commodity market monitor...april 07, 2020 wheat/urad/chilli/sugar commodity market monitor weekly...

TRANSCRIPT

April 07, 2020

WHEAT/URAD/CHILLI/SUGAR

Commodity Market

Monitor

Weekly Online

https://forms.gle/2J

gFGowMre4fxDwSA

Quizhttps://forms.g

le/LJdTxzEURqqTZA

6U9

Click on the link above to participate Participate in our weekly quiz and get a chance to win Amazon gift coupons. Winners will

be announced in next report and rewarded.

All India Weather Status

Last week all India Rainfall status: 26th

March 2020 to 01st

April 2020.

Odisha, Telangana and Uttar Pradesh states received the deficit rainfall

Uttarakhand state received the excess rainfall

Andhra Pradesh, Arunachal Pradesh, Assam, Karnataka, Kerala, Meghalaya, Nagaland, Sikkim, Tamil Nadu, Tripura and

West Bengal states received the large deficit rainfall

Gujarat, Haryana, Himachal Pradesh, Jammu & Kashmir, Madhya Pradesh, Maharashtra, Punjab and Rajasthan states

received the large excess rainfall

Chhattisgarh state received the normal rainfall

No rainfall has observed in Bihar, Goa, Jharkhand, Manipur and Mizoram state.

During the week, rainfall was below Long Period Average (LPA) by 44% over the country as a whole.

Seasonal all India Rainfall status: 1st

March 2020 to 01st

April 2020.

Meghalaya state received the deficit rainfall

Andhra Pradesh, Himachal Pradesh, Jammu & Kashmir, Kerala and Telangana states received the excess rainfall

Arunachal Pradesh, Assam, Manipur, Mizoram, Nagaland, Tamil Nadu and Tripura states received the large deficit rainfall

Bihar, Chhattisgarh, Gujarat, Haryana, Jharkhand, Madhya Pradesh, Maharashtra, Odisha, Punjab, Rajasthan, Uttar Pradesh, Uttarakhand and West Bengal states received the large excess rainfall

Karnataka and Sikkim states received the normal rainfall

No rainfall has observed only in Goa state. For the country as a whole, cumulative rainfall during 1

stMarch 2020 to 01

stApril 2020 was above Long Period

Average (LPA) by 46% over the country as a whole.

Weather Forecast:

Thunderstorm accompanied with lightning & squall (speed reached 30-40 kmph) likely at isolated places over west Rajasthan and (speed

reaching 50-60 kmph) likely at isolated places over Assam & Meghalaya and Nagaland, Manipur, Mizoram & Tripura.

Gradual rise in maximum temperature by (2-3°C) over Telangana, Rayalaseema, North Interior Karnataka and Vidarbha during next 2-3 days.

Fairly widespread to widespread rain/thundershowers likely over Northeaster States.

Isolated to scattered rain/thundershowers likely over Western Himalayan Region, north-eastern States, Kerala, Tamilnadu during this week.

Weather is likely to be dry over rest of the country.

All India Reservoir Status: as on 02nd

April 2020.

Central Water Commission is monitoring live storage status of 123 reservoirs of the country on weekly basis and is issuing weekly bulletin on every Thursday. The total live storage capacity of these 123 reservoirs is 171.090 BCM which is about 66.36% of the live storage capacity of 257.812 BCM which is estimated to have been created in the country. As per reservoir storage bulletin dated 02.04.2020, live storage available in these reservoirs is 84.767 BCM, which is 50% of total live storage capacity of these reservoirs. However, last year the live storage available in these reservoirs for the corresponding period was 52.065 BCM and the average of last 10 years live storage was 52.629 BCM. Thus, the live storage available in 123 reservoirs as per 02.04.2020 Bulletin

Source: IMD, DAC&FW and CWC

-40

-20

0

20

40

60

80

100

120

140

160

% of Departure From Normal Reservoir Storage (02nd April, 2020)

