fespa economy survey 2 - results

DESCRIPTION

FESPA's Economy Survey 2, in partnership with InfoTrends reveals superb insight and information on the latest trends in the digital printing marketplace. The report is completely free for anyone who would like to download this pdf. Conducted in December 2009 and following Economy Survey 1 in July 2009, this report tracks confidence and change in the market with specific reference to how external economic factors are affecting behaviour and trading in our community.TRANSCRIPT

At the risk of going against the “turn the page” mentality regarding 2009, the following report shows the results of a new research study conducted in December 2009 by InfoTrends in cooperation with FESPA. The subject of the research is the impact of the economic downturn and the strategies that stakeholders in the wide format printing market have employed to help their businesses survive.

1

© 2010 InfoTrendswww.infotrends.com

InfoTrends used its electronic survey software to present 13 questions to manufacturers, dealers of equipment and supplies, and wide format print service providers in the FESPA database. We received 217 completed responses.

The objectives of this study are numerous, but the primary goals are to test and measure the impact of the economic downturn. This study asks specifically how much their businesses have been hurt, if the holiday season has been better or worse than expected and if 2009 was the worst year they have ever had Theworse than expected, and if 2009 was the worst year they have ever had. The second set of goals is about examining which actions companies are employing to deal with the economic downturn and when they expect the market to bounce back.

2

© 2010 InfoTrendswww.infotrends.com

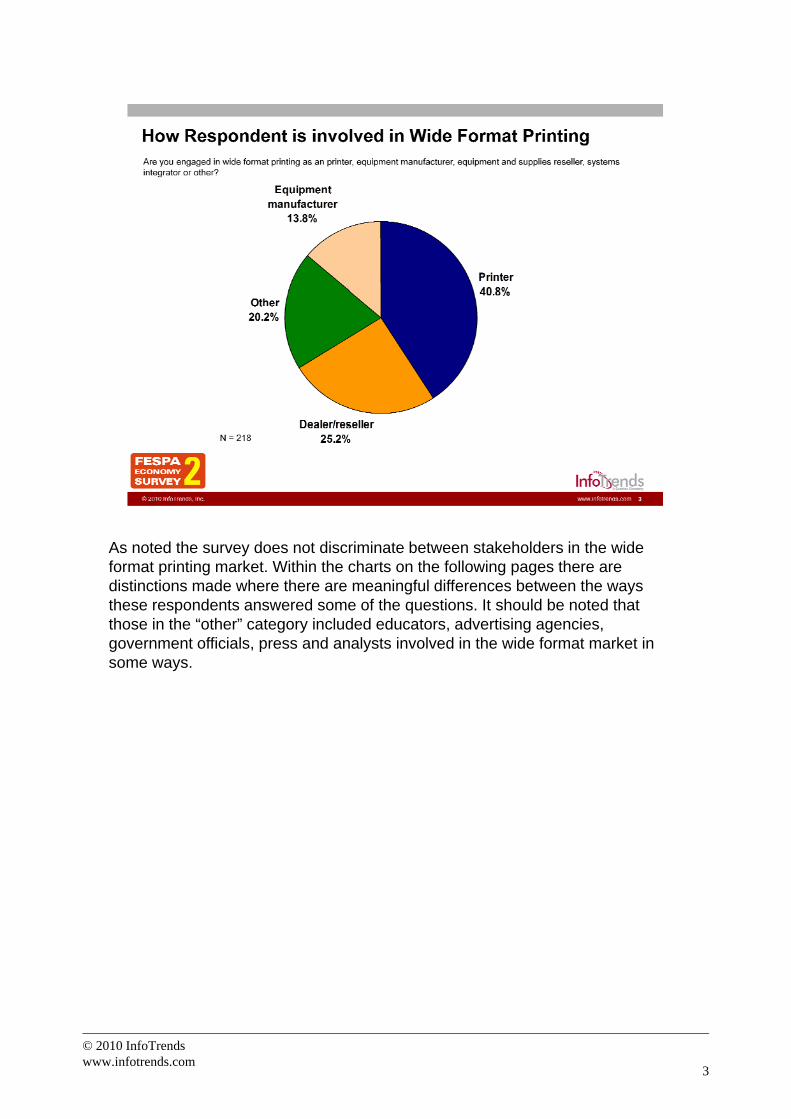

As noted the survey does not discriminate between stakeholders in the wide format printing market. Within the charts on the following pages there are distinctions made where there are meaningful differences between the ways these respondents answered some of the questions. It should be noted that those in the “other” category included educators, advertising agencies, government officials, press and analysts involved in the wide format market in some ways.

