leadingage pa financial issues seminar accounting ... · •questions & answers agenda . ......

TRANSCRIPT

LeadingAge PA Financial

Issues Seminar

Accounting & Auditing Update Mark J. Ross, CPA, Partner

Abby M. Loftus, CPA, Senior Manager

November 14, 2012

1

• Audit Risk / Risk Assessment

• Accounting for Refundable (Advance)

Entrance Fees

• Clarity Standards

• Standards Update

• Current FASB Projects

• Software Capitalization

• Questions & Answers

Agenda

Audit Risk / Risk

Assessment

3

• Audit risk is the risk that the financial

statements are materially misstated

(whether caused by error or fraud) and the

auditor fails to detect such a misstatem

Audit Risk / Risk Assessment

4

• Audit standards require that auditors gain

an understanding of the entity and its

environment.

• Information about the industry and business

risks facing the entity will help identify

potential financial reporting risks and

misstatements.

Audit Risk / Risk Assessment

5

• Auditors must obtain sufficient understanding of the entity and its environment, which includes:

– Industry, regulatory, and other external factors

– Nature of entity

– Objectives and strategies and related business risks

– Measurement and review of financial performance

– Internal control, including selection and application of accounting policies

Audit Risk / Risk Assessment

6

Industry Matters

• Demand for Services / Occupancy • Economy / Housing market

• Uncertainty related to the future of Medicare and Medical Assistance reimbursement

• Increasing levels of benevolent care

• Personnel / Employee Related Expenses – 40% - 60% of total expenses – Health insurance is a significant driver

• Generally, we see strong expense management in the industry

• “Balancing the Budget” is a Challenge

7

Industry Matters

• Financial performance – Performance improvement initiatives continue to be a focus

• Aging Physical Plants / Access to Capital

• Renewal of Letters of Credit

• Home and Community Based Services

• Health Care Reform

• Partnerships and Affiliations

• Government Initiatives / Focus – State regulators

– IRS

• Governance / Board Education / Succession

8

• After obtaining a sufficient understanding of the entity and its environment, an auditor should identify and assess the risks of material misstatement at the financial statement level and at the relevant assertion level related to classes of transactions, account balances, and disclosures

• WHAT COULD GO WRONG?

Audit Risk / Risk Assessment

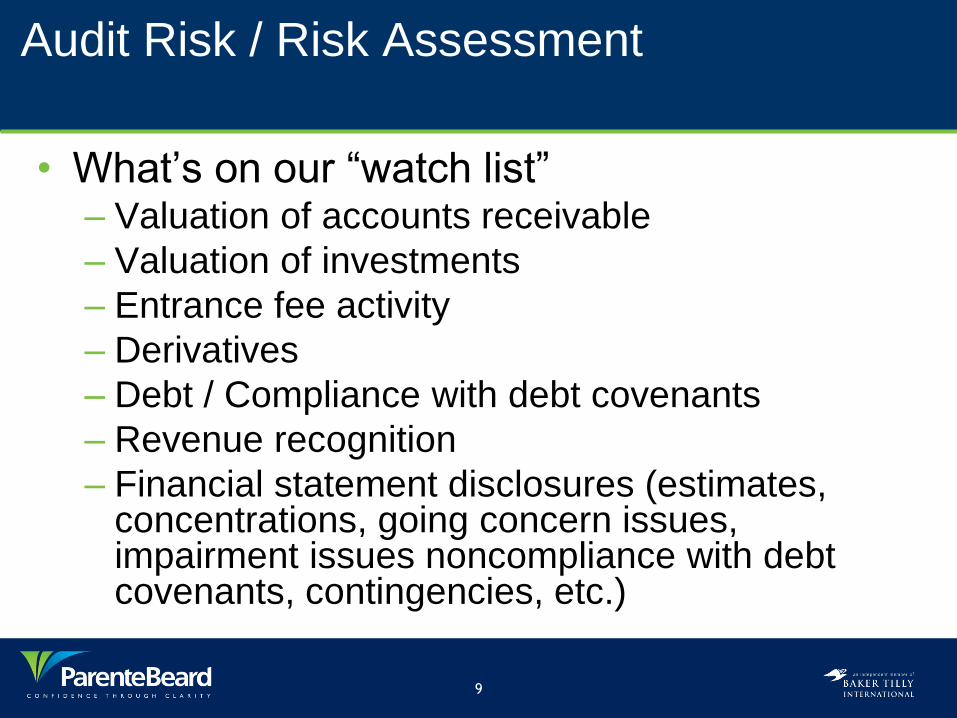

9

• What’s on our “watch list” – Valuation of accounts receivable

– Valuation of investments

– Entrance fee activity

– Derivatives

– Debt / Compliance with debt covenants

– Revenue recognition

– Financial statement disclosures (estimates, concentrations, going concern issues, impairment issues noncompliance with debt covenants, contingencies, etc.)

