ncomm ncml commodity market monitor date: 06-03 …€¦ · • latest survey by soybean...

TRANSCRIPT

0

Date: 06-03-2018 NCoMM NCML Commodity Market Monitor

HOME

• Cotton • Sugar • Soyben • RM Seed • Castor seed • Turmeric • Jeera

NCoMM

NCML COMMODITY MARKET MONITOR

Cotton | Sugar | Soybean | RM Seed | Castor seed | Turmeric | Jeera

OUTLOOK

OTHER DATA Sowing progress | Advance estimates | Kharif and rabi MSP

ANSWERS & LUCKY WINNER OF PREVIOUS WEEK’S

QUIZ

NCoMM NCML COMMODITY MARKET MONITOR

ANSWERS & LUCKY WINNER OF PREVIOUS WEEK’S QUIZ

WEEKLY ONLINE QUIZ Click on the link above to participate

Participate in our weekly quiz and get a chance to win Amazon gift coupons. Winners will be announced in next report and rewarded.

Cotton • Soybean • RM Seed • Jeera • Chilli • Castor Seed • Turmeric

0

Date: 06-03-2018 NCoMM NCML Commodity Market Monitor

• Indian cotton has gained support from the weakening of the rupee

against the US dollar as this has accelerated its export demand as per

the Cotton Association of India (CAI).

• India has so far shipped around 30 lakh bales (170 kg each) of cotton as

while contracts for exports have been signed for 35 lakh bales till date.

• Indian cotton is the cheapest in the international market. Therefore,

traditional buyers like Bangladesh, Pakistan, Vietnam, and Turkey are

fulfilling most of their requirements of cotton from India

• The CAI has pegged India's cotton exports at 55 lakh bales in 2017-18

against 63 lakh bales a year ago. However the export could be higher if

the current trend continues.

• The Cotton Association of India (CAI) has, in its latest estimate, lowered

India’s 2017-18 cotton crop size by 8 lakh bales to 367 lakh bales against

its earlier estimate of 375 lakh bales. CAI reduced the estimate citing

severe infestation with pink bollworm in states like Maharashtra &

Telangana. Last year’s production was 345 lakh bales.

• Maharashtra’s output is forecast to drop to 6 million bales for the

2017/18 marketing year, down from 10.7 million bales in the 2016/17, due

pink bollworm infestation reducing yields in 80% of state’s cotton area.

• Cotton yield in Gujarat too may take a 15% hit this year due to the pink

bollworm pest attack even as the cotton acreage in Gujarat increased

to 26.42 lakh hectares 2017-18 from 24.04 lakh hectares last season. Cotton production in Punjab, Haryana & Ganganagar, is also likely to fall

short of the targets due non-conducive weather.

• Cotton Corporation of India (CCI) and multinationals such as Louis

Dreyfus & Glencore were seen stepping up purchases of cotton amidst

arrivals across growing regions. Higher demand for better grades of

cotton are keeping market sentiments firm.

• The February USDA report has raised the world cotton production by

400,000 bales over last month, as higher estimates for China, Brazil and

South Africa offset lower expectations for India and Australia.

• USDA in its latest report pegs 2017-18 world cotton production at 121.37

mn bales (of 480-lb) against 106.57 mn bales produced in 2016-17. The

consumption is pegged at 120.50 mn bales against 114.75 mn bales in

2016-17 and the ending stocks are estimated higher at 88.55 mn bales

against 87.66 mn bales last year.

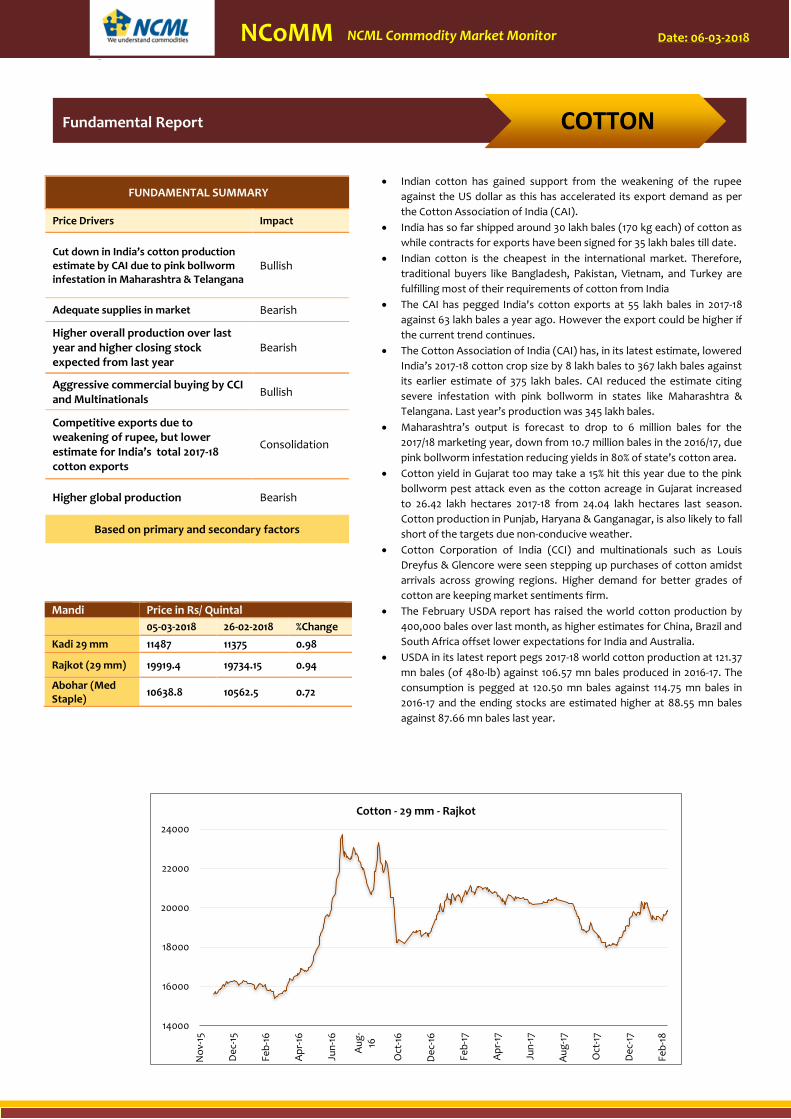

Mandi Price in Rs/ Quintal

05-03-2018 26-02-2018 %Change

Kadi 29 mm 11487 11375 0.98

Rajkot (29 mm) 19919.4 19734.15 0.94

Abohar (Med Staple)

10638.8 10562.5 0.72

14000

16000

18000

20000

22000

24000

No

v-15

De

c-15

Feb

-16

Ap

r-16

Jun

-16

Au

g-

16

Oct

-16

De

c-16

Feb

-17

Ap

r-17

Jun

-17

Au

g-1

7

Oct

-17

De

c-17

Feb

-18

Cotton - 29 mm - Rajkot

FUNDAMENTAL SUMMARY

Price Drivers Impact

Cut down in India’s cotton production estimate by CAI due to pink bollworm infestation in Maharashtra & Telangana

Bullish

Adequate supplies in market Bearish

Higher overall production over last year and higher closing stock expected from last year

Bearish

Aggressive commercial buying by CCI and Multinationals

Bullish

Competitive exports due to weakening of rupee, but lower estimate for India’s total 2017-18 cotton exports

Consolidation

Higher global production Bearish

Based on primary and secondary factors

Fundamental Report COTTON

0

Date: 06-03-2018 NCoMM NCML Commodity Market Monitor

• In the domestic market, the arrival of soybean is declining in the mandis.

