2014 may grayreports - student demand trends

TRANSCRIPT

GRAYREPORTS Demand for Educational Programs

www.GrayAssociates.com

Results through May 2014

617.401.7662 www.GrayAssociates.com 2

GRAY For more information please contact Bob Atkins. Email: [email protected]

Agenda

1. Introduction

2. Demand: National Overview

3. Demand for On-Line Programs

4. Demand for On-Ground Programs

5. Demand by Program and City

6. Demand by Consumer Segment

7. Summary

617.401.7662 www.GrayAssociates.com 3

GRAY For more information please contact Bob Atkins. Email: [email protected]

Key Demand Trends and Observations

1. Data on market demand is now available that can help guide your decisions

2. Overall demand was down slightly in May.

3. Market share is shifting between:

§ On-line and on-ground programs

§ Large programs and smaller programs

§ Largest cities and other cities

§ Traditional segments and more affluent segments

617.401.7662 www.GrayAssociates.com 4

GRAY For more information please contact Bob Atkins. Email: [email protected]

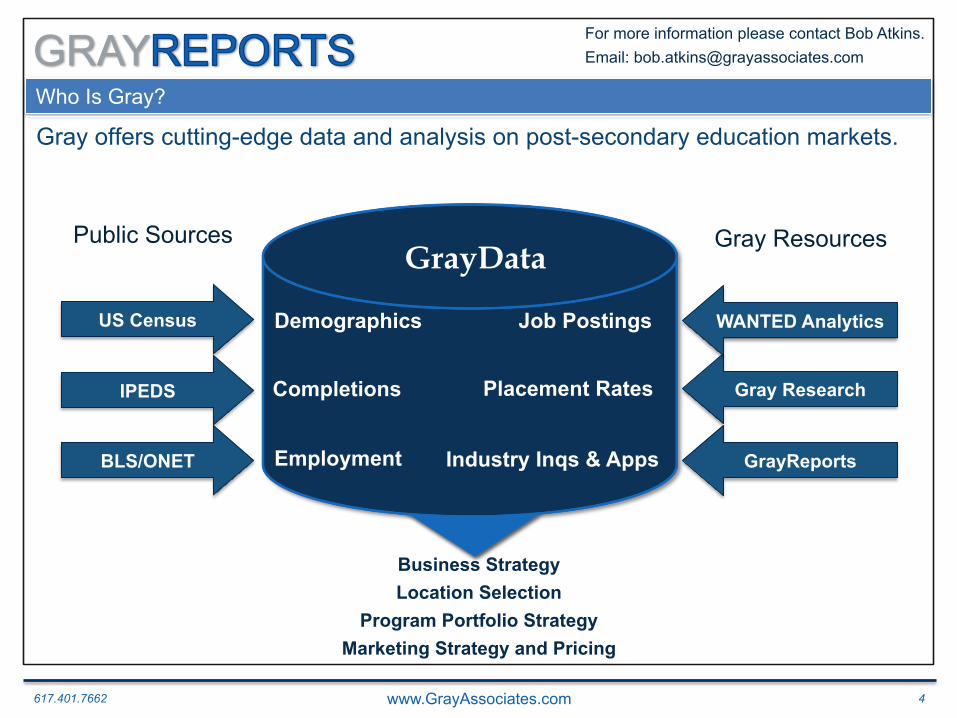

Who Is Gray?

Gray offers cutting-edge data and analysis on post-secondary education markets.

GrayReports

Completions

Employment

GrayData

Placement Rates

Industry Inqs & Apps

Demographics

BLS/ONET

Business Strategy Location Selection

Program Portfolio Strategy Marketing Strategy and Pricing

Gray Research

Job Postings

IPEDS

US Census WANTED Analytics

Public Sources Public Sources Gray Resources

617.401.7662 www.GrayAssociates.com 5

GRAY For more information please contact Bob Atkins. Email: [email protected]

What is GrayReports?

Over 31 million qualified inquiries January 2012 to the present

Over 950,000 new inquiries in April 149 programs with over 10,000 inquiries

257 cities with over 10,000 inquiries

617.401.7662 www.GrayAssociates.com 6

GRAY For more information please contact Bob Atkins. Email: [email protected]

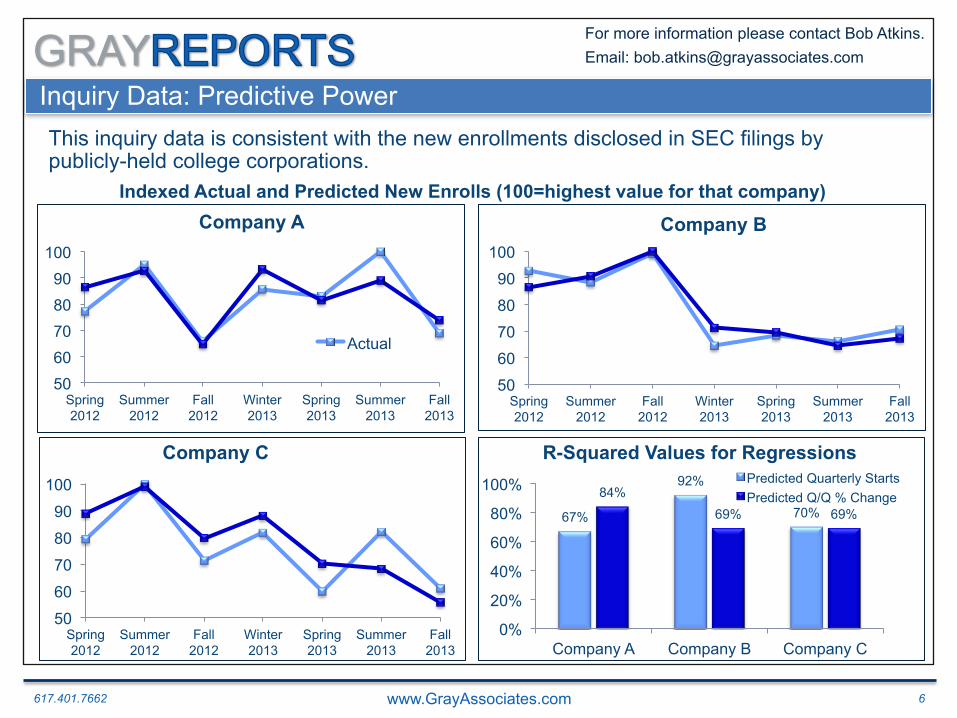

Inquiry Data: Predictive Power This inquiry data is consistent with the new enrollments disclosed in SEC filings by publicly-held college corporations.

Indexed Actual and Predicted New Enrolls (100=highest value for that company)

50 60 70 80 90

100

Spring 2012

Summer 2012

Fall 2012

Winter 2013

Spring 2013

Summer 2013

Fall 2013

Company A

Actual

50

60

70

80

90

100

Spring 2012

Summer 2012

Fall 2012

Winter 2013

Spring 2013

Summer 2013

Fall 2013

Company B

50

60

70

80

90

100

Spring 2012

Summer 2012

Fall 2012

Winter 2013

Spring 2013

Summer 2013

Fall 2013

Company C

67%

92%

70% 84%

69% 69%

0%

20%

40%

60%

80%

100%

Company A Company B Company C

R-Squared Values for Regressions Predicted Quarterly Starts Predicted Q/Q % Change

617.401.7662 www.GrayAssociates.com 7

GRAY For more information please contact Bob Atkins. Email: [email protected]

Agenda

1. Introduction

2. Demand: National Overview

3. Demand for On-Line Programs

4. Demand for On-Ground Programs

5. Demand by Program and City

6. Demand by Consumer Segment

7. Summary

617.401.7662 www.GrayAssociates.com 8

GRAY For more information please contact Bob Atkins. Email: [email protected]

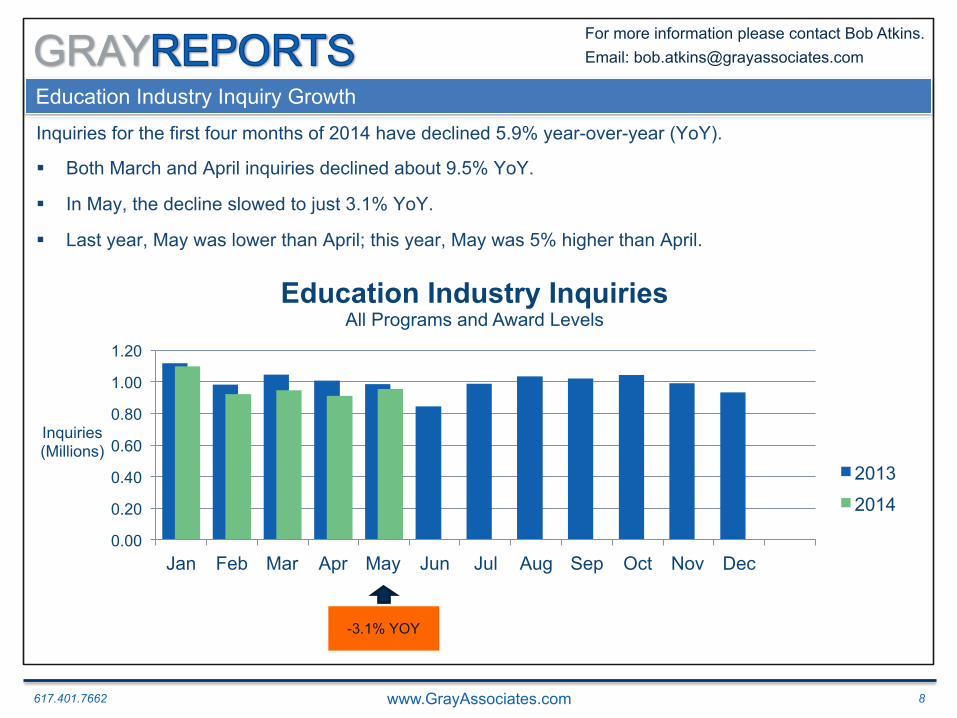

Education Industry Inquiry Growth

Inquiries for the first four months of 2014 have declined 5.9% year-over-year (YoY).

§ Both March and April inquiries declined about 9.5% YoY.

§ In May, the decline slowed to just 3.1% YoY.

§ Last year, May was lower than April; this year, May was 5% higher than April.

2012

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Inquiries (Millions)

Education Industry Inquiries All Programs and Award Levels

2013

2014

-3.1% YOY

617.401.7662 www.GrayAssociates.com 9

GRAY For more information please contact Bob Atkins. Email: [email protected]

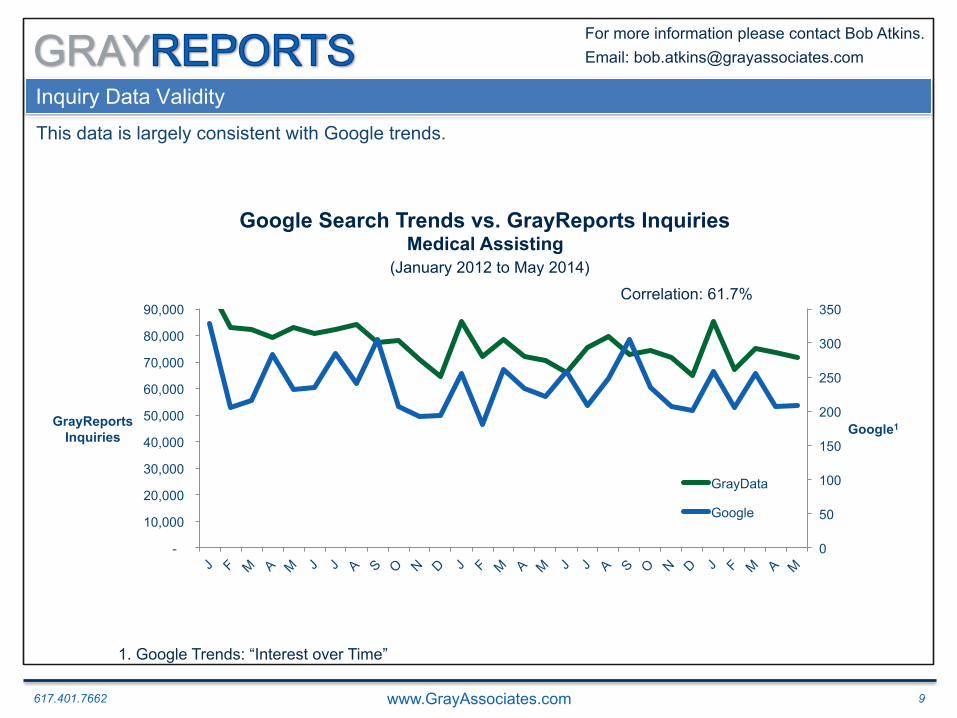

Inquiry Data Validity

This data is largely consistent with Google trends.

