natural gas markets, mechanisms - platts gas markets, structures, and ... you may use the prices,...

TRANSCRIPT

NATURAL GAS MARKETS, STRUCTURES, AND MECHANISMS Mitchell DeRubis, Senior Energy Analyst Bob Yu, Senior Energy Analyst

• Restrictions on Use: You may use the prices, indexes, assessments and other related information (collectively, “Data”) in this presentation only for your personal use. You may not publish, reproduce, distribute, retransmit, resell, create any derivative work from and/or otherwise provide access to Data or any portion thereof to any person (either within or outside your company including, but not limited to, via or as part of any internal electronic system or Internet site), firm or entity. Disclaimer: Platts, its affiliates and all of their third-party licensors disclaim any and all representations and warranties, express or implied, including, but not limited to, any warranties of merchantability or fitness for a particular purpose or use as to the data, or the results obtained by its use or as to the performance thereof. Limitation of Liability: In no event whatsoever shall Platts, its affiliates or their third-party licensors be liable for any indirect, special, incidental, punitive or consequential damages, including but not limited to loss of profits, trading losses, or lost time or goodwill, even if they have been advised of the possibility of such damages, whether in contract, tort, strict liability or otherwise. The Data is provided on an “as is” basis and your use of the Data is at your own risk. Copyright © 2016 by Platts, McGraw Hill Financial, Inc. All rights reserved. No portion of this publication may be photocopied, reproduced, retransmitted, put into a computer system or otherwise redistributed without prior authorization from Platts. Platts is a trademark of McGraw Hill Financial.