Current Crop Scenario

Corn

Acreage of Corn in the current week is 16.98 lakh hectares. While, 14.78 lakh hectares area was reported in

corresponding week of 2019.Crop is 90 to 145 days old and is in milking to maturity stage. While, harvesting is

under progress in early sown crop. Rainfall received during winter season was beneficial for the crop in entire

major growing states. Due to infestation of sucking pest (stem borer and fall army worm) crop has been

adversely affected in certain pockets of Andhra Pradesh, Bihar and Telangana state. Overall in rest of areas

crop condition is normal. Acreage of Corn in the current week is higher than corresponding week of 2019. Key

Corn producing states are Bihar, Maharashtra, Andhra Pradesh, Telangana and Karnataka. Acreage of Corn in

the current week is higher than corresponding week of 2019. Key Corn producing States are Bihar,

Maharashtra, Andhra Pradesh, Telangana and Karnataka.

Gram

Acreage: Acreage of Gram in the current week is 107.21 lakh hectares. While, 96.19 lakh hectares

area was reported in corresponding week of 2019.Crop harvesting has almost completed.

Rainfall received during winter season was beneficial for crop growth. However, crop has been

adversely affected due to rainfall and hailstorms received during month of Mar-20 in certain

districts of Rajasthan, Uttar Pradesh and Madhya Pradesh where crop is in harvesting stage and

laid on the field for drying after harvest. Further, crop harvesting has been delayed due to rains.

Incidence of sucking pest has been observed in the field and same is control using pesticides.

Overall in reaming areas crop condition is normal and yield is expected to be normal. Acreage of

Gram in the current season is significantly higher than 2018.

Lentil

Acreage of Lentil in the current week is 16.07 lakh hectares. While, 16.91 lakh hectares area was

reported in corresponding week of 2019.

Crop harvesting is under progress. Favourable climatic conditions were beneficial for crop growth.

However, crop has been adversely affected due to rainfall and hailstorms received during 1st

fortnight of Mar-20 in certain pockets of Rajasthan, Uttar Pradesh and Madhya Pradesh. Further,

crop harvesting has been delayed due to rainfall. Incidence of sucking pest and disease has been

reported by the field and same is below economic threshold level. Overall crop condition is normal

and yields are expected to be normal.

Acreage in the current season is almost similar to 2018.

Mustard

Acreage of Mustard in the current week is 69.51 lakh hectares. While, 69.76 lakh hectares area was

reported in corresponding week of 2019.Crop harvesting has almost completed. Crop has been

adversely affected due to rainfall and hailstorms received during 4th week of Feb-20 and 1st fortnight of

Mar-20 in certain districts of Rajasthan, Haryana, Uttar Pradesh and Madhya Pradesh where crop is in

maturity to harvesting stage or laid on the field for drying after harvest. Crop harvesting delayed further

due to rains. Overall in remaining areas crop condition is normal and yields are expected to be normal.

Acreage of Mustard in the current season is almost similar to 2018.

Wheat

Acreage of Wheat in the current week is 336.18 lakh hectares. While, 299.30 lakh hectares area was

reported in corresponding week of 2019.Crop harvesting has been initiated in early sown crop.

While, major sown areas crop is 110 to 125 days old and is in grain maturity to ready to harvesting

stage. Rainfall received during winter season was beneficial for the crop. Due to favourable climatic

conditions good harvests of Wheat has been expected. However, crop has been adversely affected

due to hailstorm and rainfall with wind received during 1st fortnight of Mar-20 in certain districts of

Rajasthan, Haryana, Uttar Pradesh, Punjab and Himachal Pradesh, Chhattisgarh, Bihar and Madhya

Pradesh. Further, crop maturity has been delayed due to prolong winter. Overall in remaining areas

crop condition is normal and yield are expected to be normal. Acreage of Wheat in the current

season is higher than 2018.

Most of the spot markets in the country are closed due to lockdown. Wheat prices have remained low tracking subdued trading activities and quoted in the range of Rs 1600 to Rs 2400 per quintal.

Haryana government has delayed wheat and mustard procurement this year, keeping in view the countrywide lockdown aimed to halt the spread of coronavirus. Officials admit that the wheat procurement, which will take place from April 20, will be a tough task for the government machinery because of the huge quantity that will arrive in the state mandis. The crop is good this year in spite of untimely rainfall and hailstorm and has estimated wheat production of 120 lakh MT.

