inside ferc’s gas market report - platts ferc’s gas market report analysis several major...

TRANSCRIPT

Friday, October 9, 2015

www.platts.com www.twitter.com/PlattsGas NATURAL GAS

INSIDE FERC’s GAS MARKET REPORT

ANALYSIS Several major pipeline expansion projects are scheduled to begin service November 1, the start of the winter season for the gas markets. Some will simply expand pipeline capacity and throughput, increasing takeaway capacity from the Northeast. Others are expected to facilitate incremental production growth.

In total, about 2.44 Bcf/d of incremental capacity is expected to come online through the rest of the year, pushing the total takeaway capacity from the Northeast this year to 3.9 Bcf/d — largely from REX’s Zone 3 East-to-West and TETCO’s Uniontown to Gas City.

The new capacity on REX has supported growth in Utica production; however, utilization has only averaged 79% of project capacity since September 1. The Uniontown to Gas City project has seen flows through the Sarahsville compressor jump from an average of 355 MMcf/d in August to 581 MMcf/d since September 1, though still only a 77% utilization rate based on the listed capacity of 750 MMcf/d.

Bentek Energy, a unit of Platts, expects utilization to increase as winter demand picks up and prices gain strength.

Northeast pipe expansions to boost production as winter season begins

ANALYSIS The upcoming winter in the New England gas market appears likely to be similar to last winter because there have been no major changes in infrastructure and the Federal Energy Regulatory Commission has accepted a similar reliability plan for the region.

The New England winter market has been highly constrained in the past and prone to major price spikes due to pipeline deliverability limitations. Winter cash prices at Algonquin city-gates spiked to as high as $67/MMBtu during the winter of 2013-14, prompting the expansion of a winter reliability program designed to encourage more fuel diversity and alternative supply options.

Last winter’s reliability program included LNG imports, which helped soften natural gas price spikes. The program grants end-of-season compensation for LNG contract volumes that were available for use during the winter but were not called upon to produce energy, giving utilities additional assurance when purchasing supply for the winter.

Last winter’s market was somewhat less volatile, including cash basis highs at Algonquin city-gates that only reached $26/MMBtu despite the retirement of the 563-MW Vermont Yankee nuclear plant and the 805-MW Salem Harbor coal generating station.

New England winter outlook similar to last, with LNG limiting price spikes

M&A Just three months after rejecting a takeover bid from Energy Transfer Equity as not being generous enough, The Williams Companies late last month agreed to be acquired under very similar terms.

The merger, valued at $37.7 billion, would create the third largest energy company in North America and one of the five largest energy companies in the world, the companies said in a joint statement.

Although the deal terms are similar to an unsolicited ETE takeover offer Williams turned down in June, the total value of the merger has shrunk along with the values of both companies. At the time the current deal was announced, it valued Williams at $43.50 per share. While this represents a 4.6% premium to Williams closing share price on September 26, the earlier offer had placed Williams’s stock value at $64 per share.

In another change from that earlier bid, which had been all-stock, ETE sweetened the current deal with a cash component. In the current offer, Williams’ stockholders will have the right to elect to receive either ETC common shares or a combination of cash and shares.

The merger would create a company with more than 100,000 miles of pipeline transporting gas, NGLs and other energy products, and a large network of midstream assets. Energy Transfer owns about 71,000 miles of pipeline and a midstream and processing network that

ETE purchase of Williams to create North American, global energy giant

INsIdE ThIs IssuE

Markets

Gas on top in July, edges out coal 3Production, storage to keep winter prices flat 4

LNG

LNG export developers counter dire forecasts 13Jordan Cove clears environmental hurdle 14

Pipelines

Mountain Valley targets W.Va., Va. end-users 15Algonquin maintenance to continue into November 16

Exploration and Production

E&Ps use varied strategies for downturn: IPAA speakers 17US Interior official pushes Arctic rules despite Shell’s move 18

M&A

Southern positions itself for the future with AGL: CEO 19NextEra Energy completes purchase of NET Midstream 20

Regulation

Bay defends FERC environment policies 22Moeller to leave FERC at month’s end 23

Mexico

US pipeline gas to Mexico, replacing LNG imports 24

(continued on page 26)(continued on page 26)

2

OctOber 9, 2015INSIDe Ferc’S GAS MArKet rePOrt

copyright © 2015 McGraw Hill Financial

Officers of the corporation: Harold McGraw III, chairman; Doug Peterson, President and chief executive Officer; Lucy Fato, executive Vice President and General counsel; Jack F. callahan, Jr., executive Vice President and chief Financial Officer; elizabeth O’Melia, Senior Vice President, treasury Operations.

Gas Market Report Questions?email: NAGas&[email protected]

Manager North America Gas and Power Contentrocco canonica, +1-720-264-6626Anne Swedberg, +1-720-264-6728

EditorsJim Magill, +1-713-658-3229Jasmin Melvin, +1-202-383-2161chris Newkumet, +1-202-383-2141Arjun Sreekumar, +1-713-655-2258Mark Watson, +1-713-658-3214

Editorial Director, North American Gas and Power PricingMark callahan

Editorial Director, North American Gas and Power ContentJames O’connell

Global Editorial Director, PowerSarah cottle

Manager, Advertisement SalesKacey comstock

Friday, October 9, 2015

Chief Content OfficerMartin Fraenkel

Platts PresidentImogen Dillon Hatcher

Advertisingtel : +1-720-264-6631

INSIDE FERC’s GAS MARKET REPORT

copyright © 2015 by Platts, McGraw Hill Financial

To reach Platts: e-mail:[email protected]; North America: tel:800-PLAttS-8; Latin America: tel:+54-11-4121-4810; europe & Middle east: tel:+44-20-7176-6111; Asia Pacific: tel:+65-6530-6430

Restrictions on Use: You may use the prices, indexes, assessments and other related information (collectively, “Data”) in this publication only for your personal use or, if your company has a license from Platts and you are an “Authorized User,” for your company’s internal business. You may not publish, reproduce, distribute, retransmit, resell, create any derivative work from and/or otherwise provide access to Data or any portion thereof to any person (either within or outside your company including, but not limited to, via or as part of any internal electronic system or Internet site), firm or entity, other than as authorized by a separate license from Platts, including without limitation any subsidiary, parent or other entity that is affiliated with your company, it being understood that any approved use or distribution of the Data beyond the express uses authorized in this paragraph above is subject to the payment of additional fees to Platts.

Disclaimer: DAtA IN tHIS PUbLIcAtION IS bASeD ON MAterIALS cOLLecteD FrOM ActUAL MArKet PArtIcIPANtS. PLAttS, ItS AFFILIAteS AND ALL OF tHeIr tHIrD-PArtY LIceNSOrS DIScLAIM ANY AND ALL WArrANtIeS, eXPreSS Or IMPLIeD, INcLUDING, bUt NOt LIMIteD tO, ANY WArrANtIeS OF MercHANtAbILItY Or FItNeSS FOr A PArtIcULAr PUrPOSe Or USe AS tO tHe DAtA, Or tHe reSULtS ObtAINeD bY ItS USe Or AS tO tHe PerFOrMANce tHereOF. A reFereNce tO A PArtIcULAr INVeStMeNt, SecUrItY, rAtING Or ANY ObSerVAtION cONcerNING A SecUrItY Or INVeStMeNt PrOVIDeD IN tHe DAtA IS NOt A recOMMeNDAtION tO bUY, SeLL Or HOLD SUcH INVeStMeNt Or SecUrItY Or MAKe ANY

OtHer INVeStMeNt DecISIONS. NeItHer PLAttS, NOr ItS AFFILIAteS Or tHeIr tHIrD-PArtY LIceNSOrS GUArANtee tHe ADeQUAcY, AccUrAcY, tIMeLINeSS Or cOMPLeteNeSS OF tHe DAtA Or ANY cOMPONeNt tHereOF Or ANY cOMMUNIcAtIONS, INcLUDING bUt NOt LIMIteD tO OrAL Or WrItteN cOMMUNIcAtIONS (WHetHer IN eLectrONIc Or OtHer FOrMAt), WItH reSPect tHeretO.

AccOrDINGLY, ANY USer OF tHe DAtA SHOULD NOt reLY ON ANY rAtING Or OtHer OPINION cONtAINeD tHereIN IN MAKING ANY INVeStMeNt Or OtHer DecISION. PLAttS, ItS AFFILIAteS AND tHeIr tHIrD-PArtY LIceNSOrS SHALL NOt be SUbJect tO ANY DAMAGeS Or LIAbILItY FOr ANY errOrS, OMISSIONS Or DeLAYS IN tHe DAtA. tHe DAtA AND ALL cOMPONeNtS tHereOF Are PrOVIDeD ON AN “AS IS” bASIS AND YOUr USe OF tHe DAtA IS At YOUr OWN rISK.

Limitation of Liability: IN NO eVeNt WHAtSOeVer SHALL PLAttS, ItS AFFILIAteS Or tHeIr tHIrD-PArtY LIceNSOrS be LIAbLe FOr ANY INDIrect, SPecIAL, INcIDeNtAL, PUNItIVe Or cONSeQUeNtIAL DAMAGeS, INcLUDING bUt NOt LIMIteD tO LOSS OF PrOFItS, trADING LOSSeS, Or LOSt tIMe Or GOODWILL, eVeN IF tHeY HAVe beeN ADVISeD OF tHe POSSIbILItY OF SUcH DAMAGeS, WHetHer IN cONtrAct, tOrt, StrIct LIAbILItY Or OtHerWISe.

Permission is granted for those registered with the copyright clearance center (ccc) to photocopy material herein for internal reference or personal use only, provided that appropriate payment is made to the ccc, 222 rosewood Drive, Danvers, MA 01923, phone (978) 750-8400. reproduction in any other form, or for any other purpose, is forbidden without express permission of McGraw Hill Financial. For article reprints contact: the YGS Group, phone +1-717-505-9701 x105. text-only archives available on Dialog File 624, Data Star, Factiva, LexisNexis, and Westlaw.

Platts is a trademark of McGraw Hill Financial

South American LNG is published weekly by Platts, a division of McGraw Hill Financial, registered office: two Penn Plaza, 25th Floor, New York, N.Y. 10121-2298.

spans Texas, the Gulf Coast and the Midcontinent.Williams owns about 33,000 miles of pipeline, concentrated

in the Northeast. Its most important asset, the Transcontinental Gas Pipe Line system, connects the gas-producing regions of South Texas with hungry Northeast markets, including New York City.

The merger also is expected to have a significant impact on the NGL side of the business, said Kendall Puig, an analyst with Platts unit Bentek Energy. “They’re creating a huge company that’s probably more close to the size of Enterprise,” the largest NGL player, she said.

