oil markets review - latest energy, metals & steel news, market

TRANSCRIPT

© 2013 Platts, McGraw Hill Financial. All rights reserved.

Jorge Montepeque, May 2013

Oil Markets Review

• Dated Brent reached 8 months high in first half of February, and then plummeted in mid April to lowest since beginning of July, 2012.

• Since then crude complex strengthened on the expected rate cut by European Central Bank, geopolitical concerns and strong US employment data.

• The unemployment rate in US is the lowest since December 2008 • Japan is continuing its QE, buying $70 bln in bonds, US Fed - $85 bln per

month • US showing positive signs, while EU and Japan still lag • Chinese GDP growth at 7.7% in Q1 2013, below widely expected 8% • Chinese manufacturing data weaker in April compared to March. • IMF downgraded its 2013 global growth forecasts by 0.2% to 3.3% • Policies pushed long term interest rates to record lows • Yields on US junk bonds on average fell below 5%, on more active search

by investors for higher yields.

Economic background

2

• Dated Brent reached 8 months high in first half of February, and then plummeted in mid April to near $100/bbl, the lowest since beginning of July, 2012

• WTI rises by nearly $10/bbl since mid April to above $95.00/bbl closing the gap with Brent to about $7.50/bbl

• Dubai and Oman both are hovering above the $100/bbl level • Platts launches quality premium system for Brent grades with deliveries of

Ekofisk and Oseberg for June contract • ICE announces position limits for legacy Brent futures contract, encourages

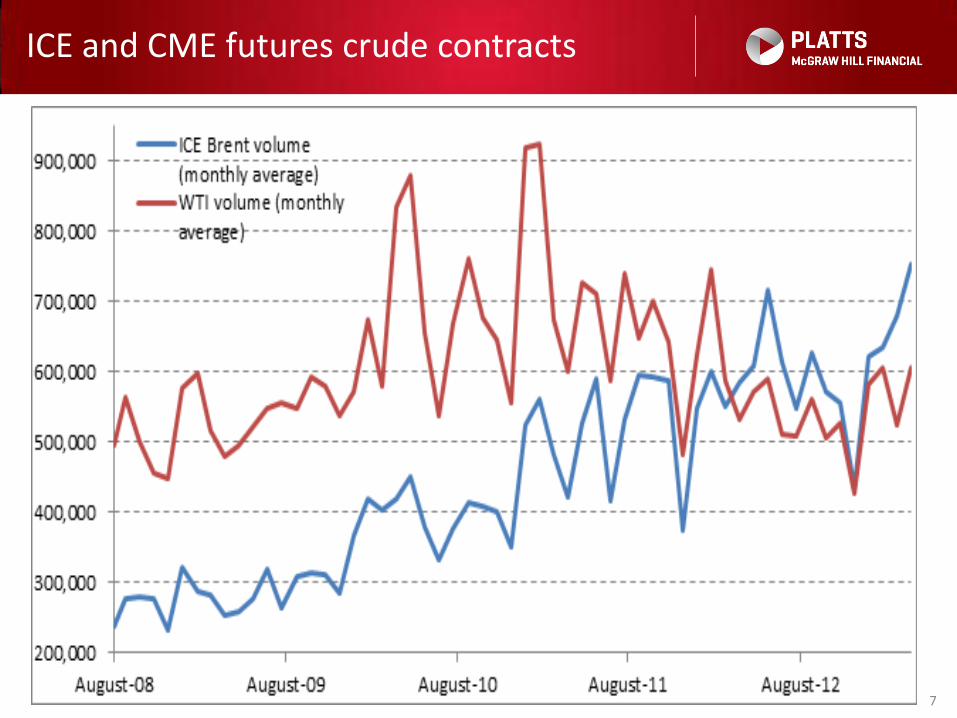

migration to NX Brent contract • Dated Brent is adopted in most areas of the world as benchmark • ICE Brent trading volumes rise above CME light crude futures • Dubai physical liquidity healthy, swaps futures volume rises to about 12-mil

bbl/day • Rising US production creates needs for price discovery, Platts launches Eagle