3

© 2010 InfoTrendswww.infotrends.com

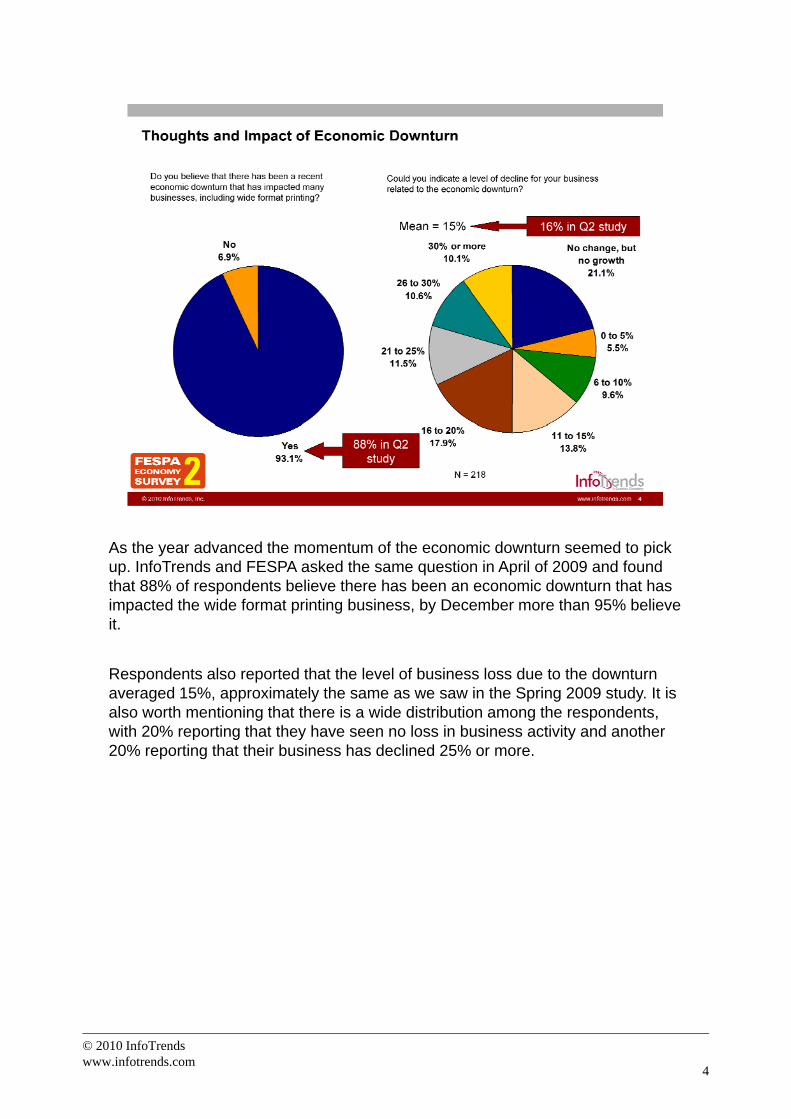

As the year advanced the momentum of the economic downturn seemed to pick up. InfoTrends and FESPA asked the same question in April of 2009 and found that 88% of respondents believe there has been an economic downturn that has impacted the wide format printing business, by December more than 95% believe it.

Respondents also reported that the level of business loss due to the downturn averaged 15% approximately the same as we saw in the Spring 2009 study It isaveraged 15%, approximately the same as we saw in the Spring 2009 study. It is also worth mentioning that there is a wide distribution among the respondents, with 20% reporting that they have seen no loss in business activity and another 20% reporting that their business has declined 25% or more.

4

© 2010 InfoTrendswww.infotrends.com

It is also worth noting that each of the different types of respondents indicated lower business levels of the same magnitude at around 15%. This point is specifically illustrated to show how tightly the supply lines are in the wide format business. InfoTrends believes that one of the biggest impacts of the economic downturn has been a tendency for printers and dealers to work with ever lower inventory levels, which of course has a “ripple effect” on manufacturers and raw materials providers.

