stock return volatility modeling by using...

TRANSCRIPT

Ministry of Education and Training

Hoa Sen University

Faculty of Economics and Commerce

-------

MARKET VOLATILITY ANSLYSIS AND FINANCIAL STOCK

RETURN VOLATILITY MODELING BY SYMMETRIC AND

ASYMMETRIC GARCH - EVIDENCE FROM FINANCIAL

INDUSTRY OF HO CHO MINH STOCK EXCHANGE

Thai Gia Hao1 and Huynh Ha Bao Tran2

(1)Faculty of Corporate Finance, Hoa Sen University, Vietnam

Email: [email protected]

Phone: 0122 8710 678

(2)Faculty of Finance and Banking, Hoa Sen University, Vietnam

Email: [email protected]

Phone: 093 646 8099

Instructors: Master. Nguyen Phuong Quynh*

*Email: [email protected]

Phone: 096 204 6820

HCMC, June 2016

MARKET VOLATILITY ANSLYSIS AND FINANCIAL STOCK

RETURN VOLATILITY MODELING BY SYMMETRIC AND

ASYMMETRIC GARCH - EVIDENCE FROM FINANCIAL

INDUSTRY OF HO CHO MINH STOCK EXCHANGE

ABSTRACT

This paper empirically examines the symmetric and asymmetric GARCH models in

stock market volatility forecasting. We study on the financial listed on the Ho Chi Minh

City Stock Exchange including four sub-industries such as insurance, real estate,

diversified finance and banks. Additionally, the four market-weighted indexes

(Vnindex, Hnxindex, VN30 index and UPCOM index) will also be employed. The

collected data, totally 45 common stocks, covered the period from the beginning of

2012 to 8th April 2016. In particular, ARCH, GARCH, GARCH-M, EGARCH,

EGARCH-M, GJRGARCH, GJRGARCH-M are employed to capture either time-

varying volatility or asymmetric effect. The hypothesis of risk-return tradeoff is

detected by GARCH-M models. In summary, both symmetric and asymmetric show

the inability of dealing with heteroscedasticity and autocorrelation in residuals on

whole financial industry. ARCH(2) and GARCH(1,1) are significantly found which

employed on the three market-weighted indexes (Vnindex, HNXindex and VN30

index). Last, the new contribution are that the samples of a whole financial industry

are investigated in this paper to detect whether time-series models are available.

Otherwise, the postestimations of heteroscedasticity and autocorrelation are carefully

focused to ascertain that there are not any disturbances in residuals.

Keywords: symmetry, asymmetry, ARCH, GARCH-type models, risk-return tradeoff,

heteroscedasticity.

1 | P a g e

1. Introduction

The study on the volatility of stock return is closely linked to the risk of financial

asset, meaning that higher volatility lead to large string of return, hence higher risk.

The volatility forecasting become an essential part of invest ment strategies and there

is two basic approaches to volatility comprising of constant variance and time-varying

volatility.

The constant variance can be capture by simplier model such as ARMA or

ARIMA model, first introduced by Box, Jenkins and Reinsel in 1994. Another problem

is the variance of error changing over time which could break the hypothesis of white-

noise residuals. The term “white-noise” indicates that the residual of return series must

be homoscedastic and unautocorrelated. We must differentiate with the term “white-

noise” in return series with finite mean and variance (Ruey S.Tsay, “Analysis of

Financial Time Series”, 2nd edition, p.31). Othewise the term of stationary is also

important showing that the mean of return series and covariance between current return

and its lagged value must be time-invariant. A well-known test of stationarity is

Dickey-Fuller (1979).

On the order hand, when the variance of error term is changing over time,

meaning heteroscedasticity, Engle (1982) proposed the Autoregressive Conditional

Heteroscedastic). The further models can be known as GARCH by Bollerslev (1986);

GARCH-in-mean by Engle, Lilien and Robins (1987); Exponential GARCH by Nelson

(1991); GJRGARCH by Glosten, Jaganathan and Runkle (1993); Threshold GARCH

might be the same as GJRGARCH. In general, according to Tim Bollerslev in 2007,

his “Glossary to ARCH(GARCH)”, GARCH-type models could be divided into two

group: the symmetric GARCH and the asymmetric GARCH. In particular, we use the

asymmetric GARCH to capture the leverage effect – one of residual behaviour. Another

essential test of ARCH effect in error term before using GARCH-family models was

Lagrange Multiplier test of Engle (1982).

2 | P a g e

Beginning with ARCH model first promoted by Engle (1982) to deal with time-

varying volatility, in ARCH model, the conditional variance of error is expressed as a

function of past squared error with the constraint of non-negative coefficients. But it

emerged some disadvantages that if these parameters are positve and the recent squared

residual are large, the current forecasted squared error will be large in magnitude in the

sense that its variance is large (Mohd. Aminul Islam, 2013). Other weakness is that

ARCH requires many parameters and maybe high order to capture the volatility while

Bollerslev (1986) remdedied this problem by Generalized ARCH model.

Furthermore, the volatility have some characteristics known as volatility clusters,

leverage effect. “Volatility clustering or volatility pooling shows that volatility may be

high for certain time periods and low for other periods, in short for the volatility

tendency in financial market to appear in bunches” (Chris Brooks, “Introductory

Econometrics for Finance”, 2nd edition, p.380). It could be detected through the

existence of significant correlation at extended lag length in correlogram and

corresponding Box-Ljung statistic (M.Tamilselvan 2016). And the term of leverage

effect indicated that volatility seems to react diffently to a big price increase or a big

price drop. This is the phenomenon of the tendency for volatility to rise more following

a large price fall than following a price rise of the same magnitude” (Chris Brooks,

“Introductory Econometrics for Finance”, 2nd edition, p.380). Basically, leverage

effect is known as the negative correlation between price movement and volatility

which first investigated by Black (1976) and the other evidence of Nelson (1991),

Gallant, Rossi and Tauchen (1992,1993).

To capture the asymmetry, a new class of GARCH was proposed such as

Exponential GARCH by Nelson (1991); GJRGARCH by Glosten, Jaganathan and

Runkle (1993); Threshold GARCH might be the same as GJRGARCH.

As an application on Vietnamese stock market, our main purposes are to

investigate and to model the stock return volatility. Likewise, the current paper will

detect whether there are any ARCH effect, volatility cluster or asymmetric effect in

3 | P a g e

stock return by both symmetric and asymmetric GARCH models (ARCH, GARCH,

EGARCH, GJRGARCH). The other useful hypothesis is that the risk-return tradeoff

is also encountered by GARCH-in-mean model.

Our paper was conducted with Financial industry on Hochiminh City Stock

Exchange (HOSE) including four sub-industries: insurance (4 tickers), real estate (30

tickers), diversified finance (6 tickers) and banks (5 tickers). Besides, we will also

investigate on market-weighted index comprising of Vnindex, HNXindex, VN30 index

and UPCOM index to detect whether GARCH models are available for market

volatility forecasting or not.

2. Research questions

The hypotheses to be tested for stock returns volatility are the following: 1)

whether there are any ARCH effect in return series using ARCH and GARCH, 2)

whether there are any asymmetric effect using EGARCH and GJRGARCH, 3) whether

the risk-return tradeoff using GARCHs-in-mean are statistically significant on

Vietnamese financial industry.

To the our best collection, it seem that few studies were officially studying on

Vietnam stock market. Moreover, there was no single one investigation of a wholly

financial industry from the year of 2012 till now (including 53 common stocks

classified by HoChiMinh Stock Exchange-HOSE). We first conduct this research on

only Financial stock marke before analyzing whole stock exchange.

Applying the model estimation progess from the below papers and the standard

proxy propose by Ruey S.Tsay (“Analysis of Financial Time Series”, 2005, the 2nd

edition, p.101-131), both symmetric and asymmetric will be utilized to take the

adequate volatility models. The stationarity Dickey-Fuller pretest and Lagrange

Multiplier (LM) test of heteroscedasticity will be executed, especially LM test included

in pre and post-estimation to ascertain that there are no remaining ARCH effect in error

term. The correlogram with ACF and PACF function are to detect the autocorrelation

in squared residuals and define the order of ARCH model.

4 | P a g e

Furthermore, the hypothesis of risk premiums in return series is to be detected

by GARCH-in-mean, EGARCH-in-mean and GJRGARCH-in-mean model while the

asymmetry will be captured by EGARCH and GJRGARCH. Model estimation will be

conducted on STATA 12 programme.

3. Literature review

There has been a large amount of literature on modelling stock market volatility,

as a proxy of risk, to define the most fittest for capturing many volatility characteristics.

However, we found no one studying on a whole industry and just employed two or

three samples.

To begin with Vietnames stock market, Tran Manh Tuyen conducted

investigation stock return volatility (using VNindex) covering the period 02/01/2009 –

16/10/2009 by both symmetric and asymmetric GARCH models (GARCH, GARCH-

In-Mean, EGARCH, GJRGARCH). VNindex is the value-weighted stock price index

of all common stocks traded on the Vietnam official stock exchange. The paper

indicated that higherrisk (proxied by the conditional variance) would not necessarily

lead to higher return (no risk-return tradeoff), meaning that GARCH-In-Mean model

was statistically insignificant. Moreover, there was no clue that the effect of shocks on

volatility was asymmetric, as well as insignificant EGARCH and TGARCH. But

essentially he did not show any test of stationary, autocorrelation and heteroscedasticity,

as well as the basic method of model order estimation. Last but not least, his study did

not retest the three characteristics of time-series after model estimation.The paper

named “Modeling volatility using GARCH models: Evidence from Vietnam) was

published on Economic Bulletin Vol.31, No.3, p.1935-1942 in 2011.

In the same year, 2011, Vo Xuan Vinh and Nguyen Thi Kim Ngan employed the

same ample (VNindex), from 01 March 2002 to 31 August 2010 and also had the same

conclusion about the symmetric volatility, meaning that TGARCH was insignificant.

But there was some differences that risk-return tradeoff hypothesis was statistically

significant with GARCH-M (1,1) model. It is doubtful that time periods of data of these

5 | P a g e

two paper was totally different. As the same deficiency as Tran Manh Tuyen, they did

not conduct the retest of autocorrelation or heteroscedasticity after model estimation.

Their paper was published on the Vietnamese Jounal of Development of Science and

Technology (14), Quarter 3-2011, page.5-20. Both papers conducting on Vietnam stock

market used the AIC and BIC criterion to selection among estimated models.

In 2011, Ahmed Alsheikh M.Ahmed and Suliman Zakaria utilized the symmetric

and asymmetric GARCH to capture the volatility of Khartoum Stock Exchange index

(KSE) from January 2006 to November 2010. Augmented Dickey-Fuller test (Dickey-

Fuller 1981) and Lagrange Multiplier proposed by Engle (1982) was used to test the

stationarity and heteroscedasticity before estimation. They directly use GARCH(1,1),

GARCH-M(1,1), EGARCH(1,1), TGARCH(1,1) and PGARCH(1,1), in spite of no

single explanation for order choosing. They had carefully retested the ARCH effect on

residuals by LM test but the serial correlation of error term was ignored. The result

showed that leverage effect and risk-return tradeoff were significant at 1% level.

Moreover, the total of Arch and Garch coefficient is approximately equal to one which

indicating highly persistent variance, namely the current level of volatility tended to be

positively correlated with its level during the immediately preceding periods. Their

research was disclosed on International Journal of Business and Social Science p.114-

128.

Another research of Suliman Zakaria with Peter Winker in 2012 displayed the

volatility model with symmetric or asymmetric studying on the Khartoum Stock

Exchange index (KSE) from Sudan and the Capital Market Authority index (CMA)

from Egypt over the periods from 2nd Jan 2006 to 30th November 2010. The Dickey-

Fuller stationary and Lagrange Multiplier (LM) of time-varying volatility test was

applied as a pre-estimation. Beside, LM test was also seen as the post-estimation to

ascertain that there was no remaining ARCH effects left in the residuals of the

estimated models. However, we discovered the same way of chossing model between

two papers of Suliman Zakaria in 2011 and 2012. The author directly using the simplest

form of GARCH-type models with the order (1,1) without any explainations. The

6 | P a g e

asymmetric (leverage) effect coefficient in both EGARCH(1,1) and TGARCH(1,1)

were respectively negatively and postively significant showing that negative shocks

imply a higher next period conditional variance than positive shocks.

Afees A.Salisu and Ismail O.Fasanya in 2012 also conducted three phases in

modeling symmetric and asymmetric volatility. To begin with the Lagrange Multilier

test of ARCH effects in squared residual, the author then proceeded to estimation and

using BIC and AIC to select the best fit one. GARCH with the order (1,1) was directly

used and ARCH model was not estimated based on the theoretical assumption that

GARCH with lower value of order provides a better fit than ARCH with high order.

The third phase was seen as postestimation using ARCH LM test to validate the

selected models as well as confirmed no remaining ARCH effect in residuals. Their

work was published on the International Journal of Energy Economics and Policy

(Vol.2, No.3, pp.167-183, ISSN: 2146-4553) which was named “Comparative

performance of volatility models for oil price”.

To capture the ARCH effect in residual and leverage effect, Sohail Chand and

coworkers had utilized the ARCH, GARCH-family models on the paper named

“Modeling and volatility analysis of share prices using ARCH and GARCH models”

which published on the World Apllied Sciences Journal 19 (1) in 2012 (p.77-82 and

ISSN: 1818-4952). The pre-estimation also began with ADF test of stationarity and

ARCH effect test. The author noted that ARCH effect was specified by correlogram of

squared residual when the ACF and PACF of squared errors show autocorrelation.

