michaud kritika black litterman i odgovor waltersa.pdf

DESCRIPTION

Black litterman model discussionTRANSCRIPT

JOIMwww.joim.com

Journal Of Investment Management, Vol. 11, No. 1, (2013), pp. 6–20

© JOIM 2013

DECONSTRUCTING BLACK–LITTERMAN: HOW TO GET THEPORTFOLIO YOU ALREADY KNEW YOU WANTEDRichard O. Michaud a, David N. Esch a and Robert O. Michaud a

The Markowitz (1952, 1959) mean–variance (MV) efficient frontier has been the theo-retical standard for defining portfolio optimality for more than half a century. However,MV optimized portfolios are highly susceptible to estimation error and difficult to managein practice (Jobson and Korkie, 1980, 1981; Michaud, 1989). The Black and Litterman(BL) (1992) proposal to solve MV optimization limitations produces a single maximumSharpe ratio (MSR) optimal portfolio on the unconstrained MV efficient frontier based onan assumed MSR optimal benchmark portfolio and active views. The BL portfolio is oftenuninvestable in applications due to large leveraged or short allocations. BL use an inputtuning process for computing acceptable sign constrained solutions. We compare con-strained BL with MV and Michaud (1998) optimization for a simple dataset. We show thatconstrained BL is identical to Markowitz and that Michaud portfolios are better diversi-fied under identical inputs and optimality criteria. The attractiveness of the BL procedureis due to convenience rather than effective asset management and not recommendablerelative to alternatives.

1 Introduction

For more than half a century, the Markowitz(1952, 1959) mean–variance (MV) efficient fron-tier has been the theoretical standard fordefining linear constrained portfolio optimal-ity. Markowitz optimization is a convenientframework for computing MV optimal portfo-lios that are designed to meet practical investmentmandates.

aNew Frontier Advisors, LLC, Boston, MA 02110, USA.

MV optimization, however, has a number ofwell-known investment limitations in practice.Optimized portfolios are unstable and ambigu-ous and highly sensitive to estimation errorin risk-return estimates. The procedure tendsto overweight/underweight assets with estimateerrors in high/low means, low/high variances, andsmall/large correlations, often resulting in poorperformance out-of-sample (Jobson and Korkie,1980, 1981). MV optimized portfolios in practiceare often investment unintuitive and inconsistentwith marketing mandates and management priors.

6 First Quarter 2013

Deconstructing Black–Litterman: How to Get the Portfolio You Already Knew You Wanted 7

Ad hoc input revisions and constraints result in anMV optimization process that is largely an exer-cise in finding “acceptable” rather than optimalportfolios (Michaud, 1989).

To address estimation error issues in MV opti-mization, Black and Litterman (BL) (1992) pro-pose a single maximum Sharpe ratio (MSR)portfolio. This portfolio is constructed assuming:an unconstrained MV optimization framework;an assumed MSR optimal benchmark or “mar-ket” portfolio; an estimation error-free covariancematrix; and active investor views. BL optimalportfolios often have large leveraged and/or shortallocations that may make them uninvestablein applications. Moreover, Jobson and Korkiedocument severe out-of-sample investment lim-itations for the unconstrained MV optimizationframework, of which BL optimization is anexample.1

BL introduce an input “tuning” parameter τ thatenables sign constrained MSR optimal solutions.2

We describe the mathematical properties of BL,including τ-adjustment, and use a simple datasetto illustrate the procedures. We show that theBL sign constrained portfolio is identical toMarkowitz MSR for the same inputs and con-sequently no less estimation error sensitive. BLoptimality is also benchmark centric and subjectto the Roll (1992) critique of optimization onthe wrong efficient frontier. The Michaud (1998)proposal to address estimation error uses MonteCarlo resampling and frontier averaging methodsto generalize the Markowitz efficient frontier.3 Wecompare BL and Michaud MSR optimized port-folios under identical assumptions and show thatthe Michaud portfolios are better diversified andrisk managed.4

Section 2 describes the mathematical charac-teristics and statistical issues associated withthe Black–Litterman procedure including τ-adjustment. Section 3 illustrates BL optimization

with a simple dataset, compares the portfolioswith Markowitz and Michaud alternatives, anddemonstrates the sensitivity to covariance esti-mation error. Section 4 discusses BL relative tobenchmark-centric optimization, unconstrainedMV framework, and investor risk aversion. Sec-tion 5 summarizes and concludes.

2 Black and Litterman optimization

2.1 Black–Litterman framework

BL optimization requires three investmentassumptions: (1) unconstrained MV optimiza-tion; (2) capital market portfolio M in “equilib-rium” on the Markowitz MV efficient frontier;and (3) covariance matrix � without estimationerror. Under these conditions M is the MSRportfolio on the MV efficient frontier. Uncon-strained MV optimization and perfectly esti-mated covariance matrix allow computation ofthe “implied” or “inverse” returns � = �M con-sistent with MV Sharpe ratio optimality (Sharpe,1974; Fisher, 1975). The result is a set of esti-mated returns � and covariance matrix � forwhich the market portfolio M is the MSR effi-cient portfolio on the unconstrained MV efficientfrontier.5

In elemental form, the BL proposal is a rationalefor the identification of a benchmark portfolio toanchor the optimization and overlay investmentviews. Benchmark anchoring of MV optimizedportfolios has a long tradition in investment prac-tice and is subject to Roll (1992) critiques.6

The procedure trivially replicates its input in theabsence of any additional investor views. Investorviews are processed using an adaptation of theTheil and Goldberger (1961) mixed estimationformula relative to the implied return estimates�.7 The revised returns with views µBL areused to compute the BL MV optimal portfolioB. Deviations from the index weights indicate

First Quarter 2013 Journal Of Investment Management

8 Richard O. Michaud et al.

optimal overweights and underweights for eachasset relative to the benchmark portfolio.

2.2 Black–Litterman mathematical structure

It is useful to briefly review the mathematicalstructure of the BL optimization framework.8

We are given data for N assets with theoreticalmean µ and known variance �. We assume Ma vector of “equilibrium” market or index port-folios weights. We construct an estimate of the“implied” or “inverse” expected returns � =�M. � represents the returns associated withmarket portfolio M in equilibrium for knowncovariance matrix �.

Views are specified as Pµ ∼ N(v, �), as where Pis a K ×N matrix whose rows are portfolios withviews, v is the vector of expected returns for theseportfolios, and � is the covariance matrix for theviews. In the terminology of Bayesian statistics,we assign the views as the prior distribution. BLintroduce a tuning parameter τ to adjust the impactof the views. They express the distribution of theequilibrium mean as N(�, τ�). The parameter τ

may be viewed as a proxy for 1/T , the reciprocalof the number of time periods in the data, or asa measure of the relative importance of the viewsto the equilibrium but is often used simply to findinvestable (long-only) BL optimal portfolios. Theresulting posterior distribution then has a normaldistribution with mean equal to the BL estimateswhich can be expressed as:

µBL = � + �P ′(

�

τ+ P�P ′

)−1

(v − P�)

= � + V. (1)

Equation (1) is useful, since it decomposes theestimate into the original data-based estimate �

and the contribution from the views V . In fact,if the mean estimate is the vector of equilibriumimplied returns �, then the maximum informa-tion ratio unconstrained portfolio optimization

results in portfolio weights P∗BL, which are pro-

portional to:

�−1µBL = M + P ′(

�

τ+ P�P ′

)−1

× (v − P�) (2)

The second term on the right-hand side of Equa-tion (2) is a multiplication of the matrix P ′,whose k columns are the portfolios with views,by the k by 1 vector (�

τ+ P�P ′)−1(v − P�).

