2014 september grayreports - student demand trends

TRANSCRIPT

GRAYREPORTS Demand for Educational Programs

www.GrayAssociates.com

Results through September 2014

617.401.7662 www.GrayAssociates.com 2

GRAY For more information please contact Bob Atkins. Email: [email protected]

Agenda

1. Introduction

2. National Inquiry Trends

3. Inquiry Sources

4. Summary

Today’s Presenter: Steve Probst, Partner at Gray Associates

617.401.7662 www.GrayAssociates.com 3

GRAY For more information please contact Bob Atkins. Email: [email protected]

Key Demand Trends and Observations

1. Trend: Total inquiries in September were down 22% year-over-year.

2. Modality: Inquiries for on-ground programs continued to gain inquiry share over on-line programs.

3. Sources: There is a limited shift taking place from external to internal inquiries, and that shift is having some surprising effects on conversion rates.

617.401.7662 www.GrayAssociates.com 4

GRAY For more information please contact Bob Atkins. Email: [email protected]

Who Is Gray?

GrayData

Completions IPEDS

Employment BLS/O*NET

Placement Rates Gray Research

Industry Inquiries GrayReports

Demographics US Census

Job Postings WANTED Analytics

Students Programs Strategy Locations § Demographic

priorities § Geo-priorities § Market share

§ City selection § Location selection § Relocation analysis § Consolidation

§ Program ideation and selection

§ Feasibility studies § R&D § Market reports

§ Business strategy and implementation

§ Acquisition analysis § Pricing § Outcome improvement

Advanced Analytics Predictive Models

Geo-Analytics

Clients: Education Institutions and Investors Mission

Help clients do well by doing good

617.401.7662 www.GrayAssociates.com 5

GRAY For more information please contact Bob Atkins. Email: [email protected]

What is GrayReports?

Your access to information on demand and marketing trends in higher education.

§ Overall Industry Trends

§ Customized Monthly Reports for Specific Programs and Markets

§ On-Line Access to Detailed Data for Specific Programs and Markets

Over 32 million qualified inquiries January 2012 to the present

Over 800,000 new inquiries in September 2014 Over 185 programs with over 10,000 inquiries

Over 300 cities with over 10,000 inquiries

617.401.7662 www.GrayAssociates.com 6

GRAY For more information please contact Bob Atkins. Email: [email protected]

Agenda

1. Introduction

2. National Inquiry Trends

3. Inquiry Sources

4. Summary

617.401.7662 www.GrayAssociates.com 7

GRAY For more information please contact Bob Atkins. Email: [email protected]

Overall Student Inquiries

The long decline in industry inquiries, which had stopped earlier in 2014, has resumed. § Inquiries were flat for the first half of 2014. § Starting in July, inquiries have fallen far behind 2013 levels, with September down 22% vs. year-ago. § Compared with 2012, the pattern is similar, except that the drop started in May rather than July.

-22% YOY

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

National Inquiries All Programs and Award Levels 2012 2013 2014

617.401.7662 www.GrayAssociates.com 8

GRAY For more information please contact Bob Atkins. Email: [email protected]

1. Applications are counted in the month in which the inquiry was received (i.e., an inquiry that is received in January and converts in March will be counted as a January inquiry). Typically, the application rate will rise for at least three months after the month in which the inquiries were received.

Inquiry to Application: Inquiry Maturation and Conversion Rates

Inquiries convert to applications over a period of time, typically flattening out in about four months. § About two-thirds of the inquiries that are going to convert do so in the month they are received. § By the end of the second month, 87% of the eventual conversions have happened. § After three months, only 5% more conversions are likely from that cohort of inquiries.

67%

87% 95% 100%

0%

20%

40%

60%

80%

100%

Same Month Month 2 Month 3 Month 4

Cumulative Inquiry Conversion Norms

617.401.7662 www.GrayAssociates.com 9

GRAY For more information please contact Bob Atkins. Email: [email protected]

1. Applications are counted in the month in which the inquiry was received (i.e., an inquiry that is received in January and converts in March will be counted as a January inquiry). Typically, the application rate will rise for at least three months after the month in which the inquiries were received.

3.0%

2.7%

3.1%

2.9%

3.0%

3.4%

3.1%

3.0%

2.7%

2.8%

2.8%

2.9%

3.2%

2.9%

3.4%

3.2%

3.3%

3.1%

3.4%

2.9%

3.0%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Inqu

iry C

onve

rsio

n R

ate

Education Industry Inquiry Conversion Rates 2013 2014

Inquiry to Application: Conversion Rates

Inquiry-to-application conversion rates have strengthened in 2014. § The first five months of 2014 outperformed 2013. § June does not fit that pattern, mostly because the 2013 conversion rate was exceptionally high. § Inquiries for July, August, and September 2014 are not yet mature. Gray forecasts that July and

September conversion rates will exceed 2013 levels, while August will be roughly comparable.