There is lower availability at the plants for crushing. This coupled with

positive tone of soybean at CBOT continue to support the market.

• Profit–booking at higher levels is limiting the upside to an extent.

• Latest survey by Soybean Processors' Association (SOPA), estimates

India's soybean output at 8.35 mn tonnes for the 2017-18 season, about

24% lower than 10.9 mn tonnes produced in the previous year. SOPA

earlier had estimated the output at 9.15 mn tonnes in its Oct survey.

• India’s soybean output will be lower this year due to 5% lower acreage

over last year, flood-induced crop damage in major growing states,

followed by blight disease in the plants.

• Soybean rates in Madhya Pradesh and Maharashtra have risen sharply

due to lower availability. Positive trend overseas and restricted supplies

in the domestic spot market are fuelling Soybean prices in India.

• Spurt in soybean prices has made Indian meal exports uncompetitive

over the past one month. SOPA has estimated India's soybean meal

exports at 1.25 million tonnes for FY 2017-18 compared to 2 mn tonnes

reported for the previous year.

• The government has recently increased import duty on crude palm oil to

44% from 30%, while custom duties on refined palmolein and refined

palm oil has been raised to 54% from 40%. However SEA is seeking hike in

import duties of soya oil too in same proportion as palm oils for farmers.

• Import duty on crude soy oil was hiked from 17.5 percent to 30 percent

while refined soy oil import duty is hiked from 20% to 35%.

• Demand of soybean is higher than normal as stockiest are active in

market. Good demand for edible oils during winter season remains

supportive to cash market. Edible oil producers are also increasing their

operating capacities due hike in import duty of vegetable oils.

• Soybean at CBOT continued the positive tone. Dry weather continues in

Argentina and output could be further affected under the current

scenario. Argentina’s production could be down by up to 10 mn tonnes.

• Harvesting has picked up in Brazil, however it is lagging behind

compared to previous year. At the annual outlook forum this year, USDA

has reduced soybean output and ending stocks this season.

• Brazil’s crop is anticipated to be bigger than last year’s record 114 mn

tonnes & global supply estimate is higher amid record crop in U.S.

2700

2980

3260

3540

3820

4100

4380

No

v-15

Mar

-16

Jun

-16

Se

p-1

6

De

c-16

Ap

r-17

Jul-1

7

Oct

-17

Jan

-18

Soybean Indore

FUNDAMENTAL SUMMARY

Price Drivers Impact

Soybean output estimated 24% lower than last year

Bullish

Robust demand from stockeist and plants

Bulllish

Declining arrivals Bullish

Profit–booking at higher levels Bearish

Lower soymeal export Bearish

Dry weather in Argentina and lagged Brazilian harvest leading to positive tone at CBOT

Bullish

Higher global output on back of high Brazil and US harvest

Bearish

Based on primary and secondary factors

Mandi Price in Rs/ Quintal

05-03-2018 26-02-2018 %Change

Indore 3931 3766 4.38

Kota 3750 3650 2.74

Nagpur 4014.75 3822.85 5.02

Fundamental Report SOYBEAN

0

Date: 06-03-2018 NCoMM NCML Commodity Market Monitor

• Castor seed prices remained weak tracking subdued demand in spot

markets across the country against higher supplies. Moreover, the

arrival pressure of new crop also kept the market sentiments low.

• Traders reported that demand of castor seed from millers remained

weak due to slow off take of castor oil.

• In addition to it, millers are aware of the fact that new crop supply will

increase from March on wards which will help them to procure castor

seed at lower price level. Overall trend of castor seed is down for near

term.

• SEA conducted Castor crop survey for crop estimation in major growing

states like Gujarat, Rajasthan, Andhra Pradesh and Telangana. It has

estimated domestic crop at 14.30 lakh tonnes for 2017-18 as compared to

10.60 lakh tonnes in 2016-17. Besides, market was expecting castor seed

crop higher by around 10-15 per cent over last year's production.

• As per ministry of Agriculture, total area under castor in India for the

year 2017-18 is estimated to be 759000 hectares as against last year’s

estimate of 830000 hectares.

• Total area under castor in Rajasthan for the year 2017-18 is taken to be

1,31,000 hectares as per the government’s estimates against last year’s

estimate of 1,42,600 hectares, which has decreased by 8% as compared

to the previous year. Total production in the state is estimated to be 1.58

lakh tons during the year 2017-18.

• Total area under castor in Gujarat for the year 2017-18 is taken to be

5,95,600 hectares as per the government’s estimates against last year’s

estimate of 5,65,400 hectares, which has increased by 5.3% as compared

to the previous year. Total production in the state is estimated to be

12.20 lakh tons during the year 2017-18.

• As per the Solvent Extractor Association of India Castor oil exports

during the financial year 2017-18 till December stood at 4.11 lakh tonnes

as against 4.15 lakh tonnes in corresponding period last year. In 2016-17

total castor oil exports reported were 5.37 lakh tonnes.