Thus, in mathematical terms, the contribution ofinvestor views to the BL portfolio is confinedto the subspace spanned by the view portfolios.More intuitively, the BL portfolio pushes itselftoward or away from each view as necessary, but islimited to directions specified by the view portfo-lios themselves. Active bets induced by includingviews result in allocations in a direction which issolely a linear combination of those views.

2.3 Investable Black–Litterman portfolios

BL unconstrained MV optimized portfolios oftenpossess large leveraged and/or short positions.In practice, investors often require that opti-mal portfolios are investable, i.e., that they aresign constrained and/or linear inequality con-strained within some specified range.9 By def-inition the equilibrium or market portfolio issign constrained. BL introduce the input “tun-ing” parameter 0 ≤ τ ≤ 1 for finding portfoliosbetween the BL portfolio B and index portfolio Mthat are nonnegative (long-only) or satisfy somesuitable inequalities. The parameter τ provides amechanism for finding investable BL portfolios.The parameter operates as a scalar that divides thevariances associated with the uncertainty of theviews. Smaller values of τ cause greater inflationof the views’ uncertainty and limit their influenceon the results. As τ is reduced, or the constantmultiplier of the standard deviations of the viewsincreased, the BL portfolio approaches the bench-mark portfolio. The value of τ may be chosen to

Journal Of Investment Management First Quarter 2013

Deconstructing Black–Litterman: How to Get the Portfolio You Already Knew You Wanted 9

compute an investable BL portfolio when it usesjust enough of the certainty in investor’s viewsto meet investability constraint boundaries. Thenet effect of the τ-adjustment is to reduce theimpact of the covariance matrix on the BL port-folio. At sufficiently high certainty, the procedureessentially ignores the covariance matrix and theoptimization framework.

Without recourse to a formal τ-adjustment, aninvestor may define an investable BL portfoliosimply by sufficiently increasing the standarddeviations of any or all of the views. However,such a process is clearly ad hoc. Indeed, in acaricature of the BL procedure, some softwareproviders have a “dial-an-optimal” option foreach view so that an investor can create whateverBL portfolio desired. In this case, BL is sim-ply optimization by definition with little regardto investment value.

2.4 Further comments on the Black–Littermanstatistical framework

We note that no standard statistical procedureproduces the implied returns as estimates forportfolio expectations. The formula comes outof theoretical assumptions of market efficiencyand equilibrium, and the additional assumptionsof current efficient equilibrium market weightsand an error-free covariance matrix. Since theestimation of the mean is ancillary to the estima-tion of variance, using a mean estimate that is afunction of the covariance estimate is tantamountto believing that there is no information for thefirst moment of the data, while there is perfectinformation for the second moment, the expectedsquared deviations from the unknowable firstmoment. From a pure data analysis perspectivethis assumption is untenable. The usual mean-ings of mean and variance have been lost, and thesignificance of these calculations is unclear otherthan as convenient inputs to an optimizer that hasbeen designed to produce preordained answers.

Additionally, the τ-adjustment itself is an ad hocmodification of the prior distribution to steer theoutcome toward some desirable result, whichviolates the principles of a rigorous Bayesiananalysis. The problem is that one does not changehis or her internal beliefs to modify an outcomewhen confronted with those beliefs. The onlyalternative characterization of τ-adjustment is amodification of the scale of the covariance of thedata, which also changes the model during themodel-fitting stage. The adjustment of τ to attaininvestability is an intervention which contami-nates the rigor of the analysis and must be viewedas an ad hoc correction of a flawed procedure,and a major departure from rigorous statisticalanalysis.

3 Black–Litterman optimizationillustrated

3.1 Risk-return inputs and investor views

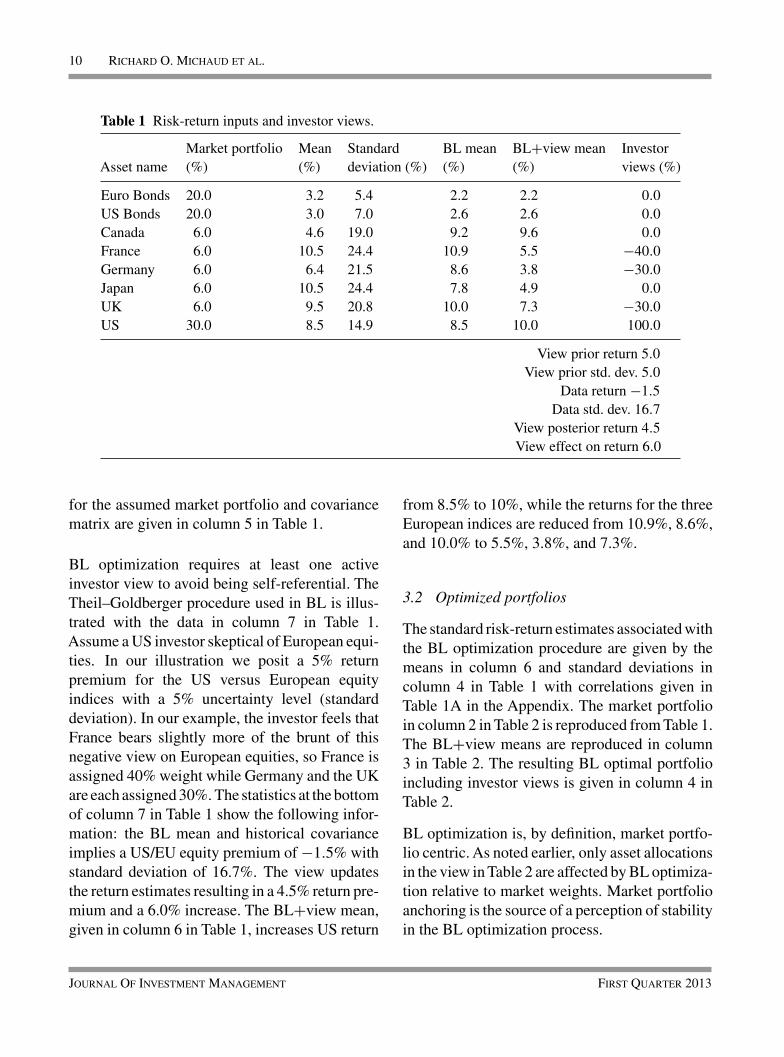

Institutional asset allocation often includes 20 ormore asset classes. For pedagogical clarity andsimplicity, we use the eight asset class datasetdescribed in Michaud (1998) to illustrate the char-acteristics of BL, Markowitz, and Michaud opti-mized portfolios.10 The eight asset classes in thedataset are displayed in column 1 in Table 1 andconsist of two bond and six country equity indices.The historical annualized risk-return estimates arebased on 18 years of monthly returns and given incolumns 3 and 4 in Table 1. The correlations aregiven in Table 1A in the Appendix.

The Michaud dataset reflects a simple globalindex universe. We define a market portfolio asa 60/40 asset mix of domestic and internationalstocks and bonds. For simplicity we equal weightthe bond indices, equal weight US versus non-USequity indices and equal weight non-US indices.Our market portfolio allocations are given in col-umn 2 in Table 1.11 The BL implied or inversemean returns from the Sharpe–Fisher procedure

First Quarter 2013 Journal Of Investment Management

10 Richard O. Michaud et al.

Table 1 Risk-return inputs and investor views.

Market portfolio Mean Standard BL mean BL+view mean InvestorAsset name (%) (%) deviation (%) (%) (%) views (%)

Euro Bonds 20.0 3.2 5.4 2.2 2.2 0.0US Bonds 20.0 3.0 7.0 2.6 2.6 0.0Canada 6.0 4.6 19.0 9.2 9.6 0.0France 6.0 10.5 24.4 10.9 5.5 −40.0Germany 6.0 6.4 21.5 8.6 3.8 −30.0Japan 6.0 10.5 24.4 7.8 4.9 0.0UK 6.0 9.5 20.8 10.0 7.3 −30.0US 30.0 8.5 14.9 8.5 10.0 100.0

View prior return 5.0View prior std. dev. 5.0

Data return −1.5Data std. dev. 16.7

View posterior return 4.5View effect on return 6.0

for the assumed market portfolio and covariancematrix are given in column 5 in Table 1.

