madeira free trade zone (mfz) 9 th of july 2014. madeira free trade zone about madeira regime...

TRANSCRIPT

MADEIRA FREE TRADE ZONE (MFZ)

9TH OF JULY 2014

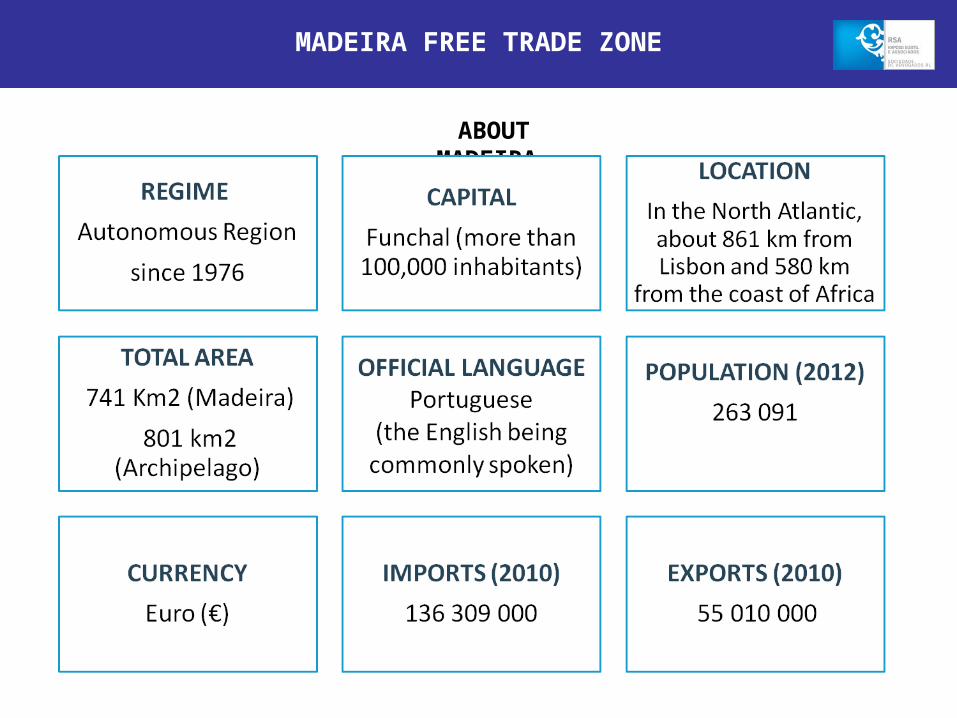

MADEIRA FREE TRADE ZONE

ABOUT MADEIRA

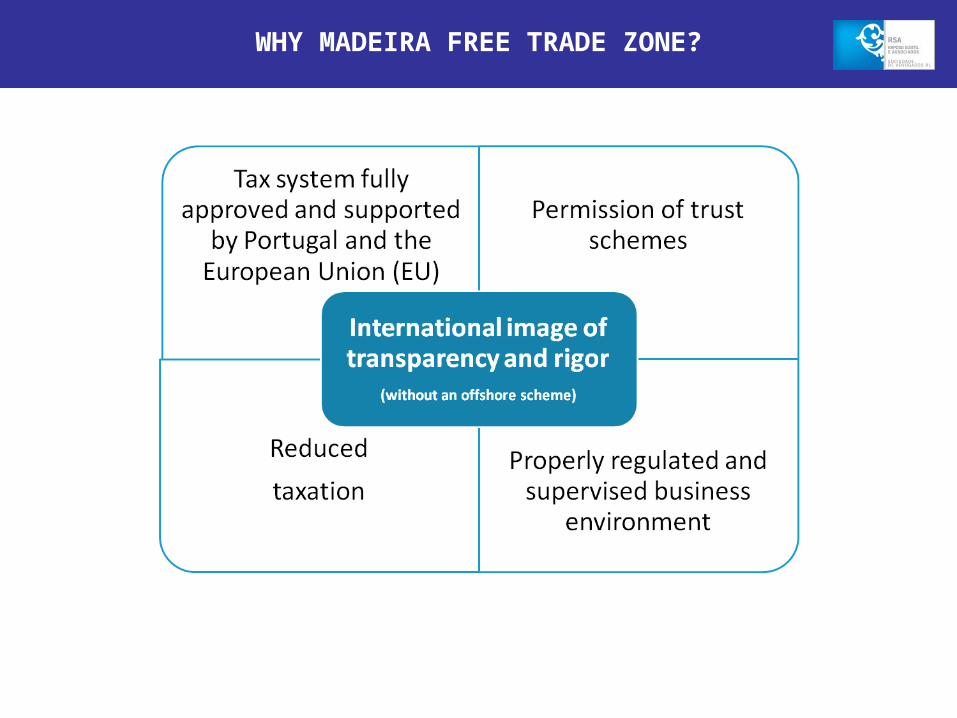

WHY MADEIRA FREE TRADE ZONE?