Audit Risk / Risk Assessment

Accounting for

Refundable (Advance)

Entrance Fees

11

• Accounting guidance related to advance fees – both refundable and nonrefundable – has been in play for 20+ years – dates back to SOP 90-8 and is currently included in FASB’s Accounting Standards Codification (“ASC”)

• This accounting guidance had not been updated over the years to address the evolution of CCRC contracts and contract options

• Further, the economic / housing market situation has caused certain CCRCs to lower entrance fees to attract prospective residents (offering “special deals”)

Historical Accounting guidance

12

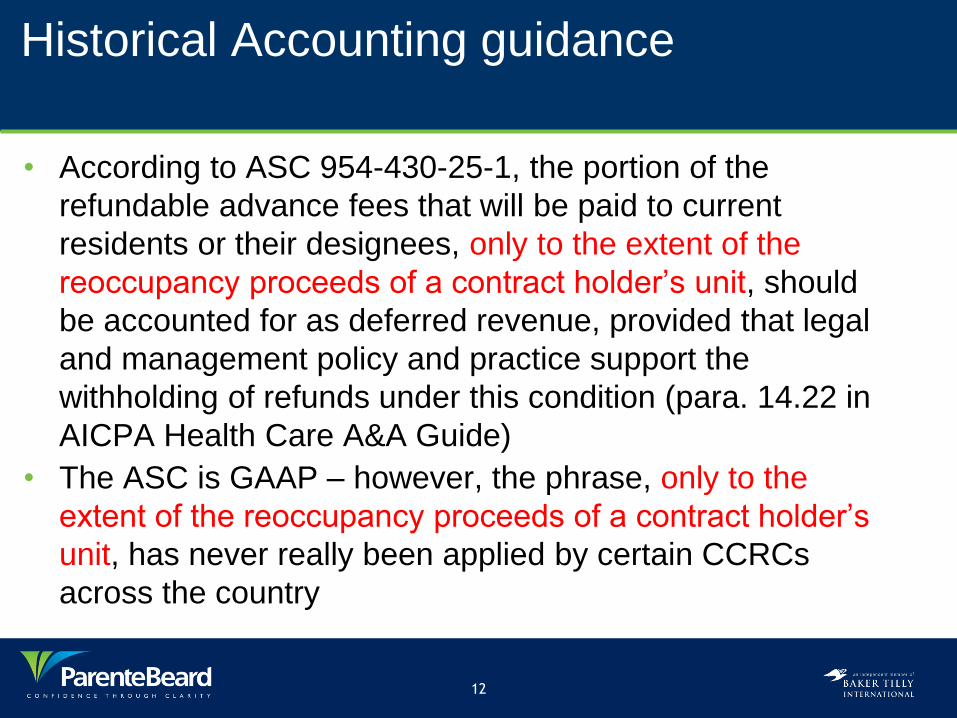

• According to ASC 954-430-25-1, the portion of the

refundable advance fees that will be paid to current

residents or their designees, only to the extent of the

reoccupancy proceeds of a contract holder’s unit, should

be accounted for as deferred revenue, provided that legal

and management policy and practice support the

withholding of refunds under this condition (para. 14.22 in

AICPA Health Care A&A Guide)

• The ASC is GAAP – however, the phrase, only to the

extent of the reoccupancy proceeds of a contract holder’s

unit, has never really been applied by certain CCRCs

across the country

Historical Accounting guidance

13

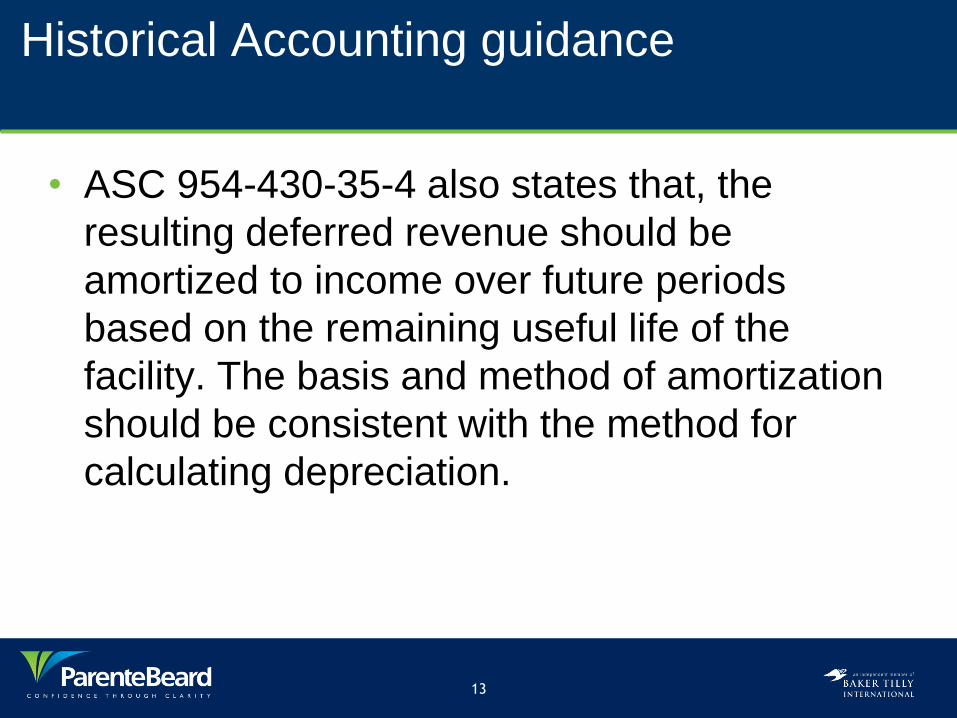

• ASC 954-430-35-4 also states that, the

resulting deferred revenue should be

amortized to income over future periods

based on the remaining useful life of the

facility. The basis and method of amortization

should be consistent with the method for

calculating depreciation.