BL optimization requires at least one activeinvestor view to avoid being self-referential. TheTheil–Goldberger procedure used in BL is illus-trated with the data in column 7 in Table 1.Assume a US investor skeptical of European equi-ties. In our illustration we posit a 5% returnpremium for the US versus European equityindices with a 5% uncertainty level (standarddeviation). In our example, the investor feels thatFrance bears slightly more of the brunt of thisnegative view on European equities, so France isassigned 40% weight while Germany and the UKare each assigned 30%. The statistics at the bottomof column 7 in Table 1 show the following infor-mation: the BL mean and historical covarianceimplies a US/EU equity premium of −1.5% withstandard deviation of 16.7%. The view updatesthe return estimates resulting in a 4.5% return pre-mium and a 6.0% increase. The BL+view mean,given in column 6 in Table 1, increases US return

from 8.5% to 10%, while the returns for the threeEuropean indices are reduced from 10.9%, 8.6%,and 10.0% to 5.5%, 3.8%, and 7.3%.

3.2 Optimized portfolios

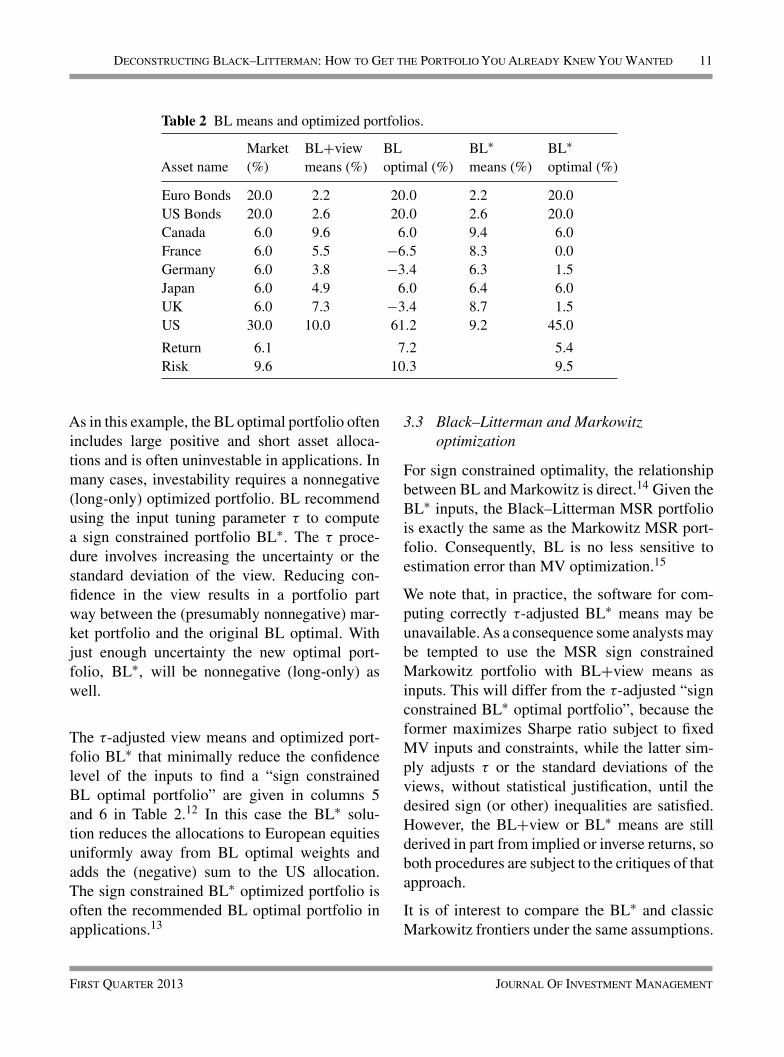

The standard risk-return estimates associated withthe BL optimization procedure are given by themeans in column 6 and standard deviations incolumn 4 in Table 1 with correlations given inTable 1A in the Appendix. The market portfolioin column 2 in Table 2 is reproduced from Table 1.The BL+view means are reproduced in column3 in Table 2. The resulting BL optimal portfolioincluding investor views is given in column 4 inTable 2.

BL optimization is, by definition, market portfo-lio centric. As noted earlier, only asset allocationsin the view in Table 2 are affected by BL optimiza-tion relative to market weights. Market portfolioanchoring is the source of a perception of stabilityin the BL optimization process.

Journal Of Investment Management First Quarter 2013

Deconstructing Black–Litterman: How to Get the Portfolio You Already Knew You Wanted 11

Table 2 BL means and optimized portfolios.

Market BL+view BL BL∗ BL∗Asset name (%) means (%) optimal (%) means (%) optimal (%)

Euro Bonds 20.0 2.2 20.0 2.2 20.0US Bonds 20.0 2.6 20.0 2.6 20.0Canada 6.0 9.6 6.0 9.4 6.0France 6.0 5.5 −6.5 8.3 0.0Germany 6.0 3.8 −3.4 6.3 1.5Japan 6.0 4.9 6.0 6.4 6.0UK 6.0 7.3 −3.4 8.7 1.5US 30.0 10.0 61.2 9.2 45.0

Return 6.1 7.2 5.4Risk 9.6 10.3 9.5

As in this example, the BL optimal portfolio oftenincludes large positive and short asset alloca-tions and is often uninvestable in applications. Inmany cases, investability requires a nonnegative(long-only) optimized portfolio. BL recommendusing the input tuning parameter τ to computea sign constrained portfolio BL∗. The τ proce-dure involves increasing the uncertainty or thestandard deviation of the view. Reducing con-fidence in the view results in a portfolio partway between the (presumably nonnegative) mar-ket portfolio and the original BL optimal. Withjust enough uncertainty the new optimal port-folio, BL∗, will be nonnegative (long-only) aswell.

The τ-adjusted view means and optimized port-folio BL∗ that minimally reduce the confidencelevel of the inputs to find a “sign constrainedBL optimal portfolio” are given in columns 5and 6 in Table 2.12 In this case the BL∗ solu-tion reduces the allocations to European equitiesuniformly away from BL optimal weights andadds the (negative) sum to the US allocation.The sign constrained BL∗ optimized portfolio isoften the recommended BL optimal portfolio inapplications.13

3.3 Black–Litterman and Markowitzoptimization

For sign constrained optimality, the relationshipbetween BL and Markowitz is direct.14 Given theBL∗ inputs, the Black–Litterman MSR portfoliois exactly the same as the Markowitz MSR port-folio. Consequently, BL is no less sensitive toestimation error than MV optimization.15

We note that, in practice, the software for com-puting correctly τ-adjusted BL∗ means may beunavailable. As a consequence some analysts maybe tempted to use the MSR sign constrainedMarkowitz portfolio with BL+view means asinputs. This will differ from the τ-adjusted “signconstrained BL∗ optimal portfolio”, because theformer maximizes Sharpe ratio subject to fixedMV inputs and constraints, while the latter sim-ply adjusts τ or the standard deviations of theviews, without statistical justification, until thedesired sign (or other) inequalities are satisfied.However, the BL+view or BL∗ means are stillderived in part from implied or inverse returns, soboth procedures are subject to the critiques of thatapproach.

It is of interest to compare the BL∗ and classicMarkowitz frontiers under the same assumptions.

