 1 & 2 in August 2012 and Trains 3 & 4 in May 2013.9 Train 1 is scheduled to be operational in late-2015 with Trains 2 & 3 coming online in 2016.10 Each train has a production capacity of approximately 4.5 million tonnes per annum (Mtpa).11 Sabine Pass LNG’s clients include Chevron (US), Total (France), BG Group (Shell), Gas Natural Fenosa (Spain), KOGAS (Korea), and GAIL (India). Cheniere secured a sales agreement for up to 26 cargoes of LNG through 2019 with French-based EDF.12 With Russia supplying one-third of Europe’s gas, the latest deal announced on August 12, 2015 is attracting attention, highlighting possible geopolitical impacts or repercussions of the US entering the export game. Cove Point, located in Maryland, is the only export terminal under construction that is not located in the Gulf of Mexico. Cove Point began receiving LNG from Algeria in 1978 and after a period of disuse the facility was transformed to store domestic natural gas. Dominion Cove Point LNG received approval in May 2015 to build a liquefaction facility to export domestic natural gas.13 Construction of the 5.25 Mtpa facility began in 2014 and is scheduled to be operational in 2017.14 Sempra-Cameron LNG, located in Hackberry, Louisiana, received approval from the US Department of Energy to export up to 12 Mtpa, or approximately 1.7 Bcfpd, of domestically produced natural gas, and received authorization from FERC to operate a liquefaction facility in June 2014.15 Three trains are planned, with Trains 1, 2 & 3 coming online in early, mid- and late-2018, respectively.16 The planned expansion (Trains 4 & 5) is currently in the application process and, if approved, will increase the facilities capacity to 24.92 Mtpa, or 3.53 Bcfpd.17

Freeport LNG will have a capacity of 1.8 Bcfpd and is scheduled to be operational in 2018. All 13.2 Mtpa of production capacity has been contracted under tolling agreements with Osaka Gas (Japan), Chubu Electric (Japan), BP (UK), Toshiba (Japan), and SK E&S (South Korea).18 The fifth export terminal that is currently under construction is Cheniere’s Corpus Christi LNG export terminal. The liquefaction project is comprised of three trains, each with a capacity of 4.5 Mtpa (a total of 13.5 Mtpa) or approximately 2.1 Bcfpd.19 Construction began on May 13, 2015 and is slated to be completed in 2018.20 The project received FERC approval on April 6, 2015.21 The Corpus Christi LNG project also includes the construction and operation of a 78-inch diameter bi-directional pipeline.22 In June 2015, Cheniere Energy announced plans to expand by adding two trains (Trains 4 & 5), expanding capacity by approximately 9 Mtpa, and the project, dubbed Corpus Christi Liquefaction, is at the pre-filing stage with FERC.23 There are currently another 24 proposed export terminals in the US, nine of which are pending applications and the remainder are in the pre-filing stage.24 Seventeen projects are proposed in the Gulf of Mexico region (nine are located in Texas and seven are located in Louisiana). A further three are located on the US East Coast (Florida, Georgia and Maine), two are located on the US West Coast (Coos Bay and Astoria, Oregon) and one is proposed in Nikiski, Alaska. It is not a coincidence that the majority of liquefaction projects are located in the Gulf of Mexico, poised to take advantage of the expansion of the Panama Canal, to be completed in early 2016. The US$5.2 billion expansion project is large enough to handle the vast majority of the global LNG fleet, cutting the costs and time for LNG vessels departing the US east coast and Gulf of Mexico to the LNG-hungry Asian markets of Japan, South Korea and China. The new dimensions will likely open Atlantic Basin LNG to Asian markets, currently satisfied by either Middle Eastern or Pacific-Australian Basin LNG. While there are several reasons why LNG export projects may not go through, such as environmental challenges or opposition from gas-intensive industries, the price of oil may yet define the US LNG story. Lower oil prices are certainly eroding the spread between US and global prices, particularly as low oil prices have reduced the cost of oil-linked contracts that still dominate the