Ford and reviews other market areas

The world of benchmarks, assessments, swaps and futures

3

Bearish commodities markets

4 Source: FT

Dated Brent, $/b

Source: Platts

95

100

105

110

115

120

Dated Brent

BFOE monthly production

6

19,000,000

24,000,000

29,000,000

34,000,000

39,000,000

44,000,000

49,000,000

54,000,000

BFOE loading (bbl/month)

ICE and CME futures crude contracts

7

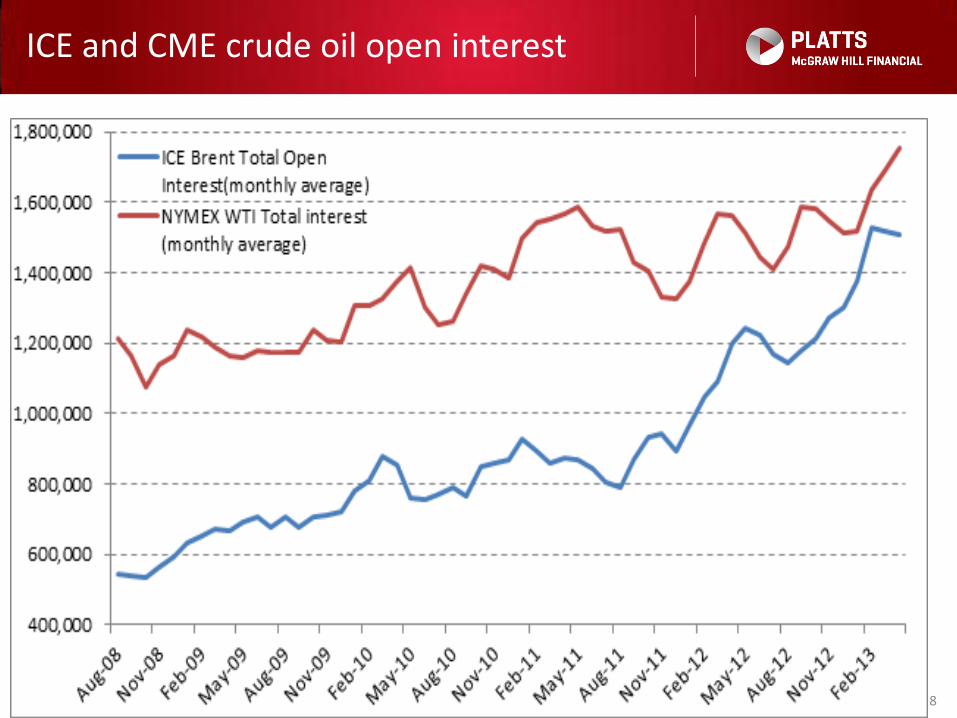

ICE and CME crude oil open interest

8

Brent/WTI, $/bbl

9 Source: Platts

0

2

4

6

8

10

12

14

16

18

20

22

24

26

Brent/WTI Spread Swap

WTI/Brent spread swaps for May 2013 – April 2016, $/bbl

10 Source: Platts

7.00

7.25

7.50

7.75

8.00

8.25

8.50

8.75

9.00

JUN

'13

JUL

'13

AU

G '1

3

SEP

'13

OC

T '1

3

NO

V '1

3

DEC

'13

JAN

'14

FEB

'14

MA

R '1

4

AP

R '1

4

MA

Y '1

4

JUN

'14

JUL

'14

AU

G '1

4

SEP

'14

OC

T '1

4

NO

V '1

4

DEC

'14

JAN

'15

FEB

'15

MA

R '1

5

AP

R '1

5

MA

Y '1

5

JUN

'15

JUL

'15

AU

G '1

5

SEP

'15

OC

T '1

5

NO

V '1

5

DEC

'15

JAN

'16

FEB

'16

MA

R '1

6

AP

R '1

6

May

'16

$/bbl

No. of Dubai partial trades each month for Jan 2012 – April 2013

11 Source: Platts

Global Oil Supply

12