First Quarter 2013 Journal Of Investment Management

12 Richard O. Michaud et al.

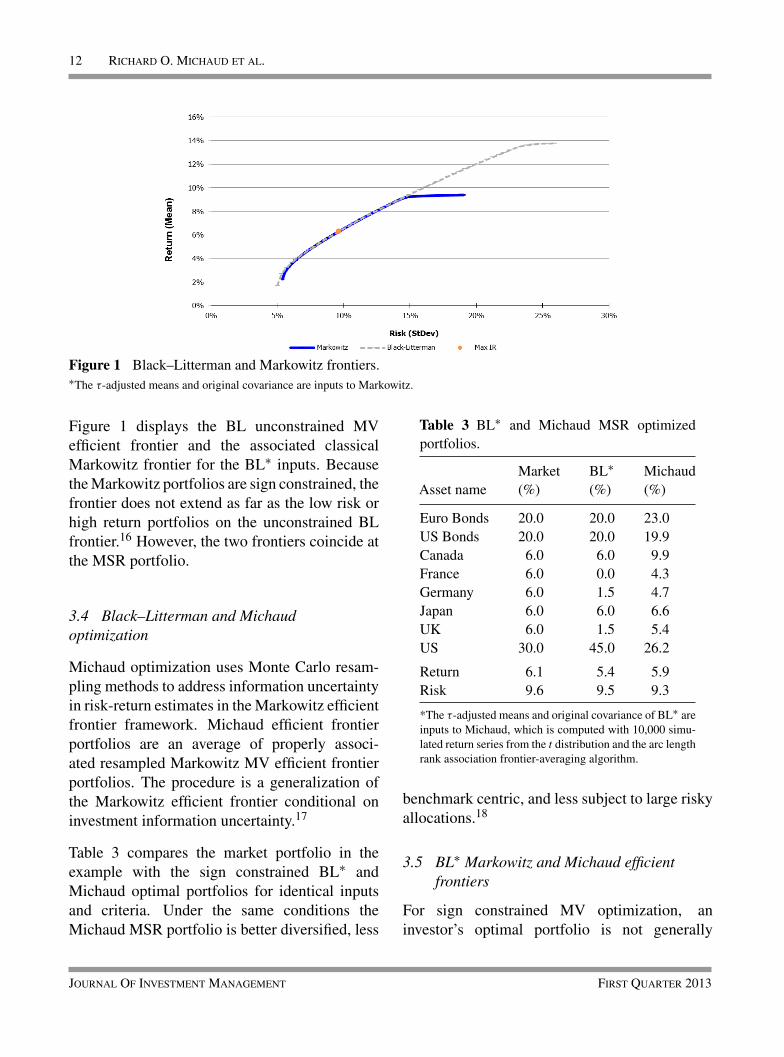

Figure 1 Black–Litterman and Markowitz frontiers.∗The τ-adjusted means and original covariance are inputs to Markowitz.

Figure 1 displays the BL unconstrained MVefficient frontier and the associated classicalMarkowitz frontier for the BL∗ inputs. Becausethe Markowitz portfolios are sign constrained, thefrontier does not extend as far as the low risk orhigh return portfolios on the unconstrained BLfrontier.16 However, the two frontiers coincide atthe MSR portfolio.

3.4 Black–Litterman and Michaudoptimization

Michaud optimization uses Monte Carlo resam-pling methods to address information uncertaintyin risk-return estimates in the Markowitz efficientfrontier framework. Michaud efficient frontierportfolios are an average of properly associ-ated resampled Markowitz MV efficient frontierportfolios. The procedure is a generalization ofthe Markowitz efficient frontier conditional oninvestment information uncertainty.17

Table 3 compares the market portfolio in theexample with the sign constrained BL∗ andMichaud optimal portfolios for identical inputsand criteria. Under the same conditions theMichaud MSR portfolio is better diversified, less

Table 3 BL∗ and Michaud MSR optimizedportfolios.

Market BL∗ MichaudAsset name (%) (%) (%)

Euro Bonds 20.0 20.0 23.0US Bonds 20.0 20.0 19.9Canada 6.0 6.0 9.9France 6.0 0.0 4.3Germany 6.0 1.5 4.7Japan 6.0 6.0 6.6UK 6.0 1.5 5.4US 30.0 45.0 26.2

Return 6.1 5.4 5.9Risk 9.6 9.5 9.3

*The τ-adjusted means and original covariance of BL∗ areinputs to Michaud, which is computed with 10,000 simu-lated return series from the t distribution and the arc lengthrank association frontier-averaging algorithm.

benchmark centric, and less subject to large riskyallocations.18

3.5 BL∗ Markowitz and Michaud efficientfrontiers

For sign constrained MV optimization, aninvestor’s optimal portfolio is not generally

Journal Of Investment Management First Quarter 2013

Deconstructing Black–Litterman: How to Get the Portfolio You Already Knew You Wanted 13

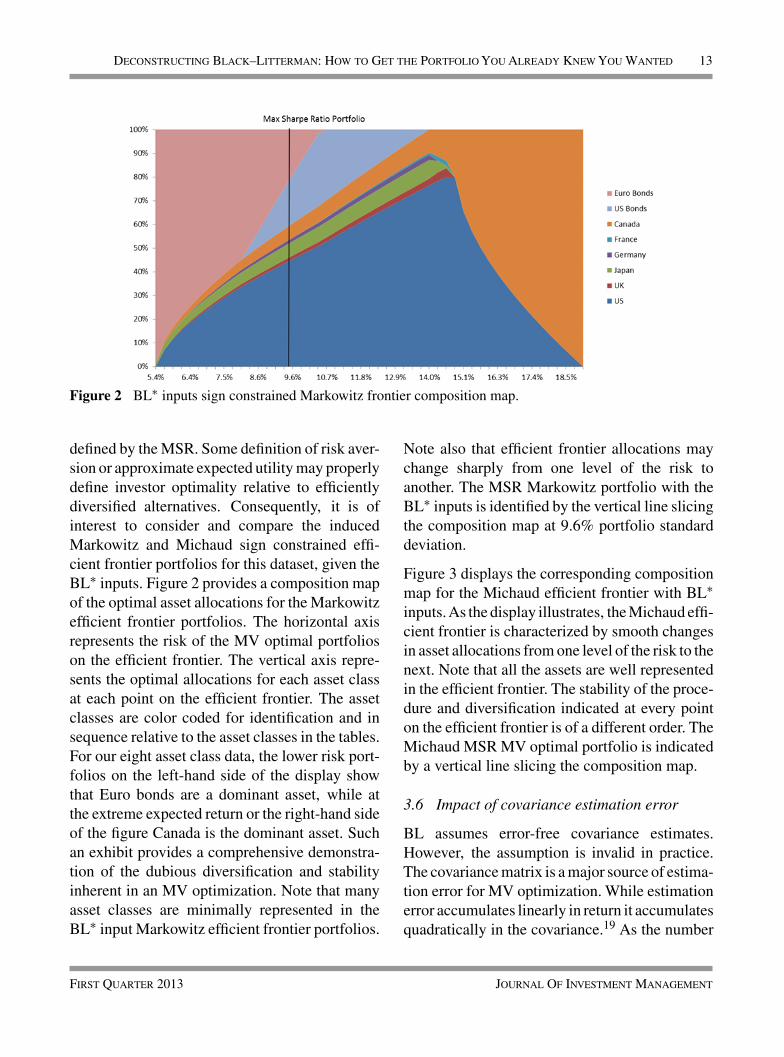

Figure 2 BL∗ inputs sign constrained Markowitz frontier composition map.

defined by the MSR. Some definition of risk aver-sion or approximate expected utility may properlydefine investor optimality relative to efficientlydiversified alternatives. Consequently, it is ofinterest to consider and compare the inducedMarkowitz and Michaud sign constrained effi-cient frontier portfolios for this dataset, given theBL∗ inputs. Figure 2 provides a composition mapof the optimal asset allocations for the Markowitzefficient frontier portfolios. The horizontal axisrepresents the risk of the MV optimal portfolioson the efficient frontier. The vertical axis repre-sents the optimal allocations for each asset classat each point on the efficient frontier. The assetclasses are color coded for identification and insequence relative to the asset classes in the tables.For our eight asset class data, the lower risk port-folios on the left-hand side of the display showthat Euro bonds are a dominant asset, while atthe extreme expected return or the right-hand sideof the figure Canada is the dominant asset. Suchan exhibit provides a comprehensive demonstra-tion of the dubious diversification and stabilityinherent in an MV optimization. Note that manyasset classes are minimally represented in theBL∗ input Markowitz efficient frontier portfolios.