Relevant • Independent • Objective

Page 3

industry. This will challenge some LNG suppliers. As a result, many industry pundits are questioning how many export liquefaction terminals will indeed be built and how many of the under construction projects may be delayed due to the drop in oil prices. This reinforces CERI’s US supply/demand forecast in its Western Canada Natural Gas Forecasts and Impacts (2015-2035) study. Part of its North American gas market assumptions include 13 Bcfpd of LNG exports from the Gulf of Mexico and 1 Bcfpd of LNG exports from Cove Point over the 2015-2035 period.25 For additional information on LNG Liquefaction in a global setting, please download a recent CERI study, LNG Liquefaction in the Asia-Pacific Market: Canada’s Place in the Global Game.26 Endnotes 1EIA website, Table 4 Principal shale gas plays, 2012-2013, http://www.eia.gov/naturalgas/crudeoilreserves/pdf/table_4.pdf 2EIA Website, U.S. Natural Gas Exports and Re-Exports by Country, http://www.eia.gov/dnav/ng/ng_move_expc_s1_a.htm 3ibid 4FERC, North American LNG Import/Export Terminals – Existing, http://www.ferc.gov/industries/gas/indus-act/lng/lng-existing.pdf 5ibid 6FERC, North American LNG Import/Export Terminals: Approved as of June 18, 2015, http://www.ferc.gov/industries/gas/indus-act/lng/lng-approved.pdf 7Cheniere Website, Sabine Pass LNG, Train 5 & 6, http://www.cheniere.com/terminals/sabine-pass/trains-5-6/ 8US Department of Energy, Energy Department Authorizes Sabine Pass Liquefaction Expansion, http://www.energy.gov/articles/energy-department-authorizes-sabine-pass-liquefaction-s-expansion-project-export-liquefied

9Cheniere Website, Sabine Pass LNG, Trains 1 & 4, http://www.cheniere.com/terminals/sabine-pass/trains-1-4/ 10ibid 11ibid 12UPI Website, France Secures LNG from United States, http://www.upi.com/Business_News/Energy-Industry/2015/08/12/France-secures-LNG-from-United-States/6421439374351/ 13Dominion Cove Point LNG Website, Cove Point, https://www.dom.com/covepoint 14ibid 15Cameron LNG Website, Project Timeline, http://cameronlng.com/project-timeline.html 16ibid 17Cameron LNG Website, Liquefaction Expansion, http://cameronlng.com/liquefaction-expansion.html 18CERI Study 148, LNG Liquefaction for the Asia-Pacific Market, Jon Rozhon, June 2015, pp. 27. 19Cheniere Website, http://www.cheniere.com/terminals/corpus-christi-project/ 20Cheniere Website, http://www.cheniere.com/terminals/corpus-christi-project/liquefaction-project-trains-1-3/cc-schedule/ 21ibid 22Oil Online Website, EIA: LNG export terminals under construction, more planned, https://www.oilonline.com/news/midstream/eia-lng-export-terminals-under-construction-more-planned 23Cheniere Website, Corpus Christi Liquefaction, Stage 3 Under Development, http://www.cheniere.com/terminals/corpus-christi-project/stage-3-expansion-project-trains-4-5/ 24FERC, North American LNG Export Terminals – Proposed, http://www.ferc.gov/industries/gas/indus-act/lng/lng-existing.pdf 25Western Canada Natural Gas Forecasts and Impacts (2015-2035), CERI Study No. 149, July 2015. 26CERI Study 148, June 2015.

CERI Commodity Report - Natural Gas

Page 4

SOU

RC

E: C

ERI,

Pla

tts

Gas

Dai

ly P

rice

Gu

ide.

SO

UR

CE:

CER

I, P

latt

s G

as D

aily

Pri

ce G

uid

e.

SOU

RC

E: C

ERI,

Pla

tts

Gas

Dai

ly P

rice

Gu

ide.

SO

UR

CE:

CER

I, P

latt

s G

as D

aily

Pri

ce G

uid

e.