Historical Accounting guidance

14

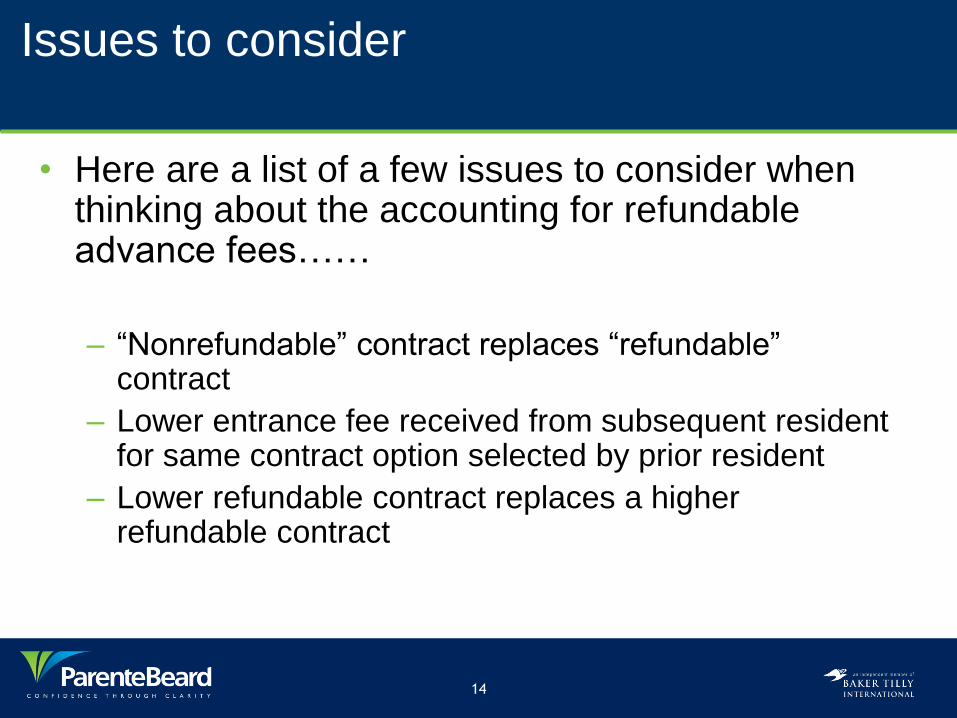

• Here are a list of a few issues to consider when thinking about the accounting for refundable advance fees……

– “Nonrefundable” contract replaces “refundable”

contract

– Lower entrance fee received from subsequent resident for same contract option selected by prior resident

– Lower refundable contract replaces a higher refundable contract

Issues to consider

15

– Application of refundable entrance fees to amounts due for personal care/assisted living or nursing care

– Depreciation life vs amortization life

– Amortization revenue is non-cash revenue – generally, amortization revenue has no impact on debt covenant calculations – if amortization revenue does impact certain covenants (i.e. debt to equity), organizations should pursue the elimination of these covenants

Issues to consider

16

• At this time last year, FASB had just issued a

proposed Technical Corrections Accounting

Standards Update (ASU); proposed ASU addressed

various issues

• Paragraphs 46 and 47 of the proposed ASU included amendments related to the accounting for refundable advance fees

Where we were last year

17

Where we were last year

• One amendment created a reference in paragraph 954-430-35-4 to paragraph 954-430-25-1

– Clarifies that to be able to treat a refundable advance fee as deferred revenue that is amortized over the life of the facility, any refund payable must be limited to the proceeds of reoccupancy of the unit, and it must be the entity’s policy or practice to comply with that limitation

18

Where we were last year

• Paragraph 954-430-25-1 was also amended to add language that states when a contract between a CCRC and a resident stipulates that a portion of the fees will be paid to current residents or their designees, only to the extent of the proceeds of reoccupancy of a contract holder’s unit, that portion shall be accounted for as deferred revenue, provided that legal and management policy and practice support the withholding of refunds under this condition

19

Where we were last year

• FASB acknowledged that amendment addressed in paragraph 47 is deemed to be more substantive than most of the other issues addressed in the ASU