0

50

100

150

200

250

300

350

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Google1 GrayReports Inquiries

GrayData

Google Search Trends vs. GrayReports Inquiries Medical Assisting

(January 2012 to May 2014)

1. Google Trends: “Interest over Time”

Correlation: 61.7%

617.401.7662 www.GrayAssociates.com 10

GRAY For more information please contact Bob Atkins. Email: [email protected]

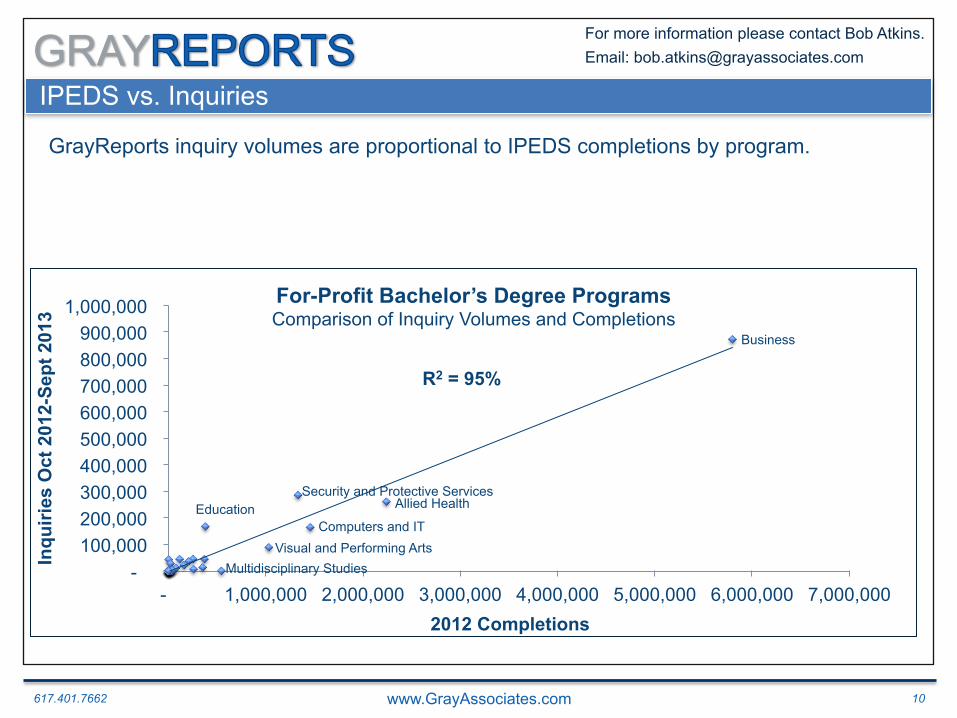

IPEDS vs. Inquiries

R2 = 95%

- 100,000 200,000 300,000 400,000 500,000 600,000 700,000 800,000 900,000

1,000,000

- 1,000,000 2,000,000 3,000,000 4,000,000 5,000,000 6,000,000 7,000,000

Inqu

iries

Oct

201

2-Se

pt 2

013

2012 Completions

For-Profit Bachelor’s Degree Programs Comparison of Inquiry Volumes and Completions

Computers and IT

Business

Security and Protective Services Allied Health

Multidisciplinary Studies Visual and Performing Arts

Education

GrayReports inquiry volumes are proportional to IPEDS completions by program.

617.401.7662 www.GrayAssociates.com 11

GRAY For more information please contact Bob Atkins. Email: [email protected]

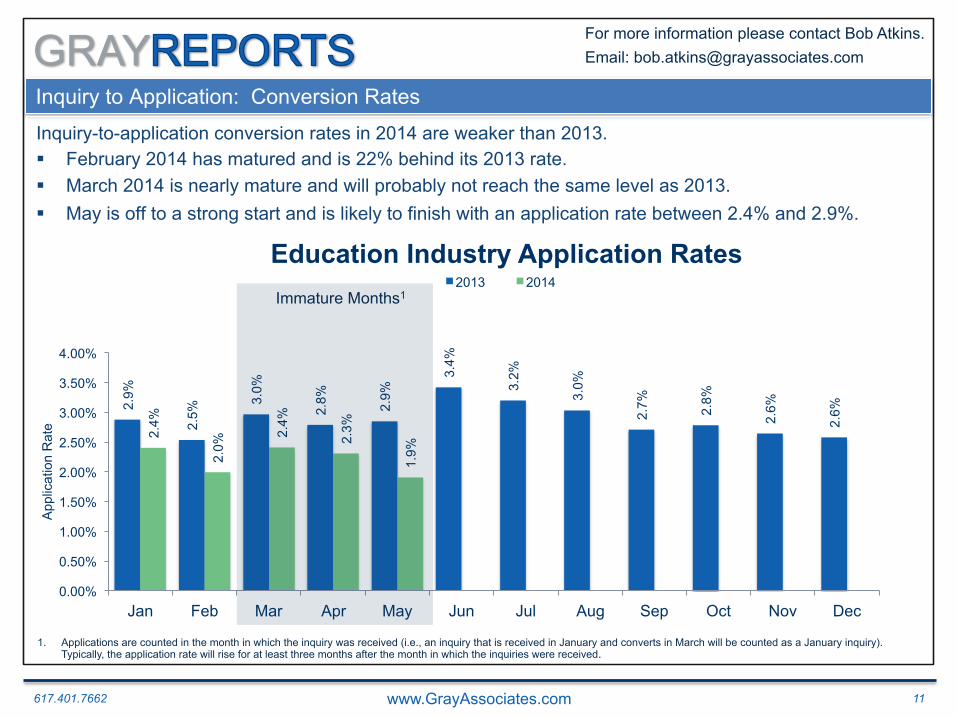

2.9%

2.5%

3.0%

2.8%

2.9%

3.4%

3.2%

3.0%

2.7%

2.8%

2.6%

2.6%

2.4%

2.0%

2.4%

2.3%

1.9%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

App

licat

ion

Rat

e

Education Industry Application Rates 2013 2014

Inquiry to Application: Conversion Rates

Immature Months1

Inquiry-to-application conversion rates in 2014 are weaker than 2013. § February 2014 has matured and is 22% behind its 2013 rate. § March 2014 is nearly mature and will probably not reach the same level as 2013. § May is off to a strong start and is likely to finish with an application rate between 2.4% and 2.9%.

1. Applications are counted in the month in which the inquiry was received (i.e., an inquiry that is received in January and converts in March will be counted as a January inquiry). Typically, the application rate will rise for at least three months after the month in which the inquiries were received.

617.401.7662 www.GrayAssociates.com 12

GRAY For more information please contact Bob Atkins. Email: [email protected]

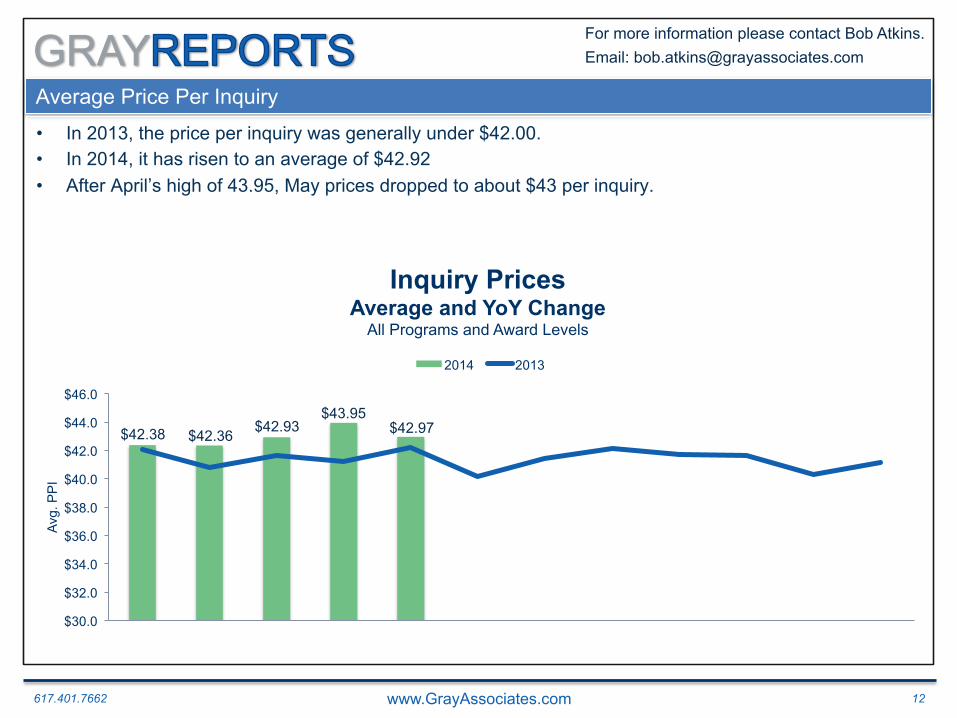

Average Price Per Inquiry

• In 2013, the price per inquiry was generally under $42.00. • In 2014, it has risen to an average of $42.92 • After April’s high of 43.95, May prices dropped to about $43 per inquiry.

$30.0

$32.0

$34.0

$36.0

$38.0

$40.0

$42.0

$44.0

$46.0

Avg.

PP

I

Inquiry Prices Average and YoY Change

All Programs and Award Levels

2014 2013

$42.38 $42.36 $42.93 $43.95

$42.97

617.401.7662 www.GrayAssociates.com 13

GRAY For more information please contact Bob Atkins. Email: [email protected]

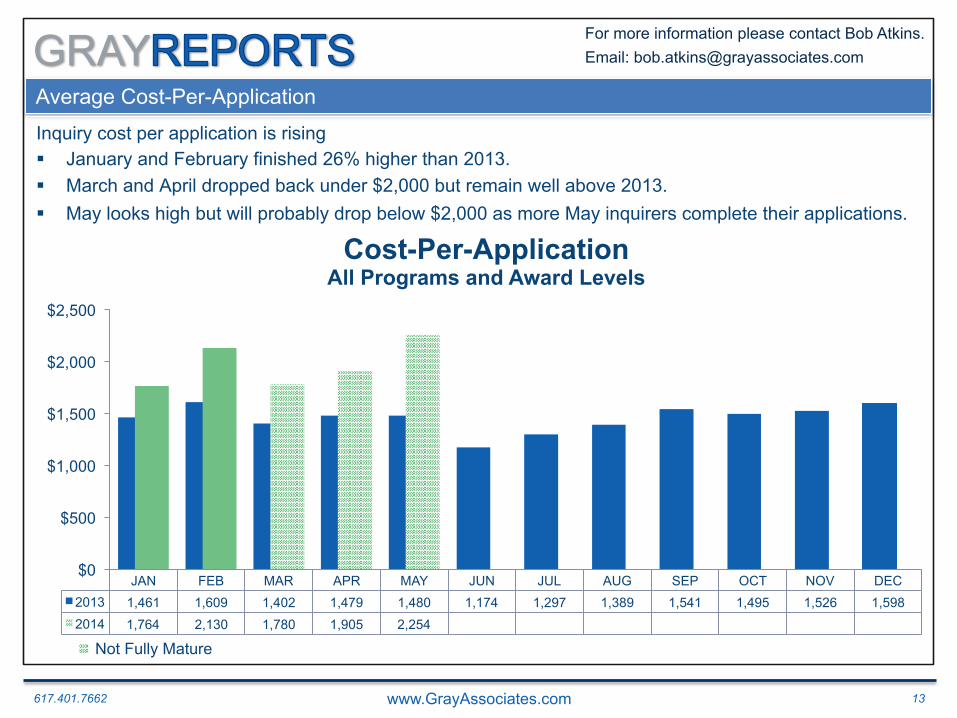

Average Cost-Per-Application

Inquiry cost per application is rising § January and February finished 26% higher than 2013. § March and April dropped back under $2,000 but remain well above 2013. § May looks high but will probably drop below $2,000 as more May inquirers complete their applications.