-113579

11

13

15 Jan

-05

Ju

l-06

Jan

-08

Ju

l-09

Jan

-11

Ju

l-12

Jan

-14

Ju

l-15

Dif

fere

nti

al

He

nry

Hu

bR

oc

kie

s

He

nry H

ub

/R

oc

kie

s

Beginning o

f N

ext M

onth S

pot P

rice (U

S$/M

MB

tu)

-113579

11

13

15 Ja

n-0

5J

ul-

06

Jan

-08

Ju

l-0

9J

an

-11

Ju

l-1

2J

an

-14

Ju

l-1

5

Dif

fere

nti

al

He

nry

Hu

bS

ou

the

rn C

ali

forn

ia

He

nry H

ub

/S

ou

th

ern

C

alifo

rn

ia

Be

gin

nin

g o

f N

ex

t M

on

th

S

po

t P

ric

e (U

S$

/M

MB

tu

)

-202468

10

12

14 Jan

-05

Ju

l-06

Jan

-08

Ju

l-09

Jan

-11

Ju

l-12

Jan

-14

Ju

l-15

Dif

fere

nti

al

He

nry

Hu

bA

EC

O-C

He

nry H

ub

/A

EC

O-C

Beginning of N

ext M

onth S

pot P

rice (U

S$/M

MB

tu)

-7-5-3-113579

11

13

15 Jan

-05

Ju

l-06

Jan

-08

Ju

l-09

Jan

-11

Ju

l-12

Jan

-14

Ju

l-15

Dif

fere

nti

al

He

nry

Hu

bC

hic

ag

o

He

nry H

ub

/C

hic

ag

o

Be

gin

nin

g o

f N

ex

t M

on

th

S

po

t P

ric

e (U

S$

/M

MB

tu

)

Relevant • Independent • Objective

Page 5

SOU

RC

E: C

anad

ian

Gas

Ass

oci

atio

n.

SOU

RC

E: C

ERI,

Can

adia

n G

as A

sso

ciati

on

, Sta

tisti

cs C

anad

a.

SOU

RC

E: N

OA

A.

SOU

RC

E: C

ERI,

NO

AA

, EIA

.

0

100

200

30

0

400

500

600

700

800

JF

MA

MJ

JA

SO

ND

5-Y

ea

r A

vg

.2

01

42

01

5

Ca

na

dia

n H

ea

tin

g D

eg

re

e D

ays

0

100

200

300

400

500

600

70

0

800

90

0

1,0

00

JF

MA

MJ

JA

SO

ND

5-Y

ea

r A

vg

.2

01

42

01

5

US

H

ea

tin

g D

eg

re

e D

ays

01234567

0

200

400

600

800

1,0

00

1,2

00 J

an

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

De

gre

e D

ay

sC

on

su

mp

tio

n

Ca

na

dia

n H

eatin

g D

eg

re

e D

ays vs R

esid

en

tia

l a

nd

Co

mm

erc

ia

l C

on

su

mptio

n

Deg

ree D

ays

BC

FP

D

010

20

30

40

50

60

0

200

400

600

800

1,0

00

1,2

00 J

an

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Ja

n-1

4J

an

-15

De

gre

e D

ay

sC

on

su

mp

tio

n

US

H

ea

tin

g D

eg

re

e D

ays vs

Re

sid

en

tia

l a

nd

C

om

me

rc

ia

l C

on

su

mp

tio

n

De

gre

e D

ay

sB

CF

PD

CERI Commodity Report - Natural Gas

Page 6

SOU

RC

E: E

nvi

ron

men

t C

anad

a.

SOU

RC

E: E

nvi

ron

men

t C

anad

a.

SOU

RC

E: N

OA

A.

SOU

RC

E: N

OA

A.

Relevant • Independent • Objective

Page 7

SOU

RC

E: N

OA

A.

SOU

RC

E: E

nvi

ron

men

t C

anad

a.

SOU

RC

E: N

OA

A.