Top oil producers in March 2013, mb/d

Country March 2013 2012 Change

Russia* 10.84 10.73 0.11

US** 9.91 9.14 0.77

Saudi Arabia 9.04 9.51 -0.47

China 4.24 4.18 0.06

Canada 3.96 3.76 0.20

Iran 2.68 3.00 -0.32

Iraq 2.96 2.95 0.01

* Including conventional crude oil, non-conventional crude oil, condensates, NGLs, **Including conventional crude oil, non-conventional crude oil, condensates, NGLs, biofuel

Source: IEA

• US total oil production (excluding NGLs) forecasting to exceed Saudi Arabia’s by 2017

• US would become virtually energy independent by 2035

• US oil production will increase to 11 mln b/d by 2020 and should allow US oil imports to decline to 4 million b/d from current 10 million b/d

• Eagle Ford and Bakken to yield 1.6 mln b/d by 2015

EIA: the US shale energy revolution

13 Source: EIA

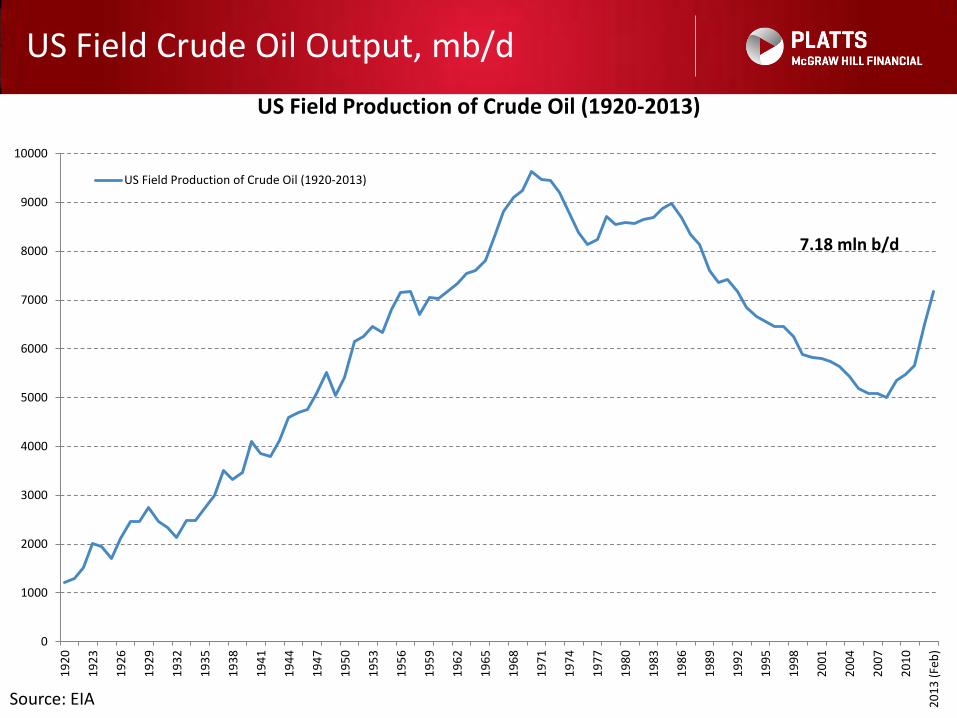

US Field Crude Oil Output, mb/d

Source: EIA

7.18 mln b/d

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

19

20

19

23

19

26

19

29

19

32

19

35

19

38

19

41

19

44

19

47

19

50

19

53

19

56

19

59

19

62

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

20

13

(Fe

b)

US Field Production of Crude Oil (1920-2013)

US Field Production of Crude Oil (1920-2013)

