voliume 7 public disclosure authorized 1 april...

TRANSCRIPT

VOLIUME 7

1 april 1999 20258

GLOBAL COMMODITY MARKETS

a comprehensive

review and price

forecast

THE WORLD BANK

Commodities Team

DLevelopment Prospects Group ISSN 1020-721X

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

VOLUME 7

1 E 3 4 ap r i 11999

GLOBAL COMMODITY MARKETS

a comprehensivereview andprice

forecast

THE WORLD BANK| Washington, D.C.

Copyright C) 1999 The International Bank for Reconstruction and Development/The World Bank

1818 H Street N.W., Washington, D.C. 20433, USA

All rights reserved.

Manufactured in the United States of America

You may not copy, reproduce, publish, distribute, transmit, create derivative works, or in anyway exploit any part of the contents of this publication without prior written permission fromthe Office of the Publisher at the address above. The contents of this publication may not beused to construct any kind of database.

The World Bank does not guarantee the accuracy of the data and forecasts presented in thisreport, and accepts no responsibility whatsoever for any consequence of their use.

ISSN 1020-721XISBN 0-8213-4516-8

Contents

Summary ......................... ............... 5

Regional Price Indices ................................ 7

Special Feature. . ............................... 8Currency Devaluations and Commodity Prices

Economic Outlook .......... 10

Ocean Freight .......... 11

EnergyC oal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12Natural Gas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14Petroleum . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .16

Non-Energy

Agriculture

BeveragesC ocoa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 20Coffee ................... 22Tea .... 24

Fats, Oils, and OilseedsFats and Oils ........ . .... .. .... .. .... .. .... .. 26Coconut Oil ......... ... ..... ..... ............ 28Palm Oil .. 30Soybean Oil . ..................... .. ... . I . . .32Soybeans .. 34

GrainsGrains .. 36M aize . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .38R ice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .40Wheat . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .42

april 1999

Contents (continued)

Agriculture (continued)

Other FoodBananas ...................... 44Shrimp ..................... ... ... ... . 46Sugar ..................... 48

Agricultural Raw MaterialsCotton ..................... 50Rubber ..................... 52Tropical Timber ..................... 54

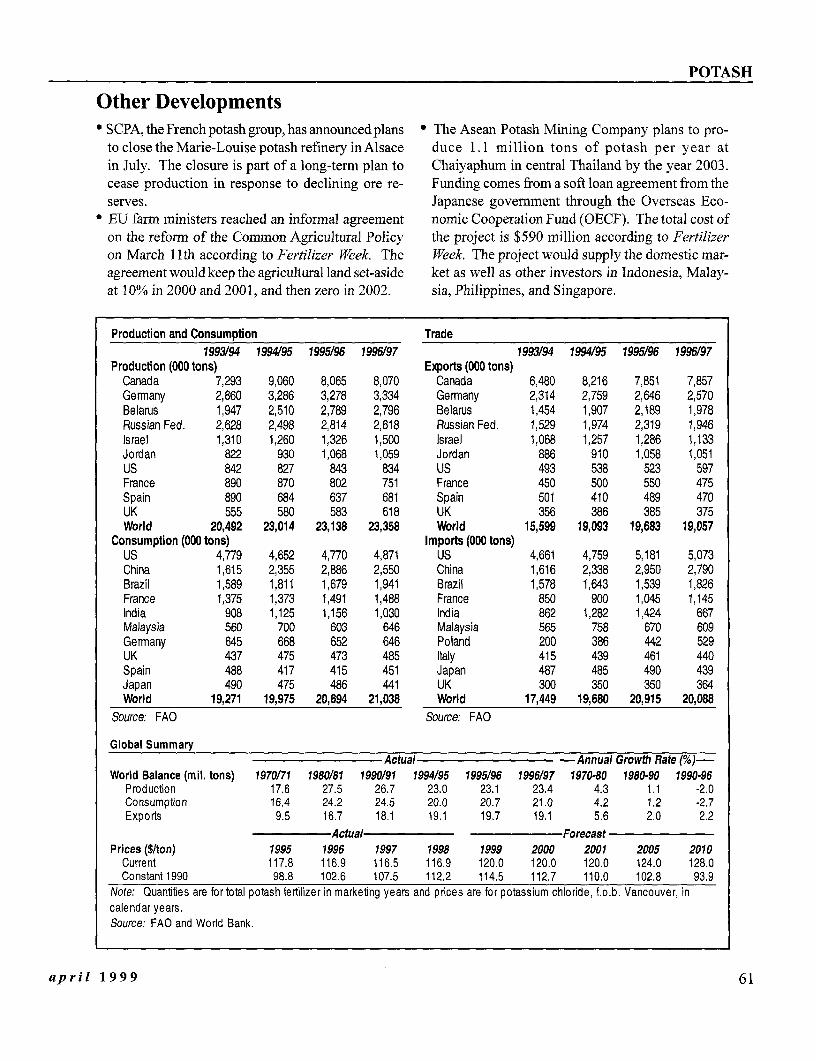

FertilizersNitrogen ..................... 56Phosphates ..................... 58Potash ..................... 60

Metals and MineralsAluminum. . ................... 62Copper. ..................... 64Gold ..................... 66Iron Ore and Steel .................... . ...... .... 68

AppendixCommodity Price Data.. . . 70Commodity Prices and Price Projections in Current Dollars .... 72Confidence Intervals for Price Projections in Current Dollars .73Commodity Prices and Price Projections in Constant 1990 Dollars . . . . 74Confidence Intervals for Price Projections in Constant 1990 Dollars. . . . 75Weighted Indices of Commodity Prices and Inflation. . . . . . . . . . . . 76

Description of Price Series .... 77

Definitions and Notes .... 79

Acronyms and Abbreviations .... 80

4 GLOBAL COMMODITY MARKETS

SUMMARY

S ummary ogy could also mean that prices will remain low for anumber of years.

The sharp price declines in most commodities The global economy is expected to face a secondare probably over, but the recovery is expected year of slow growth in 1999, with an overall increaseto be slow andfaltering. of 1.8 percent. The developing countries are expected

to have even slower growth of 1.5 percent and they areCommodity prices were generally lower during unlikely to return to long-term trend growth before

the quarter, with non-energy prices down an additional 2001. The severity of the crisis in Brazil is worse than5.0 percent from the fourth quarter. However, toward anticipated, although its effects are likely to be con-the end of the quarter, prices began to show evidence tained. Economic growth in Europe is showing signsof a rebound. Petroleum prices rallied sharply in March of weakness and the Japanese economy remains miredfollowing an agreement by OPEC members to curtail in deep recession. Not all of the news is bad, however.production, and prices of other commodities also ral- The US economy continues to show surprising strengthlied, but by lesser amounts. and there are now clear signs that the Republic of Ko-

The sharp declines in most commodity prices are rea and Thailand will be the first to emerge from theprobably over, with the recent price reductions now slump in Asia. Over the longer-term, strong economiccomparable to previous declines. However, additional growth is expected to resume. During the 2002-07price declines cannot be ruled out, and in particular, period, global growth is expected to return to the 3.1lower metals prices are possible. The recovery of prices percent per year growth of the 1 980s, and developingis expected to be slow and faltering. The continued countries are expected to grow by more than 5 percentweakness expected for the global economy, and espe- per year.cially for developing countries where the demand for The slow growth of demand for commoditiescommodities has historically grown the most rapidly, combined with rapid increases in commodity suppliesshould keep commodity demand weak and prices from has led to a surge in commodity stocks. These stocksrising significantly. Large stocks of most commodi- will need to be reduced before a recovery of pricesties will also need to be reduced before prices can can be sustained. For example, grain stocks held byrise. The large production capacity which has devel- the major exporters have increased from 60 millionoped for many commodities and the lower produc- tons in the 1995/96 marketing year to an estimatedtion costs which have come with improved technol- 140 million tons in the current marketing year. This

Non-Energy Commodity Price Index(1990 = 100)

130

110 - - - -

90 - - - - - - -

70

50

301980 1982 1984 1986 1988 1990 1992 1994 1996 1998

Source: World Bank

april 1999 5

SUMMARY

increase amounts to 40 percent of annual global trade coordinated reduction in production and exports ofof 200-210 million tons. Other commodities also have urea fertilizer following the collapse of prices in re-large stocks which will not likely disappear soon. cent months. Natural rubber producers met in Janu-Sugar production has exceeded consumption for the ary to discuss plans to cut production by 10 percent.fourth consecutive year and stocks are near record Such supply control initiatives are often only partiallylevels which has caused raw sugar prices to fall to successful as producers have an incentive to exceedless than 5 cents per pound. Metals stocks are also agreed production levels.near record levels and production capacity exceeds The decline in non-energy commodity prices sinceexpected demand. Copper stocks on the London the peak in 1996 now exceed previous declines and isMetals Exchange are the highest ever recorded. Pro- of comparable length. The graph below shows the be-duction of copper exceeded consumption in 1998, and havior of commodity prices in the 5 years followingproduction at the world's largest copper mining com- the 1980 and 1988 price peaks and also the recent pricepany, Codelco, grew by 13 percent as new capacity declines (shaded in figure on previous page). Follow-was introduced. The world's largest copper mine, ing each of the previous price peaks, commodity pricesEscondida in Chile, is now estimated to have produc- declined for an average of 34 months and by an aver-tion costs of $0.45 per pound compared to current age of 25 percent before prices either stabilized or in-world prices of about $0.70 per pound. Large surplus creased. In the recent period, non-energy commoditycapacity could lead to additional price declines. prices have declined by 29 percent over 34 months.

Commodity producers have begun to curtail pro- The behavior of prices over the next several yearsduction. Most of the initial efforts have involved co- is expected to be closely tied to overall economicordinated reductions of supplies by major producers, growth - as was the case after the two previous pricesuch as the OPEC agreement in March to reduce pro- declines. Following the 1980-82 price decline, globalduction of petroleum by 1.7 million barrels per day. GDP grew by 2.7% in 1983 and 4.3% in 1984 and com-However, there are also several other efforts to re- modity prices rose sharply. However, following theduce commodity production and individual produc- 1988-90 commodity price decline, GDP grew by lessers are also responding to lower prices. US grain pro- than 2.0% per year in the 1991-93 period and com-ducers have reported intentions to plant 3.8% less modity prices were stagnant. Growth in GDP is ex-grain area in the coming year in response to low prices. pected to be slow in the next couple of years, suggest-Russia and Ukraine have reportedly met to discuss a ing commodity prices may rise slowly.