The combination would connect Williams’ gas processing plants and pipelines to the Energy Transfer system, which includes Sunoco, giving the Williams’ assets increased access to the petrochemical complex in Mont Belvieu, Texas, as well storage and marine terminals in the Northeast.

“Sunoco has Mariner East and Marcus Hook that could export NGLs that are being produced in William plants,” Puig said. “It connects Williams’ assets with more export options.”

Williams backs out of deal to buy affiliateIn a joint statement on September 28, the two companies

said their respective boards of directors each had approved the merger.

The ETE merger with Williams was predicated on Williams’ decision to cancel a previously announced merger agreement between Williams and its affiliate Williams Partners. Williams had announced that deal, which it valued at $13.8 billion, in May in a bid to simplify its corporate structure.

As part of the ETE/Williams merger deal, Williams Partners will retain its current name and remain an independent publicly traded

partnership headquartered in Tulsa.“I believe that the combination of Williams and ETE will create

substantial value for both companies’ stakeholders that would not be realized otherwise,” Kelcy Warren, ETE’s chairman, said in the joint statement.

“After a comprehensive evaluation of strategic alternatives, including extensive discussions with numerous parties, the Williams board of directors concluded that a merger with Energy Transfer Equity is in the best interests of Williams’ stockholders and all of our other stakeholders,” Williams Chairman Frank MacInnis said.

“Williams’ intense focus on connecting the best natural gas supplies to the best natural gas markets will be a significant complement to the ETE family of diverse energy infrastructure,” Williams President and CEO Alan Armstrong said.

ETE said it expects that the earnings from these commercial synergies will exceed $2 billion/year by 2020. The combined company is expected to make a capital investment of more than $5 billion to achieve the hoped-for synergies.

A source familiar with the deal said ETE approached Williams in April to open merger negotiations. ETE went public with its offer in a letter to Williams dated May 19, followed by a letter to the Williams board June 18, spelling out its offer of a $53 billion all-equity buyout.

Initial buyout offer rejectedWilliams’ board rejected that offer saying it “significantly

undervalues Williams and would not deliver value commensurate with what Williams expects to achieve on a standalone basis and through other growth initiatives, including the pending acquisition of [Williams Partners].”

3

OctOber 9, 2015INSIDe Ferc’S GAS MArKet rePOrt

copyright © 2015 McGraw Hill Financial

At the time, Williams said it would review its strategic alternatives and the company reportedly entered into talks with several other big pipeline companies about a possible merger, talks that eventually went nowhere.

If it is consummated, “this deal would be identical to the proposed and rejected deal outlined in mid-June (split-adjusted),” Jefferies analyst Christopher Sighinolfi said in a note to investors on September 28.

Sighinolfi added that although many William shareholders would view the merger announcement in a positive light, “we believe some shareholders may be disappointed as the implied value is identical to what was rejected just three months earlier and were perhaps expecting a marginal uplift in implied deal terms.”

The deal is expected to be immediately accretive to cash flow and distributions for both companies, the statement said.

— Jim Magill

MARkETs

Gas on top in July, edges out coal in power generation for full monthFor only the second time this year, and only the second time since such data started being collected in 1973, gas-fired power edged coal-fired generation for a full calendar month, according to a report released October 7 by the US Energy Information Administration.

For the month of July, gas fueled 35% of the nation’s total electricity generation compared to coal’s 34.9%. The only other time gas edged out coal was in April, with 92,516 GWh for gas versus 88,516 GWh for coal for the month.

But coal quickly took back the lead in May. At the time, EIA predicted it would be the last time in 2015 gas would best coal in power generation. They made the prediction based on an expected increase in gas prices that never materialized.

“Monthly coal-fired generation is expected to continue exceeding natural gas-fired generation for the remainder of 2015, as natural gas prices slowly rise from their April average price of $2.61/MMBtu to about $3.30/MMBtu by December,” read the EIA report at the time.

Instead, gas prices have continued a downward trend due to unprecedented production levels coupled with improved efficiencies. The monthly average price at Henry Hub declined from $4.14/MMBtu in July 2014 to $2.91/MMBtu in July 2015, and it has since fallen to $2.72/MMBtu for September. The sustained low prices hint July is not the last time this year gas passes coal for a month. The winter is also expected to set another record for gas production, averaging 74 Bcf/d throughout the season.

Since last July, coal-fired generation has slipped in every region, but was most pronounced in the Mid-Atlantic where it fell 3.6%, according to EIA data. Texas was next where it witnessed a 1.9% drop. Meanwhile, gas-fired power gained ground in every region, growing the most in the Southeast at 7.6% followed by the Central US at 6.6%.

A recent winter outlook study by Natural Gas Supply Association (NGSA) expects continued growth in the electric sector throughout the winter. The study forecast a substantial winter-over-winter gas demand

growth in the power sector of 5% or 1.1 Bcf/d, with a total winter fuel switching of 5.6 Bcf/d. The winter record of 6 Bcf/d of coal-to-gas switching occurred in winter 2011-12.

“The continued stability and abundant supply of natural gas is great news for consumers,” said Bill Green, NGSA chairman. “We anticipate neutral pressure on prices compared to last winter.”

“We anticipate temporary fuel-switching to natural gas to reach near-record levels this winter,” Green added.

Multiple factors have played a role in coal’s slow demise. Gas started climbing the ladder when the shale boom began in 2007 leading to lower prices. More recently, stricter environmental standards have prompted more and more utilities to switch from coal- to gas-fired power plants as well as adding renewables to company portfolios. These regulations include the US Environmental Protection Agency’s Mercury and Air Toxics Standard and the more recently unveiled Clean Power Plan.

And the new ozone standards announced last week might prompt even more coal plant closures. Under the EPA’s new 70 ppb limit of ground-level ozone, 37 coal-fired generators scattered across the country fail to meet the new standards. According to the EPA’s Regulatory Impact Analysis, 30 of those plants either do not have selective catalytic reduction systems, or scrubbers, while the remaining seven have scrubbers, but fail to use them on a regular basis.

— Brandon Evans

Production, storage, other factors expected to keep winter prices flatChanges in natural gas production, storage, weather and customer demand are likely to keep this winter’s natural gas prices flat compared to last year, the Natural Gas Supply Association said September 30 in its winter outlook.

The combined factors are likely to “place neutral pressure” on winter 2014-15 prices, compared with last winter when Henry Hub prices averaged $3.21/MMBtu, NGSA said.

Slightly lower demand this winter will be balanced by a rise in domestic production levels, partially offset by lower net imports, according to an analysis prepared for the group by Energy Ventures Analysis. The net effect should be storage withdrawals of about 1.1 Bcf/d less than last winter, EVA said.

NGSA emphasized strong natural gas production and storage inventories approaching a new record.

“The picture that emerged for the upcoming winter is one of a flexible natural gas market that is able to respond to changes in weather and customer demand with abundant production and storage,” said Bill Green, chairman of NGSA and vice president of downstream marketing for Devon Energy.

The forecast predicts a slight dip in overall demand, down 0.7% to 90.2 Bcf/d, driven mostly by weather that is likely to be 7% warmer, lowering demand from residential and commercial sectors by 2.5 Bcf/d on average. That decline would be partly offset by strong demand growth of 5% or 1.1 Bcf/d in the electric sector, mostly attributed to fuel switching when utilities change over to gas-fired power temporarily

4

OctOber 9, 2015INSIDe Ferc’S GAS MArKet rePOrt

copyright © 2015 McGraw Hill Financial

because of lower fuel costs.EVA expects winter fuel switching to be 5.6 Bcf/d, near record

levels and up from 4.8 Bcf/d last year, NGSA said. Also driving the power sector increase is the permanent shift to gas-fired generation as coal plants are retired in efforts to comply with EPA Mercury and Air Toxics Standards.

On the demand side, the forecast sees a less than 1% increase from the industrial sector, although farther out, NGSA projected 3.9 Bcf in new industrial demand between now and 2020, pointing to 51 new projects and 15 expansions approved and under construction.

Projections call for demand to mirror last year’sThe demand projections assume average growth in GDP similar to

last winter, applying neutral pressure on prices. Manufacturing output is projected to grow only 0.7%, down from 3.3% growth the prior winter, it said, in part reflecting world economic conditions and a strong dollar.

The outlook predicts record natural gas production of 74.4 Bcf/d this winter, buoyed by drilling efficiencies and new pipeline infrastructure, to provide more than enough supply and putting neutral pressure on prices. That’s up from 73.0 Bcf/d last winter.

On storage, the group saw a potential for record inventories of gas this winter, applying downward pressure on prices.

The forecast assumes weather this winter at 3% warmer than the 30-year average, accounting for 3,432 heating degree days versus 3,685 days a year earlier. But it said the greatest uncertainty is in the weather forecast — if the winter turns out to be very cold, or similar to last winter, demand could be 2.5 Bcf/d more than projected, according to EVA.

Looking more closely at production, the report said declines in gas and oil prices have pulled down gas and oil-directed drilling 41% and 58% respectively, but that on a year-or-year basis, production is still up, with a 1.5 Bcf/d rise projected for this winter.

“Since 2013, shale’s continued to outperform our expectations and continue to grow,” Green told reporters. “The story is supply, supply, supply. It just keeps coming.”

Last year’s outlook “missed it” on the weather, which turned out to be colder than projected, and production, which surpassed expectations, Green noted.

He pointed to technological advances, such as the potential for repeat hydraulic fracking on older wells where only a portion of the gas was extracted, as averting a production drop in response to the current low-price environment and the drop in the number of well completions.

Separately, net imports are projected to decline, the EVA report said, due to increased exports to Mexico, the start of LNG exports from the Lower 48 states this winter and the reduction in Canadian imports, EVA said.

In the near term, Green said the early LNG exports are unlikely to affect prices, given the supply resources available.

The outlook relied on data from Energy Ventures Analysis and the Energy Information Administration for its demand and supply projections and IHS Economics for its economic projections.

— Maya Weber

Maintenance helps lift Northeast bidweek prices; other regions fallMonthly bidweek natural gas prices for October delivery fell at most locations, though Northeast points increased as the region was entering the chillier part of the year with several pipeline maintenance events on the books.

New England prices got the biggest lifts, with the Algonquin Gas Transmission city-gates and Tennessee Gas Pipeline zone 6 delivered both rising more than 80 cents month over month, Platts’ Inside FERC’s Gas Market Report price survey showed.

At Transcontinental Gas Pipe Line, zone 6 New York, prices were up 10 cents, or about 5%, to $2.23/MMBtu.

Transco began maintenance on Thursday at Station 515 as part of ongoing work on the Leidy Southeast Project expansion, which is set to enter service December 1. The Station 515 maintenance is scheduled to last through October 22.