CERI Commodity Report - Natural Gas

Page 8

SOU

RC

E: S

tati

stics

Can

ada.

SO

UR

CE:

Sta

tisti

cs C

anad

a, N

EB.

SOU

RC

E: E

IA.

SOU

RC

E: E

IA.

02468

10

12

14

16 J

an

-09

Jan

-10

Ja

n-1

1J

an

-12

Ja

n-1

3J

an

-14

Ja

n-1

5

Ind

us

tria

l &

Po

we

rC

om

me

rcia

lR

es

ide

nti

al

Ca

na

dia

n C

on

su

mp

tio

n

By S

ec

to

r (B

cfp

d)

02468

10

12

14

16

18

20 J

an

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

BC

, Y

uk

on

, N

WT

AB

SK

E.

Co

as

t

Ca

na

dia

n M

arke

ta

ble

Pro

du

ctio

n

By P

ro

vin

ce

/R

eg

io

n (B

cfp

d)

0

20

40

60

80

100

120

140 J

an

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Ind

us

tria

lE

lec

tric

Po

we

rC

om

me

rcia

lR

es

ide

nti

al

US

C

on

su

mp

tio

n

By S

ec

to

r (B

cfp

d)

0

10

20

30

40

50

60

70

80

90 J

an

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

US

To

tal

Lo

uis

ian

aG

OM

Fe

de

ral

Wa

ters

Te

xa

s

US

M

ark

eta

ble

P

ro

du

ctio

n (B

cfp

d)

Relevant • Independent • Objective

Page 9

SOU

RC

E: S

tati

stics

Can

ada,

NEB

. SO

UR

CE:

Sta

tisti

cs C

anad

a, N

EB.

SOU

RC

E: S

tati

stics

Can

ada,

NEB

. SO

UR

CE:

Sta

tisti

cs C

anad

a, N

EB.

0.0

1.0

2.0

3.0

4.0

5.0

JF

MA

MJ

JA

SO

ND

20

13

20

14

20

15

BC

, Y

uk

on

, N

WT

M

ark

eta

ble

Pro

du

ctio

n (B

cfp

d)

02468

10

12

14

16

JF

MA

MJ

JA

SO

ND

20

13

20

14

20

15

Alb

erta

M

ark

eta

ble

P

ro

du

ctio

n (B

cfp

d)

0.0

0.5

1.0

JF

MA

MJ

JA

SO

ND

20

13

20

14

20

15

Sa

sk

atc

he

wan M

arke

ta

ble

Pro

du

ctio

n (B

cfp

d)

0.0

0

0.2

5

0.5

0

JF

MA

MJ

JA

SO

ND

20

13

20

14

20

15

Ea

st C

oa

st M

ark

eta

ble

P

ro

du

ctio

n (B

cfp

d)

CERI Commodity Report - Natural Gas

Page 10

SOU

RC

E: C

ERI.

SO

UR

CE:

CER

I.

SOU

RC

E: N

EB.

SOU

RC

E: N

EB.

02468

10

12

14

16

JF

MA

MJ

JA

SO

ND

20

13

20

14

20

15

Syste

m F

ie

ld

R

ec

eip

ts

Tra

nsC

an

ad

a +

W

estc

oa

st; M

on

th

ly A

ve

ra

ge

(B

cfp

d)

02468

10

12

14

16

Ju

l-14

Sep

-14

No

v-1

4Jan

-15

Mar-

15

May-1

5Ju

l-15

Em

pre

ss

Mc

Ne

ill

AB

-BC

All

ian

ce

Alb

erta

S

yste

m D

elive

rie

s (B

cfp

d)

0123456789

10

Ju

n-1

4A

ug

-14

Oct-

14

Dec-1

4F

eb

-15

Ap

r-15

Ju

n-1

5

Kin

gs

ga

teM

on

ch

yE

lmo

reH

un

tin

gd

on

Ca

na

dia

n G

as E

xp

orts to

th

e U

S

By E

xp

ort P

oin

t -W

est (B

cfp

d)

0123456

Ju

n-1

4A

ug

-14

Oct-

14

Dec-1

4F

eb

-15

Ap

r-15

Ju

n-1

5

Em

ers

on

Iro

qu

ois

Oth

ers

Nia

ga

ra

Ca

na

dia

n G

as E

xp

orts to

th

e U

S

By E

xp

ort P

oin

t -E

ast (

Bc

fp

d)

Relevant • Independent • Objective

Page 11

SOU

RC

E: N

EB.

