update of stats sa building statistics aug 2012 data dr johan snyman medium-term forecasting...

TRANSCRIPT

Update of Stats SA Building Statistics

AUG 2012 Data

Dr Johan Snyman

Medium-Term Forecasting Associates

STELLENBOSCH

21 October 2012

MEDIUM-TERM FORECASTING ASSOCIATESBuilding Economists Tel: (021) 881-3887 PO Box 7119 Fax: (021) 881-3887STELLENBOSCH, 7599 E-mail: [email protected]

Vehicle sales show a V-shaped recovery, with a U-shaped revival in the case of residential buildings. In the case of BPP, Aug 2012 data were a little better than July 2012 figures. Since end-2009, BPP Res data are moving virtually sideways within a fairly narrow band

COMPARISON TOTAL VEHICLE SALES & TOTAL REAL RESIDENTIAL PLANS PASSED INDEX 1970 = 100

0

50

100

150

200

250

300

350

| 71 | 74 | 77 | 80 | 83 | 86 | 89 | 92 | 95 | 98 | 01 | 04 | 07 | 10 | 13

Source: NAAMSA; Stats SA; SARB; MFA DATABASE

IND

EX

19

70

= 1

00

TOTAL VEHICLE SALES TOTAL REAL RESIDENTIAL BPP

The trend in the cyclical movements correspond closely; vehicle sales in Sep 2012 were 12% higher than a year ago, with residential BPP -8% lower y-o-y in Aug 2012

TOTAL VEHICLE SALES & TOTAL REAL RESIDENTIAL PLANS PASSED ANNUAL PERCENTAGE CHANGE

-60

-40

-20

0

20

40

60

80

100

| 71 | 74 | 77 | 80 | 83 | 86 | 89 | 92 | 95 | 98 | 01 | 04 | 07 | 10 | 13

Source: NAAMSA; STATS SA; SARB, MFA DATABASE (Economic upswings shaded)

AN

NU

AL

PE

RC

EN

TA

GE

CH

AN

GE

TOTAL VEHICLE SALES TOTAL RESIDENTIAL BPP

Shaded areas represent theupswing phases of the business cycle

The year-on-year improvement in the annual percentage change of the number of houses (left-hand scale) is currently 3%, pointing to a modest revival, with interest rates at their lowest levels since 1973 (right-hand scale inverted). Observe the “mini-growth cycle” developing in houses, similar to the period 1999/2004

PRIME RATE COMPARED TO BPP NUMBER OF HOUSES (>80m²) BPP ANNUAL PERCENTAGE CHANGE

-60

-40

-20

0

20

40

60

80

| 81 | 84 | 87 | 90 | 93 | 96 | 99 | 02 | 05 | 08 | 11 |

Source: Stats SA; SARB; MFA DATABASE

BP

P H

OU

SE

S A

NN

UA

L P

ER

CE

NT

AG

E

CH

AN

GE

8

10

12

14

16

18

20

22

24

26

28

PR

IME

RA

TE

(INV

ER

TE

D)