Likewise, this test was redone with the error obtained from the estimated models (with

the selection of AIC and BIC) to confirm well ARCH effect modelling.

To further research on the risk-return tradeoff, Heping Liu and Jing Shi in 2013

utilized various forms of GARCH-in-mean such as GJRGARCH-in-mean, EGARCH-

in-mean. Their paper was published on the Energy Economics 37 (p.152-166), namely

“Applying ARMA-GARCH approaches to forecasting short-term electricity prices”.

To conincide with other further researches, the author also employed the PACF of

7 | P a g e

residuals to disclose whether there were significant autocorrelations among the

residuals of estimated models or not.

The same as purpose of Heping Liu, Mohd. Aminul Islam in 2013 executed the

GARCH-in-mean models to test the risk-return hypothesis on Indonesian, Malaysian

and Singapore stock market with the sticker: JKSE, KLCI and STI respectively. The

data was collected from Jan 2007 to Dec 2012 which using daily log return. To embrace

the time-series progress, ADF test of stationarity and LM test of squared time-varying

error were executed. The author also used the GARCH with the simplest form with

order (1,1).Addiationally, the post-estimation with LM ARCH effect test and

autocorrelation function was preceded. Their result was disclosed on the Middle-East

Journal of Scientific Research 18 (7) (page.991-999 and ISSN: 1990-9233).

Likewise,another relevant conclusions of Ching Mun Lim and Siok Kun Sek in

2013 also contributes to our research for the countries in ASEAN, particularly Vietnam.

The authors had divided the data period (from 1990 to Dec 2010) into three phases: pre

crisis 1997, during crisis and post-crisis 1997, also using both symmetric and

asymmetric GARCH (Conventional GARCH, EGARCH and TGARCH) to modeling

the stock market volatility. In the normal condition (pre and post crisis), symmetric

GARCH seemed to be more preferred while asymmetric GARCH was highly

appreciated in the crisis period and post-crisis. They applied the conditional mean

equation of stock return which was constructed by the constant term plus the error

terms (rt=μ+εt). Ching Mun Lim also directly utilized the simplest form of GARCH

with the order (1,1). Additionally, there did not exist any test of stationarity, ARCH

effect and serial correlation in residuals for pre and post analysis. They just apllied

some error measures like mean squared error (MSE), root mean squared error (RMSE)

and mean absolute percentage error (MAPE) for ranking the GARCH performances.

Some doubts emerged whether there was any heterocsedastic residual to apply

GARCH models or not. Other problem arrived that no post-estimation was to ascertain

no remaining ARCH effect in residuals. Their result was published on the Procedia

Economics and Finance 5 (p.478-487).

8 | P a g e

Mohd. Aminul Islam in 2013 executed the study on Asian market (Malaysia,

Singapore, Japan and Hongkong) with the period from Jan 2007 to Dec 2012. The

author pointed out another research of Stock & Watson in 2012 (p.703) showing the

disadvantage of ARCH of the non-negative coeffients contraints since the variance

could not be negative. If these coefficients are positive and the recent squared error are

large, ARCH will predicts that current squared error will be large . As a consequence,

the simplest form GARCH (1,1) by Bollerslev 1986 was applied. Asymmetric GARCH

(EGARCH, TGARCH and PGARCH) was employed to tackle with leverage effect.

Otherwise, the risk-return relationship was again examined by GARCH-in-mean

(Engle, Lilien and Robin 1987). The writer also carefully conducted the ARCH LM

test test after model estimation. The result was pulished on the Australian Journal of

Basic and Applied Sciences 7(11) (p.294-303).

On Turkish stock market, R.Ilker Gokbulut and Mehmet Pekkaya researched on

BIST-100 index from 02/01/2002 to 04/02/2014 with 3027 daily observations of retuns.

Lagrange Multiplier test (1982) was preceding in pre and post estimation. Moreover,

AIC and BIC were used in model selection but writer also highlight that it was

inadequate with the still remaining ARCH effect of selected models if the AIC or BIC

value was smallest. This is an critical base for our research because both symmetric or

asymmetric GARCH can not capture the ARCH effect in spite of many remedial

measure like differencing and log normal functions. The paper of R.Ilker Gokbulut was

published on the International Journal of Economics and Finance (Vol.6, No.4 and

ISSN: 1916-971X) by Canadian Center of Science & Education.

Correlogram of autocorrelation to specify ACF and PACF of squared residuals

was also used by Yogendra Singh Rajavat and Amitabh Joshi in 2014. Their paper

named “Volatility in returns of BSE Small Cap Index using GARCH(1,1)” was

displayed on the Journal of Applied Management (Vol.II, Issue.I & ISSN: 2321-2535).

The other important test of ARCH disturbance in residuals was conducted. But the

paper seemed to be the same as the above literatures studying on only few samples.

9 | P a g e

As the same as the above papers, Trilochan Tripathy and Luis A. Gil-Alana in

2015 based on the error measures such as mean squared error (MSE), mean absolute

error (MAE) and mean absolute percent error to explain the forecast accuracy. Their

methodology included both symmetric and asymmetric GARCH (GARCH, EGARCH,

TGARCH) studying on S&P CNX Nifty of the National Stock Exchange in India (3rd

Aug 1992 to 21st Sep 2012). The test of Dickey & Fuller 1979 and Lagrange Multipiler

1982 were proposed in the pre-analysis but no single one in the post-analysis to check

out whether there was any remaining ARCH effect in residuals as standard progress.

Trilochan Tripathy et.al result was displayed on the Review of Development Finance

Journal 5 (p.91-97).

M.Tamiselvan and Shaik Mastan Vali applied GARCH, EGARCH and

TGARCH with the order (1,1) on Muscat stock market (MSM 30 Index, Financial

Index, Industrial Index, Service Index). Importantly, the coefficient of each model was

statistically significant at 1% level after estimation leading to the acceptable conclusion.

This result coincided with Tran Manh Tuyen 201. They only accepted the result if the

coefficients were all significant. Although the value of AIC and BIC was negative, they

also used as proxy to select among models.

Consequently, to our the best collection, it seems to have few studies on Vietnam

stock market in the period of 2012 till now. Moreover, most papers had been

investigated on two or three sample; there was no single one conducting on the whole

industry. Some research inadequately ignnored some post-estimation of

autocorrelation and ARCH effect in obtained residuals. The orther of GARCH model

was all used as the simplest form of (1,1). Additionally, Ruey S.Tsay gave futher

suggestion on specifying the order of GARCH model that only lower order GARCH

should be used in most application such as GARCH(1,1), GARCH(2,1) and

GARCH(1,2). As a standard proxy of error detect in pre or post-estimation, the

autocorrelation functions of squared residuals should be used to detect whether there

are any autocorrelations.

10 | P a g e

So our research will base on the instructive standard of Ruey S.Tsay in the book

of “Analysis of Financial Time Series and all references of above literature to conduct

the current investigation on Vietnamese Financial Industry, particularly. Both

symmetric and asymmetric GARCH models will be apllied to capture various

characteristics of time-series. The hypothesis of risk-return tradeoff also have been

tested by class of GARCH-in-mean models. Last, our main purpose is modelling the

stock return volatility by using univariate GARCH models.

4. Data description and methodology

4.1. Data and summary statistic

The descriptive summary: The time-series data used for modeling volatility in

this paper is the daily return of commons stock from the Financial Industry and listed

on Hochiminh Stock Exchange (HOSE). Data covers the periods from 3rd January 2012

to 8th April 2016.

The daily returns are calculated from daily closing stock prices collected from

cophieu68.com which are calculated as simple return (denoted rt): rt = [(Pt – Pt-1)/Pt-1].

Such a remedial measure, we will use the continously compounded return which are

the difference in logarithm of closing prices: rt = log(Pt/Pt-1) where Pt and Pt-1 are the

closing price at the current and previous day, respectively.

But we have to note that during the time-frame from the beginning of 2012 to 8th

April 2016, just getting the working day, common stocks will have their own different

number of trading days. Data comprises whole Financial industry with total 45

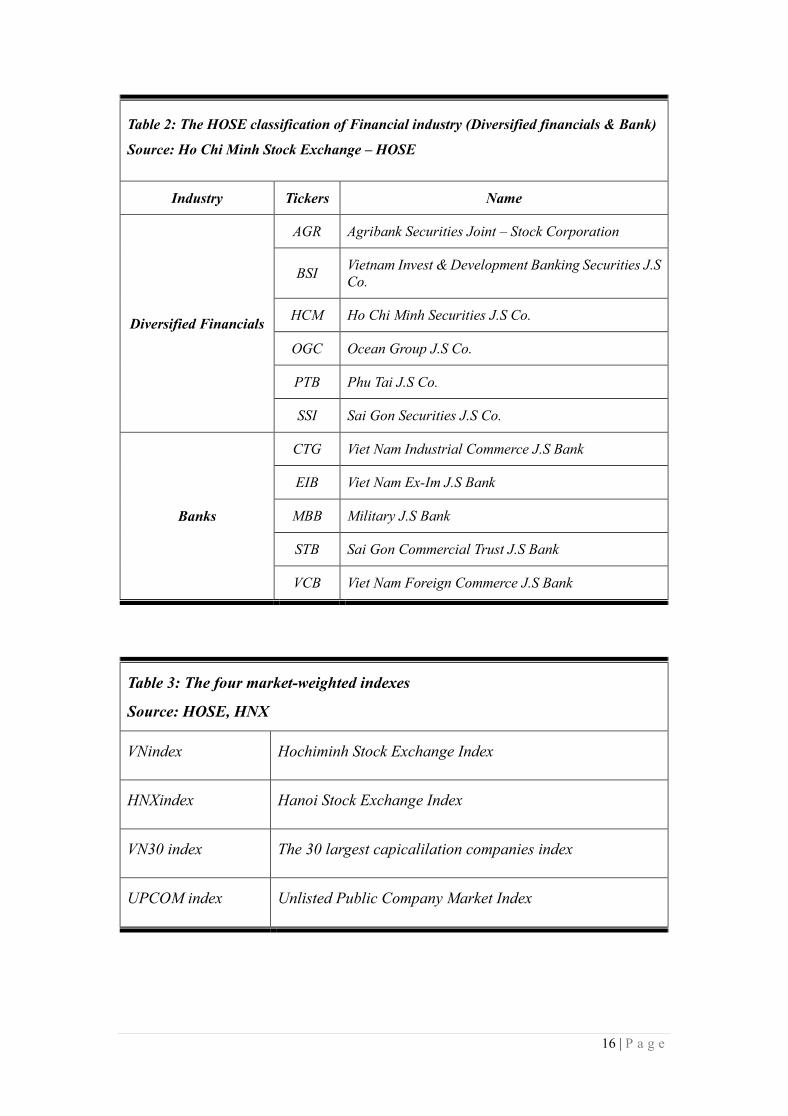

common stocks which is classified into 4 sub-industries by HOSE inclusing Insurance,

Real estate, Bank and Diversified financial (see table 1 & 2).

The four market-weighted index (Vnindex, HNXindex, VN30 index and

UPCOM index) cover the period also from the beginning of 2012 to 8th April 2016.

Vnindex and HNXindex are the market-weighted index of all common stocks which

are listed on the HOSE and HNX, respectively. VN30 index is also the market-

11 | P a g e

weighted index for 30 common stocks which have the largest capitalization, basing on

the oustanding shares, listed shares and charted capital. UPCOM is Unlisted Public

Company Market for which companies are under-conditional listed on HNX and

HOSE (see table 3).

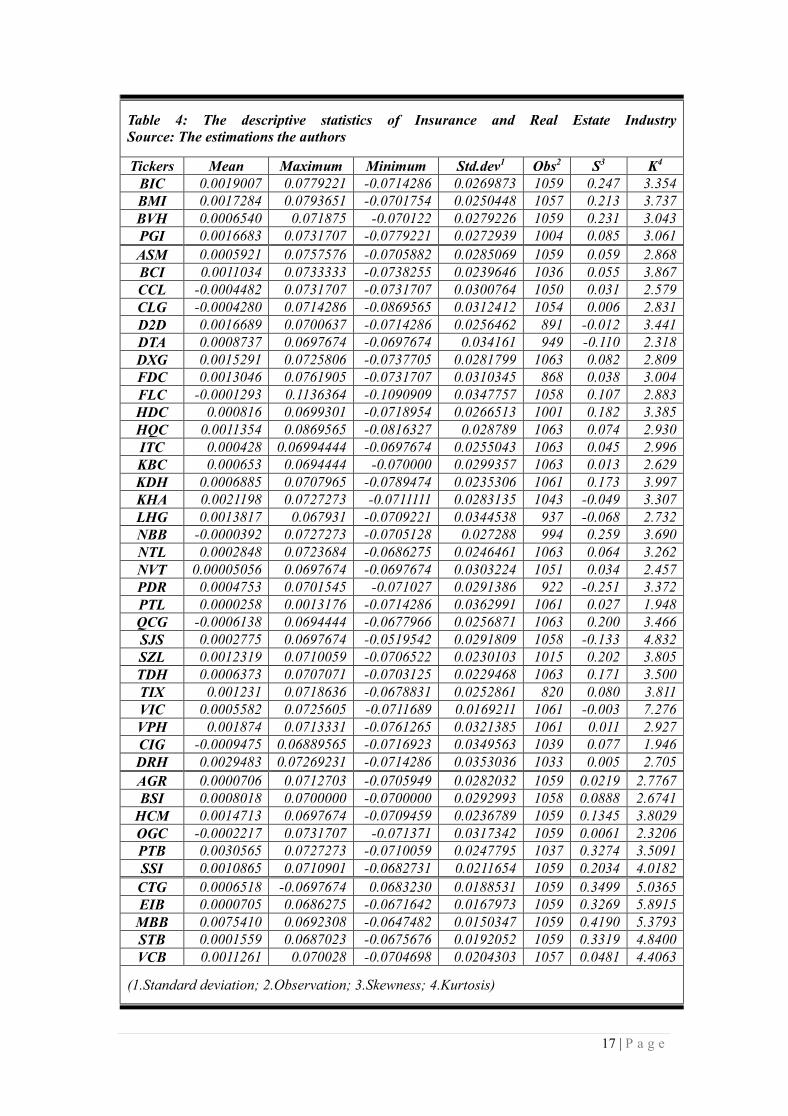

During the collected periods, the mean return of the insurance group is about

0.11488% while the mean return of the real estate is approximately 0.0709%. And the

mean return of the diversifed financial industry is 0.1044% and 1.1909% for banks

industry (see table 4)

Besides, the kurtosis and the skewness are used to show the form of distribution

of return. The “kurtosis” describe the degree of the peak of the distribution when the

“skewness” describe the asymmetric from the normal distribution. For normal

distribution, the skewness is equal to zero and the kurtosis is equal to three (excess

kurtosis equals zero). If the skewness is different from zero showing the

nonsymmetrical distribution when one side of the distribution does not mirror the other.