5

© 2010 InfoTrendswww.infotrends.com

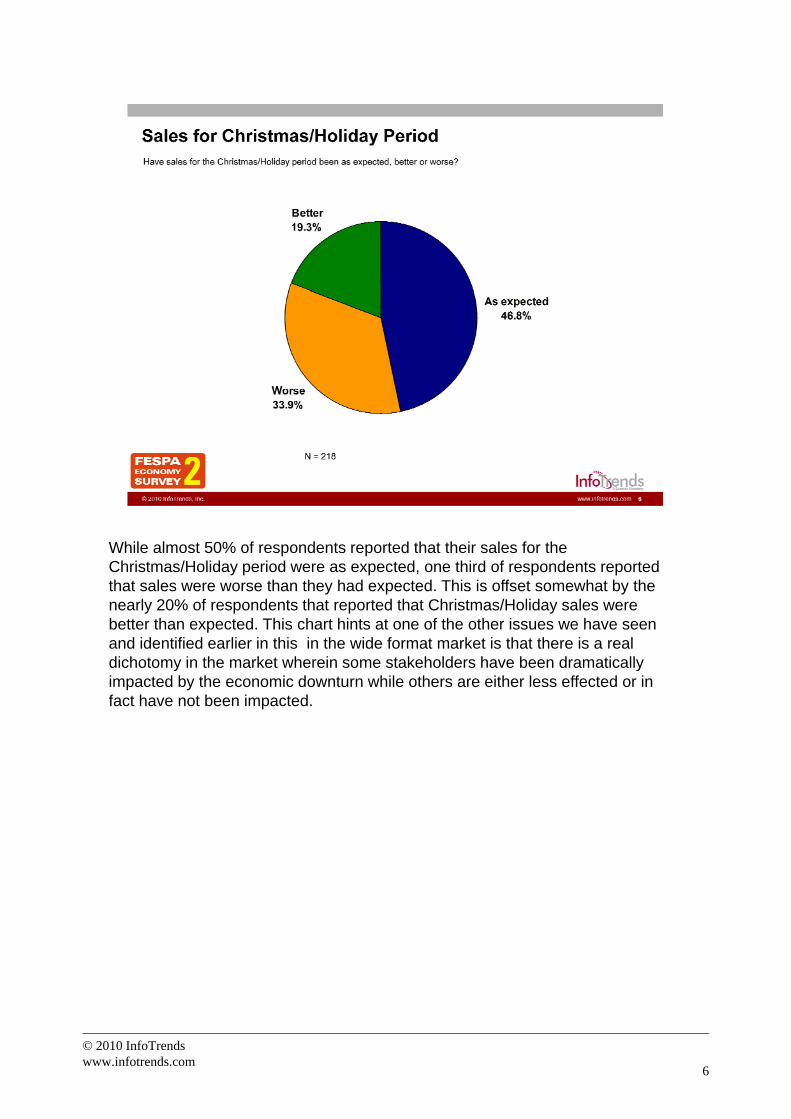

While almost 50% of respondents reported that their sales for the Christmas/Holiday period were as expected, one third of respondents reported that sales were worse than they had expected. This is offset somewhat by the nearly 20% of respondents that reported that Christmas/Holiday sales were better than expected. This chart hints at one of the other issues we have seen and identified earlier in this in the wide format market is that there is a real dichotomy in the market wherein some stakeholders have been dramatically impacted by the economic downturn while others are either less effected or in fact have not been impacted.

6

© 2010 InfoTrendswww.infotrends.com

The wide format market is typically slower in the fourth quarter or at the end of the year. Nearly half of the survey respondents reported that they are seeing fourth-quarter business at the levels they expect and almost 20% reported sales are better than they expect. Unfortunately 34% reported that fourth-quarter sales are worse than they expected.

Almost 60% of the respondents reported that they think 2009 was the worst year they have ever seen in the wide format market. InfoTrends certainly agrees with that assessment, at least in the last nine or ten years as we have seen so muchthat assessment, at least in the last nine or ten years as we have seen so much progress in the adoption of digital wide format printing.