20

• As a result of comment letters received and

further deliberations by FASB, which included

dialogue with members of the AICPA Health

Care Expert Panel, FASB carved out the

CCRC specific pieces of the proposed

Technical Corrections ASU and created an

ASU specific to this issue

Where we are now

21

• In July 2012, FASB issued ASU 2012-01

– Continuing Care Retirement Communities –

Refundable Advance Fees

• Effective for years beginning after December 15, 2012

(calendar 2013 / fiscal 2014) for public entities –

Public entities include conduit debt obligors

• Effective for years beginning after December 15, 2013

(calendar 2014 / fiscal 2015) for nonpublic entities

Where we are now

22

• Guidance clarifies the accounting for

refundable entrance fee contracts. In order for

a CCRC to be able to treat a refundable

entrance fee as deferred revenue that is

amortized to income over the life of the facility,

any refund payable must be limited to the

proceeds of reoccupancy of the unit, and it

must be the entity’s policy or practice to

comply with that limitation

ASU 2012-01

23

• ASU added language to ASC 954-430-25-1, which states:

– “when a contract between a CCRC and a resident stipulates that a

portion of the fees will be paid to current residents or their

designees, only to the extent of the proceeds of reoccupancy of a

contract holder’s unit, that portion shall be accounted for as

deferred revenue, provided that legal and management policy and

practice support the withholding of refunds under this condition”

• If contract does not include the above language, a CCRC will no longer be able to amortize the refundable entrance fees to income and must restore the refundable entrance fee liability to the full refund amount in the resident agreement with a corresponding decrease in equity (net assets).

ASU 2012-01

24

• Application of the ASU will result in the recording of a cumulative-effect adjustment to opening equity (net assets) as of the beginning of the earliest period presented

ASU 2012-01

25

• ASU 2012-01 may also result in changes to the calculation of the obligation to provide future services and use of facilities (FSO) for CCRCs that offer Type A and Type B contracts, and if applicable, should be discussed with the CCRC’s actuary

What about the FSO?

26

Balance Sheet Classification of

Refundable Advance Fees

• Diversity in practice exists regarding classification of the refundable

portion of advance fees

• In practice, refundable advance fees should be classified based upon

the expected timing of refunds to be made

• The classification as current and noncurrent depends upon the

CCRCs own history of refunds and the terms of its resident

agreements – Contract types may also impact this issue

• How should an organization arrive at a “current liability” for its

refundable advance fees?

Clarity Standards

28

Auditing Standards Board (“ASB”)

Clarity Project

• Began after the creation of the Public Company Accounting Oversight Board (“PCAOB”)

• ASB aligned its projects with the International Auditing and Assurance Standards Board (“IAASB”) and also determined to minimize differences with the PCAOB

• Redraft all of the extant auditing standards into a standardized structure, which had been developed by the IAASB

• Standards to be principle based

• Effective for audits of entities with years ending after December 15, 2012

29

Clarity Project

• Drafting conventions:

– Establish objectives for each standard

– Include a definitions section where relevant

– Separate requirements from application material

– Provide special considerations for smaller non-complex entities

– Special considerations for governmental audits

30

Clarity Project

• What are the major issues? – Consideration of laws and regulations

• Requires additional procedures to be performed

• Must obtain an understanding of relevant legal and regulatory framework

• How is entity complying?

• Understand whether the auditor has external reporting requirements for violations

• Document identified or suspected non compliance

• Written representation

• More documentation and testing

31

Clarity Project

– Communicating internal control matters • Now must communicate with management all

deficiencies noted, not just significant deficiencies or material weaknesses

• Must communicate the potential effects of the significant deficiencies and material weaknesses to those charged with governance

• Required to communicate, in writing or orally, only to management, other deficiencies of sufficient importance that, in the auditor’s professional judgment, merit management’s attention

32

Clarity Project

– Related parties • Must consider risk of material misstatement, regardless of financial

reporting framework

• Adds more explicit requirements as to procedures and documentation

• The objectives of the auditor are to:

– Obtain an understanding of related party relationships and transactions sufficient to be able to recognize fraud risk factors, if any, arising from those relationships and transactions and conclude, based on the audit evidence obtained, whether the financial statements, insofar as they are affected by those relationships and transactions, achieve fair presentation.

– Obtain sufficient appropriate audit evidence about whether related party

relationships and transactions have been appropriately identified, accounted

for, and disclosed in the financial statements.

• ASB considers this to be a high-risk area

33

Clarity Project

– Group audits • The definition of “group” is quite broad and may scope

in many more situations

• The requirements of the clarified SAS address the following:

– Acceptance and continuation considerations

– Group engagement team’s process to assess risk

– Determination of materiality to be used to audit the group financial statements and audit components

– Selection of components and account balances for testing

– Assessing adequacy of audit evidence by the group engagement team

34

Clarity Project

– Clarifications on external confirmations

• The auditor is required to consider whether external

confirmation procedures are to be performed as

substantive audit procedure

• Oral responses are not confirmations

• Access to a website is not an external confirmation

35

Clarity Project

– Opening balances on initial audit engagements – • Clarified SAS requires auditor to obtain sufficient

appropriate audit evidence about whether:

– Opening balances contain misstatements that materially effect the current period’s financial statements

– Accounting policies reflected in the opening balances have been consistently applied in the current period’s financial statements and adequately presented and disclosed

• Specifically makes clear that reviewing predecessor auditors’ workpapers cannot be the only audit procedure performed

– Documenting the use of a specialist now applies to the firm’s own internal specialists

36

Clarity Project

– Auditors’ report • Four paragraphs rather than three: (1) introduction (2)

management responsibilities (3) auditor responsibilities (4) opinion. Fifth paragraph required if other than unmodified report

• Improved language as to management’s responsibility

• Clarified format with specific headings

• Expanded description of an audit

• Two new terms – emphasis-of-matter and other-matter

paragraphs. Replaces explanatory paragraph

37

Sample Auditors’ Report

Report on the Financial Statements

We have audited the accompanying consolidated balance sheets of ABC Company and its subsidiaries, as of December 31, 2012 and 2011, and

the related consolidated statements of income, retained earnings, and cash flows for the years then ended.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting

principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control

relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to

fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in

accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the

audit to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements.