NOTION

The IBCM consists of a set of incentives, particularly tax, applicable

to a wide range of activities that can be developed, in particular, by

commercial companies (also branches, agencies, offices);

All type of service-oriented companies may be licensed to carry out

activities, namely: International Trading, Consultancy,

Management of Intellectual property, e-business,

telecommunications, Share Holding (SGPS).

The administration and operation of the MFZ are the sole

responsibility of the “SDM - Sociedade de Desenvolvimento da

Madeira, S.A.” (to which is due by entities operating in the MFZ, the

payment of an application fee and an annual operating fee).

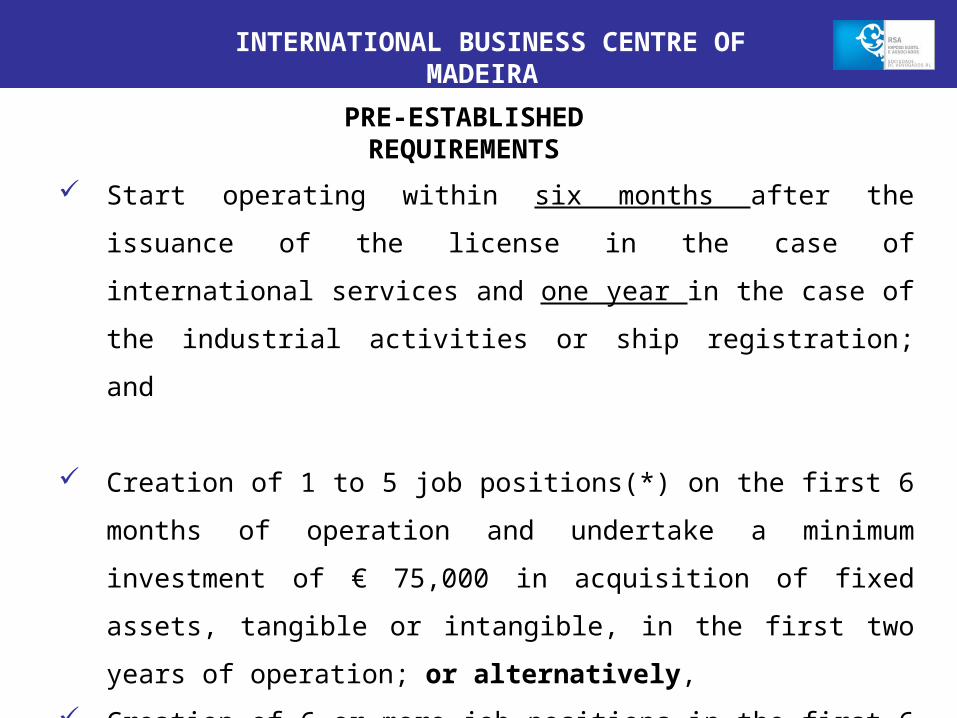

INTERNATIONAL BUSINESS CENTRE OF MADEIRA

PRE-ESTABLISHED REQUIREMENTS

Start operating within six months after the issuance of the license in the

case of international services and one year in the case of the industrial

activities or ship registration; and

Creation of 1 to 5 job positions(*) on the first 6 months of operation and

undertake a minimum investment of € 75,000 in acquisition of fixed

assets, tangible or intangible, in the first two years of operation; or

alternatively,

Creation of 6 or more job positions in the first 6 months of operation.

(*) It is not mandatory to develop the labour activity exclusively in Madeira.