7

© 2010 InfoTrendswww.infotrends.com

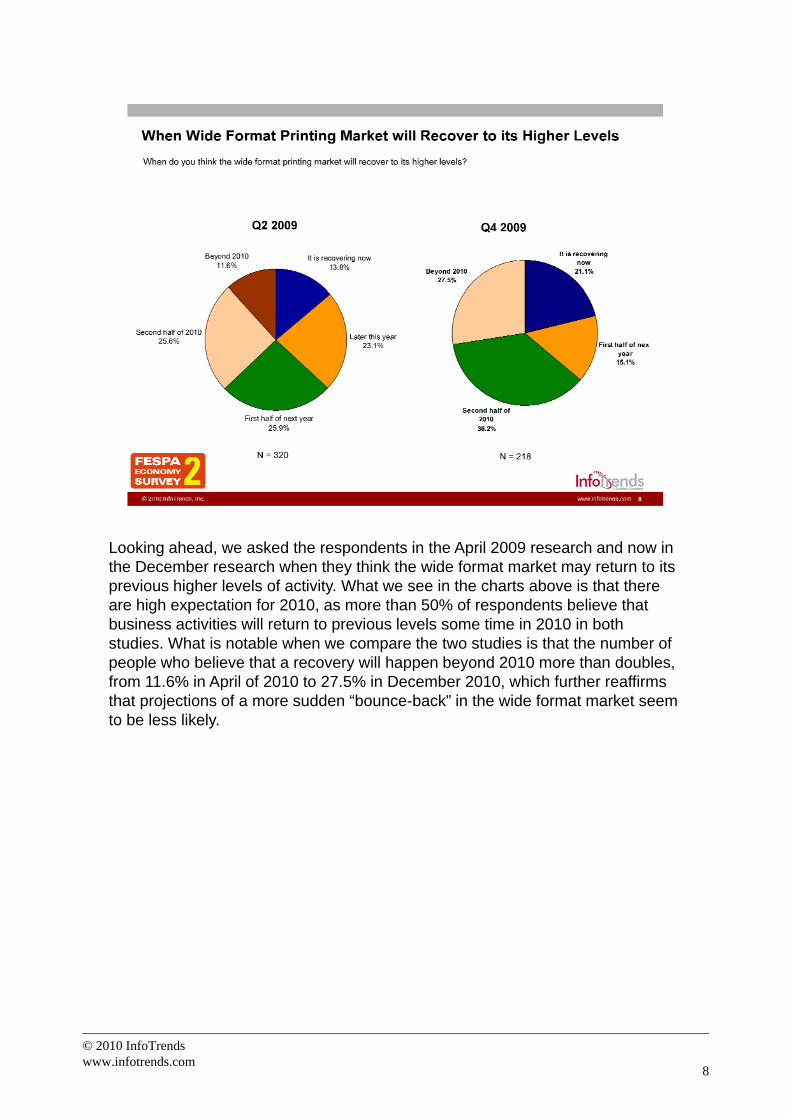

Looking ahead, we asked the respondents in the April 2009 research and now in the December research when they think the wide format market may return to its previous higher levels of activity. What we see in the charts above is that there are high expectation for 2010, as more than 50% of respondents believe that business activities will return to previous levels some time in 2010 in both studies. What is notable when we compare the two studies is that the number of people who believe that a recovery will happen beyond 2010 more than doubles, from 11.6% in April of 2010 to 27.5% in December 2010, which further reaffirms that projections of a more sudden “bounce-back” in the wide format market seem to be less likely.