The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated

financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s

preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the

circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control.2 An audit also includes

evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as

well as evaluating the overall presentation of the consolidated financial statements. We believe that the audit evidence we have obtained is

sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of ABC

Company and its subsidiaries as of December 31, 2012 and 2011, and the results of their operations and their cash flows for the years then

ended in accordance with accounting principles generally accepted in the United States of America.

Standards Update

39

• Historically, guidance required disclosure of charity care revenue recognition policy and amount, if material

• ASU 2010-23, Health Care Entities Measuring Charity Care for Disclosure issued in August 2010

• Objective is to reduce the diversity in practice regarding the measurement basis in the disclosure of charity care

• Effective for fiscal years beginning after December 15, 2010 and should be applied retrospectively to all periods presented

ASU 2010-23 - Charity care

40

ASU 2010-23

• Requires that cost be used as the measurement basis for charity care disclosure purposes

– A technique will have to be developed by the organization to

determine direct and indirect costs

• Also requires disclosure of the method used to identify or determine such costs

• Funds received to offset or subsidize charity services (ex. gifts or grants restricted for charity care) should also be disclosed

41

ASU 2010-24 - Insurance Claims and

Related Insurance Recoveries

• ASU 2010-24, Health Care Entities: Presentation of

Insurance Claims and Related Insurance Recoveries issued

in August 2010

• Clarifies that a health care entity should not net insurance

recoveries against a related claim liability and the amount of

the claim liability should be determined without

consideration of insurance recoveries

• Effective for fiscal years beginning after December 15,

2010, early application is permitted

42

ASU 2010-24

• Eliminates an industry exception to the

general principle on determining when net

presentation is permitted

– An insurance receivable should be recognized at

the same time the liability is recognized, subject

to the need for a valuation of allowance for

uncollectible amounts

43

ASU 2010-24

• Insurance receivable is subject to need for

valuation allowance for uncollectible amounts

• What does this mean for you??

– Materiality considerations

– Contact actuary to discuss potential impact

44

ASU 2011-07 – Presentation of Bad

Debts; Additional Disclosure

requirements • ASU 2011-07, Health Care Entities: Presentation and Disclosure of Patient Service Revenue, Provision for Bad Debts, and the Allowance for Doubtful Accounts for Certain Health Care Entities

• Objective - Provide financial statement users with greater transparency about a healthcare entity’s sources of net revenue and changes in its allowance for doubtful collections

• ASU was issued in July 2011; effective for fiscal years beginning after December 15, 2011, with early adoption permitted

45

ASU 2011-07

• Paragraphs 954-310-50-3 and 954-6-5-50-

4 require expanded disclosure with respect

to the allowance for doubtful accounts and

major payor sources when the “entity

recognizes significant amounts of patient

service revenue at the time the services

are rendered even though it does not

assess the patient’s ability to pay.”

46

ASU 2011-07

• Paragraph 954-605-45-4 also requires the provision for

bad debts to be reported as a component of net patient

service revenue under the same circumstances quoted in

the bullet above. However, Paragraph 954-605-45-5b

states “bad debts that shall continue to be presented as

an operating expense in the statement of operations are

the following: bad debts related to receivables from

patient service revenue if the entity only recognizes

revenue to the extent it expects to collect that amount.”

47

ASU 2011-07

• Most, if not all senior living providers undergo an

extensive analysis and assessment of each resident’s

ability to pay during the application/admission process,

and as a result, establish a very clear expectation of that

residents’ ability to pay

• The applicability of this ASU to each organization needs

to be evaluated

48

ASU 2011-08 – Testing goodwill for

impairment

• ASU 2011-08, Intangibles – Goodwill and Other (Topic 350) – Testing Goodwill for Impairment

• Objective – To simplify how entities, both public and nonpublic, test goodwill for impairment

• ASU was issued in September 2011; effective for fiscal years beginning after December 15, 2011, with early adoption permitted

49

ASU 2011-08

• ASU was intended to address concerns over the cost and complexity of performing the annual quantitative impairment test for goodwill

• Entities will have the option to first assess qualitative factors before performing the two-step goodwill impairment test (“Step 0”)

50

ASU 2011-08

– Based on facts and circumstances, if it is “more likely

than not” that the fair value of the reporting unit

exceeds its carrying value, then the two-step goodwill

impairment test is not necessary

– Examples of more likely than not that the carrying

value exceeds FV

• Deterioration in general economic conditions

• Deterioration in industry and market conditions

• Overall financial performance of reporting unit

• Entity-specific events (significant management turnover,

contemplating selling reporting unit or bankruptcy)