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC 2013 1,461 1,609 1,402 1,479 1,480 1,174 1,297 1,389 1,541 1,495 1,526 1,598 2014 1,764 2,130 1,780 1,905 2,254

$0

$500

$1,000

$1,500

$2,000

$2,500

Cost-Per-Application All Programs and Award Levels

Not Fully Mature

617.401.7662 www.GrayAssociates.com 14

GRAY For more information please contact Bob Atkins. Email: [email protected]

Agenda

1. Introduction

2. Demand: National Overview

3. Demand for On-Line Programs

4. Demand for On-Ground Programs

5. Demand by Program and City

6. Demand by Consumer Segment

7. Summary

617.401.7662 www.GrayAssociates.com 15

GRAY For more information please contact Bob Atkins. Email: [email protected]

0

100,000

200,000

300,000

400,000

500,000

600,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Inqu

iries

Inquiries for On-Line Programs All Programs and Award Levels

2013

2014

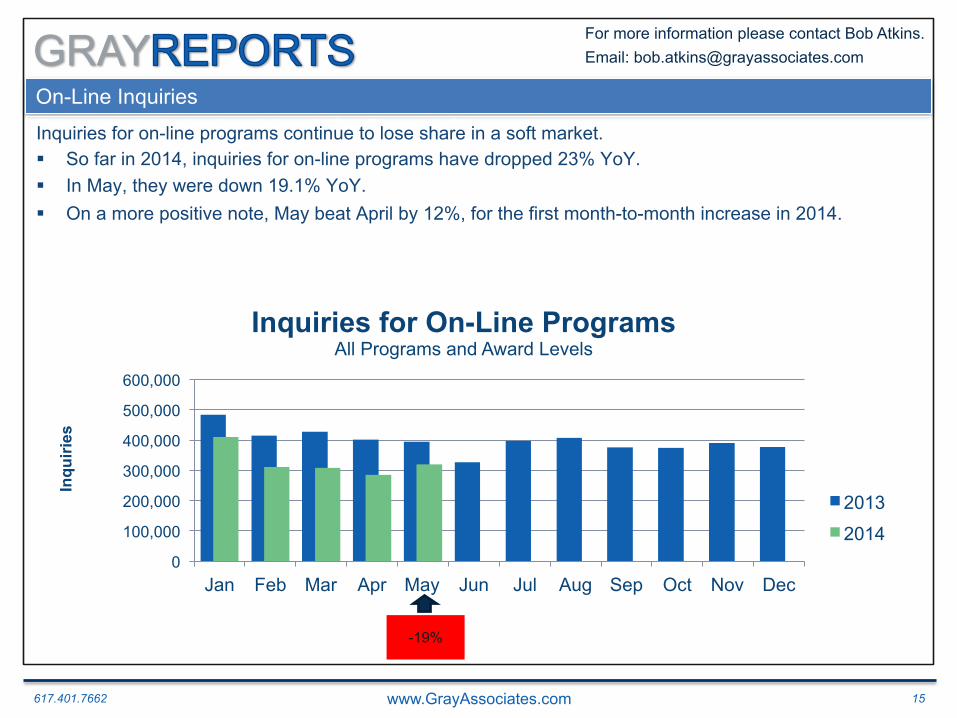

On-Line Inquiries Education Industry Inquiries: YOY Percent Change Inquiries for on-line programs continue to lose share in a soft market. § So far in 2014, inquiries for on-line programs have dropped 23% YoY. § In May, they were down 19.1% YoY. § On a more positive note, May beat April by 12%, for the first month-to-month increase in 2014.

-19%

617.401.7662 www.GrayAssociates.com 16

GRAY For more information please contact Bob Atkins. Email: [email protected]

1.8%

1.8%

2.1%

2.2%

2.1%

3.6%

1.9%

2.1%

2.0%

2.1%

1.8%

1.8%

1.5%

1.3%

1.8%

1.9%

1.7%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

App

licat

ion

Rat

e

On-Line Education Industry Application Rates 2013 2014

On-Line Inquiry to Application: Conversion Rates

Immature Months1

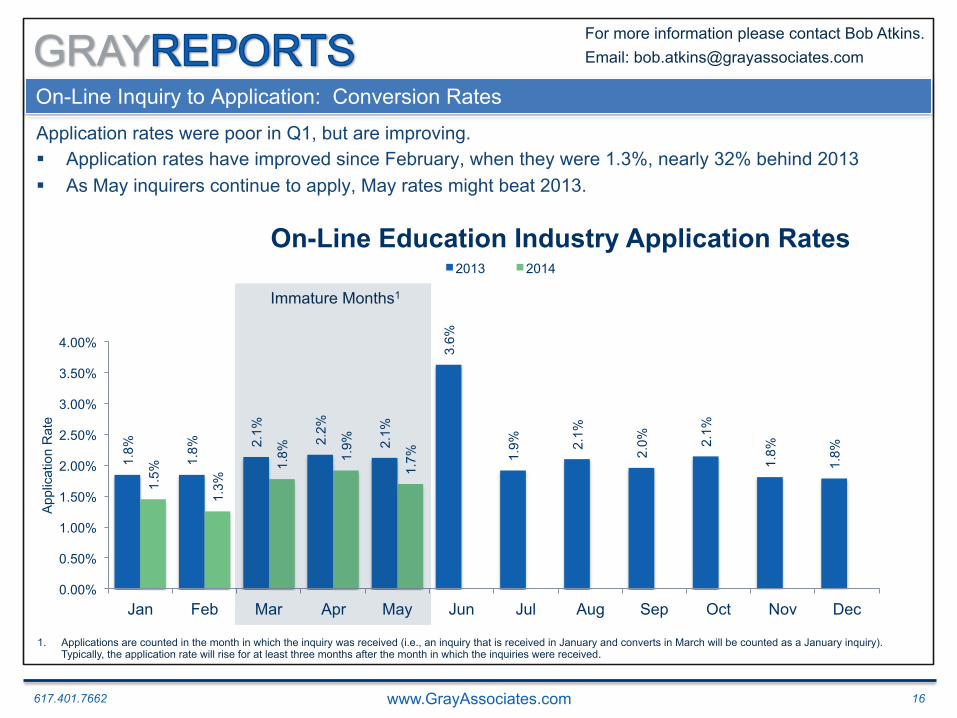

Application rates were poor in Q1, but are improving. § Application rates have improved since February, when they were 1.3%, nearly 32% behind 2013 § As May inquirers continue to apply, May rates might beat 2013.

1. Applications are counted in the month in which the inquiry was received (i.e., an inquiry that is received in January and converts in March will be counted as a January inquiry). Typically, the application rate will rise for at least three months after the month in which the inquiries were received.

617.401.7662 www.GrayAssociates.com 17

GRAY For more information please contact Bob Atkins. Email: [email protected]

On-line Average Price Per Inquiry

Inquiries for on-line programs are getting more expensive. • Until May, price per inquiry rose every month. • May prices were lower than in April but still 10% higher than last year

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

$40.0

$45.0

$50.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Avg.

PP

I

On-line Inquiry Prices Average and YoY Change

All Programs and Award Levels

2014 2013

$41.94 $42.45 $43.53 $45.91 $44.41

617.401.7662 www.GrayAssociates.com 18

GRAY For more information please contact Bob Atkins. Email: [email protected]

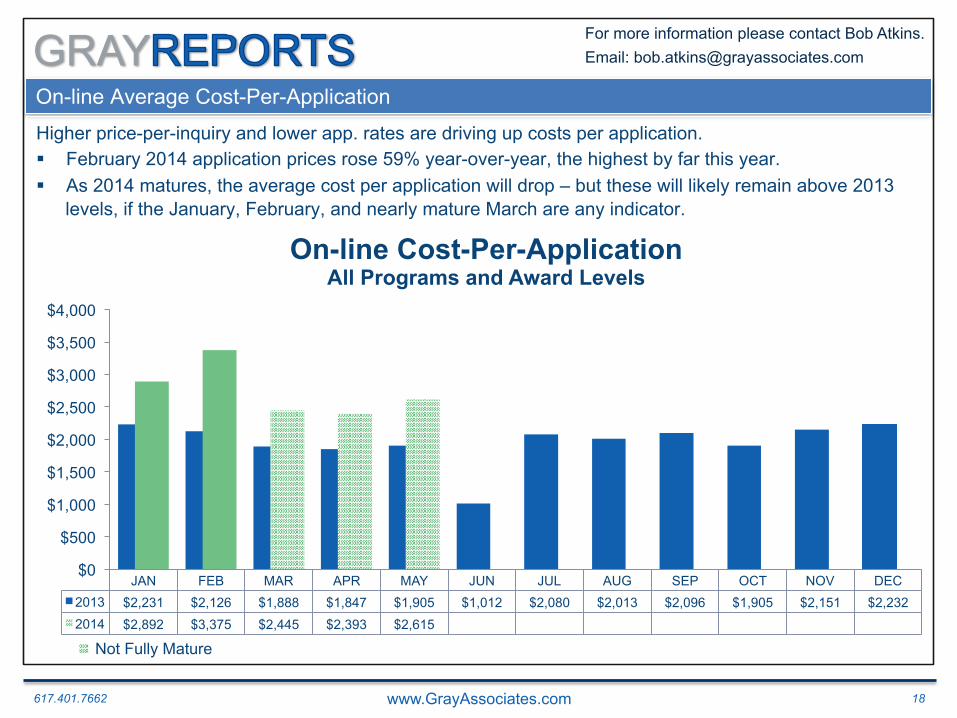

On-line Average Cost-Per-Application

Higher price-per-inquiry and lower app. rates are driving up costs per application. § February 2014 application prices rose 59% year-over-year, the highest by far this year. § As 2014 matures, the average cost per application will drop – but these will likely remain above 2013

levels, if the January, February, and nearly mature March are any indicator.

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC 2013 $2,231 $2,126 $1,888 $1,847 $1,905 $1,012 $2,080 $2,013 $2,096 $1,905 $2,151 $2,232 2014 $2,892 $3,375 $2,445 $2,393 $2,615

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

On-line Cost-Per-Application All Programs and Award Levels

Not Fully Mature

617.401.7662 www.GrayAssociates.com 19

GRAY For more information please contact Bob Atkins. Email: [email protected]

Agenda

1. Introduction

2. Demand: National Overview

3. Demand for On-Line Programs

4. Demand for On-Ground Programs

5. Demand by Program and City

6. Demand by Consumer Segment

7. Summary

617.401.7662 www.GrayAssociates.com 20

GRAY For more information please contact Bob Atkins. Email: [email protected]

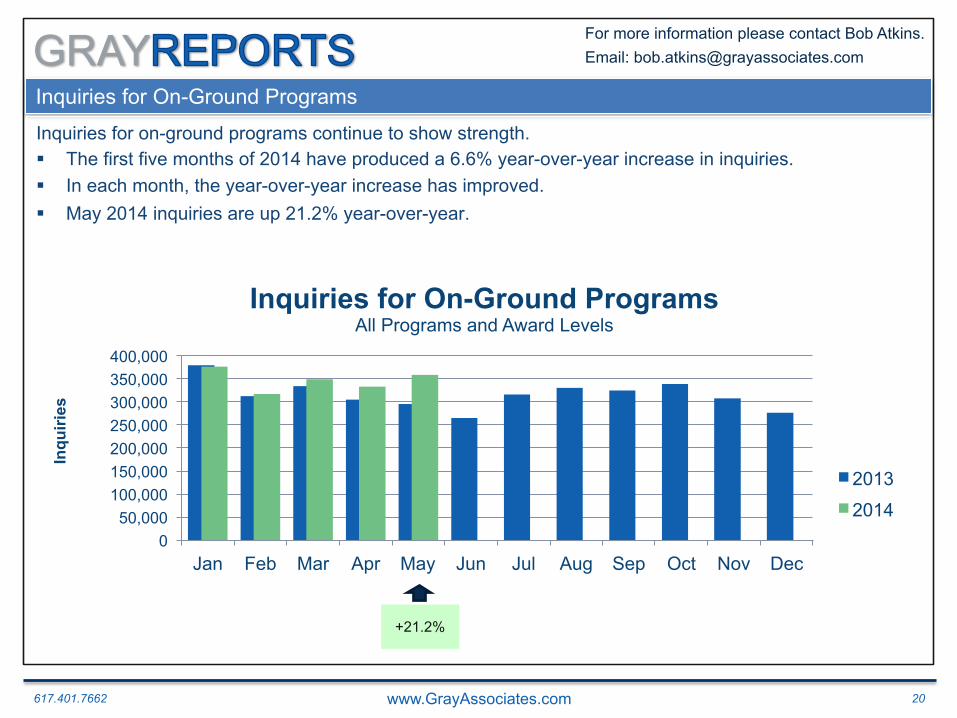

Inquiries for On-Ground Programs

Inquiries for on-ground programs continue to show strength. § The first five months of 2014 have produced a 6.6% year-over-year increase in inquiries. § In each month, the year-over-year increase has improved. § May 2014 inquiries are up 21.2% year-over-year.