The Punjab government has decided to stagger its wheat procurement, which was scheduled to start Apr 15, to avert huge turnouts that may fuel spread of COVID-19. The state may also incentivise farmers for bringing their produce over a longer period.

Punjab has proposed to give an incentive of 100 rupees per 100 kg over the minimum support price of Rs 1,925 per 100 kg to farmers for bringing their crop in May and an incentive of 200 rupees per 100 kg over the support price if they bring it in June. This year Punjab has pegged its wheat output at 17.9 million tonne about 2 per cent lower than last year. The state is usually the largest contributor to the centre's wheat pool.

As per the 02nd advance estimates for 2019-20 crops, Wheat production is estimated to increase at a record 106.21 million tonnes, higher by 2.61 million tonnes as compared to wheat production during 2018-19.

As per market sources, wheat stock in central pool as on 1st March 2020 stood at 275.21 lakh tonnes. This quantity is higher by around 36.86 per cent compared to last year for the same month. Government has already applied import duty on wheat to curb imports and provide support to domestic prices. Therefore, government has abundant supplies this year.

The International Grains Council (IGC) forecasts a record global grains crop of 2.22 billion tonnes in 2020-21, up 2 per cent from last year. The council pegged global wheat production at 768 MMT, up from this year’s 764 MMT. Global domestic consumption in 2020-21 is estimated at 760 MMT, up from this year’s 754 MMT.