NATURAL GAS MIDSTREAM FUNDAMENTALS

Mitchell DeRubis, Senior Energy Analyst

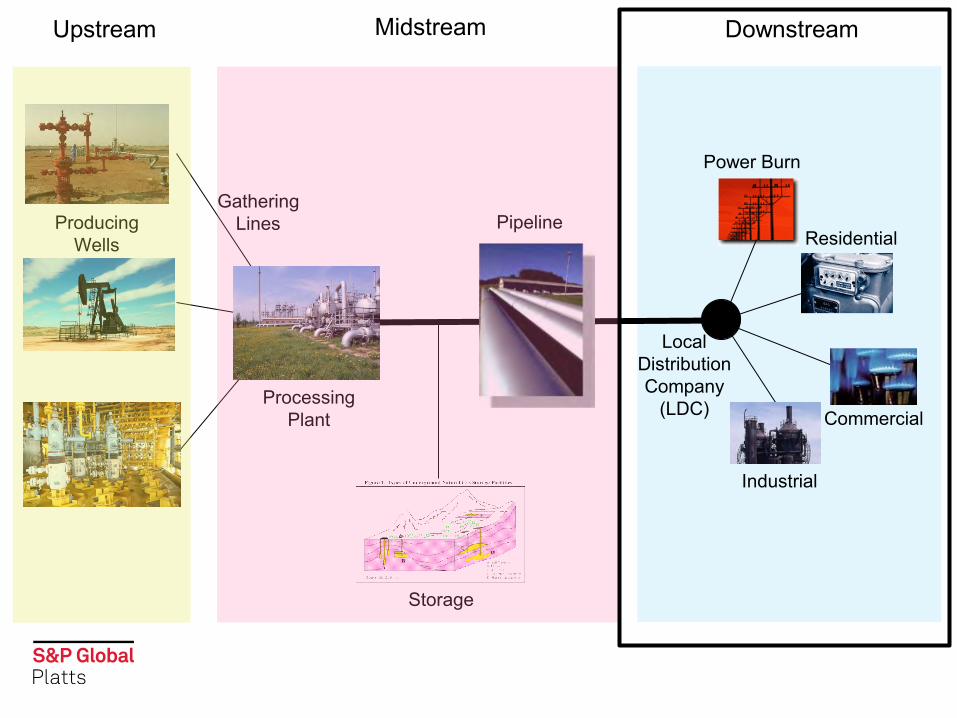

Production Demand

Supply Demand

Where it’s needed, when it’s needed

From Wellhead

Producing Basin

Processing Gathering

Source: EIA

Benposium 2017

To Burner-Tip

Storage

LDC

Industrial

Power

Industrial

Power

Res/Comm

Benposium 2017

Storage

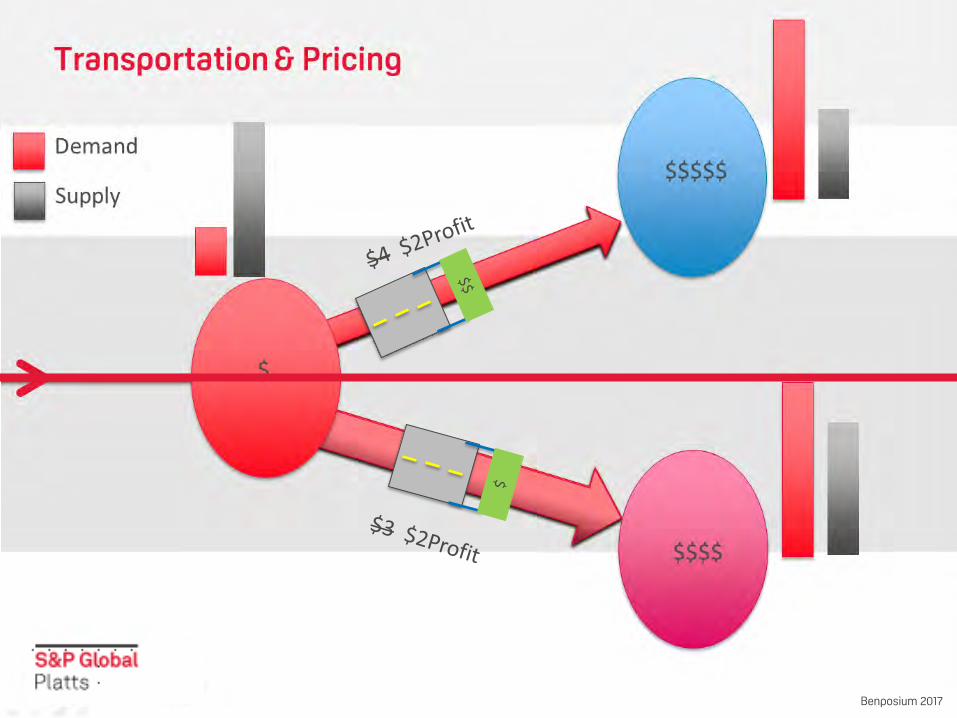

Transportation & Pricing

Demand

Supply $$$$ $$$$$

Hub $

$ $

$

$

$

$

$

$

$

Surp

lus

Sho

rtage

Sho

rtage

$

$

$

$$

$$$$ $$$

$$$

$$$

Prices reflect Supply/Demand Balance

Benposium 2017

Benposium 2017

• Firm • Reserved • Reservation rate (fixed) + variable costs

• Interruptible • Variable costs only

Quick Microeconomics Refresher

P

Q

ATC

AVC

MC

P = MR PROFIT

LOSS

FC

AFC

Benposium 2017

P = Price, Q = Quantity, MR = Marginal Revenue, MC = Marginal Cost, ATC = Average Total Cost, AVC = Average Variable Cost

How Does This Apply to Pipeline Economics?