Current and Previous Declines of Non-Energy Commodity Price Index(Peak= 100)

105

t,^-s/^ V~May 1996-March 1999Juneury 1988-Manary 1985 \

7585 *_d .. ... ~ -~ ~~~~~~

SO0 -~

0 12 24 36 48 60Months from Peak

Source: World Bank

6 GLOBAL COMMODITY MARKETS

REGIONAL PRICE INDICES

Regional Price Indices 120 East Asia and Pacific

Prices of developing countries' commodityexports fell twice as fast as those of all 105 ..... ...... . ......... . ...

exporters during the first quarter. World

Prices of non-energy commodities exported by 90

developing countries fell 7.4% from December to East Asia and PacificMarch compared to a 3.6% decline for all exporters. 75 __The greater price declines were due largely to the de-

clines in beverages, oilseeds, and sugar which are 60

heavily concentrated in developing countries. Bever- Mar-95 Mar-96 Mar-97 Mar-98 Mar-99

age prices fell 10.9% from December to March, fats

and oils prices fell 18.6%, and sugar prices fell 25%. 120 Latin America and CaribbeanCountries which devalued their currencies such Latin America and

as Brazil saw higher domestic currency prices which Caribbean

partially offset the dollar price declines, while coun- 105tries which did not devalue their currencies relative to

the dollar saw sharp price declines in both local cur- 90 ---

rencies and dollar terms. WorlAmong developing countries, those in Latin 75.. .

America fared worst, with an average price decline of

nearly 10% for non-energy commodities which they 60

export. Developing countries in other regions fared Mar-95 Mar-96 Mar-97 Mar-98 Mar-99

better, but still saw prices of their non-energy com- South Asiamodities fall faster than those of all exporters. The 120

price index for Sub-Saharan Africa fell 7.5% due to Revisedlower cocoa (-13.8%), robusta coffee (-12.6%), and Worldsugar prices (-25%). Exporters in East Asia had an 40 -

overall 7.3% decline in their non-energy commodity

prices due to lower vegetable oil prices, with palm oil 90 South ----

down 25%. South Asian exporters fared relatively S A

betterthan other developing country exporters, but still 75 -------------------------

saw their prices fall 6% from December to March.

Tea prices in both Calcutta and Colombo were down 60

sharply, 13.6% and 16.0%, respectively, due to in- Mar-95 Mar-96 Mar-97 Mar-98 Mar-99

creased supplies and weak imports from Russia. Sub-Saharan AfricaThe total terms of trade for lower- and middle- 120

income developing countries fell by 5.7% in 1998. RevisedThe greatest declines were in those countries which

were heavily dependent on oil exports, since crude oil Worldprices fell 32%. The terms of trade for Sub-Saharan

Africa fell 9.9% in 1998, East Asia's terms of trade 90.

fell 1.5%, Latin America and Caribbean's terms of

trade fell 4.9%, and South Asia had a 5.6% improve- 75

ment in its total terms of trade. Sub-Saharan Afri

Note: The regional price indexes use the non-energy commodity 60export basket of each region to compute the price index. This Mar-95 Mar-96 Mar-97 Mar-98 Mar-99index is then compared with the index using global exports.

april 1999 7

SPECIAL FEATUREurrencv Devaluations largely domestic.

Currency Devaluations . If devaluation is accompanied by a recession anda reduction of disposable income (which has re-

and Com m odity Prices cently been the case), domestic demand will con-tract even more and hence the supply availability

In the last two years, currency devaluations in the world market will be even greater.have played an important role in shaping * The effects of reduced income and higher domes-commodity markets. Starting in East Asia, tic prices on the world price of a commodity arethen in Russia, and more recently in Brazil, negative if the country is a major importer. Aftercommodity prices have responded quickly to the devaluation of the ruble, tea prices declined

as Russia temporarily dropped out of the tea mar-ket (Russia is the dominant tea importer account-ing for 17% of world imports). Following theBrazilian devaluation, US cotton prices declined

The "Textbook" Effects (Brazil imports cotton from the US).The devaluation of a small country's currency of- * Markets can react through substitute products.

ten goes largely unnoticed in commodity markets since Following the EastAsian crisis, cotton prices wereit does not affect world markets in any significant way. not affected significantly since East Asian cottonHowever, devaluations in countries with large trade imports were partially supported by the US andshares of commodity markets, or when a group of small Australian export guarantee programs. However,countries devalues which, taken together have a large because ofthe devaluations, chemical fiber pricestrade share, then the devaluation can have significant (close cotton substitutes) collapsed, in turn de-effects.* In a "textbook"' setting these effects can be pressing cotton prices (with an 8-month lag).summarized as follows:

• Following a devaluation, prices received by ex- The cases of Thailand and Brazil give a sense ofporters (denominated in domestic currency) in- the quantitative effects of devaluation. Thailand accountscrease, and induce exporters to deplete stocks and for nearly one-third of world rice exports and is consid-direct domestic supplies to intemational markets. ered the world price leader for rice. The Thai currencyDepending on the export share, increased supplies has been devalued twice in the last two decades; it wasin the world market will depress the dollar prices devalued from 23.00 baht/US$ in October 1984 to 27.95accordingly. The opposite effects apply to im- baht/US$ in February 1985. The US$ price of Thai riceports. exports declined from $256/tonto $220/ton overthe same

* The cost of producing the commodity may in- period. The devaluation of the currency was 21.52%crease depending on the use of imported inputs. and the decline in the US$ rice price was 14.15%. AGenerally, for commodities, the value added is parallel situation existed in 1997. The baht was deval-

1997 Shares of Major Exporting Countries in Selected Commodity Markets(excluding US and EU)Country Commodity Share (%) Country Commodity Share (%)Argentna Soybean Oil 34 Ecuador Bananas 38Australia Coal 30 Indonesia Coconut Oil 46Australia Iron Ore 30 Indonesia Palm Oil 24Brazil Coffee 29 Indonesia Rubber 32Brazil Iron Ore 29 Malaysia Coconut Oil 45Brazil Soybeans 21 Malaysia Palm Oil 64Brazil Sugar 21 Thailand Rice 28Canada Potassium 41 Thailand Rubber 41Cote d'lvoire Cocoa 55 Sr Lanka Tea 22Source: World Bank

8 GLOBAL COMMODITY MARKETS

SPECIAL FEATURE

ued from 25.78 baht/US$ in June 1997 to 37.40 baht/ the inflationrate exceeding 20% inAugust 1998),US$ in October 1997 and the US$ price of rice exports one would expect that the demand for automo-decreased from $323/ton in June to $266/ton in Octo- biles - and the demand for rubber to produce tiresber. The decline in the baht was 45% and the decline in - would have plummeted. Reports indicate how-the US$ price of rice was 18%. ever, that automobile sales continued to expand.

In many ways, the situations in Thailand and Bra- In fact, the expansion was driven by Russian con-zil are quite comparable. Brazil accounts for one-third sumers purchasing vehicles as a hedge againstof arabica coffee exports. Both rice and coffee face inflation.inelastic world import demand schedules in the short-run. And in the case of Thailand, the US$ price de- Expectations and fears of a potential devaluationclined by 40% and 66% of the amount of the currency or economic turmoil may affect commodity markets asdevaluation. Following the devaluation of the real, well.which was on the order of 35%, the nearby arabica * Brazil. When reports of a potential devaluationcoffee contract in New York declined by 17%, i.e., about of the real and possible economic turmoil in thehalf of the devaluation was translated into a coffee price Brazilian economy first appeared shortly after thereduction. Russian crisis, coffee exporters vigorously started

converting coffee stocks to dollars, which may... beyond the "Textbook" Effects have contributed to the decline of arabica prices.

Large devaluations, like those in Brazil, East Asia, In anticipation of the devaluation and economicand Russia, which are followed by domestic economic instability agents (i.e., coffee exporters) acted ininstability, often induce trade policy changes, as the fol- a rational way (i.e., by converting stocks to dol-lowing two examples illustrate: lars).

* Indonesia. The Indonesian govemment imposed The behavior of Brazilian exporters may havean export ban on palm oil in early 1998, fearing pushed coffee prices down even before the real's de-increased civil unrest following the financial cri- valuation. On the other hand, Malaysia's andsis. Palm oil is an important component of the Indonesia's policy changes had a positive effect ondomestic diet. Indonesia's palm oil production prices but, if removed, the effect will be reversed.and export shares were 32% and 25%, respec- Therefore, the effects of the devaluation on prices maytively. The export ban was later replaced by a be "stretched out" in both directions far more than the60% export tax, effectively keeping Indonesia out fundamentals dictate.of the export market, which explains why theprices of palm oil and soybean oil (a close substi- Conclusiontute to palm oil) rose following the crisis. Ultimately, the response of commodity prices to

* Malaysia. Malaysia's imposition of capital con- devaluations depends mainly on the trade share. Expe-trols in September 1998 is another example ofhow rience has shown that in commodity markets where apolicy changes may affect commodity markets. particular country's share is about one-third of worldThe imposition of capital controls effectively nul- trade, half of the devaluation is translated into a pricelified many rubber export contracts and compli- decline. Often, however, devaluations induce policycated the process of negotiating new ones. Natu- changes, which in turn alter the expected behavior ofral rubber importers turned to Indonesian and Thai commodity prices. Eventually, policy distortions maysuppliers, thus putting upward pressure on rubber be removed and the full impact of devaluation take place.prices - Thailand, Indonesia, and Malaysia ac- If the new exchange rate is sustained, the country's po-count for 41%, 32%, and 13%, respectively of sition in the world market may be durably altered bynatural rubber exports. making its exports more competitive.

Changes in savings behavior can impact commod- *Even in cases where a country accounts for only a small shareity prices in unexpected ways. of world trade, a devaluation may affect commodity prices if the

itysprices In the aftermath oftheRussianecon country is a major producer and consumer. A devaluation will* Russia. In the aftermath of the Russian economIc divert the commodity from domestic consumption to the export

crisis (with GDP shrinking by more than 8% and market.

april 1999 9

ECONOMIC OUTLOOK* ] * of world trade has been cut from 5.7% to 4.2%. Ex-Economic Outlook ternal finance is likely to remain tight, with access

A more difficult international economic envi- largely restricted to the most creditworthy borrowers,ronmentfor developing countries and at much higher spreads.