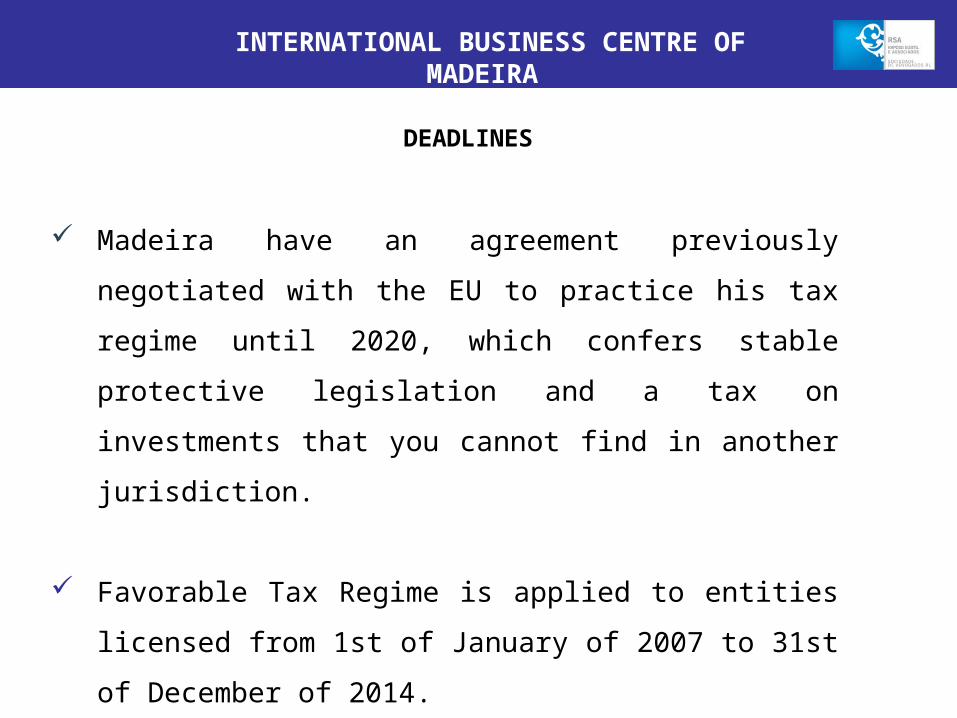

INTERNATIONAL BUSINESS CENTRE OF MADEIRA

DEADLINES

Madeira have an agreement previously negotiated with the EU

to practice his tax regime until 2020, which confers stable

protective legislation and a tax on investments that you cannot

find in another jurisdiction.

Favorable Tax Regime is applied to entities licensed from 1st of

January of 2007 to 31st of December of 2014.

INTERNATIONAL BUSINESS CENTRE OF MADEIRA

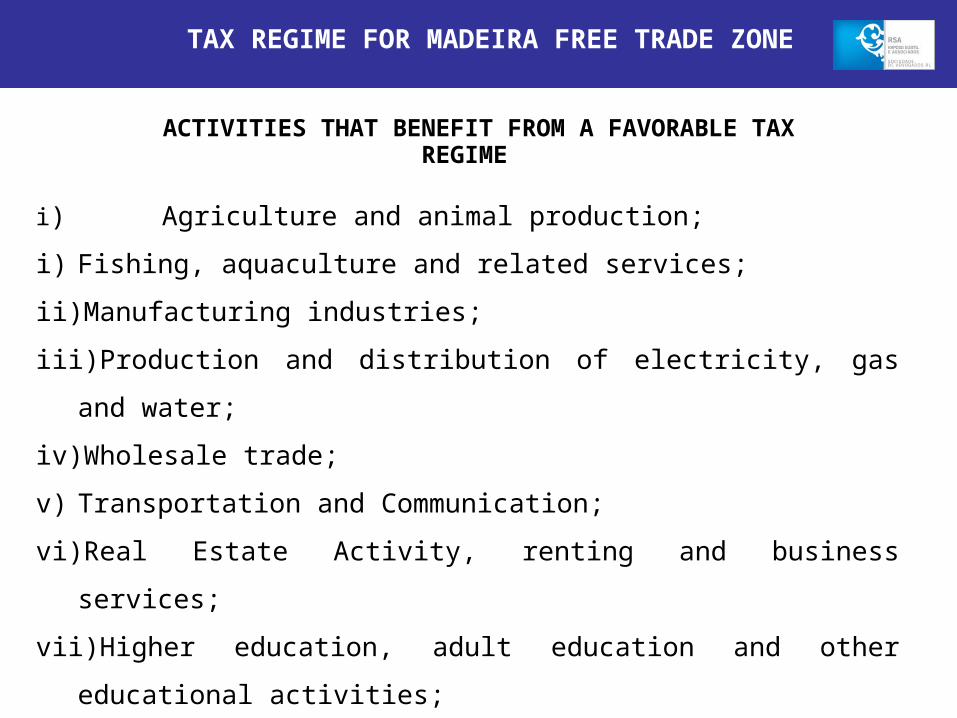

TAX REGIME FOR MADEIRA FREE TRADE ZONE

i) Agriculture and animal production;

i) Fishing, aquaculture and related services;

ii) Manufacturing industries;

iii) Production and distribution of electricity, gas and water;

iv) Wholesale trade;

v) Transportation and Communication;

vi) Real Estate Activity, renting and business services;

vii) Higher education, adult education and other educational activities;

viii) Other community services, namely activities related to sanitation, as well as

recreational, cultural and sporting activities.