P

Q

MC

MR = D

ATC

Benposium 2017

Benposium 2017

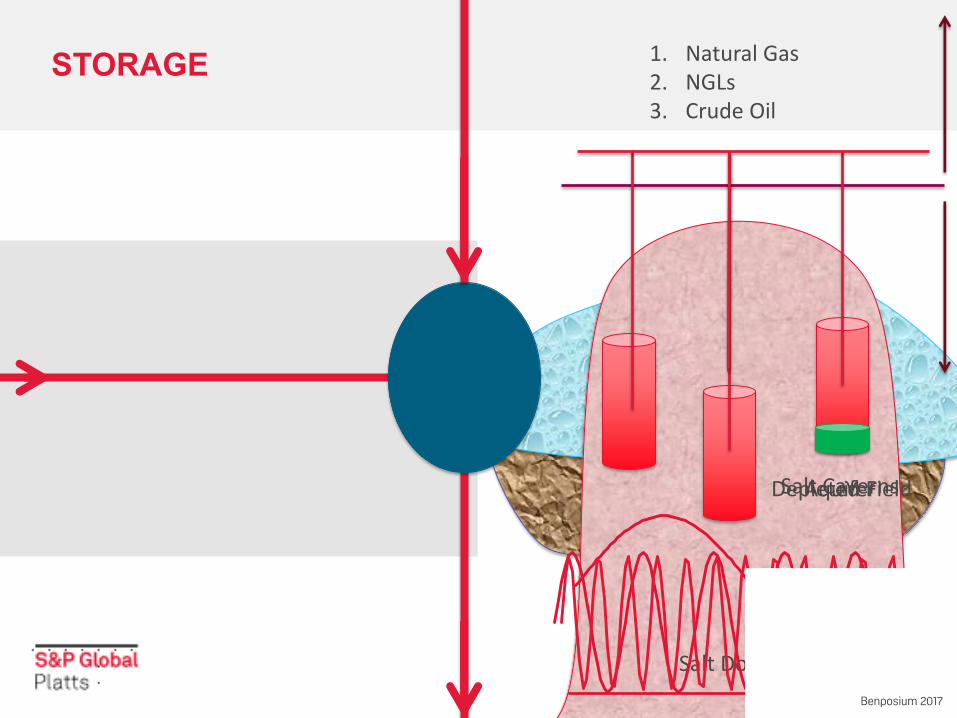

STORAGE

Salt Dome

Salt Caverns Aquifer Depleted Field

1. Natural Gas 2. NGLs 3. Crude Oil

Benposium 2017

STORAGE

Benposium 2017

1 Tcf Aquifer

Depleted Field

Salt Dome

1.2 Tcf

461 Bcf

416 Bcf

1.5 Tcf

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

01-Jan-10 01-Jan-11 01-Jan-12 01-Jan-13 01-Jan-14 01-Jan-15 01-Jan-16 01-Jan-17

Bcf

US Inventories

$2.00

$2.20

$2.40

$2.60

$2.80

$3.00

$3.20

$3.40

$3.60

$/M

MB

tu Henry Hub Futures

Intrinsic Value

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

(1,500)

(1,000)

(500)