Particularly, the positive skewness indicates long right tail distribution which specifies

frequent small negative outcomes; when the negative skewness signs the long left tail

distribution which indicates a greater chance of extremenly negative scenarios.

Additionally, if it is the higher positive excess kurtosis (leptokurtosis) showing a higher

peak with fat tail than the normal distribution. The lower negative excess kurtosis

(platykurtosis) showing a lower peak with thin tail than normal (Ruey S.Tsay, 2005,

“Analsysis of Financial Time Series”, p.7-16).

According to the above descriptive statistic (see table 4 & 5), it shows that most

return series have not normal distribution. For insurance group, all stocks return have

the over-three kurtosis and positive non-zero skewness while for real estate, half of

them have over-three kurtosis and half have the lower-three kurtosis. Moreover, real

estate shows that seven stocks return have negative non-zero skewness and the

remainers have the postive skewness. For diversified financial industry, all stocks

return haave positive non-zero skewness; four lower-3-kurtosis tickers and two over-

12 | P a g e

3-kurtosis tickers. About banking group, the result shows that all had over-three

kurtosis and positive non-zero skewness.

To the four market-weighted indexes, all have over-three kurtosis and negative

skewness. Negative skewness signs the long left tail distribution which indicates a

greater chance of extremenly negative scenarios. And the higher positive excess

kurtosis (leptokurtosis) showing a higher peak with fat tail than the normal distribution.

In brief, for descriptive summary, either the general financial industry or the four

market-weighted had non-normal distribution of return (see table 5)

Pretesting for Stationarity (see table 6.1 to 6.3): The ADF (Dickey-Fuller 1979)

will test the null hypothesis of nonstationary and the alternative hypothesis of

stationary. It will reject the null hypothesis if the absolute value of ADF test statistic

exceeds the absolute critical value at 1%, 5% or 10% significance level (Mohd.Aminul

Islam 2013; Nguyen Quang Dong 2012, p.524-528; Ruey S.Tsay 2005). The test as

following:

𝒓𝒕 = 𝒄𝒕 + 𝜷𝒓 + ∑ 𝜱𝒊∆𝒓𝒕−𝒊 + 𝒆𝒊

𝒑−𝟏

𝒊=𝟏

𝑯𝟎: 𝜷 = 𝟏

𝑯𝟏: 𝜷 < 𝟏

We denote the rt is the return series; while ct can be zero or constant, ∆𝑥𝑡−𝑖 is the

differced series of rt . The the ADF-test statistic is calculated as below:

𝑨𝑫𝑭 − 𝒕𝒆𝒔𝒕 = �̂� − 𝟏

𝒔𝒕𝒅(�̂�) ; �̂� 𝑖𝑠 𝑡ℎ𝑒 𝑙𝑒𝑎𝑠𝑡 𝑠𝑞𝑢𝑎𝑟𝑒𝑑 𝑒𝑠𝑡𝑖𝑚𝑎𝑡𝑒 𝑜𝑓 𝛽

As consequence, we can conculde that all sample result show the stationary (see table

6a, 6b & 6c). This is the fundamental for the following step of forecasting. The same

application in the others papers could be listed as Mohd.Aminul Islam 2013; Ahmed

Elsheikh M.Ahmed & Suliman Zakaria 2011; Rilker Gokbulut & Mehmet Pekkaya

2014; Dana Al.Najjar 2016; Sohail Chand, Shahid Kamal & Imran Ali 2012; Suliman

13 | P a g e

Zakaria & Peter Winker 2012; M.Tamilselvan & Shaik Mastan Vali 2016, Trilochan

Tripathy & Luis A.Gil-Alana 2015.

Pretesting for Heteroscedasticity (see table 7.1 to 7.3): The other

characteristics series are the heteroscedaticity which must be tested by Lagrange

Multiplier test (Engle, 1982). Additionally, one of the most important issue before

applying ARCH or GARCH models is to first examine the residuals for evidence of

heteroscedaticity by the Lagrange Multiplier Test proposed by Engle 1982 which

previously applied by Ahmed Alsheikh M.Ahmed & Suliman Zakaria 2011; Suliman

Zakaria & Peter Winker 2012; Rilker Gokbulut & Mehmet Pekkaya 2014; Sohail

Chand, Shahid Kamal & Imran Ali 2012; Afees A.Salisu & Ismail O.Fasanya 2012;

M.Tamilselvan & Shaik Mastan Vali 2016. We will obtain the residuals from the OLS

regression of mean equation then squared its as below:

𝒆𝒕𝟐 = 𝜶𝟎 + 𝜶𝟏𝒆𝒕−𝟏

𝟐 + ⋯ + 𝜶𝒒𝒆𝒕−𝒒𝟐 + 𝜺𝒕

The null hypothesis that there is no ARCH effect formulated as:

H0: α1 = α2 =…= αq = 0

H1: αi ≠ 0 (for at least one i= 1,2,…,q)

(Another form H1: α12+ α2

2+…+ αq2

>0)

If the value of LM test statistic (TR2) is greater than the critical value from the X2(q)

distibution or the coeffient of the lagged term is statistically significant, the null

hypothesis will be rejected. The same conclusion can be achieved of the F-version of

the test is considered. As consequence, we get all the value of LM test of all research

sample showing that there is ARCH effect in the squared error

Pretesting the autocorrelation in residual (see table 8.1 to 8.3): According to

intruction of Ruey S.Tsay in the book named “Analysis of Financial Time Series”

published by John Wiley and Sons 2005 (The 2nd edition, p.107-119), by

reinvestigating on the squared residual obtained by mean equation, we check out the

14 | P a g e

autocorrelation function (ACF – autocorrelation function or PACF – partial

autocorrelation function), if it is statically different from zero, the autocorrelation in

residuals is ascertained. As can be seen from the result of table 8.1-8.3, all sample show

that the error terms are autocorrelated

In summary, we find the evidence of stationary but existing the ARCH effect and

autocorraltion in residuals. It is also the principal condition to apply ARCH, GARCH

models.

The orders of ARCH and GARCH-type models will be discussed in the section

5.2 of methodology. It is the common way using ACF and PACF of squared errors to

specifying the order m of ARCH proposed by Ruey S.Tsay (2005, p.106-107). Tim

Bollerslev, in 1992, demonstrated that GARCH could be adapted by low orders such

as GARCH(1,1), GARCH(1,2) and GARCH(2,1) (T.Bollerslev, Ray Y.Chou 1992 and

Kroner, “ARCH modelling in finance: A reivew of the theory and empirical evidence”,

Journal of econometrics 52).

15 | P a g e

Table 1: The HOSE classification of Financial industry (Insurance & Real Estate)

Source: Ho Chi Minh Stock Exchange – HOSE

Industry Tickers Name

Insurance

BIC The Vietnam Investment & Development Banking Insurance Co.

BMI Bao Minh J.S Company

BVH Bao Viet Insurance Corporation

PGI Petrolimex J.S Company

Rea

l es

tate

ASM Sao Mai J.S Company

BCI Binh Chanh Investment & Construction J.S Company

CCL Cuu Long Investment & Development J.S Company

CIG Coma18 J.S Company

CLG Cotec Housing Investment and Devepment J.S Co.

D2D The Two Industrial Development J.S Company

DRH Dream House Investment J.S Company

DTA De Tam J.S Company

DXG Dat Xanh Real Estate Service & Construction J.S Co.

FDC Ho Chi Minh Foreign & Invest Development J.S Co.

FLC FLC Corporation J.S Company

HAR An Duong Thao Dien Commercial Real Estate Investment J.S

Company

HDC Ba Ria Vung Tau Housing Development J.S Company

HQC Hoang Quan Real Estate Commerce & Service J.S Company

ITC Housing Investment J.S Company

KBC Kinh Bac City Development J.S Company

KDH Khang Dien Housing Investment J.S Company

KHA Khanh Hoi Investment & Service J.S Company

LDG Long Dien Investment J.S Company

LHG Long hau J.S Company

NBB Nam Bay Bay Investment J.S Company

NLG Nam Long Investment J.S Company

NTL Tu Liem City Development J.S Company

NVT Ninh Van Bay Real Estate & Traveling J.S Company

PDR Phat Dat Real Estate Development J.S Company

PTL Petro City & Infrastructure Investment J.S Co.

QCG Quoc Cuong Gia Lai J.S Co.

SJS Song Da City & Industry Development J.S Co.

SZL Sonadezi Long Thanh J.S Co.

TDH Thu Duc House Development J.S Co.

TIX Tan Binh Export Import Service & Investment J.S Co.

VIC Vingroup J.S Co.

VPH Van Phat Hung J.S Co.

16 | P a g e

Table 2: The HOSE classification of Financial industry (Diversified financials & Bank)

Source: Ho Chi Minh Stock Exchange – HOSE

Industry Tickers Name

Diversified Financials

AGR Agribank Securities Joint – Stock Corporation

BSI Vietnam Invest & Development Banking Securities J.S

Co.

HCM Ho Chi Minh Securities J.S Co.

OGC Ocean Group J.S Co.

PTB Phu Tai J.S Co.

SSI Sai Gon Securities J.S Co.