BPP NO OF HOUSES PRIME RATE

Introduction of National Credit ActBanks' stricter lending criteria applied

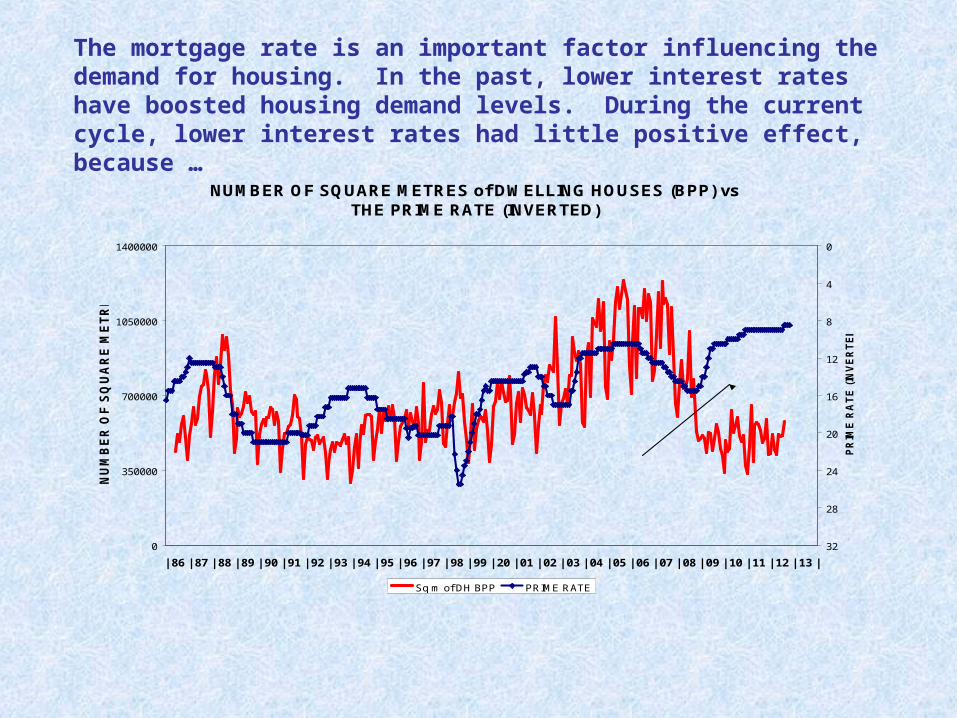

The mortgage rate is an important factor influencing the demand for housing. In the past, lower interest rates have boosted housing demand levels. During the current cycle, lower interest rates had little positive effect, because …

NUMBER OF SQUARE METRES of DWELLING HOUSES (BPP) vs THE PRIME RATE (INVERTED)

0

350000

700000

1050000

1400000

| 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

NU

MB

ER

OF

SQ

UA

RE

ME

TR

ES

0

4

8

12

16

20

24

28

32

PR

IME

RA

TE

(IN

VE

RT

ED

)

Sq m of DH BPP PRIME RATE

This unusual gap reflects poor housing demand

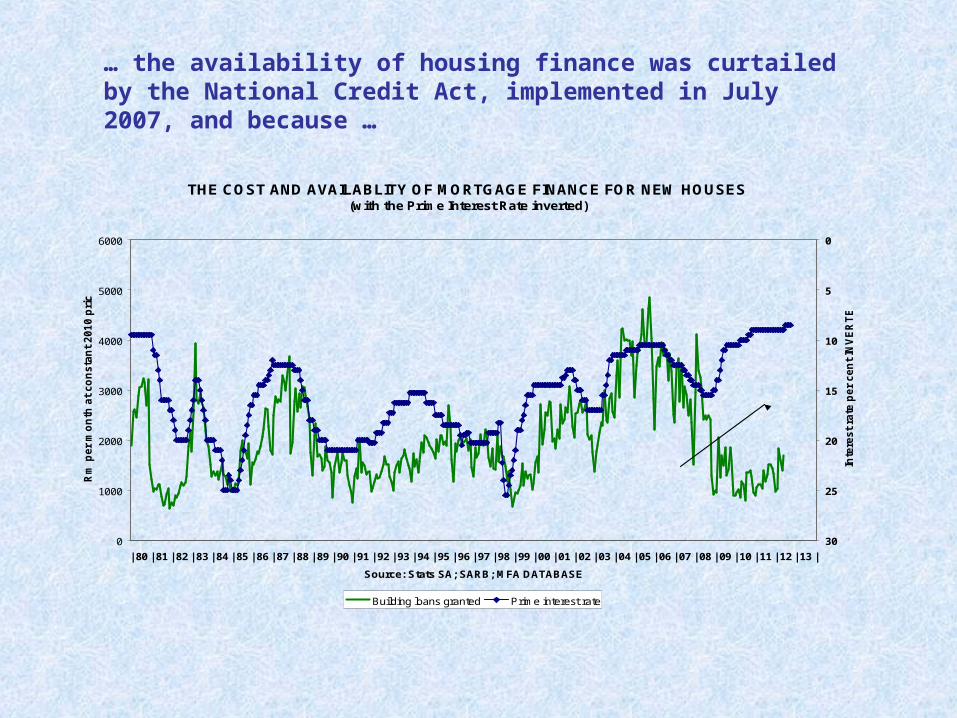

… the availability of housing finance was curtailed by the National Credit Act, implemented in July 2007, and because …

THE COST AND AVAILABLITY OF MORTGAGE FINANCE FOR NEW HOUSES(with the Prime Interest Rate inverted)

0

1000

2000

3000

4000

5000

6000

| 80 | 81 | 82 | 83 | 84 | 85 | 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 00 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: Stats SA; SARB; MFA DATABASE

Rm

per

mo

nth

at

co

ns

tan

t 2

01

0 p

rice

s

0

5

10

15

20

25

30

Inte

rest

rate

pe

r c

en

t IN

VE

RT

ED

Building loans granted Prime interest rate

THIS UNUSUAL GAP HAS WORSENED THE DOWNTURN IN HOMEBUILDING

… the banks applied stricter credit lending criteria during the global recession. They currently view their lending criteria as slightly “stricter” than “normal” given the prevailing monetary environment. One can conclude that they are being more cautious in the prevailing uncertain economic conditions.