Throughput at 515 will be capped at about 1.4 Bcf/d during the maintenance, down from a prior-month average of 1.7 Bcf/d, according to Bentek Energy, a unit of Platts.

Amid the maintenance, the Transco, Leidy Line receipts point remained one of the lowest prices in the October survey at just over $1/MMBtu, though its increase of 14 cents, or about 16%, marked one of the larger month-over-month increases.

Elsewhere on the Northeastern grid, Algonquin has several maintenance events slated for the month, including maintenance on the 30-inch-diameter mainline, will reduce capacity through the Stony Point compressor station to 530 MMcf/d from October 20 to November 2, down from a design capacity of roughly 1.5 Bcf/d.

AGT said based on historical nominations through Stony Point, it anticipates restrictions to interruptible, secondary services and potentially primary firm services.

The Algonquin city-gates index price was the only point in the survey higher than it was in the same month a year ago, topping the October 2014 price by 15 cents, according to Platts historical data.

With many weather forecasts painting pictures of a mild October, strong power burn has continued to give Northeast prices some support.

Year to date, Northeast power demand has averaged 6 Bcf/d, about 100 MMcf/d higher than the same period in 2012. Bentek said it expects the trend to continue through the rest of 2015 for an expected yearly average of 5.8 Bcf/d. That compares with an average of nearly 5.6 Bcf/d in the record year of 2012, according to Bentek data.

Texas Eastern Transmission gave notice to the US Federal Energy Regulatory Commission that it has commenced partial service on its Ohio Pipeline Energy Network project.

The OPEN project is will enable TETCO to flow an incremental 550 MMcf/d of firm capacity south from Zone M-2 to delivery points in Zones M-1 and West Louisiana.

TETCO M-2 October bidweek prices rose 5 cents to average $1.18/MMBtu, while TETCO M-3 inched up 2 cents to average $1.28/MMBtu.

Along the Gulf Coast, Henry Hub fell 8 cents to average $2.56/MMBtu. That closely mirrored the NYMEX Henry Hub October futures contract’s settlement of $2.563/MMBtu, down from September’s

5

OctOber 9, 2015INSIDe Ferc’S GAS MArKet rePOrt

copyright © 2015 McGraw Hill Financial

CLosING PRICEs foR NYMEX hENRY hub GAs fuTuREs CoNTRACT

Trading date 9/23 9/24 9/25 9/28 9/29 9/30 10/1 10/2 10/5 10/6Contract volume 253,756 336,894 305,592 301,577 255,583 288,925 361,754 270,858 219,946 317,670open interest 904,728 909,250 904,663 904,442 906,835 929,768 941,278 935,680 939,200 943,756

Oct 2015 $2.569 $2.591 $2.564 $2.563** $—- $—- $—- $—- $—- $—-Nov 2015 2.638 2.674 2.631 2.670 2.586 2.524 2.433 2.451 2.450 2.470Dec 2015 2.793 2.841 2.802 2.837 2.763 2.701 2.631 2.664 2.676 2.673Jan 2016 2.907 2.958 2.918 2.951 2.884 2.831 2.763 2.798 2.806 2.806Feb 2016 2.912 2.965 2.925 2.957 2.891 2.842 2.775 2.808 2.816 2.818Mar 2016 2.882 2.935 2.895 2.926 2.861 2.814 2.749 2.778 2.787 2.791Apr 2016 2.759 2.802 2.764 2.788 2.731 2.688 2.629 2.651 2.663 2.672May 2016 2.761 2.802 2.766 2.789 2.735 2.695 2.639 2.661 2.676 2.688Jun 2016 2.792 2.832 2.799 2.822 2.770 2.731 2.675 2.697 2.712 2.724Jul 2016 2.827 2.865 2.833 2.856 2.806 2.769 2.713 2.735 2.749 2.761Aug 2016 2.840 2.878 2.845 2.868 2.818 2.780 2.727 2.748 2.761 2.772Sep 2016 2.836 2.873 2.838 2.861 2.813 2.774 2.722 2.742 2.755 2.766Oct 2016 2.863 2.899 2.866 2.889 2.840 2.801 2.750 2.770 2.784 2.793Nov 2016 2.945 2.985 2.947 2.964 2.918 2.881 2.831 2.852 2.872 2.882Dec 2016 3.104 3.145 3.108 3.123 3.086 3.050 3.001 3.022 3.044 3.054Jan 2017 3.209 3.250 3.213 3.227 3.189 3.152 3.102 3.123 3.146 3.152Feb 2017 3.205 3.244 3.206 3.219 3.181 3.146 3.096 3.117 3.139 3.145Mar 2017 3.145 3.185 3.147 3.155 3.120 3.086 3.034 3.056 3.075 3.083

12-month ave. 2.793 2.835 2.798 2.824 2.792 2.746 2.684 2.709 2.720 2.728

Source: New York Mercantile Exchange

**Final Settlement price

$2.638/MMBtu.The October Henry bidweek price marked about a 37% decline

from the October 2014 price of $4.04/MMBtu.In southeast Texas, the Houston Ship Channel was down 12 cents

to $2.50/MMBtu. West Texas point El Paso-Permian Basin dropped 11 cents to a $2.42/MMBtu average.

Upper Midwest prices saw some mixed movements, with the Chicago city-gates stumbling 8 cents to $2.70/MMBtu. Dawn, Ontario ticked upward 1 cent to a $2.94/MMBtu average.

The Rockies Express Pipeline East-to-West Project capacity that has come online in the last couple of months is likely contributing downward pressure to the Chicago market as the project allows additional supply from the Marcellus to flow into that area.

Rockies points also may be feeling the effects of the project as Cheyenne Hub dropped 6 cents to average $2.41/MMBtu.

In Western Canada, Westcoast, Station 2 plummeted 31 cents, or 22%, to C$1.09/Gj as capacity restrictions downstream at the Huntingdon delivery area were scheduled to continue through October.

Northwest Pipeline at the Canadian Border was flat to average $2.41/MMBtu.

To the south, the Pacific Gas & Electric city-gate dipped 3 cents to $3.07/MMBtu, while Southern California Gas fell 9 cents to $2.62/MMBtu.

— Patrick Badgley

EIA forecasts drop for winter heating expense; warmer weather predictedExpectations for winter temperatures to be above the 10-year average across much of the US would drag natural gas expenditures for the average household down 10% from last winter’s costs, the Energy Information Administration said October 6 in its monthly outlook.

The agency’s October Short-Term Energy Outlook, which took a hard look at projected winter fuel needs, forecast residential gas demand to fall 6% this winter.

Henry Hub natural gas spot prices are expected to be 13% below last winter’s prices, EIA said, but residential prices for gas will only see a 4% decline from last winter. EIA explained that “changes in spot prices do not quickly translate into lower delivered residential prices” as the rates utilities charge are often “set by state utility commissions a year or more in advance and reflect the cost of gas purchased over many months.” The agency added that residential prices also “include a fixed component to cover utility operating costs and the cost to transport the natural gas.”

Nearly half of all US households keep warm during the winter with gas.

“Natural gas supplies should be adequate to meet demand this winter, as average household natural gas consumption during the heating season is expected to be the lowest in four years,” EIA Administrator Adam Sieminski said in an October 6 statement.

He added, “If winter temperatures come in as expected by US government weather forecasters, US consumers will pay less to stay warm this winter no matter what heating fuel they use.”

About 39% of US households rely on electricity as their primary heating source. Those households are expected to spend about $30, or 3%, less on heating costs this winter “as a result of 1% lower residential electricity prices and 2% lower consumption than last winter,” EIA said.

However, these projections, EIA cautioned, are based on the latest forecasts from the National Oceanic and Atmospheric Administration, and “weather can be unpredictable.”

“Under a 10% colder scenario, EIA projects natural gas consumption to be 1% higher than last year, but expenditures would still be 4% lower than last year. Under a 10% warmer scenario, EIA

6

OctOber 9, 2015INSIDe Ferc’S GAS MArKet rePOrt

copyright © 2015 McGraw Hill Financial

PRICEs of sPoT GAs dELIvEREd To PIPELINEs, oCTobER 1 ($/MMbtu)

Index Low high volume deals

ANR Pipeline Co.

Louisiana IGBBF03 2.49 2.49 2.49 4 4Oklahoma IGBBY03 2.36 2.34 2.38 170 13

Enable Gas Transmission, LLC.

East IGBCA03 2.45 2.45 2.46 30 6

Colorado Interstate Gas Co.

Rocky Mountains IGBCK03 2.36 2.33 2.43 313 20

Columbia Gas Transmission Corp.

Appalachia IGBDE03 2.39 2.37 2.45 131 34Appalachia (Non-IPP) IGBJU03 1.18 1.18 1.18 28 4

Columbia Gulf Transmission Co.

Louisiana IGBBG03 2.50 2.49 2.50 25 2Mainline IGBBH03 2.47 2.42 2.48 290 37

dominion Transmission Inc.

Appalachia IGBDC03 1.17 1.15 1.22 363 78

El Paso Natural Gas Co.

Permian Basin IGBAB03 2.42 2.40 2.46 451 65San Juan Basin IGBCH03 2.43 2.41 2.46 103 18

florida Gas Transmission Co.

Zone 1 IGBAW03 2.54 2.54 2.55 15 3Zone 2 IGBBJ03 2.54 2.53 2.56 70 13Zone 3 IGBBK03 2.56 2.55 2.58 139 17

kern River Gas Transmission Co.

Wyoming IGBCL03 2.46 2.44 2.53 282 48

Millennium Pipeline Co

East receipts IGBIW03 1.08 1.04 1.13 81 26

Natural Gas Pipeline Co. of America

Midcontinent zone IGBBZ03 2.46 2.41 2.51 146 21Texok zone IGBAL03 2.50 2.45 2.51 245 25South Texas zone IGBAZ03 2.48 2.47 2.48 45 6

Northern border Pipeline Co.

Ventura Transfer Point IGBGH03 2.65* 2.65 2.65 NA 0

Northern Natural Gas Co.

Demarcation IGBDV03 2.63 2.57 2.68 212 35Ventura, Iowa IGBDU03 2.64 2.62 2.70 43 8

Northwest Pipeline Corp.

Rocky Mountains IGBCP03 2.43 2.37 2.53 445 55Canadian border IGBCT03 2.41 2.38 2.46 101 22

oneok Gas Transportation LLC

Oklahoma IGBCD03 2.38 2.34 2.43 322 31

Panhandle Eastern Pipe Line Co.

Texas, Oklahoma (mainline) IGBCE03 2.38 2.37 2.45 336 30

southern Natural Gas Co.