Fundamental Analysis- WHEAT

Mandi Price in Rs/ Quintal

Location 4/6/2020 3/30/2020 %

Change

Indore Closed Closed N/A

Jaipur Closed Closed N/A

Hanumangarh Closed Closed N/A

FUNDAMENTAL SUMMARY

Price Drivers Impact

Lockdown in many States due to coronavirus

Bearish

Expectation of higher production in Haryana

Bearish

Availability of higher stocks with Government agencies

Bearish

All-India Wheat production estimated at a record 106.21 million tonnes

Bearish

IGC forecasted higher global wheat production at 768 million tonnes

Bearish

Based on Primary & Secondary Sources

0.00

500.00

1000.00

1500.00

2000.00

2500.00

07

/06

/20

04

07

/06

/20

05

07

/06

/20

06

07

/06

/20

07

07

/06

/20

08

07

/06

/20

09

07

/06

/20

10

07

/06

/20

11

07

/06

/20

12

07

/06

/20

13

07

/06

/20

14

07

/06

/20

15

07

/06

/20

16

07

/06

/20

17

07

/06

/20

18

07

/06

/20

19

Wheat

Fundamental Analysis- URAD

3,500.00

4,500.00

5,500.00

6,500.00

7,500.00

8,500.00

9,500.00

Urad_Mumbai

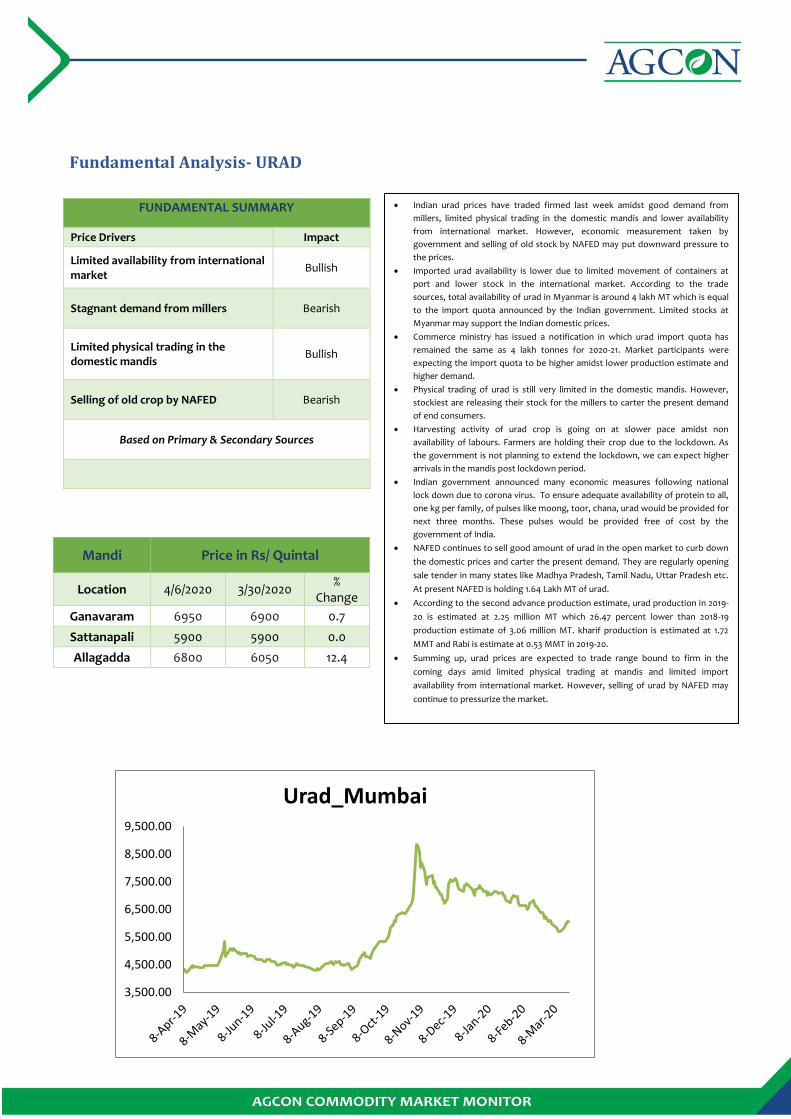

Indian urad prices have traded firmed last week amidst good demand from

millers, limited physical trading in the domestic mandis and lower availability

from international market. However, economic measurement taken by

government and selling of old stock by NAFED may put downward pressure to

the prices.

Imported urad availability is lower due to limited movement of containers at

port and lower stock in the international market. According to the trade

sources, total availability of urad in Myanmar is around 4 lakh MT which is equal

to the import quota announced by the Indian government. Limited stocks at

Myanmar may support the Indian domestic prices.

Commerce ministry has issued a notification in which urad import quota has

remained the same as 4 lakh tonnes for 2020-21. Market participants were

expecting the import quota to be higher amidst lower production estimate and

higher demand.

Physical trading of urad is still very limited in the domestic mandis. However,

stockiest are releasing their stock for the millers to carter the present demand

of end consumers.

Harvesting activity of urad crop is going on at slower pace amidst non

availability of labours. Farmers are holding their crop due to the lockdown. As

the government is not planning to extend the lockdown, we can expect higher

arrivals in the mandis post lockdown period.

Indian government announced many economic measures following national

lock down due to corona virus. To ensure adequate availability of protein to all,

one kg per family, of pulses like moong, toor, chana, urad would be provided for

next three months. These pulses would be provided free of cost by the

government of India.

NAFED continues to sell good amount of urad in the open market to curb down

the domestic prices and carter the present demand. They are regularly opening

sale tender in many states like Madhya Pradesh, Tamil Nadu, Uttar Pradesh etc.

At present NAFED is holding 1.64 Lakh MT of urad.

According to the second advance production estimate, urad production in 2019-

20 is estimated at 2.25 million MT which 26.47 percent lower than 2018-19

production estimate of 3.06 million MT. kharif production is estimated at 1.72

MMT and Rabi is estimate at 0.53 MMT in 2019-20.

Summing up, urad prices are expected to trade range bound to firm in the

coming days amid limited physical trading at mandis and limited import

availability from international market. However, selling of urad by NAFED may

continue to pressurize the market.