BANKS' LENDING CRITERIA Percentage of respondents

30

40

50

60

70

80

90

100

| 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: BER; Ernst & Young; MFA DATABASE (Economic upswings shaded)

VE

RY

EA

SY

< E

AS

IER

<

> S

TR

ICT

ER

>

VE

RY

ST

RIC

T

Global FinancialCrisis

National Credit ActIntroduced

STRICT

EASY EASY

VERYSTRICT

NORMAL

In terms of (smoothed) numbers, private house plans in Aug 2012 were about 3% (y-o-y) better than in Aug 2011

BPP & BC: NUMBER of DWELLING HOUSES LARGER THAN 80m² 3 MONTH MOVING AVERAGE

0

1000

2000

3000

4000

5000

| 80 | 81 | 82 | 83 | 84 | 85 | 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 00 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: Stats SA; MFA DATABASE

NU

MB

ER

OF

DW

EL

LIN

G H

OU

SE

S

BPP BC

Historical Peak4502

Lowest Point1000

LONG TERM MONTHLYAVERAGE2100 housesapproved

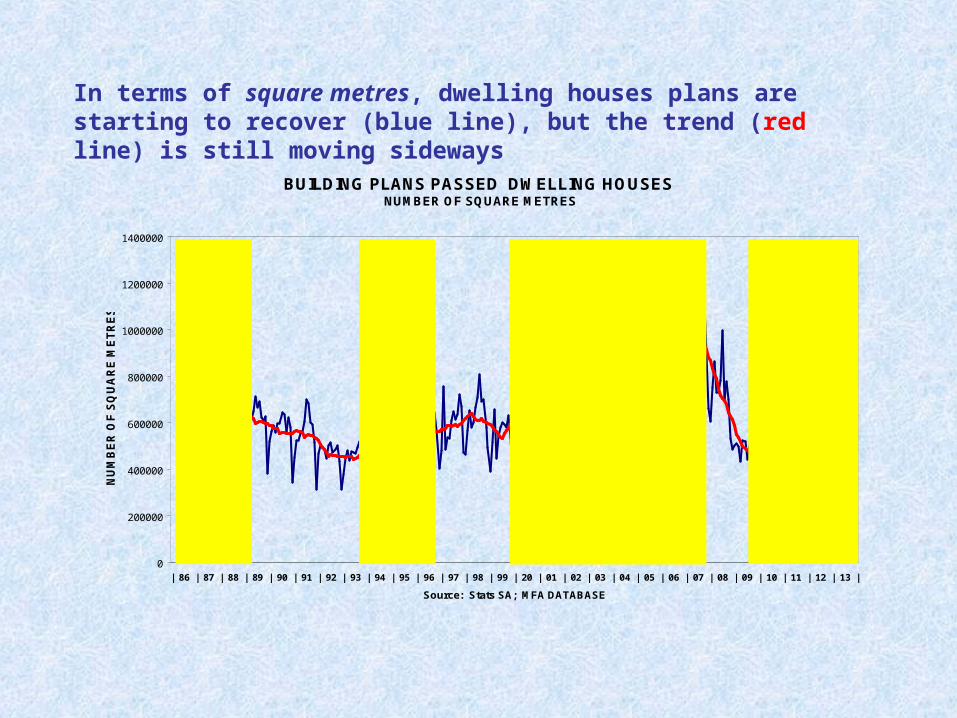

In terms of square metres, dwelling houses plans are starting to recover (blue line), but the trend (red line) is still moving sideways

BUILDING PLANS PASSED DWELLING HOUSES NUMBER OF SQUARE METRES

0

200000

400000

600000

800000

1000000

1200000

1400000

| 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: Stats SA; MFA DATABASE

NU

MB

ER

OF

SQ

UA

RE

ME

TR

ES

`

Data of townhouses and flats were 11.5% lower in Aug 2012 than in Aug 2011. As is the case with dwelling houses, a prolonged sideways movement at a low level is evident