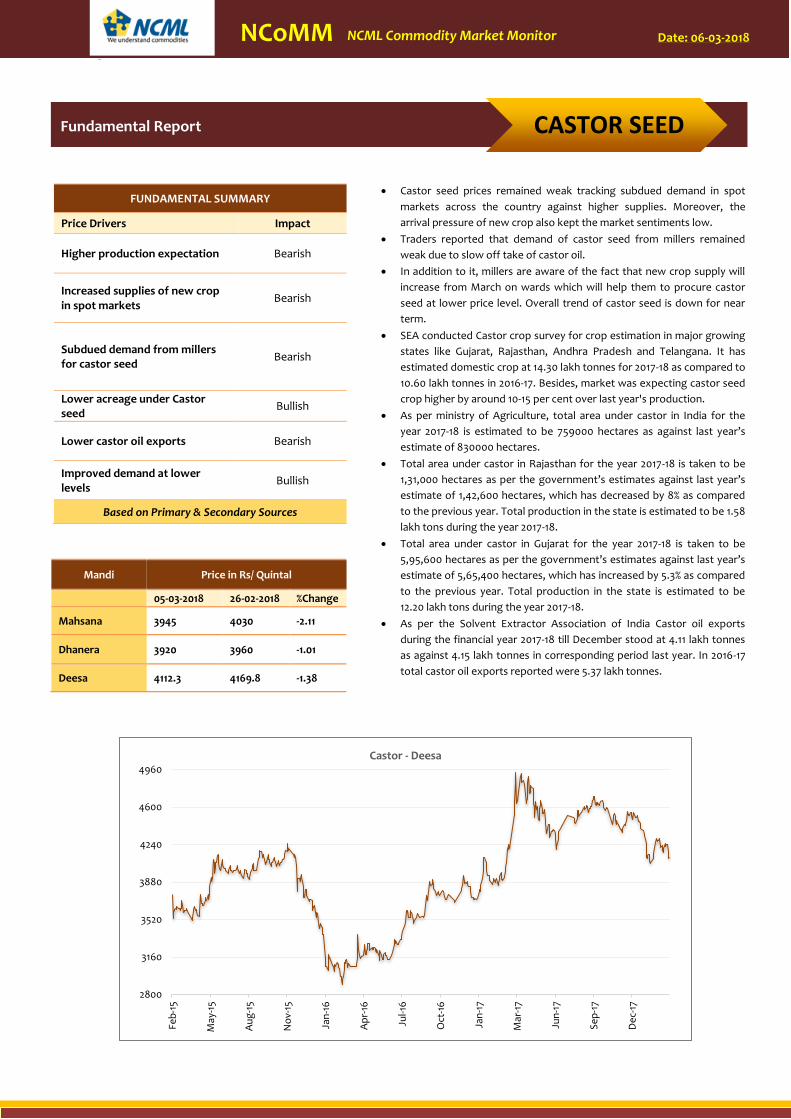

Mandi Price in Rs/ Quintal

05-03-2018 26-02-2018 %Change

Mahsana 3945 4030 -2.11

Dhanera 3920 3960 -1.01

Deesa 4112.3 4169.8 -1.38

2800

3160

3520

3880

4240

4600

4960

Feb

-15

May

-15

Au

g-1

5

No

v-15

Jan

-16

Ap

r-16

Jul-1

6

Oct

-16

Jan

-17

Mar

-17

Jun

-17

Se

p-1

7

De

c-17

Castor - Deesa

FUNDAMENTAL SUMMARY

Price Drivers Impact

Higher production expectation Bearish

Increased supplies of new crop in spot markets

Bearish

Subdued demand from millers for castor seed

Bearish

Lower acreage under Castor seed

Bullish

Lower castor oil exports Bearish

Improved demand at lower levels

Bullish

Based on Primary & Secondary Sources

Fundamental Report CASTOR SEED

0

Date: 06-03-2018 NCoMM NCML Commodity Market Monitor

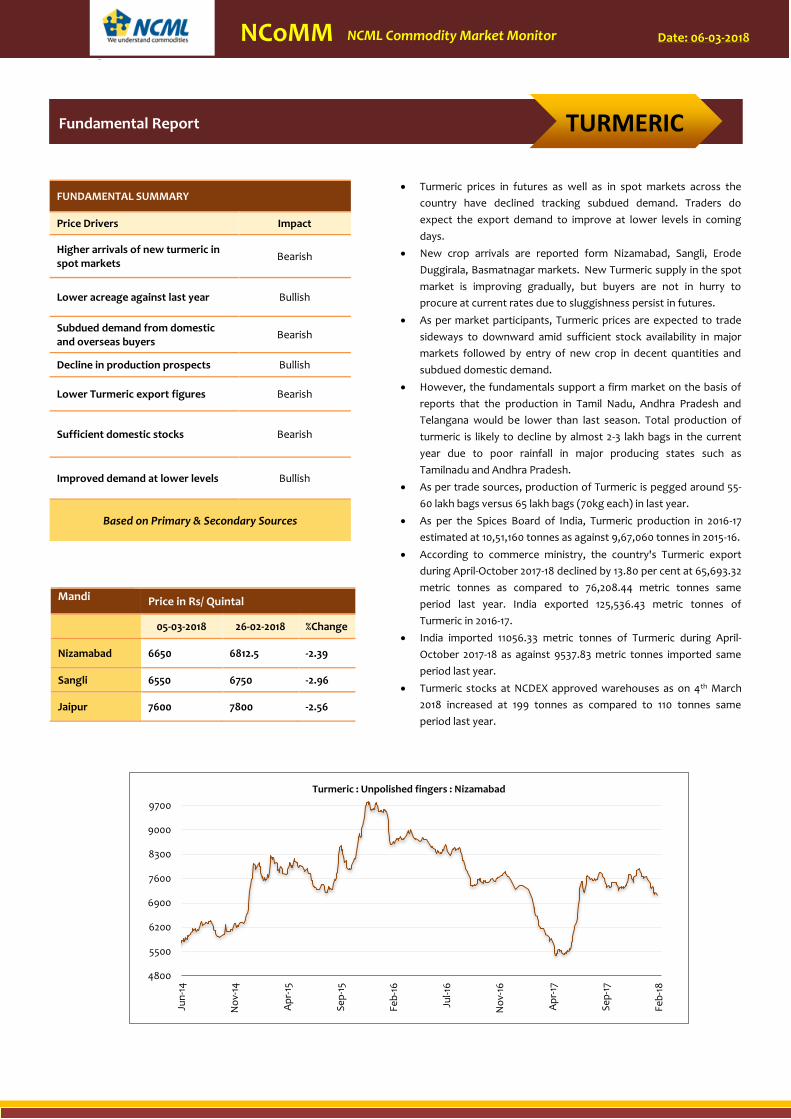

Fundamental Report TURMERIC

• Turmeric prices in futures as well as in spot markets across the

country have declined tracking subdued demand. Traders do

expect the export demand to improve at lower levels in coming

days.

• New crop arrivals are reported form Nizamabad, Sangli, Erode

Duggirala, Basmatnagar markets. New Turmeric supply in the spot

market is improving gradually, but buyers are not in hurry to

procure at current rates due to sluggishness persist in futures.

• As per market participants, Turmeric prices are expected to trade

sideways to downward amid sufficient stock availability in major

markets followed by entry of new crop in decent quantities and

subdued domestic demand.

• However, the fundamentals support a firm market on the basis of

reports that the production in Tamil Nadu, Andhra Pradesh and

Telangana would be lower than last season. Total production of

turmeric is likely to decline by almost 2-3 lakh bags in the current

year due to poor rainfall in major producing states such as

Tamilnadu and Andhra Pradesh.

• As per trade sources, production of Turmeric is pegged around 55-

60 lakh bags versus 65 lakh bags (70kg each) in last year.

• As per the Spices Board of India, Turmeric production in 2016-17

estimated at 10,51,160 tonnes as against 9,67,060 tonnes in 2015-16.

• According to commerce ministry, the country's Turmeric export

during April-October 2017-18 declined by 13.80 per cent at 65,693.32

metric tonnes as compared to 76,208.44 metric tonnes same

period last year. India exported 125,536.43 metric tonnes of

Turmeric in 2016-17.

• India imported 11056.33 metric tonnes of Turmeric during April-

October 2017-18 as against 9537.83 metric tonnes imported same

period last year.