US Monthly Raw Natural Gas Liquids (NGLs)

15 Source: EIA

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2,400

2,500

2,600

Feb

-200

7

Ap

r-2

00

7

Jun

-20

07

Au

g-2

00

7

Oct

-20

07

De

c-2

00

7

Feb

-200

8

Ap

r-2

00

8

Jun

-20

08

Au

g-2

00

8

Oct

-20

08

De

c-2

00

8

Feb

-200

9

Ap

r-2

00

9

Jun

-20

09

Au

g-2

00

9

Oct

-200

9

De

c-2

00

9

Feb

-201

0

Ap

r-2

01

0

Jun

-20

10

Au

g-2

01

0

Oct

-20

10

De

c-2

01

0

Feb

-201

1

Ap

r-2

01

1

Jun

-20

11

Au

g-2

01

1

Oct

-20

11

De

c-2

01

1

Feb

-201

2

Ap

r-2

01

2

Jun

-20

12

Au

g-2

01

2

Oct

-20

12

De

c-2

01

2

Feb

-201

3

MBPD

2,453 MBPD

US light sweet crude imports

16

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

(Ja

n-F

eb

)

US Light Sweet Crude Oil Imports (>35 API & <1.10 S%)

Source: EIA

MMBPD

US heavy crude oil imports

17

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

3.50

3.75

4.00

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

(Ja

n-F

eb

)

US Heavy Crude Oil Imports (<25 API & all S%)

Source: EIA

MMBPD

USGC crude prices follow global trends

18

95

100

105

110

115

120

Dated Brent

LLS @ St. James

Eagle Ford Marker

Investments into US shale oil

Foreign Domestic Amount

Partner Country Partner Shale Play ($B) Year

British Petroleum UK Chesapeake Woodford 1.70 2008

British Gas UK EXCO Marcellus 0.95 2009

StatoilHydro Norway Chesapeake Marcellus 3.38 2009

Reliance India Pioneer Eagle Ford 1.36 2010

Reliance India Atlas Marcellus 1.70 2010

Reliance India Carrizo Marcellus 0.39 2010

Total France Chesapeake Barnett 2.25 2010

CNOOC China Chesapeake Niobrara 0.57 2010

British Gas UK EXCO Haynesville 1.30 2010

Mitsui Japan Anadarko Marcellus 1.40 2010

CNOOC China Chesapeake Eagle Ford 1.08 2011

KNOC Korea Anadarko Eagle Ford 1.55 2011

Marubeni Japan Marathon Niobrara 0.27 2011

Mitsui Japan SM Energy Eagle Ford 0.68 2011

GAIL India Carrizo Eagle Ford 0.10 2011

Total France Chesapeake/EnerVest Utica 2.30 2012

Sinopec China Devon TMS, Niobrara,Utica 2.20 2012

Marubeni Japan Hunt Oil Eagle Ford 1.30 2012

Osaka Gas Japan Cabot Oil and Gas Pearsall(Eagle Ford) 0.25 2012

Sumitomo Japan Devon Midland-Wolfcamp 1.40 2012

Total…… 26.47

Source: EIA

20

Eagle Ford

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

MBPD

Source: Bentek Energy

Bakken expected production

21

-

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Bakken Crude Oil Production Forecast

ND MT

MBPD

Source: Bentek Energy

Permian Basin Production Forecast

22

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

TX NM

MBPD

Source: Bentek Energy

• Enterprise Seaway Pipeline (400 kb/d) – reversed in May 2012 – a 50:50 joint venture between Enbridge and Enterprise -- ships crude oil from Cushing to Freeport through Jones Creek, northwest of Freeport, to Texas City

• TransCanada Keystone XL is to ship crude from the Athabasca oil sands in Canada to Cushing, Oklahoma (830 kb/d) and onward to the US Gulf Coast (591 kb/d)