In most developing countries, private investmentThere have been important favorable develop- plans are being scaled back and restrictive policies

ments in recent months. Interest rate cuts in the United are being adopted to adjust to the reduced ability toStates and Europe, and the adoption of enormous fis- import. Domestic weaknesses remain, includingcal stimulus and financial restructuring plans in Ja- chronic fiscal deficits in several large developing coun-pan are likely to provide considerable support to de- tries, the need to undertake corporate and financialmand in the industrial countries in 1999. The US restructuring in many countries in Asia, and civil oreconomy has continued to show surprising strength, international conflicts in Africa.and there are clear signs that Korea and Thailand will The developing countries as a group are expectedbe the first to emerge from the slump in Asia. to experience very low growth in 1999, and are un-

Unfortunately, a broad review of the data indi- likely to return to long-termn trend growth rates beforecates more weakness than previously anticipated. 2001. Domestic factors will play a critical role, e.g.World industrial production fell 1% year-on-year in the rate at which fiscal consolidation progresses inthe fourth quarter. The crisis in Brazil is severe, al- countries such as Brazil, India, Russia, and Turkey;though its spillover effects are likely to be contained. the extent of financial and corporate restructuring inThere are also signs of faltering growth in Europe, several Asian countries; and the resolution of civil andand the Japanese economy remains mired in deep re- intemational conflicts in a number of regions.cession. There remain substantial risks to the forecast,

On balance, the external environment facing although the likelihood of markedly worse outcomesmost developing economies has continued to deterio- has receded in recent months. Among the risks arerate, reflecting weaker commodity prices, world trade, worsening economic conditions in Japan, a protractedand capital flows. The year-over-year growth of world withdrawal of capital market financing to Latintrade volumes in the fourth quarter of 1998 is esti- America, and a large stock market correction in themated at near zero and the 1999 forecast for growth United States and Europe.

World Growth, 1981-2007(Change in real GDP)

ForecastsRegion 1981-90 1991-97 1998 1999 2000 2001 2002-07World total 3.1 2.3 1.9 1.8 2.4 2.8 3.1

High-income countries 3.1 2.1 1.9 1.8 2.1 2.3 2.6OECD countries 3.0 1.9 2.0 1.8 2.0 2.2 2.5Non-OECD countries 6.6 6.1 -1.7 1.6 3.8 4.7 5.2

Developing countries 3.0 3.1 1.9 1.5 3.7 4.6 5.1East Asia 7.7 9.4 1.8 4.0 5.5 6.3 6.8Europe and Central Asia 2.6 -4.0 -0.3 -1.5 2.3 3.6 4.7Latn America and the Caribbean 1.9 3.6 2.0 -0.8 2.5 3.9 4.3Middle East and North Africa 1.0 2.9 1.5 0.7 2.5 3.3 3.7South Asia 5.7 5.5 5.2 4.4 4.8 5.2 5.0Sub-Saharan Africa 1.9 2.2 2.1 2.5 4.0 4.0 4.1

Memorandum itemEast Asian crisis countries 6.9 6.9 -7.7 0.3 3.5 4.5 5.3

Indonesia, the Republic of Korea, Malaysia, Philippines, and Thailand.Note: GDP is measured at market prices and expressed in 1987 prices and exchange rates. Growth rates over historic intervalsare computed using the least squares method.Source: Global Development Finance, World Bank. Data and baseline projectons, March 1999.

10 GLOBAL COMMODITY MARKETS

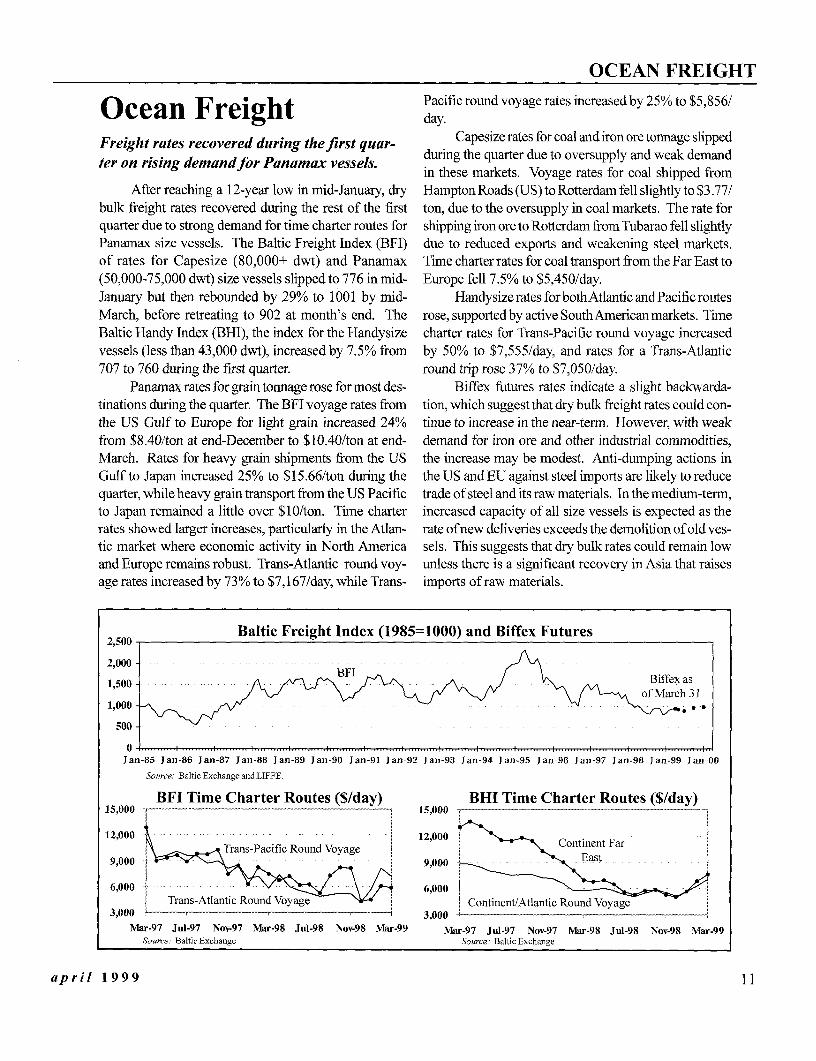

OCEAN FREIGHT

O c e an F reight Pacific round voyage rates increased by 25% to $5,856/Ocean Freight ~~~~~~~~day.

Freight rates recovered during thefirst quar- Capesize rates for coal and iron ore tonnage slipped.oridemandfor Panamax vessels, during the quarter due to oversupply and weak demand

in these markets. Voyage rates for coal shipped fromAfter reaching a 12-year low in mid-January, dry Hampton Roads (US) to Rotterdam fell slightly to $3.77/

bulk freight rates recovered during the rest of the first ton, due to the oversupply in coal markets. The rate forquarter due to strong demand for time charter routes for shipping iron ore to Rotterdam from Tubarao fell slightlyPanamax size vessels. The Baltic Freight Index (BFI) due to reduced exports and weakening steel markets.of rates for Capesize (80,000+ dwt) and Panamax Time charter rates for coal transport from the Far East to(50,000-75,000 dwt) size vessels slipped to 776 in mid- Europe fell 7.5% to $5,450/day.January but then rebounded by 29% to 1001 by mid- Handysize rates for bothAtlantic and Pacific routesMarch, before retreating to 902 at month's end. The rose, supported by active SouthAmericanmarkets. TimeBaltic Handy Index (BHI), the index for the Handysize charter rates for Trans-Pacific round voyage increasedvessels (less than 43,000 dwt), increased by 7.5% from by 50% to $7,555/day, and rates for a Trans-Atlantic707 to 760 during the first quarter. round trip rose 37% to $7,050/day.

Panamax rates for grain tonnage rose for most des- Biffex futures rates indicate a slight backwarda-tinations during the quarter. The BFI voyage rates from tion, which suggest that dry bulk freight rates could con-the US Gulf to Europe for light grain increased 24% tinue to increase in the near-term. However, with weakfrom $8.40/ton at end-December to $10.40/ton at end- demand for iron ore and other industrial commodities,March. Rates for heavy grain shipments from the US the increase may be modest. Anti-dumping actions inGulf to Japan increased 25% to $15.66/ton during the the US and EU against steel imports are likely to reducequarter, while heavy grain transport from the US Pacific trade of steel and its raw materials. In the medium-term,to Japan remained a little over $10/ton. Time charter increased capacity of all size vessels is expected as therates showed larger increases, particularly in the Atlan- rate of new deliveries exceeds the demolition of old ves-tic market where economic activity in North America sels. This suggests that dry bulk rates could remain lowand Europe remains robust. Trans-Atlantic round voy- unless there is a significant recovery in Asia that raisesage rates increased by 73% to $7,167/day, while Trans- imports of raw materials.

2,500 - Baltic Freight Index (1985=1000) and Biffex Futures

2,000-BF

1,500-Bifxa

1,000

500

Jan-85 Jan-86 Jan-87 Jan-88 Jan-89 Jan-90 Jan-91 Jan-92 Jan-93 Jan-94 Jan-95 Jan-96 Jan-97 Jan-98 Jan-99 Jan-00

Source: Baltic Exchange andLIFFE.

BFI Time Charter Routes ($/day) BHI Time Charter Routes ($/day)1 5,000 - -- _ ..... _.------.......... 1 5 000 ~~~~~ ~

12,000~~~~~~~~ 12,00012,000 \ Trans-Pacific Round Voyage Continent Far

9,000 9,000 East

6,000 - 6,000

3,000 Trans-Atlantic Round Voyage Continent/Atlantic Round Voyage

Mar-97 Jul-97 Nov-97 Mar-98 Jul-98 Nov-98 Mar-99 Mar-97 Jul-97 Nov-97 Mar-98 Jul-98 Nov-98 Mar-99Source: Baltic Exchange Source: Baltic Exchange

april 1999 11

ENERGY

Coal Monthly Prices ($/ton)

International coal prices remain depressedbecause of weak demand and oversupply. 41

Sharply lower contract prices for fiscal year 38

(FY) 1999 will likely result in the closure ofhigh-cost mines. 35

International coal prices fell slightly to $26.10 perton in the first quarter. Spot prices remain several dol- 32 . ..... ... IH..... H .,.

lars below the FY1998 contract price of $34.50/ton be- Mar-95 Mar-96 Mar-97 Mar-98 Mar-99Source: Coal Weeklnternational

cause of weak demand and excess supply.Australian thermal coal suppliers agreed to a bench- World Balance (million tons)

mark price of $29.95/ton for FY1999 deliveries begin- 4,000ning April 1, a decrease of 13% or $4.55/ton. This fol-lows an 18% or $9 decrease in coking coal contract priceS 3,500

in December. Production

Low prices will likely result in the closure of some 3,000

high-cost operations and reduce investment in new ca-pacity. Mergers and consolidations, which have already 2,500

begun in the US and Canada, are expected to continue.Coal prices are expected to remain flat next year, 2,000 I l

although declines are possible if global economic activ- 1970 1975 1980 1985 1990 1995

ity weakens further. In the medium-term, a recovery in Source: IEAandWorldBank

Asian demand will help reduce excess supply and, withsome reduction in capacity, allow prices to rise moder- 600 Exports (million tons)ately. However, continued advances in technology, fur-ther productivity gains, and development of new low- 450

cost mines are expected to result in continued declinesin real prices. Over the longer-term, the implementation 300

of policies to reduce greenhouse gas emissions couldaffect thermal coal demand significantly. 150

US coal prices remained flat in the first quarter asmild weather reduced electricity demand and resulted 0 -in a large build-up of stocks. In addition, low oil and gas Source: 1EA ad 80 1985 W990 99

prices encouraged the use of these fuels to meet incre-mental and, in some cases, base-load requirements. US Annual Prices ($Iton)While the recent sharp rise in oil prices will cause utili- 80ties to switch back to coal, large inventories are expected Constant Forecast

to dampen demand this year. 65 -

US coal exports are expected to continue to fall aslower-priced coals from Australia and South Africa, and so -

growing coal export industries in Indonesia, Colombia,and Venezuela, increase their market shares. Steam coal 35 Current

exports will suffer most, while coking coal exports will Current

be supported by the demand for higher quality US coals. 20

Over the longer-term real prices are expected to 1977 1982 1987 1992 1997 2002 2007decline due to continued productivity improvements and Source: Coal WeekInternational and World Bank forecasts.

a shift to lower-cost, low-sulfur western coal.