Note also that efficient frontier allocations maychange sharply from one level of the risk toanother. The MSR Markowitz portfolio with theBL∗ inputs is identified by the vertical line slicingthe composition map at 9.6% portfolio standarddeviation.

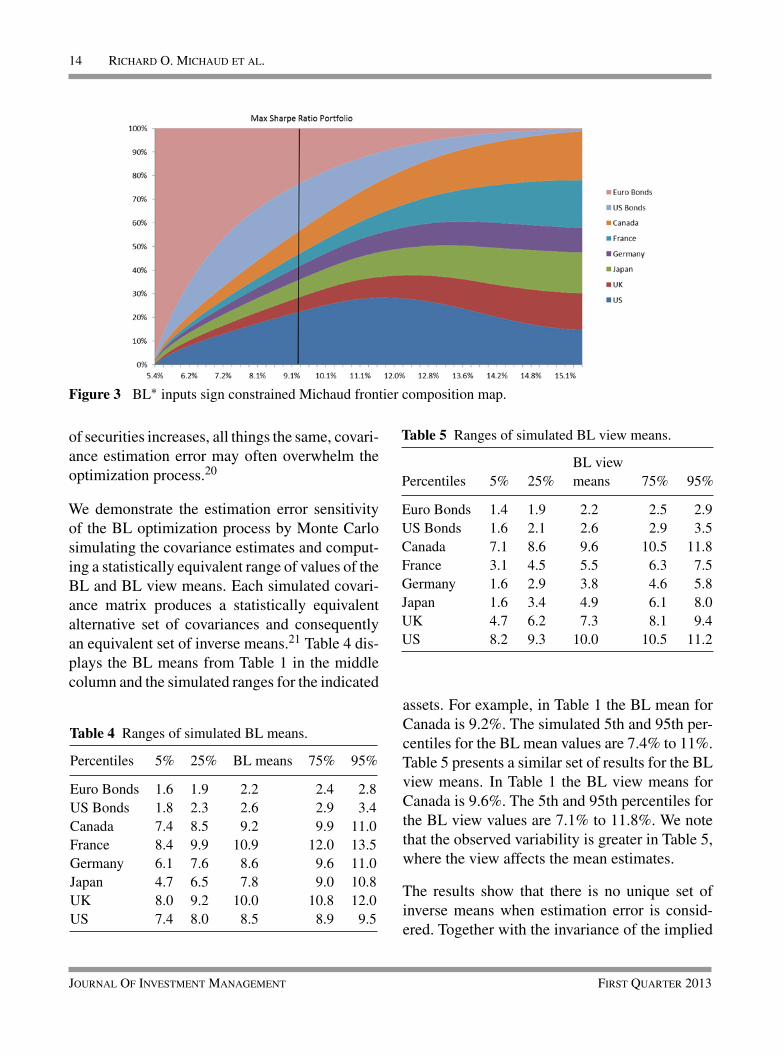

Figure 3 displays the corresponding compositionmap for the Michaud efficient frontier with BL∗inputs.As the display illustrates, the Michaud effi-cient frontier is characterized by smooth changesin asset allocations from one level of the risk to thenext. Note that all the assets are well representedin the efficient frontier. The stability of the proce-dure and diversification indicated at every pointon the efficient frontier is of a different order. TheMichaud MSR MV optimal portfolio is indicatedby a vertical line slicing the composition map.

3.6 Impact of covariance estimation error

BL assumes error-free covariance estimates.However, the assumption is invalid in practice.The covariance matrix is a major source of estima-tion error for MV optimization. While estimationerror accumulates linearly in return it accumulatesquadratically in the covariance.19 As the number

First Quarter 2013 Journal Of Investment Management

14 Richard O. Michaud et al.

Figure 3 BL∗ inputs sign constrained Michaud frontier composition map.

of securities increases, all things the same, covari-ance estimation error may often overwhelm theoptimization process.20

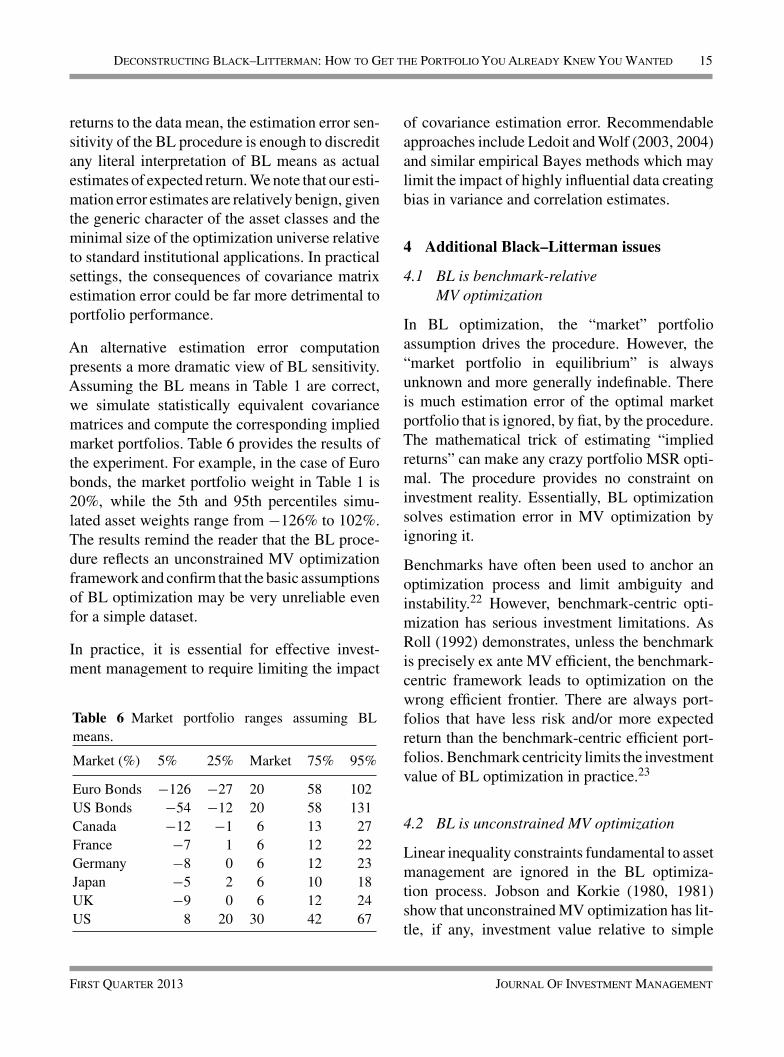

We demonstrate the estimation error sensitivityof the BL optimization process by Monte Carlosimulating the covariance estimates and comput-ing a statistically equivalent range of values of theBL and BL view means. Each simulated covari-ance matrix produces a statistically equivalentalternative set of covariances and consequentlyan equivalent set of inverse means.21 Table 4 dis-plays the BL means from Table 1 in the middlecolumn and the simulated ranges for the indicated

Table 4 Ranges of simulated BL means.