Louisiana IGBBO03 2.52 2.52 2.56 40 9Southern Star Central Gas Pipeline Inc.Texas, Oklahoma, Kansas IGBCF03 2.41 2.38 2.47 34 15

Tennessee Gas Pipeline Co.

Louisiana, 500 leg IGBBP03 2.50 2.49 2.60 75 18Louisiana, 800 leg IGBBQ03 2.48 2.48 2.49 50 9Texas, zone 0 IGBBA03 2.46 2.46 2.47 139 8Zone 4-Ohio IGBHO03 NA NA NA NA 0Zone 4-200 leg IGBJN03 1.60 1.58 1.66 195 20Zone 4-300 leg IGBFL03 0.96 0.94 1.06 136 39Zone 4-313 pool IGCFL03 1.28 1.27 1.30 25 8

Texas Eastern Transmission Corp.

M-1 30-inch (Kosi) IGBDI03 2.37 2.36 2.38 6 3M-2 receipts IGBJE03 1.18 1.13 1.22 242 50East Louisiana zone IGBBS03 2.42 2.41 2.43 33 7West Louisiana zone IGBBR03 2.46 2.46 2.46 40 4East Texas zone IGBAN03 2.47 2.47 2.47 0.79 1South Texas zone IGBBB03 2.47 2.47 2.47 8 1

Texas Gas Transmission Corp.

Zone 1 IGBAO03 2.47 2.46 2.50 101 8Zone SL IGBBT03 2.51* 2.51 2.51 NA 0

Transcontinental Gas Pipe Line Corp.

Zone 1 IGBBC03 2.49 2.48 2.50 103 22Zone 2 IGBBU03 2.51* 2.51 2.51 NA 0Zone 3 IGBBV03 2.53 2.53 2.54 31 9Zone 4 IGBDJ03 2.53 2.53 2.55 189 29Leidy Line receipts IGBIS03 1.03 1.01 1.15 405 70

Transwestern Pipeline Co.

Permian Basin IGBAE03 2.36 2.35 2.39 82 13San Juan Basin IGBGK03 2.45 2.40 2.48 35 4

Trunkline Gas Co.

Louisiana IGBER03 2.49* 2.49 2.49 NA 0Zone 1A IGBGF03 2.47 2.47 2.50 23 6

expects declines of 14% in consumption and 17% in expenditures compared with last year,” the agency said.

For households that heat with electricity, a colder winter would see a 1% rise in residential electricity demand, with expenditures expected to be flat from last winter, EIA said. “Residential electricity prices would not rise immediately, but the effect of colder temperatures would pass through to retail electricity rates over the succeeding months of 2016.”

The report highlighted that pipeline constraints continue to pose a threat to gas-fired generation, so day-to-day price volatility was still likely for the winter.

But an analyst speaking at a supply and demand forecast event Tuesday said that he believed the market was “tremendously overpricing … New England gas this winter out of fear, auto-correlation and the ‘I don’t know’ factors” inherent to such projections.

Charles Blanchard, lead natural gas analyst at Bloomberg New Energy Finance, referred to spot gas prices at the Algonquin Citygate hub as “a spiky market” that must be thought about in terms of the frequency of price spikes and the level to which prices will spike.

“We determined, given NOAA’s outlook on temperatures this year, how many price spikes should there be, and it’s fewer than last year,” he told attendees at the 2015 Winter Energy Outlook Conference hosted by DOE’s Office of Electricity Delivery and Energy Reliability, EIA and the National Association of State Energy Officials.

Further, he said price spikes would be constrained to the cost of generators’ fuel alternatives, which in New England are LNG and oil. “Both of those are much cheaper than they were last winter,” he said.

According to Blanchard, distillate fuel oil is currently priced at about $11.50/MMBtu delivered to Boston, while residual oil is at about $7.50/MMBtu. Spot LNG prices are closer to $7/MMBtu now as well.

“So whereas last year you might have had the spike to $12, $13, $15 for LNG, this year you don’t have to spike too much above $7 to get hold of incremental gas or incremental negative molecules of gas by oil switching,” Blanchard said.

Fear and the natural auto-correlation phenomenon, where individuals assume this winter will be bad because the last two winters bad, were driving expectations for higher gas prices in New England.

Blanchard added that the pipeline capacity issues that have driven up New England gas prices in the past would probably be solved by the

Index Low high volume deals

7

OctOber 9, 2015INSIDe Ferc’S GAS MArKet rePOrt

copyright © 2015 McGraw Hill Financial

addition of one or two new pipelines “in the pretty near future.”Sieminski noted that gas-fired electricity generation surpassed

generation from coal for July — the second time that has ever happened. But “higher natural gas prices by February are expected to keep the amount of natural gas-fired electric generation below coal-fired generation levels at least through the winter months,” Sieminski said.

EIA lowered its forecast for fourth-quarter Henry Hub natural gas spot prices to $2.83/MMBtu, 12 cents below its estimate in September. The agency expects monthly average spot prices “to remain lower than $3/MMBtu through January, and lower than $3.50/MMBtu” through the end of 2016, the report said.

The report added that Henry Hub natural gas prices are projected to average $2.81/MMBtu in 2015 and $3.05/MMBtu in 2016.

Despite these relatively low gas prices, “increases in drilling efficiency will continue to support growing natural gas production,” EIA said.

The agency raised its natural gas marketed production estimate for Q3 by 350 MMcf/d to 79.37 Bcf/d, while its Q4 estimate was unchanged at 79.61 Bcf/d.

The report added that gas marketed production is expected to grow at an annual rate of 5.6% in 2015 to 79.06 Bcf/d and at 1.9% in 2016 to 80.58 Bcf/d.

Production continues to outpace demand through EIA’s forecasted period.

The agency raised its Q3 demand estimate by 320 MMcf/d to 66.39 Bcf/d, while lowering its Q4 demand estimate by 1 Bcf/d to 77.99 Bcf/d.

EIA said that demand for US gas for the full year is expected to average 76.20 Bcf/d — 320 MMcf/d below last month’s estimate — compared with 73.15 Bcf/d in 2014.

By sector, gas demand for power is projected to rise in 2015, supported by gas prices below $3/MMBtu, but fall off in 2016 as gas prices edge up, EIA said. “Industrial sector consumption remains flat in 2015 and increases by 4.2% in 2016, as new industrial projects, particularly in the fertilizer and chemicals sectors, come online late this year and next year, and as industrial consumers continue to experience low natural gas prices,” the agency said.

Gas demand in the residential and commercial sectors is forecast to decline in both 2015 and 2016, the report said.

— Jasmin Melvin

spark spreads differ by region amid gas and power price drop ANALYSIS Spark spread movements have varied by region following a drop in both gas and power prices as such factors as renewables and weather have impacted margins earned by generators.

Based on gas and power prices at 13 major electricity trading hubs across the US, the simple average October spark spread is down $5.17/MWh from September and $10.51/MWh from August.

Power prices at those hubs this year have averaged about $40/MWh, down 35% from the same period in 2014.

Henry Hub natural gas prices have averaged $2.78/MMBtu year to date, 39% below the same period in 2014. Henry Hub prices recently hit their lowest level since early 2012, $2.26/MMBtu.

Regional trends mixed for gas-fired generatorsGas-fired generators in the Northeast and Midwest have benefited

from firming power prices on account of unseasonably high September demand, while generation margins were pressured in the rest of the country by factors like higher-than-normal wind generation or regionally elevated gas prices.

Temperatures in the Midwest and Northeast were about 3-4 degrees above normal, which sustained cooling demand and drove elevated power demand. Average September peak load registered 5% higher than 2014 in ISO-NE and MISO and 8% higher in NYISO.

Elevated demand in these regions propped up power prices in the face of falling fuel costs, and gas-fired generators saw market clearing spark spreads rise approximately $3-4/MWh.

While ERCOT and SPP also saw higher-than-normal peak load and falling gas prices in September, high levels of wind generation weighed

MARkET CENTER sPoT GAs PRICEs, oCTobER 1 ($/MMbtu) Index Low high volume deals

Northeast

Texas Eastern, zone M-3 IGBEK03 1.28 1.26 1.35 176 42Transco, zone 5 delivered IGBEN03 2.61 2.60 2.64 71 19Transco, zone 6 N.Y. IGBEM03 2.23 2.18 2.26 103 22Transco, zone 6 non-N.Y. IGBEL03 2.27 2.20 2.43 116 33Transco, zone 6 non-N.Y. North IGBJS03 2.24 2.20 2.28 92 27Transco, zone 6 non-N.Y. South IGBJT03 2.38 2.31 2.43 24 6Iroquois, receipts IGBCR03 3.00 2.96 3.06 76 25Iroquois, zone 2 IGBEJ03 3.03 2.98 3.06 16 10Algonquin city-gates IGBEE03 3.50 3.41 3.61 75 21Tennessee, zone 6 delivered IGBEI03 3.36 3.31 3.45 72 25Niagara IGBCS03 1.62 1.61 1.81 5 2Leidy Hub IGBDD03 1.21 1.21 1.21 30 2Lebanon Hub IGBFJ03 2.57 2.52 2.62 25 4Rockies Express, Clarington Ohio IGBGO03 NA NA NA NA 0

upper Midwest

Chicago city-gates IGBDX03 2.70 2.66 2.73 105 24Consumers Energy city-gate IGBDY03 2.89 2.88 2.90 33 9Mich Con city-gate IGBDZ03 2.86 2.84 2.88 186 33Emerson, Viking GL IGBCW03 2.78 2.74 2.79 16 4ANR Pipeline, ML 7 IGBDQ03 2.79 2.76 2.90 7 4Dawn, Ontario IGBCX03 2.94 2.92 3.00 277 73

south Louisiana

Henry Hub IGBBL03 2.56 2.55 2.56 75 9

East Texas

Houston Ship Channel IGBAP03 2.50 2.50 2.53 25 3Katy IGBAQ03 2.53 2.52 2.56 15 3

West Texas

Waha IGBAD03 2.40 2.38 2.44 160 18

Rockies/Northwest

Cheyenne Hub IGBCO03 2.41 2.39 2.43 99 10TCPL Alberta, AECO-C# IGBCU03 2.64 2.56 2.73 769 182Westcoast Energy, station 2# IGBCZ03 1.09 0.97 1.37 138 34

California

PG&E Malin, Ore. IGBDO03 2.52 2.50 2.57 78 22PG&E city-gate IGBEB03 3.07 2.96 3.13 232 44PG&E South IGBDM03 2.60* 2.60 2.60 NA 0Southern California Gas Co. IGBDL03 2.62 2.58 2.68 223 32SoCal Gas city-gate IGBGG03 2.80 2.70 2.85 89 16

National Average

# All prices $/MMBtu except TCPL Alberta, AECO-C and Westcoast Energy, station 2, which is Canadian$/GJ (gigajoule). All volumes in (000) MMBtu/day.