• Energy Transfers Partners have proposed to convert a natural gas pipeline into a 400 kbd Trunkline crude oil line from Illinois to Texas

• Magellan Longhorn Segment Products Pipeline Conversed to Crude Oil (mid-April 2013) to ship 75,000 b/d crude movements from Crane, TX to Houston refineries. The pipeline will increase to the full 225,000 b/d capacity in Q3 2013 and will be expanded to 295,000 b/d later

• Sunoco Logistics Partners' Permian Express Pipeline - 150,000 b/d crude movements from Wichita Falls to Nederland/Beaumont, TX

US key pipeline projects

23

Pipelines to bring crude oil from Cushing to USGC

24 Source: Platts

Proposed pipeline projects for Cushing to US Gulf Coast

New Capacity

Completion date Status

Enterprise Seaway Pipeline 850,000 Q2 2014

Phase 1 Completed

TransCanada Keystone XL 591,000 4Q 2013

Under Construction

Energy Partners Trunkline 400,000 TBD

Regulatory Review

Cushing to USGC Capacity 1,841,000

Jan 22, 2013 – Keystone XL received approval from Nebraska governor, awaits approval from Obama administration

25

Permian Basin

Completion date

New/Expanded Capacity

Total Capacity

Destination Status

Magellan Longhorn Segment Reversal

1Q 2013 225,000 225,000 Houston Near Completion

BridgeTex (50/50 Oxy & Magellan)

Mid-2014 300,000 300,000 Houston Developmental Stage

Permian Express (Sunoco Logistics)

2H 2014 350,000 350,000 Beaumont Phase 1 Construction

Phase I 2H 2013 150,000 Beaumont

Phase II 2H 2014 200,000

Sunoco West Texas Gulf

1Q 2013 100,000 140,000 Beaumont Construction

Total 975,000

26

Rail terminals in North Dakota…

1

2

3

4

5

6

7

8 9

10

11

12

14

13

1) EOG Rail - Stanley, ND 8) Enbridge Rail - Berthold, ND

2) Rangeland COLT - Epping, ND 9) Plains - Ross, ND

3) Hess - Tioga, ND 10) Basin Transload - Zap, ND

4) Bakken Oil Express - Dickinson, ND 11) Dakota Plains - New Town, ND

5) Plains/USD - Van Hook, ND 12) Great Northern - Fryburg, ND

6) Musket Corp. - Dore, ND 13) Musket Corp. – Dickinson

7) Savage Rail - Trenton, ND 14) Centennial Energy - Donnybrook

27

Owner/Project Capacity (Mb/d) Start Date 1) EOG Rail - Stanley, ND 65 <2010

2) Rangeland COLT - Epping, ND 80 May-12

3) Hess - Tioga, ND 25 - 60 Mar-12 - Dec-12

4) Bakken Oil Express - Dickinson, ND 100 - 200 Oct-11 - Jun-12

5) Plains/USD - Van Hook, ND 35 - 65 Sep-12 - Jun-13

6) Musket Corp. - Dore, ND 10 - 60 <2010 - Jun-11

7) Savage Rail - Trenton, ND 90 May-12

8) Enbridge Rail - Berthold, ND 10 - 80 Sep-12 - Feb-13

9) Plains - Ross, ND 20 - 65 Jan-12 - Nov-12

10) Basin Transload - Zap, ND 10 - 40 <2010 - Jun-12

11) Dakota Plains - New Town, ND 20 - 40 <2010 - Mar-11

12) Great Northern - Fryburg, ND 60 Jan-13

Other Rail

13) Musket Corp. - Dickinson 8 2010

14) Centennial Energy - Donnybrook 10 2010

Total Rail Capacity 833

Rail capacity

• Bakken production at 697,896 b/d average December 2012-February 2013

• US East Coast refineries substitute WAF, North Sea and East Canadian barrels with North Dakota’s Bakken Blend (by rail).

• In 2012, Bakken deliveries to the East Coast averaged near 70,000 b/d.