Current FASB

Projects

52

International Convergence

of Accounting Standards

• FASB and the International Accounting Standards Board

(IASB) have a common goal of one set of accounting

standards for international use

• International Financial Reporting Standards (IFRS) was

originally going to be adopted in 2011

• Most recent “progress report” issued in April 2011 –

Describes progress made to date on joint convergence

work

53

International Convergence

of Accounting Standards

• In July 2009, the IASB issued IFRS for Small and

Medium-Sized Entities (for Private Companies) –

Project started in September 2003

– Principles simplified

– Various Topics and Disclosures eliminated

• IFRS do not currently address not-for-profit

organizations

54

International Convergence

of Accounting Standards

• The move to IFRS?

– Continued debate on whether the United States

should adopt IFRS

• “single set of high-quality globally accepted accounting

standards”

– SEC initially issued a “roadmap” in 2008 to

discuss how SEC filers may move to IFRS

compliance

55

International Convergence

of Accounting Standards

– SEC issued a Final Staff Report in July 2012

• Does not make a recommendation on whether to adopt

IFRS for SEC filers

• Raises several concerns:

– Lack of LIFO inventory accounting

– Perception that quality “gap” in IFRS is greater than U.S.

GAAP

– Little or no industry-specific guidance

– Funding issues with IFRS Foundation

– Costs of conversion

56

Revenue Recognition Project

• Joint project of the FASB and IASB

• Exposure draft, Revenue From Contracts From Customers, issued 11/14/11, comment period was open until 3/13/12

• This is actually a re-exposure of the original 2010 exposure draft, in response to nearly 1,000 comment letters received

• Standard would not be effective earlier than annual reporting periods beginning on or after 1/1/15, based on current timetable

57

Revenue Recognition Project

• Proposed guidance is intended to….

– Provide a more robust framework for addressing revenue recognition issues

– Remove inconsistencies and weaknesses from existing revenue recognition requirements

– Improve comparability of revenue recognition practices across companies, industries, and capital markets

– Provide more useful information to users of financial statements through improved disclosure requirements

– Simplify the preparation of financial statements by streamlining the volume of accounting guidance

58

Revenue Recognition Project

• Core principle in proposed guidance is that an entity shall recognize revenue to depict the transfer of goods or services to customers in an amount that reflects the consideration the entity receives, or expects to receive, in exchange for those goods or services

59

Revenue Recognition Project

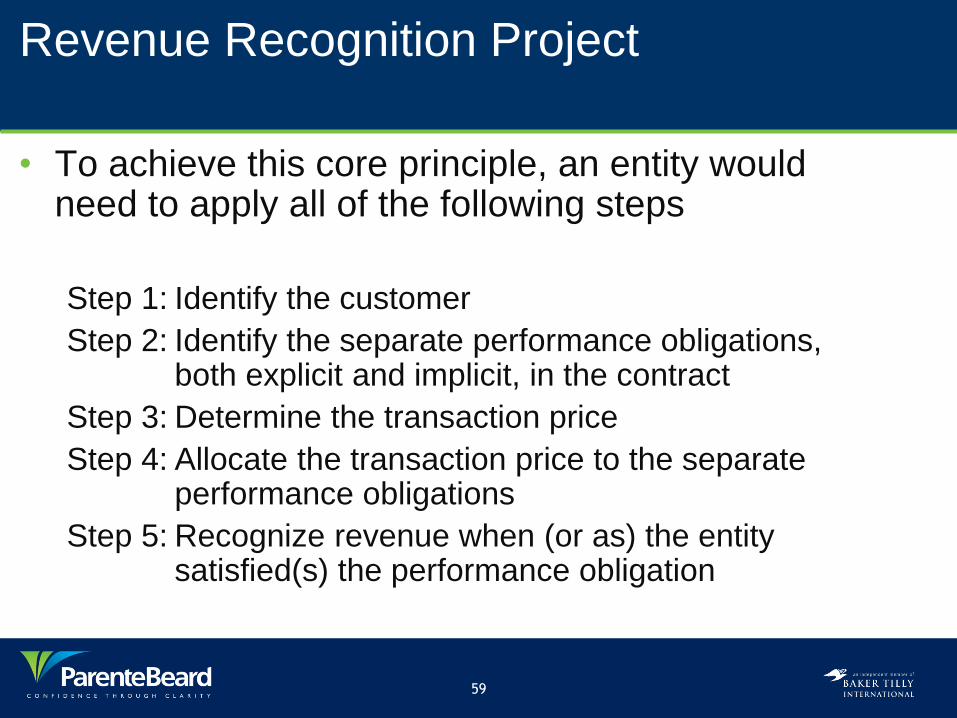

• To achieve this core principle, an entity would need to apply all of the following steps

Step 1: Identify the customer

Step 2: Identify the separate performance obligations, both explicit and implicit, in the contract

Step 3: Determine the transaction price

Step 4: Allocate the transaction price to the separate performance obligations

Step 5: Recognize revenue when (or as) the entity satisfied(s) the performance obligation

60

Revenue Recognition Project

• The proposed guidance would apply to all entities in all industries and would replace all of the general and industry-specific revenue guidance current in the ASC

• Impact on not-for-profit senior living organizations, specifically CCRC’s, is difficult to assess as there may be more questions than answers at this point……

61

Revenue Recognition Project –

What could this mean to CCRC’s

• Paragraph 57 of the Exposure Draft states, “If an entity receives consideration from a customer and expects to refund some or all of that consideration to the customer, the entity shall recognize as a refund liability the amount of consideration that the entity reasonably expects to refund to the customer”

– How does this impact the accounting for refundable

advance fees?