ACTIVITIES THAT BENEFIT FROM A FAVORABLE TAX REGIME

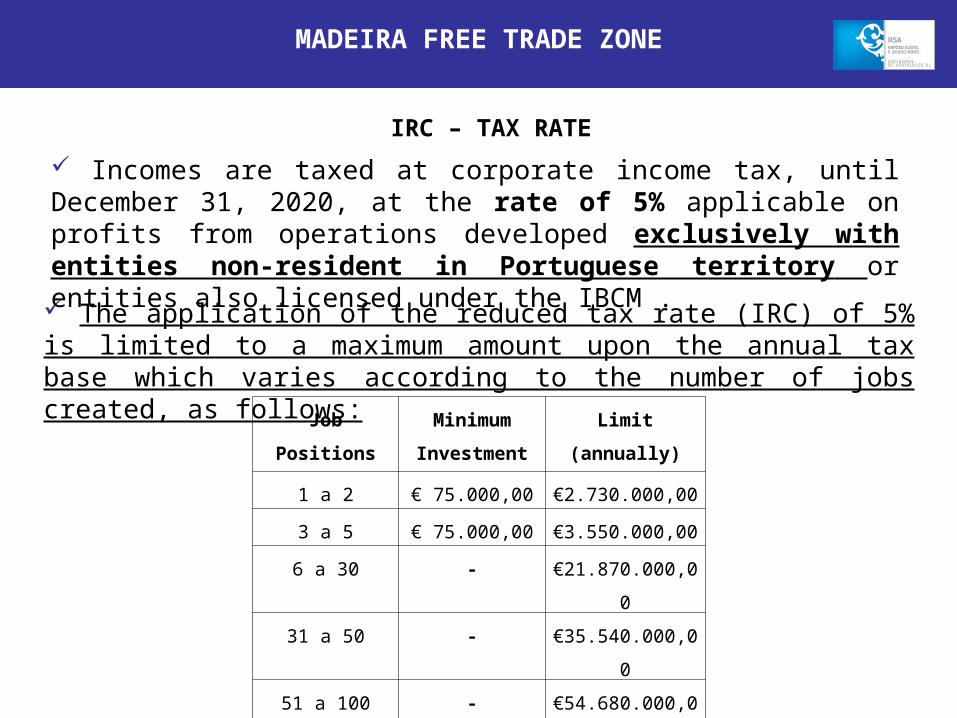

The application of the reduced tax rate (IRC) of 5% is limited to a maximum amount upon the annual tax base which varies according to the number of jobs created, as follows:

Incomes are taxed at corporate income tax, until December 31, 2020, at the rate of 5% applicable on profits from operations developed exclusively with entities non-resident in Portuguese territory or entities also licensed under the IBCM .

MADEIRA FREE TRADE ZONE

Job Positions Minimum

Investment

Limit (annually)