Percentiles 5% 25% BL means 75% 95%

Euro Bonds 1.6 1.9 2.2 2.4 2.8US Bonds 1.8 2.3 2.6 2.9 3.4Canada 7.4 8.5 9.2 9.9 11.0France 8.4 9.9 10.9 12.0 13.5Germany 6.1 7.6 8.6 9.6 11.0Japan 4.7 6.5 7.8 9.0 10.8UK 8.0 9.2 10.0 10.8 12.0US 7.4 8.0 8.5 8.9 9.5

Table 5 Ranges of simulated BL view means.

BL viewPercentiles 5% 25% means 75% 95%

Euro Bonds 1.4 1.9 2.2 2.5 2.9US Bonds 1.6 2.1 2.6 2.9 3.5Canada 7.1 8.6 9.6 10.5 11.8France 3.1 4.5 5.5 6.3 7.5Germany 1.6 2.9 3.8 4.6 5.8Japan 1.6 3.4 4.9 6.1 8.0UK 4.7 6.2 7.3 8.1 9.4US 8.2 9.3 10.0 10.5 11.2

assets. For example, in Table 1 the BL mean forCanada is 9.2%. The simulated 5th and 95th per-centiles for the BL mean values are 7.4% to 11%.Table 5 presents a similar set of results for the BLview means. In Table 1 the BL view means forCanada is 9.6%. The 5th and 95th percentiles forthe BL view values are 7.1% to 11.8%. We notethat the observed variability is greater in Table 5,where the view affects the mean estimates.

The results show that there is no unique set ofinverse means when estimation error is consid-ered. Together with the invariance of the implied

Journal Of Investment Management First Quarter 2013

Deconstructing Black–Litterman: How to Get the Portfolio You Already Knew You Wanted 15

returns to the data mean, the estimation error sen-sitivity of the BL procedure is enough to discreditany literal interpretation of BL means as actualestimates of expected return. We note that our esti-mation error estimates are relatively benign, giventhe generic character of the asset classes and theminimal size of the optimization universe relativeto standard institutional applications. In practicalsettings, the consequences of covariance matrixestimation error could be far more detrimental toportfolio performance.

An alternative estimation error computationpresents a more dramatic view of BL sensitivity.Assuming the BL means in Table 1 are correct,we simulate statistically equivalent covariancematrices and compute the corresponding impliedmarket portfolios. Table 6 provides the results ofthe experiment. For example, in the case of Eurobonds, the market portfolio weight in Table 1 is20%, while the 5th and 95th percentiles simu-lated asset weights range from −126% to 102%.The results remind the reader that the BL proce-dure reflects an unconstrained MV optimizationframework and confirm that the basic assumptionsof BL optimization may be very unreliable evenfor a simple dataset.

In practice, it is essential for effective invest-ment management to require limiting the impact

Table 6 Market portfolio ranges assuming BLmeans.

Market (%) 5% 25% Market 75% 95%

Euro Bonds −126 −27 20 58 102US Bonds −54 −12 20 58 131Canada −12 −1 6 13 27France −7 1 6 12 22Germany −8 0 6 12 23Japan −5 2 6 10 18UK −9 0 6 12 24US 8 20 30 42 67

of covariance estimation error. Recommendableapproaches include Ledoit and Wolf (2003, 2004)and similar empirical Bayes methods which maylimit the impact of highly influential data creatingbias in variance and correlation estimates.

4 Additional Black–Litterman issues

4.1 BL is benchmark-relativeMV optimization

In BL optimization, the “market” portfolioassumption drives the procedure. However, the“market portfolio in equilibrium” is alwaysunknown and more generally indefinable. Thereis much estimation error of the optimal marketportfolio that is ignored, by fiat, by the procedure.The mathematical trick of estimating “impliedreturns” can make any crazy portfolio MSR opti-mal. The procedure provides no constraint oninvestment reality. Essentially, BL optimizationsolves estimation error in MV optimization byignoring it.

Benchmarks have often been used to anchor anoptimization process and limit ambiguity andinstability.22 However, benchmark-centric opti-mization has serious investment limitations. AsRoll (1992) demonstrates, unless the benchmarkis precisely ex ante MV efficient, the benchmark-centric framework leads to optimization on thewrong efficient frontier. There are always port-folios that have less risk and/or more expectedreturn than the benchmark-centric efficient port-folios. Benchmark centricity limits the investmentvalue of BL optimization in practice.23

4.2 BL is unconstrained MV optimization

Linear inequality constraints fundamental to assetmanagement are ignored in the BL optimiza-tion process. Jobson and Korkie (1980, 1981)show that unconstrained MV optimization has lit-tle, if any, investment value relative to simple

First Quarter 2013 Journal Of Investment Management

16 Richard O. Michaud et al.

equal weighting. Frost and Savarino (1988)demonstrate that constraints often reduce theimpact of estimation error on MV optimality.Regulatory restrictions and institutional limita-tions are real-world considerations in defining anoptimal portfolio. Importantly, Markowitz (2005)shows that consideration of necessary linear con-straints in any practical application of portfoliooptimization alters the viability of tools of modernportfolio management and important theoremsof modern finance. From either a theoretical orpractical point of view, proper linear constraintsare a necessary condition for effective investmentmanagement.

4.3 BL ignores investor risk aversion

BL optimization computes a single optimal port-folio and does not control for level of investorrisk aversion. However, a wide consensus existsin the academic and professional financial com-munity that the choice of portfolio risk is thesingle most important investment decision.24 Thelinear constrained Markowitz and Michaud effi-cient frontiers provide a range of risk habitatsfor rational investment decision making. The BLportfolio risk level may often be inappropriate formany investors. Efficient frontiers are essentialfor managing investor risk habitats.

5 Summary and conclusion

Black–Litterman (BL) (1992) optimization pro-duces a single maximum Sharpe ratio (MSR)optimal portfolio on the unconstrained MV effi-cient frontier based on an assumed MSR opti-mal benchmark portfolio and active views. BLoptimization often results in uninvestable port-folios in applications due to large leveragedand/or short allocations. BL introduce an inputtuning parameter τ to compute BL∗ sign con-strained portfolios. We present a mathematical

and statistical analysis of BL optimization andillustrate the procedure with a simple datasetof eight asset classes. We compare constrainedBL with Markowitz and Michaud under identicalconditions.

BL optimization claims to solve the investmentlimitations in practice associated with classi-cal Markowitz MV optimization. However, weshow that the ad hoc “market” portfolio assump-tion drives the process and that the estimationerror associated with estimating the “market port-folio in equilibrium” is solved by ignoring it.In addition, the unconstrained MV optimizationframework used by BL is known to have little,if any, investment value, and sign-constrainedBL optimization is identical to Markowitz andconsequently inherits the known limitations ofMV optimization. Moreover, the process of com-puting “inverse” returns and adjusting the priorwith τ-adjustment is inconsistent with princi-ples of modern statistical inference and rigor-ous Bayesian analysis. Finally, the BL optimalsolution ignores the importance of investor riskaversion, while the resampling process associatedwith Michaud optimization produces superior riskmanaged and diversified portfolios.

Portfolio “acceptability” is more the norm forasset management in practice than widely rec-ognized. Many investment firms do not useoptimization technology and their investmentprocess closely mirrors the BL framework ofpositing a benchmark and considering invest-ment tilts.25 Even in a more formal optimizationinvestment process, instability and unintuitive-ness often motivate ad hoc practices that amountto little more than the computation of a commit-tee’s notion of “acceptable” portfolios. However,acceptable is not investment effective. Effectiveasset management requires an inequality con-strained optimization framework, an efficientfrontier of optimal risk managed portfolios for

Journal Of Investment Management First Quarter 2013

Deconstructing Black–Litterman: How to Get the Portfolio You Already Knew You Wanted 17

satisfying risk habitats, input estimation con-sistent with modern statistical inference, andestimation error effective portfolio optimiza-tion. While BL may be convenient it isnot recommendable, given available alter-natives. The potential for adding valuewith rigorous investment and statistical

principles seems a challenge well worth theeffort.