Banks

CTG Viet Nam Industrial Commerce J.S Bank

EIB Viet Nam Ex-Im J.S Bank

MBB Military J.S Bank

STB Sai Gon Commercial Trust J.S Bank

VCB Viet Nam Foreign Commerce J.S Bank

Table 3: The four market-weighted indexes

Source: HOSE, HNX

VNindex Hochiminh Stock Exchange Index

HNXindex Hanoi Stock Exchange Index

VN30 index The 30 largest capicalilation companies index

UPCOM index Unlisted Public Company Market Index

17 | P a g e

Table 4: The descriptive statistics of Insurance and Real Estate Industry

Source: The estimations the authors

Tickers Mean Maximum Minimum Std.dev1 Obs2 S3 K4

BIC 0.0019007 0.0779221 -0.0714286 0.0269873 1059 0.247 3.354

BMI 0.0017284 0.0793651 -0.0701754 0.0250448 1057 0.213 3.737

BVH 0.0006540 0.071875 -0.070122 0.0279226 1059 0.231 3.043

PGI 0.0016683 0.0731707 -0.0779221 0.0272939 1004 0.085 3.061

ASM 0.0005921 0.0757576 -0.0705882 0.0285069 1059 0.059 2.868

BCI 0.0011034 0.0733333 -0.0738255 0.0239646 1036 0.055 3.867

CCL -0.0004482 0.0731707 -0.0731707 0.0300764 1050 0.031 2.579

CLG -0.0004280 0.0714286 -0.0869565 0.0312412 1054 0.006 2.831

D2D 0.0016689 0.0700637 -0.0714286 0.0256462 891 -0.012 3.441

DTA 0.0008737 0.0697674 -0.0697674 0.034161 949 -0.110 2.318

DXG 0.0015291 0.0725806 -0.0737705 0.0281799 1063 0.082 2.809

FDC 0.0013046 0.0761905 -0.0731707 0.0310345 868 0.038 3.004

FLC -0.0001293 0.1136364 -0.1090909 0.0347757 1058 0.107 2.883

HDC 0.000816 0.0699301 -0.0718954 0.0266513 1001 0.182 3.385

HQC 0.0011354 0.0869565 -0.0816327 0.028789 1063 0.074 2.930

ITC 0.000428 0.06994444 -0.0697674 0.0255043 1063 0.045 2.996

KBC 0.000653 0.0694444 -0.070000 0.0299357 1063 0.013 2.629

KDH 0.0006885 0.0707965 -0.0789474 0.0235306 1061 0.173 3.997

KHA 0.0021198 0.0727273 -0.0711111 0.0283135 1043 -0.049 3.307

LHG 0.0013817 0.067931 -0.0709221 0.0344538 937 -0.068 2.732

NBB -0.0000392 0.0727273 -0.0705128 0.027288 994 0.259 3.690

NTL 0.0002848 0.0723684 -0.0686275 0.0246461 1063 0.064 3.262

NVT 0.00005056 0.0697674 -0.0697674 0.0303224 1051 0.034 2.457

PDR 0.0004753 0.0701545 -0.071027 0.0291386 922 -0.251 3.372

PTL 0.0000258 0.0013176 -0.0714286 0.0362991 1061 0.027 1.948

QCG -0.0006138 0.0694444 -0.0677966 0.0256871 1063 0.200 3.466

SJS 0.0002775 0.0697674 -0.0519542 0.0291809 1058 -0.133 4.832

SZL 0.0012319 0.0710059 -0.0706522 0.0230103 1015 0.202 3.805

TDH 0.0006373 0.0707071 -0.0703125 0.0229468 1063 0.171 3.500

TIX 0.001231 0.0718636 -0.0678831 0.0252861 820 0.080 3.811

VIC 0.0005582 0.0725605 -0.0711689 0.0169211 1061 -0.003 7.276

VPH 0.001874 0.0713331 -0.0761265 0.0321385 1061 0.011 2.927

CIG -0.0009475 0.06889565 -0.0716923 0.0349563 1039 0.077 1.946

DRH 0.0029483 0.07269231 -0.0714286 0.0353036 1033 0.005 2.705

AGR 0.0000706 0.0712703 -0.0705949 0.0282032 1059 0.0219 2.7767

BSI 0.0008018 0.0700000 -0.0700000 0.0292993 1058 0.0888 2.6741

HCM 0.0014713 0.0697674 -0.0709459 0.0236789 1059 0.1345 3.8029

OGC -0.0002217 0.0731707 -0.071371 0.0317342 1059 0.0061 2.3206

PTB 0.0030565 0.0727273 -0.0710059 0.0247795 1037 0.3274 3.5091

SSI 0.0010865 0.0710901 -0.0682731 0.0211654 1059 0.2034 4.0182

CTG 0.0006518 -0.0697674 0.0683230 0.0188531 1059 0.3499 5.0365

EIB 0.0000705 0.0686275 -0.0671642 0.0167973 1059 0.3269 5.8915

MBB 0.0075410 0.0692308 -0.0647482 0.0150347 1059 0.4190 5.3793

STB 0.0001559 0.0687023 -0.0675676 0.0192052 1059 0.3319 4.8400

VCB 0.0011261 0.070028 -0.0704698 0.0204303 1057 0.0481 4.4063

(1.Standard deviation; 2.Observation; 3.Skewness; 4.Kurtosis)

18 | P a g e

Table 5: The descriptive statistics of the four market-weighted indexes

Source: The estimations the authors

Tickers Mean Maximum Minimum Std.dev1 Obs2 S3 K4

Vnindex 0.0004643 0.0392557 -0.0605465 0.0112674 1059 -0.5596313 5.501443

HNXindex 0.0003258 0.0556075 -0.064800 0.0127936 1059 -0.540226 5.992988

VN30 0.0003941 0.0416241 -0.0577473 0.0112687 1060 -0.4343574 5.474966

UPCOM 0.0005316 0.0742958 -0.0644823 0.0111791 1059 -0.1658537 14.52935

19 | P a g e

Table 6.1: Dickey-Fuller test of stationary for Insurance and Real Estate

Industry

Source: The estimation of authors

Tickers Test Statistic

Z(t) 1% level 5% level 10% level

BIC -30.926 -3.430 -2.860 -2.570

BMI -32.845 -3.430 -2.860 -2.570

BVH -29.435 -3.430 -2.860 -2.570

PGI -38.553 -3.430 -2.860 -2.570

ASM -30.115 -3.430 -2.860 -2.570

BCI -31.552 -3.430 -2.860 -2.570

CCL -31.074 -3.430 -2.860 -2.570

CIG -29.892 -3.430 -2.860 -2.570

D2D -38.416 -3.430 -2.860 -2.570

DRH -28.163 -3.430 -2.860 -2.570

DTA -28.035 -3.430 -2.860 -2.570

DXG -30.062 -3.430 -2.860 -2.570

FDC -29.644 -3.430 -2.860 -2.570

FLC -30.012 -3.430 -2.860 -2.570

HDC -36.813 -3.430 -2.860 -2.570

HQC -31.190 -3.430 -2.860 -2.570

ITC -32.189 -3.430 -2.860 -2.570

KBC -31.597 -3.430 -2.860 -2.570

KDH -30.117 -3.430 -2.860 -2.570

KHA -44.270 -3.430 -2.860 -2.570

LHG -32.622 -3.430 -2.860 -2.570

NBB -30.991 -3.430 -2.860 -2.570

NTL -30.948 -3.430 -2.860 -2.570

NVT -31.269 -3.430 -2.860 -2.570

PDR -31.287 -3.430 -2.860 -2.570

PTL -33.009 -3.430 -2.860 -2.570

QCG -30.893 -3.430 -2.860 -2.570

SJS -28.641 -3.430 -2.860 -2.570

SZL -35.677 -3.430 -2.860 -2.570

TDH -29.447 -3.430 -2.860 -2.570

TIX -36.731 -3.430 -2.860 -2.570

VIC -33.915 -3.430 -2.860 -2.570

VPH -31.781 -3.430 -2.860 -2.570

20 | P a g e

Table 6.2: Dickey-Fuller test of Stationarity for Diversified finance and Banks

Source: The estimation of authors

Tickers Test statistic

Z(t)

1% Critical

value

5% Critical

value

10%

Critical

value

P-value for

Z(t)

AGR -33.954 -3.430 -2.860 -2.570 0.000

BSI -30.455 -3.430 -2.860 -2.570 0.000

HCM -31.368 -3.430 -2.860 -2.570 0.000

OGC -30.327 -3.430 -2.860 -2.570 0.000

PTB -32.681 -3.430 -2.860 -2.570 0.000

SSI -32.869 -3.430 -2.860 -2.570 0.000

CTG -32.367 -3.430 -2.860 -2.570 0.000

EIB -29.909 -3.430 -2.860 -2.570 0.000

MBB -34.659 -3.430 -2.860 -2.570 0.000

STB -29.979 -3.430 -2.860 -2.570 0.000

VCB -31.725 -3.430 -2.860 -2.570 0.000

Table 6.3: Pretest of Stationarity for Vnindex, HNXindex, VN30index, UPCOMindex

Source: The estimation of authors

Tickers Test statistic 1% Critical

value

5% Critical

value

10% Critical

value

P-value

VNindex -30.417 -3.439 -2.860 -2.571 0.00000

HNXindex -33.373 -3.340 -2.860 -2.570 0.00000

VN30index -30.464 -3.430 -2.860 -2.570 0.00000

UPCOMindex -18.852 -3.420 -2.830 -2.570 0.00000

21 | P a g e

Table 7.1: Pre-estimation of heteroscedasticity for Insurance and Real Estate

Industry

Source: Estimated by the authors

Tickers LM test statistic P-value

BIC 106.474 0.00000

BMI 40.354 0.00000

BVH 150.515 0.00000

PGI 38.153 0.00000

ASM 41.592 0.00000

BCI 54.639 0.00000

CCL 61.987 0.00000

CIG 79.241 0.00000

CLG 112.242 0.00000

D2D 66.681 0.00000

DRH 71.523 0.00000

DTA 71.741 0.00000

DXG 32.385 0.00000

FDC 123.424 0.00000

FLC 58.442 0.00000

HDC 38.913 0.00000

HQC 37.659 0.00000

ITC 38.443 0.00000

KBC 59.228 0.00000

KDH 94.132 0.00000

KHA 104.797 0.00000

LHG 57.406 0.00000

NBB 106.293 0.00000

NTL 32.55 0.00000

NVT 40.173 0.00000

PDR 92.299 0.00000

PTL 36.19 0.00000

QCG 83.189 0.00000

SJS 68.075 0.00000

SZL 37.714 0.00000

TDH 49.02 0.00000

TIX 85.908 0.00000

VIC 11.401 0.00070

VPH 6.855 0.00880

22 | P a g e

Table 7.2: Pre-estimation of heteroscedasticity for Diversified finance and Banks

Source: The estimation of author

Tickers L-M test statistic P-value

AGR 75.370 0.000

BSI 28.925 0.000

HCM 45.606 0.000

OGC 22.285 0.000

PTB 66.774 0.000

SSI 16.473 0.000

CTG 43.306 0.000

EIB 144.625 0.000

MBB 20.998 0.000

STB 123.713 0.000

VCB 18.074 0.000

Table 7.3: Pretest of Heteroscedasticity for VNindex, HNXindex, VN30 index and UPCOM

index

Source: The estimation of authors

Tickers Lagrange Multiplier test statistic P-value

VNindex 15.794 0.00010

HNXindex 29.166 0.00000

VN30index 16.681 0.00000

UPCOMindex 449.943 0.00000

23 | P a g e

Table 8.1: Pretest of autocorrelation in squared error for Insurance and real estate

Source: The estimation of authors

Tickers AC PAC Q statisitc Prob

BIC 0.3171 0.3172 106.79 0.00000

BMI 0.1954 0.1955 40.487 0.00000

BVH 0.3771 0.3771 151.00 0.00000

PGI 0.1950 0.1951 38.286 0.00000

ASM 0.1982 0.1983 41.717 0.00000

BCI 0.2292 0.2293 54.600 0.00000

CCL 0.2430 0.2431 62.157 0.00000

CIG 0.2761 0.2764 79.455 0.00000

CLG 0.3264 0.3266 112.61 0.00000

D2D 0.2737 0.2737 66.948 0.00000

DRH 0.2631 0.2632 71.687 0.00000

DTA 0.2751 0.2751 72.026 0.00000

DXG 0.1746 0.1746 32.495 0.00000

FDC 0.3771 0.3773 123.86 0.00000

FLC 0.2350 0.2352 58.614 0.00000

HDC 0.1972 0.1973 39.041 0.00000

HQC 0.1882 0.1883 37.765 0.00000

ITC 0.1902 0.1903 38.569 0.00000

KBC 0.2361 0.2361 59.407 0.00000

KDH 0.2979 0.2979 94.397 0.00000

KHA 0.3170 0.3171 105.13 0.00000

LHG 0.2474 0.2474 57.548 0.00000

NBB 0.3268 0.3268 106.46 0.00000

NTL 0.1739 0.1762 32.245 0.00000

NVT 0.1955 0.1956 40.274 0.00000

PDR 0.3163 0.3165 92.558 0.00000

PTL 0.1846 0.1848 36.255 0.00000

QCG 0.2797 0.2798 83.373 0.00000

SJS 0.2537 0.2538 68.31 0.00000

SZL 0.1928 0.1928 37.848 0.00000

TDH 0.2148 0.2148 49.189 0.00000

TIX 0.3238 0.3238 86.282 0.00000

VIC 0.1037 0.1037 11.442 0.00007

VPH 0.1084 0.1085 6.878 0.00870

24 | P a g e

Table 8.2: Pretest of autocorrelation in squared error for Diversified finance and

banks

Source: The estimation of authors

Tickers AC PAC Q statisitc Prob

AGR 0.2653 0.2679 74.771 0.00000

BSI 0.1653 0.1654 29.005 0.00000

HCM 0.2076 0.2076 45.760 0.00000

OGC 0.1451 0.1451 22.369 0.00000

PTB 0.2538 0.2539 66.979 0.00000

SSI 0.1248 0.1248 16.530 0.00000

CTG 0.2015 0.2016 43.126 0.00000

EIB 0.3697 0.3697 145.16 0.00000

MBB 0.1409 0.1409 21.07 0.00000

STB 0.3415 0.3416 123.88 0.00000

VCB 0.1308 0.1308 18.136 0.00000

Table 8.3: Pretest of autocorrelation in squared error for the hour market-

weighted indexes

Source: The estimation authors

Tickers AC PAC Q statisitc Prob

Vnindex 0.1222 0.1222 15.848 0.0001

HNXindex 0.1660 0.1660 29.271 0.0000

VN30 index 0.1255 0.1255 16.738 0.0000

UPCOM index 0.6521 0.6521 451.58 0.0000

25 | P a g e

4.2. Methodology

Conditional heteroscedastic models are the basic econometrics tools used to

estimate and forecast asset return volatility depending on each time-series

characteristics. In the section we will review both symmetric (ARCH, GARCH) and

asymmetric GARCH-type models (EGARCH, GJRGARCH). Our aims are to study

some statistical methods and econommetric models avaible in the literature for

modelling the conditional heteroscedastic volatility model.

The univariate volatility models include the autoregressive conditional

heteroscedastic (ARCH) model of Engle (1982), the generalized ARCH (GARCH)

model of Bollerslev (1986), GARCH-in-mean of Engle, Lilien and Robin (1987), the

exponential GARCH (EGARCH) model of Nelson (1991), the GJRGARCH model of

Glosten, Jagannathan & Runkle (1993). These are models which will be displayed in

our current paper using the information selection criteria (AIC and BIC) to choose the

best fit. Following Ching Mun Lim & Siok Kun Sek (2013), we assume that the

conditional mean equation of stock return is defined as the constant term plus residuals

term: rt = μ + εt.