-

500

1,000

1,500

$/M

MB

tu

Bcf

Henry Hub Vs. Rolling 5-Year Storage Surplus/Deficit

Historic Surplus/Deficit Henry Hub Cash

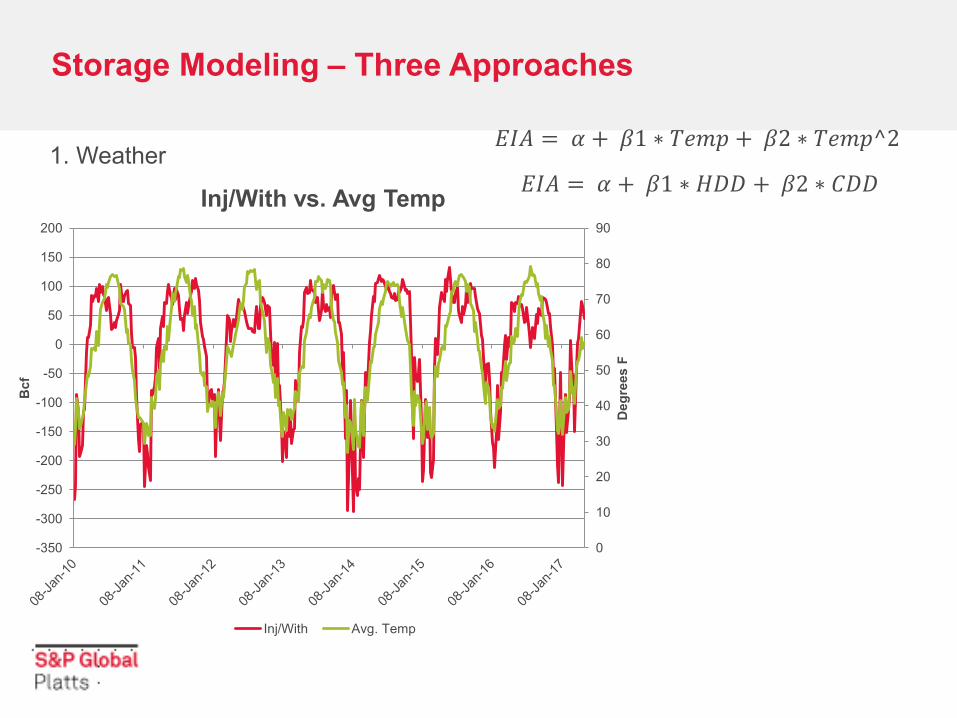

Storage Modeling – Three Approaches

1. Weather

0

10

20

30

40

50

60

70

80

90

-350

-300

-250

-200

-150

-100

-50

0

50

100

150

200

Deg

rees

F

Bcf

Inj/With vs. Avg Temp

Inj/With Avg. Temp

𝐸𝐼𝐴 = 𝛼 + 𝛽1 ∗ 𝑇𝑒𝑚𝑝 + 𝛽2 ∗ 𝑇𝑒𝑚𝑝^2

𝐸𝐼𝐴 = 𝛼 + 𝛽1 ∗ 𝐻𝐷𝐷 + 𝛽2 ∗ 𝐶𝐷𝐷

Storage Modeling – Three Approaches

2. Supply/Demand Implied

Total Supply

Total Demand

𝐸𝐼𝐴 = 𝑇𝑜𝑡𝑎𝑙 𝑆𝑢𝑝𝑝𝑙𝑦 − 𝑇𝑜𝑡𝑎𝑙 𝐷𝑒𝑚𝑎𝑛𝑑

Total Supply = 496 +41 +3 = 540 Bcf

Total Demand = 29 + 15 + 446 = 490 Bcf

Storage Modeling – Three Approaches

3. Storage Sample / Flow Based

-100

-80

-60

-40

-20

0

20

40

60

Bcf

Midwest Sample vs. EIA

Midwest Sample Midwest Non-Sample

𝐸𝐼𝐴 = 𝛼 + 𝛽1 ∗ 𝑆𝑎𝑚𝑝𝑙𝑒

NATURAL GAS DOWNSTREAM FUNDAMENTALS

Bob Yu, Senior Energy Analyst

No content below the line No content below the line

Gathering Lines

Upstream

Pipeline Producing Wells

Storage

Local Distribution Company

(LDC) Processing Plant

Industrial

Residential

Power Burn

Commercial

Midstream Downstream

No content below the line No content below the line

Natural Gas

19

• Introduction to natural gas demand sources

• Drivers of natural gas demand – how do we quantify the effects?

• Long term trends affecting demand growth

Agenda

No content below the line No content below the line

Natural Gas

20

Sources of Natural Gas Demand

Residential Commercial

Industrial Power Burn

No content below the line No content below the line

Natural Gas

21

42%

18%

8%

32%

Commercial End Use

Space Heating Water Heating Cooking Other

Space Heating Drives ResComm Demand

36%

36%

25%

3%

Residential End Use

Source: EIA

No content below the line No content below the line

Natural Gas

22

Sources of Natural Gas Demand

Residential Commercial

Industrial Power Burn

No content below the line No content below the line

Natural Gas

23

39%

16% 10%

10% 1%

1%

0%

0%

0%

1%

7%

1%

2% 5% 3%

1%

1%

1%

2%

0% 0%

Industrial Sector

Chemicals

Petroleum and Coal Products

Food

Primary Metals

Beverage and Tobacco Products

Textile Mills

Textile Product Mills

Apparel

Leather and Allied Products

Wood Products

Paper

Printing and Related Support

Plastics and Rubber Products

Nonmetallic Mineral Products

Fabricated Metal Products

The Many Sectors of Manufacturing

Source: EIA

No content below the line No content below the line

Natural Gas

24

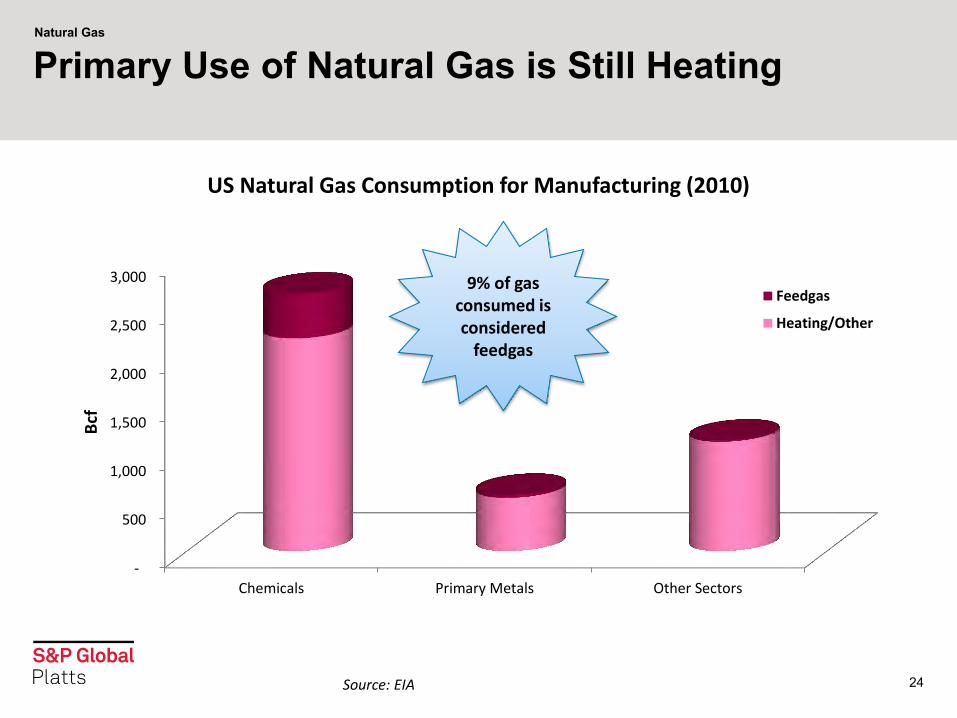

-

500

1,000

1,500

2,000

2,500

3,000

Chemicals Primary Metals Other Sectors

Bcf

US Natural Gas Consumption for Manufacturing (2010)