Mandi Price in Rs/ Quintal

Location 4/6/2020 3/30/2020 %

Change

Ganavaram 6950 6900 0.7

Sattanapali 5900 5900 0.0

Allagadda 6800 6050 12.4

FUNDAMENTAL SUMMARY

Price Drivers Impact

Limited availability from international market

Bullish

Stagnant demand from millers Bearish

Limited physical trading in the domestic mandis

Bullish

Selling of old crop by NAFED Bearish

Based on Primary & Secondary Sources

Fundamental Analysis-CHILLI

10,000.00

15,000.00

20,000.00

25,000.00

30,000.00

35,000.00

Chilli_Banglore

Mandi Price in Rs/ Quintal

Location 4/6/2020 3/30/2020 %

Change

Nandyal 13000 13000 0.0

Kondepi 12500 12500 0.0

Chilakaluripet 10500 10500 0.0

Chilli market remain closed due to lockdown to check Coronavirus

spread.

In the mean while Andhra Pradesh farmers have requested to state

governments to allow transportation of harvested chilli to cold storage,

so that they can save their produce.

Farmers are also facing harvesting issues as labour availability has

reduced due to lockdown. In Telangana Khammam farmers are facing

issue to store the harvested crop in cold stores.

Chilli cold store stock has reached around 40 lakh bales in Guntur region.

Chilli area is reduced by 14.7% over last year in Andhra Pradesh. Yield is

expected to be better due to favourable weather conditions during crop

growth period and overall crop is expected to be better by 7% over last

year in AP. Similar condition is expected in Telangana where crop is

expected to be higher by 6%.

Excessive and untimely rainfall has resulted in losses in Karnataka &

Madhya Pradesh in range of 11% to 13%. But over-all production is

estimated higher by 3% over last year.

On supply and demand balance sheet the total supply is lower than last

year due to very tight opening stocks and current scenario is also not

leaving much carry forward stock for next year.

Farmers are also facing harvesting issues as labour availability is a

problem in lockdown. In Telangana Khammam farmers are facing issue to

store the harvested crop in cold stores.

Markets are closed till 15th April, as chilli balance sheet is tight so prices

are expected to remain strong even after opening of market, but delay in

harvesting may impact quality of crop.

FUNDAMENTAL SUMMARY

Price Drivers Impact

Increase in Arrival of new crop in Andhra Pradesh

Bearish

Lower opening stocks Bullish

Lower stocks of premium variety (Teja)