8

© 2010 InfoTrendswww.infotrends.com

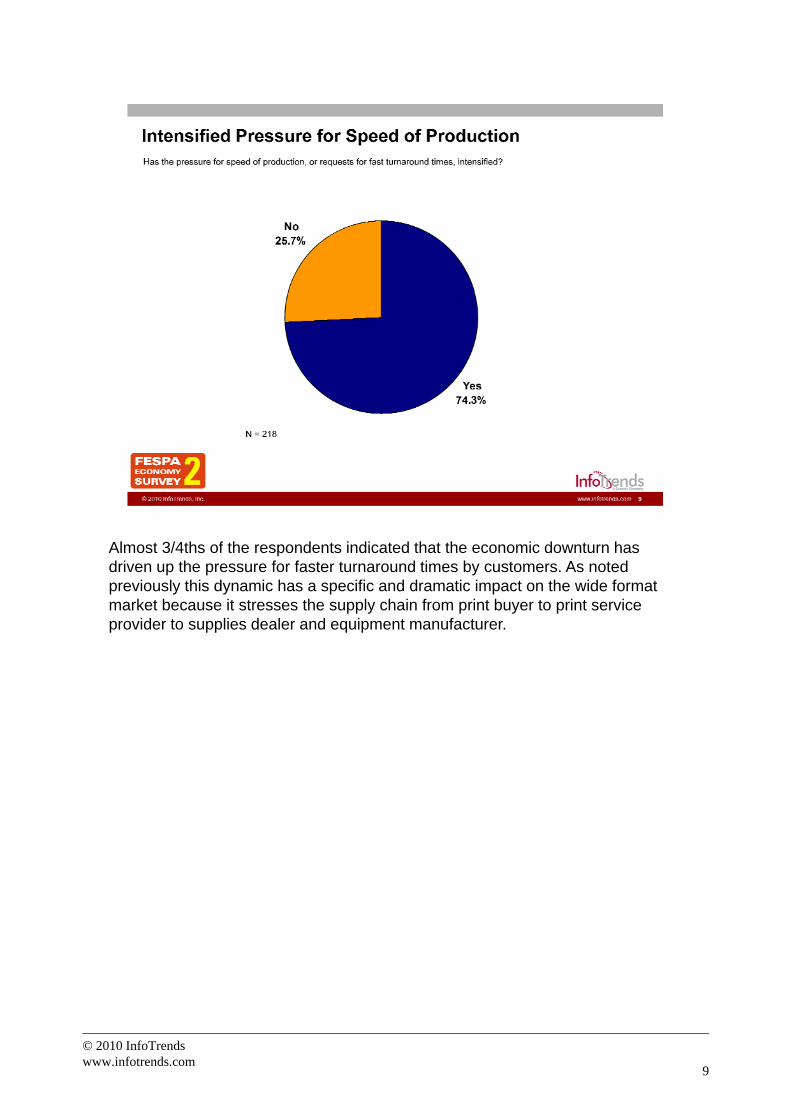

Almost 3/4ths of the respondents indicated that the economic downturn has driven up the pressure for faster turnaround times by customers. As noted previously this dynamic has a specific and dramatic impact on the wide format market because it stresses the supply chain from print buyer to print service provider to supplies dealer and equipment manufacturer.

9

© 2010 InfoTrendswww.infotrends.com

Another issue that has been at the forefront of the wide format market has been sustainability or planet-friendly printing policies and practices. The issue of sustainability is acute in the wide format digital printing market because, unlike some of the other segments of the printing market, so much printing is onto substrates that are difficult to recycle and so much of the ink is solvent-based. However, the cost of using more easily recycled products and different ink formulations is higher, so one of the questions we asked is whether planet-friendly wide format printing has become de-emphasized in light of the economic downturn. While 60% of the respondents reported that it has, InfoTrends believes that it is remarkable that 40% of respondents reported that the downturn has not made planet-friendly printing any less important.