BUILDING PLANS PASSED TOWNHOUSES AND FLATS NUMBER OF SQUARE METRES

0

100000

200000

300000

400000

500000

600000

700000

800000

| 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: Stats SA; MFA DATABASE

NU

MB

ER

OF

SQ

UA

RE

ME

TR

ES

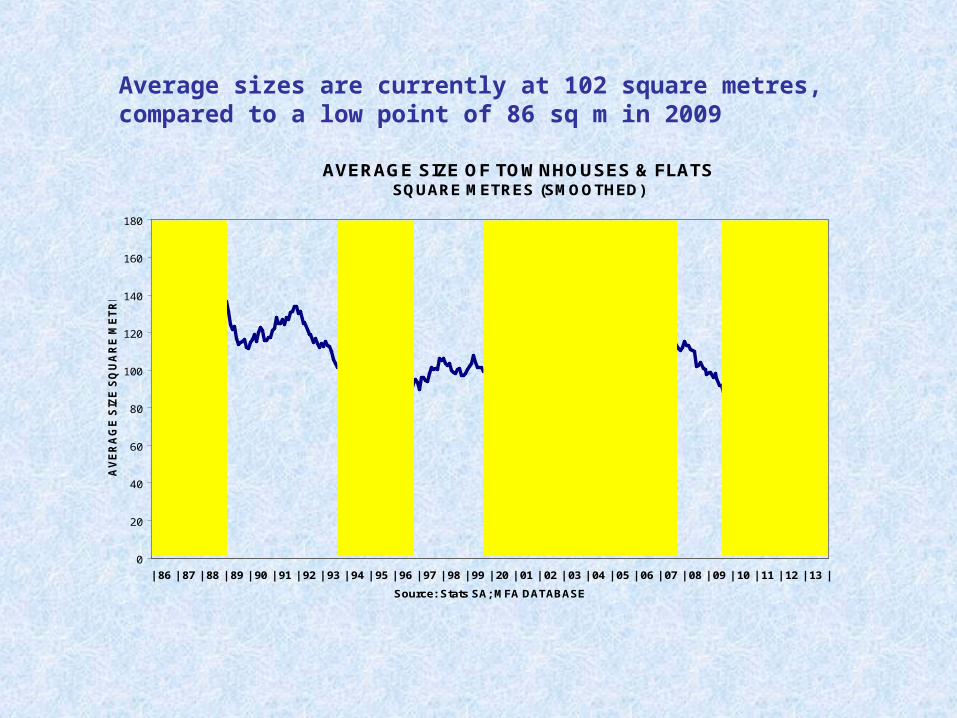

Average sizes are currently at 102 square metres, compared to a low point of 86 sq m in 2009

AVERAGE SIZE OF TOWNHOUSES & FLATS SQUARE METRES (SMOOTHED)

0

20

40

60

80

100

120

140

160

180

| 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: Stats SA; MFA DATABASE

AV

ER

AG

E S

IZE

SQ

UA

RE

ME

TR

ES

CURRENTLY RISING FROM A LOW POINT of 86 to 95 SQUARE METRES

The building cost of townhouses and flats is currently at R559 000 per unit

AVERAGE BUILDING COST OF TOWNHOUSES & FLATS RAND (DATA SMOOTHED)

0

100000

200000

300000

400000

500000

600000

| 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: Stats SA; MFA DATABASE

CO

ST

IN R

AN

D

CURRENTLY ABOUT R559 000 PER UNIT(on average)