2012

0 50,000

100,000 150,000 200,000 250,000 300,000 350,000 400,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Inqu

iries

Inquiries for On-Ground Programs All Programs and Award Levels

2013

2014

+21.2%

617.401.7662 www.GrayAssociates.com 21

GRAY For more information please contact Bob Atkins. Email: [email protected]

4.1%

3.5%

4.5%

4.1%

4.3%

4.0%

5.5%

3.8%

3.9%

3.8%

3.8%

4.0%

2.9%

2.4%

2.9%

2.7%

2.3%

0%

1%

2%

3%

4%

5%

6%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Inquiry-to- Application

Conversion Rate

Education Industry Application Rates 2013 2014

On-Ground Inquiry to Application: Conversion Rates

Immature Months1

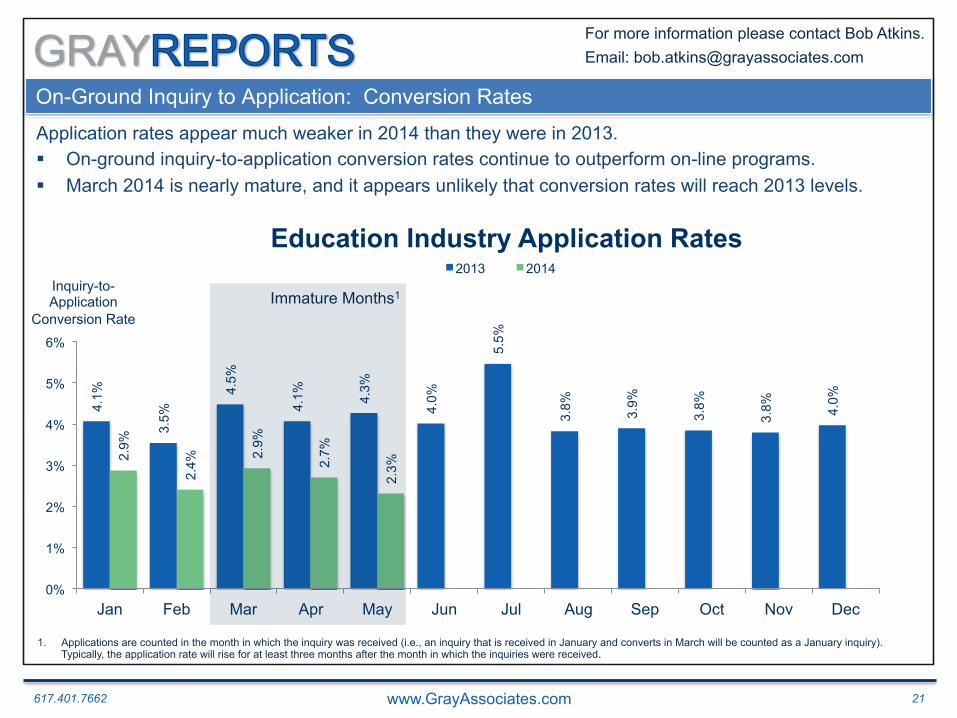

Application rates appear much weaker in 2014 than they were in 2013. § On-ground inquiry-to-application conversion rates continue to outperform on-line programs. § March 2014 is nearly mature, and it appears unlikely that conversion rates will reach 2013 levels.

1. Applications are counted in the month in which the inquiry was received (i.e., an inquiry that is received in January and converts in March will be counted as a January inquiry). Typically, the application rate will rise for at least three months after the month in which the inquiries were received.

617.401.7662 www.GrayAssociates.com 22

GRAY For more information please contact Bob Atkins. Email: [email protected]

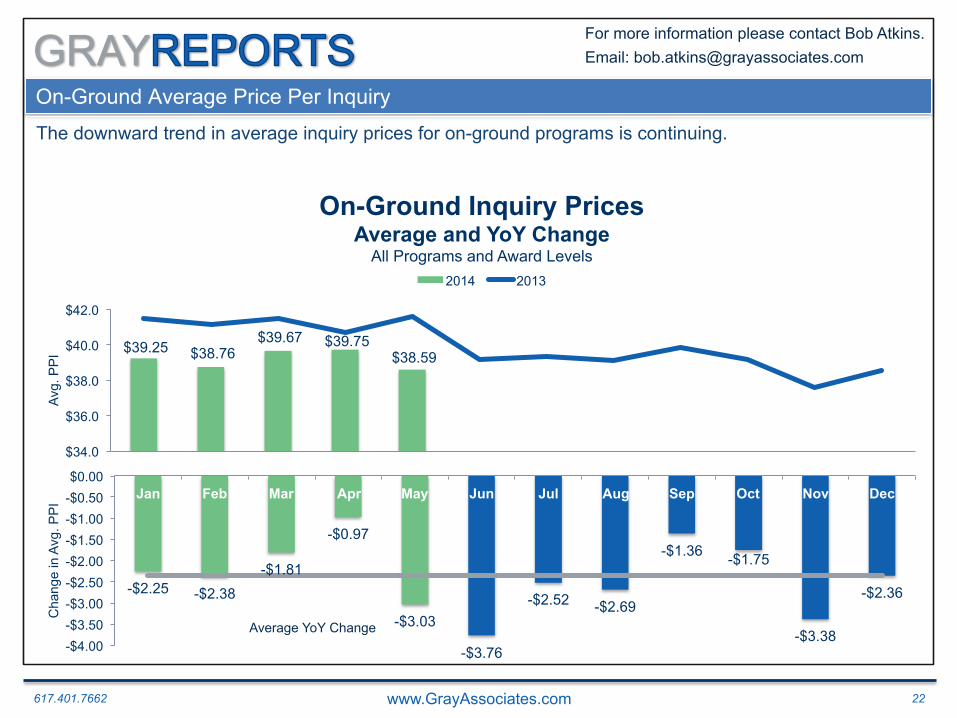

On-Ground Average Price Per Inquiry

The downward trend in average inquiry prices for on-ground programs is continuing.

$39.25 $38.76 $39.67 $39.75

$38.59

$34.0

$36.0

$38.0

$40.0

$42.0

Avg.

PP

I

On-Ground Inquiry Prices Average and YoY Change

All Programs and Award Levels 2014 2013

-$2.25 -$2.38 -$1.81

-$0.97

-$3.03

-$3.76

-$2.52 -$2.69

-$1.36 -$1.75

-$3.38

-$2.36

-$4.00 -$3.50 -$3.00 -$2.50 -$2.00 -$1.50 -$1.00 -$0.50 $0.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Cha

nge

in A

vg. P

PI

Average YoY Change

617.401.7662 www.GrayAssociates.com 23

GRAY For more information please contact Bob Atkins. Email: [email protected]

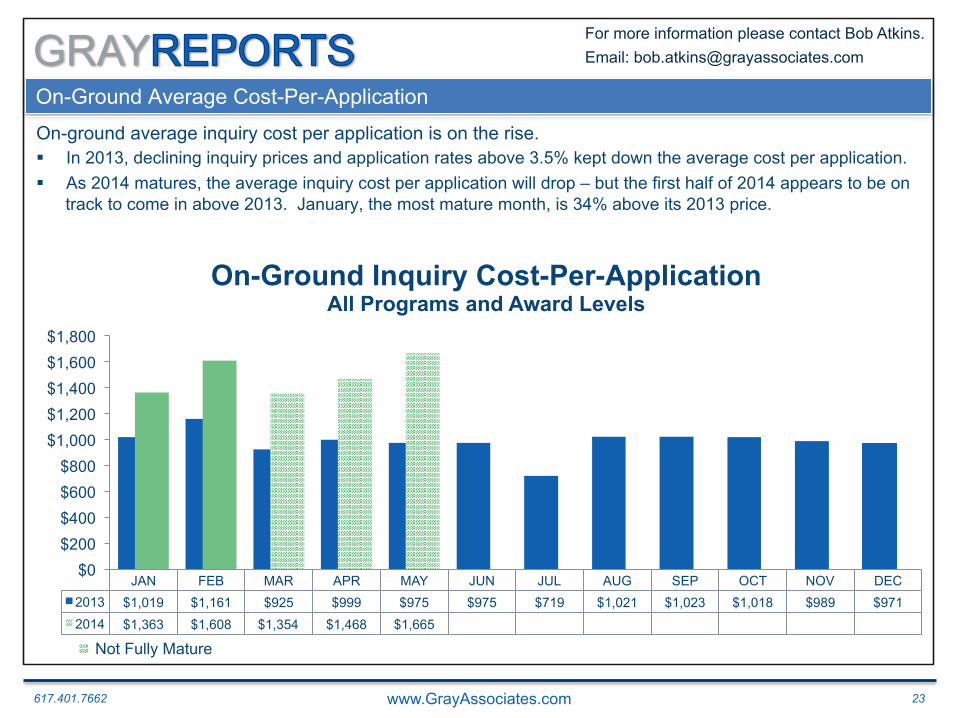

On-Ground Average Cost-Per-Application

On-ground average inquiry cost per application is on the rise. § In 2013, declining inquiry prices and application rates above 3.5% kept down the average cost per application. § As 2014 matures, the average inquiry cost per application will drop – but the first half of 2014 appears to be on

track to come in above 2013. January, the most mature month, is 34% above its 2013 price.

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC 2013 $1,019 $1,161 $925 $999 $975 $975 $719 $1,021 $1,023 $1,018 $989 $971 2014 $1,363 $1,608 $1,354 $1,468 $1,665

$0 $200 $400 $600 $800

$1,000 $1,200 $1,400 $1,600 $1,800

On-Ground Inquiry Cost-Per-Application All Programs and Award Levels

Not Fully Mature

617.401.7662 www.GrayAssociates.com 24

GRAY For more information please contact Bob Atkins. Email: [email protected]

Agenda

1. Introduction

2. Demand: National Overview

3. Demand for On-Line Programs

4. Demand for On-Ground Programs

5. Demand by Program and City

6. Demand by Consumer Segment

7. Summary

617.401.7662 www.GrayAssociates.com 25

GRAY For more information please contact Bob Atkins. Email: [email protected]

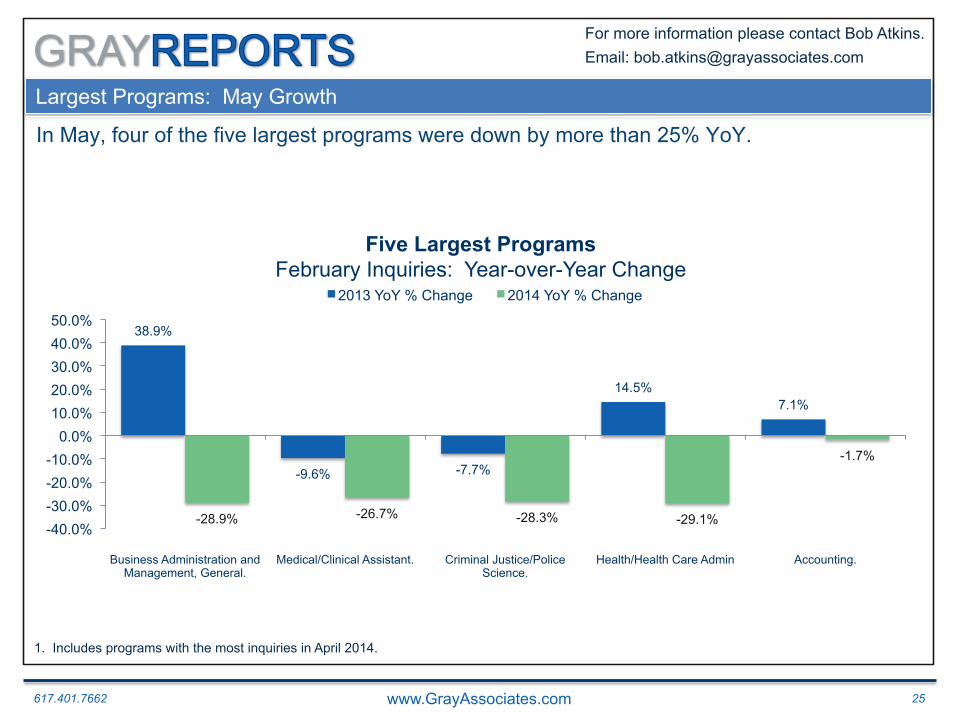

Largest Programs: May Growth

In May, four of the five largest programs were down by more than 25% YoY.

38.9%

-9.6% -7.7%

14.5% 7.1%

-28.9% -26.7% -28.3% -29.1%

-1.7%

-40.0% -30.0% -20.0% -10.0%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0%

Business Administration and Management, General.

Medical/Clinical Assistant. Criminal Justice/Police Science.

Health/Health Care Admin Accounting.

Five Largest Programs February Inquiries: Year-over-Year Change

2013 YoY % Change 2014 YoY % Change

1. Includes programs with the most inquiries in April 2014.

617.401.7662 www.GrayAssociates.com 26

GRAY For more information please contact Bob Atkins. Email: [email protected]

Top 5 Fastest-Growing Programs in May

The five fastest-growing programs1 all grew over 95% year-over-year in May. § Two are traditional hands-on trade programs: Welding and Electrical Technician. § Health Information/Medical Records came in third, with over 100% growth. § The we have two programs that are new to list, Photography and Applied Behavior Analysis.