Bullish

Losses in Karnataka and MP due to incessant rains

Bullish

Coronavirus Pandemic leading to India lock down

Bearish

Increase in Arrival of new crop in Andhra Pradesh

Bearish

Fundamental Analysis- SUGAR

FUNDAMENTAL SUMMARY

Price Drivers Impact

Coronavirus lock down, impacting bulk demand

Bearish

Lower volume back to back trades for retail sale

Bullish

Lower sugar production YOY Neutral

Domestic sale quota of 18 lakh mt for Apr 2020

Bearish

Sugar Production higher than Consumption

Bearish

Lower than expected exports - Higher opening stocks for 2020-21

Bearish

Mandi Price in Rs/ Quintal

Location 4/6/2020 3/30/2020 %

Change

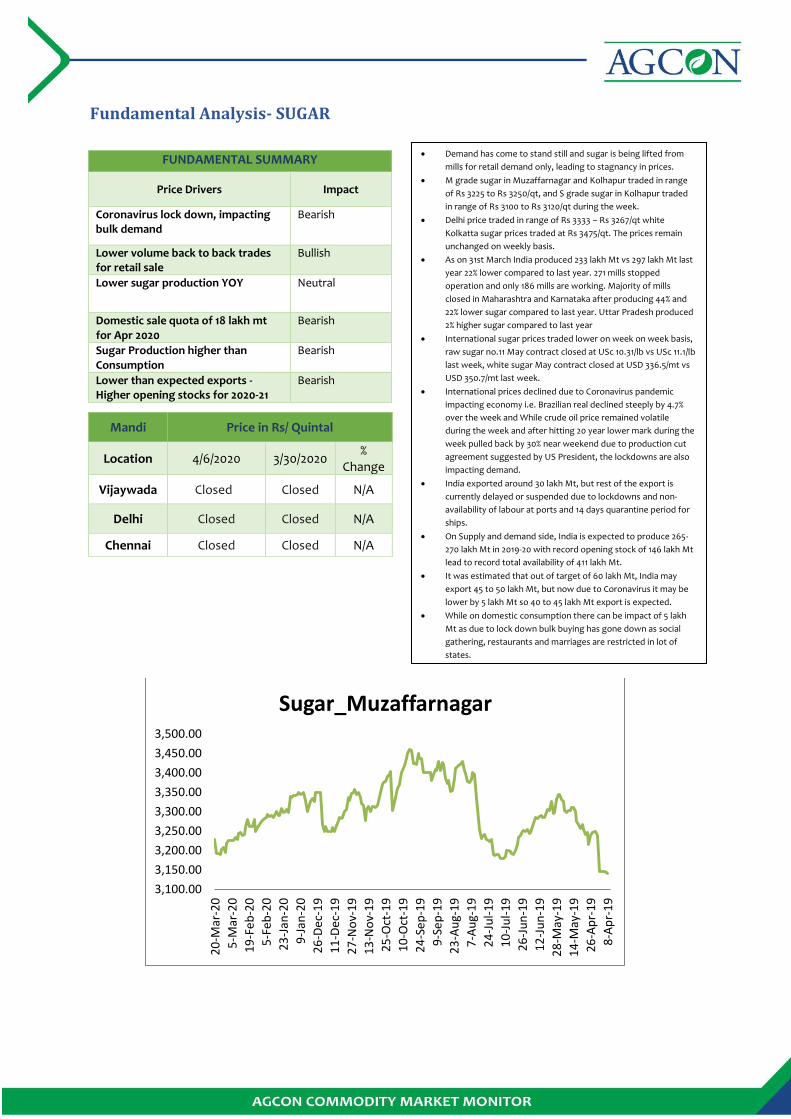

Vijaywada Closed Closed N/A

Delhi Closed Closed N/A

Chennai Closed Closed N/A

Demand has come to stand still and sugar is being lifted from

mills for retail demand only, leading to stagnancy in prices.

M grade sugar in Muzaffarnagar and Kolhapur traded in range

of Rs 3225 to Rs 3250/qt, and S grade sugar in Kolhapur traded

in range of Rs 3100 to Rs 3120/qt during the week.

Delhi price traded in range of Rs 3333 – Rs 3267/qt white

Kolkatta sugar prices traded at Rs 3475/qt. The prices remain

unchanged on weekly basis.

As on 31st March India produced 233 lakh Mt vs 297 lakh Mt last

year 22% lower compared to last year. 271 mills stopped

operation and only 186 mills are working. Majority of mills

closed in Maharashtra and Karnataka after producing 44% and

22% lower sugar compared to last year. Uttar Pradesh produced

2% higher sugar compared to last year

International sugar prices traded lower on week on week basis,

raw sugar no.11 May contract closed at USc 10.31/lb vs USc 11.1/lb

last week, white sugar May contract closed at USD 336.5/mt vs

USD 350.7/mt last week.

International prices declined due to Coronavirus pandemic

impacting economy i.e. Brazilian real declined steeply by 4.7%

over the week and While crude oil price remained volatile

during the week and after hitting 20 year lower mark during the

week pulled back by 30% near weekend due to production cut

agreement suggested by US President, the lockdowns are also

impacting demand.

India exported around 30 lakh Mt, but rest of the export is

currently delayed or suspended due to lockdowns and non-

availability of labour at ports and 14 days quarantine period for

ships.

On Supply and demand side, India is expected to produce 265-

270 lakh Mt in 2019-20 with record opening stock of 146 lakh Mt

lead to record total availability of 411 lakh Mt.

It was estimated that out of target of 60 lakh Mt, India may

export 45 to 50 lakh Mt, but now due to Coronavirus it may be

lower by 5 lakh Mt so 40 to 45 lakh Mt export is expected.

While on domestic consumption there can be impact of 5 lakh

Mt as due to lock down bulk buying has gone down as social

gathering, restaurants and marriages are restricted in lot of

states.

Overall India carry forward stock will increase and is

expected to close 2019-20 with a big closing stock of 115

to 120 lakh Mt.