1 a 2 € 75.000,00 €2.730.000,00

3 a 5 € 75.000,00 €3.550.000,00

6 a 30 - €21.870.000,00

31 a 50 - €35.540.000,00

51 a 100 - €54.680.000,00

Mais de 100 - €205.500.000,00

IRC – TAX RATE

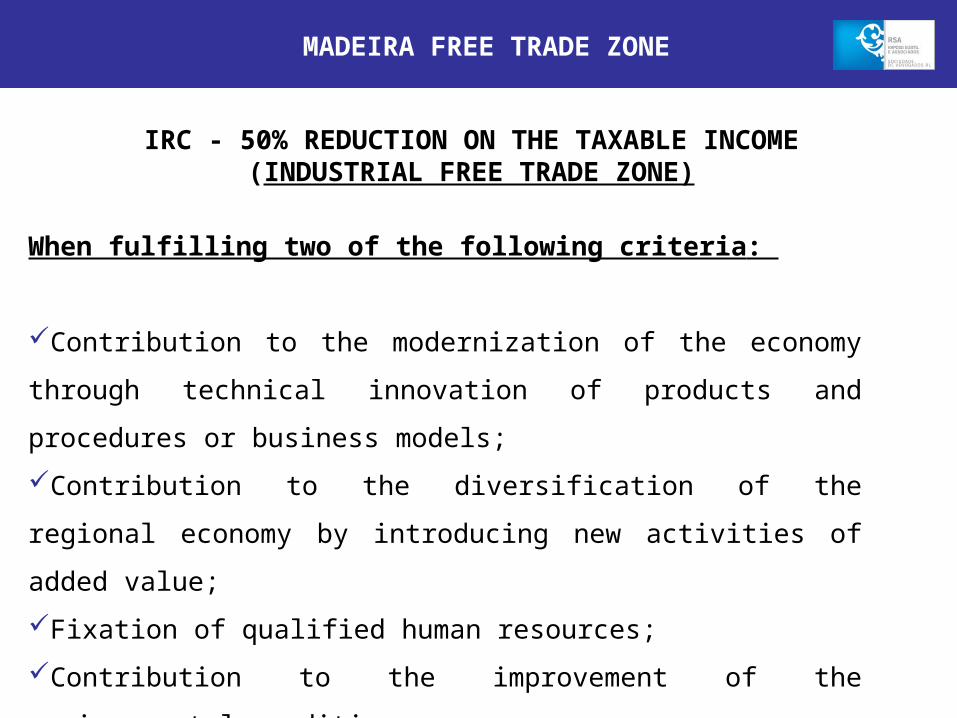

When fulfilling two of the following criteria:

Contribution to the modernization of the economy through technical

innovation of products and procedures or business models;

Contribution to the diversification of the regional economy by introducing

new activities of added value;

Fixation of qualified human resources;

Contribution to the improvement of the environmental conditions;

Creation of 15 jobs for a period of 5 years.

IRC - 50% REDUCTION ON THE TAXABLE INCOME (INDUSTRIAL FREE TRADE ZONE)

MADEIRA FREE TRADE ZONE

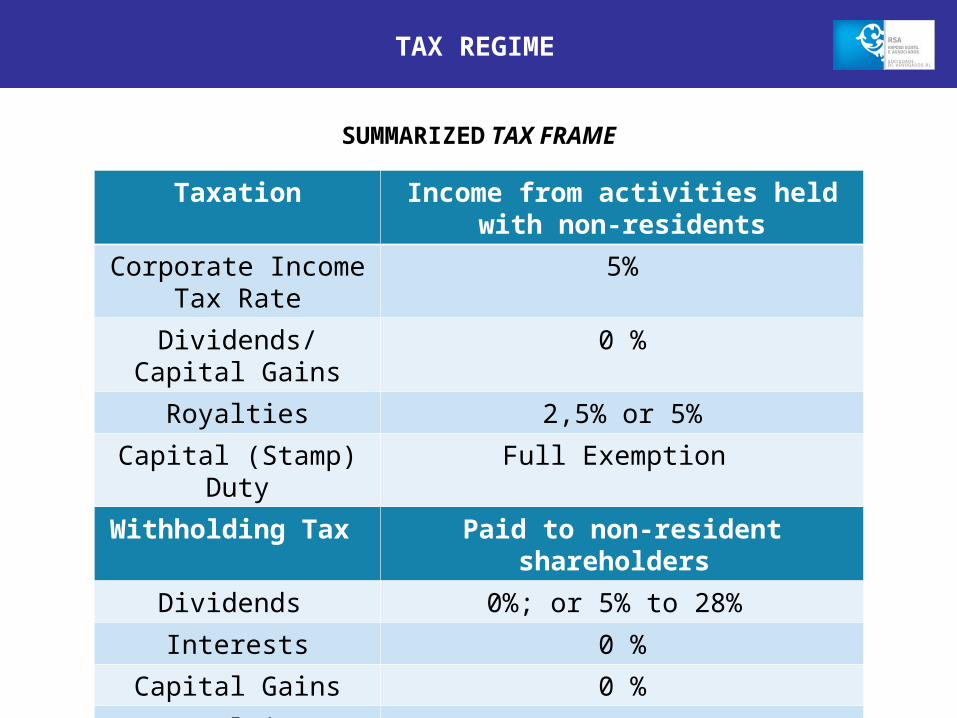

TAX REGIME

SUMMARIZED TAX FRAME

Taxation Income from activities held with non-residents

Corporate Income Tax Rate

5%

Dividends/ Capital Gains 0 %

Royalties 2,5% or 5%

Capital (Stamp) Duty Full Exemption

Withholding Tax Paid to non-resident shareholders

Dividends 0%; or 5% to 28%

Interests 0 %

Capital Gains 0 %

Royalties 0 %

Services 0 %

MORE FAVORABLE REGIME

OTHER TAX BENEFITS

Exemption of Stamp Duty Tax on every documents, contracts, acts, books, papers and any other operations;

Profits distributed to IRC taxpayers are exempted or taxed at a 5% rate;

Exemption of Capital Gains Tax on Share Capita l Increase;

Exemption of Land Transfer Tax and Stamp Duty Tax on transmissions of shares, stocks and other assets that comprise the assets of the company situated at MFTZ;

It will be considered as a cost for tax purposes the injection of share capital.