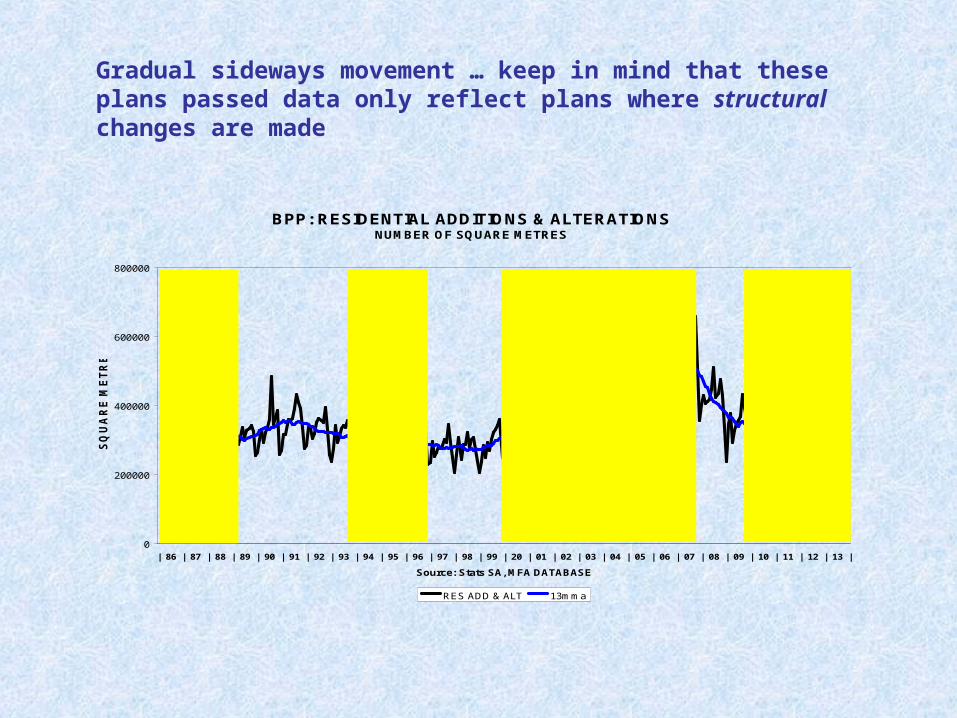

Gradual sideways movement … keep in mind that these plans passed data only reflect plans where structural changes are made

BPP: RESIDENTIAL ADDITIONS & ALTERATIONS NUMBER OF SQUARE METRES

0

200000

400000

600000

800000

| 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: Stats SA, MFA DATABASE

SQ

UA

RE

ME

TR

ES

RES ADD & ALT 13mma

It seems as if the lower turning point in offices was recorded late in 2010. Smoothed Aug 2012 data are 28.3% higher than Aug 2011 figures

OFFICES BUILDING PLANS PASSED: SQUARE METRES

0

40000

80000

120000

160000

200000

| 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: Stats SA; MFA DATABASE

SQ

UA

RE

ME

TR

ES

Office vacancy levels (vacancies line inverted) remain high at about 10.5% of available space

OFFICE VACANCIES & BUILDING PLANS PASSED OFFICES

0

50000

100000

150000

200000

| 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: SARB; Stats SA; RODE DATABASE; SAPOA; MFA DATABASE

BP

P S

QU

AR

E M

ET

RE

S (

3 M

MA

)

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

% N

AT

ION

AL

OF

FIC

E V

AC

AN

CIE

S

(IN

VE

RT

ED

)

BPP OFFICES VACANCIES

BPP

VACANCIESINVERTED(RIGHT HANDSCALE)

Since the low point recorded in April 2011, an improvement is evident. Aug 2012 figures are 4.5% higher than Aug 2011 data

SHOPPING SPACE BUILDING PLANS PASSED: SQUARE METRES

0

40000

80000

120000

160000

200000

240000

| 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: Stats SA; MFA DATABASE

SQ

UA

RE

ME

TR

ES

The smoothed data for industrial buildings in Aug 2012 are 17.7% than Aug 2011 figures

INDUSTRIAL & WAREHOUSING BUILDING PLANS PASSED: SQUARE METRES

0

50000

100000

150000

200000

250000

300000

| 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: Stats SA; MFA DATABASE

SQ

UA

RE

ME

TR

ES

Industrial vacancies remain relatively high (vacancies line inverted, right-hand scale), but dropped somewhat during recent months

INDUSTRIAL VACANCIES & INDUSTRIAL BUILDING PLANS PASSED

0

50000

100000

150000

200000

250000

300000

| 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: RODE; STATS SA; SARB; MFA DATABASE

IND

US

TR

IAL

BB

P S

QU

AR

E M

ET

RE

S (

3m

ma

)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

HIG

HE

R

<

VA

CA

NC

Y R

AT

E

>

LO

WE

R

(IN

VE

RT

ED

)