Feedgas

Heating/Other

Primary Use of Natural Gas is Still Heating

9% of gas consumed is considered

feedgas

Source: EIA

No content below the line No content below the line

Natural Gas

25

Sources of Natural Gas Demand

Residential Commercial

Industrial Power Burn

No content below the line No content below the line

Natural Gas

26

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Mill

ion

KW

h

Annual Retail Sales of Electricity

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Mill

ion

KW

h

Annual Power Generation By Fuel Type

Other Renewables NuclearHydro Coal Gas

Electricity Load and Fuel Switching Drive Power Burn Demand

Source: EIA

No content below the line No content below the line

Natural Gas

27

-

10

20

30

40

50

60

70

80

Bcf

/d

Commercial Residential Industrial Power Burn

Power Burn Leads Demand Growth

Source: EIA

No content below the line No content below the line

Natural Gas

-

5

10

15

20

25

30

-

10

20

30

40

50

60

70

80

90

100

De

gre

e D

ays

Bcf

/d

Historic Demand Vs. Normal Weather

ResComm Industrial Power Burn Heating Degree Days Cooling Degree Days

Weather is the Primary Driver of Demand

Source: Platts Bentek CellModel 28

No content below the line No content below the line

Natural Gas

29

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

52

54

56

58

60

62

64

66

68

70

Deg

ree

Day

s

Bcf

/d

Heating Demand Vs. HDDs

ResComm and Indutrial Demand Total HDDs

Weather is the Primary Driver of Demand

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

-

5

10

15

20

25

30

35

Deg

ree

Day

s

Bcf

/d

Cooling Demand Vs. CDDs

Power Burn Demand Total CDDs

Source: Platts Bentek CellModel, CustomWeather

No content below the line No content below the line

Natural Gas

30

5

10

15

20

25

30

15 25 35 45 55 65 75 85 95

Bcf

/d

Degrees Fahrenheit

US Power Plant Nominations Vs. Population-Weighted Temperature

Sample (2014 - Present)

US Power Burn Nominations Vs Temperature

Source: Platts Bentek Power Burn Report

No content below the line No content below the line

Natural Gas

31

5

10

15

20

25

30

15 25 35 45 55 65 75 85 95

Bcf

/d

Degrees Fahrenheit

US Power Plant Nominations Vs. Population-Weighted Temperature

2014 2015 2016 2017 YTD

US Power Burn Nominations Vs Temperature

Source: Platts Bentek Power Burn Report

No content below the line No content below the line

Natural Gas

32

-

5

10

15

20

25

30

Gas

Eq

uiv

ale

nt

Qu

anti

ty (

Bcf

/d)