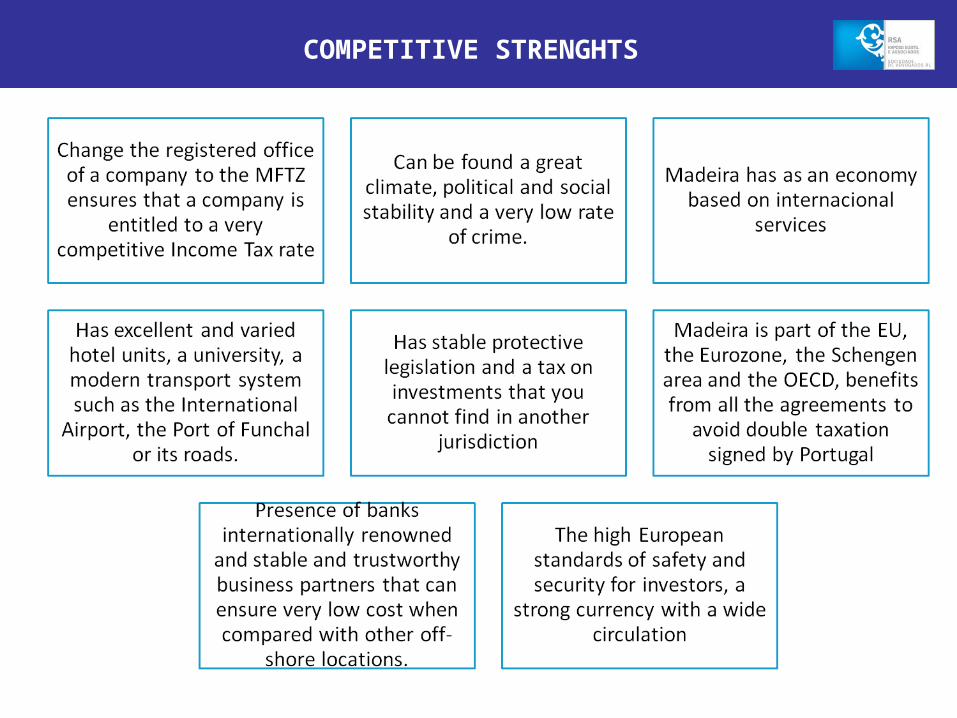

COMPETITIVE STRENGHTS

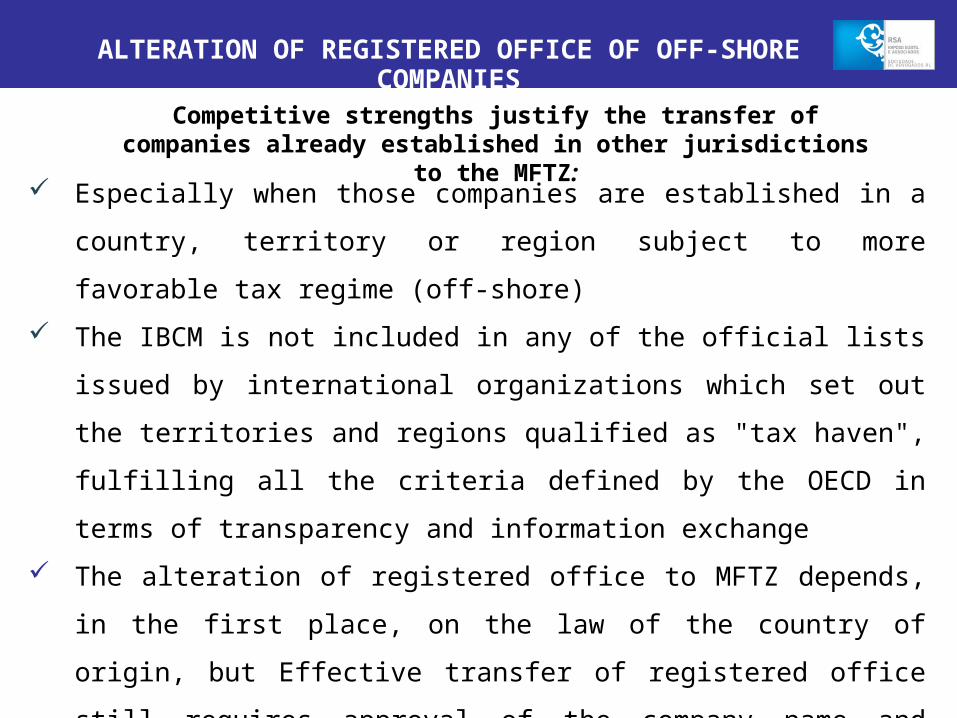

ALTERATION OF REGISTERED OFFICE OF OFF-SHORE COMPANIES

Competitive strengths justify the transfer of companies already established in other jurisdictions to the MFTZ:

Especially when those companies are established in a country, territory or

region subject to more favorable tax regime (off-shore)

The IBCM is not included in any of the official lists issued by international

organizations which set out the territories and regions qualified as "tax

haven", fulfilling all the criteria defined by the OECD in terms of transparency

and information exchange

The alteration of registered office to MFTZ depends, in the first place, on the

law of the country of origin, but Effective transfer of registered office still

requires approval of the company name and object in the Portuguese

Companies House, the issuance of the license to operate at MFTZ and the

respective registrations.

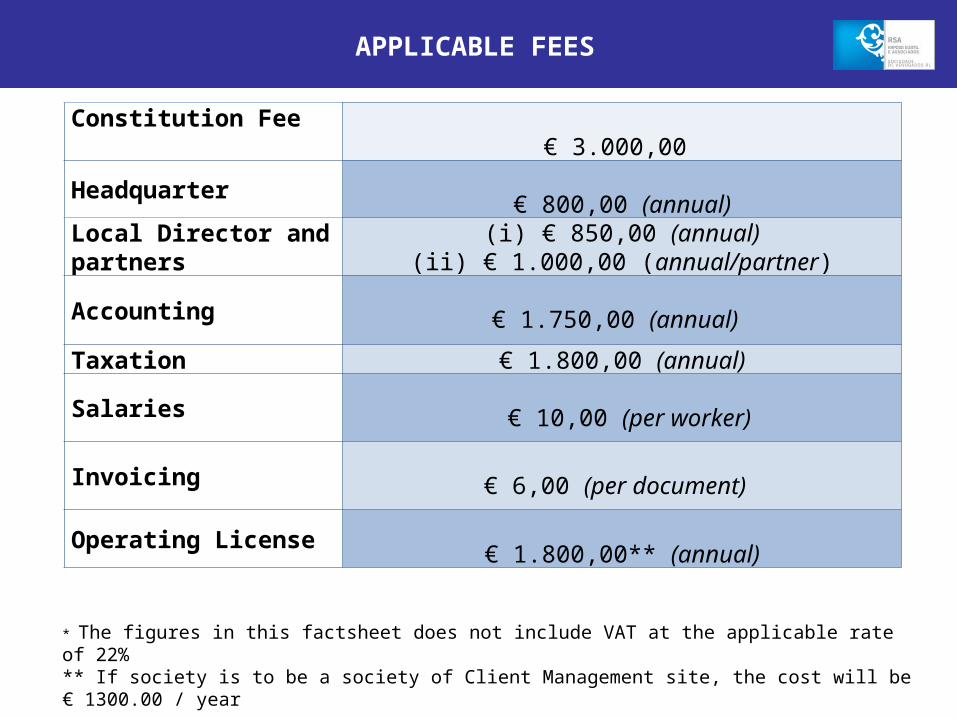

APPLICABLE FEES

DESCRIPTION FEE

Constitution Fee 1.000 €

Annual Operating Fee 1.800 € (1.300 € if using local Management Company)

Aditional Operating Fee (only for SGPS)

0,5 % of taxable income that exceeds 1 Million €

Registration of Trust 300 €

Constitution Fee for Trust Branches

1.000 €

Annual Operating Fee for Trust Branches

2.400 €

APPLICABLE FEES

Constitution Fee € 3.000,00

Headquarter € 800,00 (annual)Local Director and partners

(i) € 850,00 (annual)(ii) € 1.000,00 (annual/partner)

Accounting

€ 1.750,00 (annual)

Taxation € 1.800,00 (annual)

Salaries € 10,00 (per worker)

Invoicing

€ 6,00 (per document)

Operating License € 1.800,00** (annual)

* The figures in this factsheet does not include VAT at the applicable rate of 22% ** If society is to be a society of Client Management site, the cost will be € 1300.00 / year