INDUSTRIAL BPP INDUSTRIAL VACANCIES

VACANCIES INVERTEDRIGHT HAND SCALE

BPP

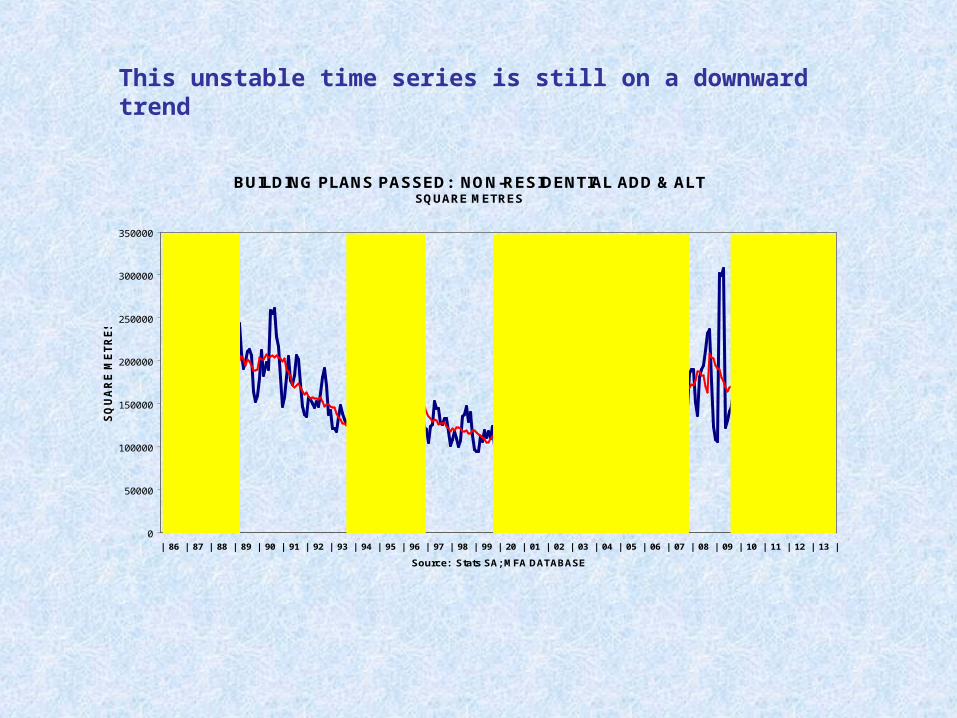

This unstable time series is still on a downward trend

BUILDING PLANS PASSED: NON-RESIDENTIAL ADD & ALT SQUARE METRES

0

50000

100000

150000

200000

250000

300000

350000

| 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: Stats SA; MFA DATABASE

SQ

UA

RE

ME

TR

ES

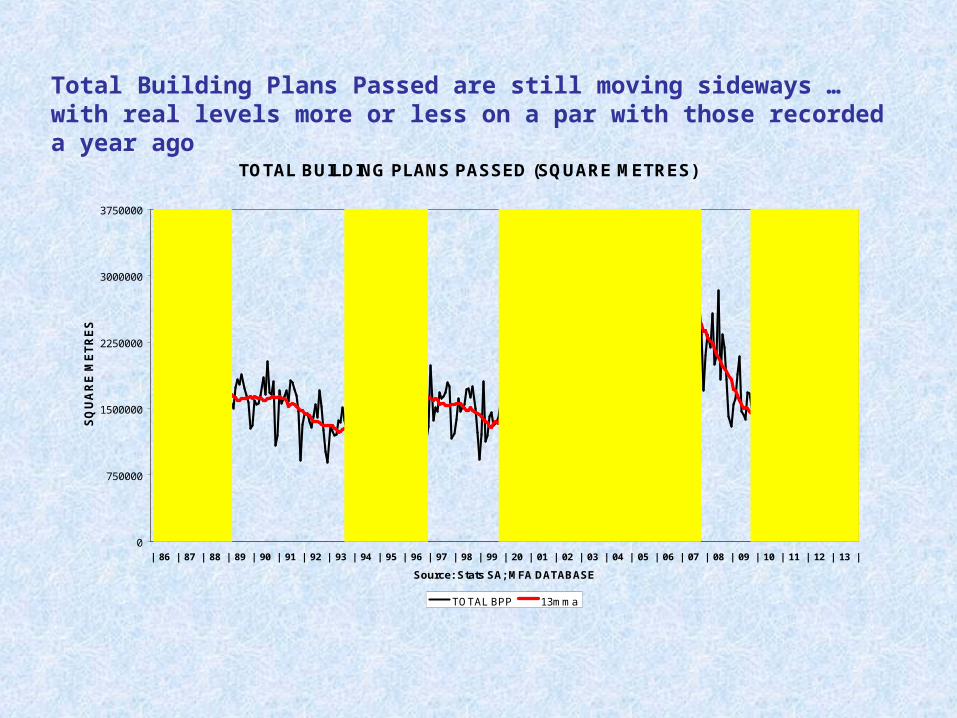

Total Building Plans Passed are still moving sideways … with real levels more or less on a par with those recorded a year ago

TOTAL BUILDING PLANS PASSED (SQUARE METRES)