78.7%

-17.0%

61.5%

-9.2%

331.9%

206.6%

121.1% 98.7% 96.8%

-50.0% 0.0%

50.0% 100.0% 150.0% 200.0% 250.0% 300.0% 350.0% 400.0%

Welding Tech./Welder. Photography. Health Information/Medical Records Admin.

Electrical, Electronic & Comms. Engineering

Tech.

Applied Behavior Analysis.

Industry Inquiries Fastest Growing Programs – April 2014

2013 YoY % Change 2014 YoY % Change

1. Includes only programs within the top 75 for total inquiries since January 2012.

617.401.7662 www.GrayAssociates.com 27

GRAY For more information please contact Bob Atkins. Email: [email protected]

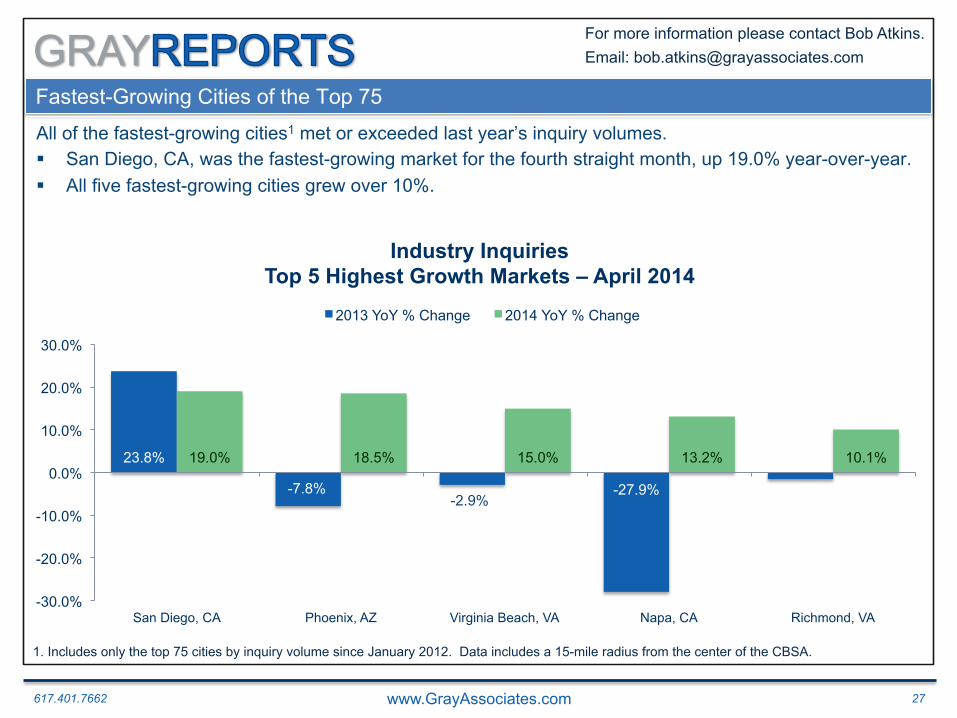

Fastest-Growing Cities of the Top 75

All of the fastest-growing cities1 met or exceeded last year’s inquiry volumes. § San Diego, CA, was the fastest-growing market for the fourth straight month, up 19.0% year-over-year. § All five fastest-growing cities grew over 10%.

23.8%

-7.8% -2.9%

-27.9% -1.6%

19.0% 18.5% 15.0% 13.2% 10.1%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

San Diego, CA Phoenix, AZ Virginia Beach, VA Napa, CA Richmond, VA

Industry Inquiries Top 5 Highest Growth Markets – April 2014

2013 YoY % Change 2014 YoY % Change

1. Includes only the top 75 cities by inquiry volume since January 2012. Data includes a 15-mile radius from the center of the CBSA.

617.401.7662 www.GrayAssociates.com 28

GRAY For more information please contact Bob Atkins. Email: [email protected]

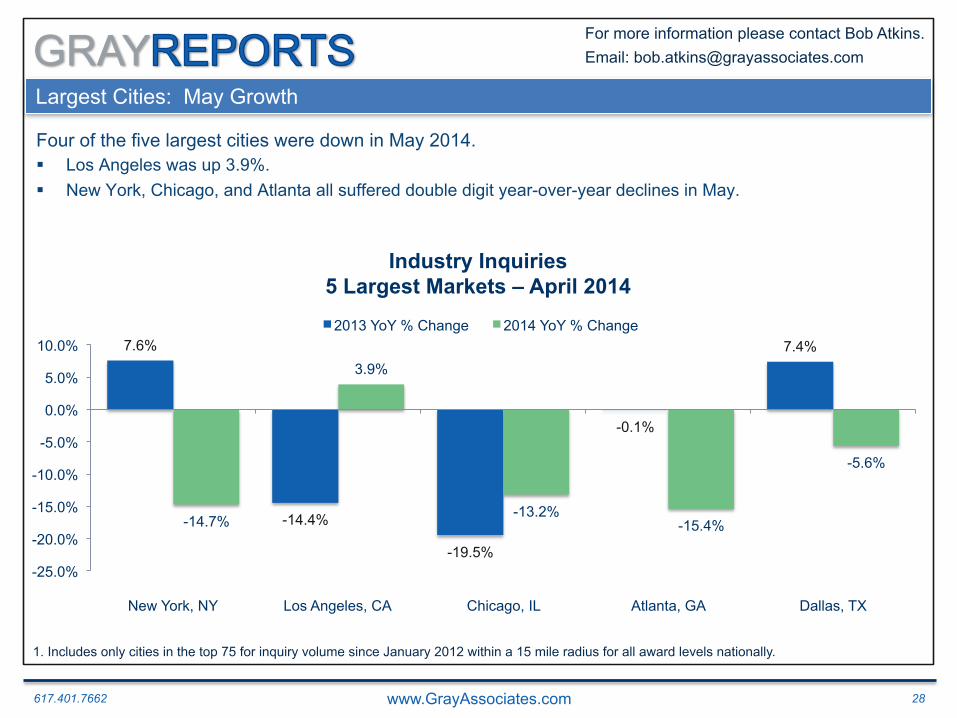

Largest Cities: May Growth

Four of the five largest cities were down in May 2014. § Los Angeles was up 3.9%. § New York, Chicago, and Atlanta all suffered double digit year-over-year declines in May.

7.6%

-14.4%

-19.5%

-0.1%

7.4%

-14.7%

3.9%

-13.2% -15.4%

-5.6%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

New York, NY Los Angeles, CA Chicago, IL Atlanta, GA Dallas, TX

Industry Inquiries 5 Largest Markets – April 2014

2013 YoY % Change 2014 YoY % Change

1. Includes only cities in the top 75 for inquiry volume since January 2012 within a 15 mile radius for all award levels nationally.

617.401.7662 www.GrayAssociates.com 29

GRAY For more information please contact Bob Atkins. Email: [email protected]

Agenda

1. Introduction

2. Demand: National Overview

3. Demand for On-Line Programs

4. Demand for On-Ground Programs

5. Demand by Program and City

6. Demand by Consumer Segment

7. Summary

617.401.7662 www.GrayAssociates.com 30

GRAY For more information please contact Bob Atkins. Email: [email protected]

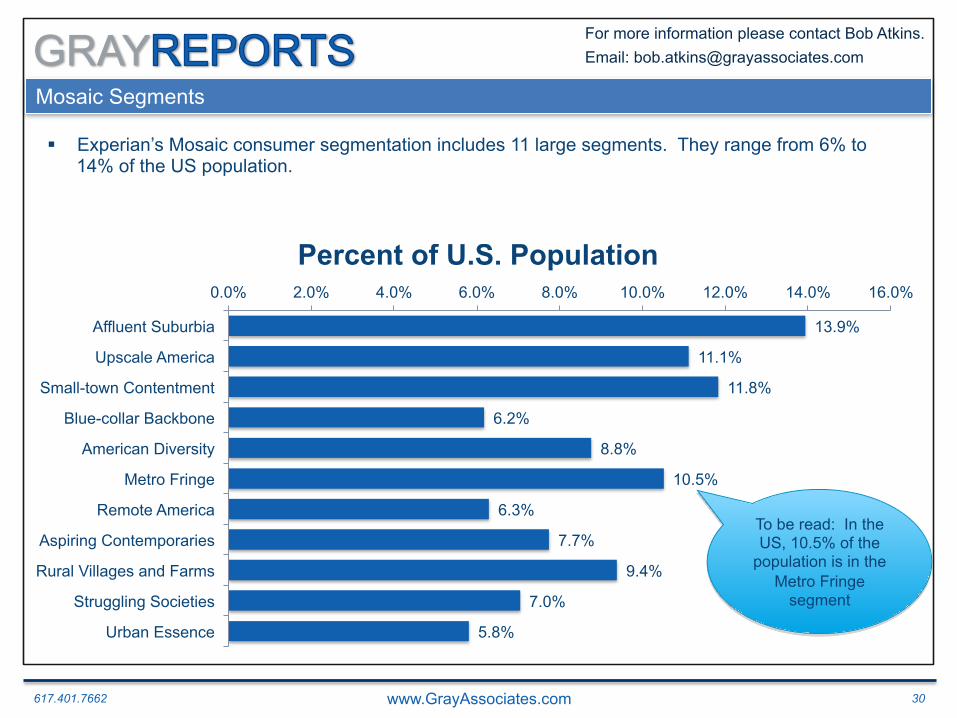

Mosaic Segments

13.9%

11.1%

11.8%

6.2%

8.8%

10.5%

6.3%

7.7%

9.4%

7.0%

5.8%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0%

Affluent Suburbia

Upscale America

Small-town Contentment

Blue-collar Backbone

American Diversity

Metro Fringe

Remote America

Aspiring Contemporaries

Rural Villages and Farms

Struggling Societies

Urban Essence

Percent of U.S. Population

§ Experian’s Mosaic consumer segmentation includes 11 large segments. They range from 6% to 14% of the US population.

To be read: In the US, 10.5% of the

population is in the Metro Fringe

segment

617.401.7662 www.GrayAssociates.com 31

GRAY For more information please contact Bob Atkins. Email: [email protected]

High-Demand Tracts

§ 74,000 total tracts in the US § 15,000 high-demand tracts

§ Top 20% of tracts in inquiry volume

§ Average of 800 inquiries per tract

617.401.7662 www.GrayAssociates.com 32

GRAY For more information please contact Bob Atkins. Email: [email protected]

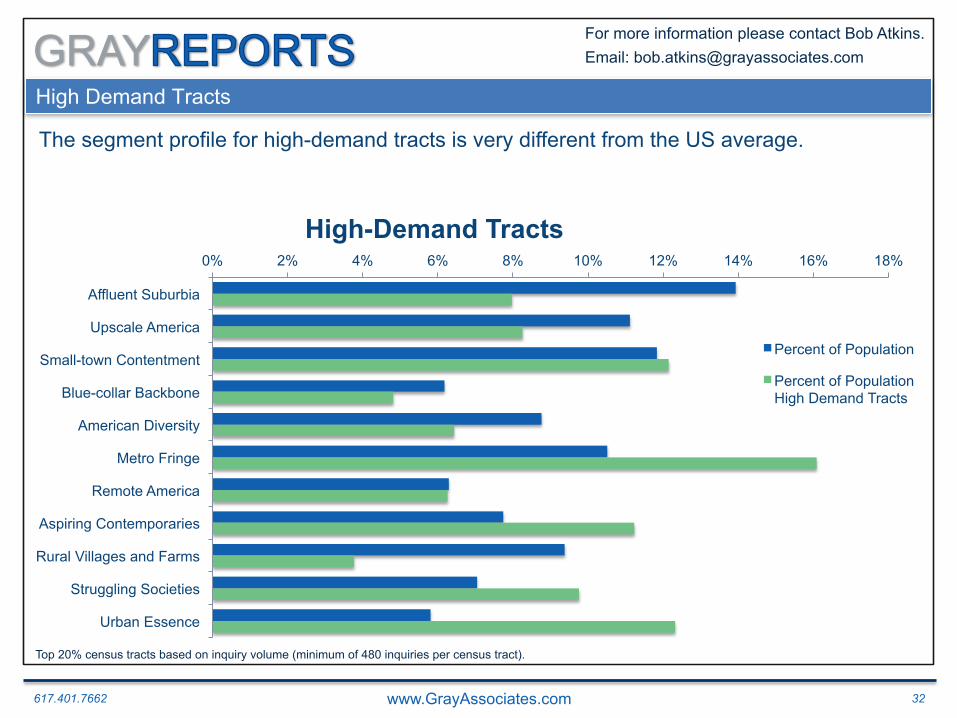

High Demand Tracts

The segment profile for high-demand tracts is very different from the US average.