12 GLOBAL COMMODITY MARKETS

COAL

Other Developments* Shell Australia has settled on a coking coal price of * The Australian Bureau of Agriculture and Resource

$33.70/ton with Brazilian steel mills, about $4 be- Economics (ABARE) projects that world thermallow mid-1998 spot levels. Last year's contract coal trade will increase by 4.6% p.a. over the nextprices for most Australian hard coking brands were five years, primarily reflecting higher economicin the $42.00-$43.00 range. growth rates in Asia. World metallurgical coal trade

* Ingwe, reporting for the first time as a wholly is expected to increase by only 1% p.a., with littleowned subsidiary of parent Billiton Plc, cut its growth expected in the short-term until blast fur-unit cost of sales at its Australian operations by nace steel production recovers. Shifts toward amore than 15% in A$ terms for the six-months greater share of steel production coming from elec-prior to end-December 1998. Including depre- tric arc furnaces are expected to contribute to theciation of the A$, its equates to a cost reduction slow growth in metallurgical coal consumption. Inof more than 25%. the steam coal sector, strong competition for ex-

* Steam coal exports from the US (excluding Canada) port markets, further increases in mining produc-began 1999 at an even slower pace than last year. tivity, and the addition of new, low-cost mines, areJanuary's shipments were barely half of December's, expected to cause real prices to ease further overand were 4% lower than January 1998. the medium-term.

Production (million tons) Exports (million tons)1994 1995 1996 1997 1994 1995 1996 1997

China 1,239.9 1,360.7 1,396.7 1,348.0 Australia 128.8 136.4 138.6 146.4US 857.7 858.6 884.1 908.9 US 64.7 80.3 82.1 78.7India 257.8 273.4 285.6 310.2 S. Africa, Rep, 54.8 59.7 60.2 63.4S. Afrca, Rep. 195.8 206.2 206.4 220.1 China 24.2 28.6 36.5 30.7Australia 176.7 191.1 193.4 207.5 Indonesia 21.9 31.3 36.4 41.7Russian Fed. 176.8 176.9 166.5 156.6 Canada 31.6 34.0 34.4 36.5Poland 133.9 137.2 138.0 138.0 Poland 27.7 31.9 28.9 29.5Kazakhstan 99.6 79.5 73.0 n.a Russian Fed. 23.1 26.3 25.6 21.6Ukraine 91.3 81.3 70.5 n.a Colombia 18.4 18.3 24.8 25.7Germany 57.6 58.9 53.2 51.2 Kazakhstan 26.0 12.9 21.7 n.a.UK 49.3 54.6 51.9 48.5 Czech Rep. 6.2 7.0 6.7 6.6Indonesia 32.3 41.1 50.2 54.5 Venezuela 4.4 4.3 3.5 4.2Canada 36.6 38.6 40.0 41.3 Netherands 3.1 2.9 2.4 3.5Colombia 22.7 25.7 30.1 32.6 Vietnam 2.1 1.8 2.1 1.7Korea, D. R. 28.0 26.0 24.1 24.0 Ukraine 4.6 2.4 2.0 n.a.Czech Rep. 17.4 17.2 16.5 16.0 New Zealand 0.9 1.3 1.6 1.2Spain 14.1 13.7 13.7 13.9 Belgium 1.0 0.8 1.2 1.5Vietnam 6.2 6.6 11.2 10.9 UK 1.2 0.9 1.0 1.1France 8.1 8.5 7.8 6.3 Germany 2.0 1.9 1.0 0.5World 3,551.6 3,698.7 3,754.9 3,775.1 World 413.6 464.6 483.9 494.3

Source: lEA Source: IEA

Global SummaryActual -Annual Growth Rate (%l)-

World Balance (mil. tons) 1970 1980 1990 1995 1996 1997 1970-80 1980-90 1990-97Producton 2,185 2,807 3,561 3,699 3,755 3,775 2.8 2.8 1.1Consumption 2,175 2,783 3,516 3,698 3,744 3,777 2.8 2.9 1.3Exports 167 263 401 465 484 494 4.4 4.9 3.5

Actual ForecastPrices ($/ton) 1995 1996 1997 1998 1999 2000 2001 2005 2010

Current 39.19 37.21 36.39 34.38 33.50 33.50 34.00 36.00 38.50Constant 1990 32.88 32.58 33.58 33.00 31.96 31.46 31.16 29.86 28.23

Source: IEA and World Bank forecasts.

april 1999 13

ENERGY

Natural Gas - US Monthly Prices ($/mbbtu)4.25-

High inventories and mild weather keep US Spotgas prices low, but inventory rebuilding and 3.50 -

concerns about domestic supplies cause a 275 -

recentfirming ofprices. .75

US natural gas prices fell 5.2% in the first quar- 2.00 -ter to $1.81 per million btu (mmbtu) on continued highinventories and weak demand. However, spot prices 1.25 - ....... I ..... ...firmed toward the end of March as bargain purchases Mar-96 Mar-97 Mar-98 Mar-99 Mar-00

for inventory pulled up prices. *Futures are end-March.Source: WSJ and NYMEX.

Storage levels at the end of the first quarter are Production (Tcf)estimated to have fallen near 1400 billion cubic feet 23(Bcf), but were still 20% higher than at the same timelast year, and more than 40% above levels two years 21earlier. In order to reach relatively full storage at the Consumptionend of October (last year was 3176 Bcf), a lower rate 19of injections is required this year.

Demand is projected to rise only moderately, 1 / roduction

partly due to the decline in industrial production. How- 17ever, higher oil prices will allow gas to recapture aportion of the dual-fuel market on the Atlantic coast. 15

US gas production is poised to decline slightly 1970 1975 1980 1985 1990 1995this year because of low oil and gas prices that has Source: US DOE

reduced investment for development drilling. Higher 4 Poil prices will benefit associated gas production, butmay not be sufficient to achieve positive growth in 3total output this year. But rising oil and gas prices areexpected to raise domestic production next year. 2

Imports from Canada are on the rise followingcompletion of more than 1.2 Bcf per day of additional 1pipeline capacity. It will take time to fill the new ca-pacity, and surplus pipeline capacity is expected to 0 - .endure well into 2000. 1970 1975 1980 1985 1990 1995

Gas prices are expected to decline this year due to Source: US DOE

ample supply and reduced pressure on injections because Annual Prices ($/mmbtu)of current high levels of inventories. In 2000 and be- 4 -yond, nominal prices are expected to rise on relatively Con Forecaststrong demand growth in the power generation sector, 3but real prices are not expected to increase. Another 1.2Bcf of new pipeline capacity from Canada is expected 2to be completed by the end of 2000, and new capacity urrentand higher exports are expected over the forecast pe- 1riod. US production is projected to increase moderately,with much of the growth occurring from conventional 0 - .onshore areas. However, unconventional onshore and 1970 1975 1980 1985 1990 1995 2000 2005 2010offshore gains - particularly from the deepwater Gulf of Source: US DOE, WSJ, and World Bank forecasts.

Mexico - will contribute to rising production.

14 GLOBAL COMMODITY MARKETS

NATURAL GAS

Natural Gas - Europe 3.50 Monthly Prices ($/mmbtu)

European gas prices continue to fall because European

of the lagged effect of low oilprices, but the 3.00 -

rebound in petroleum prices will pull gas 2.50

prices higher.European gas prices fell 4% in the first quarter 2.00 -

due to the lagged effect of low oil prices, as long-termcontracts of imported gas are indexed to petroleum 1.50-prices. The decline brings European gas prices to their Mar-95 Mar-96 Mar-97 Mar-98 Mar-99lowest levels in more than 20 years, and also down to Source: World Gas Intelligence

North American levels where prices are largely deter- Production (BCM)mined by gas-on-gas competition. However, the re- 500surgence of oil prices will raise European prices, de-pending on how petroleum markets perform and the 400pace of energy market liberalization in Europe. Production

Demand rose 3% in 1998 and is projected to in- 300crease by 4% this year as the fast pace of new house-hold connections continues. The ongoing switch to 200gas in the Italian power sector and the steady increase Consumption

in southern and central Europe are also adding to gas 100 -demand. Liberalization of the electricity and gas sec- 1970 1975 1980 1985 1990 1995tors and increasing environmental concerns are ex- Source: BP and World Bank estimates.

pected to raise gas demand over the longer-term. FSU* Production (BCM)There is more than ample capacity to supply Eu- 800 -

ropean markets from domestic and foreign sources, Production

and no resource constraints are envisioned in the dis- 600

tant future. Norwegian gas supplies continue to risefrom the volume buildup under the Troll field con- 400 -snp.tracts, and Russia's capacity to deliver gas to Turkeythrough Romania and Bulgaria will expand next year. 200

UK exports to the continent began in the fourth o -quarter through the Interconnector Pipeline, but low 1970 1975 1980 1985 1990 1995gas prices on the continent prevented UK prices from *Countries of the former Soviet Union.

rising. The pipeline flow was reversed in December Source: BP

as low continental gas prices drew mainland gas into Annual Prices ($/mmbtu)the UK. In addition, relatively low storage capacity 8in the UK provides an opportunity for continental gas Cntt Forecast

to satisfy a portion of peak-season British demand if 6the economics so warrant.

New supply routes through France are adding tothe increasingly competitive environment in Europe. 2The NorFra Pipeline to Dunkirk commissioned in Oc- Currenttober is the fourth major gas export line from Norway oto the continent. Along with additional imports of 1973 1978 1983 1988 1993 1998 2003 2008Nigerian LNG, France is positioned to deliver gas to Source: World Gas Intelligence and World Bank forecasts.

other countries, either physically or through swaps ofRussian and Algerian gas.

april 1999 15

ENERGY

Petroleum Monthly Prices ($/bbl)24 -

Anticipation of OPEC production cuts led tosoaring futures prices in March. Inventories 20 - Spot IPE Brent

remain high but with reasonable quota com- \ Futures

pliance they will fall in the second-half of the 1

year, leading to higher prices. 12 -

Oil prices rose sharply in March as anticipated 8 - .. ,

production cuts by OPEC led to strong speculative de- Mar-96 Mar-97 Mar-98 Mar-99 Mar-00

mand on futures markets. From mid-February to end- *World Bank average. Futures prices are end-March.