Gas Equivalent Price

Cumulative Price by Volume Chart

Southeast Northeast Midwest Texas Southwest Rockies

Commodity Prices Dictate Market Share

Source: EIA 923

No content below the line No content below the line

Natural Gas

33

5

10

15

20

25

30

15 25 35 45 55 65 75 85 95

Bcf

/d

Degrees Fahrenheit

US Power Plant Nominations Vs. Population-Weighted Temperature

2014 2015 2016 2017 YTD $0.00 - $2.50 $2.50 - $3.50 Above $3.50

US Power Burn Nominations Vs Temperature

Source: Platts Bentek Power Burn Report

No content below the line No content below the line

Natural Gas

34

-

20

40

60

80

100

120

GW

h

CAISO Hydro Generation

5 Year Range 2017 5 Year Average

-

50

100

150

200

250

300

350

400

GW

h

BPA Hydro Generation

5 Year Range 2017 5 Year Average

Other Factors Influence Power Burn as Well

Source: Platts Bentek Power Burn Report

No content below the line No content below the line

Natural Gas

35

Other Factors Influence Power Burn as Well

0

1

2

3

4

5

6

7

8

1-Jan 1-Feb 1-Mar 1-Apr 1-May 1-Jun 1-Jul 1-Aug 1-Sep 1-Oct 1-Nov 1-Dec

Bcf

/d

West Power Burn Demand

5 Year Range 2017 5 Year Average

Source: Platts Bentek Power Burn Report

No content below the line No content below the line

Natural Gas

36

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

$180.00

$200.00

- 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000

Var

iab

le O

&M

Co

sts

Cumulative Summer Capacity

ERCOT Supply Curve

Biomass Coal Natural Gas Wind Solar Hydro Nuclear Oil Other

A Holistic View of Power Markets

Source: S&P Market Intelligence

No content below the line No content below the line

Natural Gas

37

A Holistic View of Power Markets

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

$180.00

$200.00

- 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000

Var

iab

le O

&M

Co

sts

Cumulative Summer Capacity

ERCOT Supply Curve

Biomass Coal Natural Gas Wind Solar Hydro Nuclear Oil Other

Cheaper Gas Prices

Source: S&P Market Intelligence

No content below the line No content below the line

Natural Gas

38

A Holistic View of Power Markets

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

$180.00

$200.00

- 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000

Var

iab

le O

&M

Co

sts

Cumulative Summer Capacity

ERCOT Supply Curve

Biomass Coal Natural Gas Wind Solar Hydro Nuclear Oil Other

Source: S&P Market Intelligence

No content below the line No content below the line

Natural Gas

39

A Holistic View of Power Markets

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

$180.00

$200.00

- 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000

Var

iab

le O

&M

Co

sts

Cumulative Summer Capacity

ERCOT Supply Curve

Biomass Coal Natural Gas Wind Solar Hydro Nuclear Oil Other

Nuke Outages

Source: S&P Market Intelligence

No content below the line No content below the line

Natural Gas

40

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

$180.00

$200.00

- 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000

Var

iab

le O

&M

Co

sts

Cumulative Summer Capacity

ERCOT Supply Curve

Biomass Coal Natural Gas Wind Solar Hydro Nuclear Oil Other

A Holistic View of Power Markets

2016 Minimum Summer Load: 25,107 MW

2016 Peak Summer Load: 71,093 MW

Source: S&P Market Intelligence

No content below the line No content below the line

41

Longer Term Trends and Risks to Natural Gas Demand Growth

No content below the line No content below the line

Natural Gas

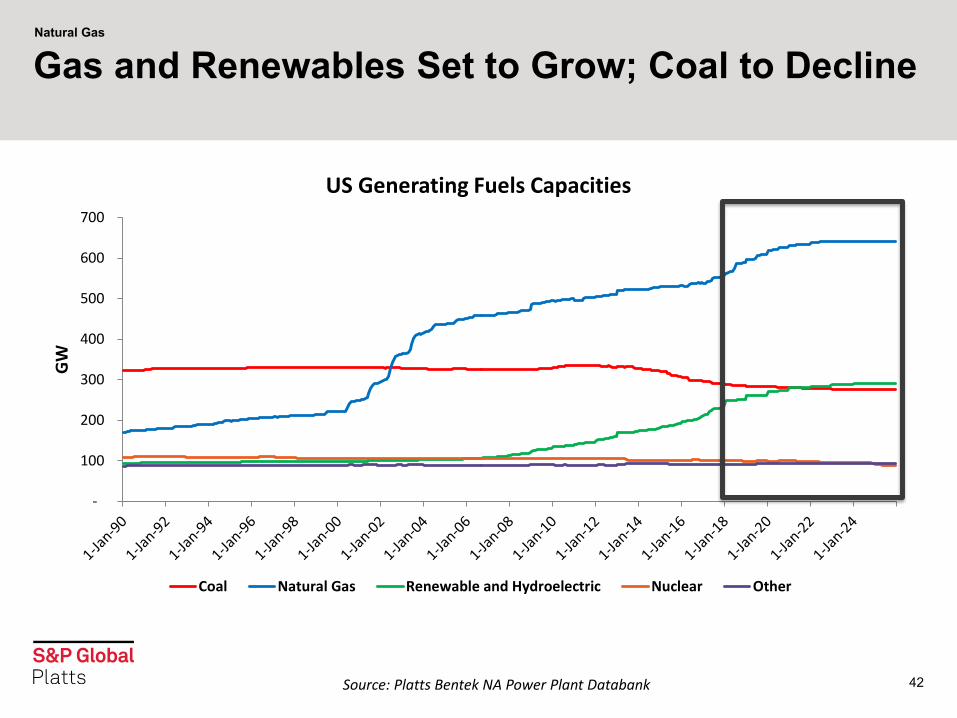

42

-

100

200

300

400

500

600

700

GW

US Generating Fuels Capacities

Coal Natural Gas Renewable and Hydroelectric Nuclear Other

Gas and Renewables Set to Grow; Coal to Decline

Source: Platts Bentek NA Power Plant Databank

No content below the line No content below the line

Natural Gas

43

(40)

(20)