Immature Months1

3.2%

2.6% 2.0%

617.401.7662 www.GrayAssociates.com 10

GRAY For more information please contact Bob Atkins. Email: [email protected]

Student Inquiry Conversions

For the most recent months, it looks like higher-than-year-ago conversion rates will not be sufficient to compensate for much-lower-than-year-ago inquiry volumes. § Inquiry conversions were up year-over-year for every month through May. § While June inquiries were as strong as the year before, June conversion rates were lower, causing lower

total conversions. § It now looks like July will match year-ago conversions, while August and September will fall short.

- 5,000

10,000 15,000 20,000 25,000 30,000 35,000 40,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Education Industry Inquiry Conversions All Programs and Award Levels

2013 2014

1. Applications are counted in the month in which the inquiry was received (i.e., an inquiry that is received in January and converts in March will be counted as a January inquiry). Typically, the application rate will rise for at least three months after the month in which the inquiries were received.

Immature Months1

617.401.7662 www.GrayAssociates.com 11

GRAY For more information please contact Bob Atkins. Email: [email protected]

Average Wholesale Price for Pay-per-Lead Inquiries

After being stable for three months, wholesale price per inquiry rose in September. § For January through May, prices were stable and slightly above year-ago levels. § Prices jumped about 8% in June and were steady for three months at about 7% above year-ago levels. § In September, prices rose another 3%.

$42.13 $42.24 $42.13 $42.87 $41.59

$44.97 $44.67 $44.86 $46.18

$30

$32

$34

$36

$38

$40

$42

$44

$46

$48

Jan. Feb. Mar. April May June July Aug. Sept. Oct. Nov. Dec.

Avg.

Who

lesa

le P

rice

per I

nqui

ry

Wholesale Prices of Pay-per-Lead Inquiries All Programs and Award Levels

2014 2013

Note: Inquiry price is the average wholesale price for pay-per-lead inquiries.

617.401.7662 www.GrayAssociates.com 12

GRAY For more information please contact Bob Atkins. Email: [email protected]

Average Wholesale Cost Per Converted Inquiry

Cost-per-converted-inquiry now exceeds year-ago levels. § For the first five months of 2014, average cost per converted inquiry was 5% to 8% lower than in 2013,

with higher conversion rates more than compensating for slightly higher prices. § June’s cost per conversion jumped up, driven by the increase in price per inquiry. § July 2014’s cost per converted inquiry will be essentially the same as in 2013. § However, costs per converted inquiry in August and September are likely to exceed 2013 levels.

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC 2013 $1,378 $1,532 $1,335 $1,397 $1,387 $1,151 $1,287 $1,347 $1,484 $1,436 $1,418 $1,419 2014 $1,306 $1,439 $1,232 $1,327 $1,276 $1,447 $1,387 $1,762 $2,300

$0

$500

$1,000

$1,500

$2,000

$2,500 Cost Per Converted Inquiry All Programs and Award Levels

617.401.7662 www.GrayAssociates.com 13

GRAY For more information please contact Bob Atkins. Email: [email protected]

Largest Programs: September Growth

While overall inquiries were down 22% in September, four of the top five programs saw worse declines. § Medical Assisting was the healthiest of the top five programs, falling less than the overall average after

rising during the same period in 2013. § Criminal Justice/Police Science fared worst, down 70% in two years. § The other three top-five programs all declined substantially, on top of small 2013 drops.

-4%

7%

-19%

-5% -2%

-27% -19%

-62%

-30%

-44%

-70% -60% -50% -40% -30% -20% -10%

0% 10% 20%

Business Admin and Management

Medical Assisting Criminal Justice/Police Science

Health Care Admin/Management

Accounting

Year-over-year Change in September Inquiries Five Largest Programs

2013 YoY % Change 2014 YoY % Change

617.401.7662 www.GrayAssociates.com 14

GRAY For more information please contact Bob Atkins. Email: [email protected]

Top 5 Fastest-Growing Programs in September

The two fastest-growing programs1 nearly quadrupled their inquiry counts in September. § The two fastest-growing programs – Welding, and Electrical Tech – are both in the trades. § The next two fastest-growing programs are both computer-related, but with very different skill sets.