Acknowledgment

We wish to acknowledge the helpful commentsby Paul Erlich.

Appendix

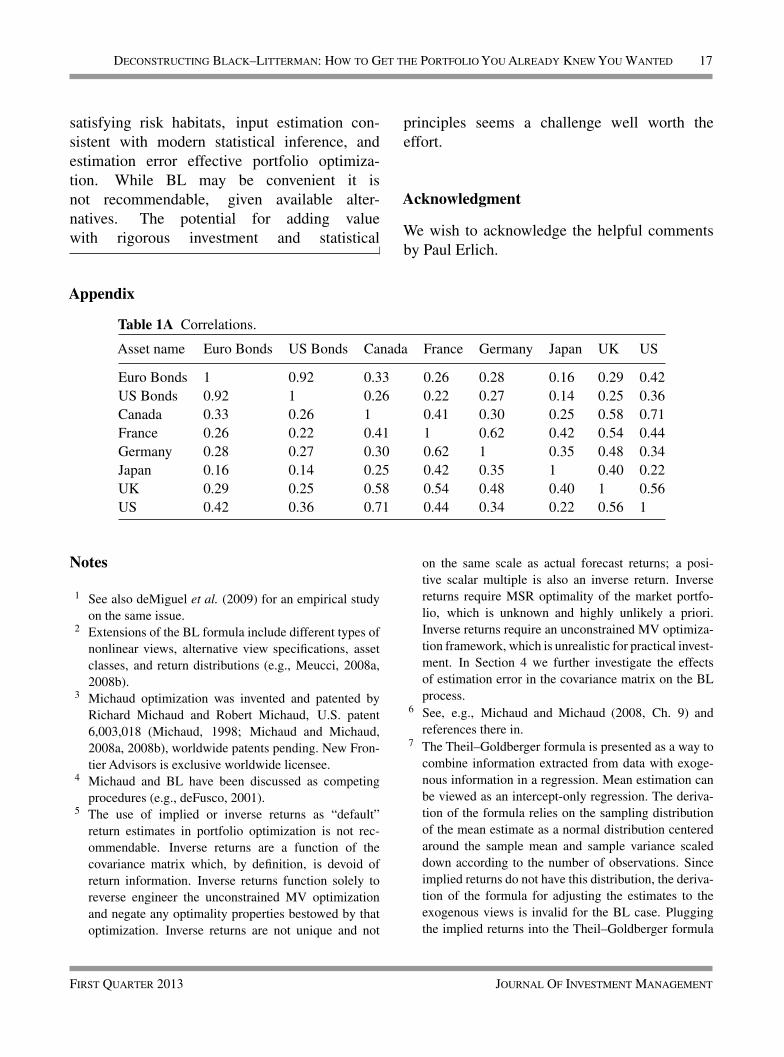

Table 1A Correlations.

Asset name Euro Bonds US Bonds Canada France Germany Japan UK US

Euro Bonds 1 0.92 0.33 0.26 0.28 0.16 0.29 0.42US Bonds 0.92 1 0.26 0.22 0.27 0.14 0.25 0.36Canada 0.33 0.26 1 0.41 0.30 0.25 0.58 0.71France 0.26 0.22 0.41 1 0.62 0.42 0.54 0.44Germany 0.28 0.27 0.30 0.62 1 0.35 0.48 0.34Japan 0.16 0.14 0.25 0.42 0.35 1 0.40 0.22UK 0.29 0.25 0.58 0.54 0.48 0.40 1 0.56US 0.42 0.36 0.71 0.44 0.34 0.22 0.56 1

Notes

1 See also deMiguel et al. (2009) for an empirical studyon the same issue.

2 Extensions of the BL formula include different types ofnonlinear views, alternative view specifications, assetclasses, and return distributions (e.g., Meucci, 2008a,2008b).

3 Michaud optimization was invented and patented byRichard Michaud and Robert Michaud, U.S. patent6,003,018 (Michaud, 1998; Michaud and Michaud,2008a, 2008b), worldwide patents pending. New Fron-tier Advisors is exclusive worldwide licensee.

4 Michaud and BL have been discussed as competingprocedures (e.g., deFusco, 2001).

5 The use of implied or inverse returns as “default”return estimates in portfolio optimization is not rec-ommendable. Inverse returns are a function of thecovariance matrix which, by definition, is devoid ofreturn information. Inverse returns function solely toreverse engineer the unconstrained MV optimizationand negate any optimality properties bestowed by thatoptimization. Inverse returns are not unique and not

on the same scale as actual forecast returns; a posi-tive scalar multiple is also an inverse return. Inversereturns require MSR optimality of the market portfo-lio, which is unknown and highly unlikely a priori.Inverse returns require an unconstrained MV optimiza-tion framework, which is unrealistic for practical invest-ment. In Section 4 we further investigate the effectsof estimation error in the covariance matrix on the BLprocess.

6 See, e.g., Michaud and Michaud (2008, Ch. 9) andreferences there in.

7 The Theil–Goldberger formula is presented as a way tocombine information extracted from data with exoge-nous information in a regression. Mean estimation canbe viewed as an intercept-only regression. The deriva-tion of the formula relies on the sampling distributionof the mean estimate as a normal distribution centeredaround the sample mean and sample variance scaleddown according to the number of observations. Sinceimplied returns do not have this distribution, the deriva-tion of the formula for adjusting the estimates to theexogenous views is invalid for the BL case. Pluggingthe implied returns into the Theil–Goldberger formula

First Quarter 2013 Journal Of Investment Management

18 Richard O. Michaud et al.

is an approximation with unknown bias and errorproperties.

8 We use the traditional notation of the BL literature (e.g.,Black and Litterman, 1992; Meucci, 2008a).

9 See Markowitz (2005) for a discussion of why inequal-ity constraints are fundamentally important for financialtheory as well as practical application.

10 This dataset is widely available and has been usedin a number of estimation error optimization studies.We note that the pedagogical simplicity of a relativelysmall generic set of assets may minimize the instabilitythat often exists in institutional asset allocation port-folios, particularly with respect to estimation error inthe covariance matrix which accumulates quickly as thenumber of assets increases.

11 We note that this “market” portfolio is in fact very closeto in-sample MV efficient for the data.

12 The value of τ for the BL∗ portfolio is approximately0.0702788871. The sign constrained BL optimal portfo-lio can be computed directly by dividing the view stan-dard deviation, 5% in Table 1, by

√τ = 0.26510165421,

resulting in a revised standard deviation of18.8607%.

13 As noted earlier, 1/T is sometimes proposed as the valueof tau in the Black–Litterman formula. For this choiceof τ, the BL solution for our example is nearly thesame as in Table 2: 20%, 20%, 6%, 0.11%, 1.58%,6%, 1.58%, and 44.73%. For a rigorous data-drivenBayesian analysis, tau represents the factor 1/T whichmultiplies the covariance matrix of an observation toobtain the covariance of the sample mean vector. Theprocedure is, of course, incorrect for implied returns.Because of the arbitrary scaling of the view standarddeviations, setting τ, to 1/T does not change any of ourconclusions.

14 These results can be generalized for inequality con-strained optimality.

15 It is worth noting that the formal identity between theBL and Markowitz MSR portfolios with BL∗ inputs inno way indicates foundational similarity. Unlike BL,the Markowitz MV framework is consistent with stan-dard statistical procedures of inference purely fromdata.

16 We note that reasonable asset upper bounds on the BLunconstrained efficient frontier were necessary in orderthat the graph of the frontier would be bounded above.