0

750000

1500000

2250000

3000000

3750000

| 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: Stats SA; MFA DATABASE

SQ

UA

RE

ME

TR

ES

TOTAL BPP 13mma

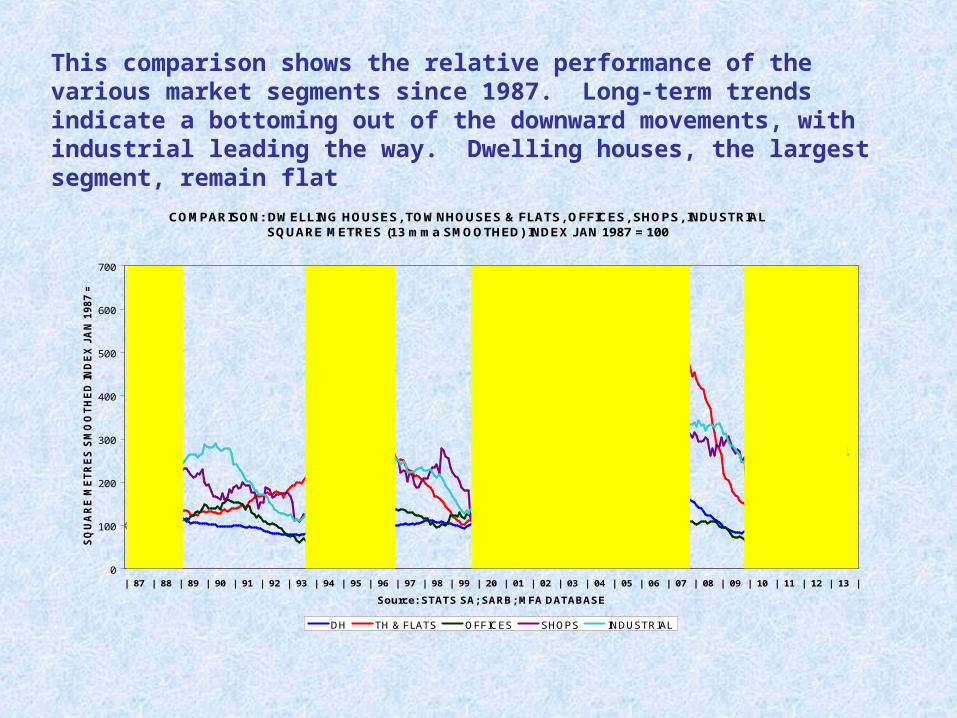

This comparison shows the relative performance of the various market segments since 1987. Long-term trends indicate a bottoming out of the downward movements, with industrial leading the way. Dwelling houses, the largest segment, remain flat

COMPARISON: DWELLING HOUSES, TOWNHOUSES & FLATS, OFFICES, SHOPS, INDUSTRIAL SQUARE METRES (13 mma SMOOTHED) INDEX JAN 1987 = 100

0

100

200

300

400

500

600

700

| 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: STATS SA; SARB; MFA DATABASE

SQ

UA

RE

ME

TR

ES

SM

OO

TH

ED

IN

DE

X J

AN

19

87

= 1

00

DH TH & FLATS OFFICES SHOPS INDUSTRIAL

Offices

Houses

Shops

Industrial

Townhouses& Flats

BUILDING PLANSPASSED

This comparison of long term trends shows the lagged pattern. Against expectations, the traditional long-term pattern is no longer evident, i.e. non-res seems to be leading during the current cycle. Res has lingered for much longer (2007-2012) in the downswing phase than before

COMPARISON TO ILLUSTRATE THE LAG BETWEEN RESIDENTIAL & NON-RESIDENTIAL BUILDING PLANS PASSED. INDEX Jan 1987 = 100

0

50

100

150

200

250

| 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 | 13 |

Source: Stats SA; SARB; MFA DATABASE

IND

EX

Ja

n 1

98

7 =

10

0

RESIDENTIAL BPP NON-RESIDENTIAL

33 MONTH LAG

18 MONTH LAG

26 MONTH LAG

30 MONTH LAG

IN THE PAST , NON-RESIDENTIAL LAGGED RESIDENTIAL BY 27 MONTHS, ON AVERAGE, OR BY JUST MORE THAN 2 YEARS

BC is showing the normal lagged pattern

BPP AND BC: TOTAL RESIDENTIALAT CONSTANT 2010 PRICES

0

1

2

3

4

5

6

| 70 | 71 | 72 | 73 | 74 | 75 | 76 | 77 | 78 | 79 | 80 | 81 | 82 | 83 | 84 | 85 | 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 20 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 |