-23%

22%

69%

-17%

44%

292% 280%

77% 70% 48%

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

350%

Welding Tech Electrical, Electronic, and Comm. Tech

Web Page, Digital/ Multimedia Design

Network and System Admin

Criminal Justice/ Safety Studies

Year-over-Year Change in September Inquiries Five Fastest-Growing Programs

2013 YoY % Change 2014 YoY % Change

1. Includes only programs within the top 75 for total inquiries since January 2012.

617.401.7662 www.GrayAssociates.com 15

GRAY For more information please contact Bob Atkins. Email: [email protected]

Largest Cities for Inquiries

All five of the largest inquiry markets beat the industry’s trend in September. § The two biggest markets – New York and Los Angeles – both saw higher inquiry volumes than in 2013. § Chicago and Atlanta both experienced single-digit drops, better than the market’s overall 22% drop. § Atlanta, the smallest of the top-five markets, saw a small increase. § In contrast, all five of the top markets saw their inquiry volumes shrink in September 2013.

-9% -10% -16%

-9% -16%

9% 16%

-9% -4%

4%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

New York Los Angeles Chicago Philadelphia Atlanta

Year-over-Year Change in September Inquiries Top Five Cities for Inquiries

2013 YoY % Change 2014 YoY % Change

Note: The market for each city is defined as a 15-mile radius around the population center of its CBSA.

617.401.7662 www.GrayAssociates.com 16

GRAY For more information please contact Bob Atkins. Email: [email protected]

Fastest-Growing Cities for All Inquiries

Among the 75 largest cities, the fastest-growing cities1 are all up dramatically for September. § All of the fastest-growing markets were located in California, Florida, or Virginia. § Jacksonville’s growth moved it into the top five markets for inquiries.

1% 1%

-2% -2% -20%

96% 80%

38% 38% 33%

-100%

-50%

0%

50%

100%

150%

Jacksonville, FL San Diego, CA Riverside, CA Lakeland-Winter Haven, FL

Virginia Beach, VA

Year-over-Year Change in September Inquiries Top 5 Fastest-Growing Cities for All Inquiries

2013 YoY % Change 2014 YoY % Change

1. Includes only the top 75 cities by inquiry volume since January 2012. Data includes a 15-mile radius from the center of the CBSA.

617.401.7662 www.GrayAssociates.com 17

GRAY For more information please contact Bob Atkins. Email: [email protected]

Agenda

1. Introduction

2. National Inquiry Trends

3. Inquiry Sources

4. Summary

617.401.7662 www.GrayAssociates.com 18

GRAY For more information please contact Bob Atkins. Email: [email protected]

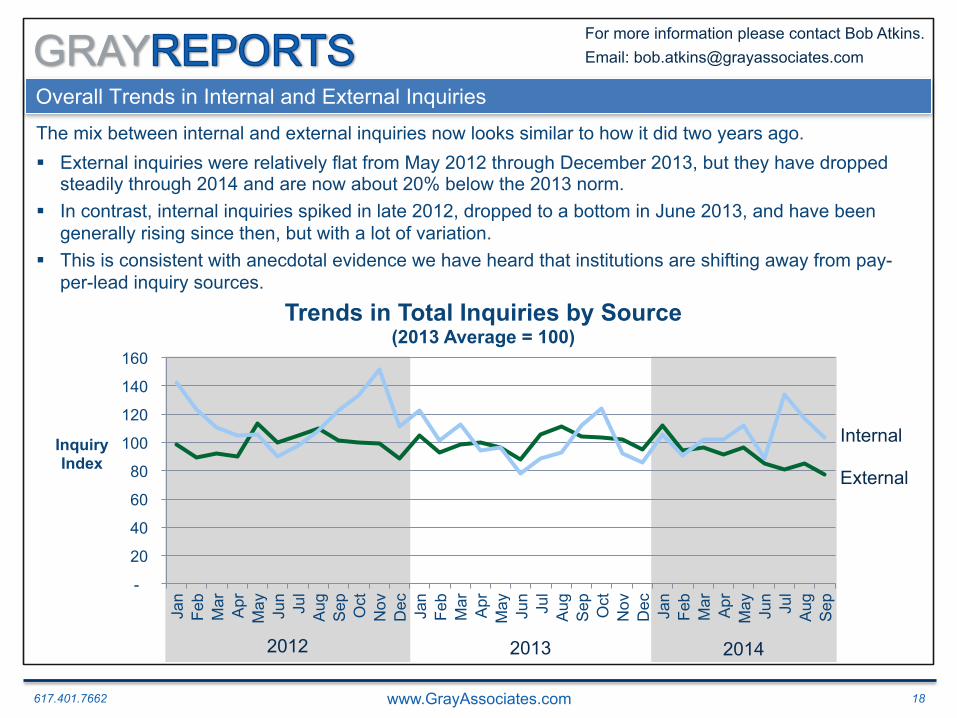

The mix between internal and external inquiries now looks similar to how it did two years ago. § External inquiries were relatively flat from May 2012 through December 2013, but they have dropped

steadily through 2014 and are now about 20% below the 2013 norm. § In contrast, internal inquiries spiked in late 2012, dropped to a bottom in June 2013, and have been

generally rising since then, but with a lot of variation. § This is consistent with anecdotal evidence we have heard that institutions are shifting away from pay-

per-lead inquiry sources.