SOU

RC

E: N

EB.

SOU

RC

E: N

EB, E

IA.

SOU

RC

E: N

EB.

02468

10

12

Ju

n-1

4A

ug

-14

Oct-

14

Dec-1

4F

eb

-15

Ap

r-15

Ju

n-1

5

We

st

Mid

We

st

Ea

st

US

Im

po

rts o

f C

an

ad

ia

n G

as

By U

S R

eg

io

n (B

cfp

d)

02468

10

12

14

16

18

Ju

n-1

4A

ug

-14

Oct-

14

Dec-1

4F

eb

-15

Ap

r-15

Ju

n-1

5

We

st

Mid

We

st

Ea

st

Ave

ra

ge

C

an

ad

ia

n E

xp

ort P

ric

e

By U

S R

eg

io

n (C

$/G

J)

01234

Ju

n-1

4A

ug

-14

Oc

t-1

4D

ec

-14

Fe

b-1

5A

pr-

15

Ju

n-1

5

Co

urt

rig

ht

Sa

rnia

St.

Cla

irO

the

r

Ca

na

dia

n G

as Im

po

rts

By Im

po

rt P

oin

t (B

cfp

d)

02468

10

12

14 Ma

y-1

4J

ul-

14

Sep

-14

No

v-1

4J

an

-15

Ma

r-1

5M

ay

-15

Ca

na

da

Me

xic

o

To

ta

l U

S P

ip

elin

e G

as Im

po

rts (B

cfp

d)

CERI Commodity Report - Natural Gas

Page 12

SOU

RC

E: C

ERI,

Pla

tts

Gas

Dai

ly.

SOU

RC

E: C

ERI,

Pla

tts

Gas

Dai

ly.

SOU

RC

E: C

ERI,

Pla

tts

Gas

Dai

ly.

SOU

RC

E: C

ERI,

Pla

tts

Gas

Dai

ly.

0

100

200

300

400

500

600

700

800

900

1,0

00

JF

MA

MJ

JA

SO

ND

5-Y

ea

r A

vg

.2

01

42

01

5

Ca

na

dia

n W

ork

ing

G

as S

to

ra

ge

(B

cf, M

onth-end)

0

500

1,0

00

1,5

00

2,0

00

2,5

00

3,0

00

3,5

00

4,0

00

4,5

00

Ju

l-1

4S

ep

-14

No

v-1

4J

an

-15

Ma

r-1

5M

ay

-15

Ju

l-1

5

Ea

st

We

st

Pro

du

cin

g R

eg

ion

US

S

torage by R

egion (B

cf, M

onth

-end)

0

500

1,0

00

1,5

00

2,0

00

2,5

00

3,0

00

3,5

00

4,0

00

4,5

00

JF

MA

MJ

JA

SO

ND

5-Y

ea

r A

vg

.2

01

42

01

5

US

L

ow

er-4

8 W

ork

in

g G

as S

to

ra

ge

(B

cf, M

on

th

-e

nd

)

0

10

0

200

300

400

500

600

700

80

0

900

Ju

l-1

4S

ep

-14

No

v-1

4J

an

-15

Ma

r-1

5M

ay

-15

Ju

l-1

5

We

st

Ea

st

Canadian S

torage by R

egion (B

cf, M

onth-end)

Relevant • Independent • Objective

Page 13

SOU

RC

E: C

ERI,

Pla

tts

Gas

Dai

ly.

SOU

RC

E: C

ERI,

Pla

tts

Gas

Dai

ly.