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Affluent Suburbia

Upscale America

Small-town Contentment

Blue-collar Backbone

American Diversity

Metro Fringe

Remote America

Aspiring Contemporaries

Rural Villages and Farms

Struggling Societies

Urban Essence

High-Demand Tracts

Percent of Population

Percent of Population High Demand Tracts

Top 20% census tracts based on inquiry volume (minimum of 480 inquiries per census tract).

617.401.7662 www.GrayAssociates.com 33

GRAY For more information please contact Bob Atkins. Email: [email protected]

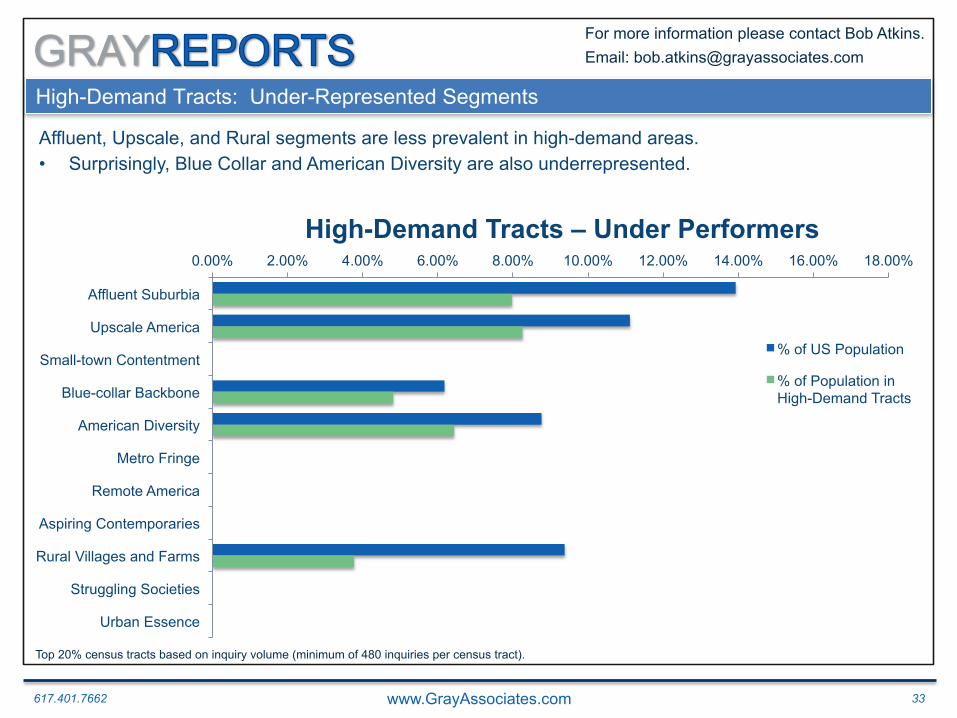

High-Demand Tracts: Under-Represented Segments

Affluent, Upscale, and Rural segments are less prevalent in high-demand areas. • Surprisingly, Blue Collar and American Diversity are also underrepresented.

0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00% 16.00% 18.00%

Affluent Suburbia

Upscale America

Small-town Contentment

Blue-collar Backbone

American Diversity

Metro Fringe

Remote America

Aspiring Contemporaries

Rural Villages and Farms

Struggling Societies

Urban Essence

High-Demand Tracts – Under Performers

% of US Population

% of Population in High-Demand Tracts

Top 20% census tracts based on inquiry volume (minimum of 480 inquiries per census tract).

617.401.7662 www.GrayAssociates.com 34

GRAY For more information please contact Bob Atkins. Email: [email protected]

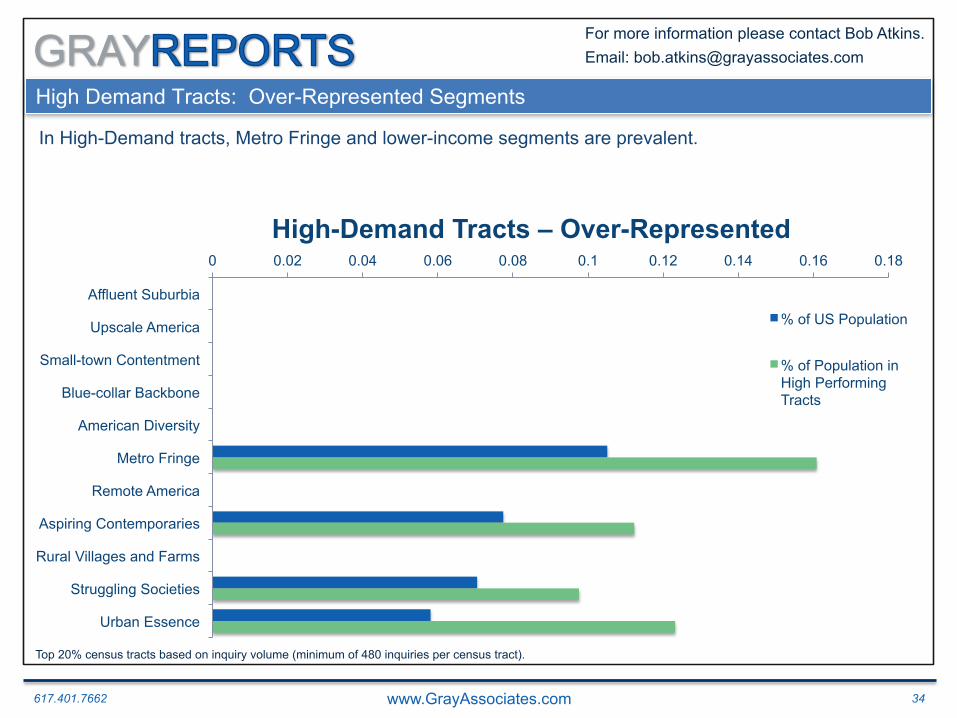

High Demand Tracts: Over-Represented Segments

In High-Demand tracts, Metro Fringe and lower-income segments are prevalent.

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18

Affluent Suburbia

Upscale America

Small-town Contentment

Blue-collar Backbone

American Diversity

Metro Fringe

Remote America

Aspiring Contemporaries

Rural Villages and Farms

Struggling Societies

Urban Essence

High-Demand Tracts – Over-Represented

% of US Population

% of Population in High Performing Tracts

Top 20% census tracts based on inquiry volume (minimum of 480 inquiries per census tract).

617.401.7662 www.GrayAssociates.com 35

GRAY For more information please contact Bob Atkins. Email: [email protected]

Metro Fringe

Steadfast Conservatives, Moderate Conventionalists, Southern Blues, Urban Grit, Grass-roots Living

• Metro Fringe is a collection of five racially mixed, lower-middle-class Types located primarily in satellite cities such as Kissimmee, Fla.; Flint, Mich.; Joliet, Ill.; and Fresno, Calif.

• Many of the group’s households consist of young singles and couples who work at blue-collar and service-industry jobs. They tend to live in older single-family homes, semidetached houses and low-rise apartments.

• Overall, this group is relatively active and pursues sports-oriented lifestyles, participating in activities such as soccer and softball, rollerblading and skateboarding, go-carting and video-gaming.

• As shoppers, they patronize discount retailers, where they buy the latest fashion and tech gear at low prices.

• In their homes, they’re fans of electronic media, whether it’s watching youth- oriented cable channels like Spike TV, FX and Cartoon Network or going online to chat, search job listings or download music.

617.401.7662 www.GrayAssociates.com 36

GRAY For more information please contact Bob Atkins. Email: [email protected]

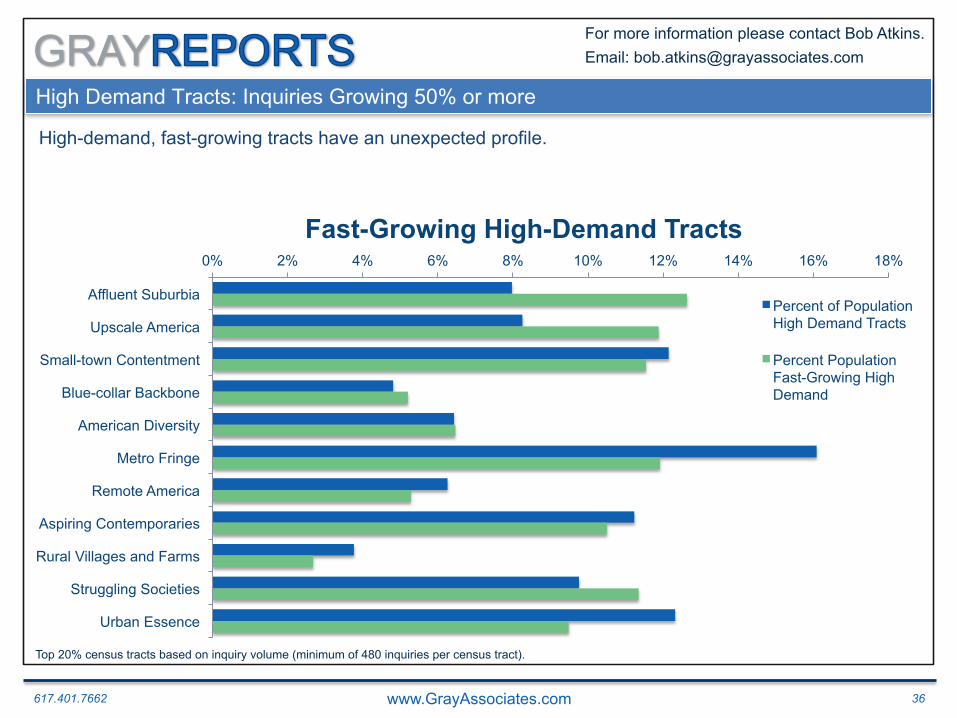

High Demand Tracts: Inquiries Growing 50% or more

High-demand, fast-growing tracts have an unexpected profile.

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Affluent Suburbia

Upscale America

Small-town Contentment

Blue-collar Backbone

American Diversity

Metro Fringe

Remote America

Aspiring Contemporaries

Rural Villages and Farms

Struggling Societies

Urban Essence

Fast-Growing High-Demand Tracts

Percent of Population High Demand Tracts

Percent Population Fast-Growing High Demand

Top 20% census tracts based on inquiry volume (minimum of 480 inquiries per census tract).

617.401.7662 www.GrayAssociates.com 37

GRAY For more information please contact Bob Atkins. Email: [email protected]

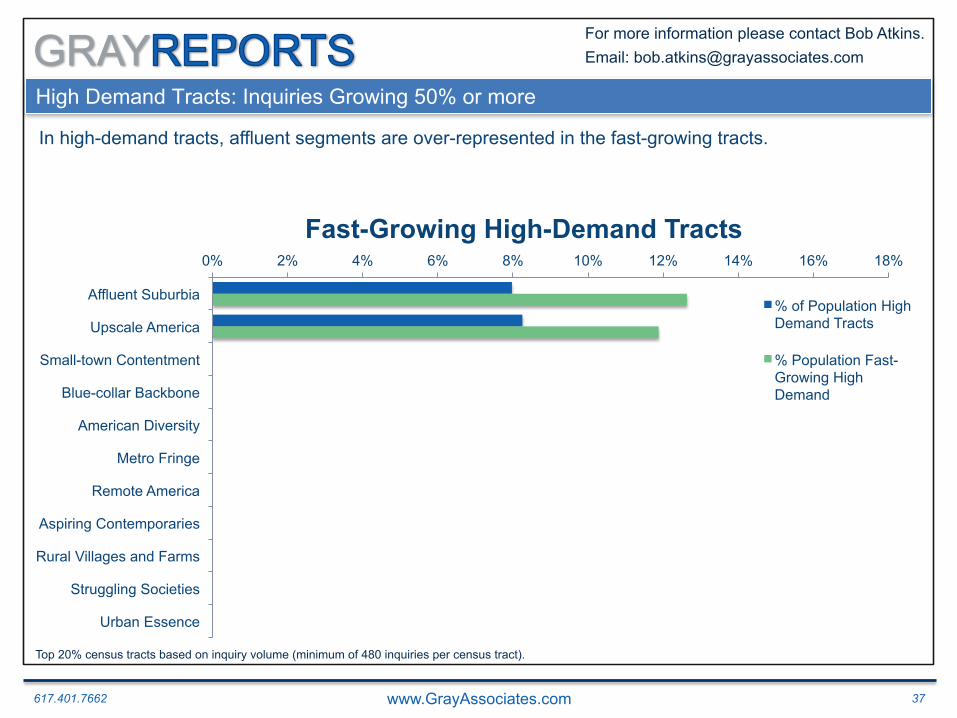

High Demand Tracts: Inquiries Growing 50% or more

In high-demand tracts, affluent segments are over-represented in the fast-growing tracts.