10

© 2010 InfoTrendswww.infotrends.com

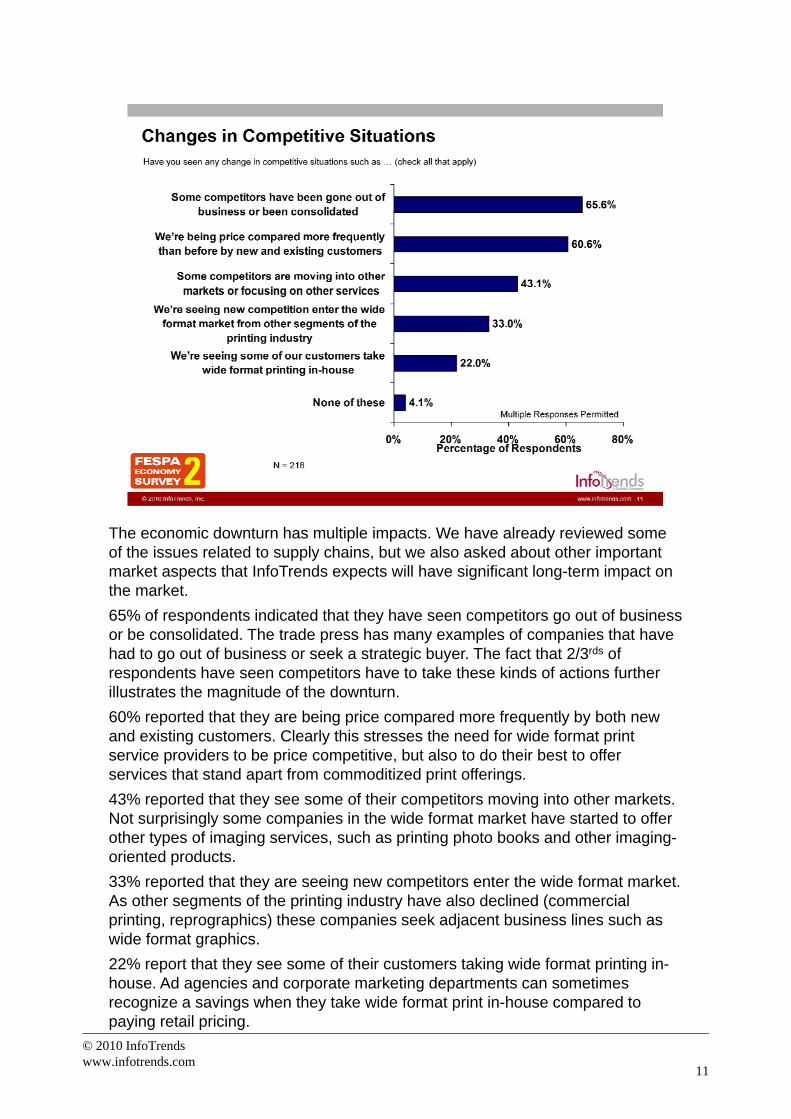

The economic downturn has multiple impacts. We have already reviewed some of the issues related to supply chains, but we also asked about other important pp y , pmarket aspects that InfoTrends expects will have significant long-term impact on the market.

65% of respondents indicated that they have seen competitors go out of business or be consolidated. The trade press has many examples of companies that have had to go out of business or seek a strategic buyer. The fact that 2/3rds of respondents have seen competitors have to take these kinds of actions further illustrates the magnitude of the downturnillustrates the magnitude of the downturn.

60% reported that they are being price compared more frequently by both new and existing customers. Clearly this stresses the need for wide format print service providers to be price competitive, but also to do their best to offer services that stand apart from commoditized print offerings.

43% reported that they see some of their competitors moving into other markets. Not surprisingly some companies in the wide format market have started to offer p g y pother types of imaging services, such as printing photo books and other imaging-oriented products.

33% reported that they are seeing new competitors enter the wide format market. As other segments of the printing industry have also declined (commercial printing, reprographics) these companies seek adjacent business lines such as wide format graphics.

22% t th t th f th i t t ki id f t i ti i

11

© 2010 InfoTrendswww.infotrends.com

22% report that they see some of their customers taking wide format printing in-house. Ad agencies and corporate marketing departments can sometimes recognize a savings when they take wide format print in-house compared to paying retail pricing.