SOU

RC

E: C

ERI,

Pla

tts

Gas

Dai

ly.

-140

-100

-60

-20

20

60

100

JF

MA

MJ

JA

SO

ND

WC

_IJ

_W

D

5-Y

ea

r A

vg

.2

01

42

01

5

We

ste

rn

C

an

ad

a S

to

ra

ge

In

je

ctio

ns/W

ith

dra

wals

(B

cf, M

on

th

-e

nd

)

-250

-200

-150

-100

-500

50

100

150

JF

MA

MJ

JA

SO

ND

5-Y

ea

r A

vg

.2

01

42

01

5

Canadian S

torage

Injections/W

ithdraw

als (B

cf, M

onth

-end)

-100

-80

-60

-40

-200

20

40

60

80

JF

MA

MJ

JA

SO

ND

5-Y

ea

r A

vg

.2

01

42

01

5

Eastern C

anadian S

torage Injections/W

ithdraw

als

(B

cf, M

onth-end)

CERI Commodity Report - Natural Gas

Page 14

SOU

RC

E: C

ERI,

Pla

tts

Gas

Dai

ly.

SOU

RC

E: C

ERI,

Pla

tts

Gas

Dai

ly.

SOU

RC

E: C

ERI,

Pla

tts

Gas

Dai

ly.

SOU

RC

E: C

ERI,

Pla

tts

Gas

Dai

ly.

-150

-100

-500

50

100

JF

MA

MJ

JA

SO

ND

5-Y

ea

r A

vg

.2

01

42

01

5

US

W

estern C

onsum

ing R

egion S

torage

Injections/W

ithdraw

als (B

cf, M

onth-end)

-400

-300

-200

-1000

10

0

200

JF

MA

MJ

JA

SO

ND

5-Y

ea

r A

vg

.2

01

42

01

5

US

P

roducing R

egion S

torage Injections/W

ithdraw

als

(B

cf, M

onth-end)

-12

00

-10

00

-800

-600

-400

-2000

200

400

600

800

JF

MA

MJ

JA

SO

ND

5-Y

ea

r A

vg

.2

01

42

01

5

US

S

torage

Injections/W

ithdraw

als (B

cf, M

onth-end)

-700

-500

-300

-100

100

300

500

JF

MA

MJ

JA

SO

ND

5-Y

ea

r A

vg

.2

01

42

01

5

US

E

astern S

torage

Relevant • Independent • Objective

Page 15

SOU

RC

E: U

S D

OE.

SO

UR

CE:

US

DO

E.

SOU

RC

E: U

S D

OE.

No

te:

Ther

e w

ere

no

LN

G im

po

rts

for

the

mo

nth

of

No

vem

ber

20

14

.

SOU

RC

E: U

S D

OE.

02468

Ju

n-1

3S

ep

-13

Dec-1

3M

ar-

14

Ju

n-1

4S

ep

-14

Dec-1

4M

ar-

15

Ju

n-1

5

Fre

ep

ort

La

ke

Ch

arl

es

Sa

bin

e P

as

sC

am

ero

nG

old

en

Pa

ss

Gu

lf L

NG

US

G

oM

L

NG

Im

po

rts B

y F

ac

ility (B

cf)

05

10

15

20

Ju

n-1

3S

ep

-13

Dec-1

3M

ar-

14

Ju

n-1

4S

ep

-14

Dec-1

4M

ar-

15

Ju

n-1

5

Oth

er

Nig

eri

aT

rin

ida

dN

orw

ay

Qa

tar

Ye

me

n

US

L

NG

Im

po

rts B

y O

rig

in

(B

cf)

02468

10

12

14

16

Ju

n-1

3S

ep

-13

De

c-1

3M

ar-

14

Ju

n-1

4S

ep

-14

De

c-1

4M

ar-

15

Ju

n-1

5

Co

ve

Po

int

Elb

a I

sla

nd

Ev

ere

ttN

E G

ate

wa

yN

ep

tun

e

Ea

ste

rn

U

S L

NG

Im

po

rts B

y F

ac

ility (B

cf)

02468

10

12

14

16

18

JF

MA

MJ

JA

SO

ND

20

13

20

14

20

15

Volum

e-W

eighted A

verage LN

G P

rice (U

S$/M

MB

tu)

CERI Commodity Report - Natural Gas

Page 16

SOU

RC

E: U

S D

OE,

NEB

. SO

UR

CE:

US

DO

E.