-

20

40

60

80

100

120

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

GW

Natural Gas, Coal, and Renewable Generation Capacity Changes

New Gas Generation Capacity New Renewable Generation Capacity Coal Retirements

Gas and Renewables Set to Grow; Coal to Decline

Source: Platts Bentek NA Powerplant Databank

No content below the line No content below the line

Natural Gas

44

62%

63%

64%

65%

66%

67%

68%

69%

70%

71%

0%

1%

2%

3%

4%

5%

6%

7%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Foss

il Fu

el G

en

era

tio

n M

arke

t Sh

are

Re

new

able

Ge

ne

rati

on

Mar

ket

Shar

e

Fossil Fuel Vs. Renewable Generation Market Share

Renewable Market Share Fossil Fuel Market Share

Emerging Renewable Generation a Threat to Fossil Fuel

Source: EIA 923

No content below the line No content below the line

Natural Gas

45

-

10

20

30

40

50

60

70

80

GW

New Generation Capacity Additions by Year (Operating Power Plants)

Gas Coal Oil Nuclear Renewables Other

New Generation Capacity Additions by Year

Source: Platts Bentek NA Powerplant Databank

No content below the line No content below the line

Natural Gas

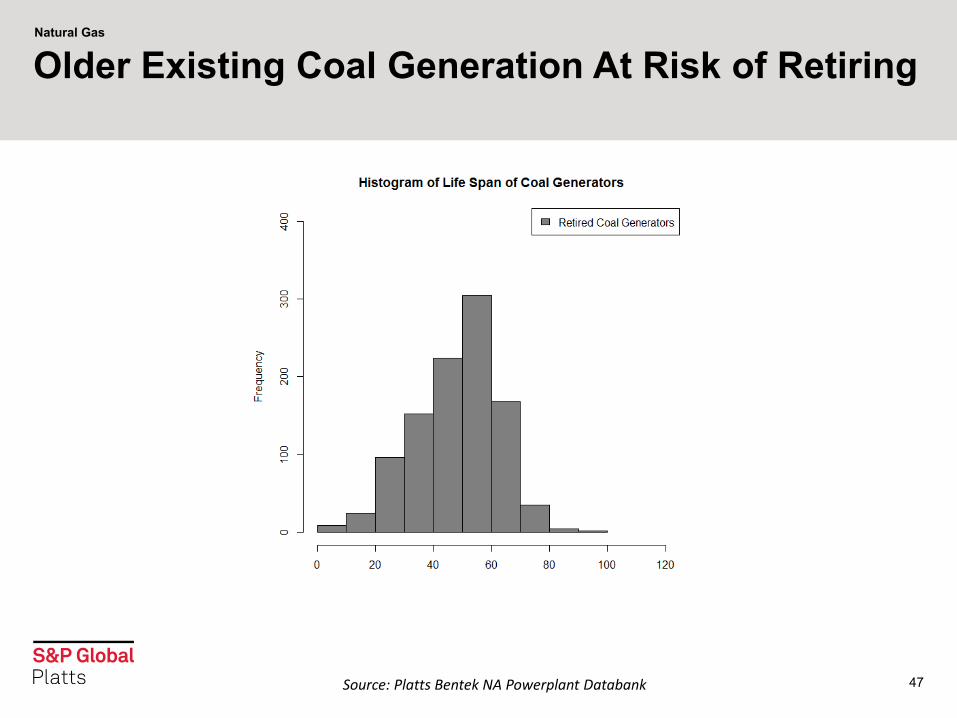

46

Older Existing Coal Generation At Risk of Retiring

Source: Platts Bentek NA Powerplant Databank

No content below the line No content below the line

Natural Gas

47

Older Existing Coal Generation At Risk of Retiring

Source: Platts Bentek NA Powerplant Databank

No content below the line No content below the line

Natural Gas

48

Older Existing Coal Generation At Risk of Retiring

Source: Platts Bentek NA Powerplant Databank

No content below the line No content below the line

Natural Gas

49

-

50

100

150

200

250

300

5 15 25 35 45 55 65 75 85

GW

Years

Cumulative Distribution of Operating Coal Capacity by Age

Older Existing Coal Generation At Risk of Retiring

150 GW of existing coal generators greater than 40 years old

Source: Platts Bentek NA Powerplant Databank

No content below the line No content below the line

Natural Gas

50

-

0.02

0.04

0.06

0.08

0.10

0.12

MM

cf/y

ear

Annual Household Natural Gas Consumption

Offsetting Trends in Residential Demand

Source: EIA

No content below the line No content below the line

Natural Gas

51

-

50

100

150

200

250

300

350

400

450

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050 2060

Mill

ion

s

US Population Continues to Grow

Historic Population Population Projection