• By the end of 2013, Bakken rail deliveries to the East Cost could average 100,000-150,000 b/d

• Bakken consumers in USAC:

- Astra Oil is railing Bakken in to its 40,000 b/d refinery in Tacoma, Washington

- BP is constructing a railway project at its 234,000 b/d Cherry Point refinery in Ferndale, Washington to receive Bakken crude oil.

- Philadelphia Energy Solutions‘ refinery currently rails in 20 kb/d of Bakken (potential increase to 140-180 kb/d) PES is planning to rely on Midcontinent crudes for 55% of the refinery's crude oil capacity in the coming years.

- Phillips 66's Bayway refinery in New Jersey to buy 50,000 b/d effective 2013

- Delta Airlines’ Trainer refinery effective 2013

- PBF Energy’s Delaware City refinery

US East Coast diverts to Bakken Blend

28

• Eagle Ford oil production average at 340,000 b/d Jan-Nov 2012 • Eagle Ford condensate production average at 72,126 b/d Jan-Nov 2012 • Valero replaced all its foreign light oil imports with domestic crude at

its Gulf Coast and Memphis, Tennessee, plants in Q4 2012 • Valero is currently consuming a total of 140,000 b/d of Eagle Ford Shale

crude at its refineries (95,000 b/d Three Rivers refinery, 205,000 b/d Corpus Christie refinery, 90,000 b/d Houston refinery in Texas, 135,000 b/d Meraux in Louisiana)

• Canadian heavy crude oil flows push back import from Mexico and Venezuela

• LyondellBasell terminated shipments of Saharan Blend into USGC refineries

• Philadelphia Energy Solutions will ship Eagle Ford and other Gulf Coast crudes by Jones Act vessels when the arbitrage allows

• Petrobras' Pasadena Refining System Inc is also refining about 20,000-30,000 b/d of Eagle Ford

US Gulf Coast diverts to domestic crude oil

29

• Statoil exports US Bakken crude to Canada

• Valero received a one-year permit to export Eagle Ford to Eastern Canada

• BP received a permit summer 2012

• Shell applied for a permit

US is to export unwanted crude oil to Canada and possibly elsewhere

30

New crude is found elsewhere

31

Australia: 233 bln barrels found?

Permian basin in Texas: 1.2 mb/d

Bazhenov in Russia: 182 bln bbls recoverable reserves

Bazhenov size = Texas and Gulf of Mexico combined Bazhenov may provide 0.8-1.0 mln b/d by 2020

Developed by Rosneft jointly with ExxonMobil and Statoil

Lukoil Gazpromneft and Shell

• Kashagan oil field discovered in 2000 in the Caspian Sea.

• The production is expected to start in October 2013, according to Kazakhstan’s oil and gas minister.

• Expected to produce around 60-120 kb/d by the end of 2013 or early 2014. During 2014 to rise to 370 kb/d.

• Kashagan estimated to have 38 billion barrels of oil, including 13 billion of proven recoverable reserves, due to complicated structure of reservoir.

• Preliminary tests showed that crude is light (45 API) and 1% sulfur.

• Being developed by North Caspian Operating Consortium:

New Oil: Kashagan

32

ENI 16.81%

Shell 16.81%

ExxonMobil 16.81%

KMG 16.81%

Total 16.81%

Conoco 8.39%

Inpex 7.56%

• US dependence on OPEC members to decline • Light crude oil looking for markets • US role as a product exporter to increase • Low interest rates to continue to funnel capital to

producing areas • Demand in Europe and US to remain lacklustre • Some markets in the US to change from an import to an

export mode • Internal competition in the US to heighten between gas

and oil • Platts to monitor and launch new instruments in the US,

i.e. Eagle Ford, Permian and other domestic streams

Conclusion

33

twitter.com/plattsoil

The Barrel Blog

platts.com/BlogDetails/oilblog

EMEA Oil Events