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Affluent Suburbia

Upscale America

Small-town Contentment

Blue-collar Backbone

American Diversity

Metro Fringe

Remote America

Aspiring Contemporaries

Rural Villages and Farms

Struggling Societies

Urban Essence

Fast-Growing High-Demand Tracts

% of Population High Demand Tracts

% Population Fast-Growing High Demand

Top 20% census tracts based on inquiry volume (minimum of 480 inquiries per census tract).

617.401.7662 www.GrayAssociates.com 38

GRAY For more information please contact Bob Atkins. Email: [email protected]

Affluent Suburbia

America’s Wealthiest, Dream Weavers, White-collar Suburbia, Upscale Suburbanites… § The seven Types in the Affluent Suburbia

group comprise the wealthiest households in the nation. These segments outrank all other Mosaic USA Types in terms of household income, home value and educational achievement.

§ Concentrated in exclusive suburban neighborhoods, these households are predominantly white, college-educated, and filled with baby-boom parents and their children.

§ With their managerial and executive positions paying six-figure-plus incomes, they enjoy the good life in fashionable houses outfitted with the latest technology.

§ These are the Americans who drive luxury cars, belong to country clubs, travel abroad, and relax by sailing, golfing or skiing. Many are culture buffs who attend the theater, art shows, dance performances and concerts, all at high rates.

§ Both their purchasing behavior and media choices reflect their interests in money management, travel, computers and gourmet foods.

617.401.7662 www.GrayAssociates.com 39

GRAY For more information please contact Bob Atkins. Email: [email protected]

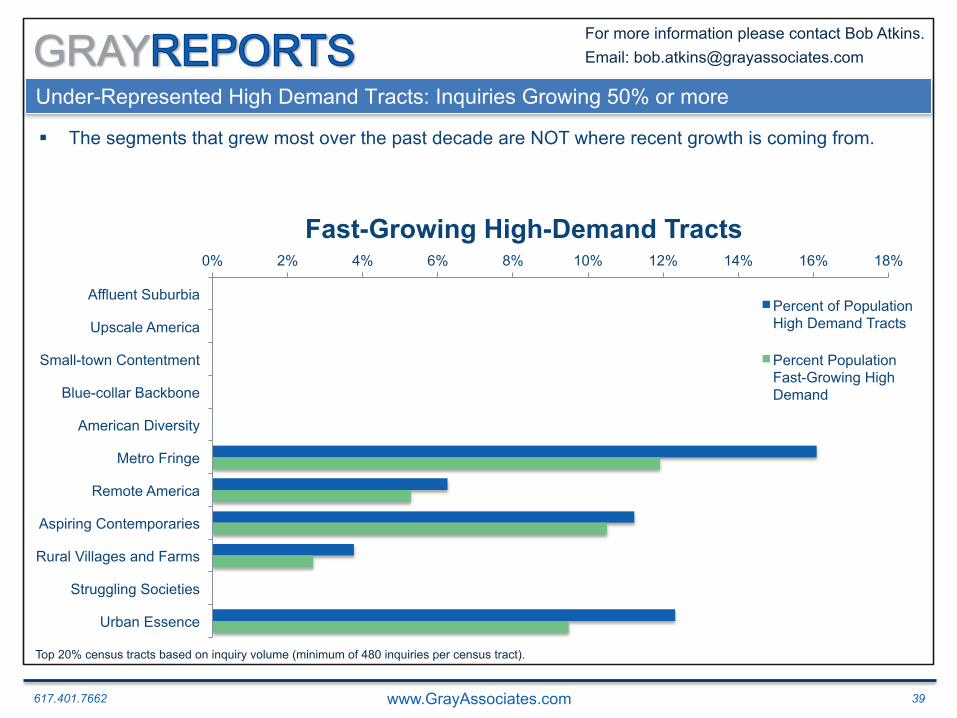

Under-Represented High Demand Tracts: Inquiries Growing 50% or more

§ The segments that grew most over the past decade are NOT where recent growth is coming from.

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Affluent Suburbia

Upscale America

Small-town Contentment

Blue-collar Backbone

American Diversity

Metro Fringe

Remote America

Aspiring Contemporaries

Rural Villages and Farms

Struggling Societies

Urban Essence

Fast-Growing High-Demand Tracts

Percent of Population High Demand Tracts

Percent Population Fast-Growing High Demand

Top 20% census tracts based on inquiry volume (minimum of 480 inquiries per census tract).

617.401.7662 www.GrayAssociates.com 40

GRAY For more information please contact Bob Atkins. Email: [email protected]

Agenda

1. Introduction

2. Demand: National Overview

3. Demand for On-Line Programs

4. Demand for On-Ground Programs

5. Demand by Program and City

6. Demand by Consumer Segment

7. Summary

617.401.7662 www.GrayAssociates.com 41

GRAY For more information please contact Bob Atkins. Email: [email protected]

“Miami Plus 30” Business Programs

Market § Greater Miami, including the entire area within 30 miles of the

population-weighted center of the CBSA1

Programs § CIP 52: Business, Management, Marketing, and Related

Support Services § Award Levels: All

5 Miles 1. Core-Based Statistical Area: Miami, Fort Lauderdale, West Palm Beach Florida

617.401.7662 www.GrayAssociates.com 42

GRAY For more information please contact Bob Atkins. Email: [email protected]

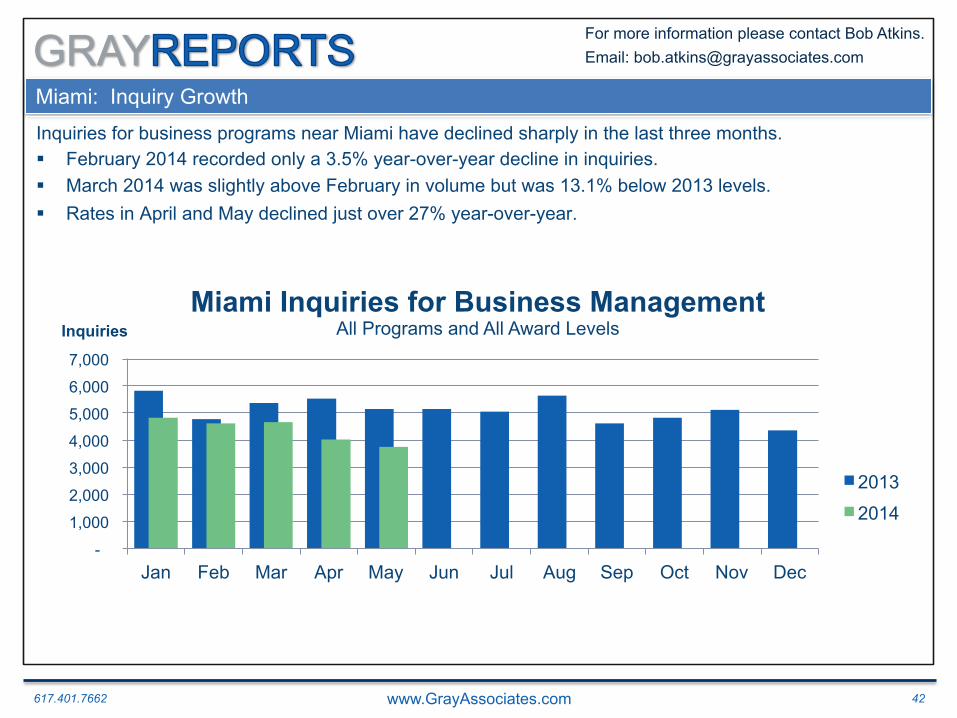

Miami: Inquiry Growth

Inquiries for business programs near Miami have declined sharply in the last three months. § February 2014 recorded only a 3.5% year-over-year decline in inquiries. § March 2014 was slightly above February in volume but was 13.1% below 2013 levels. § Rates in April and May declined just over 27% year-over-year.

2012

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Inquiries Miami Inquiries for Business Management

All Programs and All Award Levels

2013

2014

617.401.7662 www.GrayAssociates.com 43

GRAY For more information please contact Bob Atkins. Email: [email protected]

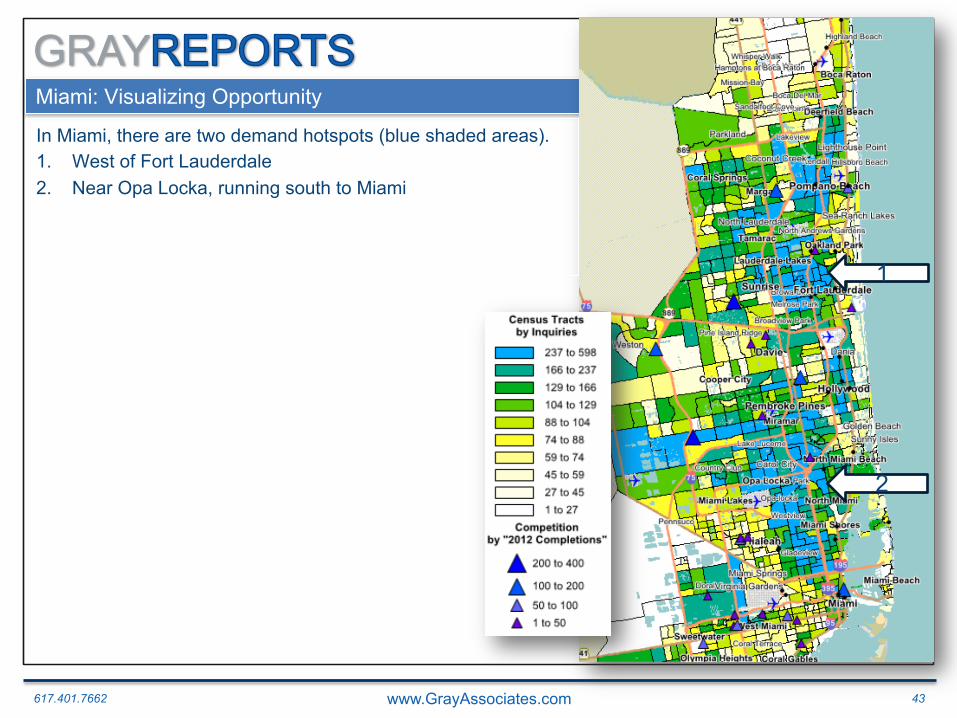

Miami: Visualizing Opportunity

In Miami, there are two demand hotspots (blue shaded areas). 1. West of Fort Lauderdale 2. Near Opa Locka, running south to Miami

2

1

617.401.7662 www.GrayAssociates.com 44

GRAY For more information please contact Bob Atkins. Email: [email protected]

Distance Factor

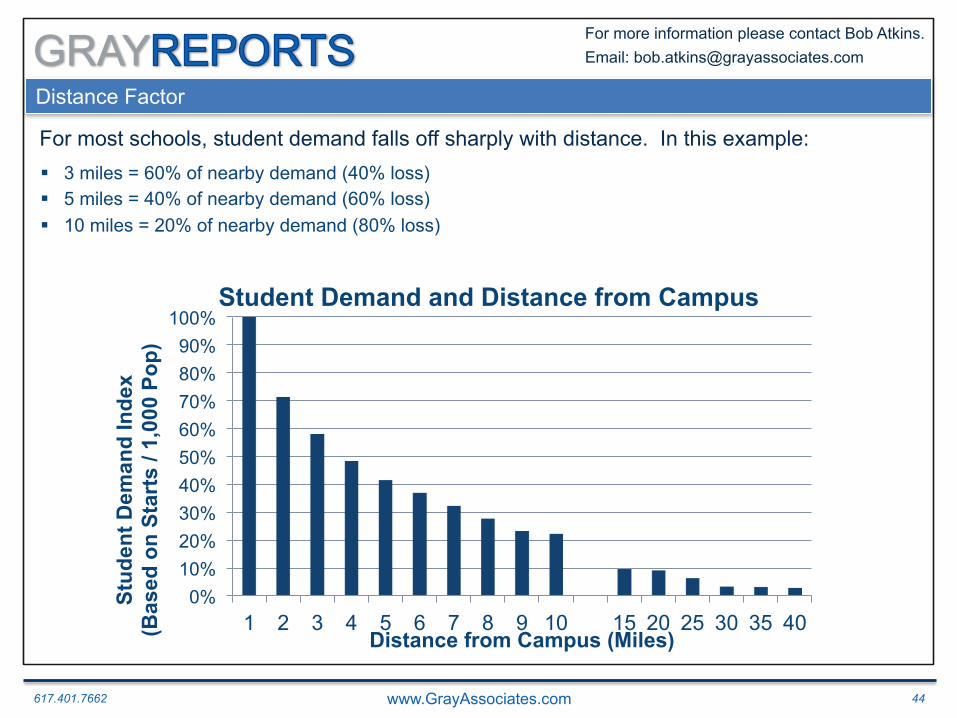

§ 3 miles = 60% of nearby demand (40% loss) § 5 miles = 40% of nearby demand (60% loss) § 10 miles = 20% of nearby demand (80% loss)