Source: STATS SA; SARB; MFA DATABASE

RA

ND

BIL

LIO

N P

ER

MO

NT

H

BPP TOTAL RES BC TOTAL RES

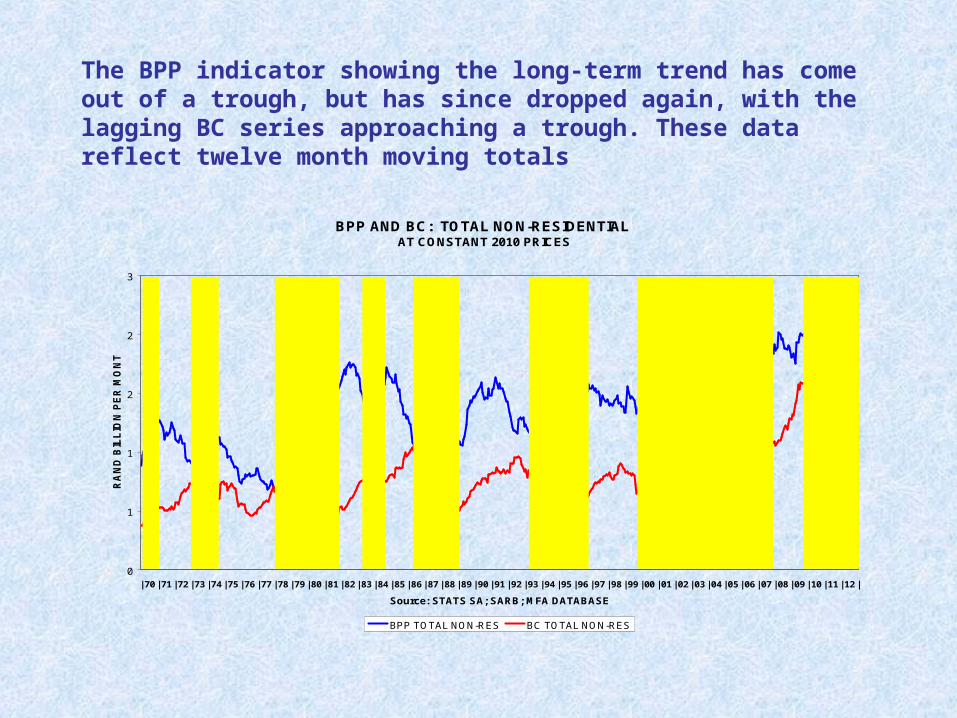

The BPP indicator showing the long-term trend has come out of a trough, but has since dropped again, with the lagging BC series approaching a trough. These data reflect twelve month moving totals

BPP AND BC: TOTAL NON-RESIDENTIAL AT CONSTANT 2010 PRICES

0

1

1

2

2

3

| 70 | 71 | 72 | 73 | 74 | 75 | 76 | 77 | 78 | 79 | 80 | 81 | 82 | 83 | 84 | 85 | 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 00 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 |

Source: STATS SA; SARB; MFA DATABASE

RA

ND

BIL

LIO

N P

ER

MO

NT

H

BPP TOTAL NON-RES BC TOTAL NON-RES

Both indicators are still reflecting a downward trend

BPP AND BC: TOTAL ADDITIONS AND ALTERATIONS AT CONSTANT 2010 PRICES

0

1

1

2

2

3

3

| 70 | 71 | 72 | 73 | 74 | 75 | 76 | 77 | 78 | 79 | 80 | 81 | 82 | 83 | 84 | 85 | 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 00 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 |

Source: STATS SA; SARB; MFA DATABASE

RA

ND

BIL

LIO

N P

ER

MO

NT

H

BPP TOTAL ADD & ALT BC TOTAL ADD & ALT

Total BPP seems to be forming a trough, i.e. the movement is sideways, but for the lagging BC series there could be more downside potential …

TOTAL BUILDING PLANS PASSED AND BUILDINGS COMPLETED AT CONSTANT 2010 PRICES

0

2

4

6

8

10

12

| 70 | 71 | 72 | 73 | 74 | 75 | 76 | 77 | 78 | 79 | 80 | 81 | 82 | 83 | 84 | 85 | 86 | 87 | 88 | 89 | 90 | 91 | 92 | 93 | 94 | 95 | 96 | 97 | 98 | 99 | 00 | 01 | 02 | 03 | 04 | 05 | 06 | 07 | 08 | 09 | 10 | 11 | 12 |

Source: STATS SA; SARB; MFA DATABASE

RA

ND

BIL

LIO

N P

ER

MO

NT

H

BPP TOTAL BC TOTAL