8

OctOber 9, 2015INSIDe Ferc’S GAS MArKet rePOrt

copyright © 2015 McGraw Hill Financial

on power prices, driving spark spreads lower.Average peak load in ERCOT was 5% higher this September

compared to last year, but total wind generation climbed almost 5% from August and accounted for 9.3% of the fuel mix in September, up from 7.7% in August and 6.3% in September 2014.

ERCOT reached a new record wind generation peak on September 13 of 11,467 MW, which was close to 30% of the load.

As a result, spark spreads at ERCOT North Hub fell to $13.05/MWh, less than half of August levels. Ignoring peak demand days in August, which led to scarcity pricing events in ERCOT, September spark spreads were still down almost $9/MWh.

Similarly, gas prices in SPP averaged about $2.66/MMBtu in September, down 12 cents/MMBtu from August and $1.24/MMBtu from 2014. Wind generation, however, accounted for almost 14% of market share in September, up from 9% in August, driving spark spreads at SPP North Hub down almost $4/MWh from August to settle at $16.81/MWh.

PJM and CAISO also saw falling spark spreads in September. However, these declines were the result of regional gas price increases. Gas prices for generators in the PJM Western region also climbed 21% over August to hit $1.42/MMBtu in September. Average gas prices for generators in the CAISO SP15 region climbed 39% from August to an average of $3.51/MMBtu in September.

Year-to-date spark spreads declineOn a national level, power prices have fallen faster than gas prices,

pushing the year-to-date simple average spark spread down 67 cents to $16.11/MWh.

Spark spreads in CAISO, PJM, ISO-NE, and SPP have all slid more than 10% year over year. SPP has seen the biggest decline with year-to-date average spark spreads down over 35% to $19.05/MWh.

Spark spreads in the MISO region have increased 3% to $15.20/MWh so far in 2015.

Despite recent downward trends, ERCOT spark spreads have increased 15%, to an average of $11.67/MWh this year.

Gas-fired generators in NYISO have posted the highest average spark spreads in 2015 at $22.53/MWh, up more than 20% from last year.

— George McGuirk

LNG

LNG export developers counter dire forecasts with demand expectationsA Cheniere Energy executive pushed back against the recent spate of grim analyst assessments of the global LNG market, arguing that upcoming supplies would help open up new demand markets, particularly as the decade turns over, with Europe presenting a promising outlet for North American supplies.

Speaking at the North American Gas Forum in Washington, DC, on October 5, Cheneire Senior Vice President Anatol Feygin said there has been “too much emphasis on the negative,” and an excessive focus on weakness in demand from Asia driven by South Korea.

The biggest factor leading to sluggish global LNG demand has been a lack of incremental supply rather than a lack of demand, he argued, noting there was only one meaningful LNG expansion, Exxon’s Paupau New Guinea project, in the past year.

As more supply comes online, the market will see healthy demand growth play out, he said, and particularly as the decade draws to a close, he said the balance will change.

“We do think that we’ll see a meaningful incremental supply coming to the market toward the end of this decade,” he said.

In the medium term, he said, low oil prices may be felt as legacy contracts and business models, such as 20-year take-or-pay contracts unable to support incremental investments.

But, going forward, legacy markets are not likely to be major contributors, and the type of contracts used are likely to be altered as well, he said, suggesting those 20-year contracts may no longer be the norm.

Europe as a swing factorHe identified Europe as having the potential to be a more dynamic

and price sensitive market for additional volumes.Europe may serve as a swing factor in the Atlantic market, especially,

as legacy contracts run out, and the supply from legacy sources is less economic and those countries are less long in LNG, he said.

“In general, that will aid buyers with portfolio diversity and pricing diversity,” once North American LNG hits the market, he argued. Europe is well-placed, with substantial vaporization capacity and underutilized import capability, to import more as merchant generators become more sophisticated and price signals pass through more efficiently, he said.

European production declines will also add opportunities for North American players, he added.

He acknowledged that in 2015, 20-year take-or-pay contracts were essentially non-existent, in part because buyers didn’t need added volumes — and he said 2015 saw very few projects moving through final investment decisions amid continued low oil prices.

But, with projects in limbo, he suggested there could a substantial risk to supply at the end of this decade into next.

As prices move lower, the world has not yet recalibrated to the new normal, Feygin said. But as buyers start to believe the new dynamic is structural, rather than passing price volatility, the market may see more demand from the industrial and power sector — a shift that may quickly play out with use of new large floating storage and regasification, he said.

A more flexible market is emerging on the buyer and supplier side, he added, suggesting there will no longer be a need for 20-year deals for integrated projects. That shift, he said, has been behind Cheneire’s moved toward incremental brownfield projects and small-scale LNG.

‘Whole pockets of demand’: sempra LNG presidentSimilarly, Octavio Simoes, president of Sempra LNG, questioned

analysts’ bleak projections for the global LNG market, saying that “if you look back, there weren’t that many consultants that ever really forecast many things right when they happened.”

While he noted demand has declined in Europe, citing a variety of

9

OctOber 9, 2015INSIDe Ferc’S GAS MArKet rePOrt

copyright © 2015 McGraw Hill Financial

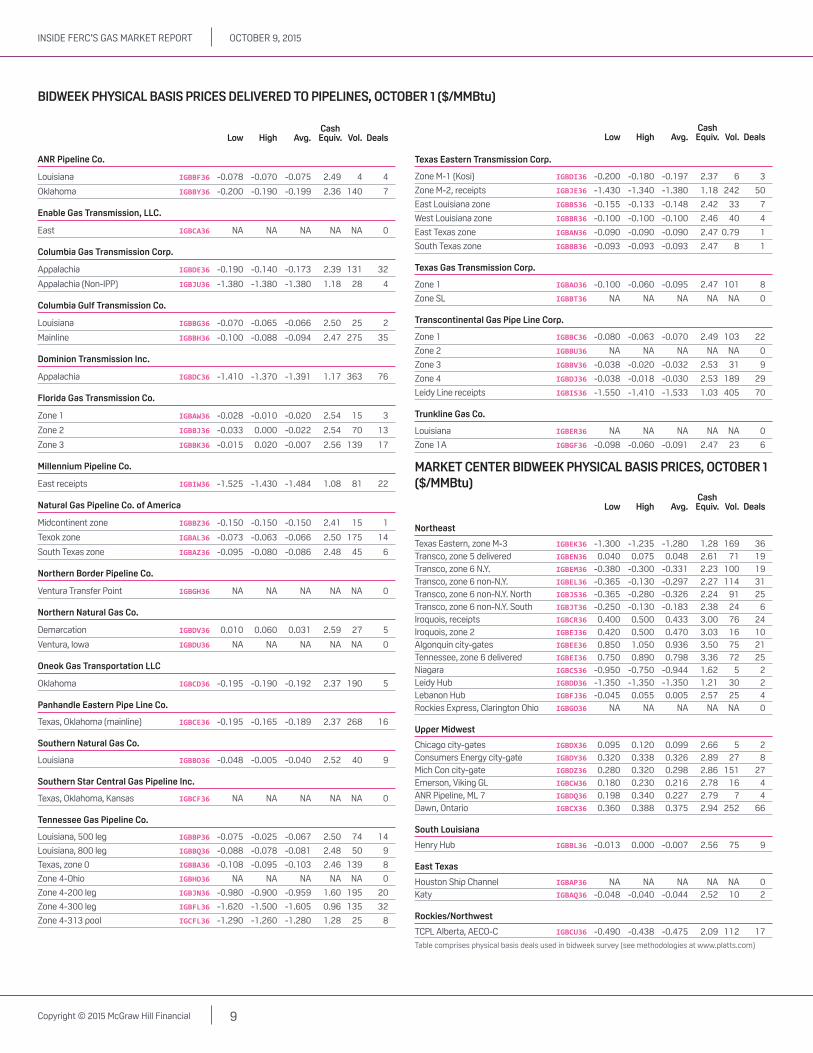

bIdWEEk PhYsICAL bAsIs PRICEs dELIvEREd To PIPELINEs, oCTobER 1 ($/MMbtu)

Cash Low high Avg. Equiv. vol. deals

ANR Pipeline Co.

Louisiana IGBBF36 -0.078 -0.070 -0.075 2.49 4 4

Oklahoma IGBBY36 -0.200 -0.190 -0.199 2.36 140 7

Enable Gas Transmission, LLC.

East IGBCA36 NA NA NA NA NA 0

Columbia Gas Transmission Corp.

Appalachia IGBDE36 -0.190 -0.140 -0.173 2.39 131 32

Appalachia (Non-IPP) IGBJU36 -1.380 -1.380 -1.380 1.18 28 4

Columbia Gulf Transmission Co.

Louisiana IGBBG36 -0.070 -0.065 -0.066 2.50 25 2

Mainline IGBBH36 -0.100 -0.088 -0.094 2.47 275 35

dominion Transmission Inc.

Appalachia IGBDC36 -1.410 -1.370 -1.391 1.17 363 76

florida Gas Transmission Co.

Zone 1 IGBAW36 -0.028 -0.010 -0.020 2.54 15 3

Zone 2 IGBBJ36 -0.033 0.000 -0.022 2.54 70 13

Zone 3 IGBBK36 -0.015 0.020 -0.007 2.56 139 17

Millennium Pipeline Co.

East receipts IGBIW36 -1.525 -1.430 -1.484 1.08 81 22

Natural Gas Pipeline Co. of America

Midcontinent zone IGBBZ36 -0.150 -0.150 -0.150 2.41 15 1

Texok zone IGBAL36 -0.073 -0.063 -0.066 2.50 175 14

South Texas zone IGBAZ36 -0.095 -0.080 -0.086 2.48 45 6

Northern border Pipeline Co.

Ventura Transfer Point IGBGH36 NA NA NA NA NA 0

Northern Natural Gas Co.

Demarcation IGBDV36 0.010 0.060 0.031 2.59 27 5

Ventura, Iowa IGBDU36 NA NA NA NA NA 0

oneok Gas Transportation LLC

Oklahoma IGBCD36 -0.195 -0.190 -0.192 2.37 190 5

Panhandle Eastern Pipe Line Co.

Texas, Oklahoma (mainline) IGBCE36 -0.195 -0.165 -0.189 2.37 268 16

southern Natural Gas Co.

Louisiana IGBBO36 -0.048 -0.005 -0.040 2.52 40 9

southern star Central Gas Pipeline Inc.