62

Revenue Recognition Project –

What could this mean to CCRC’s

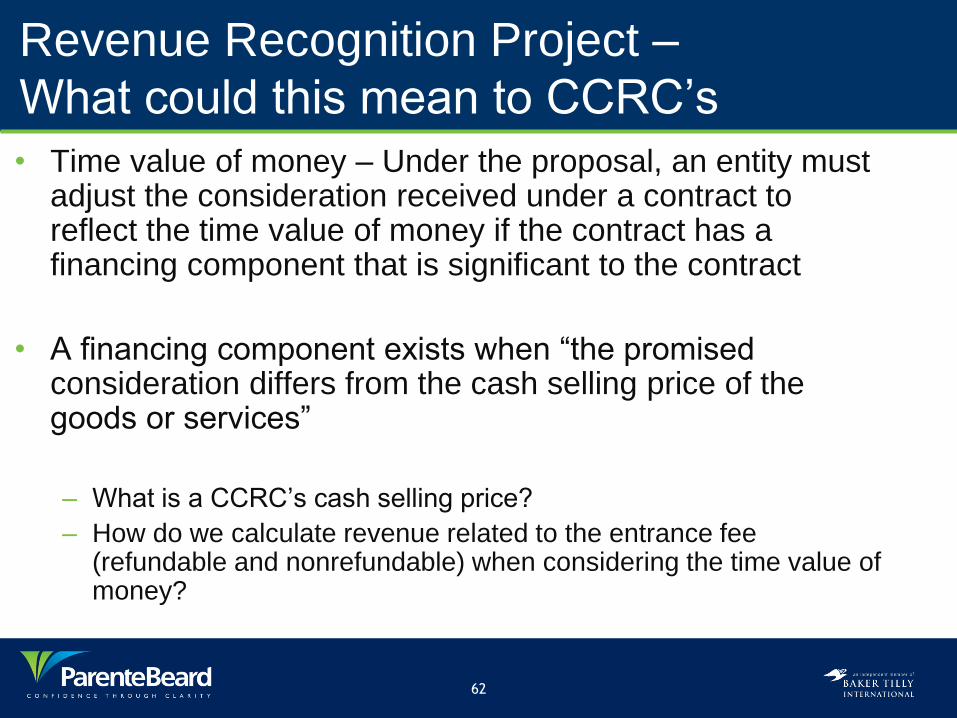

(cont’d) • Time value of money – Under the proposal, an entity must adjust the consideration received under a contract to reflect the time value of money if the contract has a financing component that is significant to the contract

• A financing component exists when “the promised consideration differs from the cash selling price of the goods or services”

– What is a CCRC’s cash selling price?

– How do we calculate revenue related to the entrance fee (refundable and nonrefundable) when considering the time value of money?

63

Revenue Recognition Project –

What could this mean to CCRC’s

(cont’d) • Performance obligation(s) and pattern of

transfer – CCRC’s will be required to evaluate the performance obligation(s) inherent in a CCRC contract and evaluate the pattern of transfer of benefit over time

• Performance obligations are different in Type A, B, and C contracts

64

Revenue Recognition Project –

What could this mean to CCRC’s

(cont’d) • Objective is to “depict the transfer of control of

goods or services to the customer”

– What are a CCRC’s performance obligations?

– For life care communities, are there 3 separate performance obligations – One in IL, AL, and Nursing?

– Would revenue need to be “back-end loaded?”

65

Revenue Recognition Project –

What could this mean to CCRC’s

(cont’d) • Obligation to provide future services

– What does the FSO calculation look like under the proposed guidance?

66

Revenue Recognition Project –

What could this mean to CCRC’s

(cont’d) • There is clearly a significant need for

implementation guidance that CCRC’s can use to implement the proposed guidance when it becomes effective

• Absent effective, clear implementation guidance, there may be inconsistencies related to how CCRC’s recognize revenue in the future

67

Revenue Recognition - Reminder

• Revenue recognition – SOP-00-1

– Recognition that auditors expertise is in accounting and

auditing rather than operational, clinical or legal matters

68

Proposed ASU – Leases

• Joint project of FASB and IASB

• Stated Project Objective

– To create common lease accounting requirements to ensure that

assets and liabilities arising from leases are recognized in the

statement of financial position

• Other “Unstated” Reasons – Similar transactions accounted for differently

– Ability to structure transactions to achieve desired result

– Reduced comparability for users

– Complexity of existing standards

69

Leases

• August 17, 2010 – Exposure Draft issued

• December 15, 2010 – Comment period ended

• Significant activity / deliberations between December 15, 2010 and today – Most recent deliberations were held during March 21-22, 2011 FASB meeting