SOU

RC

E: E

IA, U

S D

OE.

SO

UR

CE:

US

DO

E.

0123456 Ju

n-1

3S

ep

-13

Dec-1

3M

ar-

14

Ju

n-1

4S

ep

-14

Dec-1

4M

ar-

15

Ju

n-1

5

Japan

US

L

NG

E

xp

orts to

J

ap

an

(B

cf)

01234567 Ju

n-1

3S

ep

-13

Dec-1

3M

ar-

14

Ju

n-1

4S

ep

-14

Dec-1

4M

ar-

15

Ju

n-1

5

Me

xic

oB

razil

Ja

pa

n

US

L

NG

R

e-E

xp

orts

By D

estina

tion

(B

cf)

Relevant • Independent • Objective

Page 17

SOU

RC

E: C

ERI,

CA

OD

C, B

aker

Hu

ghes

. SO

UR

CE:

CER

I, C

AO

DC

.

SOU

RC

E: C

ERI,

CA

OD

C.

SOU

RC

E: C

ERI,

CA

OD

C.

0

500

1,0

00

1,5

00

2,0

00

2,5

00

3,0

00 Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

US

WC

SB

North A

merican A

ctive R

igs

0

100

200

300

400

500

600

700

800

900

1,0

00 Ja

n-0

6J

an

-07

Ja

n-0

8J

an

-09

Ja

n-1

0J

an

-11

Jan

-12

Jan

-13

Ja

n-1

4J

an

-15

Ac

tiv

e R

igs

To

tal

Rig

Dri

llin

g F

lee

t

Ca

na

dia

n R

ig

F

le

et U

tiliza

tio

n

We

ek

ly A

ve

ra

ge

Ac

tive

Rig

s

0

100

200

300

400

500

600

70

0 Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

SK

AB

BC

WC

SB

A

ctive

R

ig

s b

y P

ro

vin

ce

We

ek

ly A

ve

ra

ge

-

100

200

300

400

500

600

700

800

15

913

17

21

25

29

33

37

41

45

49

5-Y

ea

r A

vg

.2

01

42

01

5

We

ste

rn

C

an

ad

a A

ctive

R

ig

s

Wee

kly A

ve

ra

ge

Week N

um

ber

CERI Commodity Report - Natural Gas

Page 18

SOU

RC

E: C

ERI,

Bak

er H

ugh

es.

SO

UR

CE:

CER

I, B

aker

Hu

ghe

s.

SOU

RC

E: C

ERI,

Bak

er H

ugh

es.

0%

10%

20%

30%

40%

50%

60%

70%

80

%

90%

100%

0

200

400

600

800

1,0

00

1,2

00

1,4

00

1,6

00

1,8

00

2,0

00

2,2

00

2,4

00 Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Oil

-dir

ec

ted

Ga

s-d

ire

cte

dG

as-d

ire

cte

d %

US

T

ota

l A

ctive

R

ig

s

0

50

0

1,0

00

1,5

00

2,0

00

2,5

00 Jan

-06

Ja

n-0

7J

an

-08

Ja

n-0

9J

an

-10

Jan

-11

Jan

-12

Jan

-13

Ja

n-1

4J

an

-15

To

tal

Oil

-dir

ec

ted

Go

M G

as

-dir

ec

ted

On

sh

ore

Ga

s-d

ire

cte

d

US

T

ota

l A

ctive

R

ig

s

0

20

40

60

80

100

120 J

an

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Oil

-dir

ec

ted

Ga

s-d

ire

cte

d

US

G

ulf o

f M

ex

ic

o A

ctive

R

ig

s