• Turmeric stocks at NCDEX approved warehouses as on 4th March

2018 increased at 199 tonnes as compared to 110 tonnes same

period last year.

4800

5500

6200

6900

7600

8300

9000

9700

Jun

-14

No

v-14

Ap

r-15

Se

p-1

5

Feb

-16

Jul-1

6

No

v-16

Ap

r-17

Se

p-1

7

Feb

-18

Turmeric : Unpolished fingers : Nizamabad

FUNDAMENTAL SUMMARY

Price Drivers Impact

Higher arrivals of new turmeric in spot markets

Bearish

Lower acreage against last year Bullish

Subdued demand from domestic and overseas buyers

Bearish

Decline in production prospects Bullish

Lower Turmeric export figures Bearish

Sufficient domestic stocks Bearish

Improved demand at lower levels Bullish

Based on Primary & Secondary Sources

Mandi Price in Rs/ Quintal

05-03-2018 26-02-2018 %Change

Nizamabad 6650 6812.5 -2.39

Sangli 6550 6750 -2.96

Jaipur 7600 7800 -2.56

0

Date: 06-03-2018 NCoMM NCML Commodity Market Monitor

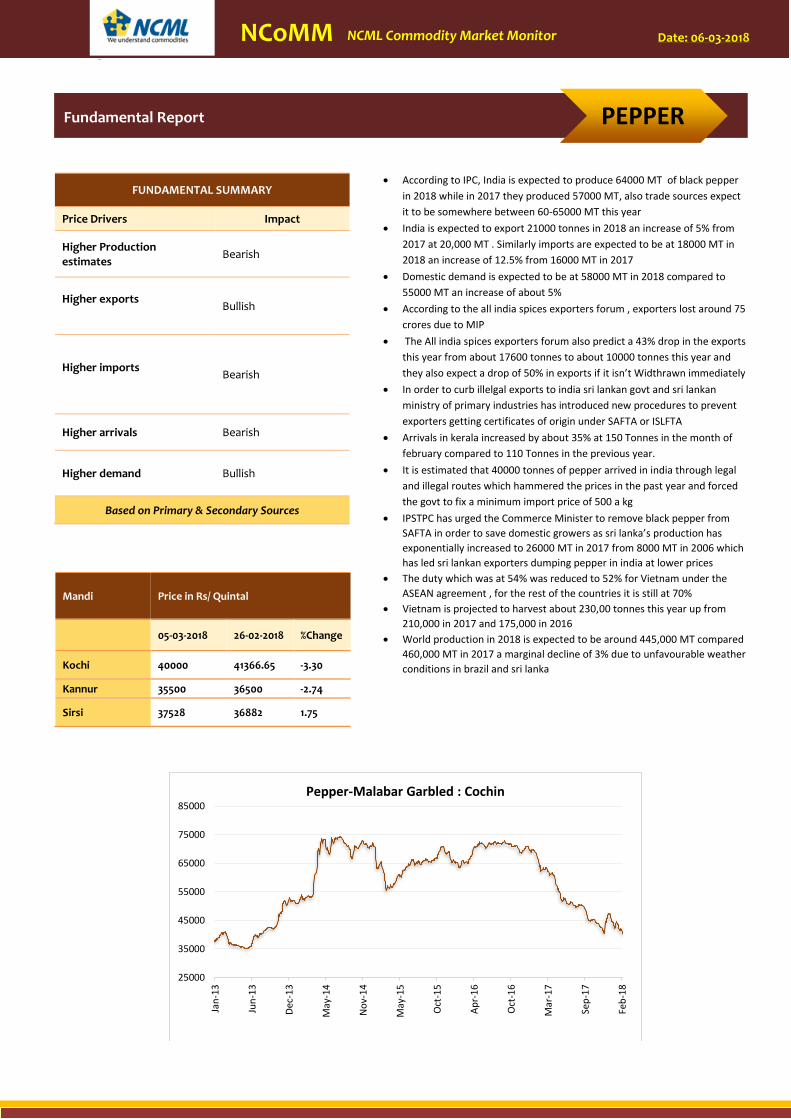

• According to IPC, India is expected to produce 64000 MT of black pepper

in 2018 while in 2017 they produced 57000 MT, also trade sources expect

it to be somewhere between 60-65000 MT this year

• India is expected to export 21000 tonnes in 2018 an increase of 5% from

2017 at 20,000 MT . Similarly imports are expected to be at 18000 MT in

2018 an increase of 12.5% from 16000 MT in 2017

• Domestic demand is expected to be at 58000 MT in 2018 compared to

55000 MT an increase of about 5%

• According to the all india spices exporters forum , exporters lost around 75

crores due to MIP

• The All india spices exporters forum also predict a 43% drop in the exports

this year from about 17600 tonnes to about 10000 tonnes this year and

they also expect a drop of 50% in exports if it isn’t Widthrawn immediately

• In order to curb illelgal exports to india sri lankan govt and sri lankan

ministry of primary industries has introduced new procedures to prevent

exporters getting certificates of origin under SAFTA or ISLFTA

• Arrivals in kerala increased by about 35% at 150 Tonnes in the month of

february compared to 110 Tonnes in the previous year.