Offsetting Trends in Residential Demand

Source: US Census Bureau

No content below the line No content below the line

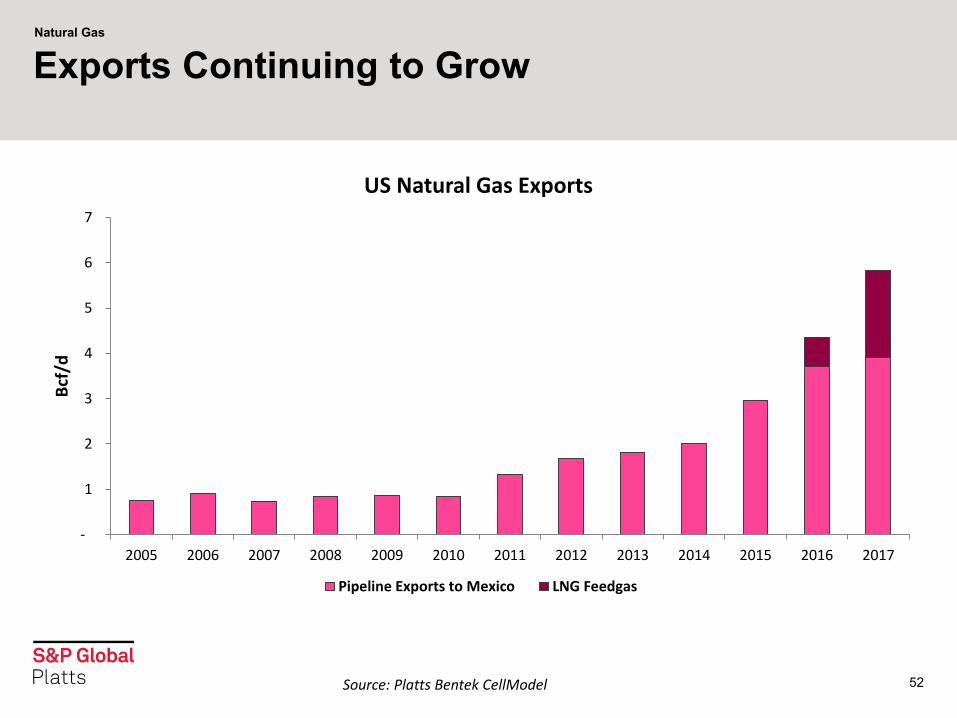

Natural Gas

52

-

1

2

3

4

5

6

7

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Bcf

/d

US Natural Gas Exports

Pipeline Exports to Mexico LNG Feedgas

Exports Continuing to Grow

Source: Platts Bentek CellModel

No content below the line No content below the line

Natural Gas

53

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

-

10

20

30

40

50

60

70

80

90

100

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Pe

rce

nt

of

Tota

l De

man

d

Bcf

/d

US Natural Gas Demand History and Outlook

ResComm Industrial PowerBurn Exports Exports Percent

Exports Will Drive Demand Growth Going Forward

Source: Platts Bentek CellCAST

No content below the line No content below the line

Natural Gas

54

• Weather is the primary driver of natural gas demand. Residential and commercial buildings use natural gas primarily for space and water heating. In the summer months, warm temperatures increase electricity demand which boosts power burn.

• Power burn demand has been responsible for a large portion of the demand growth over the past decade. Cheaper gas prices and environmental regulations have allowed gas generation to compete with coal generation.

• While there will likely be continued domestic demand growth, exports will lead the demand charge.

Takeaways

No content below the line No content below the line

Thank you!

Platts Analytics Mitchell DeRubis [email protected] Bob Yu [email protected]

DISCLAIMER. THIS REPORT IS FURNISHED ON AN “AS IS”BASIS. BENTEK DOES NOT WARRANT THE ACCURACY OR CORRECTNESS OF THE REPORT OR THE INFORMATION CONTAINED THEREIN. BENTEK MAKES NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE USE OF ANY INFORMATION CONTAINED IN THIS REPORT IN CONNECTION WITH TRADING OF COMMODITIES, EQUITIES, FUTURES, OPTIONS OR ANY OTHER USE. BENTEK MAKES NO EXPRESS OR IMPLIED WARRANTIES AND EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANT- ABILITY OR FITNESS FOR A PARTICULAR PURPOSE. RELEASE AND LIMITATION OF LIABILITY: IN NO EVENT SHALL BENTEK BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL, INCIDENTAL, OR CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFIT) ARISING OUT OF OR RELATED TO THE ACCURACY OR CORRECTNESS OF THIS REPORT OR THE INFORMATION CONTAINED THEREIN,WHETHER BASED ON WARRANTY, CONTRACT, TORT OR ANY OTHER LEGAL THEORY.

1800 Larimer Street in Denver, CO