March, oil prices shot up 50% to end the quarter at SoWrce:Bloombergand lPE.

$15.50 per barrel (bbl). 80 World Balance (mb/d)For the first quarter, average oil prices actually

fell slightly because weak demand, high inventories, 70

and the unwillingness of producers to reduce supplies Production Consumption

kept prices low in January and February. But the abrupt 60

action of producers to remove significant volumes ofoil from market - compared with a lack thereof last 50

fall - quickly reversed market sentiment. The new out-put cuts will help reduce the surplus and result in higher 40 I I

prices, but the magnitude will depend on the level of 1970 1975 1980 1985 1990 1995

compliance and the pace of oil demand. Source. BP, FEA, and Uorld Bank.

Ten OPEC producers (excluding Iraq) agreed on OECD Total Stocks (million bbl)March 23 to reduce production by 6.9% or 1.7 mb/d 2,900 -

for one year beginning April 1. All producers acceptedreductions of 7.3% except Venezuela which was per- 2,750

mitted a 4.4% cut of 0.125 mb/d (see table). Nearly End-month

half of the volume reductions are bome by Saudi Arabia 2,600

and Iran with cuts of 0.585 mb/d and 0.264 mb/d, re-spectively. 2,450

The agreement was preceded by a meeting inAmsterdam between non-OPEC Mexico, Saudi Arabia, 2,300- l I

and Venezuela. They decided that more than 2 mb/d Mar-94 Mar-95 Mar-96 Mar-97 Mar-98 Mar-99Source. lEA an d World Bank.should be removed from the market, of which non-

OPEC producers were expected to contribute around Annual Prices ($/bbl)0.4 mb/d. Mexico agreed to cut 0.125 mb/d, Norway 600.1 mb/d, and Oman 0.06 mb/d. Constant Forecast

This is the third time in the past year that OPEC 45

has agreed to reduce production - the previous accordswere inApril 1998 (1.2 mb/d) and July 1998 (1.1 mb/ 30

d). The earlier cuts were less than effective in support-ing prices because, in addition to weak demand, they 15 -were needed to undo the 10% rise of quotas in the fourth Currentquarter of 1997, leading to the price collapse last year. 0 _ I I

Moreover, Iraq's production has risen by more than 1 1970 1975 1980 1985 1990 1995 2000 2005 2010

mb/d, which has offset cuts by other members. The Source: API, Bloomberg, and World Bank forecasts.

net effect is that OPEC is still producing more oil than

16 GLOBAL COMMODITY MARKETS

PETROLEUM

Petroleum (continued) Crude Oil Production (mb/d)before it raised quotas in late 1997 - OPEC production Oth

in the first quarter of this year of 30.6 mb/d was 0.5 24

mb/d higher than in the 3Q97 (see table).OPEC continued to produce about 0.5 mb/d above 16 Spot

quota in the first quarter, putting their rate of compli- Spotance at about 80% of the 1998 cuts. The largest over- 8

producers were Iran, Saudi Arabia (including their share usof Neutral Zone output), and Venezuela. 1970 1975 1980 1985 1990 1995

Non-OPEC production has been seriously af- *ForrnerCentrallyPlannedEconormes.

fected by low prices, as its overall production failed to Source: API and IEA.

increase in the first quarter. This follows growth ofonly 0.2 mb/d last year. Low prices have substantially 24 OPEC Crude Oil Production (mb/d)reduced industry revenues and upstream capital expen- Other

ditures, which in turn has caused a sharp decline in 18

development drilling. Nevertheless, production con-tinued to increase in a number of countries as a result 12of new developments, e.g., Brazil, Canada, Colombia,Mexico, and the UK. 6 Saud/

Higher prices will benefit non-OPEC producers, krabia

but it will take time for production to recover follow- 0 -iing more than a year of low prices. The wave of con- 1970 1975 1980 1985 1990 1995

solidation and merger activity will result in fewer com- Source: IEA and World Bank.

panies which could result in reduced investment in the OPEC Oil Export Revenues ($ billions)near-term. It is possible that total non-OPEC produc- 200 - othertion could fall this year despite higher prices. Other

Demand continues to increase moderately in the 150 - OEdeveloped world, due to continued strong economicactivity. In addition, German heating oil demand has 100been particularly strong in advance of an April tax hike.In the developing countries demand remains weak as a 50s-/,

result of the financial crises in Asia, and more recently Middle East

in Russia and Brazil. Demand appears to be stabiliz- 0ing in Asia, and there are indications that a recovery is 1970 1975 1980 1985 1990 1995

taking place. Republic of Korea oil demand rose by Source: IEAandWorldBank.

11% in January, but this was compared to a very low World Oil Demand (mb/d)level last year when heavy destocking occurred. More- 48 -over, the January level was lower than in December.Demand rose by less than 3% in February, but it is too 36

soon to know the underlying trend in consumption.24

Inventories have started to decline, but remain oprecariously high (see graphs). In recent weeks US 12USUproduct stocks have declined sharply due to relativelystrong demand, refinery problems, and spring mainte- 0 I

nance. Crude oil stocks, however, continue to rise. 1970 1975 1980 1985 1990 1995*Countries ofthe formier Soviet Union.Stocks will have to be reduced for prices to re- Source: BP and LeEA.

cover on a sustained basis. OPEC's production cuts

april 1999 17

ENERGY

Petroleum (continued) Growth in Quarterly Demand (mb/d)

could cause stocks to fall fairly quickly depending on Other*

the level of compliance and the pace of demand.Should OPEC fully comply with its new quotas, 1.0 -

production would fall by 2.2 mb/d, which includes the0.5 mb/d currently over quota plus the new cut of 1.7mb/d. A reduction of this magnitude could more than 0.0 -remove last year's build-up of stocks and lead to a very Asia-Pacific

tight market this winter. -1.0 - . I ._I_._ I_._I_._I

It is unlikely that OPEC will fully comply, as was 1Q93 1Q94 1Q95 1Q96 1Q97 1Q98 1Q99the case last year. Assuming 70% compliance of the *Excludes countries ofthe former Soviet Union.

needed cuts (2.2 mb/d), production would fall by 1.5 Sourrce: IEA

mb/d for the remainder for the year. Given prospects 40for moderate growth in demand and little increase in Non-

OPEC*non-OPEC supplies, stocks would not begin to fall sig- 36

nificantly until the second-half of the year. The annualdecline in inventories would be only half of last year's 32

build-up, but the projected draw in the fourth quarter ECwould imply a fairly tight market. 28

The pace of oil demand could assist or impedeOPEC's ability to raise prices. Should a recovery in 24 I I I

the developing countries not materialize and the econo- 1Q93 1Q94 1Q95 1Q96 1Q97 1Q98 1Q99

mies in Europe and North America begin to slow, then *ExCludes countries ofthe former Soviet Union.Source: IEA

the pressure on stocks to fall would subside accord- Europe Crude Oil Stocks (million bbl)ingly. On the other hand, should the developing world 380

indeed recover and help sustain robust growth in NorthAmerica and Europe, tightness in markets later in the 355

year could be expected. Should OPEC also fully com- End-Month*

ply with its quotas, the market may require higher pro- 330 -

duction to prevent a price spike next winter.For non-OPEC production, the benefits of higher 305 -

prices will take several months, if not much longer, towork their way through the system. It will also take 280 -companies time to recover from the financial constraints Mar-94 Mar-95 Mar-96 Mar-97 Mar-98 Mar-99and consolidations this past year. *March 1993 to February 1999.

If OPEC maintains output at a level that keeps N. America Product Stock (million bbl)prices in the upper teens over the next couple of years, 750 -

market pressures of the past decade will return. Overtime, competing supplies will renew their upward trend 700 -and impinge on OPEC's ability to raise market share. End-Month*

As more countries attract foreign capital and technol- 650 -

ogy, it will lead to growing competition in supplyingoil. Demand is projected to grow moderately over the 600longer-term but could be restrained by environmentalconcerns and policies to implement the reduction of 550 I I I

greenhouse gas emissions. Thus real prices are ex- Mar-94 Mar-95 Mar-96 Mar-97 Mar-98 Mar-99

pected to continue their long-term decline over the next *March 1993 to February 1999.

decade. Source: IEA

18 GLOBAL COMMODITY MARKETS

PETROLEUM

OPEC Crude Oil Production and Quotas Non-OPEC Oil Supply(Millions of barrels per day) (Millions of barrels per day)

1099- Quota New Change3Q97 4098 1.99 Quota Apr-99 Cutbacks 1996 1997 4Q98 1Q99 4098-1099

Algeria 0.85 0.81 0.82 0.03 0.731 0.057 US 8.59 8.65 8.16 8.11 -0.05Indonesia 1.37 1.31 1.30 0.02 1.187 0.093 Mexico 3.28 3.41 3.45 3.52 0.07Iran, Islamic R. 3.58 3.60 3.76 0.14 3.359 0.264 Canada 2.46 2.57 2.68 2.59 -0.09Iraq 1.22 2.41 2.53 UK 2.81 2.74 2.98 3.01 0.03Kuwait* 1.83 1.71 1.72 0.02 1.836 0.144 Norway 3.23 3.28 3.10 3.06 -0.04Libya 1.43 1.35 1.36 0.04 1.227 0.096 Other OECD 1.35 1.42 1.26 1.33 0.07Neutral Zone 0.54 0.53 0.57 Afrca 2.64 2.73 2.74 2.71 -0.03Nigera 2.28 1.96 2.01 -0.02 1.885 0.148 China 3.12 3.19 3.19 3.20 0.01Qatar 0.65 0.62 0.67 0.03 0.593 0.047 OtherAsia 2.11 2.11 2.16 2.19 0.03Saudi Arabia* 8.08 7.96 7.87 0.13 7.438 0.585 FSU 7.07 7.20 7.35 7.27 -0.08UAE 2.25 2.17 2.19 0.03 2.000 0.157 Eastem Europe 0.21 0.20 0.19 0.19 0.00Venezuela 3.22 2.98 2.93 0.09 2.720 0.125 Lain Amerca 3.25 3.43 3.86 3.90 0.04Total Crude 27.28 27.40 27.73 0.51 22.976 1.716 Middle East 1.93 1.89 1.87 1.89 0.02Excluding Iraq 26.06 24.99 25.20 0.51 22.976 1.716 Processing gain 1.52 1.57 1.66 1.69 0.03NGLs 2.83 2.88 2.90 Total non-OPEC 43.57 44.39 44.64 44.64 0.00Total OPEC 30.12 30.29 30.63 Note: Includes natural gas liquids (NGLs), unconventonal,*Quota includes share of Neutral Zone producton. and other supply sources.Source: IEA and OPECNA. Source: IEA