Texas, Oklahoma, Kansas IGBCF36 NA NA NA NA NA 0

Tennessee Gas Pipeline Co.

Louisiana, 500 leg IGBBP36 -0.075 -0.025 -0.067 2.50 74 14

Louisiana, 800 leg IGBBQ36 -0.088 -0.078 -0.081 2.48 50 9

Texas, zone 0 IGBBA36 -0.108 -0.095 -0.103 2.46 139 8

Zone 4-Ohio IGBHO36 NA NA NA NA NA 0

Zone 4-200 leg IGBJN36 -0.980 -0.900 -0.959 1.60 195 20

Zone 4-300 leg IGBFL36 -1.620 -1.500 -1.605 0.96 135 32

Zone 4-313 pool IGCFL36 -1.290 -1.260 -1.280 1.28 25 8

Texas Eastern Transmission Corp.

Zone M-1 (Kosi) IGBDI36 -0.200 -0.180 -0.197 2.37 6 3

Zone M-2, receipts IGBJE36 -1.430 -1.340 -1.380 1.18 242 50

East Louisiana zone IGBBS36 -0.155 -0.133 -0.148 2.42 33 7

West Louisiana zone IGBBR36 -0.100 -0.100 -0.100 2.46 40 4

East Texas zone IGBAN36 -0.090 -0.090 -0.090 2.47 0.79 1

South Texas zone IGBBB36 -0.093 -0.093 -0.093 2.47 8 1

Texas Gas Transmission Corp.

Zone 1 IGBAO36 -0.100 -0.060 -0.095 2.47 101 8

Zone SL IGBBT36 NA NA NA NA NA 0

Transcontinental Gas Pipe Line Corp.

Zone 1 IGBBC36 -0.080 -0.063 -0.070 2.49 103 22

Zone 2 IGBBU36 NA NA NA NA NA 0

Zone 3 IGBBV36 -0.038 -0.020 -0.032 2.53 31 9

Zone 4 IGBDJ36 -0.038 -0.018 -0.030 2.53 189 29

Leidy Line receipts IGBIS36 -1.550 -1.410 -1.533 1.03 405 70

Trunkline Gas Co.

Louisiana IGBER36 NA NA NA NA NA 0

Zone 1A IGBGF36 -0.098 -0.060 -0.091 2.47 23 6

MARkET CENTER bIdWEEk PhYsICAL bAsIs PRICEs, oCTobER 1 ($/MMbtu) Cash Low high Avg. Equiv. vol. deals

Northeast

Texas Eastern, zone M-3 IGBEK36 -1.300 -1.235 -1.280 1.28 169 36Transco, zone 5 delivered IGBEN36 0.040 0.075 0.048 2.61 71 19Transco, zone 6 N.Y. IGBEM36 -0.380 -0.300 -0.331 2.23 100 19Transco, zone 6 non-N.Y. IGBEL36 -0.365 -0.130 -0.297 2.27 114 31Transco, zone 6 non-N.Y. North IGBJS36 -0.365 -0.280 -0.326 2.24 91 25Transco, zone 6 non-N.Y. South IGBJT36 -0.250 -0.130 -0.183 2.38 24 6Iroquois, receipts IGBCR36 0.400 0.500 0.433 3.00 76 24Iroquois, zone 2 IGBEJ36 0.420 0.500 0.470 3.03 16 10Algonquin city-gates IGBEE36 0.850 1.050 0.936 3.50 75 21Tennessee, zone 6 delivered IGBEI36 0.750 0.890 0.798 3.36 72 25Niagara IGBCS36 -0.950 -0.750 -0.944 1.62 5 2Leidy Hub IGBDD36 -1.350 -1.350 -1.350 1.21 30 2Lebanon Hub IGBFJ36 -0.045 0.055 0.005 2.57 25 4Rockies Express, Clarington Ohio IGBGO36 NA NA NA NA NA 0

upper Midwest

Chicago city-gates IGBDX36 0.095 0.120 0.099 2.66 5 2Consumers Energy city-gate IGBDY36 0.320 0.338 0.326 2.89 27 8Mich Con city-gate IGBDZ36 0.280 0.320 0.298 2.86 151 27Emerson, Viking GL IGBCW36 0.180 0.230 0.216 2.78 16 4ANR Pipeline, ML 7 IGBDQ36 0.198 0.340 0.227 2.79 7 4Dawn, Ontario IGBCX36 0.360 0.388 0.375 2.94 252 66

south Louisiana

Henry Hub IGBBL36 -0.013 0.000 -0.007 2.56 75 9

East Texas

Houston Ship Channel IGBAP36 NA NA NA NA NA 0Katy IGBAQ36 -0.048 -0.040 -0.044 2.52 10 2

Rockies/Northwest

TCPL Alberta, AECO-C IGBCU36 -0.490 -0.438 -0.475 2.09 112 17

Table comprises physical basis deals used in bidweek survey (see methodologies at www.platts.com)

Cash Low high Avg. Equiv. vol. deals

10

OctOber 9, 2015INSIDe Ferc’S GAS MArKet rePOrt

copyright © 2015 McGraw Hill Financial

dAILY PRICEs of sPoT GAs dELIvEREd To PIPELINEs ($/MMbtu) Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint 9/23 9/24 9/25 9/28 9/29 9/30 10/1 10/2 10/5 10/6

ANR Pipeline Co.Louisiana 2.515 2.500 2.455 2.535 2.480 2.405 2.325 2.235 2.255 2.290Oklahoma 2.440 2.425 2.375 2.460 2.380 2.380 2.270 2.110 2.170 2.270

Enable Gas Transmission, LLC.East 2.540 2.495 2.460 2.505 2.435 2.390 2.240 2.115 2.185 2.205

Colorado Interstate Gas Co.Rocky Mountains 2.485 2.470 2.410 2.425 2.415 2.305 2.215 2.050 2.075 2.155

Columbia Gas Transmission Corp.Appalachia 2.435 2.415 2.375 2.465 2.390 2.340 2.250 2.125 2.185 2.215Appalachia non-IPP 1.300 N.A. 1.120 N.A. 1.280 1.250 1.260 N.A. 1.170 N.A.

Columbia Gulf Transmission Co.Louisiana 2.520 2.485 2.460 2.525 2.470 2.405 2.320 2.235 2.275 2.295Mainline 2.505 2.480 2.450 2.540 2.455 2.395 2.310 2.200 2.255 2.280

dominion Transmission Inc.South Point 1.275 1.190 1.035 1.185 1.240 1.220 1.200 0.840 1.140 1.010North Point 1.280 1.180 1.050 1.175 1.245 1.210 1.195 0.825 1.135 1.010

El Paso Natural Gas Co.Permian Basin 2.545 2.530 2.465 2.530 2.465 2.385 2.330 2.135 2.250 2.265San Juan Basin 2.540 2.550 2.460 2.530 2.465 2.385 2.310 2.130 2.240 2.260Bondad 2.530 2.540 2.460 2.530 2.450 2.360 2.310 2.125 2.230 2.255South Mainline 2.720 2.735 2.650 2.705 2.630 2.545 2.490 2.330 2.440 2.405

florida Gas Transmission Co.Zone 1 2.540 2.520 2.500 2.580 2.485 2.440 2.340 2.230 2.270 2.325Zone 2 2.550 2.530 2.505 2.590 2.495 2.445 2.350 2.245 2.295 2.315Zone 3 2.550 2.530 2.500 2.585 2.520 2.480 2.365 2.260 2.300 2.310

kern River Gas Transmission Co.Opal plant 2.550 2.555 2.485 2.540 2.465 2.395 2.330 2.120 2.230 2.265

Millennium Pipeline Co.East receipts 1.220 1.155 1.035 1.135 1.220 1.025 0.970 0.825 0.935 0.960

Natural Gas Pipeline Co. of AmericaMidcontinent zone 2.535 2.515 2.460 2.565 2.480 2.405 2.315 2.165 2.225 2.290Texok zone 2.535 2.510 2.480 2.575 2.495 2.415 2.330 2.200 2.260 2.315South Texas zone 2.525 2.475 2.460 2.585 2.450 2.400 2.325 2.195 2.250 2.330Amarillo reciept 2.585 2.535 2.500 2.580 2.530 2.475 2.360 2.195 2.230 2.310

Northern border Pipeline Co.Ventura Transfer Point 2.650 2.615 2.540 2.630 2.630 2.530 2.410 2.270 2.330 2.385

Northern Natural Gas Co.Demarcation 2.650 2.625 2.545 2.635 2.570 2.520 2.430 2.280 2.310 2.365Ventura, Iowa 2.660 2.620 2.550 2.640 2.595 2.535 2.420 2.275 2.320 2.385

Northwest Pipeline Corp.Wyoming 2.530 2.510 2.455 2.510 2.440 2.355 2.270 2.070 2.150 2.195Canadian border (Sumas) 2.535 2.495 2.455 2.515 2.450 2.680 2.290 2.025 2.135 2.200South of Green River 2.520 2.500 2.440 2.495 2.430 2.325 2.265 2.060 2.180 2.220

oneok Gas Transportation LLCOklahoma 2.410 2.380 2.365 2.460 2.390 2.345 2.265 2.100 2.175 2.190

Panhandle Eastern Pipe Line Co.Texas, Oklahoma (mainline) 2.465 2.455 2.410 2.520 2.480 2.300 2.270 2.090 2.145 2.160

Questar Pipeline Co.Rocky Mountains N.A. 2.490 2.450 2.500 2.400 2.330 2.260 N.A. 2.130 N.A.

southern Natural Gas Co.Louisiana 2.550 2.515 2.480 2.575 2.490 2.435 2.345 2.255 2.295 2.310

southern star Central Gas Pipeline, Inc.Texas, Oklahoma, Kansas 2.455 2.450 2.390 2.465 2.430 2.345 2.265 2.110 2.155 2.175

Tennessee Gas Pipeline Co.Louisiana, 500 leg 2.525 2.480 2.470 2.540 2.465 2.415 2.320 2.260 2.290 2.315Louisiana, 800 leg 2.515 2.475 2.470 2.540 2.470 2.410 2.325 2.250 2.275 2.320Texas, zone 0 2.520 2.470 2.450 2.510 2.460 2.400 2.325 2.200 2.255 2.300Zone 4-Ohio N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A.Zone 4-200 leg 1.725 1.615 1.520 1.430 1.470 1.445 1.460 1.025 1.200 1.1502Zone 4-300 leg 1.075 1.075 0.965 1.065 1.085 0.820 0.700 0.685 0.860 0.850Zone 4-313 pool 1.320 1.280 1.205 1.215 1.320 1.305 1.265 0.990 1.130 1.070