4.2.1. ARCH (m) – Engle 1982

Ruey S.Tsay in 2005 gave some instructions of model building with four phase:

specifying the mean equation and obtaining the residuals; conducting ARCH effect test

on the obtained residuals, the third with ARCH/GARCH model estimationand last step

of careful checking the fittest model and refining if necessary. The general model of

ARCH (m) process is as follow (Engle, 1982):

𝒓𝒕 = 𝝁 + 𝒖𝒕

𝒖𝒕 = 𝝈𝒕𝜺𝒕

𝝈𝒕𝟐 = 𝜱𝟎 + 𝜱𝟏𝒖𝒕−𝟏

𝟐 + ⋯ + 𝜱𝒎𝒖𝒕−𝒎𝟐

𝝈𝒕𝟐 = 𝜱𝟎 + ∑ 𝜱𝒊

𝒎

𝒊=𝟏

𝒖𝒕−𝒊𝟐

(𝜱𝟎 > 𝟎, 𝜱𝒊 ≥ 𝟎 𝒇𝒐𝒓 𝒊 > 𝟎)

Where Φ0 is constant, бt2 is the squared conditional variance of error term, ut-m

is the lagged value of error term. In general, бt2 is expressed as a function of past

squared errors. Another issue is that the unknown coefficients (Φ0, Φ1, Φ2,… Φm) must

26 | P a g e

be non-negative since the variance can not be negative meaning that ARCH assume

that positive and negative shocks have the same effects on volatility because it depends

on the squared of previous shocks. However the asymmetric literature proved that

return of financial asset responds differently to either positive or negative shocks (Ruey

S.Tay 2005; Nelson 1991; Glosten, Jagannathan and Runkle 1993 and Zakoian 1994;

Ding, Granger and Engle 1993).

If these coefficient are positive and the recent squared residual are large, ARCH

predicts that the current squared error will be large in magnitude in the sense that its

variance is large. Hence, ARCH models are likely to overpredict the volatility because

they respond slowly to large isolated shocks to return series (Ruey S.Tay 2005).

And if the ARCH effect is found to be statistically significant, we can use PACF

of ut2 (squared error term specified by correlogram in Stata programme) to intepret the

ARCH order (m). We have:

бt2 = Φ0 + Φ1u2

t-1 + Φ2 u2t-2 + … +Φm u2

t-m

Hence, u2t is an unbiased estimate of the squared variance of error term

(бt2).Otherwise, it is expected that u2

t is the linear regression of u2t-1, u2

t-2,…,u2t-m

as same as the autoregressive function AR(q) when the PACF is the useful tool for

determing the order of AR(q). For AR(q) model, the lagged (1) sample of PACF will

be close to zero. In brief, for an AR(q) series, the sample PACF cuts off at lag q and

the same version for ARCH(m) model based on PACF of squared errors (Ruey S.Tay

2005).

However, ARCH models are likely to overpredict the volatility since they

respond slowly to large shocks to the return. Additionally, ARCH(m) estimation will

often require a large number of parameters and higher order m to capture the volatility

process. As consequence, to remedy this problem, Bollerslev 1986 developed the

Generalized ARCH model (GARCH).

27 | P a g e

4.2.2. GARCH (m,s) - Bollerslev 1986

The standard GARCH (m,s) model espresses the variance at time t as following:

𝒓𝒕 = 𝝁 + 𝒖𝒕 𝒖𝒕 = 𝝈𝒕𝜺𝒕

𝝈𝒕𝟐 = 𝜱𝟎 + ∑ 𝜱𝒊

𝒎

𝒊=𝟏

𝒖𝒕−𝒊𝟐 + ∑ 𝜽𝒋

𝒔

𝒋=𝟏

𝝈𝒕−𝒋𝟐

[ 𝜱𝟎 > 𝟎, 𝜱𝒊 & 𝜽𝒋 ≥ 𝟎, ∑ (

𝒎𝒂𝒙(𝒎.𝒔)

𝒊=𝟏

𝜱𝒊 + 𝜽𝒋) < 𝟏 ]

The GARCH model allows the error variance (б2t) depending on either its own

past squared errors (u2t-m) or its own past values (б2

t-s) where m is the order of ARCH

terms and s is the order of GARCH term. GARCH also assumes that the variance is

non-negative. Large s order signs that shocks to the conditional variance take a long

time to die out meaning highly persistent volatility while large m order implies a

sizeable reaction of volatility to market movement. Hence, if 𝜱𝒊 + 𝜽𝒋 is close to untity,

the shock at t time will be persistent for many future periods. And one of the weakness

of GARCH model is the asumption of symmetry in volatility estimation.

We will apply GARCH(1,1), GARCH(1,2) and GARCH(2,1) with low order to

model the volatility and then use the information criteria to select the best fit (Ruey

S.Tsay 2005). Tim Bollerslev, in 1992, also specified that most low order GARCH such

as GARCH(1,1), GARCH(1,2) or GARCH(2,1) were employed (Tim Bollerslev, Ray

Y.Chou, Kenneth F.Kroner, “ARCH modeling in finance- A review of theory and

empirical evidence”, Journal of econometrics 52 (100), 1992, p.21-22).

4.2.3. GARCH-in-mean (m,s) – Engle, Lilien and Robin (1987)

Engle assume that the return of a security my depend on its volatility. To model

such a phenomenon, GARCH-in-mean was introduced with the following model:

𝒓𝒕 = 𝝁 + 𝒖𝒕 + 𝒄𝝈𝒕𝟐

𝒖𝒕 = 𝝈𝒕𝜺𝒕

𝝈𝒕𝟐 = 𝜱𝟎 + ∑ 𝜱𝒊

𝒎

𝒊=𝟏

𝒖𝒕−𝒊𝟐 + ∑ 𝜽𝒋

𝒔

𝒋=𝟏

𝝈𝒕−𝒋𝟐

28 | P a g e

The parameter c is called the risk premium parameter. The term of variance 𝝈𝒕𝟐

is added into the conditional mean equation intepreting the risk-return tradeoff

hypothesis. As an application, it can be listed such as Mohd.Aminul Islam 2013,

Suliman Zakaria & Peter Winkers 2012, Ahmed Elsheikh & Suliam Zakaria 2011.

If the parameter c is statistically positive, it will confirm the positive relationship

between return and volatility meaning high risk – high return. In order words, an

increase in return is caused by an increasse in the conditional variance (Enders, 2004,

“Applied Econometric Time Series, 2nd edition, Wiley Series in Probability and

Statistics). But either GARCH or GARCH-in-mean are also considered to be

symmetric model assuming that both positive and negative shocks of equal size

generate an equal effect on volatility.

Nonetheless, the negative shocks tend to have a larger impact on future volatility

than the positive one, namely asymmetric or leverage effect which has to be captured

by others asymmetric GARCH models (for instance: Exponential GARCH model

(EGARCH) of Nelson 1991 and GJRGARCH model of Glosten, Jagannathan and

Runkle 1993 as following sections).

4.2.4. Exponential GARCH (EGARCH) – Nelson 1991

To remedy some weakness of symmetric GARCH model, Nelson advanced the

following model as: EGARCH(m,s):

𝒓𝒕 = 𝝁 + 𝒖𝒕

𝒖𝒕 = 𝝈𝒕𝜺𝒕

𝒍𝒏(𝝈𝒕𝟐) = 𝜱𝟎 + ∑ 𝜱𝒊

𝒔

𝒊=𝟏

|𝒖𝒕−𝒊| + 𝜸𝒊𝒖𝒕−𝒊

𝝈𝒕−𝒊+ ∑ 𝜽𝒋

𝒎

𝒋=𝟏

𝒍𝒏 (𝝈𝒕−𝒋𝟐 )

The presence of parameter 𝜸𝒊 indicates an asymmetric effect of shocks on

volatility and the value of is statistically different from zero or negative signing the

asymmetry or the leverage effect (Ruey S.Tsay 2005; R.Ilker Gokbulut & Mehmet

Pekkaya 2014; Mohd.Aminul Islam 2013; M.Tamiselvan & Shaik Mastan Vali 2016;

Suliman Zakaria & Peter Winker 2012; Dana Al.Najjar 2016). Nelson used the logged

conditional variance to relax the positiveness contraint of GARCH model (Ruey S.Tsay

2005) and applied the absolute value of 𝒖𝒕−𝒊 to respond asymmetrically to positive

and negative lagged value of ut .

29 | P a g e

Hence, a positive ut-i contributes Φi(1+γi)/єt-i/ to the log volatility while a

negative ut-i specifies Φi(1-γi)/єt-i/ (where 𝜺𝒕−𝒊 =𝒖𝒕−𝒊

𝝈𝒕−𝒊). Since the negative shocks

tend to have larger impact than the positive shocks with the negative. Major papers

showed we can directly test the asymmetric effect on the estimated EGARCH model

by intepreting the statistically significant γi (≠0 or <0).

4.2.5. GJRGARCH – Glosten, Jagannathan & Runkle 1993

Here is the second common volatility model used to tackle with leverage effect,

namely GJRGARCH of Glosten 1993 as following:

𝝈𝒕𝟐 = 𝜱𝟎 + ∑(𝜱𝒊 + 𝜸𝒊𝑵𝒕−𝒊 )𝒖𝒕−𝒊

𝟐

𝒔

𝒊=𝟏

+ ∑ 𝜽𝒋

𝒎

𝒋=𝟏

𝝈𝒕−𝒋𝟐

Where Nt-i is the dummy variable used to differentiate the good or bad shocks:

𝑵𝒕−𝒊 = {𝟏 𝒊𝒇 𝒖𝒕−𝒊 < 𝟎𝟎 𝒊𝒇 𝒖𝒕−𝒊 ≥ 𝟎

GJR also has the constraint of non-negative coefficients (𝜱𝒊, 𝜸𝒊, 𝜽𝒋)which is

similar to GARCH model. A positive ut-i contributes Φiu2t-i to б2t volatility while a

negative ut-i contributes (Φi + 𝜸𝒊 )u2t-i to volatility б2t . Hence, GJR had assumed that

unexpected changes in the market will have different impact on the volatility of stock

return. Noting that a non-zero significant 𝜸𝒊 indicate the asymmetry and when 𝜸𝒊 > 𝟎

signs a leverage effect.

4.2.6. Remedial measures

Taking a differencing function when there is a serial correlation among error

terms and the correlation is expressed as following:

𝒖𝒕 = 𝒀𝒕 − 𝜱𝟎 − 𝜱𝟏𝒀𝒕−𝒊

(𝒘𝒉𝒆𝒓𝒆 𝒀𝒕 & 𝒀𝒕−𝒊 𝒊𝒔 𝒔𝒕𝒂𝒕𝒊𝒐𝒏𝒂𝒓𝒚)

When Yt and Yt-i is stationary, the error term ut is stationary saying that the

residual is the first order autocorrelation as: ∆𝑌𝑡 = 𝜱𝟏∆𝒀𝒕−𝒊 + 𝜺𝒕 (Nguyen Quang

Dong and Nguyen Thi Minh, 2012, “Econometrics”, National Economics University

Press, p.315).

30 | P a g e

Normally, the economic time series, such as stock return series would deal with

autocorrelation in residuals resulting the autorrelation function value often exceeds

zero (detected by ACF and PACF functions). Denoting the autocorrelation function

ACF(k) is ρk (Ruey S.Tsay, 2005, p.25-30):

𝝆𝒌 = 𝒄𝒐𝒓𝒓(𝒀𝒕, 𝒀𝒕−𝒌) = 𝜹𝒌

𝜹𝟎, 𝒌 = 𝟎, 𝟏, 𝟐, …

𝒘𝒉𝒆𝒓𝒆 𝜹𝒌 = 𝒄𝒐𝒗(𝒀𝒌, 𝒀𝒕−𝒌), 𝒌 = 𝟎, 𝟏, 𝟐, …

𝒘𝒉𝒆𝒏 𝒌 = 𝟎, 𝜹𝟎 = 𝒗𝒂𝒓(𝒀𝒕 )

(𝒔𝒆𝒆 𝒀𝒕 𝒂𝒔 𝒆𝒓𝒓𝒐𝒓 𝒕𝒆𝒓𝒎 𝒖𝒕)

4.2.7. Autocorrelation

Noting that serial correlation is related to the variance of parameter and if, after

model estimation, there is still correlated we should reject that models. Now we have

the equation of parameter variance, perhaps homoscedasticity is satisfied (Nguyen

Quang Dong, 2012):

𝒗𝒂𝒓(𝜷�̂�) = 𝝈𝟐

∑ 𝒙𝟐𝒕𝟐

𝒕

+ 𝟐 ∑ ∑ 𝒌𝒕𝒌𝒕+𝒔𝒄𝒐𝒗(𝒖𝒕, 𝒖𝒕+𝒔)

𝒏−𝒕

𝒔=𝟏

𝒏

𝒕=𝟏

Hence, when there is autocorrelated residuals, 𝟐 ∑ ∑ 𝒌𝒕𝒌𝒕+𝒔𝒄𝒐𝒗(𝒖𝒕, 𝒖𝒕+𝒔)𝒏−𝒕𝒔=𝟏

𝒏𝒕=𝟏 will

be different from zero causing that the variance of estimated parameter will be biased.

We could not continuously adapt the models and then the remedial measure of

diiferencing and loggeg function is to be used (as discussed in section 5.2.6).