• July 21, 2011 – FASB and IASB agreed to unanimously re-expose the revised proposals in Q1 of 2013

• Effective date not yet determined

70

Leases

• Right-of-Use Model

– Materiality considerations

– Debt covenant considerations

• Lessee would recognize an asset representing its right to use an underlying asset and a liability representing its obligation to make lease payments at the date of commencement of the lease

• Lessor would recognize an asset representing its right to receive payments and a liability representing its obligation to perform under the lease at the date of commencement of the lease

• Proposal would not grandfather existing leases

71

Blue Ribbon Panel (BRP)

• BRP formed in December 2009 by the Financial Accounting Foundation (parent company of FASB), National Association of State Boards of Accountancy, and the AICPA

• To determine how accounting standards can best meet the needs of users of U.S. private company financial statements and to provide recommendations on the future standard setting for private companies

• Considered IFRS for Small and Medium-Sized Entities (for Private Companies) in deliberations

• Work limited to for-profit companies

• Report issued in January 2011

72

BRP

• BRP concluded that there are urgent and growing systemic issues that need to be addressed in current system of U.S. accounting standard setting

• Current system has not done a good job of….. – Understanding the information that users of private

company financial statements consider decision-useful and how those information needs differ from those of users of public company financial statements

– Weighing the costs and benefits of GAAP for use in private company financial reporting

73

BRP

• Proposed enhancements aimed at fostering an accounting standard setting system that would maintain a high degree of financial reporting comparability for business entities

• In the near term, system should focus on making exceptions and modifications to U.S. GAAP for private companies rather than move to a separate, self-contained GAAP for private companies

• Proposed the establishment of a private company standards board to ensure that appropriate and sufficient modifications are made, for both new and existing standards

• And more……..

74

Recent Activity by Financial Accounting Foundation

• Established the Private Company Council (PCC) on 5/23/2012 – Council would develop criteria for determining “whether exceptions or

modifications to existing nongovernmental US GAAP are necessary to address the needs of users of private company financial statements”

• PCC will determine which elements of existing GAAP to consider for possible exceptions or modifications by a vote of two-thirds of all sitting members, in consultation with the FASB and with input from stakeholders

– However, any proposed changes would be subject to ratification by FASB and submitted to the public for comment

– The PCC also will serve as the primary advisory body to the FASB on the appropriate treatment for private companies for items under active consideration on the FASB’s technical agenda.

75

Not-for-Profit Advisory Committee (NAC)

• 3 working groups established to study initiatives that might be undertaken to improve the NFP (including health care) financial reporting model

– Reporting Financial Performance

– Telling the Story

– Liquidity / Financial Health

76

NAC

• Press release on 10/3/11 in which NAC identified four key recommendations where FASB could improve existing reporting standards for not-for-profits

• Revisiting current net asset classifications and how they may be relabeled or redefined, in conjunction with improving how liquidity is portrayed in a not-for-profit’s statement of financial position and notes

• Improving the statements of activities and cash flows to more clearly communicate financial performance

77

NAC

• Creating a framework for not-for-profit directors and managers to provide commentary and analysis about the organization’s financial health and operations, somewhat similar to the MD&A provided by publicly traded companies in their annual reports, to help bring context to their financial story

• Streamlining, where possible, existing not-for-profit specific disclosure requirements to improve their relevance and clarity

78

NAC

• In addition to these four recommendations, the NAC identified potential ways to create greater awareness among not-for-profits on ways to improve their financial reporting that are currently permitted by U.S. GAAP

79

Other Current FASB Projects

• See FASB website – http://www.fasb.org/

Software

Capitalization

81

Capitalization of Software Costs

• ASC Topic 350-40

• Applies to software purchased or developed

for internal use

• Does not apply to software to be sold or

used for research and development

82

Software Capitalization – 3 Stages

• Preliminary project stage

– Process of evaluating software options

– Decision to commit and fund a computer software project

has not yet been made

• Application development stage

• Post-implementation-operation stage

83

Software Capitalization

• Capitalization of costs can begin only when

– Preliminary project stage is completed

– Commitment is made on a particular software project

and funding

• Capitalization of costs ceases when the software

project is substantially complete and is ready for its

intended use

84

Software Capitalization

• Examples of costs to be capitalized

– Costs for developing software

– Costs for software that allows for access to or conversion of old data by new systems

– Payroll and payroll-related costs • Only for time directly related to the project

– Interest costs incurred

85

Software Capitalization

• Examples of costs not to be capitalized

– Data conversion

– General and administrative (i.e. overhead)

– Training

– Maintenance

86

Upgrades or Replacements

• Upgrades should be capitalized or expensed

in the same fashion as the original software

– Should provide additional functionality

• If activities to obtain/develop new software

take place, should re-evaluate useful life of

current software

– Old software is not written off until replaced

Questions and

Answers