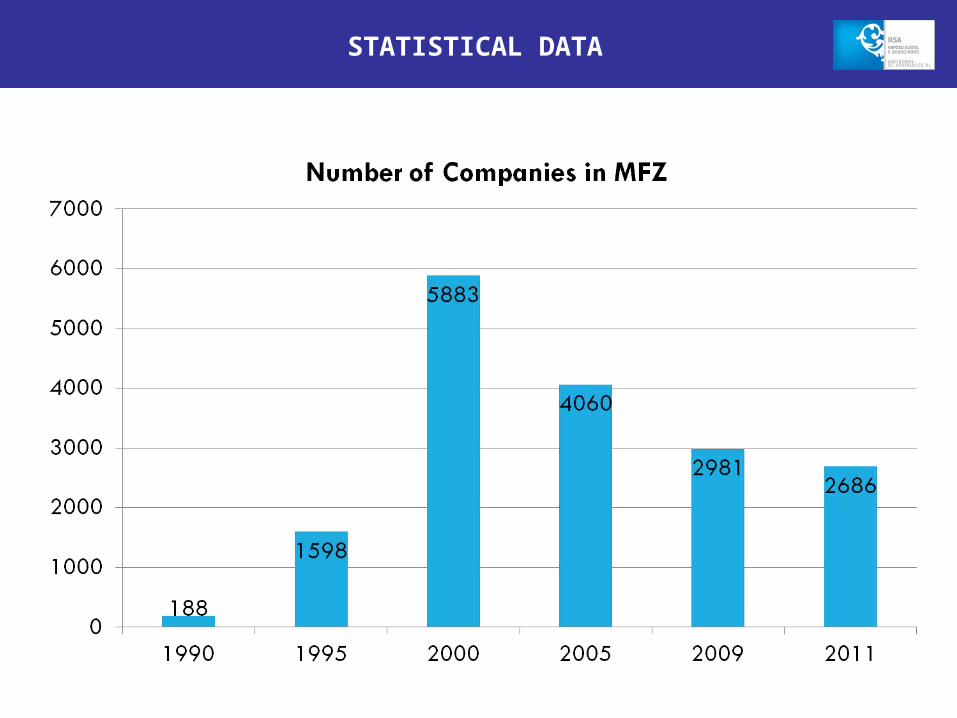

STATISTICAL DATA

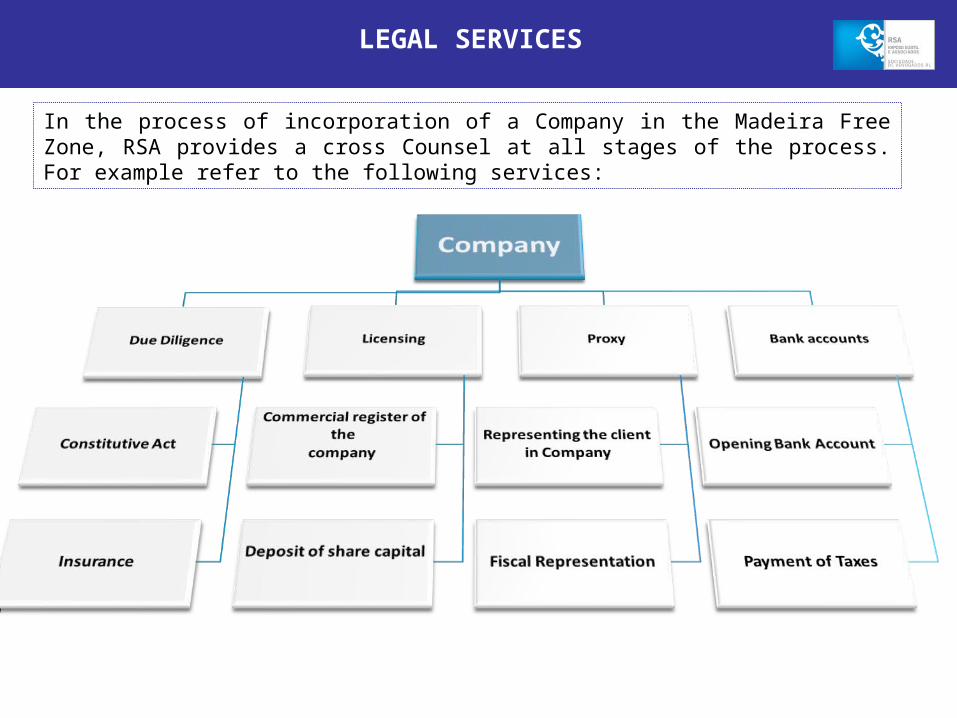

In the process of incorporation of a Company in the Madeira Free Zone, RSA provides a cross Counsel at all stages of the process. For example refer to the following services:

LEGAL SERVICES

THANK YOU!

LISBONRua Bernardo Lima, 3

1150-074 LisboaT. +351 213 566 400

F. +351 213 566 488 | 9

Contact: [email protected]

www.rsa-advogados.pt

LISBON - OPORTO – COIMBRA - ALGARVE - AZORES - MADEIRA - ANGOLA - BRAZIL - MOZAMBIQUE-CAPE VERDE