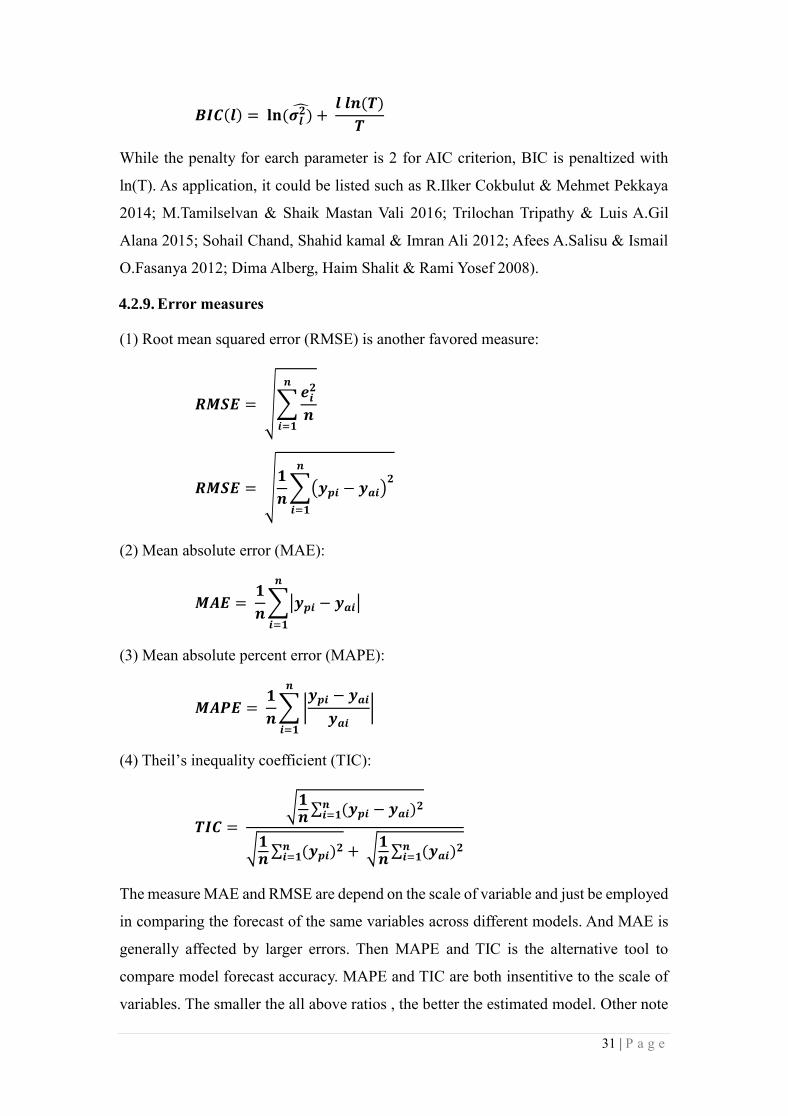

4.2.8. Model information criteria

Akaike (1973) proposed AIC (Akaike information criteria) for model selection

(ARIMA, GARCHs) denoted as following:

𝑨𝑰𝑪(𝒍) = 𝐥𝐧 (𝝈𝒍𝟐)̂ +

𝟐𝒍

𝑻

𝒘𝒉𝒆𝒓𝒆 𝑻 𝒊𝒔 𝒔𝒂𝒎𝒑𝒍𝒆 𝒔𝒊𝒛𝒆 & 𝒍 𝒊𝒔 𝒕𝒐𝒕𝒂𝒍 𝒐𝒓𝒅𝒆𝒓

& 𝝈𝒍�̂� 𝒊𝒔 𝒕𝒉𝒆 𝒎𝒂𝒙𝒊𝒎𝒖𝒎 𝒍𝒊𝒌𝒆𝒍𝒊𝒉𝒐𝒐𝒅 𝒆𝒔𝒕𝒊𝒎𝒂𝒕𝒆 𝒐𝒇 𝝈𝒍

𝟐

𝝈𝒍𝟐 𝒊𝒔 𝒕𝒉𝒆 𝒄𝒐𝒏𝒅𝒊𝒕𝒊𝒐𝒏𝒂𝒍 𝒗𝒂𝒓𝒊𝒂𝒏𝒄𝒆 𝒐𝒇 𝒖𝒕

The first phrase of AIC measures the goodness of fit and the second phrase expressed

as the penalty function of the criterion. And Schwarz Bayesian (1978) introduced

another criteria (BIC):

31 | P a g e

𝑩𝑰𝑪(𝒍) = 𝐥𝐧 (𝝈𝒍𝟐)̂ +

𝒍 𝒍𝒏(𝑻)

𝑻

While the penalty for earch parameter is 2 for AIC criterion, BIC is penaltized with

ln(T). As application, it could be listed such as R.Ilker Cokbulut & Mehmet Pekkaya

2014; M.Tamilselvan & Shaik Mastan Vali 2016; Trilochan Tripathy & Luis A.Gil

Alana 2015; Sohail Chand, Shahid kamal & Imran Ali 2012; Afees A.Salisu & Ismail

O.Fasanya 2012; Dima Alberg, Haim Shalit & Rami Yosef 2008).

4.2.9. Error measures

(1) Root mean squared error (RMSE) is another favored measure:

𝑹𝑴𝑺𝑬 = √∑𝒆𝒊

𝟐

𝒏

𝒏

𝒊=𝟏

𝑹𝑴𝑺𝑬 = √𝟏

𝒏∑(𝒚𝒑𝒊 − 𝒚𝒂𝒊)

𝟐𝒏

𝒊=𝟏

(2) Mean absolute error (MAE):

𝑴𝑨𝑬 = 𝟏

𝒏∑|𝒚𝒑𝒊 − 𝒚𝒂𝒊|

𝒏

𝒊=𝟏

(3) Mean absolute percent error (MAPE):

𝑴𝑨𝑷𝑬 = 𝟏

𝒏∑ |

𝒚𝒑𝒊 − 𝒚𝒂𝒊

𝒚𝒂𝒊|

𝒏

𝒊=𝟏

(4) Theil’s inequality coefficient (TIC):

𝑻𝑰𝑪 =

√𝟏𝒏

∑ (𝒚𝒑𝒊 − 𝒚𝒂𝒊)𝟐𝒏𝒊=𝟏

√𝟏𝒏

∑ (𝒚𝒑𝒊)𝟐𝒏𝒊=𝟏 + √𝟏

𝒏∑ (𝒚𝒂𝒊)𝟐𝒏

𝒊=𝟏

The measure MAE and RMSE are depend on the scale of variable and just be employed

in comparing the forecast of the same variables across different models. And MAE is

generally affected by larger errors. Then MAPE and TIC is the alternative tool to

compare model forecast accuracy. MAPE and TIC are both insentitive to the scale of

variables. The smaller the all above ratios , the better the estimated model. Other note

32 | P a g e

that TIC is ranges between zero and one with the value of TIC converging to zero

showing the better. Heping Liu & Jing Shi 2013, Ching Mun Lim & Siok Kun Sek

2013 and Dima Alberg 2008 had applied these measure into their papers to compare

among defined symmetric and asymmetric volatility models. Hence, we just utilize the

MAPE and TIC to compare the model’s accuracy.

4.2.10. The l-step ahead forecast

The last phases came for forecasting with the l-step ahead forecast for ARCH(m) at the

forecast origin h (Ruey S.Tsay, 2005). The 1-step ahead forecast is denoted б2h+1:

𝝈𝒉𝟐(𝟏) = ɸ𝟎 + ɸ𝟏𝒖𝒉

𝟐 + ⋯ + ɸ𝒎𝒖𝒉+𝟏−𝒎𝟐

The 2-step ahead forecast б2h+2 :

𝝈𝒉𝟐(𝟐) = ɸ𝟎 + ɸ𝟏𝝈𝒉

𝟐(𝟏) + ɸ𝟐𝒖𝒉𝟐 + ⋯ + ɸ𝒎𝒖𝒉+𝟐−𝒎

𝟐

We have the general equation for l-step forecast as following:

𝝈𝒉𝟐(𝒍) = ɸ𝟎 + ∑ ɸ𝒊

𝒎

𝒊=𝟏

𝝈𝒉𝟐(𝒍 − 𝒊)

𝒘𝒉𝒆𝒓𝒆 𝝈𝒉𝟐(𝒍 − 𝒊) = 𝒖𝒉+𝒍−𝒊

𝟐 𝒘𝒊𝒕𝒉 (𝒍 − 𝒊 < 𝟎)

But we have to note that the weakness of ARCH models are likely to overpredict the

volatility because they respond slowly to large shock to return. GARCH also has others

shortcoming that the large past squared value of residual and variance give an increase

to the current variance. GARCH’s phenomenon showed that the large shock in the past

tended to be followed by another large shock (as volatility clustering). Additionally,

the 1-step ahead forecast of GARCH(1,1) at the forecast origin h, as following:

𝝈𝒉+𝟏𝟐 = ɸ𝟎 + ɸ𝟏𝒖𝒉

𝟐 + 𝜷𝟏𝝈𝒉𝟐

(𝑤ℎ𝑒𝑟𝑒 𝑢ℎ & 𝜎ℎ2 𝑎𝑟𝑒 𝑘𝑛𝑜𝑤𝑛 𝑎𝑡 𝑡ℎ𝑒 𝑡𝑖𝑚𝑒 ℎ)

In general, for l-step ahead forecast in GARCH model, we have:

𝝈𝒉𝟐(𝒍) = ɸ𝟎 + (ɸ𝟏 + 𝜷𝟏)𝝈𝒉

𝟐(𝒍 − 𝟏), 𝒍 > 𝟏

33 | P a g e

5. EMPIRICAL RESULTS AND DISCUSSIONS

` To again introduce, data mangement is performed by Stata 12 programme. After

we pre-test the return seires in the section 5.1, the result displays that there was ARCH

effect in the residual but stationary.

The following sections are divided into two sections: section 5.1-the model

estimation for the financial industry, section 5.2-the model estimation for the four

market-weighted indexes.

The model we applied are ARCH(m), GARCH(m,s), GARCH-M(m,s)

EGARCH(m,s), EGARCH-M(m,s), GJRGARCH(m,s) and GJRGARCH-M(m,s).

For both section 5.1 and 5.2, we estimate the proper model and the value of BIC

and AIC will be generated after each model estimation in order to compare which is

more available. In our paper, we only disclose the result after using the AIC and BIC

to filter (see appendix 1)

Each section will also include the first post-estimation of ARCH effect and

serial correlation using again Lagrange-Multilier and ACF, respectively basing the

preceeding filter result.

If there is still remaning the ARCH effect or autocorrelation in residuals meaning

useless inadequate model, reject it. To remedy, we have to refine the model by

differencing and natural logarithic functions. We, first, also have to generate the ARCH

effect test. Then redefining the model on remedied data (see appendix 2)