Overall Trends in Internal and External Inquiries

-

20

40

60

80

100

120

140

160

Jan

Feb

Mar

A

pr

May

Ju

n Ju

l A

ug

Sep

O

ct

Nov

D

ec

Jan

Feb

Mar

A

pr

May

Ju

n Ju

l A

ug

Sep

O

ct

Nov

D

ec

Jan

Feb

Mar

A

pr

May

Ju

n Ju

l A

ug

Sep

Inquiry Index

Trends in Total Inquiries by Source (2013 Average = 100)

External

Internal

2012 2013 2014

617.401.7662 www.GrayAssociates.com 19

GRAY For more information please contact Bob Atkins. Email: [email protected]

External inquiries are actually generating a higher share of conversions than in the past. § Relative to 2013, internal inquiries are generating about the same number of conversions, though June

(the most recent “mature” month) looks weak. § For January through May, external inquiries were generating more conversions than in 2013 or even in

most of 2012. § The most recent months are not yet mature enough to assess the relative number of conversions from

each source.

Internal and External Inquiry Conversions

-

20

40

60

80

100

120

140

160

Jan

Feb

Mar

A

pr

May

Ju

n Ju

l A

ug

Sep

O

ct

Nov

D

ec

Jan

Feb

Mar

A

pr

May

Ju

n Ju

l A

ug

Sep

O

ct

Nov

D

ec

Jan

Feb

Mar

A

pr

May

Ju

n Ju

l A

ug

Sep

Inquiry Conversion

Index

Trends in Inquiry Conversions by Source (2013 Average = 100)

External Internal

2012 2013 2014

617.401.7662 www.GrayAssociates.com 20

GRAY For more information please contact Bob Atkins. Email: [email protected]

The relationship between conversion rates for internal and external inquiries is changing. § In 2013, conversion rates for internal and external inquiries moved up and down together. § For the first half of 2014, internal inquiries converted at the same rates as they had in 2013, while

external inquiries saw a 20% improvement in conversion rates. § While July inquiries are not yet mature, and one month does not make a trend, it appears that

conversion rates for external inquiries are continuing to improve, while internal rates are not.

Internal and External Inquiry Conversion Rates

0.0% 0.5% 1.0% 1.5% 2.0% 2.5%

Jan

Feb

Mar

A

pr

May

Ju

n Ju

l A

ug

Sep

O

ct

Nov

D

ec

Jan

Feb

Mar

A

pr

May

Ju

n Ju

l A

ug

Sep

O

ct

Nov

D

ec

Jan

Feb

Mar

A

pr

May

Ju

n Ju

l A

ug

Sep

Inquiry Conversion

Rate Index

External

Internal

2012 2013 2014

0% 2% 4% 6% 8%

10% 12%

Inquiry Conversion

Rate Index

Trends in Inquiry Conversion Rates by Source

2013 Average

2013 Average

617.401.7662 www.GrayAssociates.com 21

GRAY For more information please contact Bob Atkins. Email: [email protected]

Agenda

1. Introduction

2. National Inquiry Trends

3. Inquiry Sources

4. Summary

617.401.7662 www.GrayAssociates.com 22

GRAY For more information please contact Bob Atkins. Email: [email protected]

Key Findings

Inquiry quality has improved. Demand is shifting away from on-line programs.

§ Inquiry volumes are continuing to drop.

§ Inquiries for on-ground programs are trending better than for on-line programs.

§ Institutions appear to be focusing more on internal inquiries relative to external inquiries.

─ However, the remaining external inquiries are converting at a better rate than they did last year.

─ This year’s external inquiries are more expensive than last year, but higher conversion rates make them a better value than last year’s.

─ Internal inquiries have been converting at the same rate as last year, but July’s inquiries may indicate that that is changing for the worse.

617.401.7662 www.GrayAssociates.com 23

GRAY For more information please contact Bob Atkins. Email: [email protected]

How do I get Information for My Locations and Programs?

Gray Reports is offered as an annual subscription. § Customized for your locations § Customized for your programs § Monthly PDF overview of inquiry, application, and pricing tends in your markets § On-line access to your market data by program, campus, veteran’s status, years since

high school and other factors

617.401.7662 www.GrayAssociates.com 24

GRAY For more information please contact Bob Atkins. Email: [email protected]

Questions and Contacts

Please feel free to contact: Bob Atkins

CEO Gray Associates, Inc.

617-401-7662

For the presentation or a recording of the session, please visit: GrayAssociates.com

Today’s Presenter: Steve Probst, Partner at Gray Associates