17 The assumed level of information in risk-return inputs isa parameter of the Michaud optimization process. Dif-ferent levels of information lead to different efficient

frontiers. In this context the Markowitz efficient fron-tier is a Michaud frontier conditional on 100% certainty.See Michaud and Michaud (2008a, Ch. 6) for furtherdiscussion of the patented Forecast Certainty (FC) levelparameter. In this case the parameter has been set tomatch the 18 years of monthly historical return data inthe Michaud dataset.

18 Rigorous simulation studies have also shown thatthe Michaud optimized portfolios enhance the out-of-sample investment value of optimized portfolios relativeto the MV optimized alternatives (Michaud, 1998,Ch. 6; Markowitz and Usmen (MU), 2003), Michaudand Michaud (2008a, 2008b). Harvey et al. (HLL)(2008a) present two studies where they dispute theinvestment enhancement results of Michaud optimiza-tion reported in MU. However, Michaud and Michaud(2008c) note that the HLL studies possess significantissues that limit the reliability of their conclusions.Michaud and Michaud (2008c) conclude that HLL’sresults do not contradict either MU or previous workby Michaud, which they acknowledge in Harvey et al.(2008b).

19 Noted by Jorion and referenced in Michaud (1998),personal communication.

20 There is a persistent widespread error associated withthe relative importance of estimation error in returnrelative to risk or the covariance matrix in the pro-fessional and academic financial community, usuallyassociated with Chopra and Ziemba (1993). Their anal-ysis is an in-sample and utility function specific studythat in no way correctly represents the actual results ofthe impact of estimation error in rigorous out-of-sampleMV optimization simulation tests. As Jorion has noted,estimation error in the covariance matrix may often over-whelm the optimization process as the number of assetsincreases.

21 This simulation requires some care. This is because thecovariance matrix is devoid of information on return andimplied market weights are unique only up to a pos-itive scalar multiple. The simulations in Tables 4 and5 are normalized so that the average return is alwaysthe same as for the original BL means. The assumptionof which mean is not material to the simulations. Theassumption that the mean is the same limits observedvariability.

22 There may be financially valid reasons for usingbenchmark-centric optimization. One example may bethe definition of a benchmark in terms of the “useof invested assets.” In this context the benchmark

Journal Of Investment Management First Quarter 2013

Deconstructing Black–Litterman: How to Get the Portfolio You Already Knew You Wanted 19

portfolio may represent an individual’s or institution’sliability. Grinold and Kahn (1995) provide a usefulresidual return framework suitable for many equity port-folio management mandates in institutional practice.However, their analysis is generally not addressed toasset allocation applications. See Michaud and Michaud(2008a, Chs. 9, 10) for further references.

23 Roll notes in his conclusion that the suboptimality of thebenchmark may need to be balanced against the impactof estimation error on MV optimization.

24 Brinson et al. (1986, 1991).25 The process is described in Michaud (1989).

References

Black, F. and Litterman, R. (1992). “Global Portfo-lio Optimization,” Financial Analysts Journal 48(5),32–43.

Brinson, G., Hood, R., and Beebower, G. (1986). “Deter-minants of Portfolio Performance,” Financial AnalystJournal 42(4), 39–44.

Brinson, G., Singer, B., and Beebower, G. (1991).“Determinants of Portfolio Performance II: An Update,”Financial Analysts Journal 47(3), 40–48.

DeFusco, R., McLeavey, D., Pinto, J., and Runkle,D. (2001). Quantitative Methods for Investment Anal-ysis. Charlottesville, VA: Association for InvestmentManagement and Research.

DeMiguel, V., Garlappi, L., and Uppal, R. (2009). “Optimalversus Naive Diversification: How Inefficient is the 1/NPortfolio Strategy?” Review of Financial Studies 22(5),1915–1953.

Fisher, L. (1975). “Using Modern Portfolio Theory toMaintain an Efficiently Diversified Portfolio,” FinancialAnalysts Journal 31(3), 73–85.

Frost, P. A. and Savarino, J. E. (1988). “For Better Perfor-mance Constrain Portfolio Weights,” Journal of PortfolioManagement 15, 29–34.

Grinold, R. and Kahn, R. (1995). Active Portfolio Manage-ment: Quantitative Theory and Applications. Chicago:Irwin.

Harvey, C., Liechty, J., and Liechty, M. (2008a). “Bayesvs. Resampling: A Rematch,” Journal of InvestmentManagement 6(1), 29–45.

Harvey, C., Liechty, J., and Liechty, M. (2008b). “AResponse to Richard Michaud and Robert Michaud:

Letter to the Editor,” Journal of Investment Management6(3), 114.

Jobson, J. D. and Korkie, B. (1980). “Estimation forMarkowitz Efficient Portfolios,” Journal of the AmericanStatistical Association 75(371), 544–555.

Jobson, J. D. and Korkie, B. (1981). “Putting MarkowitzTheory to Work,” Journal of Portfolio Management 7(4),70–74.

Ledoit, O. and Wolf, M. (2003). “Improved Estimationof the Covariance Matrix of Stock Returns with anApplication to Portfolio Selection,” Journal of EmpiricalFinance 10, 603–621.

Ledoit, O. and Wolf, M. (2004). “A Well-ConditionedEstimator for Large-Dimensional Covariance Matrices,”Journal of Multivariate Analysis 88, 365–411.

Markowitz, H. (1952). “Portfolio Selection,” Journal ofFinance 7(1), 77–91.

Markowitz, H. (1959). Portfolio Selection: Efficient Diver-sification of Investments, 2nd ed. New York: Wiley.Cambridge, MA: Basil Blackwell, 1991.

Markowitz, H. (2005). “Market Efficiency: A TheoreticalDistinction and So What!” Financial Analysts Journal61(5), 17–30.

Markowitz, H. and Usmen, N. (2004). “Resampled Fron-tiers versus Diffuse Bayes: An Experiment,” Journal ofInvestment Management 1(4), 9–25.

Meucci, A. (2008a). “The Black–Litterman Approach:Original Model and Extensions,” in The Encyclopediaof Quantitative Finance, Wiley, 2010.

Meucci, A. (2008b) “Fully Flexible Views: Theory andPractice Fully Flexible Views: Theory and Practice,” Risk21(10), 97–102.

Michaud, R. (1989). “The Markowitz OptimizationEnigma: Is Optimized Optimal?” Financial AnalystsJournal 45(1), 31–42.

Michaud, R. and Michaud, R. (2008a). Efficient Asset Man-agement: A Practical Guide to Stock Portfolio Optimiza-tion and Asset Allocation. New York: Oxford UniversityPress. 1st ed. 1998, Originally Published by HarvardBusiness School Press, Boston.

Michaud, R. and Michaud, Robert (2008b). “Estima-tion Error and Portfolio Optimization: A ResamplingSolution,” Journal of Investment Management 6(1),8–28.

Michaud, R. and Michaud, Robert (2008c). “Discussion onarticle by C. Harvey, J. Liechty, and M. Liechty: Letterto the Editor,” Journal of Investment Management 6(3),113–114.

First Quarter 2013 Journal Of Investment Management

20 Richard O. Michaud et al.

Roll, R. (1992). “A Mean/Variance Analysis of TrackingError,” Journal of Portfolio Management 18(4), 13–22.

Sharpe, W. (1974). “Imputing Expected Returns fromPortfolio Composition,” Journal of Financial and Quan-titative Analysis 9(3), 463–472.

Theil, H. and Goldberger, A. (1961). “On Pure and MixedStatistical Estimation in Economics,” International Eco-nomic Review 2(1), 65–78.

Keywords: Portfolio optimization; asset alloca-tion; Black–Litterman; Markowitz optimization;Michaud optimization; estimation error; MonteCarlo simulation; Bayesian theory; impliedreturns; unconstrained optimization; market equi-librium portfolio; computational finance.

Journal Of Investment Management First Quarter 2013