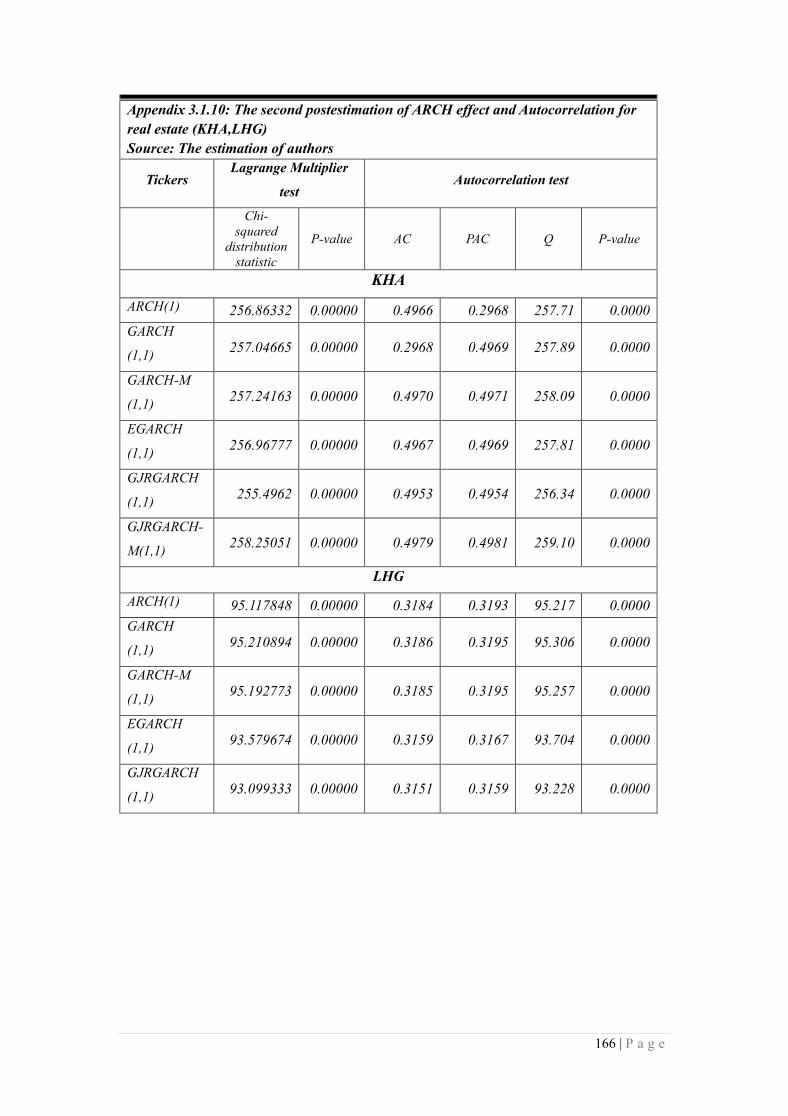

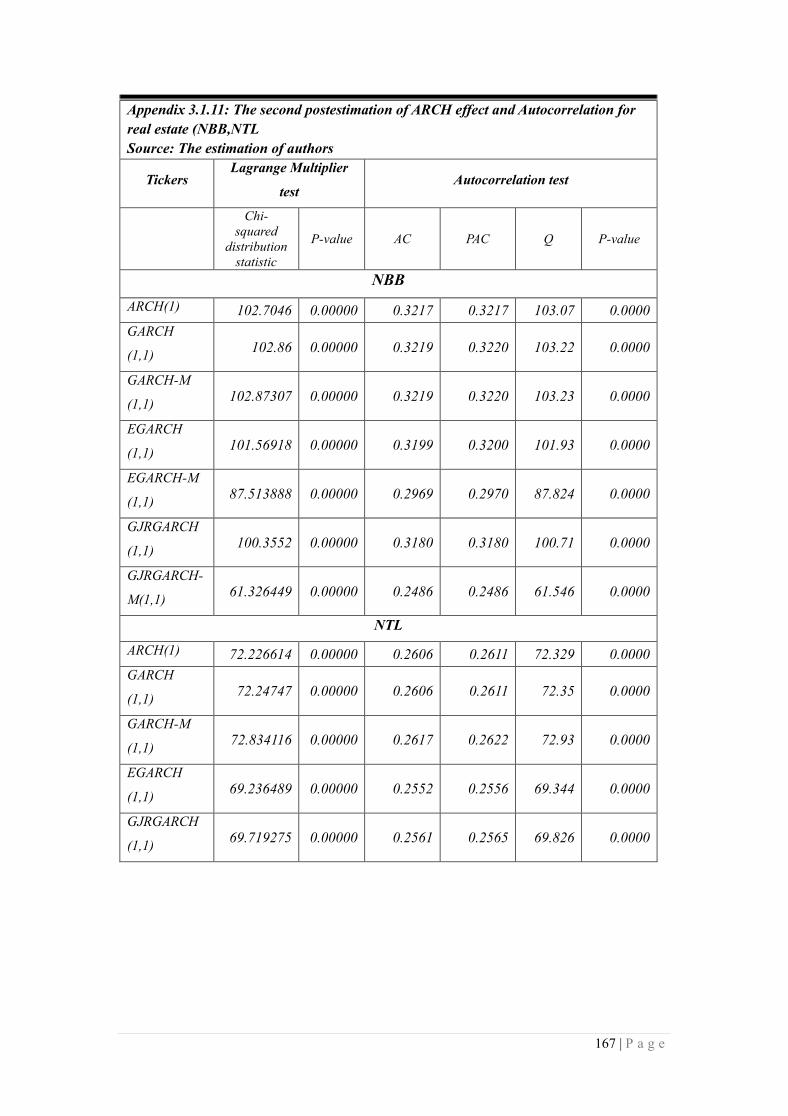

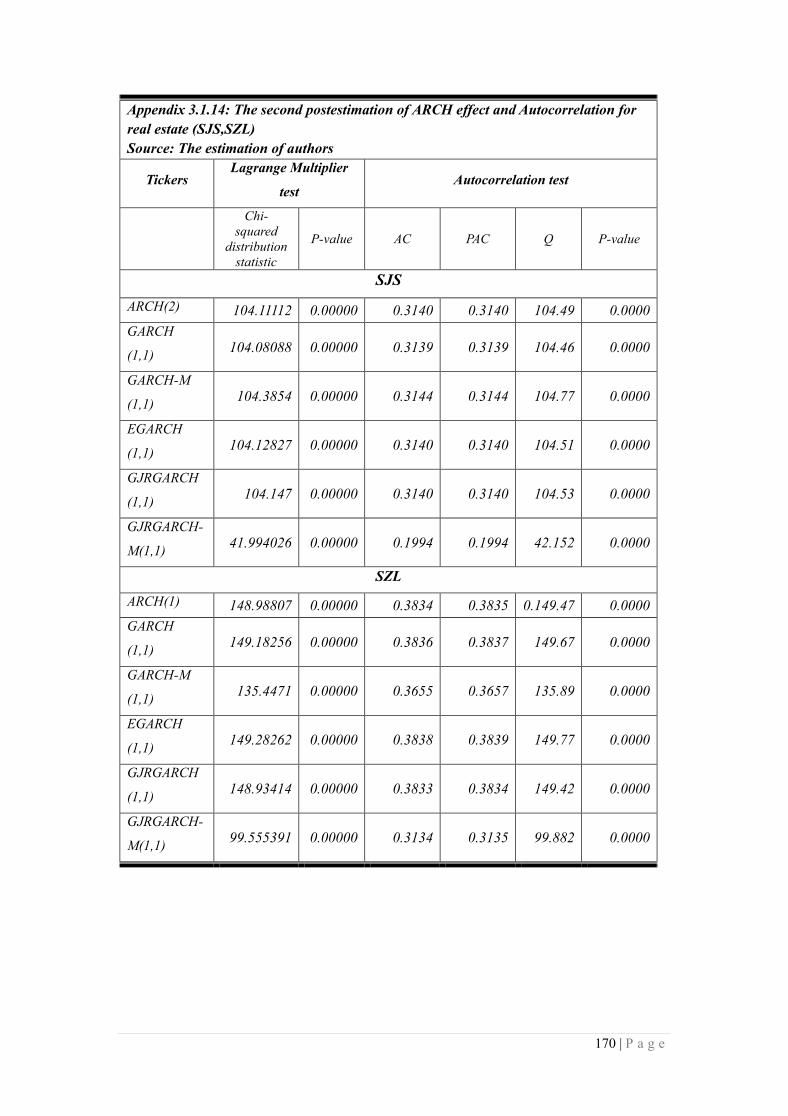

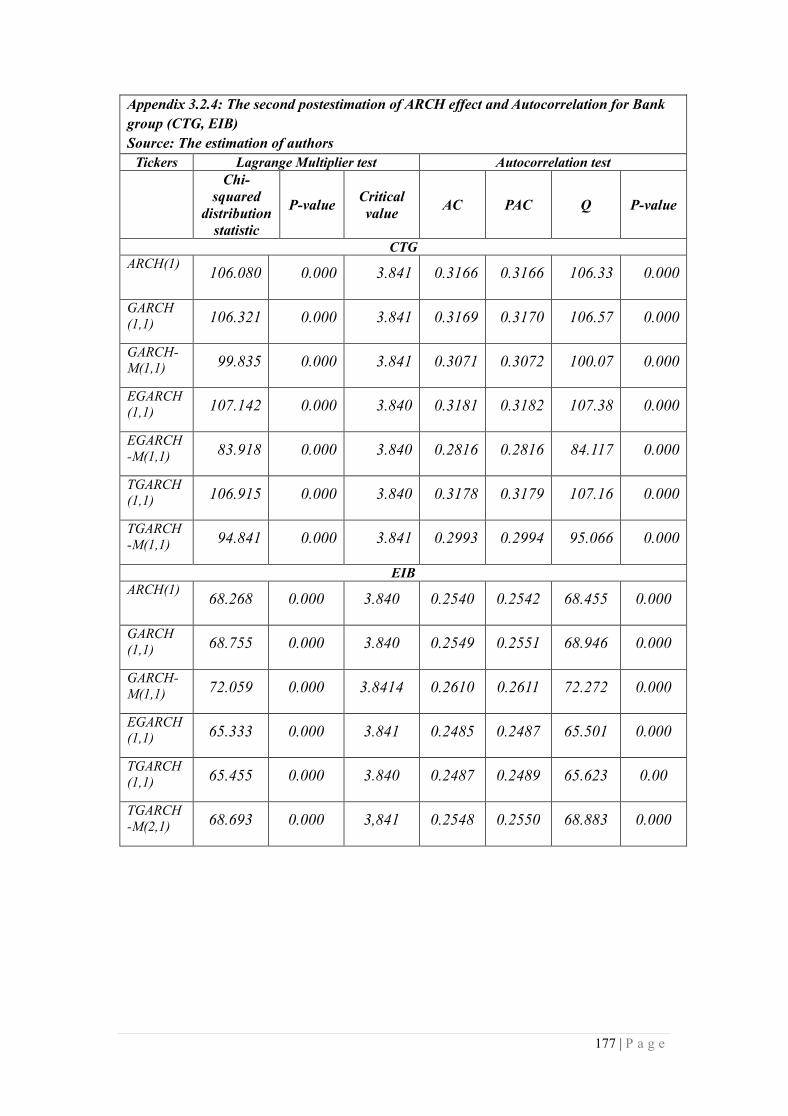

Last, the second post-estimation of ARCH effect and autocorrealtion must be

executed (see appendix 3). If the post-estimated model, again, can not capture the

ARCH effect or serial correlation, reject it. Last, the remainers which can totally

capture the ARCH effect and serial correlation are used to forecast. The error measures

will be generated to choose which is the best accuracy one.

34 | P a g e

5.1. The model estimation result of the financial industry

5.1.1.The model selection

After executing both symmetric and asymmetric GARCH, the two information

criterions (AIC & BIC) were used to select the model and the detailed model

parameters will be attached on the appendix 1 (Appendix 1: The model parameters

result of financial industry)

ARCH model estimation (see table 9): For insurance industry including BIC,

PGI, BMI and BVH, the first two tickers followed ARCH(1) while the last two follow

ARCH(3) and no one was available for ARCH(4) and ARCH(5).

For real estate including 30 common stocks, the majority were available for

lower order ARCH models (ARCH(1) and ARCH(2)). There were five tickers followed

ARCH(3) which were BCI, CLG, FLC, NTL, TDH and the last one ITC followed

ARCH(4). In short, most tickers in real estate followed the ARCH(1) & ARCH(2).

For diversified finance, three tickers followed ARCH(3) which were HCM, OGC,

SSI. The ARCH(1) was fitted by BSI and AGR was used for ARCH(2). Especially,

only one tickers followed ARCH(4) which was PTB.

Beside, banking tickers seemed to be available for high order ARCH, at least 2.

We had CTG and MBB following much high order ARCH(4) and ARCH(5).

Now we have to focus the principle of the ARCH’s weakness. ARCH model

often require many parameter to adequately describe the volatility process of return

series so that we other proper model was GARCH-family models. Our results seemed

to correspond with the previous papers, GARCH(1,1) was more available for most

tickers

GARCH-family models estimation (see table 10.1 – 10.2): The insurance

industry was totally captured by both symmetric and asymmetric GARCH(1,1). For

real estate, 16 tickers also followed the simplest model of GARCH and the others 14

tickers followed higher order. While most tickers in diversified finance and banking

group follow the lowest order GARCHs

Noting that, we can not applied these models if the post-estimation of

heteroscedasticity and autocorrelation test were not executed. And if the post results

indicated that they could not capture the problem, we have to refine the model by

35 | P a g e

differencing and logging functions.

5.1.2. The first postestimation of heteroscedasticity and autocorrelation

The test for conditional heteroscedasticity is the Lagrange multiplier (LM) test

proposed by Engle 1982. The test is equivalent to the F statistic for testing αi =0

(i=1,…,m) in this auxiliary linear regression (Ruey S.Tsay, “Analysis of financial time

series”, Second edition, page. 101-102). To retest whether there are any remaining

Arch Effect in the residuals, the LM test was also applied in R.Ilker Gokbulut &

Mehmet Pekkaya, 2014, “Estimating and forecasting volatility of financial markets

using Asymmetric Garch models: An application on Turkish financial markets”,

International Journal of Economics & Finance, vol.6, no.4, ISSN 1916-971X. Afees

A.Salisu & Ismail O.Fasanya in 2012 also conducted the ARCH LM test on order to

ascertain of the chosen models had captured these effects; the same as Kolade Sunday

Adesina.

Here below is the auxiliary regression of squared residual and its lagged value

on m lags which haved been previously selected using AIC and BIC information

criterion:

And the null hypothesis H0: α1=....=αm=0. First we have to obtain the residual and

square them. Then, we define the test statistic (TR2) and compare the p-value from this

statistic to the desired test level (α) and reject the null hypothesis if the p-value is

smaller (Ruey S.Tsay,” Analysis of financial time-series, Second edition, John Wiley

& Sons Publication, p.101-102).

Additionally, the autocorrelation of residuals have also been retested to confirm

whether there are any serial correlation by autocorrelation function of the obtained

squared residual from previous model selection phase (Ruey S.Tsay, “Analysis of

financial time-series”, Second edition, page. 116-120). The empirical test of

autocorrelation by ACF was also proposed by Walter Enders, “Applied Econometric

Time-Series”, John Wiley & Sons Publication, page.147-153.

If the both tests of heteroscedasticity and serial correlation in residuals show that

there is still remaining the ARCH effect or autocorrelation, the remedial measure

Tmtwhere

euuu tmtmtt

,...,1

... 22

110

2

36 | P a g e

including the log normal of return and differencing function must be applied (Nguyen

Quang Dong, “Econometrics”, 2012, page.295-317).

In term of application of autocorrelation retest, Haping Liu and Jing Shi in 2013

also employed the partial autocorrelation function (PACF) of residual to determine that

there did not exist significant autocorrelation among the residual gathered after each

model estimation. Their paper, in 2013, studied “Applying Arma-Garch approaches to

forecasting short-term electricity prices” which was published on the Journal of Energy

Economics p.152-166.