For most schools, student demand falls off sharply with distance. In this example:

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

100%

1 2 3 4 5 6 7 8 9 10 15 20 25 30 35 40

Stud

ent D

eman

d In

dex

(Bas

ed o

n St

arts

/ 1,

000

Pop)

Distance from Campus (Miles)

Student Demand and Distance from Campus

617.401.7662 www.GrayAssociates.com 45

GRAY For more information please contact Bob Atkins. Email: [email protected]

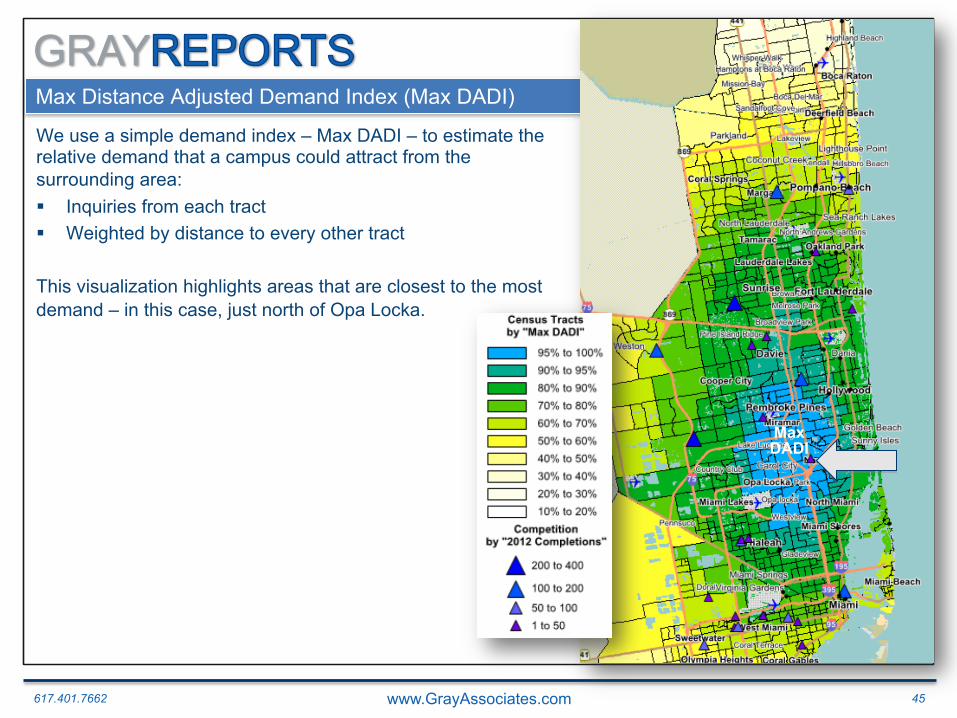

Max Distance Adjusted Demand Index (Max DADI)

We use a simple demand index – Max DADI – to estimate the relative demand that a campus could attract from the surrounding area: § Inquiries from each tract § Weighted by distance to every other tract This visualization highlights areas that are closest to the most demand – in this case, just north of Opa Locka.

Max DADI

617.401.7662 www.GrayAssociates.com 46

GRAY For more information please contact Bob Atkins. Email: [email protected]

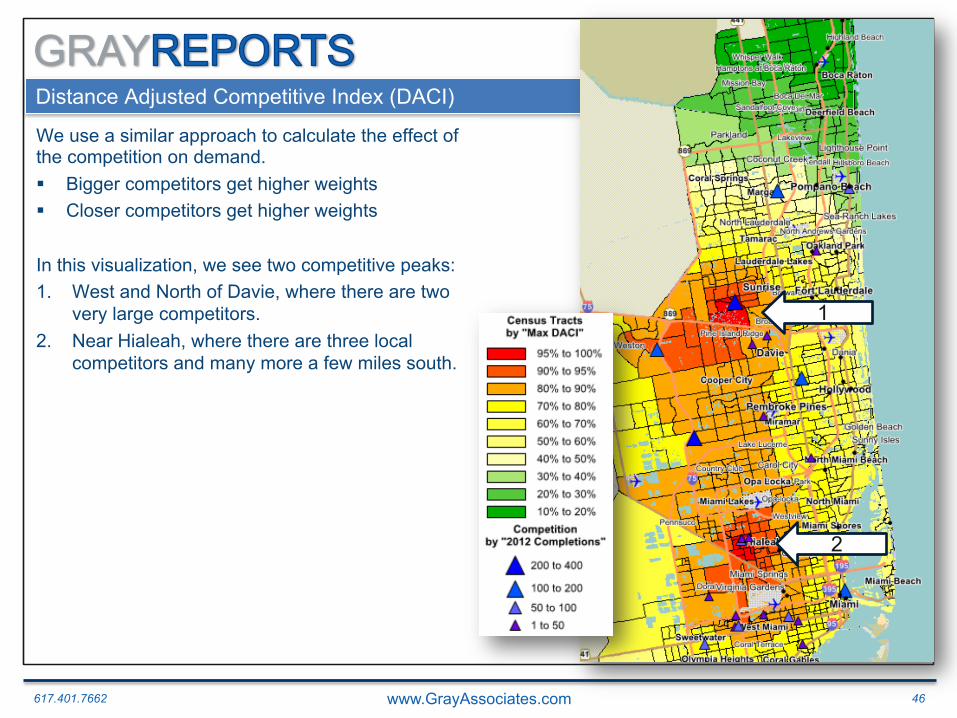

Distance Adjusted Competitive Index (DACI)

We use a similar approach to calculate the effect of the competition on demand. § Bigger competitors get higher weights § Closer competitors get higher weights

In this visualization, we see two competitive peaks: 1. West and North of Davie, where there are two

very large competitors. 2. Near Hialeah, where there are three local

competitors and many more a few miles south.

1

2

617.401.7662 www.GrayAssociates.com 47

GRAY For more information please contact Bob Atkins. Email: [email protected]

Distance Adjusted Competitive Index (DACI)

Purpose: § Identify under-performing areas § Determine their characteristics § Enable targeted marketing efforts to capture

opportunity

Method § Start with industry inquiry volumes § Estimate “expected share” of inquiries based on:

§ Market inquiries for relevant programs § Distance from campus § Competitive intensity (DACI)

§ Compare actual inquiries to expected share of market inquiries

§ Explore areas where actuals are less than expected

617.401.7662 www.GrayAssociates.com 48

GRAY For more information please contact Bob Atkins. Email: [email protected]

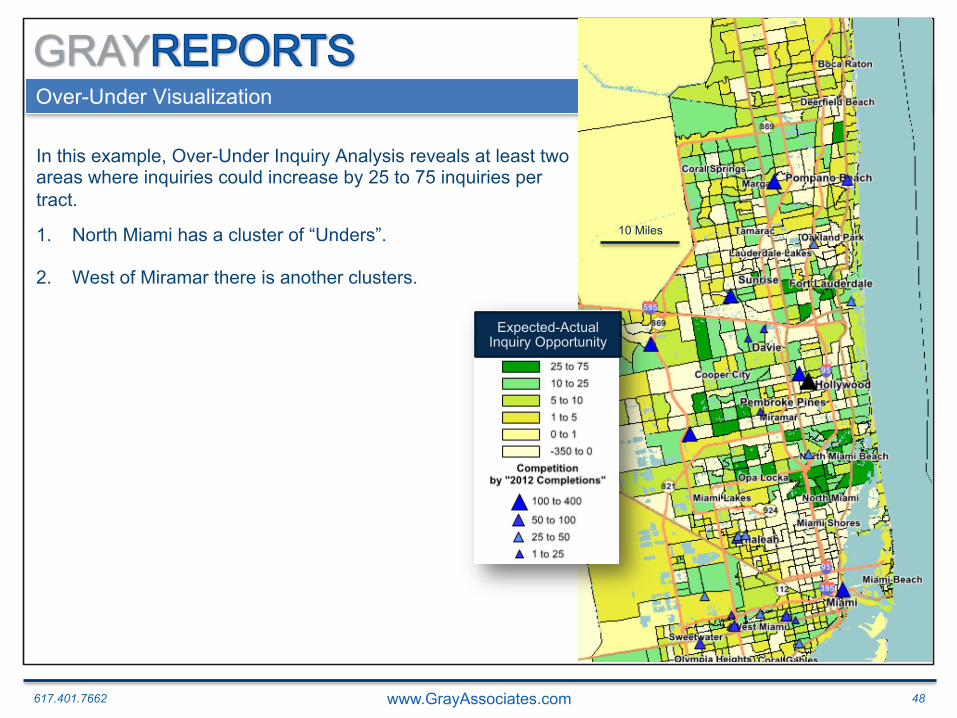

Over-Under Visualization

In this example, Over-Under Inquiry Analysis reveals at least two areas where inquiries could increase by 25 to 75 inquiries per tract.

1. North Miami has a cluster of “Unders”.

2. West of Miramar there is another clusters.

1

10 Miles

Expected-Actual Inquiry Opportunity

617.401.7662 www.GrayAssociates.com 49

GRAY For more information please contact Bob Atkins. Email: [email protected]

Miami: Over-Under Analysis

The “Unders” show clear differences by segment. § Heavier concentrations of Affluent Surburbia and American Diversity § Fewer Metro Fringe and Aspiring Contemporaries

0% 5% 10% 15% 20% 25% 30% 35% 40%

Affluent Suburbia

Upscale America

Small-town

Blue-collar Backbone

American Diversity

Metro Fringe

Remote America

Aspiring

Rural Villages and

Struggling Societies

Urban Essence

Varying Lifestyles

Miami Campus 10-Miles

Miami Campus 10-mile Under-Performing by 5% or More

Under-Over Analysis by Mosaic Segment

617.401.7662 www.GrayAssociates.com 50

GRAY For more information please contact Bob Atkins. Email: [email protected]

Agenda

1. Introduction

2. Demand: National Overview

3. Demand for On-Line Programs

4. Demand for On-Ground Programs

5. Demand by Program and City

6. Demand by Consumer Segment

7. Summary

617.401.7662 www.GrayAssociates.com 51

GRAY For more information please contact Bob Atkins. Email: [email protected]

Key Findings

1. Several long-term market trends appear to be reversing.

§ Inquiries are down 19% for On-line Programs.

§ Inquiries for on-ground programs increased over 20% in May.

§ Cost per application is up over 2013, but less so in the last few months.

§ Low-income, urban, minority segments may be declining.

§ Affluent Segments may be showing more interest in career colleges.

617.401.7662 www.GrayAssociates.com 52

GRAY For more information please contact Bob Atkins. Email: [email protected]

How do I get Information for My Locations and Programs?

Gray Reports is offered as an annual subscription. § Customized for your locations § Customized for your programs § Monthly PDF overview of inquiry, application, and pricing tends in your markets § On-line access to your market data by program, campus, veteran’s status, years since

high school and other factors

617.401.7662 www.GrayAssociates.com 53

GRAY For more information please contact Bob Atkins. Email: [email protected]

Questions and Contacts

Please feel free to contact me: Bob Atkins

CEO Gray Associates, Inc.

617-401-7662

For the presentation or a recording of the session, please visit: GrayAssociates.com

617.401.7662 www.GrayAssociates.com 54

GRAY For more information please contact Bob Atkins. Email: [email protected]

Aspiring Contemporaries

Young Cosmopolitans, Minority Metro Communities, Stable Careers, Aspiring Hispania

• The four Types in Aspiring Contemporaries are all filled with upward strivers. The households tend to be young, ethnically diverse (about 40 percent are minorities) and unattached (about two-thirds are single or divorced).

• Yet despite traditional barriers to affluence, the members of these metropolitan types are already solidly middle-class.

• Many live in relatively new homes or apartments valued at more than the national average — a reliable sign of upward mobility.

• They’re big culture buffs who like to see plays, movies, comics and live bands. They spend a lot of their discretionary income on the latest fashions and consumer electronics.

• They are heavy media consumers, listening to jazz on the radio and reading the Sunday paper for science and technology news.

• Raised on technology, they are very Internet savvy, spending their leisure time online to chat, shop, search for jobs, send instant messages, bid in auctions and frequent dating Web sites.