Worldc Petroleum Demand and Supply(Millions of barrels per day)

1995 1996 1997 1098 2098 3098 4Q98 1998 1Q99 2Q99 3099 4Q99 1999Demand

OECD 44.9 46.0 46.7 47.2 45.3 46.6 47.9 46.8 48.0 46.0 47.1 48.6 47.4FSU 4.8 4.4 4.3 4.6 4.2 4.1 4.1 4.3 4.1 4.1 4.0 4.1 4.1Other 20.2 21.3 22.4 22.9 22.9 22.7 22.8 22.7 22.8 23.1 23.1 23.5 23.1Total 69.9 71.7 73.4 74.7 72.4 73.4 74.8 73.8 74.9 73.2 74.2 76.2 74.6

SupplyOECD 21.1 21.7 22.1 22.6 22.0 21.3 21.6 21.9 21.6 21.4 21.6 22.3 21.7FSU 7.1 7.1 7.2 7.3 7.2 7.2 7.3 7.3 7.3 7.2 7.1 7.0 7.1Other* 14.3 14.8 15.1 15.4 15.4 15.4 15.7 15.4 15.7 15.6 15.7 15.7 15.8OPEC** 27.7 28.5 30.0 31.3 31.0 30.2 30.3 30.7 30.6 29.0 29.0 29.0 29.4Total 70.1 72.0 74.3 76.5 75.6 74.1 74.9 75.3 75.3 73.2 73.4 74.0 74.0

Stock changeOECD -0.3 0.0 0.3 -0.2 1.7 0.5 -0.7 0.3Other/misc.** 0.5 0.2 0.6 2.1 1.5 0.2 0.8 1.1Total 0.2 0.3 0.9 1.8 3.2 0.6 0.1 1.4 0.4 0.0 -0.8 -2.2 -0.6

*Includes processing gains (1.6 mb/d in 1998 and 1.7 mb/d in 1999). **lncludes NGLs (2.8 mb/d in 1998 and 2.9 mb/d in 1999).***lncludes floafing storage, oil in transit, and miscellaneous to balance.Note: Includes natural gas liquids (NGLs), nonconventonal, and other supply sources.Source: ItA data and estimates, and World bank torecasts.

Global SummaryActual -Annual Growth Rate (%O)-

World Balance (mb/d) 1970 1980 1990 1996 1997 1998 1970-80 1980-90 1990-98Producton 48.5 63.9 66.9 72.0 74.3 75.3 2.9 1.0 1.6Consumpton 46.7 62.7 66.3 71.7 73.4 73.8 3.1 0.9 1.5Stock Change and Misc. 1.8 1.2 0.6 0.3 0.9 1.4

Actual ForecastPrices ($1bbl) 1995 1996 1997 1998 1999 2000 2001 2005 2010

Current 17.17 20.42 19.17 13.07 14.50 16.50 17.00 18.00 19.00Constant 1990 14.41 17.88 17.69 12.54 13.83 15.49 15.58 14.93 13.93

Source: BP and lEA, and World Bank forecasts.

april 1999 19

AGRICULTURE

Cocoa 180 Monthly Prices (,/kg)

Weakness continues in the cocoa market with Indicator

prices reaching a low of 131¢/kg in March. 165 -

Unless demand recovers, prices will remain 150 - LIFFE

weak for the rest of 1999 and possibly into Futures*

2000. Cote d'Ivoire's cocoa sector is expected 135 -

to be fully liberalized by the end of 1999.120 - .. ... . .... ....

Cocoa prices averaged 139¢/kg this quarter, Miar-96 Mar-97 Mar-98 Mar-99 MIar-00down more than 12% from last quarter's average of * Futures purces are end-March expressed in ¢/kg.

159¢/kg, and 17% lower than last year's first quarter World Balance (million tons)average. The bearish mood on prices was evident in 3 W0futures. In London, the second position fell to a lowof £821/ton on March 11, the lowest level since Sep- 2.5tember 1993. New York futures also reached a low of Production

$1,200/ton, the lowest level since May 1994. 2.0 -According to the most recent estimates by the Grindings

International Cocoa Organization (ICCO), the current 1.5

season's crop is expected to produce 2.71 million tons,up 1% from 2.68 million tons in 1997/98 (October to 1.0 - i

September). Following a late start, C6te d'Ivoire, the 1970 1975 1980 1985 1990 1995

world's dominant producer, is expected to produce Source: ICCO

1.10 million tons, slightly down from last season's 1.11 Ending Stocks (million tons)million tons. Ghana's output is also expected to be 40 2.0thousand tons less than last season's 409 million tons. WorldSubstantial recovery is anticipated in Ecuador, where 1.5 -

70 thousand tons (from last season's 3 5 thousand tons)is expected. Indonesia will reach 350 thousand tons 1.0(from 325 thousand tons last season), while Malaysiais expected to reach 85 thousand tons (up from 70 0.5thousand tons last season). ICCO

ICCO also estimates grindings in 1998/99 to be 0.0 -2.80 million tons. Substantial reductions are expected 1970 1975 1980 1985 1990 1995in Russia and Eastern Europe, down 27% and 17%, Source: ICCO

respectively. C6te d'Ivoire is expected to increase Annual Prices (OIkg)grindings (from 205,000 to 240,000). Western Euro- 800 -

pean grindings are expected to remain at their 1997/ 'Forecast98 levels. 600 Constant

Little growth in consumption is expected to take (1990)place in OECD countries where the most cocoa is con- 400

sumed. On the other hand, recent liberalization trends- which in most cases imply that producers will get a 200 -

much higher share ofthe f.o.b. price - may induce some Current

supply response. Thus, prices are not expected to re- 0oI - E

cover in the near-term. Instead, they are expected to 1970 1975 1980 1985 1990 1995 2000 2005 2010

fluctuate around 135¢/kg during 1999 while it will take Source: ICCO and World Bank forecasts.

at least two years before they return to 1998 levels.

20 GLOBAL COMMODITY MARKETS

BEVERAGES COCOA

Other Developments* Bloomberg reported that Sifca, C6te d'Ivoire's larg- Ghana Cocoa Board has expressed a commitment

est cocoa exporter, will merge with a local competi- that Ghanaian farmers will receive at least 60% oftor, Jean Abile Gal. The new company is expected to the world price by 2002. At that point, the market ishandle one-third of the country's cocoa exports and a expected to be liberalized.quarter of its coffee exports. Currently there are 62 * C6te d'Ivoire's liberalization process continues asregistered coffee and cocoa exporters in C6te d'Ivoire. planned. Caistab, the parastatal which handles mar-Sifca processes about 250,000 tons of cocoa per year. keting and trade of cocoa, has been liquidated and

* Cocoa growers of C6te d'Ivoire and Ghana are still its workforce has been reduced to 600 employeesreceiving the lowest share of f.o.b. prices compared (from 1,050), with a further reduction to 150.to their Brazilian and Malaysian counterparts. How- Caistab's debt is now about 21 billion CFA (aboutever, the gap has narrowed in recent months, and is 3 5 million dollars). The government of C6te d'Ivoireexpected to be eliminated for C6te d'Ivoire after lib- will allow donors to pay off all of this debt by Octo-eralization is complete. On the other hand, the ber 1, 1999.

Production and Grindings Trade1995196 1996/97 1997/98 1998/99 1995/96 1996/97 1997/98 1998/99

Gross Production (000 tons) Exports (000 tons)Cote d'lvoire 1,200 1,108 1,113 1,100 Cote d'lvoire 1,038 928 931 966Ghana 404 323 409 370 Ghana 331 267 336 311Indonesia 285 325 325 350 Indonesia 224 264 148 212Nigeria 158 160 165 180 Nigeria 147 137 141 142Brazil 231 185 170 160 Cameroon 93 95 86 91Cameroon 135 126 127 130 World 2,116 1,942 1,912 1,990Malaysia 115 100 70 85 Imports (000 tons)Ecuador 103 103 35 70 US 445 353 402 400Dominican R. 55 52 58 48 Netherlands 405 464 300 389Colombia 50 50 45 46 Germany 299 327 302 309World 2,916 2,711 2,683 2,707 UK 248 176 207 210

Grindings (000 tons) France 117 111 100 110Netherlands 385 402 425 435 Singapore 88 92 85 89US 342 394 399 395 Russian Fed. 75 85 83 81C6te dIlvoire 140 160 205 240 Italy 71 71 73 72Germany 266 240 226 205 Belgium 45 54 66 55Brazil 205 180 185 185 Spain 50 49 66 55UK 191 172 174 170 Estonia 5 65 81 50France 113 106 100 107 Japan 49 54 47 50Malaysia 95 95 100 100 Canada 39 34 45 39World 2,713 2,751 2,791 2,800 World 2,191 2,225 2,178 2,198

Source: ICCO Source: ICCO and World Bank.

Global SummaryActual - Est.- -Annual Growth Rate f%J -

World Balance (000 tons) 1970/71 1980/81 1990/91 1996/97 1997/98 1998/99 1970-80 1980-90 1990-97Production 1,554 1,695 2,506 2,711 2,683 2,707 0.9 3.9 0.6Grindings 1,418 1,556 2,335 2,751 2,791 2,800 0.9 4.1 1.5Exports 1,186 1,126 1,733 1,942 1,912 1,990 -0.5 4.3 1.1Ending Stocks 497 675 1,791 1,399 1,210 1,090 3.1 9.8 -4.0

Actual ForecastPrices (¢/kg) 1995 1996 1997 1998 1999 2000 2001 2005 2010

Current 143.2 145.6 161.9 167.6 135.0 145.0 160.0 200.0 210.0Constant 1990 120.2 127.7 149.4 160.9 128.8 136.2 146.6 165.9 154.0

Note: Production refers to gross crop. Quantities refer to cocoa beans. Crop year begins October 1, 2001.Source: ICCO and World Bank.

april 1999 21

AGRICULTURE

Coffee Monthly Prices (,/kg)

Arabica and robusta prices fell 5.7% and3.9%, respectively, this quarter mainly due to 450 -

the Brazilian real's 40% devaluation. Prelimi- CSCE

nary estimates put the global 1999/00 coffee 300 Futures*

crop at 102.5 million bags. Brazil's output is 150expected to be about 24 million bags. Robusta LIFFE

Futures*

The arabica indicator price for January-March Mar-96,Mar-97,Mar-98,Mar,99 ,Mar-00averaged 238¢/kg, down from 252¢/kg in the previ- * Futures prices are end-March expressed in i/kg.

ous quarter, and 37% lower than last year's first quar- Source: ICO, LIFFE, and CSCE.ter average. Robusta prices averaged 172.7¢/kg this 120 World Balance (million tons)quarter, down from 179.7¢/kg in the last quarter of Production

1998. This quarter's news was dominated by Brazil's 100

devaluation of the real in January. The currency wasfloated, resulting in a depreciation of 40% over the 80US dollar.