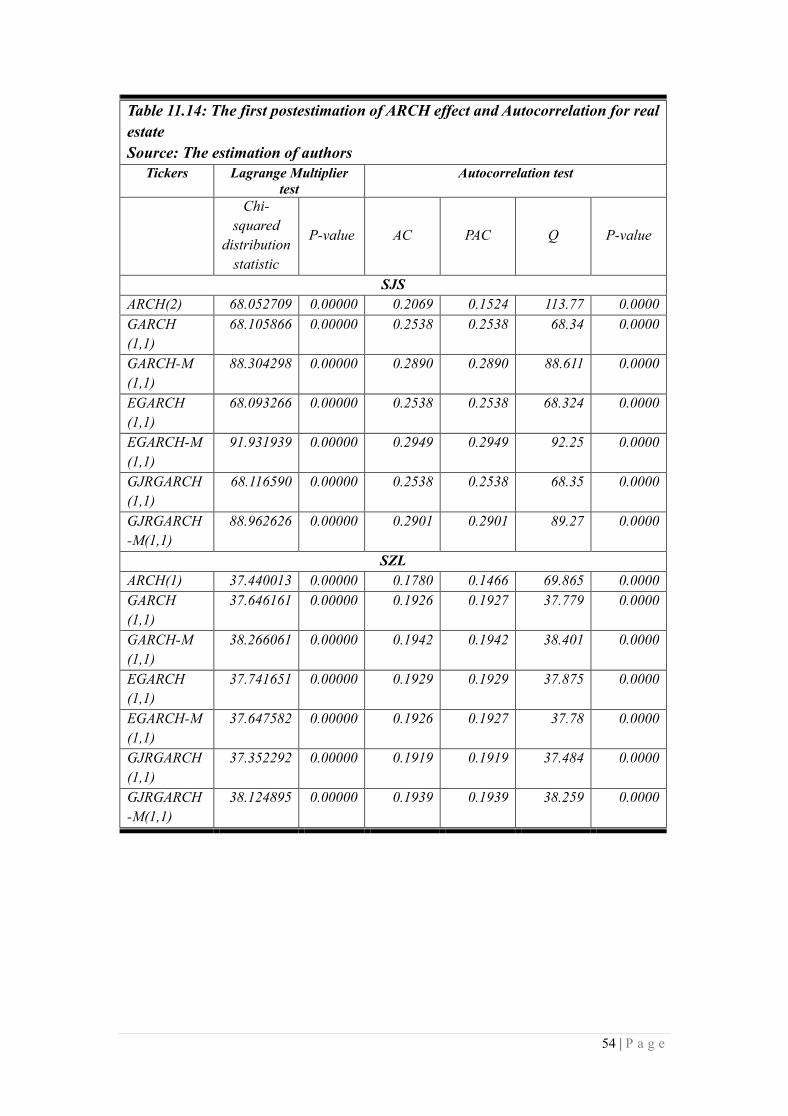

The result was unexpected. All of the four sub-industies was heteroscedastic

and serial corralted even if we applied both symmetric and asymmetric volatility

models (See table 11.1 to table 13.3). Table 11.1 to table 11.17 will present the first

post-test of ARCH effect and autocorrelation for insurance and real estate. Table 12.1

to table 12.3 will display the pre-test result of the diversified finance industry and table

13.1 to table 13.3 will display the result of banking industry.

There still existed a very high value of Chi squared distribution test and a zero

P-value much less than α (1%, 5% and 10%). As consequence, the null hypothesis of

no ARCH effect must be rejected. Other wise the test of autocorrelation also was

unsatisfactory as same as the ARCH effect result with a non-zero ACF and PACF and

p-value of zero much less than the α (1%, 5% or 10%).

This result was not satisfactory. Infact, this is an very important post-estimation

we have to execute. However, some researches ignored this phase such as Tran Manh

Tuyen, 2011, “Model volatility using GARCH models: Evidence from Vietnam”,

Economics Bulletin, Vol.31, no.3, pp.1935-1942. The lack of this postestimation was

also seen at the paper of Dana Al.Najjar, 2016 (Asian Journal of Finance & Accounting,

ISSN: 1946-052X, Vol8, No.1, p.152-167). The same inadequacy was signed at the

study of Shing Mun Lim & Siok Kun Sek, 2013 (Procedia Economics and Finance 5,

p.478-487) and of Dima Alberg, Haim Shalit and Rami Yosef, 2008 (Applied Financial

Economics 18, p.1201-1208).

37 | P a g e

Table 9: The first ARCH model classification for the Financial industry

Source: The estimation of authors

Model Group Tickers

ARCH (1)

Insurance BIC, PGI

Real estate

D2D, DTA, FDC, HDC,

HQC, KHA, NVT, QCG, TIX,

VIC, VPH

Diverisified finance BSI

Bank None

ARCH(2)

Insurance None

Real estate

ASM, CCL, CIG, DXG,

DRH, KBC, KDH, LHG,

NBB, PDR, PTL, SJS, SZL.

Diverisified finance AGR

Bank STB, VCB

ARCH (3)

Insurance BMI, BVH

Real estate BCI, CLG, FLC, NTL, TDH

Diverisified finance HCM, OGC, SSI

Bank EIB

ARCH (4)

Insurance None

Real estate ITC

Diverisified finance PTB

Bank CTG

ARCH(5) Bank MBB

38 | P a g e

39 | P a g e

Table 10.1: The first symmetric and asymmetric GARCH classification for

insurance & real estate industries.

Source: The estimation of authors

Models Group Tickers

Sym

met

ric

&

asy

mm

etri

c

GA

RC

H (

1,1

)

Insurance BIC, BMI, BVH, PGI

Real estate

ASM, BCI, CCL, CIG, CLG, DTA, FLC,

KBC, KDH, KHA, LHG, NBB, NVT, QCG,

SJS, SZL,

GARCH(1,2)

Real estate

FDC, ITC, PDR, D2D, DXG

GARCH-M(1,2) FDC, ITC, PDR, D2D, DXG,

GARCH(2,1) None

GARCH-M(2,1) None

EGARCH(1,2) FDC, HQC, NTL, D2D, DXG, VPH

EGARCH-M(1,2) TIX

EGARCH(2,1) None

EGARCH-M(2,1) HDC, PTL, TDH, VIC, DRH

GJRGARCH(1,2) FDC, ITC, PDR, D2D, DXG

GJRGARCH-M(1,2) FDC, ITC, PDR, DXG,

GJRGARCH(2,1) VPH

GJRGARCH-M(2,1) VPH

40 | P a g e

Table 10.2: The first symmetric and asymmetric GARCH estimation for

diversified & banking industries.

Source: The estimation of authors

Models Group Tickers

Symmetric & asymmetric

GARCH (1,1)

Diverisified finance AGR, BSI, HCM, OGC,

PTB

Bank CTG, STB, MBB, VCB

EGARCH(1,2) Diverisified finance OGC

Bank MBB

EGARCH-M(2,1) Diverisified finance SSI

Bank EIB

GJRGARCH(2,1) Diverisified finance SSI

GJRGARCH-M(2,1) Diverisified finance SSI

Bank EIB

41 | P a g e

Table 11.1: The first postestimation of ARCH effect and Autocorrelation for

insurance

Source: The estimation of authors

Tickers Lagrange Multiplier

test

Autocorrelation test

Chi-

squared

distribution

statistic

P-value AC PAC Q P-value

BIC

ARCH(1) 108.43402 0.00000 0.3200 0.3201 108.76 0.0000

GARCH

(1,1)

107.79909 0.00000 0.3191 0.3192 108.12 0.0000

GARCH-M

(1,1)

88.006431 0.00000 0.2883 0.2884 88.27 0.0000

EGARCH

(1,1)

107.4123 0.00000 0.3185 0.3186 107.73 0.0000

EGARCH-M

(1,1)

95.653566 0.00000 0.3006 0.3007 95.94 0.0000

GJRGARCH

(1,1)

107.91426 0.00000 0.3192 0.3194 108.24 0.0000

GJRGARCH

-M(1,1)

88.216387 0.00000 0.2886 0.2888 88.481 0.0000

BMI

ARCH(3) 39.901002 0.00000 0.2103 0.1475 142.12 0.0000

GARCH

(1,1)

41.522099 0.00000 0.1982 0.1983 41.658 0.0000

GARCH-M

(1,1)

37.860777 0.00000 0.1893 0.1893 37.985 0.0000

EGARCH

(1,1)

40.45812 0.00000 0.1957 0.1957 40.591 0.0000

EGARCH-M

(1,1)

40.230582 0.00000 0.1951 0.1952 40.363 0.0000

GJRGARCH

(1,1)

40.757242 0.00000 0.1964 0.1965 40.891 0.0000

GJRGARCH

-M(1,1)

38.595779 0.00000 0.1911 0.1912 38.723 0.0000

42 | P a g e

Table 11.2: The first postestimation of ARCH effect and Autocorrelation for

insurance

Source: The estimation of authors

Tickers Lagrange Multiplier

test

Autocorrelation test

Chi-

squared

distribution

statistic

P-value AC PAC Q P-value

BVH

ARCH(3) 150.52471 0.00000 0.2917 0.1538 340.16 0.0000

GARCH

(1,1)

150.53229 0.00000 0.3771 0.3771 151.02 0.0000

GARCH-M

(1,1)

147.49588 0.00000 0.3733 0.3733 147.97 0.0000

EGARCH

(1,1)

150.34731 0.00000 0.3769 0.3769 150.83 0.0000

EGARCH-M

(1,1)

149.97207 0.00000 0.3764 0.3764 150.46 0.0000

GJRGARCH

(1,1)

150.44582 0.00000 0.3770 0.3770 150.93 0.0000

GJRGARCH

-M(1,1)

149.42046 0.00000 0.3757 0.3757 149.90 0.0000

PGI

ARCH(1) 38.339163 0.00000 0.1955 0.1956 38.473 0.0000

GARCH

(1,1)

38.289641 0.00000 0.1953 0.1954 38.423 0.0000

GARCH-M

(1,1)

35.99811 0.00000 0.1894 0.1895 36.124 0.0000

EGARCH

(1,1)

38.484227 0.00000 0.1958 0.1959 38.618 0.0000

EGARCH-M

(1,1)

26.88057 0.00000 0.1637 0.1637 26.976 0.0000

GJRGARCH

(1,1)

38.419713 0.00000 0.1957 0.1958 38.554 0.0000

GJRGARCH

-M(1,1)

26.510063 0.00000 0.1625 0.1626 26.603 0.0000

43 | P a g e

Table 11.3: The first postestimation of ARCH effect and Autocorrelation for real

estate

Source: The estimation of authors

Tickers Lagrange Multiplier

test

Autocorrelation test

Chi-

squared

distribution

statistic

P-value AC PAC Q P-value

ASM

ARCH(2) 41.759259 0.00000 0.1986 0.1987 41.885 0.0000

GARCH

(1,1)

42.119993 0.00000 0.1995 0.1995 42.248 0.0000

GARCH-M

(1,1)

45.238885 0.00000 0.2067 0.2068 45.377 0.0000

EGARCH

(1,1)

41.673309 0.00000 0.1984 0.1985 41.799 0.0000

EGARCH-M

(1,1)

46.361165 0.00000 0.2093 0.2093 46.503 0.0000

GJRGARCH

(1,1)

41.934257 0.00000 0.1990 0.1991 42.061 0.0000

GJRGARCH

-M(1,1)

45.869302 0.00000 0.2081 0.2082 46.009 0.0000

BCI

ARCH(3) 54.515267 0.00000 0.1971 0.1375 131.53 0.0000

GARCH

(1,1)

54.714153 0.00000 0.2294 0.2295 54.681 0.0000

GARCH-M

(1,1)

56.099385 0.00000 0.2323 0.2324 56.062 0.0000

EGARCH

(1,1)

54.668005 0.00000 0.2293 0.2294 54.631 0.0000

EGARCH-M

(1,1)

57.466926 0.00000 0.2351 0.2352 57.425 0.0000

GJRGARCH

(1,1)

54.727109 0.00000 0.2294 0.2295 54.695 0.0000

GJRGARCH

-M(1,1)

56.386576 0.00000 0.2329 0.2330 56.352 0.0000

44 | P a g e

Table 11.4: The first postestimation of ARCH effect and Autocorrelation for real

estate

Source: The estimation of authors

Tickers Lagrange Multiplier

test

Autocorrelation test

Chi-

squared

distribution

statistic

P-value AC PAC Q P-value

CCL

ARCH(2) 62.108926 0.00000 0.1691 0.1171 92.431 0.0000

GARCH

(1,1)

61.923385 0.00000 0.2428 0.1172 92.227 0.0000

GARCH-M

(1,1)

62.226053 0.00000 0.2434 0.2436 62.397 0.0000

EGARCH

(1,1)

61.843787 0.00000 0.2427 0.2428 62.013 0.0000

EGARCH-M

(1,1)

61.821969 0.00000 0.2426 0.2428 61.991 0.0000

GJRGARCH

(1,1)

61.919838 0.00000 0.2428 0.2430 62.090 0.0000

GJRGARCH

-M(1,1)

62.226281 0.00000 0.2434 0.2436 62.397 0.0000

CLG

ARCH(3) 113.10917 0.00000 0.2335 0.1264 240.09 0.0000

GARCH

(1,1)

113.89439 0.00000 0.3288 0.3290 114.27 0.0000

GARCH-M

(1,1)

108.32648 0.00000 0.3207 0.3208 108.68 0.0000

EGARCH

(1,1)

113.32106 0.00000 0.3280 0.3281 113.69 0.0000

EGARCH-M

(1,1)

106.52929 0.00000 0.3180 0.3181 106.88 0.0000

GJRGARCH

(1,1)

113.61636 0.00000 0.3284 0.3286 113.99 0.0000

GJRGARCH

-M(1,1)

107.15899 0.00000 0.3189 0.3191 107.51 0.0000

45 | P a g e

Table 11.5: The first postestimation of ARCH effect and Autocorrelation for real

estate

Source: The estimation of authors

Tickers Lagrange Multiplier

test

Autocorrelation test

Chi-

squared

distribution

statistic

P-value AC PAC Q P-value

D2D