Texas Eastern Transmission Corp.East Louisiana zone 2.500 2.375 2.380 2.495 2.445 2.395 2.295 2.230 2.240 2.295West Louisiana zone 2.515 2.495 2.475 2.535 2.470 2.435 2.345 2.275 2.310 2.340East Texas zone 2.510 2.490 2.465 2.515 2.480 2.420 2.360 2.235 2.200 2.290South Texas zone 2.540 2.485 2.490 2.540 2.490 2.470 2.355 2.290 2.310 2.325M-1 30-inch (Kosi) 2.455 N.A. 2.330 2.480 2.410 2.380 2.280 2.190 2.210 2.280M-1 24-inch N.A. 2.440 2.400 N.A. N.A. N.A. N.A. N.A. N.A. N.A.M-2, receipts 1.265 1.205 1.025 1.200 1.240 1.215 1.215 0.875 1.180 1.055

11

OctOber 9, 2015INSIDe Ferc’S GAS MArKet rePOrt

copyright © 2015 McGraw Hill Financial

Texas Gas Transmission Corp.Zone 1 2.510 2.495 2.465 2.540 2.465 2.410 2.320 2.215 2.265 2.275Zone SL N.A. N.A. N.A. N.A. N.A. N.A. N.A. 2.220 2.250 2.260

Transcontinental Gas Pipe Line Corp.Zone 1 2.520 2.450 2.445 2.530 2.485 2.440 2.325 2.225 2.315 2.295Zone 2 2.520 2.490 2.430 2.550 2.500 N.A. 2.320 2.235 2.280 2.310Zone 3 2.535 2.515 2.480 2.565 2.480 2.445 2.345 2.260 2.300 2.325Zone 4 2.555 2.520 2.485 2.575 2.510 2.455 2.360 2.290 2.300 2.335Leidy Line receipts 1.125 1.170 1.020 1.125 1.105 0.830 0.680 0.755 0.970 0.940

Transwestern Pipeline Co.Permian Basin 2.500 2.510 2.400 2.485 2.450 2.345 2.300 2.105 2.220 2.235San Juan Basin 2.545 2.540 2.465 2.530 2.475 2.375 2.320 2.130 2.250 2.255

Trunkline Gas Co.West Louisiana N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A.East Louisiana 2.540 2.495 2.520 N.A. 2.470 N.A. 2.350 2.280 2.290 N.A.Zone 1A 2.510 2.485 2.455 2.535 2.470 2.410 2.310 2.210 2.275 2.275

MARkET CENTER sPoT GAs PRICEs, ($/MMbtu) Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint 9/23 9/24 9/25 9/28 9/29 9/30 10/1 10/2 10/5 10/6

NortheastTexas Eastern, zone M-3 1.380 1.305 1.115 1.305 1.345 1.345 1.310 0.960 1.295 1.100Transco, zone 6 N.Y. 2.305 2.190 1.525 2.050 2.015 2.440 2.130 1.580 2.280 2.395Transco, zone 6 non-N.Y. 2.305 2.225 1.665 2.065 2.015 2.410 2.235 1.705 2.265 2.405Transco, zone 6 non-N.Y. North 2.300 2.175 1.585 2.035 1.990 2.390 2.180 1.675 2.260 2.405Transco, zone 6 non-N.Y. South 2.330 2.280 1.880 2.110 2.085 2.455 2.295 1.810 2.280 2.400Algonquin city-gates 1.975 1.975 1.660 2.025 2.055 1.905 2.045 1.490 2.890 2.870Tennessee, zone 6 delivered 2.005 1.945 1.645 1.940 2.120 2.055 2.025 1.320 2.850 2.800Tennessee, z6 (300 leg) del. N.A. N.A. N.A. N.A. N.A. 1.500 1.500 N.A. N.A. N.A.Niagara N.A. N.A. N.A. N.A. N.A. 1.480 1.500 N.A. N.A. N.A.Leidy Hub N.A. N.A. 1.130 N.A. N.A. 1.240 N.A. N.A. N.A. N.A.Lebanon Hub 2.585 2.570 2.515 2.585 2.530 2.465 2.365 2.225 2.280 2.320Iroquois, receipts 2.905 2.730 2.195 2.900 2.575 2.615 2.580 2.260 2.750 2.730Algonquin, receipts N.A. N.A. N.A. N.A. N.A. N.A. 1.260 N.A. N.A. N.A.Iroquois, zone 2 2.975 2.505 1.845 N.A. 2.510 2.475 2.570 2.025 2.890 2.810Transco, zone 5 delivered 2.600 2.520 2.440 2.645 2.550 2.505 2.405 2.295 2.360 2.400Rockies Express, Clarington Ohio N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A.

southeastFlorida city-gates 2.860 2.860 2.800 N.A. N.A. 2.730 2.660 2.580 N.A. N.A.

upper MidwestChicago city-gates 2.655 2.615 2.590 2.670 2.650 2.570 2.460 2.265 2.350 2.380Consumers Energy city-gate 2.970 2.935 2.910 2.960 2.905 2.825 2.700 2.480 2.530 2.620Mich Con city-gate 2.920 2.875 2.865 2.915 2.860 2.775 2.660 2.450 2.515 2.580ANR Pipeline, ML 7 2.805 2.760 2.640 2.810 2.735 2.630 2.750 2.550 2.420 2.540Dawn, Ontario 3.010 2.985 2.960 3.015 2.950 2.870 2.700 2.380 2.620 2.695Emerson, Viking GL 2.725 2.705 2.650 2.735 2.705 2.630 2.540 2.295 2.550 2.555Alliance, into interstates 2.790 2.760 2.690 2.765 2.785 2.650 2.480 2.300 2.440 2.530Dracut, Mass. N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A.

south LouisianaHenry Hub 2.590 2.565 2.545 2.635 2.530 2.475 2.375 2.265 2.325 2.350

East/south TexasHouston Ship Channel 2.565 2.510 2.520 2.520 2.520 2.530 2.430 2.305 2.340 2.365Katy 2.550 2.515 2.495 2.540 2.520 2.495 2.375 2.290 2.315 2.360Carthage Hub 2.530 2.475 2.465 2.510 2.460 2.385 2.315 2.210 2.185 2.275Agua Dulce 2.640 N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A. N.A.

West TexasWaha 2.535 2.520 2.465 2.505 2.450 2.380 2.320 2.135 2.235 2.280

Rockies/NorthwestCheyenne Hub 2.500 2.470 2.400 2.475 2.425 2.330 2.235 2.090 2.155 2.230TCPL Alberta, AECO-C* 2.680 2.655 2.655 2.750 2.680 2.645 2.535 2.495 2.475 2.470Stanfield, Ore. 2.565 2.525 2.460 2.500 2.460 2.385 2.260 2.115 2.210 2.225Kern River, delivered 2.715 2.735 2.665 2.740 2.635 2.550 2.480 2.325 2.435 2.440GTN, Kingsgate 2.310 2.320 2.300 2.350 2.270 2.240 2.220 2.100 2.175 2.175Westcoast, station 2 1.025 0.990 0.460 0.400 0.855 0.875 0.800 1.510 1.980 1.490White River Hub 2.515 2.505 2.440 2.490 2.430 2.340 2.270 2.095 2.180 2.220

CaliforniaPG&E Malin, Ore. 2.620 2.605 2.550 2.610 2.530 2.455 2.390 2.195 2.295 2.325PG&E city-gate 3.070 3.055 3.055 3.125 3.060 2.990 2.910 2.820 2.920 2.920PG&E South 2.710 2.725 2.640 2.705 2.625 2.515 2.445 2.305 2.385 2.400Southern California Gas Co. 2.705 2.725 2.635 2.720 2.630 2.530 2.465 2.305 2.425 2.420SoCal Gas city-gate 2.900 2.910 2.825 2.920 2.825 2.750 2.670 2.325 2.635 2.620

* NOTE: Price in C$ per gj.

dAILY PRICEs of sPoT GAs dELIvEREd To PIPELINEs ($/MMbtu) Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint Midpoint 9/23 9/24 9/25 9/28 9/29 9/30 10/1 10/2 10/5 10/6

12

OctOber 9, 2015INSIDe Ferc’S GAS MArKet rePOrt

copyright © 2015 McGraw Hill Financial

factors including loss of industrial competitiveness and policies pushing renewables, he said there are big opportunities for LNG to compete in the long term.

Sempra has looked carefully at declining prices in the short term and nonetheless sees the potential for LNG to compete against long-haul pipe and indigenous production, he said. He pointed to prices in China at the city-gate, as well as those in Algeria and Norway.

“There are whole pockets of demand that have not been accounted for, he said.

He also made a case for US Gulf Coast projects being very competitive, with costs falling below those in Southeast Asia. Another benefit of US liquefaction is that it has broken a paradigm by offering customers volume flexibility, he said.

— Maya Weber

oregon’s Jordan Cove LNG clears environmental hurdle after delaysThe Jordan Cove LNG export project planned for Coos Bay, Oregon, took an important step on September 30 toward securing regulatory approval, when the US Federal Energy Regulatory Commission released the environmental impact statement for the project and an associated pipeline.

The EIS schedule had twice been delayed, most recently because the Department of the Interior’s Bureau of Land Management required more information from Pacific Connector about an alternative pipeline route affecting BLM lands. December 29 is the federal authorization decision deadline for the LNG project and pipeline.

FERC staff in the EIS found the projects would have some limited adverse impacts, but that those could be reduced to “less-than-significant” levels with mitigation measures proposed by the applicants and further steps suggested in the EIS (CP13-483, CP13-492).

Jordan Cove has said the project would use competitively priced gas from Western Canadian and Rocky Mountain sources to export to overseas markets around the Pacific Rim.

It filed an application in May 2013 to build liquefaction and export facilities, including four liquefaction trains, two 160,000-cubic-meter full-containment storage tanks and a new marine slip with two berths. The export terminal, estimated to cost $5.3 billion, would be capable of liquefying the LNG equivalent of 900 MMcf/d of gas.

Pacific Connector Gas Pipeline in June 2013 applied to build a 232-mile pipeline to feed gas to the facility. The 1.06-million Dt/d pipeline would connect with Ruby Pipeline and Gas Transmission Northwest near Malin, Oregon, and run to the proposed export project in Coos County. The $1.74 billion project would also include a 41,000-horsepower compressor station in Klamath County, as well as a number of meter stations.

The projects have faced vehement opposition from the environmental community, which contends the facilities would increase the region’s dependence on natural gas and encourage hydraulic fracturing. Others had focused opposition on the LNG terminal’s location in an area vulnerable to earthquakes and tsunamis, and on the risk of wildfires along the pipeline route.