The depreciation prompted Brazilian exporters 60Eto vigorously increase coffee exports and reap the ben- V

efits of high domestic prices before any currency re-bound. In February, Brazil exported 1.85 million bags, 1970 1975 1980 1985 1990 1995almost twice as much as in the same month in 1998. Source: ICO and USDA.

The Brazilian Association of Coffee Exporters Arabica Annual Prices (p/kg)(Abecafe) said that exports in March are expected to 1,200 -be around 1.7 million bags, compared to 0.73 million Constant Forecast

bags in March 1998. 900 (

Global coffee production in 1998/99 is expectedto reach 106.8 million bags, second only to the 1986/ 60087 crop. Some preliminary estimates released by theAssociation of Coffee Producing Countries (ACPC) 300 -indicate that the 1999/00 crop is going to be around102.5 million bags, 4% lower than the 1998/99 crop. - Current

With global consumption estimated between 98 and 1970 1975 1980 1985 1990 1995 2000 2005 2010

99 million bags, the market is expected to register a Source: ICO and World Bask forecasts.

surplus of 3.5 million bags in the 1999/00 season. Robusta Annual Prices (,/kg)Brazil, the world's dominant producer, is expected to 1,200 -produce between 23.15 and 24.74 million bags next Forecast

season (down from 35.6 million bags in 1998/99). 900India's Coffee Board reported that next season's cropwill be about 4.8 million bags, up from 3.8 million 600 -bags in 1998/99.

With production expected to exceed consump- 300 -tion by an estimated 8 to 9 million bags, prices areunlikely to recover soon. Arabica and robusta prices 0 Iareexpectedto average231¢/kg and l63¢/kgfor 1999. 1970 1975 1980 1985 1990 1995 2000 2005 2010Depending on the actual size of next season's crop, Source: ICO and World Bask forecasts.

some recovery may take place in 2000.

22 GLOBAL COMMODITY MARKETS

BEVERAGES COFFEE

Other Developments* A two-week coffee festival (sponsored by the ICO) The London International Financial and Futures Ex-

took place in China (Beijing and Shanghai) in March change plans to upgrade its coffee contract on Feb-1999. Its purpose was to promote coffee consump- ruary 1, 2000. The new contract will make a dis-tion in China, which has traditionally been a tea tinction between coffee beans with the majority ofmarket. their surface covered in mould and those covered

* After establishing the Coffee Futures Exchange in only partially.Bangalore, India's Coffee Board unveiled plans to * C6te d'Ivoire's coffee sector has been liberalized.expand the domestic market base of coffee with as- Producers are expected to be the main beneficiariessistance from the private sector, according to The of liberalization as they will receive higher prices,Public Ledger. Indian coffee consumption has been from 50% of f.o.b. prior to liberalization to aroundstagnant at 840,000 bags during the last decade. 80% following liberalization.

Production (000 bags) Stocks and Consumption1995/96 1996/97 1997/98 1998199 1995/96 1996/97 1997/98 1998199

Brazil* 16,800 28,000 23,500 35,600 Ending Stocks (000 bags)Colombia* 12,939 10,779 11,932 12,500 Brazil 16,000 14,128 11,278 15,278Indonesia 5,800 7,900 7,200 6,800 Colombia 6,328 4,420 3,929 3,669Vietnam 3,917 5,500 6,667 6,333 Congo, D. R. 239 365 790 765Mexico* 5,400 5,300 4,950 4,950 Costa Rica 1,149 1,200 1,050 760India 3,717 3,417 3,833 3,835 Cote d'lvoire 1,499 2,915 1,885 653C6te d'lvoire 2,900 5,333 4,080 3,750 Cameroon 234 529 570 570Uganda 4,200 4,297 3,000 3,600 Kenya 638 367 592 519Ethiopia* 3,800 3,500 3,500 3,500 Indonesia 851 298 368 370Guatemala* 2,827 4,141 3,982 2,825 World 32,699 28,875 25,054 27,002Honduras* 2,254 2,279 2,980 2,260 Consumption (000 bags)Costa Rica* 2,595 2,376 2,400 2,165 US 17,600 18,490 18,130 18,290Peru* 1,811 1,583 1,780 1,900 Brazil 10,230 10,880 10,880 11,320El Salvador* 2,325 2,498 2,040 1,790 Germany 9,480 9,440 9,260 9,300Venezuela* 1,067 843 981 1,380 Japan 5,750 5,820 5,800 5,710Cameroon 581 1,432 1,417 1,200 France 5,230 5,350 5,290 5,300PNG 1,002 1,089 1,080 1,100 Italy 4,640 4,670 4,650 4,700Congo, D. R. 1,000 950 1,143 1,000 UK 2,380 2,440 2,380 2,419Thailand 1,317 1,403 1,383 1,000 Canada 2,800 2,960 2,920 2,291World 88,749 103,696 97,675 106,800 World 96,300 99,500 99,400 98,000

Source: ICO and USDA. Source: ICO and USDA.

Global SummaryActual -Est. - -Annual Growth Rate (%) -

World Balance (000 bags) 1970/71 1980/81 1990/91 1996/97 1997/98 1998199 1970-80 1980890 1990-98Producton 64,161 86,174 88,749 103,696 97,675 106,800 2.95 0.29 1.48Consumpbon 71,536 79,100 96,300 99,500 99,400 98,000 1.01 1.97 0.14Exports 54,186 60,995 76,163 84,248 77,264 79,771 1.18 2.22 0.37Ending Stocks n.a. 30,979 45,096 28,875 25,054 27,002 na 3.75 -4.10

Actual ForecastArabica Prices (¢/kg) 1995 1996 1997 1998 1999 2000 2001 2005 2010

Current 333.2 269.4 416.8 298.1 231.0 243.0 236.0 254.0 265.0Constant 1990 279.6 236.4 384.6 286.1 220.4 228.2 216.3 210.7 194.3

Robusta Prices (¢/kg)Current 277.1 180.6 173.6 182.3 163.0 172.0 176.0 186.0 192.0Constant 1990 232.4 158.4 160.2 174.9 155.5 161.5 161.3 154.3 140.8

*Indicates that the country is prmarily an arabica producer. One bag equals 60 kg. Quantites refer to country-specific crop years.Source: ICO, USDA, and Word Bank.

april 1999 23

AGRICULTURE

Tea 290 Monthly Prices (,/kg)

Russian imports declined again this quarter,adding further downward pressure on Co- 250 -

lombo and Calcutta auctions, which fell 12% Average

and 14%, respectively. 210 -

The three auction prices averaged 167.3¢/kg dur- 170 -

ing the first quarter, down 6.1% from the previous 1quarter. Colombo auction prices fell almost 12% from ,last quarter, mainly reflecting reduced exports to the Mar-95 Mar-96 Mar-97 Mar-98 Mar-99

FSU. The Calcutta auction price registered a quar- Source: ITC

terly decline of almost 14%. The Mombasa auction's World Balance (million tons)price, on the other hand, increased by 9%. 3.5 -

World tea production in 1998 reached a recordhigh of 2.89 million tons, up 5% from 1997. Produc- 2.8 -

tion in India, Kenya, and Sri Lanka totaled, 860, 280, Production

and 271 thousand tons, respectively, in 1998. These 2.0

figures are 7.3% (India), 33.3% (Kenya) and 3.7% (SriLanka) higher in 1997. 1.3 - - Net Imports

India's 1999 output may decline due to longerthan usual hot and dry weather in Assam and West 0.5 I IBengal. Production in Kenya for the first quarter was 1970 1975 1980 1985 1990 1995

also lower compared to last year following an extended Source: FAO and ITC.

period of dry weather which lasted until February. On UK Ending Stocks (thousand tons)the other hand, output in Sri Lanka for January reached 100 Ea record high of 24.6 thousand tons. I Warehouses

Sri Lanka maintained its position as the world's 75 -largest tea exporter in 1998 with exports totaling 271thousand tons. Kenya, the largest exporter in 1995 and 50

1996, was second, exporting 264 thousand tons. India, 50 salersthe largest producer with a significant domestic mar- 25s-

ket, followed with 205 thousand tons. India's domestic 25

consumption last year was about 650 thousand tons,whereas Sri Lanka's was around 30 thousand tons. 0 -

Demand for Indian tea slowed this quarter as 1970 1975 1980 1985 1990 1995Source: ITC

exports to Poland and the FSU dropped following a Annual Prices (¢/kg)large inventory build-up. Sri Lanka's tea exports in 450January of this year fell about 20% compared to Janu- Forecast

ary 1998 as exports to FSU declined by more than 350 -

20%. Demand for Kenyan tea firmed in March inanticipation of lower supplies. Demand from Paki- 250 -

stan was particularly strong. Demand from other ma-jor buyers of Kenyan tea, such as the UK, Sudan, 150 -Yemen, and Middle Eastern countries also firmed. urrent

We projectthe 3-auction average to fluctuate be- 50 I . Itween 170¢/kg and 180¢/kg forthe remainder of 1999 1970 1975 1980 1985 1990 1995 2000 2005 2010and possibly to drop below the 170-mark next year. Source: ITCandWorldBankforecasts.

Some recovery is expected to take place in 2001.

24 GLOBAL COMMODITY MARKETS

BEVERAGES TEA

Other Developments* The Indian government decided to abolish an 8% an agreement with the Russian Tea and Coffee As-

excise duty on packaged tea and impose an ex- sociation to assist Russian firms with importing In-cise duty of 2 rupees per kilogram on bulk tea in dian tea. Russia currently accounts for 44% or 90February. Following the announcement, shares thousand tons of India's tea exports.of Indian tea companies rose sharply. This deci- * Sri Lanka and India signed a free trade agreementsion, however, is unlikely to benefit tea produc- which promotes greater access to each other's mar-ers who only receive auction prices that are al- kets. The implementation, however, has been de-ready very low. layed due to the difference in views on which items

* The Sri Lankan govemment offered an insurance to exempt, one of which is tea. India, which cur-scheme to local exporters to alleviate cash short- rently imposes a 19% import duty on Sri Lankanages due to delays in payments from Russia, the larg- tea, opposed the tax exemption on tea fearing thatest importer of Sri Lankan tea. Sri Lankan tea, which is less expensive, may domi-

* In December 1998, the Tea Board of India signed nate the domestic tea industry.