• It is estimated that 40000 tonnes of pepper arrived in india through legal

and illegal routes which hammered the prices in the past year and forced

the govt to fix a minimum import price of 500 a kg

• IPSTPC has urged the Commerce Minister to remove black pepper from

SAFTA in order to save domestic growers as sri lanka’s production has

exponentially increased to 26000 MT in 2017 from 8000 MT in 2006 which

has led sri lankan exporters dumping pepper in india at lower prices

• The duty which was at 54% was reduced to 52% for Vietnam under the

ASEAN agreement , for the rest of the countries it is still at 70%

• Vietnam is projected to harvest about 230,00 tonnes this year up from

210,000 in 2017 and 175,000 in 2016

• World production in 2018 is expected to be around 445,000 MT compared

460,000 MT in 2017 a marginal decline of 3% due to unfavourable weather

conditions in brazil and sri lanka

Mandi Price in Rs/ Quintal

05-03-2018 26-02-2018 %Change

Kochi 40000 41366.65 -3.30

Kannur 35500 36500 -2.74

Sirsi 37528 36882 1.75

25000

35000

45000

55000

65000

75000

85000

Jan

-13

Jun

-13

Dec

-13

May

-14

No

v-1

4

May

-15

Oct

-15

Ap

r-1

6

Oct

-16

Mar

-17

Sep

-17

Feb

-18

Pepper-Malabar Garbled : Cochin

FUNDAMENTAL SUMMARY

Price Drivers Impact

Higher Production estimates

Bearish

Higher exports

Bullish

Higher imports

Bearish

Higher arrivals Bearish

Higher demand Bullish

Based on Primary & Secondary Sources

Fundamental Report PEPPER

0

Date: 06-03-2018 NCoMM NCML Commodity Market Monitor

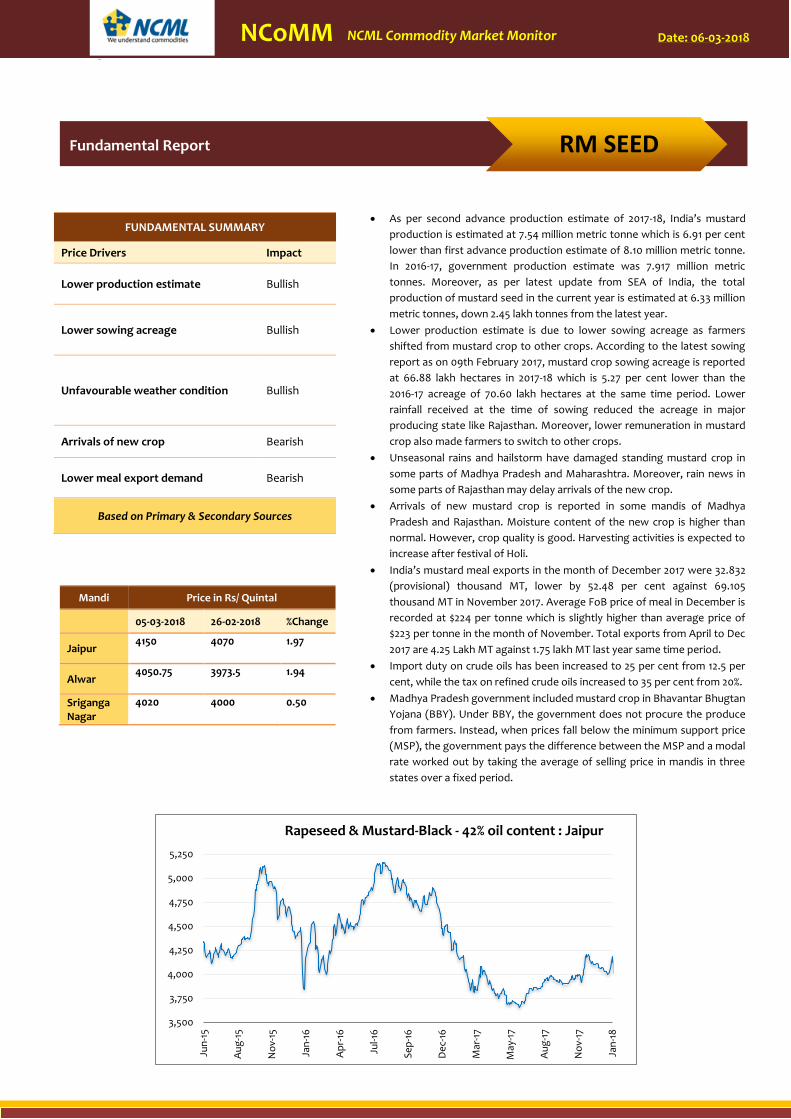

• As per second advance production estimate of 2017-18, India’s mustard

production is estimated at 7.54 million metric tonne which is 6.91 per cent

lower than first advance production estimate of 8.10 million metric tonne.

In 2016-17, government production estimate was 7.917 million metric

tonnes. Moreover, as per latest update from SEA of India, the total

production of mustard seed in the current year is estimated at 6.33 million

metric tonnes, down 2.45 lakh tonnes from the latest year.

• Lower production estimate is due to lower sowing acreage as farmers

shifted from mustard crop to other crops. According to the latest sowing

report as on 09th February 2017, mustard crop sowing acreage is reported

at 66.88 lakh hectares in 2017-18 which is 5.27 per cent lower than the

2016-17 acreage of 70.60 lakh hectares at the same time period. Lower

rainfall received at the time of sowing reduced the acreage in major

producing state like Rajasthan. Moreover, lower remuneration in mustard

crop also made farmers to switch to other crops.

• Unseasonal rains and hailstorm have damaged standing mustard crop in

some parts of Madhya Pradesh and Maharashtra. Moreover, rain news in

some parts of Rajasthan may delay arrivals of the new crop.

• Arrivals of new mustard crop is reported in some mandis of Madhya

Pradesh and Rajasthan. Moisture content of the new crop is higher than

normal. However, crop quality is good. Harvesting activities is expected to

increase after festival of Holi.

• India’s mustard meal exports in the month of December 2017 were 32.832

(provisional) thousand MT, lower by 52.48 per cent against 69.105

thousand MT in November 2017. Average FoB price of meal in December is

recorded at $224 per tonne which is slightly higher than average price of

$223 per tonne in the month of November. Total exports from April to Dec

2017 are 4.25 Lakh MT against 1.75 lakh MT last year same time period.

• Import duty on crude oils has been increased to 25 per cent from 12.5 per

cent, while the tax on refined crude oils increased to 35 per cent from 20%.

• Madhya Pradesh government included mustard crop in Bhavantar Bhugtan

Yojana (BBY). Under BBY, the government does not procure the produce

from farmers. Instead, when prices fall below the minimum support price

(MSP), the government pays the difference between the MSP and a modal

rate worked out by taking the average of selling price in mandis in three

states over a fixed period.