Due to lockdown demand has taken a hit and offtake has

significantly reduced from mills, so we expect on short

term basis the prices will remain range bound for next 2-3

weeks as retail demand will remain there and trade

volume will remain low. S grade sugar may trade at Rs

3100 to Rs 3150/qt and M grade between Rs 3200 Rs

3250/qt. But on long term basis the fundamentals are

bearish.

3,100.00

3,150.00

3,200.00

3,250.00

3,300.00

3,350.00

3,400.00

3,450.00

3,500.00

20

-Mar

-20

5-M

ar-2

0

19

-Fe

b-2

0

5-F

eb

-20

23

-Jan

-20

9-J

an-2

0

26

-De

c-1

9

11

-De

c-1

9

27

-No

v-1

9

13

-No

v-1

9

25

-Oct

-19

10

-Oct

-19

24

-Se

p-1

9

9-S

ep

-19

23

-Au

g-1

9

7-A

ug-

19

24

-Ju

l-1

9

10

-Ju

l-1

9

26

-Ju

n-1

9

12

-Ju

n-1

9

28

-May

-19

14

-May

-19

26

-Ap

r-1

9

8-A

pr-

19

Sugar_Muzaffarnagar

Rice exporters in India seek European

pesticides norms Government tweaks guidelines to

ensure sugar exports meet the target

India to harvest record wheat

production of 106.21 MT in 2019-20:

Report

Govt pegs 7 per cent rise in onion

output this yr; sees production fall in

major fruits

NCML releases first estimate of rabi

crop, indicates record food grain

production

States asked to set up PSFs to combat

price volatility

To purchase the India

Commodity Year Book 2020,

contact us at

The Week That Was!

MINIMUM SUPPORT PRICE (Rs/Qtl.)

Commodity 2018-19 2019-20

KHARIF **NEW**

Paddy Common 1750 1815

paddy grade A 1770 1835

Jowar Hybrid 2430 2550

Jowar Maldandi 2450 2570

Bajra 1950 2000

Ragi 2897 3150

Maize 1700 1760

Tur/Arhar 5675 5800

Moong 6975 7050

Urad 5600 5700

Groundnut 4890 5090

Sunflower seed 5388 5650

Soybean Yellow 3399 3710

Sesame 6249 6485

Niger seed 5877 5940

Cotton (Medium Staple) 5150 5255

Cotton (Long Staple) 5450 5550

RABI**NEW**

Commodity 2018-19 2019-20

Wheat 1840 1925

Barley 1440 1525

Gram 4620 4875

Masoor (Lentil) 4475 4800

Rapeseed/Mustard 4200 4425

Safflower 4945 5215

*includes bonus of Rs 200 per quintal

# includes bonus of Rs 100 per quintal

Commodity Latest Fortnight

ago Month

ago Year ago

20 Mar-20 05 March

20 20-Feb 20 20 -Mar-19

Wheat 1875 1950 2140 1875

Chana 4070 4022 4032 4100

Rice/Paddy 2600 2600 2850 3450

Tur 4400 4150 4350 4300

Maize 1807 1856 2031 2087

Official Production Estimates

Second Advance Estimates 2019-20 & previous years’ estimates: Fourth advance estimates 2018-19 Link for commodity-wise and market-

wise prices and arrivals:

http://agmarknet.gov.in/PriceAndArrival

s/CommodityWiseDailyReport2.aspx

PRICE TRACKER

Crop & PHMF Division Progress area coverage under Rabi crops as on 31.01.2020

Area : In lakh hectare

Sl.no Crop Normal Rabi Area (DES)