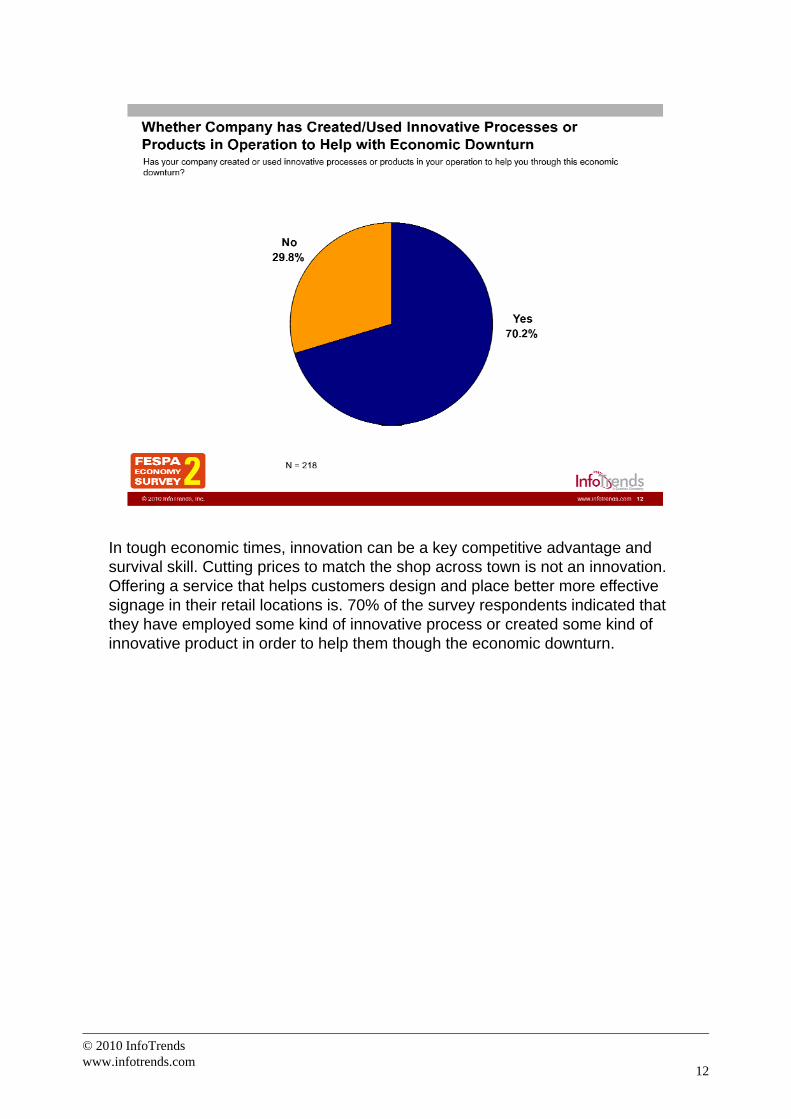

In tough economic times, innovation can be a key competitive advantage and survival skill. Cutting prices to match the shop across town is not an innovation. Offering a service that helps customers design and place better more effective signage in their retail locations is. 70% of the survey respondents indicated that they have employed some kind of innovative process or created some kind of innovative product in order to help them though the economic downturn.