Mandi Price in Rs/ Quintal

05-03-2018 26-02-2018 %Change

Jaipur 4150 4070 1.97

Alwar 4050.75 3973.5 1.94

Sriganga Nagar

4020 4000 0.50

3,500

3,750

4,000

4,250

4,500

4,750

5,000

5,250

Jun

-15

Au

g-1

5

No

v-15

Jan

-16

Ap

r-16

Jul-1

6

Se

p-1

6

De

c-16

Mar

-17

May

-17

Au

g-1

7

No

v-17

Jan

-18

Rapeseed & Mustard-Black - 42% oil content : Jaipur

FUNDAMENTAL SUMMARY

Price Drivers Impact

Lower production estimate Bullish

Lower sowing acreage Bullish

Unfavourable weather condition Bullish

Arrivals of new crop Bearish

Lower meal export demand Bearish

Based on Primary & Secondary Sources

Fundamental Report RM SEED

0

Date: 06-03-2018 NCoMM NCML Commodity Market Monitor

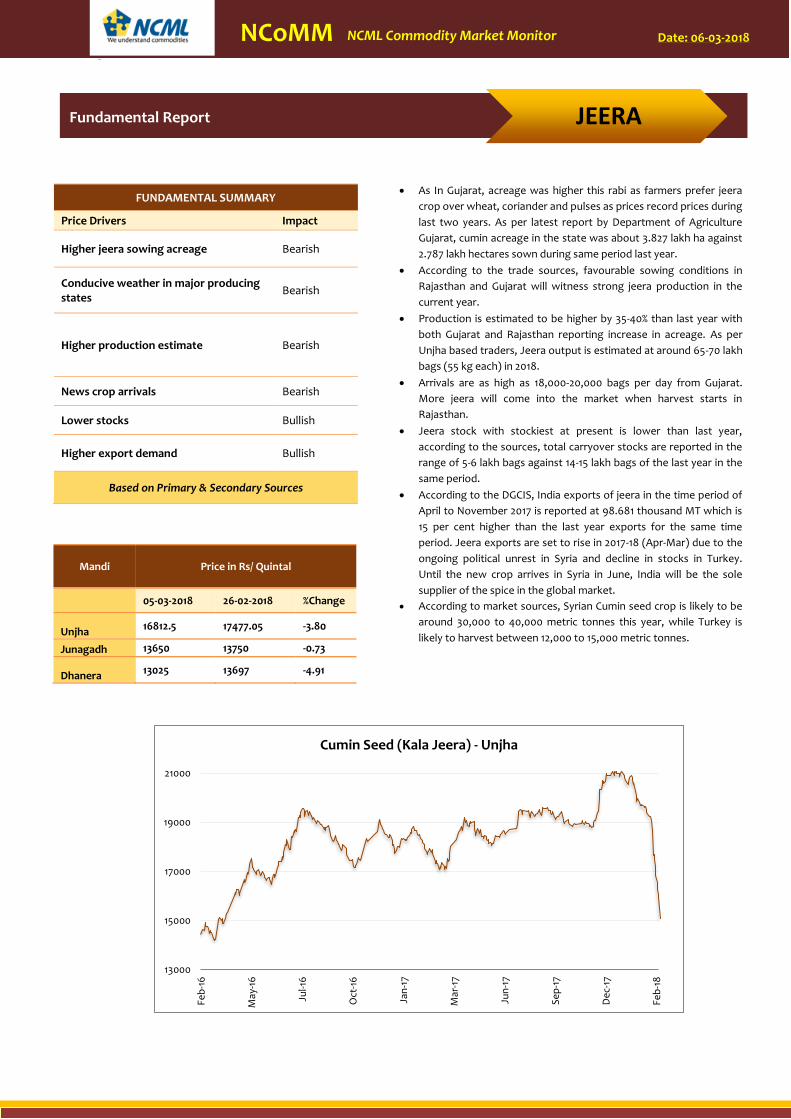

• As In Gujarat, acreage was higher this rabi as farmers prefer jeera

crop over wheat, coriander and pulses as prices record prices during

last two years. As per latest report by Department of Agriculture

Gujarat, cumin acreage in the state was about 3.827 lakh ha against

2.787 lakh hectares sown during same period last year.

• According to the trade sources, favourable sowing conditions in

Rajasthan and Gujarat will witness strong jeera production in the

current year.

• Production is estimated to be higher by 35-40% than last year with

both Gujarat and Rajasthan reporting increase in acreage. As per

Unjha based traders, Jeera output is estimated at around 65-70 lakh

bags (55 kg each) in 2018.

• Arrivals are as high as 18,000-20,000 bags per day from Gujarat.

More jeera will come into the market when harvest starts in

Rajasthan.

• Jeera stock with stockiest at present is lower than last year,

according to the sources, total carryover stocks are reported in the

range of 5-6 lakh bags against 14-15 lakh bags of the last year in the

same period.

• According to the DGCIS, India exports of jeera in the time period of

April to November 2017 is reported at 98.681 thousand MT which is

15 per cent higher than the last year exports for the same time

period. Jeera exports are set to rise in 2017-18 (Apr-Mar) due to the

ongoing political unrest in Syria and decline in stocks in Turkey.

Until the new crop arrives in Syria in June, India will be the sole

supplier of the spice in the global market.

• According to market sources, Syrian Cumin seed crop is likely to be

around 30,000 to 40,000 metric tonnes this year, while Turkey is

likely to harvest between 12,000 to 15,000 metric tonnes.

Mandi Price in Rs/ Quintal

05-03-2018 26-02-2018 %Change

Unjha 16812.5 17477.05 -3.80

Junagadh 13650 13750 -0.73

Dhanera 13025 13697 -4.91

13000

15000

17000

19000

21000

Feb

-16

May

-16

Jul-1

6

Oct

-16

Jan

-17

Mar

-17

Jun

-17

Se

p-1

7

De

c-17

Feb

-18

Cumin Seed (Kala Jeera) - Unjha

FUNDAMENTAL SUMMARY

Price Drivers Impact

Higher jeera sowing acreage Bearish

Conducive weather in major producing states

Bearish

Higher production estimate Bearish

News crop arrivals Bearish

Lower stocks Bullish

Higher export demand Bullish

Based on Primary & Secondary Sources

Fundamental Report JEERA

0

Date: 06-03-2018 NCoMM NCML Commodity Market Monitor

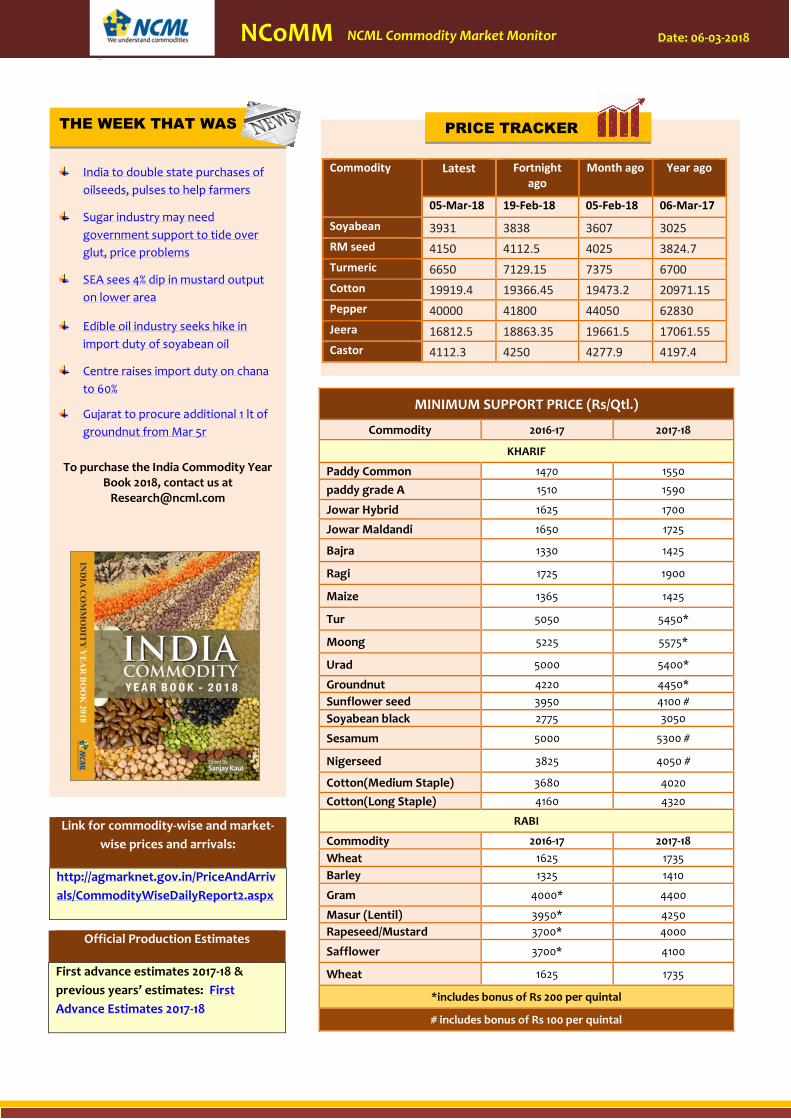

India to double state purchases of

oilseeds, pulses to help farmers

Sugar industry may need

government support to tide over

glut, price problems

SEA sees 4% dip in mustard output

on lower area

Edible oil industry seeks hike in

import duty of soyabean oil

Centre raises import duty on chana

to 60%

Gujarat to procure additional 1 lt of

groundnut from Mar 5r

To purchase the India Commodity Year Book 2018, contact us at

Official Production Estimates

First advance estimates 2017-18 &

previous years’ estimates: First

Advance Estimates 2017-18

MINIMUM SUPPORT PRICE (Rs/Qtl.)