Normal of corresponding

week

Area sown Difference of 2019-20 over

2019-20

2018-19

Normal of corresponding

week

2018-19

1 Wheat 305.58 303.69 336.18 299.6 32.49 36.88

2 Rice 42.76 22.7 28.8 25.31 6.1 3.49

3 Pulses 146 151.1 161.17 151.78 10.06 9.39

a Gram 93.53 95.38 107 96.19 11.83 11.02

b Lentil 14.19 16.09 16.07 16.91 -0.02 -0.84

c Field pea 9.45 10.33 9.64 10.46 -0.69 -0.81

d Kulthi 2.04 4.59 5.15 5.43 0.57 -0.28

e Urad bean 8.61 8.4 7.63 7.53 -0.77 0.1

f Moong bean 10.1 6.51 6.19 6.1 -0.31 0.09

g Lathyrus 4.13 3.7 3.31 3.09 -0.4 0.02

h Other pulses 3.94 6.1 5.96 6.07 -0.14 -0.11

4 Coarse Cereals 60.78 55.06 55.69 47.77 0.63 7.92

a Jowar 35.75 31.64 30.22 25.03 -1.42 5.19

b Bajra 0.31 0.21 0.2 0.13 -0.1 0.07

c Ragi 0.46 0.55 0.47 0.62 -0.08 -0.16

d Maize 17.49 15.22 16.98 14.78 1.76 2.2

e Barley 6.77 7.44 7.82 7.2 0.38 0.62

5 Oilseed 78.85 81.36 80.29 80.36 -1.07 -0.07

a Rapeseed & mustard 60.48 67.73 69.51 69.76 1.78 -0.24

b Groundnuts 7.76 5.95 4.76 4.59 -1.2 0.17

c Safflower 1.41 0.85 0.63 0.43 -0.22 0.2

d Sunflower 2.96 2.14 1.04 1.13 -1.1 -0.09

e Sesamum 3.12 0.76 0.56 0.71 -0.21 -0.15

f Linseed 2.99 3.51 3.46 3.44 -0.06 0.02

g Other oilseed 0.14 0.42 0.34 0.3 -0.08 0.04

Total crops 633.98 613.91 662.13 604.52 48.21 57.61

AGCON QUIZ ANSWERS OF THE PREVIOUS WEEK

S.no Name Location Department

1 SaiKumar Palaparti Hyderabad CWIG

2 Anil solanki Jodhpur CM

4 Akshay Rajaram Bhalmode Mumbai IT

5 Ritu Sangawat Gurugram SCM

6 Anilkumar Parvathaneni Gurgaon Risk

7 BASKARAN R ARNI CM

8 vamshikrishna g adilabad S&P

9 Piyush Kabra Jodhpur CM

10 Javeed M Davangere S&P

11 Abhishek bhati Boranada S&P

1 As per APEDA, Basmati Rice exports during April-January 2019-20 declined at … tonnes?

32,99,299

2 According to the second advance production estimate, Indian chana production in 2019-20 is?

11 .22 Mil l ion MT

3 Present total stock of cotton with Indian government agencies?

103 Lakh bales

Name of the Winner

Advisory Team

Nalin Rawal Head [email protected]

Sreedhar Nandam Vice President [email protected]

S. Anisul Hassan Head - Business Development [email protected]

Research Team

Sachin Wadhwa Head Research Soft Commodities [email protected]

Ankur Gupta Data Scientist [email protected]

Mukesh Upamanyu Agri Analyst [email protected]

Suresh Solanki Assistant Manager [email protected]

Akash Jaiswal Research Analyst [email protected]

Ratanpriya Assistant Manager [email protected]

Bhaskar M Quality Officer [email protected]

Shefali Jain Operation Executive [email protected]

Surbhi Taneja Operation Executive [email protected]

Rajiv Kumar Associate [email protected]

Disclaimer:

This consultancy report has been prepared by NCML AGRI BUSINESS CONSULTANTS PRIVATE LIMITED for the sole benefit of the

addressee. Neither the report nor any part of the report shall be provided to third parties without the written consent of AGCON. Any

third party in possession of the report may not rely on its conclusions without the written consent of AGCON. AGCON has exercised

reasonable care and skill in preparation of this consultancy report but has not independently verified information provided by others.

No other warranty, express or implied, is made in relation to this report. Therefore, AGCON assumes no liability for any loss resulting

from errors, omissions or misrepresentations made by others. Any recommendations, opinions and findings stated in this report are

based on circumstances and facts as they existed at the time of preparation of this report. Any change in circumstances and facts on

which this report is based may adversely affect any recommendations, opinions or findings contained in this report.

© NCML AGRI BUSINESS CONSULTANTS PRIVATE LIMITED (AGCON) 2019

BASKARAN R

CM