12

© 2010 InfoTrendswww.infotrends.com

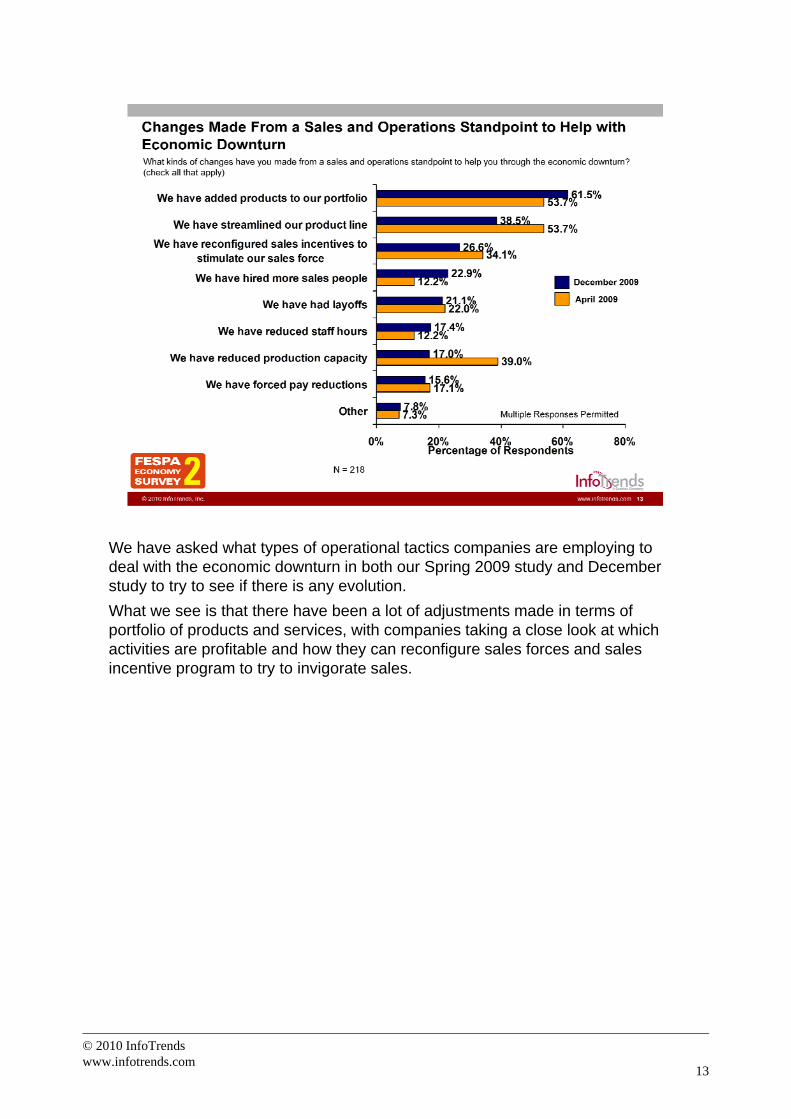

We have asked what types of operational tactics companies are employing to deal with the economic downturn in both our Spring 2009 study and December study to try to see if there is any evolution.

What we see is that there have been a lot of adjustments made in terms of portfolio of products and services, with companies taking a close look at which activities are profitable and how they can reconfigure sales forces and sales incentive program to try to invigorate sales.

13

© 2010 InfoTrendswww.infotrends.com

Page 4 of this report showed a chart that illustrated that more than 20% of the respondents to this economic survey have not experienced a business decline. The chart above shows the responses to the question separated by whether or not the respondent has experienced a decline in business or not. There is not a real big statistical difference between the top four actions – adding products to portfolio, streamlining a product line, reconfiguring sales incentives, and hiring more sales people – that respondents have taken.

The chart shows that those that have not experienced any business decline haveThe chart shows that those that have not experienced any business decline have not had to go through the restructuring in the way of layoffs, reduced staff hours, reduced capacity, and pay cuts. Naturally, business don’t generally do these things unless they are forced to.

So, InfoTrends believes that those 20% of businesses not seeing any loss of business represent those that are the closest to their customers, they are the most technologically advanced and they are the companies that are the best managed continuously which means they have not had to make these drastic strategic andcontinuously, which means they have not had to make these drastic strategic and operational actions to survive in a downturn.

14

© 2010 InfoTrendswww.infotrends.com

The stakeholders in the wide format market have also employed multiple tactics in terms of selling strategies to offset business declines. The one that they employed the most is that they have entered new business areas, perhaps that means they have focused on additional application areas or expended extra effort to try to reach new customers. Similarly, nearly 40% indicated that they have made changes within their go-to-market strategy while another 37% reported that they are getting their sales force to focus on key market segments. At the bottom of the chart there were other sales-specific initiatives including hiring a dedicated sales force or re-assignment of sales forces.

We also see that 33% of respondents have been aggressive with financing and payment terms and 23% have more aggressively used rebates and price promotions.

15

© 2010 InfoTrendswww.infotrends.com

As a result of this study we can put some numbers on what many in the wide format will look back on as the worst year in memory due to the overall economic downturn and its impact on the wide format market.

InfoTrends expects that one of the long-term impacts on the wide format market for all of the industry stakeholders will be the need for operational efficiency. Competing in a dynamic market that has intense competition, continuous technological advancements, and serves a wide array of end users segments means that PSPs, equipment and supplies dealers, and manufacturers all needmeans that PSPs, equipment and supplies dealers, and manufacturers all need to examine their outward service offering for profitability and their own supply chains to manage cash flows. At the same time, it is always important for those stakeholders to be flexible enough to respond to profitable ad hoc opportunities because as we have seen, the economic downturn has even accelerated the demand for higher service levels.

While the requirement for faster and more capable equipment has become a given in the wide format market the research tells us that innovation is seen bygiven in the wide format market, the research tells us that innovation is seen by the market as a key method for a positive outcome for 2010 with new markets and new application areas what most respondents are looking for during this economic downturn. Manufacturers and dealers, who get close to their customers, understand their businesses and help them recognize where the new market opportunities are will likely be more appreciated and successful.

16

© 2010 InfoTrendswww.infotrends.com