Commodity 2016-17 2017-18

KHARIF

Paddy Common 1470 1550

paddy grade A 1510 1590

Jowar Hybrid 1625 1700

Jowar Maldandi 1650 1725

Bajra 1330 1425

Ragi 1725 1900

Maize 1365 1425

Tur 5050 5450*

Moong 5225 5575*

Urad 5000 5400*

Groundnut 4220 4450*

Sunflower seed 3950 4100 #

Soyabean black 2775 3050

Sesamum 5000 5300 #

Nigerseed 3825 4050 #

Cotton(Medium Staple) 3680 4020

Cotton(Long Staple) 4160 4320

RABI

Commodity 2016-17 2017-18

Wheat 1625 1735

Barley 1325 1410

Gram 4000* 4400

Masur (Lentil) 3950* 4250

Rapeseed/Mustard 3700* 4000

Safflower 3700* 4100

Wheat 1625 1735

*includes bonus of Rs 200 per quintal

# includes bonus of Rs 100 per quintal

THE WEEK THAT WAS

Commodity Latest Fortnight ago

Month ago Year ago

05-Mar-18 19-Feb-18 05-Feb-18 06-Mar-17

Soyabean 3931 3838 3607 3025

RM seed 4150 4112.5 4025 3824.7

Turmeric 6650 7129.15 7375 6700

Cotton 19919.4 19366.45 19473.2 20971.15

Pepper 40000 41800 44050 62830

Jeera 16812.5 18863.35 19661.5 17061.55

Castor 4112.3 4250 4277.9 4197.4

PRICE TRACKER

Link for commodity-wise and market-

wise prices and arrivals:

http://agmarknet.gov.in/PriceAndArriv

als/CommodityWiseDailyReport2.aspx

0

Date: 06-03-2018 NCoMM NCML Commodity Market Monitor

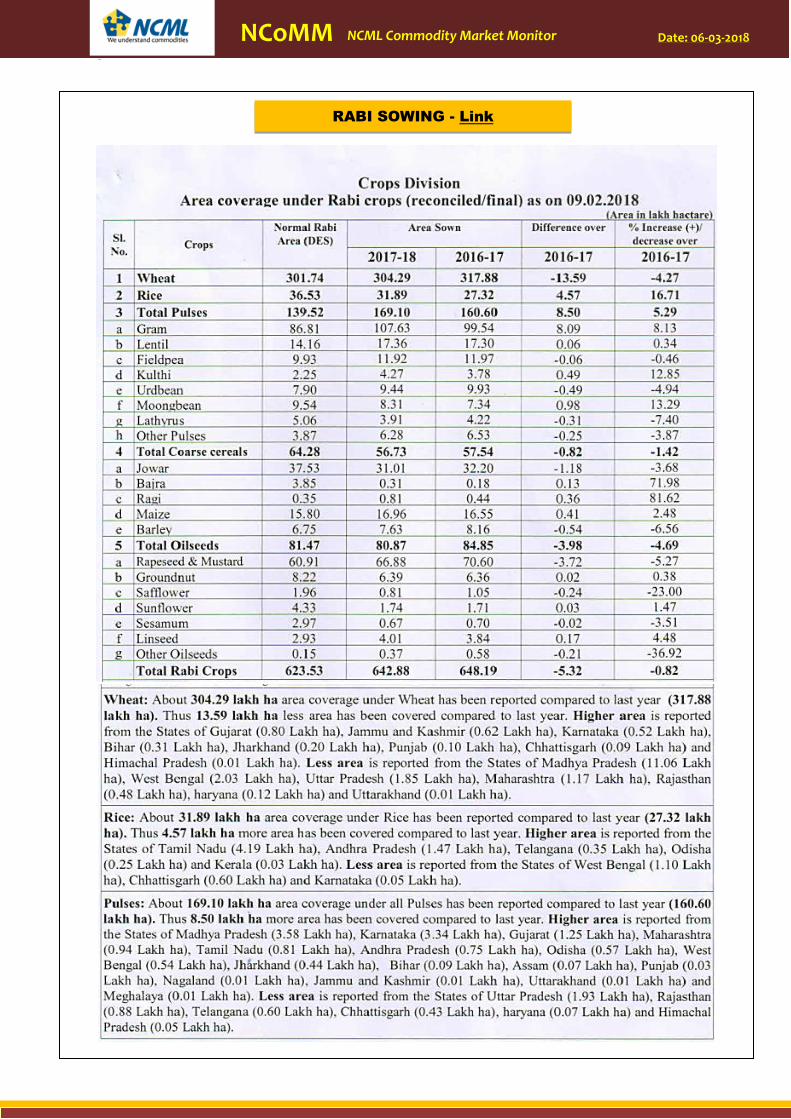

RABI SOWING - Link

0

Date: 06-03-2018 NCoMM NCML Commodity Market Monitor

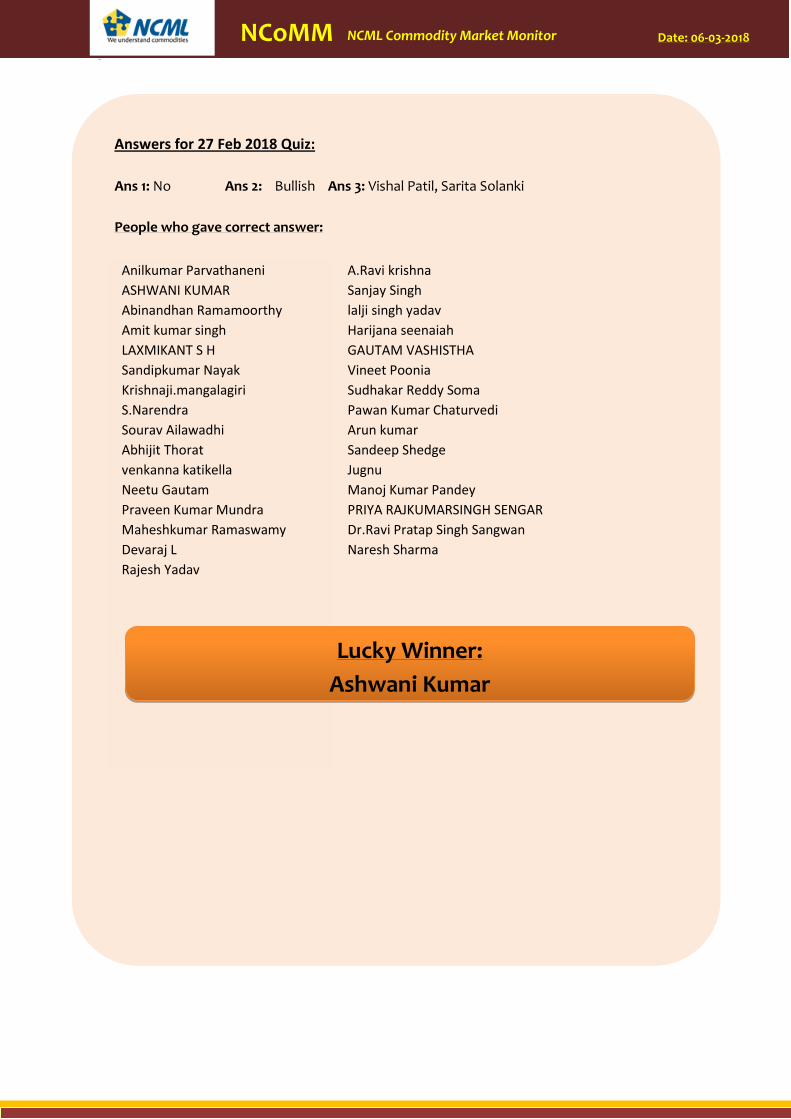

Answers for 27 Feb 2018 Quiz:

Ans 1: No Ans 2: Bullish Ans 3: Vishal Patil, Sarita Solanki

People who gave correct answer:

Anilkumar Parvathaneni

ASHWANI KUMAR

Abinandhan Ramamoorthy

Amit kumar singh

LAXMIKANT S H

Sandipkumar Nayak

Krishnaji.mangalagiri

S.Narendra

Sourav Ailawadhi

Abhijit Thorat

venkanna katikella

Neetu Gautam

Praveen Kumar Mundra

Maheshkumar Ramaswamy

Devaraj L

Rajesh Yadav

A.Ravi krishna

Sanjay Singh

lalji singh yadav

Harijana seenaiah

GAUTAM VASHISTHA

Vineet Poonia

Sudhakar Reddy Soma

Pawan Kumar Chaturvedi

Arun kumar

Sandeep Shedge

Jugnu

Manoj Kumar Pandey

PRIYA RAJKUMARSINGH SENGAR

Dr.Ravi Pratap Singh Sangwan

Naresh Sharma

Lucky Winner:

Ashwani Kumar

0

Date: 06-03-2018 NCoMM NCML Commodity Market Monitor

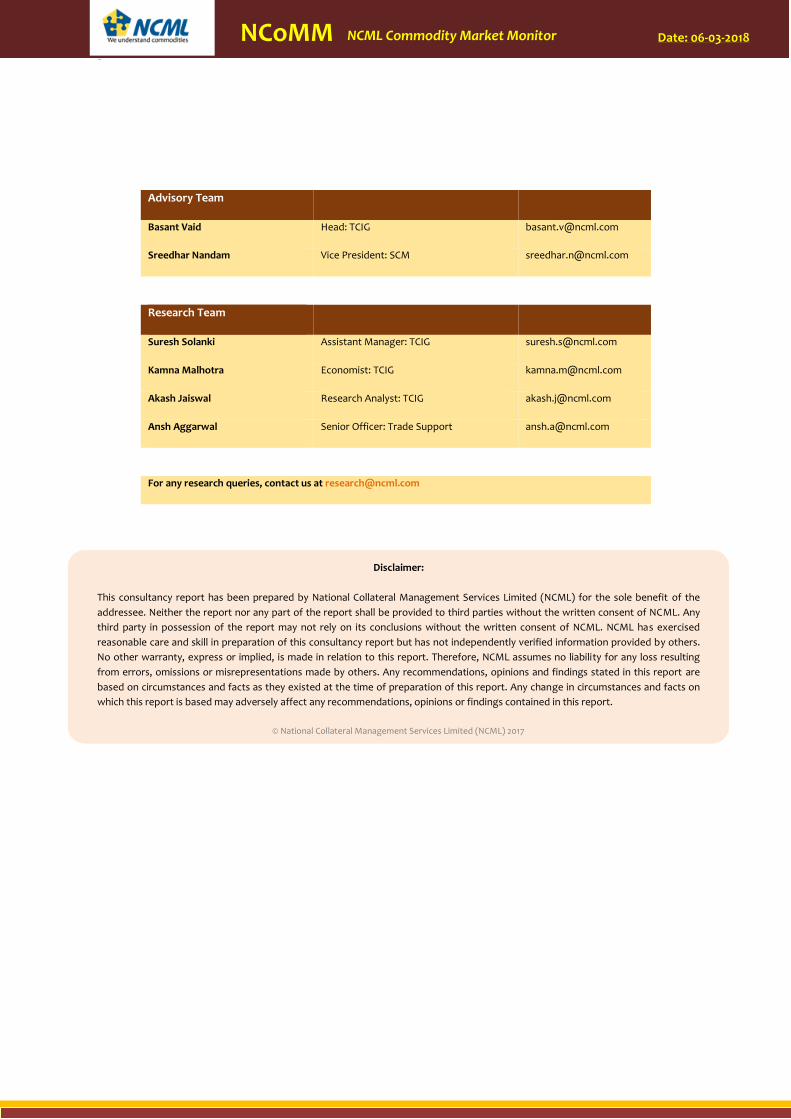

Advisory Team

Basant Vaid Head: TCIG [email protected]

Sreedhar Nandam Vice President: SCM [email protected]

Research Team

Suresh Solanki Assistant Manager: TCIG [email protected]

Kamna Malhotra Economist: TCIG [email protected]

Akash Jaiswal Research Analyst: TCIG [email protected]

Ansh Aggarwal Senior Officer: Trade Support [email protected]

For any research queries, contact us at [email protected]

Disclaimer:

This consultancy report has been prepared by National Collateral Management Services Limited (NCML) for the sole benefit of the

addressee. Neither the report nor any part of the report shall be provided to third parties without the written consent of NCML. Any

third party in possession of the report may not rely on its conclusions without the written consent of NCML. NCML has exercised

reasonable care and skill in preparation of this consultancy report but has not independently verified information provided by others.

No other warranty, express or implied, is made in relation to this report. Therefore, NCML assumes no liability for any loss resulting

from errors, omissions or misrepresentations made by others. Any recommendations, opinions and findings stated in this report are

based on circumstances and facts as they existed at the time of preparation of this report. Any change in circumstances and facts on

which this report is based may adversely affect any recommendations, opinions or findings contained in this report.

© National Collateral Management Services Limited (NCML) 2017