Addressing some of those concerns, the EIS said the final terminal

design would include seismic specifications and other measures to reduce the impacts from future earthquakes and potential tsunamis. For instance, Jordan Cove would raise the LNG processing area and surround storage tanks with a storm-surge barrier about 60 feet high. The EIS also noted that Pacific Connector would put in place a fire prevention and suppression plan.

bLM to amend land management plansBLM would amend its land management plans for areas including

national forests thorough which the pipeline would traverse. The EIS said BLM could issue a right of way for the pipeline easement over federal lands. That would require concurrence with the Forest Service and Bureau of Reclamation, based on a plan of development that would include further mitigation.

FERC staff also said other agencies will offer further biological opinions and make recommendations to avoid harm to species under their jurisdiction or destruction of critical habitat.

The report sets an additional 102 environmental conditions for the project. It notes that 821 acres of late-successional old growth forest would be impacted by the pipeline, but that the Pacific Connector would compensate with a wildlife habitat mitigation plan.

The report mentions alternatives FERC considered, including the use of existing jurisdictional pipelines. Those were rejected as impractical because either the routes failed to connect the right locations or the systems couldn’t handle sufficient volumes of gas. It said other LNG facilities on the Gulf Coast or East Coast were not reasonable alternatives because they would have longer, less direct routes to Asia, and draw gas from different parts of the country.

The EIS acknowledged that the LNG project could be a significant source of greenhouse gas emissions but found it could also reduce emissions by displacing coal use in Asia. The displacement “depends on a multitude of complex geological and economic factors that cannot reasonably be foreseen,” the EIS said.

In Washington, the EIS was welcomed by Senator John Barrasso, Republican-Wyoming, who had written FERC several times to express support for the project. He called on DOE to quickly give approval, saying the administration needs to give West Coast communities opportunities to access overseas markets that their Gulf Coast and East Coast counterparts have enjoyed.

— Maya Weber

untapped sable basin gas supportive of Nova scotia LNG projects: officialUntapped resources of some 1 Tcf of natural gas in the Sable Basin in Atlantic Canada could emerge as a potential supplier for planned LNG projects in Nova Scotia, Murray Coolican, the province’s deputy energy minister, said September 30.

“That basin is home to Encana’s Deep Panuke and ExxonMobil’s Sable gas projects that are now headed towards a natural decline,” Coolican said at the annual Maritimes Energy Association conference in Halifax. “But there are still [significant discovery licenses] there that Exxon will not develop given the current gas prices. Those could be tapped by other developers.”

13

OctOber 9, 2015INSIDe Ferc’S GAS MArKet rePOrt

copyright © 2015 McGraw Hill Financial

Significant discovery licenses, or SDLs, are defined by the first well drilled on a geological formation that shows by flow testing the existence of hydrocarbons and the potential for sustained production, he said.

Four LNG projects have been proposed for Nova Scotia, which could potentially require a sustained feedstock demand of at least 6 Bcf/d to 8 Bcf/d, Coolican said. They include the 15 million mt/year facility of AC LNG, 10 million mt/year for Goldroro LNG, 4 million mt/year for Bear Head LNG and 250,000 mt/year for Nova Scotia LNG.

“Sourcing feedstock at a cost-competitive price will be a significant element for these projects taking a final investment decision over the next two years and one way out would be to rely on a basket of sources,” Coolican later said in an interview, without giving any figure on the gas price.

Developers of LNG facilities in Nova Scotia will be better off relying on three prime sources for securing gas feedstock, he said, identifying them to be offshore Nova Scotia, the US Northeast (Marcellus and Utica shales) and the Western Canadian Sedimentary Basin in Alberta.

Besides the SDLs in the Sable basin, tapping into associated gas to be produced by BP and Shell could also be a target for developers, Coolican said.

Shell will drill its first exploratory well in its licensed blocks in the neighboring Shelburne Basin in offshore Nova Scotia this fall, while BP plans to drill two years later.

Nova Scotia is estimated to contain 30-50 Tcf of onshore shale gas, but a moratorium is in place on hydraulic fracking that will get in the way of exploiting those resources, he said.

Province faces challenges: CoolicanWhile availability of cheap feedstock poses a challenge for

proposed LNG projects along the Canadian East Coast compared with those in British Columbia in the West, Coolican is hopeful of developers taking a final investment decision from late 2016 onwards.

The shorter travel time for LNG vessels from Nova Scotia to Europe and India, compared with British Columbia, will lower transportation costs for Eastern Canadian developers, he said.

A reduction of 50 cents/MMBtu in transportation cost could result in total savings of some $6 billion for an LNG buyer under a 20-year contract, Racim Gribaa, LNG leader and managing director for corporate finance advisory at Deloitte, said separately from Calgary.

— Ashok Dutta

PIPELINEs

Mountain valley to send gas to Transco, targets end-users in W.va., va. marketsThe proposed Mountain Valley Pipeline is not only planning to send more gas to Transcontinental Gas Pipe Line for markets in the South Atlantic, it also intends to supply utilities and end-users along its bending route through the Virginias.

The pipeline, a joint venture among EQT Midstream Partners and affiliates of NextEra Energy, WGL Holdings and Vega Energy Partners,

has ironed out a deal with Roanoke Gas Company. RGC will become a shipper on the pipeline to supply and expand its southwest Virginia customer base, the companies announced October 1.

Mountain Valley Pipeline, LLC, expects to file a certificate application with the Federal Energy Regulatory Commission by the end of October for the 300-mile, 42-inch diameter pipeline, which has an estimated project cost of $3 billion to $3.5 billion.

If approved, construction is slated to begin late next year with a full in-service date targeted for the fourth quarter of 2018. The line will begin in Wetzel County, West Virginia, where it will connect with a processing plant and an existing Equitrans line. It will terminate in Pittsylvania County, Virginia, at a Transcontinental Gas Pipeline interconnect at Transco Station 165 in the Zone 5 Pool.

Similar to other new pipeline projects in the region, the pipeline is contracting with end-users and utilities rather than primarily production companies. When fully constructed, the Mountain Valley Pipeline project will provide access to the growing demand for natural gas in the Appalachian, Mid-Atlantic and South Atlantic markets for use by local distribution companies, industrial users and power generation facilities.

“RGC Midstream’s agreement with Mountain Valley Pipeline addresses the growing demand for natural gas in our region and enhances the reliability of our Roanoke Gas system,” John D’Orazio, president and CEO of RGC Resources, said in a statement.

“Strengthening our natural gas supply and bringing access to unserved communities is essential for continued progress in southwest Virginia. It will increase the opportunity for economic growth in our region through a combination of industrial expansions, job creation and new investments,” he said.

The proposed line is also designed to address infrastructure constraints associated with the rapid development of natural gas from the Marcellus and Utica shale plays. Production in the area has exceeded the current takeaway capacity on Equitrans. Production from the Utica and Marcellus shales averaged 3.1 Bcf/d in 2010, but rocketed to about 19.6 Bcf/d this year to date. Platts’ unit Bentek Energy expects production to reach more than 30 Bcf/d by 2020, bolstered by pipeline expansions, new natural gas-fired power plants and LNG exports.

The proposed PennEast and Atlantic Coast pipelines also both have almost 100% of capacity already allocated to utilities. This is a shift from recent history where 20 major pipelines slated to go in-service this year or next have 70% of planned capacity additions held by producers rather than utilities and end-users.

Mountain Valley Pipeline is but one on a growing list of proposed projects that, if completed, would have the potential to provide up to 7.5 Bcf/d of gas to the Mid Atlantic and South Atlantic regions by 2018. They all have similar expected in-service dates. The list includes:�� n Transco Western Marcellus (2 Bcf/d; projected in-service date of late 2018)�� DTI Atlantic Coast (1.5 Bcf/d; late 2018)�� Penn East (1 Bcf/d; late 2017)�� Transco Diamond (0.5-1.0 Bcf/d; mid 2018)�� Mountain Valley (2 Bcf/d; late 2018)Many of these projects are also expected to send gas south on

Transco to markets in the Southeast and Gulf Coast and for potential

14

OctOber 9, 2015INSIDe Ferc’S GAS MArKet rePOrt

copyright © 2015 McGraw Hill Financial

LNG exports.Transco’s Western Marcellus pipeline project will “for the first time

offer Western Marcellus and Utica producers serviced by Williams’ Ohio Valley Midstream direct access to the broad range of Transco markets in the Mid-Atlantic and southeastern states, as far south as Florida,” said Rory Miller, senior vice president of Williams’ Atlantic-Gulf Operating Area.

“In addition, this groundbreaking project would provide enhanced supply access for burgeoning Louisiana and Texas Gulf Coast markets accessible through our Station 65 pool.”

— Brandon Evans

Algonquin maintenance to continue into November, disrupting boston supplyAlgonquin Gas Transmission will be conducting maintenance in October and November that will restrict substantial portions of gas to the New England market. This proposed work already has led to price increases in the forward basis market for Algonquin city-gates.

In a revised planned-maintenance schedule on October 2, Algonquin delayed a maintenance project one week, change in the schedule from October 20-November 2 to October 27-November 9. This delay led to basis increases in Algonquin city-gates November contract to levels about 10-15 cents higher than they were at the same time last year.

Algonquin is one of only three major pipelines serving the Boston area — the others being Tennessee Gas Pipeline and Maritimes & Northeast. Production declines offshore eastern Canada and weak LNG imports into the Canaport terminal in New Brunswick have negatively impacted gas supply on the Maritimes pipeline. Consequently, Algonquin and Tennessee run at relatively high utilization rates. Any mainline maintenance on these pipelines is likely to impact throughput and gas prices.

The currently planned maintenance on Algonquin will take place at the Stony Point compressor station in Middlesex County, Connecticut, which has a listed capacity of 1.5 Bcf/d. During the maintenance, the capacity through the station will be reduced to only about 0.5 Bcf/d from October 27 through November 2, a 67% reduction.

Nominations through Stony Point have averaged 1.1 Bcf/d over the past 30 days, suggesting that the New England market will be about 0.6 Bcf/d short gas during the maintenance.

Capacity at Stony Point also will be reduced to 960 MMcf/d from October 21 through 23. Additionally, capacity at the Burrillville compressor station in Providence County, Rhode Island has been reduced because oif maintenance that began September 29. Capacity Burrillville has been reduced from 812 MMcf/d to 600 MMcf/d, and the work is expected to continue through October 11.

Supply alternatives during the upcoming Stony Point maintenance could include reliance on Canadian imports via Iroquois Gas Transmission, which would be a significant change from historical flow patterns. Since the Millennium Pipeline entered service, Algonquin has delivered gas to Iroquois at Brookfield, in Fairfield County, Connecticut.