Production and Crop Areas Trade1995 1996 1997 1998 1994 1995 1996 1997

Production (000 tons) Exports (000 tons)India 753.9 780.0 810.0 870.0 Sri Lanka 224.2 235.0 233.6 257.3China 609.4 616.5 636.1 648.1 China 179.7 166.6 169.7 202.5Kenya 244.5 257.2 220.7 294.0 India 149.3 163.7 160.0 200.7Sri Lanka 246.0 258.4 270.9 281.0 Kenya 183.1 237.5 244.2 194.0Indonesia 154.0 169.4 150.8 152.1 Indonesia 84.9 79.2 101.5 66.8Turkey 102.7 114.5 120.8 120.8 Argentina 43.2 41.1 41.3 56.4Japan 84.8 88.6 91.2 91.2 Malawi 38.7 32.6 36.7 49.2Iran, Is. Rep. 54.4 62.1 62.1 62.1 Bangladesh 23.6 25.4 26.2 25.2Bangladesh 52.0 47.7 53.3 57.0 Tanzania 18.6 20.5 18.4 19.0Argentina 47.1 47.1 48.5 48.5 World 1,032.6 1,080.1 1,155.3 1,155.9Malawi 34.2 37.2 43.9 45.0 Net Imports (000 tons)World 2,616.3 2,712.3 2,757.6 2,893.4 Russian Fed. 130.6 161.6 160.1 197.3

Crop Areas (000 hectares) UK 148.4 136.0 148.5 150.5China 888.1 880.0 900.0 900.0 Pakistan 106.5 115.7 110.7 86.9India 425.0 425.0 440.0 440.0 US 96.1 83.3 89.2 81.2Sri Lanka 189.0 187.6 187.6 187.6 Egypt 56.9 80.0 65.0 77.9Kenya 111.3 113.7 113.9 115.0 Japan 41.0 45.3 48.4 52.1Indonesia 113.4 108.5 108.1 109.7 Morroco 34.0 37.6 28.4 35.0World 2,306.3 2,291.6 2,332.4 2,338.6 World 1,042.9 1,077.1 1,121.8 1,152.4

Source: FAO and World Bank. Source: ITC and World Bank.

Global SummaryActual -Est.- -Annual Growth Rate (%)-

World Balance (000 tons) 1970 1980 1990 1996 1997 1998 1970-80 1980-90 1990-97Production 1.3 1.9 2.5 2.7 2.8 2.9 4.2 3.2 1.3Net Imports 0.6 0.9 1.1 1.1 1.1 1.1 3.0 2.9 -0.1Ending Stocks 113.9 91.3 48.4 39.2 37.2 38.1 -1.2 -4.1 -2.9

Crop Area (000 hectare) 1,668.3 2,368.5 2,263.0 2,291.6 2,332.4 2,338.6 4.0 -0.9 0.3Yields(hg/hectare) 7,713 7,995 11,161 11,836 11,823 12,146 0.2 4.3 1.0

Actual ForecastPrices (¢/kg) 1995 1996 1997 1998 1999 2000 2001 2005 2010

Current 148.9 166.1 206.0 204.6 177.0 168.0 171.4 179.0 198.0Constant 1990 124.9 145.7 190.1 196.4 168.9 157.8 157.1 148.5 145.2

Note: Ending stocks refer to stocks in the UK.Source: ITC, FAO, and World Bank forecasts.

april 1999 25

AGRICULTURE

Fats and Oils Monthly Prices ($/ton)

The World Bank's oils index declined by 5.1 We0ghted

9. 7%, and 9.6% in the first three months of 660 - iced

1999. With continuedproduction increases, itis doubtful whether the quarterly average of 590 -

$562/ton will be sustained throughout the 520 -

remainder of 1999.

4 50 . .. . ,.. .. . . |. . .. . . .... .,.. .. ,,.,. , .... .... ..The World Bank's oil weighted average price Mar-95 Mar-96 Mar-97 MNr-98 Mar-99

dropped 15% this quarter to $562/ton from $664/ton Source: World Bank

last quarter. This is 13% below last year's first quar- World Balance (million tons)ter average. The global output of 17 fats and oils is 120 -

expected to increase 2.61 million tons this season (Oc-tober to September), for a record of 104.49 million 90 -tons. The increase is slightly below the preceding three Production

seasons' average of 2.9 million tons. Most of the in- 60

crease is expected to come from rapeseed and sun-flower oils (6.6%), soybean oil (4.2%), and palm oil 30 -(2.1%). Lauric oils production will fall 10.8%. Exports

Exports are expected to be 33.0 million tons in 0 - i1998/99, down from 33.2 million tons in 1997/98. The 1970 1975 1980 1985 1990 1995

bulk of trade will be comprised of palm and soybean Source: Oil World

oils (35% and 23%) followed by sunflower and rape- Ending Stocks (million tons)seed oils (10% and 7%). Ending stocks are expected 13

to drop to 11.24 million tons this season from 11.61 Worldmillion tons in the last season, reducing the stock-to- 10use ratio from 11.3% to 10.7%, the second lowest inthe last three decades. 7

The first estimates for the 1999/00 season forsome oilseeds have already been reported in Oil World. 4

The first major oilseed crops to be harvested will be us and EU

rapeseed/canola. Current prospects indicate an in- 1 .crease of 3.5 million tons; the global 1998/99 esti- 1970 1975 1980 1985 1990 1995

Source: Oil Worldmate is expected to be 37.08 million tons. China,Canada, and India are the world's leading canola pro- Annual Prices ($/ton)ducers with shares of 22.3%, 20.5%, and 16.3%, re- 2,000 - Constant

spectively. On the other hand, the US Department of Cs(1990) ForecastAgriculture noted that American farmers are expected 1,500 -to plant an estimated 73.1 million acres of soybeansthis year, up from last year's 72.4 million acres. 1,000 -

Despite the low stock-to-use ratio, the expectedexpansion of palm oil production -along with goodpros- 500pects for other maj or oilseeds - will put some more pres- Curent

sure on prices. The final direction will depend on when 0 - land how much demand picks up. We expect the oil in- 1970 1975 1980 1985 1990 1995 2000 2005 2010

dex to be around of $520/ton, an average that is likely to Source: WorldBank

be maintained for the next two to three seasons.

26 GLOBAL COMMODITY MARKETS

FATS, OILS, AND OILSEEDS FATS AND OILS

Other Developments* Refined deodorized bleached (RDB) palm olein and 1998/99 production shares are: Argentina (25.1%),

palm oil are to be included in the list of goods im- Russia (11.5%), the US (9.1%), andUkraine (8.6%).ported by the private sector, following the new im- * Up to one million hectares of cropped area haveport policy change announced on March 31 by the been damaged in Argentina due to severe floods ingovernment of India, according to Oil World. How- recent weeks. While all oilseeds will be affected,ever, the government increased the import duty from sunflowerseeds may be the worst hit.16.5% to 38.5% for RDB palm oil. The 16.5% duty * It appears that a compromise forreforming the Com-is still valid for other vegetable oils. The higher mon Agricultural Policy (CAP) has been reachedimport tariff on RDB palm oil was introduced to following the EU's proposal, AGENDA 2000. Onprotect local manufacturers. Analysts believe, how- March 26, the Commission agreed to reduce areaever, that granting import licenses to the private payments for oilseeds from the present level of 94.24sector may not be of much benefit. euro/ton to 63 euro/ton within a 3-year period. The

* The government of Ukraine is considering impos- reduction, which is not crop-specific, will take placeing export restrictions on sunflowerseed. Ukraine in three steps: 12.5% in 2000/01, 9.37% in 2001/is the fourth largest sunflowerseed producer. The 02, and 9.37% in 2002/03.

Production, Exports, and Stocks of the 17 Major Fats and Oils- Production (million tons)- -Exports (million tons) - - Ending Stocks (million tons)-

Fats and Oils 1996197 1997/98 1998/99 1996/97 1997/98 1998199 1996/97 1997/98 1998/99Soybean 21.03 23.16 24.13 6.68 7.75 7.62 2.44 2.40 2.40Palm 17.49 16.96 17.32 11.87 11.66 11.54 3.01 2.43 2.41Rapeseed 11.48 12.21 13.08 1.79 2.08 2.25 1.08 1.13 1.22Sunflower 9.14 8.66 9.17 3.24 3.00 3.26 0.96 0.86 0.89Tallow 7.41 7.68 7.77 1.96 2.23 2.32 0.53 0.56 0.54Lard 5.97 6.20 6.37 0.15 0.17 0.18 0.39 0.42 0.43Butter 5.70 5.73 5.80 0.63 0.57 0.58 0.70 0.67 0.66Groundnut 4.51 4.38 4.81 0.25 0.26 0.28 0.47 0.41 0.41Cotton 4.03 4.05 3.80 0.22 0.23 0.21 0.31 0.29 0.27Coconut 3.15 3.45 2.81 1.75 2.12 1.39 0.38 0.60 0.37Olive 2.85 2.59 2.28 0.46 0.47 0.50 0.90 1.07 0.86Palm Kernel 2.18 2.18 2.22 1.04 1.05 1.16 0.26 0.29 0.25Com 1.88 1.96 2.01 0.65 0.78 0.81 0.13 0.14 0.14Fish 1.27 0.83 0.99 0.77 0.46 0.50 0.29 0.16 0.18Linseed 0.65 0.68 0.73 0.14 0.12 0.14 0.08 0.10 0.10Sesame 0.68 0.73 0.71 0.02 0.02 0.02 0.05 0.05 0.04Castor 0.45 0.46 0.50 0.23 0.26 0.27 0.06 0.05 0.07

Total 99.87 101.88 104.49 31.85 33.20 33.00 12.03 11.61 11.24Source: Oil World

Global SummaryActual -Est- -Annual Growth Rate (%o)-

World Balance (mil. tons) 1970/71 1980/81 1990/91 1996197 1997/98 1998/99 1970-80 1980-90 1990-98Producfion 39.78 58.09 80.84 99.87 101.88 104.49 3.8 3.3 2.1Consumphon 39.82 56.80 80.77 99.76 102.38 105.00 3.6 3.5 2.1Exports 8.83 17.76 26.89 31.85 33.20 33.00 7.0 4.1 1.6Ending Stocks 5.18 9.25 12.15 12.03 11.61 11.24 5.8 2.7 -0.6

Actual ForecastWeighted Price ($/ton) 1995 1996 1997 1998 1999 2000 2001 2005 2010

Current 638.8 569.7 574.0 658.8 521.0 519.0 522.0 502.4 520.2Constant 1990 535.9 498.9 529.6 632.3 497.0 487.3 478.3 416.6 381.5

Note: Crop year begins October 1. The price is a trade weighted average of soybean, palm, coconut, and groundnut oils.Source: Oil World and World Bank.

april 1999 27

AGRICULTURE

Coconut Oil Monthly Prices ($/ton)

Despite weather-related crop damage in the c.i.f

Philippines, the market showed signs of weak- R00 - otterdam

ness. Processors have increased use ofpalmkernel oil, which is an effective replacement for 700 -

soap and confection manufacturers. 600 -